Management Accounting Report on Cost Analysis and Budgeting

VerifiedAdded on 2023/01/12

|19

|2720

|81

Report

AI Summary

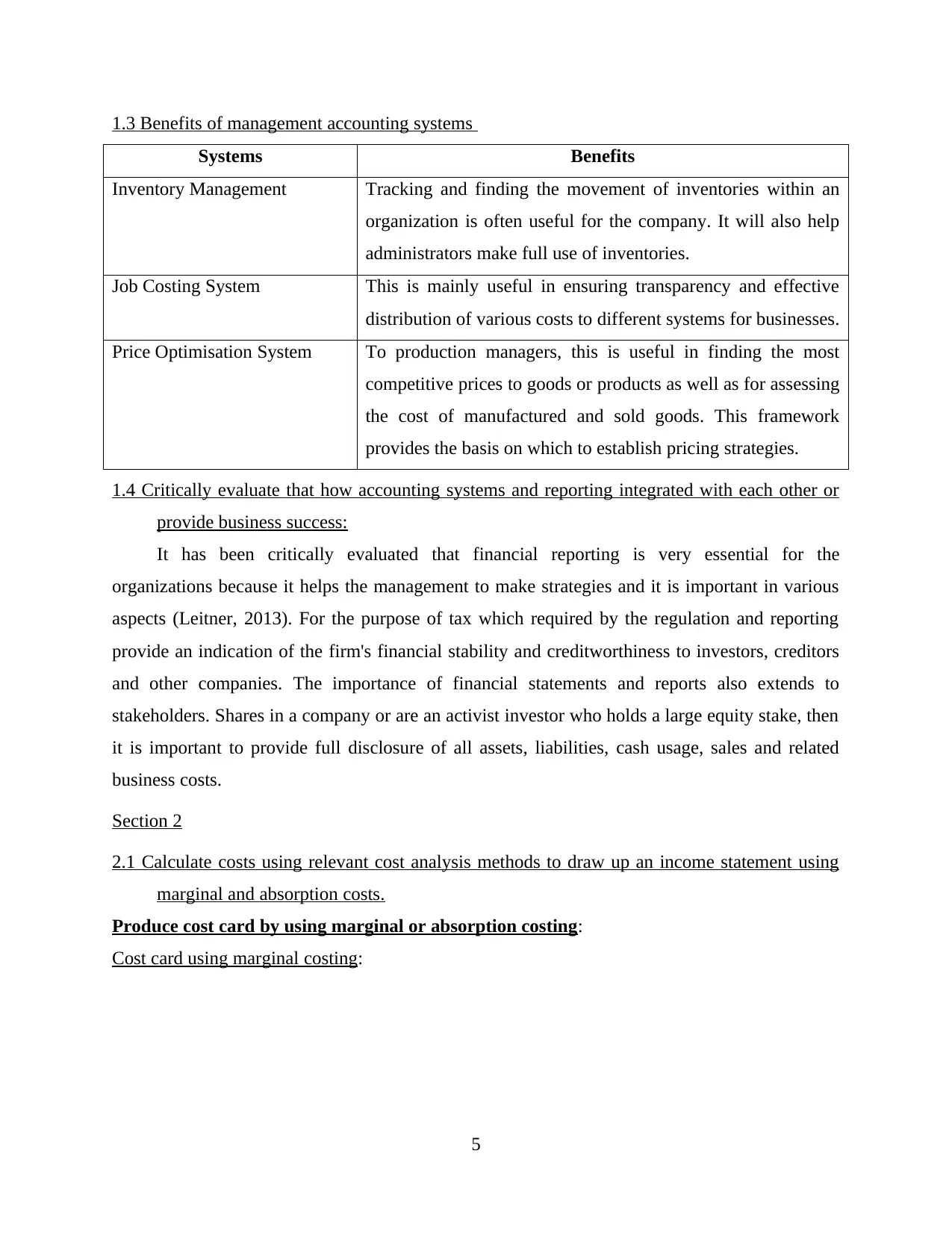

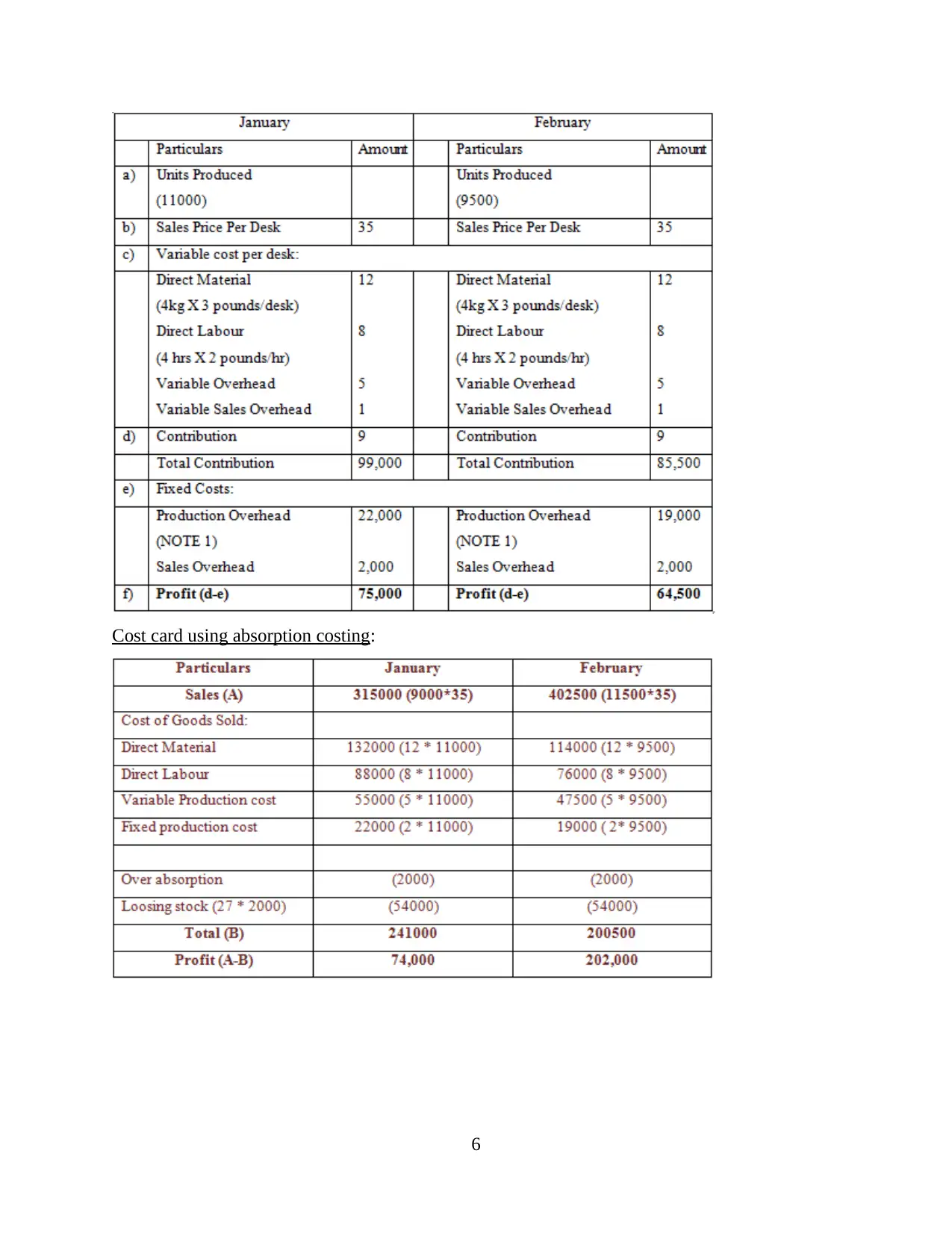

