Comprehensive Analysis of Management Accounting and Financial Reports

VerifiedAdded on 2022/12/19

|24

|4561

|84

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring various systems and their benefits within an organizational context. It examines different types of management accounting reporting, including inventory management, job costing, price optimization, and cost accounting systems. The report delves into the relevance of management accounting and its systems, including account receivable aging reports, cost reports, and performance reports. Furthermore, it presents a detailed analysis of cost cards using absorption and marginal costing, alongside financial reporting documents. The report also covers budget preparation, ratio analysis, and the identification of financial issues and planning tools. Finally, it analyzes variances and discusses strategies to overcome challenges, offering a practical understanding of financial management.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

1.1 Examination of the terms of management accounting and analysis of various kinds of

management accounting systems.................................................................................................1

1.2 Evaluation and analysis of different types of management accounting reporting that are

very important from the company’s point of view......................................................................1

1.3 Identification of the benefits of the systems of management accounting that are related

with the organisational context....................................................................................................2

1.4 Analysis of the two aspects that are management accounting and management accounting

system and its relevance with each other including examination of different methods of

accounting....................................................................................................................................3

Section Two.....................................................................................................................................4

2.1 preparation of the cost card using absorption costing as its base..........................................4

2.2 Preparation of the financial reporting document of the company by applying different

range of the techniques of management accounting that are prevailing in the current market

scenario........................................................................................................................................6

2.3 Analysis of the financial reports of the firm by appropriate application and interpretation

of the range of different type of data that are associated with the activities that are performed

in the business..............................................................................................................................9

2.4 Preparation of various statements that are very crucial in order to examine the profit that is

generated by the company over a period of time.......................................................................11

SECTION 2...................................................................................................................................12

3.1 Preparation of different kinds of budget that are very important from the firm’s point of

view............................................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

1.1 Examination of the terms of management accounting and analysis of various kinds of

management accounting systems.................................................................................................1

1.2 Evaluation and analysis of different types of management accounting reporting that are

very important from the company’s point of view......................................................................1

1.3 Identification of the benefits of the systems of management accounting that are related

with the organisational context....................................................................................................2

1.4 Analysis of the two aspects that are management accounting and management accounting

system and its relevance with each other including examination of different methods of

accounting....................................................................................................................................3

Section Two.....................................................................................................................................4

2.1 preparation of the cost card using absorption costing as its base..........................................4

2.2 Preparation of the financial reporting document of the company by applying different

range of the techniques of management accounting that are prevailing in the current market

scenario........................................................................................................................................6

2.3 Analysis of the financial reports of the firm by appropriate application and interpretation

of the range of different type of data that are associated with the activities that are performed

in the business..............................................................................................................................9

2.4 Preparation of various statements that are very crucial in order to examine the profit that is

generated by the company over a period of time.......................................................................11

SECTION 2...................................................................................................................................12

3.1 Preparation of different kinds of budget that are very important from the firm’s point of

view............................................................................................................................................12

4.1 Analysis of various kinds of ratios that are very essential to evaluate the overall working of

the company in the long run......................................................................................................15

4.2 Identification of various types of financial issues that the company is facing and examine

the important things that can be adopted by the firm so as to overcome all of those challenges

...................................................................................................................................................17

4.3 Identification and evaluation of different kinds of planning tools and techniques that are

prevailing in the industry in the present time............................................................................18

4.4 Analysis of different kinds of variances that possess a lot of value in the current market

scenario......................................................................................................................................18

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

the company in the long run......................................................................................................15

4.2 Identification of various types of financial issues that the company is facing and examine

the important things that can be adopted by the firm so as to overcome all of those challenges

...................................................................................................................................................17

4.3 Identification and evaluation of different kinds of planning tools and techniques that are

prevailing in the industry in the present time............................................................................18

4.4 Analysis of different kinds of variances that possess a lot of value in the current market

scenario......................................................................................................................................18

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is one of the most important as well as crucial aspect as it can help

a firm to grow and prosper in the current market scenario in which is highly competitive as well

as dynamic in nature as it proves beneficial in recording each and every transaction of the

business firm in an appropriate manner so that it can add value to the firm in the long run

(Amnuai, 2019). This report is a systematic and sequential examination, analysis, and evaluation

of all the related terms of management accounting that possess a lot of value in the market since

they can help the company to stand well ahead of all the rivals that are prevailing in the current

market. Apart from that the concepts of different planning tools, ratio analysis, and a preparation

of an accurate budget is also included in this report.

SECTION 1

1.1 Examination of the terms of management accounting and analysis of various kinds of

management accounting systems

Management accounting is basically regarded as a process of recording, summarising,

identifying, colleting, analysis, and evaluation of all the activities that are performed in the

company so that a detailed examination of all the aspects can be done so that it can help the

company to sustain and survive in the long term scenario. The management of the accounting

part of the organisation is a very critical part since it can help in maintaining a proper record of

all the activities so that appropriate and necessary decisions can be taken on the basis of it so that

it can help in the increase in the value of the firm by subsequently increasing its profitability.

Management accounting systems is a very important one as it helps in measuring the overall

progress of the company so that decisions can be taken which can prove in accordance with it so

that if there are some loop holes in the company’s performance so that it can be overcome by

applying effective and efficient decisions.

