Management Accounting Report: Prime Furniture Cost Analysis

VerifiedAdded on 2023/01/13

|17

|4143

|76

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices, focusing on their application within a business context, specifically using Prime Furniture as a case study. It begins by defining management accounting and outlining the essential requirements of different management accounting systems, including cost accounting, inventory management, and price optimization systems. The report then delves into various methods of management accounting reporting, emphasizing the importance of reliable and accurate information for effective decision-making. A significant portion of the report is dedicated to cost analysis, explaining different cost types, and calculating costs using marginal and absorption costing techniques to prepare income statements. Budgetary control tools, along with their advantages and disadvantages, are also discussed. Finally, the report compares the ways organizations adopt management accounting systems and concludes with a summary of the key findings and implications for businesses seeking to improve their financial management. The report aims to provide practical insights into how businesses can leverage management accounting for better financial performance and strategic decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................1

P2: Explain different methods used for management accounting reporting...............................3

TASK 2............................................................................................................................................5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................5

P4 Budgetary control tools along with their advantages and disadvantages............................10

TASK 4..........................................................................................................................................13

P5 Comparison within ways that adopts by organisation to adopt management accounting

system........................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................1

P2: Explain different methods used for management accounting reporting...............................3

TASK 2............................................................................................................................................5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................5

P4 Budgetary control tools along with their advantages and disadvantages............................10

TASK 4..........................................................................................................................................13

P5 Comparison within ways that adopts by organisation to adopt management accounting

system........................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting can be defined as the process that keep records to perform all

work as per internal information and monetary benefits. This refers that with strategic decisions

organisation is able to get better results by managing task with proper budget. Internal

stakeholders determines employees, managers, leaders etc. to analyse business entity for

performing all work with in market. This also leads external stakeholders to understand current

status of enterprise. Moreover, this report is written from perspective of Prime furniture which is

operating their business at small scale level. It also highlights on management accounting to

provide management accounting that is leading company to perform all work as per management

accounting system. Absorption and marginal costing that is used by management to analyse

actual cost of production. In the last, adoption of management accounting system to respond

financial problems will also included in this report.

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting: This is an operation in which financial information are being

analysed by the help of financial statement so that decision can be obtained and pre decided

goals can be achieved within the given specified time (Ansoff and et. al., 2018).

Evolution and origin of management accounting: At the time of industrial evolution

the management accounting concept was introduced. When the need of decision making was

based totally on financial information these concepts came into existence. Transportation and

textiles are two major components of Prime furniture in management accounting.

Management accounting system: Various type of system which are required to be

followed by organisation so that to get competitive edge and for analysis of financial

performance. Management accounting includes system of cost accounting, price optimisation

scheme etc. Prime furniture is involved in manufacturing activities in order to recognise benefits

of the systems and establishing them considerably. These factors are explained below:

Difference between financial and management accounting:

Management accounting Financial accounting

This helps the manager to take profit

generating decisions for the business

This helps the management team in

recognising real financial position of

1

Management accounting can be defined as the process that keep records to perform all

work as per internal information and monetary benefits. This refers that with strategic decisions

organisation is able to get better results by managing task with proper budget. Internal

stakeholders determines employees, managers, leaders etc. to analyse business entity for

performing all work with in market. This also leads external stakeholders to understand current

status of enterprise. Moreover, this report is written from perspective of Prime furniture which is

operating their business at small scale level. It also highlights on management accounting to

provide management accounting that is leading company to perform all work as per management

accounting system. Absorption and marginal costing that is used by management to analyse

actual cost of production. In the last, adoption of management accounting system to respond

financial problems will also included in this report.

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting: This is an operation in which financial information are being

analysed by the help of financial statement so that decision can be obtained and pre decided

goals can be achieved within the given specified time (Ansoff and et. al., 2018).

Evolution and origin of management accounting: At the time of industrial evolution

the management accounting concept was introduced. When the need of decision making was

based totally on financial information these concepts came into existence. Transportation and

textiles are two major components of Prime furniture in management accounting.

Management accounting system: Various type of system which are required to be

followed by organisation so that to get competitive edge and for analysis of financial

performance. Management accounting includes system of cost accounting, price optimisation

scheme etc. Prime furniture is involved in manufacturing activities in order to recognise benefits

of the systems and establishing them considerably. These factors are explained below:

Difference between financial and management accounting:

Management accounting Financial accounting

This helps the manager to take profit

generating decisions for the business

This helps the management team in

recognising real financial position of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

entity.