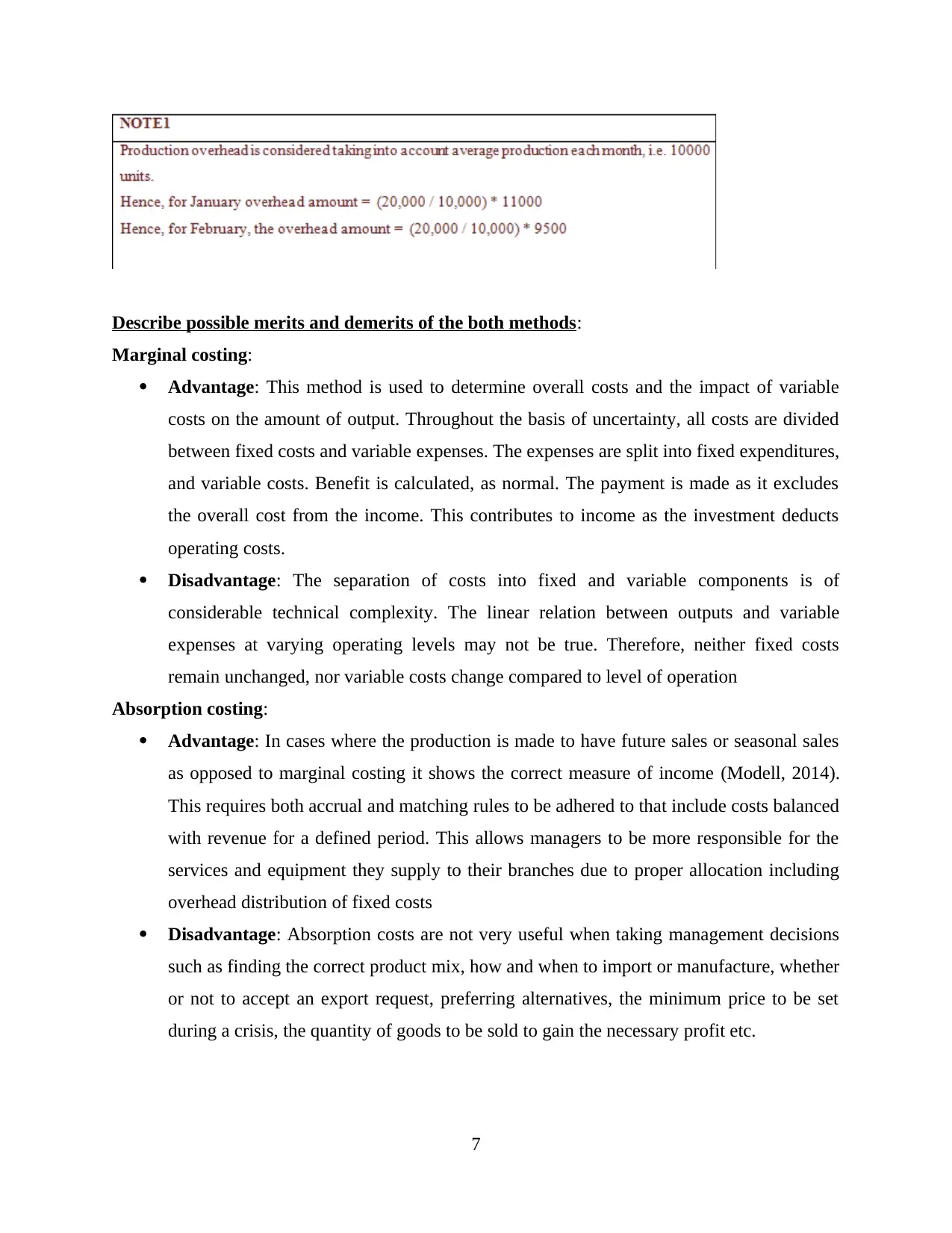

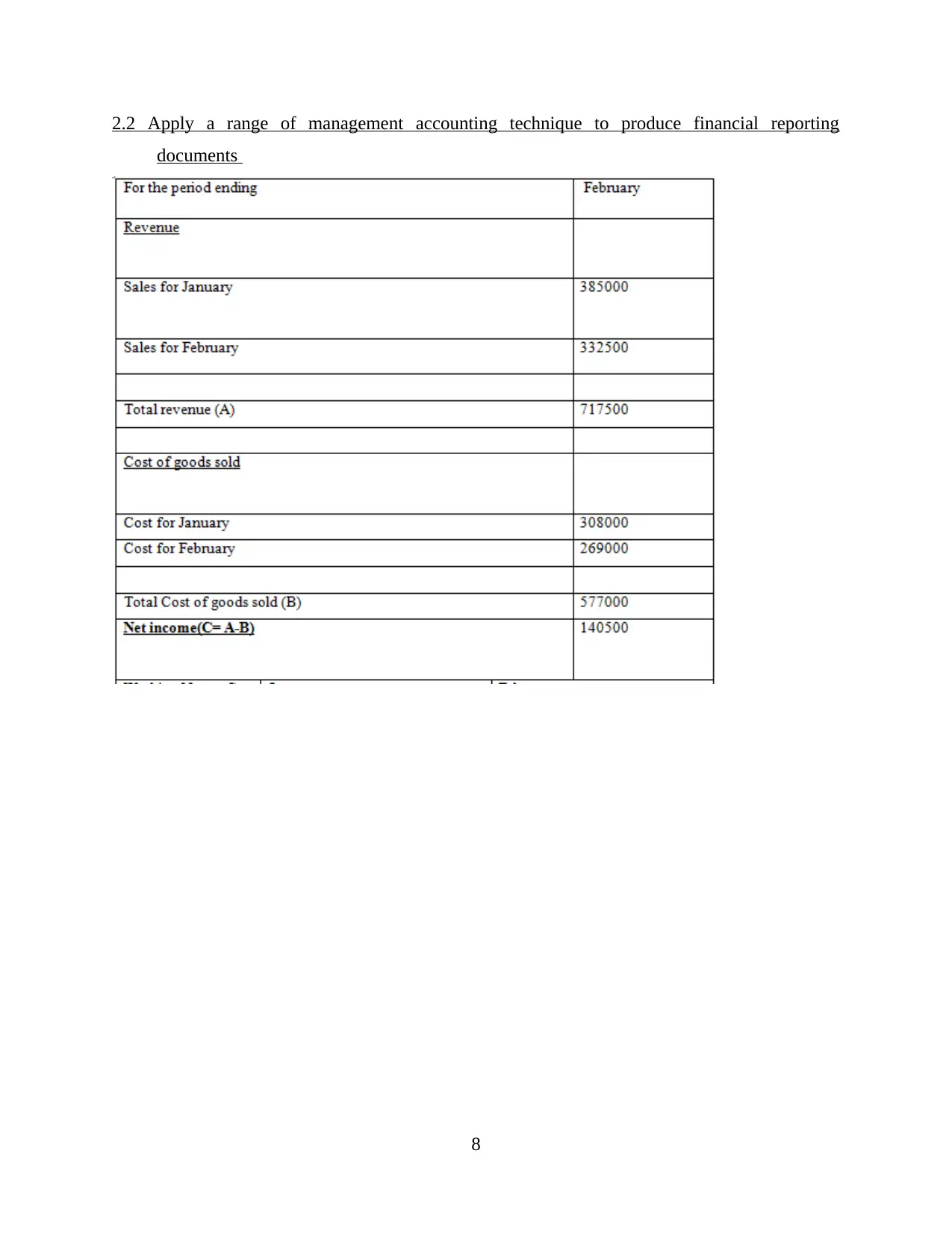

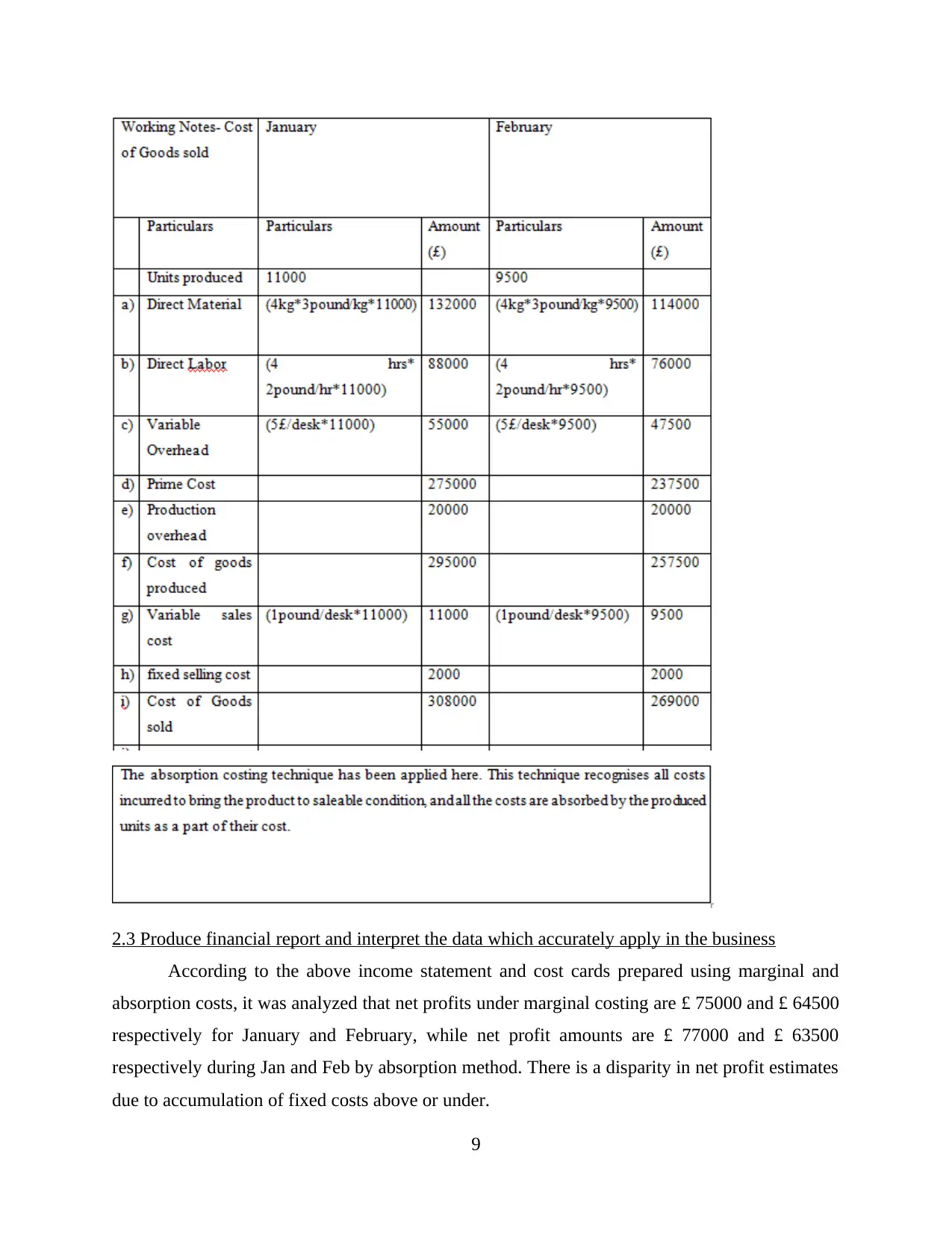

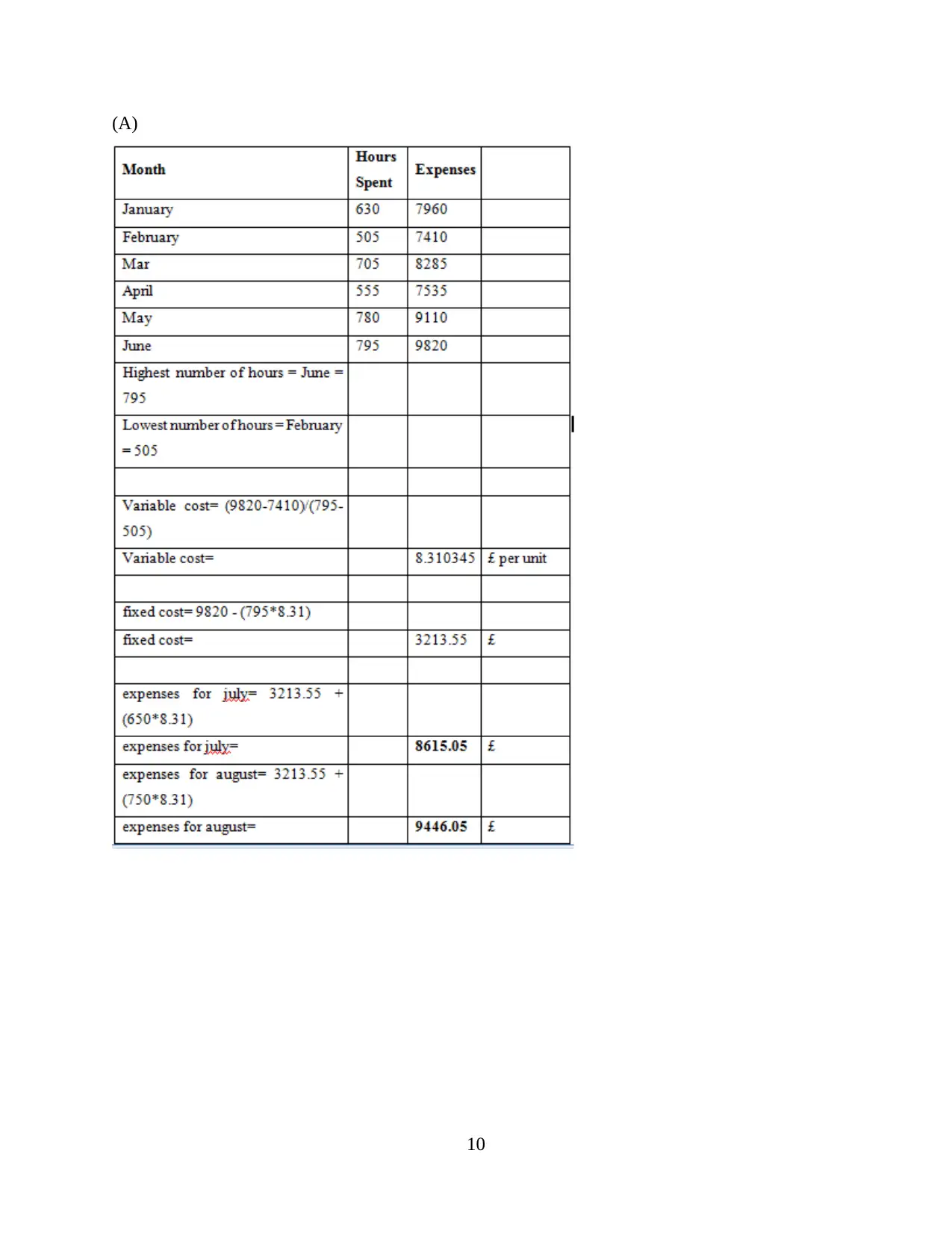

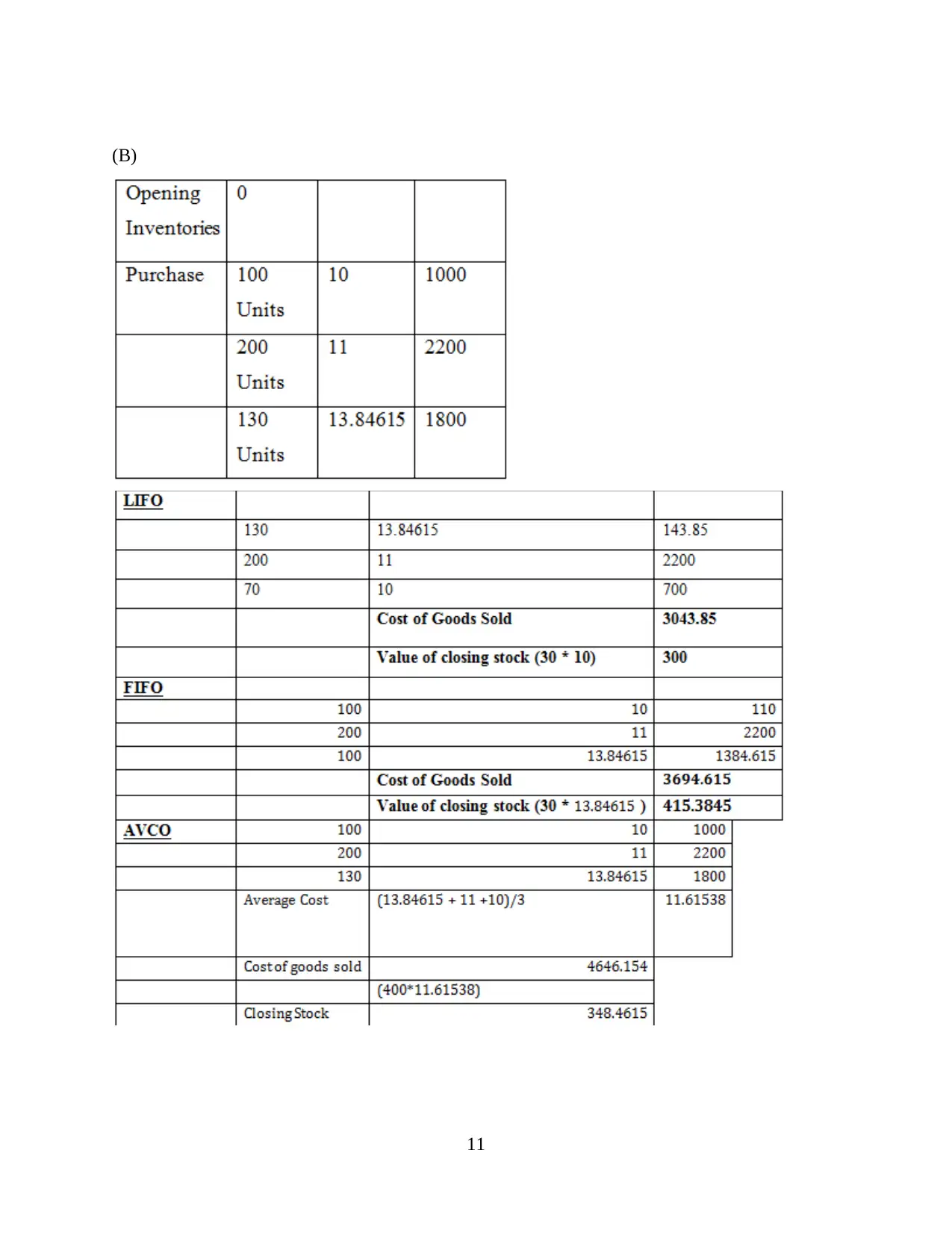