1.2 Evaluation and analysis of different types of management accounting reporting that are very

important from the company’s point of view

There are a number of different aspects that are involved in it and thus all of them are

explained in a well detailed and prescribed manner below-

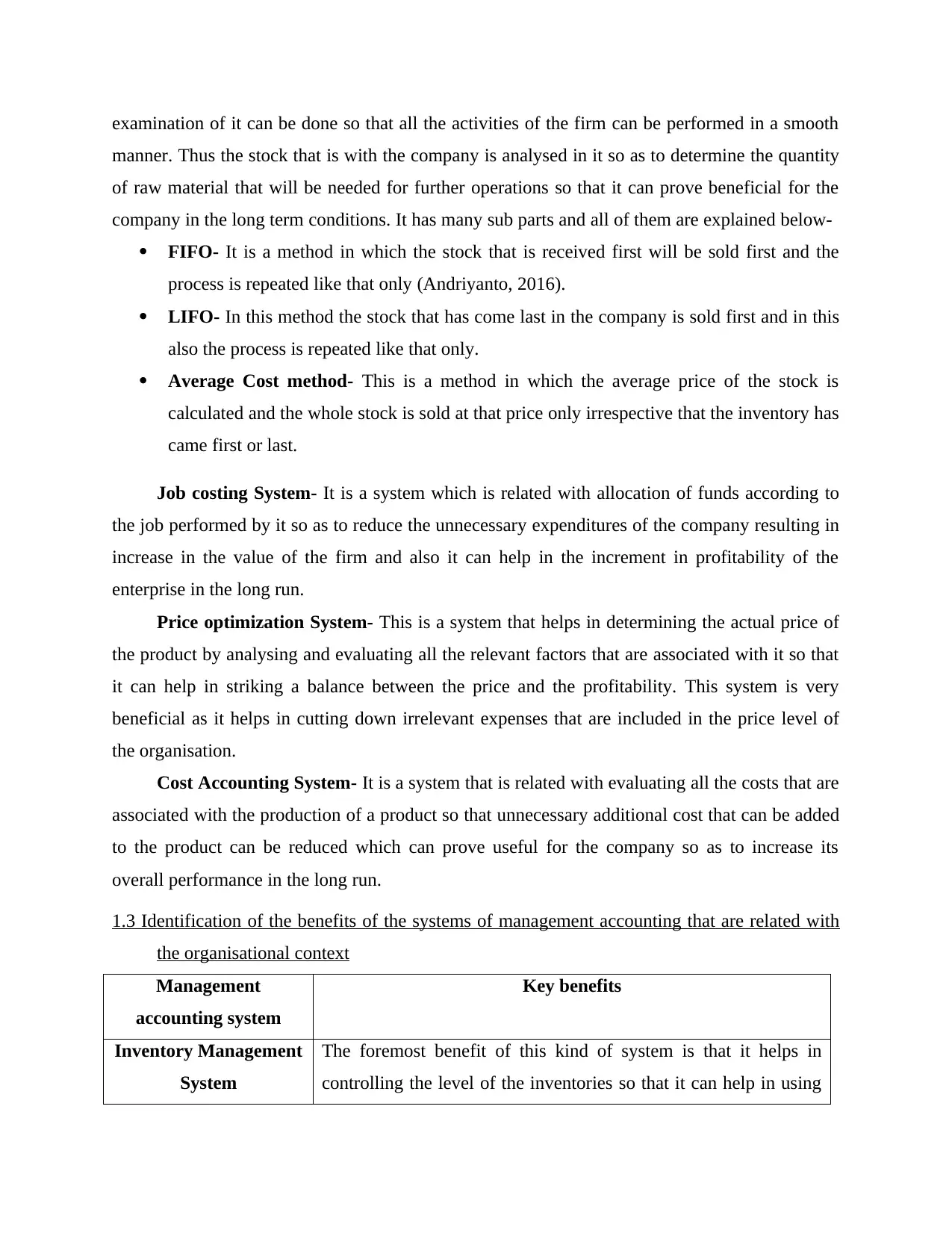

Inventory management system- It is a system that is related with the management of the

most important aspect that is inventories that are available with the company so that a detailed

Management accounting is one of the most important as well as crucial aspect as it can help

a firm to grow and prosper in the current market scenario in which is highly competitive as well

as dynamic in nature as it proves beneficial in recording each and every transaction of the

business firm in an appropriate manner so that it can add value to the firm in the long run

(Amnuai, 2019). This report is a systematic and sequential examination, analysis, and evaluation

of all the related terms of management accounting that possess a lot of value in the market since

they can help the company to stand well ahead of all the rivals that are prevailing in the current

market. Apart from that the concepts of different planning tools, ratio analysis, and a preparation

of an accurate budget is also included in this report.

SECTION 1

1.1 Examination of the terms of management accounting and analysis of various kinds of

management accounting systems

Management accounting is basically regarded as a process of recording, summarising,

identifying, colleting, analysis, and evaluation of all the activities that are performed in the

company so that a detailed examination of all the aspects can be done so that it can help the

company to sustain and survive in the long term scenario. The management of the accounting

part of the organisation is a very critical part since it can help in maintaining a proper record of

all the activities so that appropriate and necessary decisions can be taken on the basis of it so that

it can help in the increase in the value of the firm by subsequently increasing its profitability.

Management accounting systems is a very important one as it helps in measuring the overall

progress of the company so that decisions can be taken which can prove in accordance with it so

that if there are some loop holes in the company’s performance so that it can be overcome by

applying effective and efficient decisions.

1.2 Evaluation and analysis of different types of management accounting reporting that are very

important from the company’s point of view

There are a number of different aspects that are involved in it and thus all of them are

explained in a well detailed and prescribed manner below-

Inventory management system- It is a system that is related with the management of the

most important aspect that is inventories that are available with the company so that a detailed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

examination of it can be done so that all the activities of the firm can be performed in a smooth

manner. Thus the stock that is with the company is analysed in it so as to determine the quantity

of raw material that will be needed for further operations so that it can prove beneficial for the

company in the long term conditions. It has many sub parts and all of them are explained below-

FIFO- It is a method in which the stock that is received first will be sold first and the

process is repeated like that only (Andriyanto, 2016).

LIFO- In this method the stock that has come last in the company is sold first and in this

also the process is repeated like that only.

Average Cost method- This is a method in which the average price of the stock is

calculated and the whole stock is sold at that price only irrespective that the inventory has

came first or last.

Job costing System- It is a system which is related with allocation of funds according to

the job performed by it so as to reduce the unnecessary expenditures of the company resulting in

increase in the value of the firm and also it can help in the increment in profitability of the

enterprise in the long run.