This assist in providing all kind of

monetary and non monetary

information.

the organisation with the help of annual

financial statements.

It renders information only for

monetary terms.

Different management accounting systems are as under:

Cost accounting system: This is a system which assist in rendering information which

are related to cost of the company that are engaged in manufacturing numerous products and

services. In the context of Prime furniture, this system renders all the relevant information of

manufacturing activities so it is necessary for them to follow this system. Preparation of efficient

budget will be easier for department of finance so as to forecast future activities related to the

business (Bryce, 2017). Two types of coast are incurred during production process which is

direct and indirect costs. Direct cost are allocated directly to the manufacturing activities

although indirect cost s are allocated to provide assistance in direct manufacturing activities.

Inventory management system: It is a system which helps in proper maintenance of

existing stock level so that to fulfil requirements of customers. Prime furniture is supposed to

acquire this system so as to establish effective relation with clients and by keeping appropriate

level of stock in warehouse and supplying products on time to the customers they can increase

customer loyalty (Certo and et. al., 2016). Inventory management system is of three types which

are FIFO, LIFO, AVCO. LIFO can be defined as the last purchased inventory will be processed

first. FIFO means earliest purchase will be firstly processes and AVCO means the method in

which cost get distributed on the basis of produced units. Management of Prime furniture is

accountable for collecting information regarding these inventories through this system of

inventory management.

Price optimisation system: The system of price optimisation involves taking out

information regarding concept of client for newly established pricing policy that is necessary to

keep loyal customers in the business. For Prime furniture it is most suitable as this helps in

maintaining current clientele by fulfilling expectations in reference to any change in price.

Job order costing system: This is a system which support all the information regarding

actual cost allotment in process of manufacturing of every unit in the organisation. This helps the

organisation in maintaining proper records of overall costs that generates easiness for the

2

This assist in providing all kind of

monetary and non monetary

information.

the organisation with the help of annual

financial statements.

It renders information only for

monetary terms.

Different management accounting systems are as under:

Cost accounting system: This is a system which assist in rendering information which

are related to cost of the company that are engaged in manufacturing numerous products and

services. In the context of Prime furniture, this system renders all the relevant information of

manufacturing activities so it is necessary for them to follow this system. Preparation of efficient

budget will be easier for department of finance so as to forecast future activities related to the

business (Bryce, 2017). Two types of coast are incurred during production process which is

direct and indirect costs. Direct cost are allocated directly to the manufacturing activities

although indirect cost s are allocated to provide assistance in direct manufacturing activities.

Inventory management system: It is a system which helps in proper maintenance of

existing stock level so that to fulfil requirements of customers. Prime furniture is supposed to

acquire this system so as to establish effective relation with clients and by keeping appropriate

level of stock in warehouse and supplying products on time to the customers they can increase

customer loyalty (Certo and et. al., 2016). Inventory management system is of three types which

are FIFO, LIFO, AVCO. LIFO can be defined as the last purchased inventory will be processed

first. FIFO means earliest purchase will be firstly processes and AVCO means the method in

which cost get distributed on the basis of produced units. Management of Prime furniture is

accountable for collecting information regarding these inventories through this system of

inventory management.

Price optimisation system: The system of price optimisation involves taking out

information regarding concept of client for newly established pricing policy that is necessary to

keep loyal customers in the business. For Prime furniture it is most suitable as this helps in

maintaining current clientele by fulfilling expectations in reference to any change in price.

Job order costing system: This is a system which support all the information regarding

actual cost allotment in process of manufacturing of every unit in the organisation. This helps the

organisation in maintaining proper records of overall costs that generates easiness for the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manager to forecast the estimated profits. This removes difficulties for the manager of Prime

furniture to terminate the manufacture of those products which are giving less profits and include

larger amount of cost so that it enhances the overall profits of the organisation.