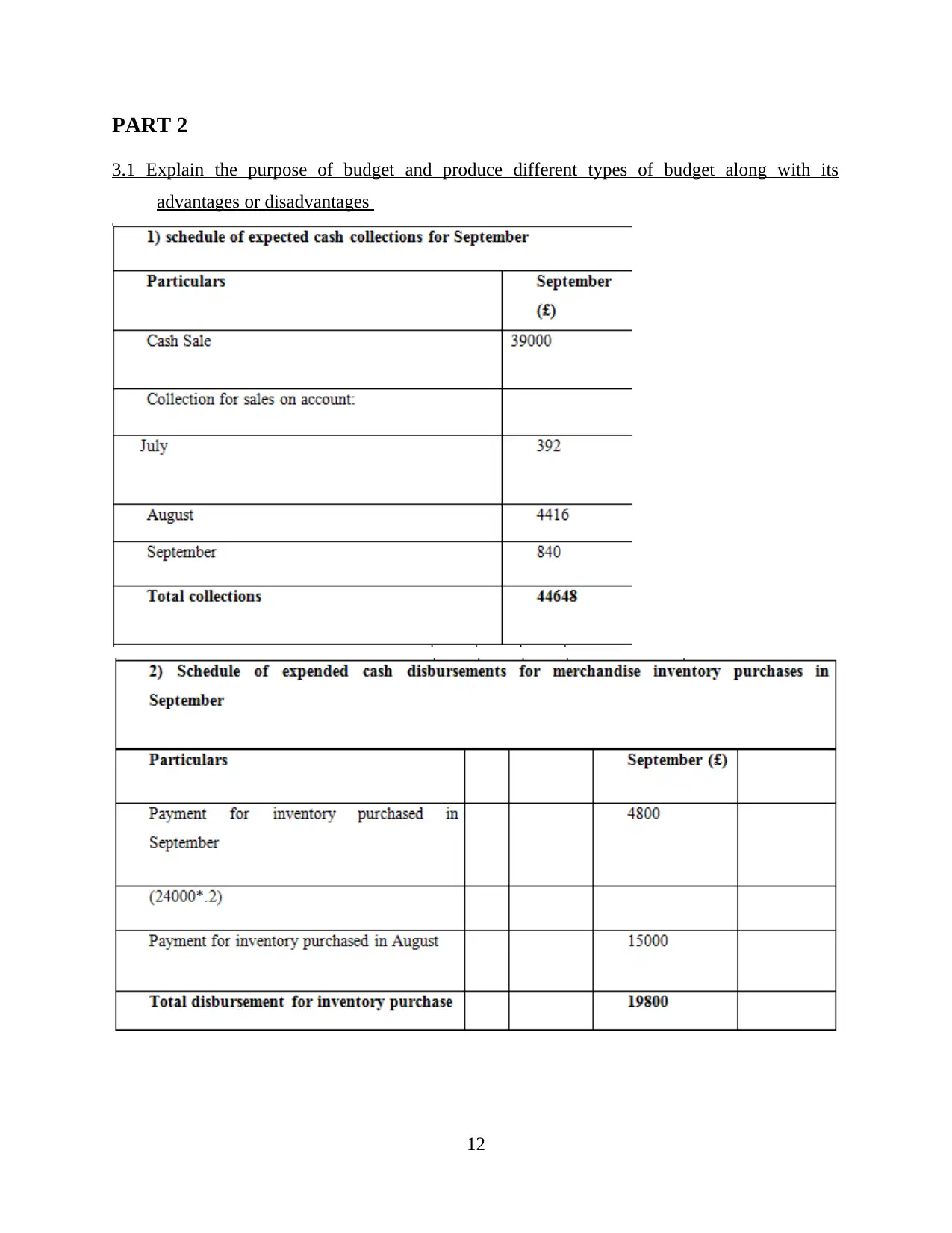

This report provides a comprehensive analysis of management accounting principles and their application within the context of UCK Furniture. It begins with an introduction to management accounting, emphasizing its role in providing financial information for managerial decision-making. The report then explores various management accounting systems, including inventory management, job costing, and price optimization, and highlights their benefits. Different methods of management accounting reporting, such as performance reports and cost managerial accounting reports, are explained. The report delves into cost analysis, calculating costs using marginal and absorption costing methods to produce income statements and cost cards, along with a discussion of their merits and demerits. Furthermore, the report examines budgeting, outlining its purpose and various types, including cash and flexible budgets, and their respective advantages and disadvantages. Finally, it addresses financial problems faced by organizations and explores performance measures, such as benchmarking and KPIs, used to assess organizational success.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.