Price optimization System- This is a system that helps in determining the actual price of

the product by analysing and evaluating all the relevant factors that are associated with it so that

it can help in striking a balance between the price and the profitability. This system is very

beneficial as it helps in cutting down irrelevant expenses that are included in the price level of

the organisation.

Cost Accounting System- It is a system that is related with evaluating all the costs that are

associated with the production of a product so that unnecessary additional cost that can be added

to the product can be reduced which can prove useful for the company so as to increase its

overall performance in the long run.

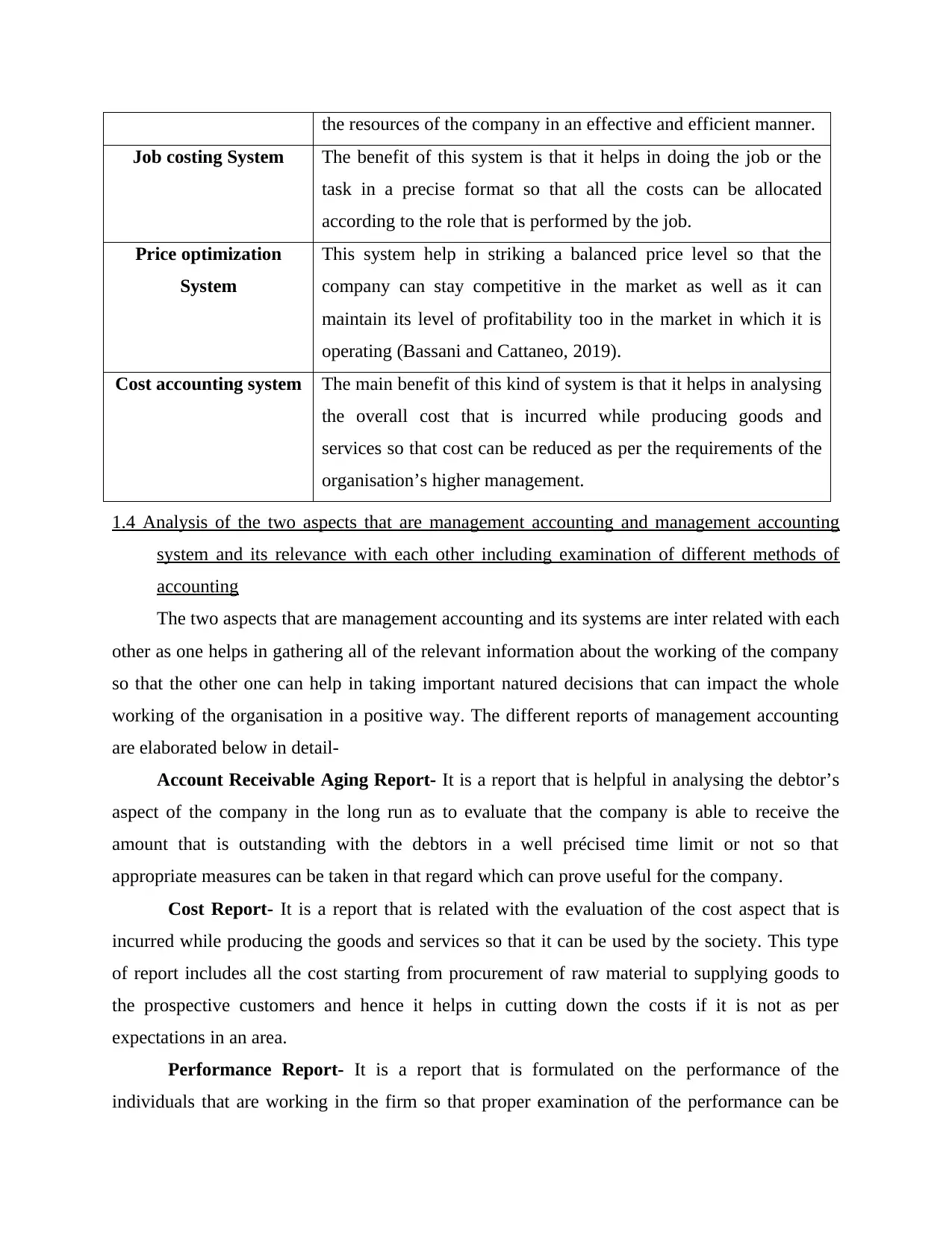

1.3 Identification of the benefits of the systems of management accounting that are related with

the organisational context

Management

accounting system

Key benefits

Inventory Management

System

The foremost benefit of this kind of system is that it helps in

controlling the level of the inventories so that it can help in using

manner. Thus the stock that is with the company is analysed in it so as to determine the quantity

of raw material that will be needed for further operations so that it can prove beneficial for the

company in the long term conditions. It has many sub parts and all of them are explained below-

FIFO- It is a method in which the stock that is received first will be sold first and the

process is repeated like that only (Andriyanto, 2016).

LIFO- In this method the stock that has come last in the company is sold first and in this

also the process is repeated like that only.

Average Cost method- This is a method in which the average price of the stock is

calculated and the whole stock is sold at that price only irrespective that the inventory has

came first or last.

Job costing System- It is a system which is related with allocation of funds according to

the job performed by it so as to reduce the unnecessary expenditures of the company resulting in

increase in the value of the firm and also it can help in the increment in profitability of the

enterprise in the long run.

Price optimization System- This is a system that helps in determining the actual price of

the product by analysing and evaluating all the relevant factors that are associated with it so that

it can help in striking a balance between the price and the profitability. This system is very

beneficial as it helps in cutting down irrelevant expenses that are included in the price level of

the organisation.

Cost Accounting System- It is a system that is related with evaluating all the costs that are

associated with the production of a product so that unnecessary additional cost that can be added

to the product can be reduced which can prove useful for the company so as to increase its

overall performance in the long run.

1.3 Identification of the benefits of the systems of management accounting that are related with

the organisational context

Management

accounting system

Key benefits

Inventory Management

System

The foremost benefit of this kind of system is that it helps in

controlling the level of the inventories so that it can help in using

the resources of the company in an effective and efficient manner.