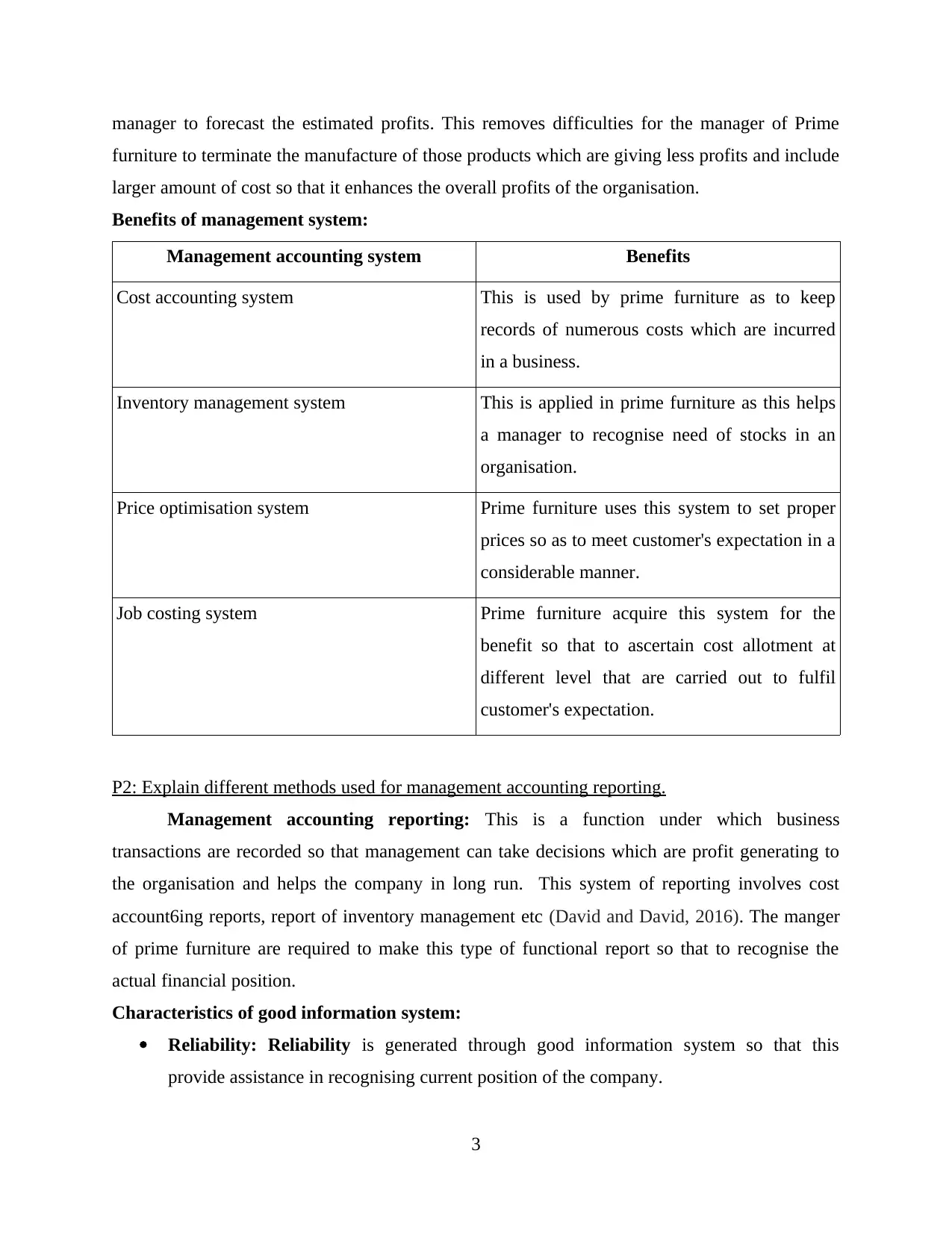

Benefits of management system:

Management accounting system Benefits

Cost accounting system This is used by prime furniture as to keep

records of numerous costs which are incurred

in a business.

Inventory management system This is applied in prime furniture as this helps

a manager to recognise need of stocks in an

organisation.

Price optimisation system Prime furniture uses this system to set proper

prices so as to meet customer's expectation in a

considerable manner.

Job costing system Prime furniture acquire this system for the

benefit so that to ascertain cost allotment at

different level that are carried out to fulfil

customer's expectation.

P2: Explain different methods used for management accounting reporting.