Job costing System The benefit of this system is that it helps in doing the job or the

task in a precise format so that all the costs can be allocated

according to the role that is performed by the job.

Price optimization

System

This system help in striking a balanced price level so that the

company can stay competitive in the market as well as it can

maintain its level of profitability too in the market in which it is

operating (Bassani and Cattaneo, 2019).

Cost accounting system The main benefit of this kind of system is that it helps in analysing

the overall cost that is incurred while producing goods and

services so that cost can be reduced as per the requirements of the

organisation’s higher management.

1.4 Analysis of the two aspects that are management accounting and management accounting

system and its relevance with each other including examination of different methods of

accounting

The two aspects that are management accounting and its systems are inter related with each

other as one helps in gathering all of the relevant information about the working of the company

so that the other one can help in taking important natured decisions that can impact the whole

working of the organisation in a positive way. The different reports of management accounting

are elaborated below in detail-

Account Receivable Aging Report- It is a report that is helpful in analysing the debtor’s

aspect of the company in the long run as to evaluate that the company is able to receive the

amount that is outstanding with the debtors in a well précised time limit or not so that

appropriate measures can be taken in that regard which can prove useful for the company.

Cost Report- It is a report that is related with the evaluation of the cost aspect that is

incurred while producing the goods and services so that it can be used by the society. This type

of report includes all the cost starting from procurement of raw material to supplying goods to

the prospective customers and hence it helps in cutting down the costs if it is not as per

expectations in an area.

Performance Report- It is a report that is formulated on the performance of the

individuals that are working in the firm so that proper examination of the performance can be

Job costing System The benefit of this system is that it helps in doing the job or the

task in a precise format so that all the costs can be allocated

according to the role that is performed by the job.

Price optimization

System

This system help in striking a balanced price level so that the

company can stay competitive in the market as well as it can

maintain its level of profitability too in the market in which it is

operating (Bassani and Cattaneo, 2019).

Cost accounting system The main benefit of this kind of system is that it helps in analysing

the overall cost that is incurred while producing goods and

services so that cost can be reduced as per the requirements of the

organisation’s higher management.

1.4 Analysis of the two aspects that are management accounting and management accounting

system and its relevance with each other including examination of different methods of

accounting

The two aspects that are management accounting and its systems are inter related with each

other as one helps in gathering all of the relevant information about the working of the company

so that the other one can help in taking important natured decisions that can impact the whole

working of the organisation in a positive way. The different reports of management accounting

are elaborated below in detail-

Account Receivable Aging Report- It is a report that is helpful in analysing the debtor’s

aspect of the company in the long run as to evaluate that the company is able to receive the

amount that is outstanding with the debtors in a well précised time limit or not so that

appropriate measures can be taken in that regard which can prove useful for the company.

Cost Report- It is a report that is related with the evaluation of the cost aspect that is

incurred while producing the goods and services so that it can be used by the society. This type

of report includes all the cost starting from procurement of raw material to supplying goods to

the prospective customers and hence it helps in cutting down the costs if it is not as per

expectations in an area.

Performance Report- It is a report that is formulated on the performance of the

individuals that are working in the firm so that proper examination of the performance can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

done so as to evaluate the reasons for deviation if any. There are different ways in which it can

be evaluated and mostly it is analysed on a yearly basis so that overall evaluation can be done in

a well précised and accurate format (Bloechl, Michalicki and Schneider, 2017).

Section Two

2.1 preparation of the cost card using absorption costing as its base

Cost Card Using Absorption costing

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) Units

produced 11000 9500

b) Direct

Material (4kg*3pound/kg*11000) 132000 (4kg * 3 pound / kg *

9500) 114000

c) Direct

Labour

(4 hrs * 2 pound / hr *

11000) 88000 (4 hrs* 2 pound /

hr*9500) 76000

d) Variable

Overhead

(5 pounds / desk *

11000) 55000 (5 pounds / desk *

9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

g)

Cost of

goods

produced

295000 257500

h) Variable

sales cost

(1 pound / desk *

11000) 11000 (1 pound / desk *

9500) 9500

i) fixed selling 2000 2000

be evaluated and mostly it is analysed on a yearly basis so that overall evaluation can be done in

a well précised and accurate format (Bloechl, Michalicki and Schneider, 2017).

Section Two

2.1 preparation of the cost card using absorption costing as its base

Cost Card Using Absorption costing

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) Units

produced 11000 9500

b) Direct

Material (4kg*3pound/kg*11000) 132000 (4kg * 3 pound / kg *

9500) 114000

c) Direct

Labour

(4 hrs * 2 pound / hr *

11000) 88000 (4 hrs* 2 pound /

hr*9500) 76000

d) Variable

Overhead

(5 pounds / desk *

11000) 55000 (5 pounds / desk *

9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

g)

Cost of

goods

produced

295000 257500

h) Variable

sales cost

(1 pound / desk *

11000) 11000 (1 pound / desk *

9500) 9500

i) fixed selling 2000 2000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost

j) Cost of

Goods sold 308000 269000

k) Profit= l-j 77000 63500

l) Sales (35 pounds / desk *

11000) 385000 (35 pounds / desk *

9500) 332500

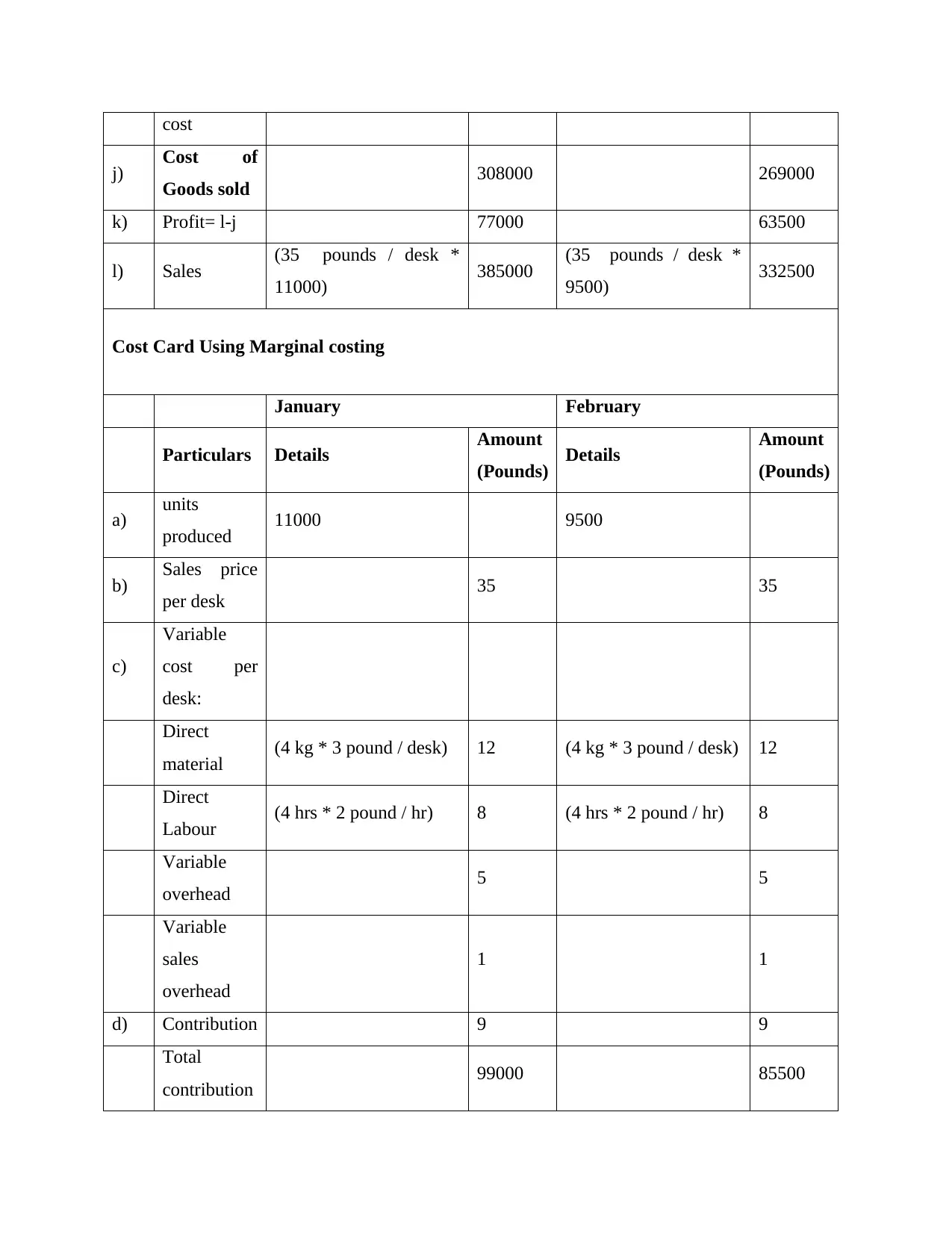

Cost Card Using Marginal costing

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) units

produced 11000 9500

b) Sales price

per desk 35 35

c)

Variable

cost per

desk:

Direct

material (4 kg * 3 pound / desk) 12 (4 kg * 3 pound / desk) 12

Direct

Labour (4 hrs * 2 pound / hr) 8 (4 hrs * 2 pound / hr) 8

Variable

overhead 5 5

Variable

sales

overhead

1 1

d) Contribution 9 9

Total

contribution 99000 85500

j) Cost of

Goods sold 308000 269000

k) Profit= l-j 77000 63500

l) Sales (35 pounds / desk *

11000) 385000 (35 pounds / desk *

9500) 332500

Cost Card Using Marginal costing

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) units

produced 11000 9500

b) Sales price

per desk 35 35

c)

Variable

cost per

desk:

Direct

material (4 kg * 3 pound / desk) 12 (4 kg * 3 pound / desk) 12

Direct

Labour (4 hrs * 2 pound / hr) 8 (4 hrs * 2 pound / hr) 8

Variable

overhead 5 5

Variable

sales

overhead

1 1

d) Contribution 9 9

Total

contribution 99000 85500

e) Fixed costs

Production

overhead NOTE 1 22000 19000

Sales

overhead 2000 2000

Profit (d-e) 75000 64500

NOTE 1- Production overheads here are regarded by considering average productions per month

= 10000 units. Thus, for Jan. month, overheads amount= (20000/10000) *11000. While, for Feb.,