Management accounting reporting: This is a function under which business

transactions are recorded so that management can take decisions which are profit generating to

the organisation and helps the company in long run. This system of reporting involves cost

account6ing reports, report of inventory management etc (David and David, 2016). The manger

of prime furniture are required to make this type of functional report so that to recognise the

actual financial position.

Characteristics of good information system:

Reliability: Reliability is generated through good information system so that this

provide assistance in recognising current position of the company.

3

furniture to terminate the manufacture of those products which are giving less profits and include

larger amount of cost so that it enhances the overall profits of the organisation.

Benefits of management system:

Management accounting system Benefits

Cost accounting system This is used by prime furniture as to keep

records of numerous costs which are incurred

in a business.

Inventory management system This is applied in prime furniture as this helps

a manager to recognise need of stocks in an

organisation.

Price optimisation system Prime furniture uses this system to set proper

prices so as to meet customer's expectation in a

considerable manner.

Job costing system Prime furniture acquire this system for the

benefit so that to ascertain cost allotment at

different level that are carried out to fulfil

customer's expectation.

P2: Explain different methods used for management accounting reporting.

Management accounting reporting: This is a function under which business

transactions are recorded so that management can take decisions which are profit generating to

the organisation and helps the company in long run. This system of reporting involves cost

account6ing reports, report of inventory management etc (David and David, 2016). The manger

of prime furniture are required to make this type of functional report so that to recognise the

actual financial position.

Characteristics of good information system:

Reliability: Reliability is generated through good information system so that this

provide assistance in recognising current position of the company.

3

Accuracy: If information system is reliable then the gathered information is accurate and

can be trusted by all the stakeholders.

Reasons behind understanding and overall easy to comprehensive of reports:

The management is required to understand and interpret all the reports so that it provides

assistance in taking appropriate decisions for future growth of the business. Stakeholders of

prime furniture are assisted by analysing all the information which are related to accounting

reports.

Types of managerial accounting reports

Performance report: This is a report which helps in keeping records of overall

performance of the company for each operation (Engert, Rauter and Baumgartner, 2016). This is

used by prime furniture for equilibrium asset management so that to record individual and

overall data. This is helpful in giving bonus and recognition as according to the performance so

that incentives can be given as per the objectives attained. This report is advantageous for the

company as this is helpful in preparing efficient strategies to increase performance.

Budget report: This is an intrinsic report which is used by businesses in designing

budget to numerous functional and operational departments (Ginter, Duncan and Swayne, 2018).

This is used by managers to make a comparative study on actual and standard cost of prime

furniture. This is essential for the businesses as this provide assistance in recognising cash

liquidity.

Account receivable report: This report represents the amount of receivable from

numerous customers. Majorly this is prepared by those companies which are giving products on

credit to their customers. Prime furniture uses this to maintain record of outstanding amount hold

by clients. This is benefited to the business as this aid in recognising the amount which is unpaid.

By the help of this report the business can make rigid policies of credit so that to avoid fund

shortage.

Various management accounting system are integrated in organisational process. Price

optimisation system is used by prime furniture in order to set proper prices for the furnitures

made by them. Accounting receivable report are helpful in making appropriate credit policies so

that to recognise money owed by the clients.

4

can be trusted by all the stakeholders.

Reasons behind understanding and overall easy to comprehensive of reports:

The management is required to understand and interpret all the reports so that it provides

assistance in taking appropriate decisions for future growth of the business. Stakeholders of

prime furniture are assisted by analysing all the information which are related to accounting

reports.

Types of managerial accounting reports

Performance report: This is a report which helps in keeping records of overall

performance of the company for each operation (Engert, Rauter and Baumgartner, 2016). This is

used by prime furniture for equilibrium asset management so that to record individual and

overall data. This is helpful in giving bonus and recognition as according to the performance so

that incentives can be given as per the objectives attained. This report is advantageous for the

company as this is helpful in preparing efficient strategies to increase performance.

Budget report: This is an intrinsic report which is used by businesses in designing

budget to numerous functional and operational departments (Ginter, Duncan and Swayne, 2018).

This is used by managers to make a comparative study on actual and standard cost of prime

furniture. This is essential for the businesses as this provide assistance in recognising cash

liquidity.

Account receivable report: This report represents the amount of receivable from

numerous customers. Majorly this is prepared by those companies which are giving products on

credit to their customers. Prime furniture uses this to maintain record of outstanding amount hold

by clients. This is benefited to the business as this aid in recognising the amount which is unpaid.