overheads amount= (20000/10000) *9500

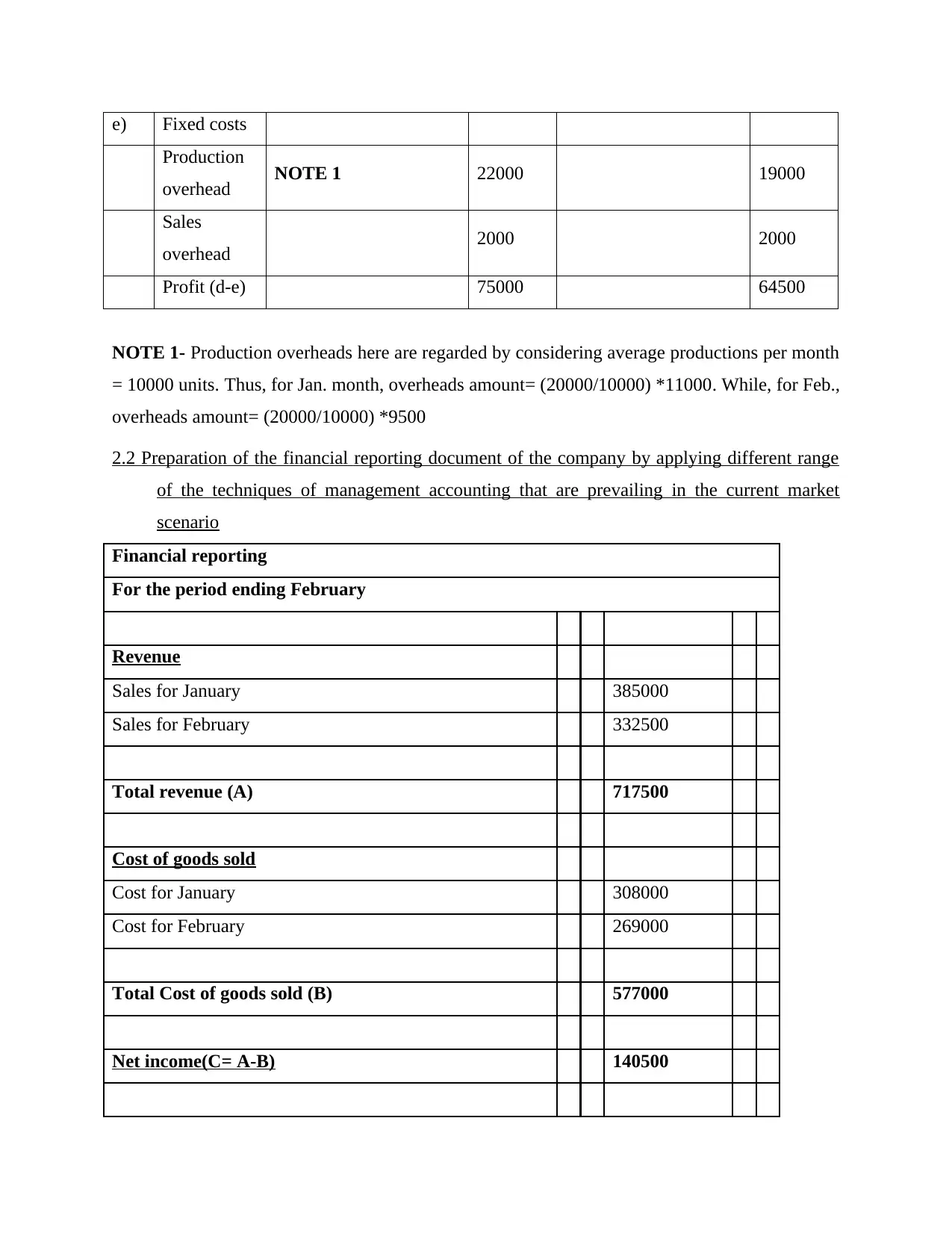

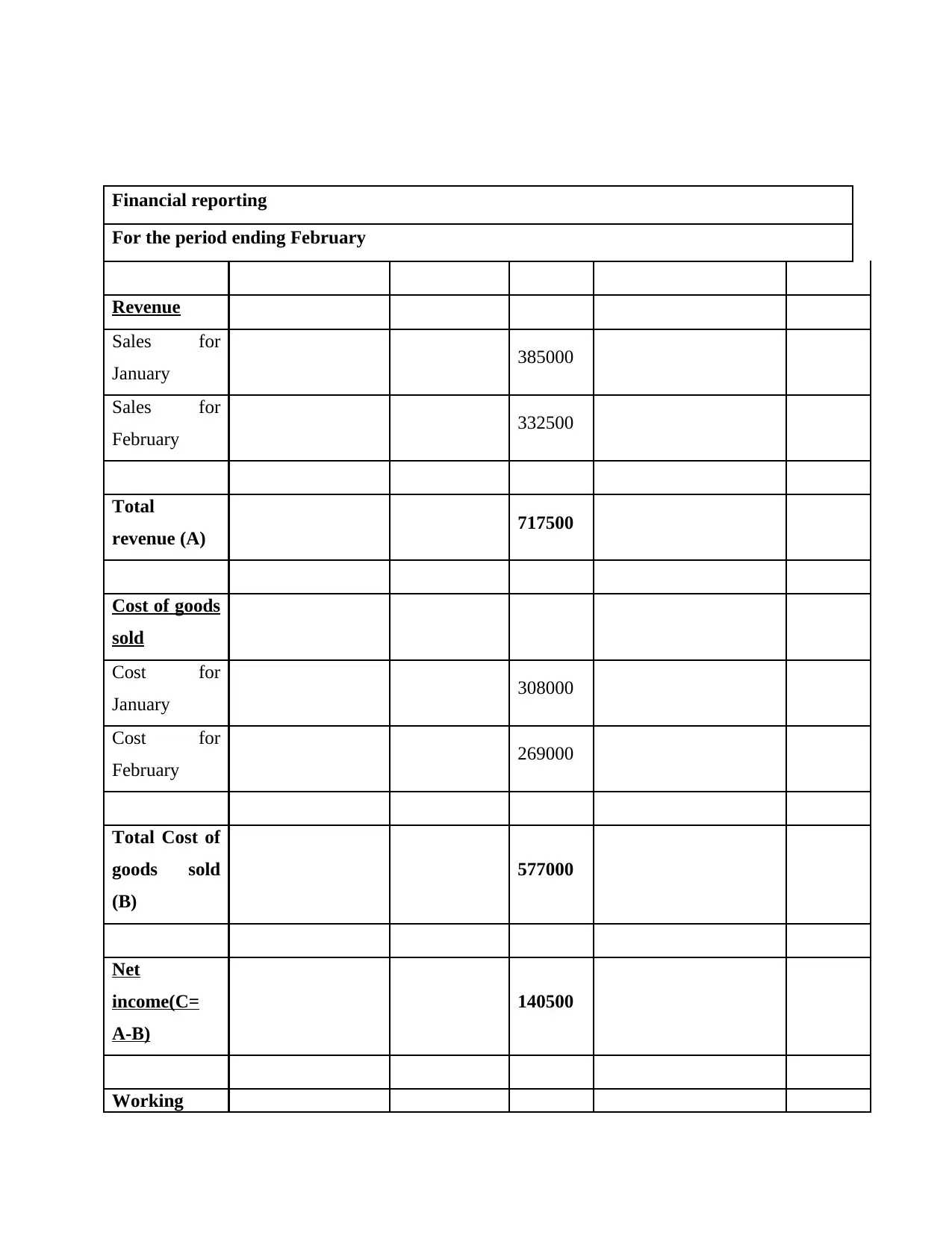

2.2 Preparation of the financial reporting document of the company by applying different range

of the techniques of management accounting that are prevailing in the current market

scenario

Financial reporting

For the period ending February

Revenue

Sales for January 385000

Sales for February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for January 308000

Cost for February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

Production

overhead NOTE 1 22000 19000

Sales

overhead 2000 2000

Profit (d-e) 75000 64500

NOTE 1- Production overheads here are regarded by considering average productions per month

= 10000 units. Thus, for Jan. month, overheads amount= (20000/10000) *11000. While, for Feb.,

overheads amount= (20000/10000) *9500

2.2 Preparation of the financial reporting document of the company by applying different range

of the techniques of management accounting that are prevailing in the current market

scenario

Financial reporting

For the period ending February

Revenue

Sales for January 385000

Sales for February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for January 308000

Cost for February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial reporting

For the period ending February

Revenue

Sales for

January 385000

Sales for

February 332500

Total

revenue (A) 717500

Cost of goods

sold

Cost for

January 308000

Cost for

February 269000

Total Cost of

goods sold

(B)

577000

Net

income(C=

A-B)

140500

Working

For the period ending February

Revenue

Sales for

January 385000

Sales for

February 332500

Total

revenue (A) 717500

Cost of goods

sold

Cost for

January 308000

Cost for

February 269000

Total Cost of

goods sold

(B)

577000

Net

income(C=

A-B)

140500

Working

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

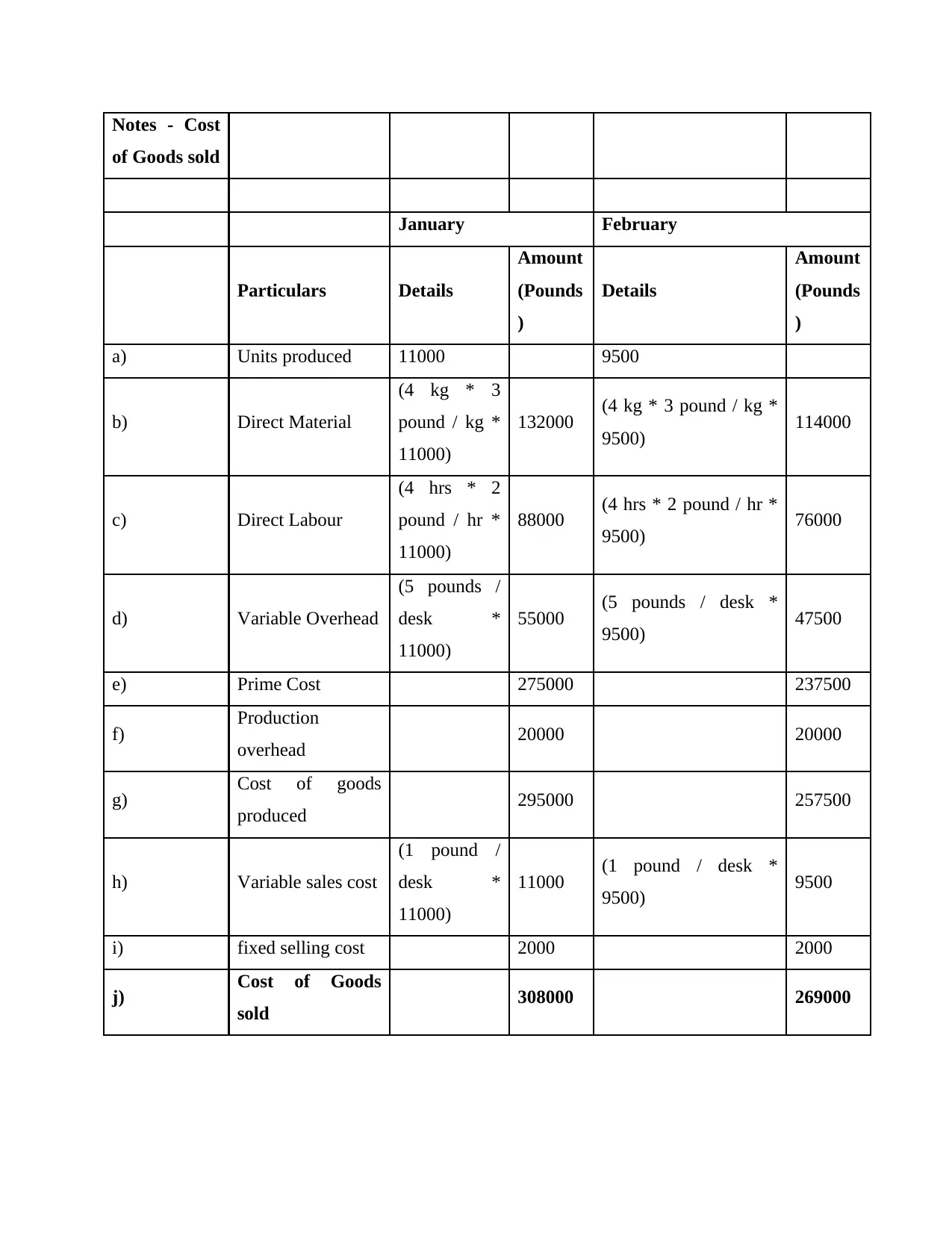

Notes - Cost

of Goods sold

January February

Particulars Details

Amount

(Pounds

)

Details

Amount

(Pounds

)

a) Units produced 11000 9500

b) Direct Material

(4 kg * 3

pound / kg *

11000)

132000 (4 kg * 3 pound / kg *

9500) 114000

c) Direct Labour

(4 hrs * 2

pound / hr *

11000)

88000 (4 hrs * 2 pound / hr *

9500) 76000

d) Variable Overhead

(5 pounds /

desk *

11000)

55000 (5 pounds / desk *

9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

g) Cost of goods

produced 295000 257500

h) Variable sales cost

(1 pound /

desk *

11000)

11000 (1 pound / desk *

9500) 9500

i) fixed selling cost 2000 2000

j) Cost of Goods

sold 308000 269000

of Goods sold

January February

Particulars Details

Amount

(Pounds

)

Details

Amount

(Pounds

)

a) Units produced 11000 9500

b) Direct Material

(4 kg * 3

pound / kg *

11000)

132000 (4 kg * 3 pound / kg *

9500) 114000

c) Direct Labour

(4 hrs * 2

pound / hr *

11000)

88000 (4 hrs * 2 pound / hr *

9500) 76000

d) Variable Overhead

(5 pounds /

desk *

11000)

55000 (5 pounds / desk *

9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

g) Cost of goods

produced 295000 257500

h) Variable sales cost

(1 pound /

desk *

11000)

11000 (1 pound / desk *

9500) 9500

i) fixed selling cost 2000 2000

j) Cost of Goods

sold 308000 269000

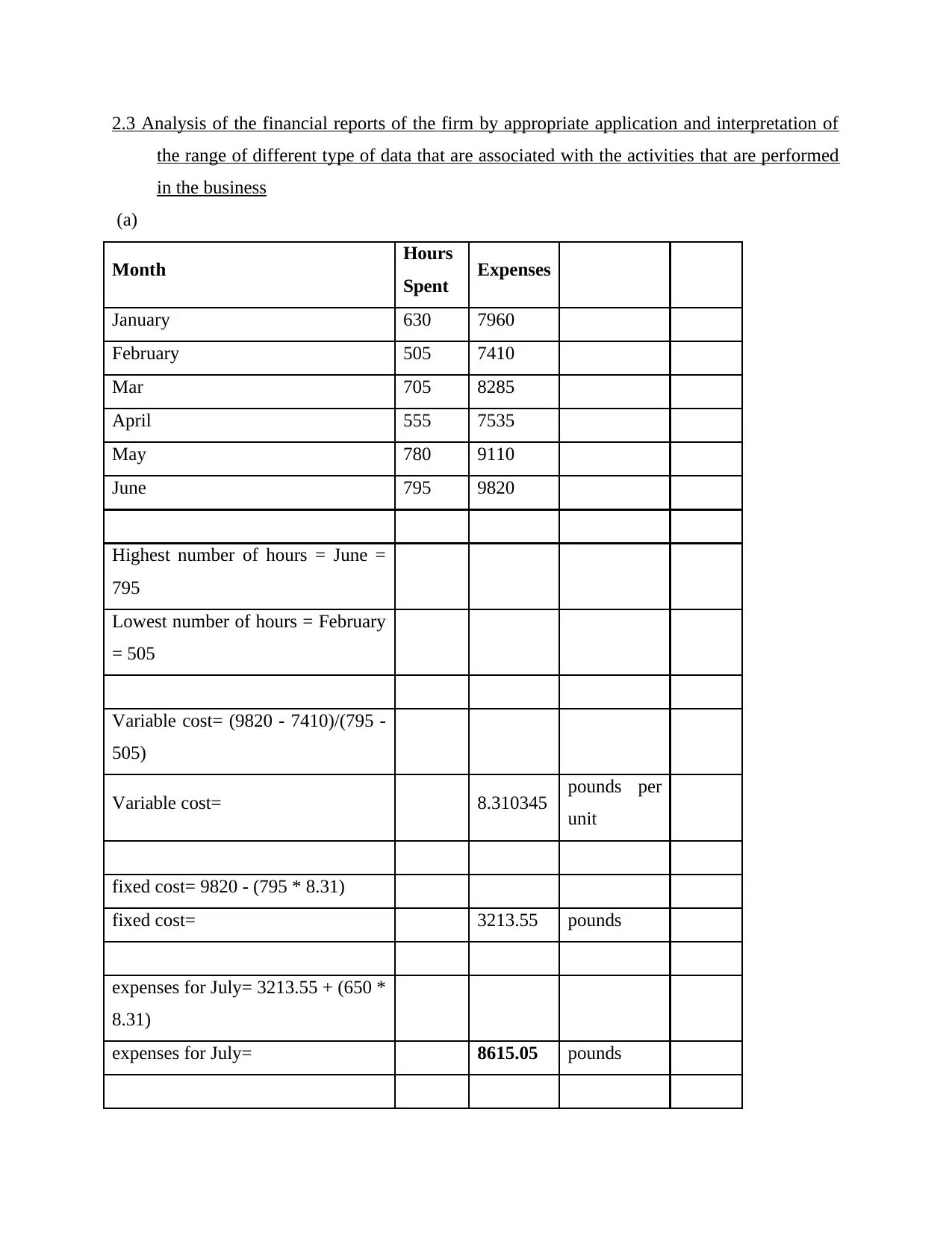

2.3 Analysis of the financial reports of the firm by appropriate application and interpretation of

the range of different type of data that are associated with the activities that are performed

in the business

(a)

Month Hours

Spent Expenses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours = June =

795

Lowest number of hours = February

= 505

Variable cost= (9820 - 7410)/(795 -

505)

Variable cost= 8.310345 pounds per

unit

fixed cost= 9820 - (795 * 8.31)

fixed cost= 3213.55 pounds

expenses for July= 3213.55 + (650 *

8.31)

expenses for July= 8615.05 pounds

the range of different type of data that are associated with the activities that are performed

in the business

(a)

Month Hours

Spent Expenses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours = June =

795

Lowest number of hours = February

= 505

Variable cost= (9820 - 7410)/(795 -

505)

Variable cost= 8.310345 pounds per

unit

fixed cost= 9820 - (795 * 8.31)

fixed cost= 3213.55 pounds

expenses for July= 3213.55 + (650 *

8.31)

expenses for July= 8615.05 pounds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.