By the help of this report the business can make rigid policies of credit so that to avoid fund

shortage.

Various management accounting system are integrated in organisational process. Price

optimisation system is used by prime furniture in order to set proper prices for the furnitures

made by them. Accounting receivable report are helpful in making appropriate credit policies so

that to recognise money owed by the clients.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

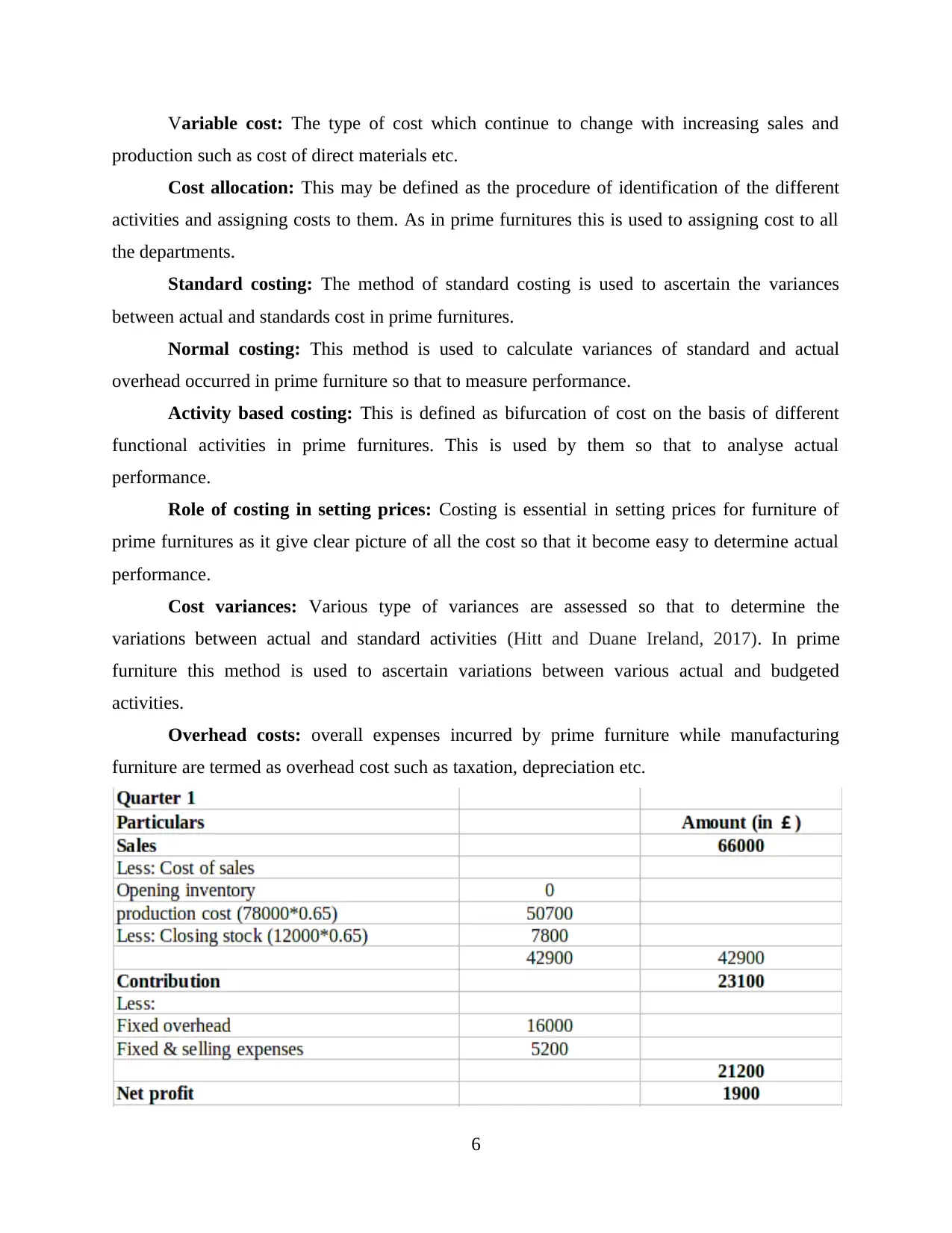

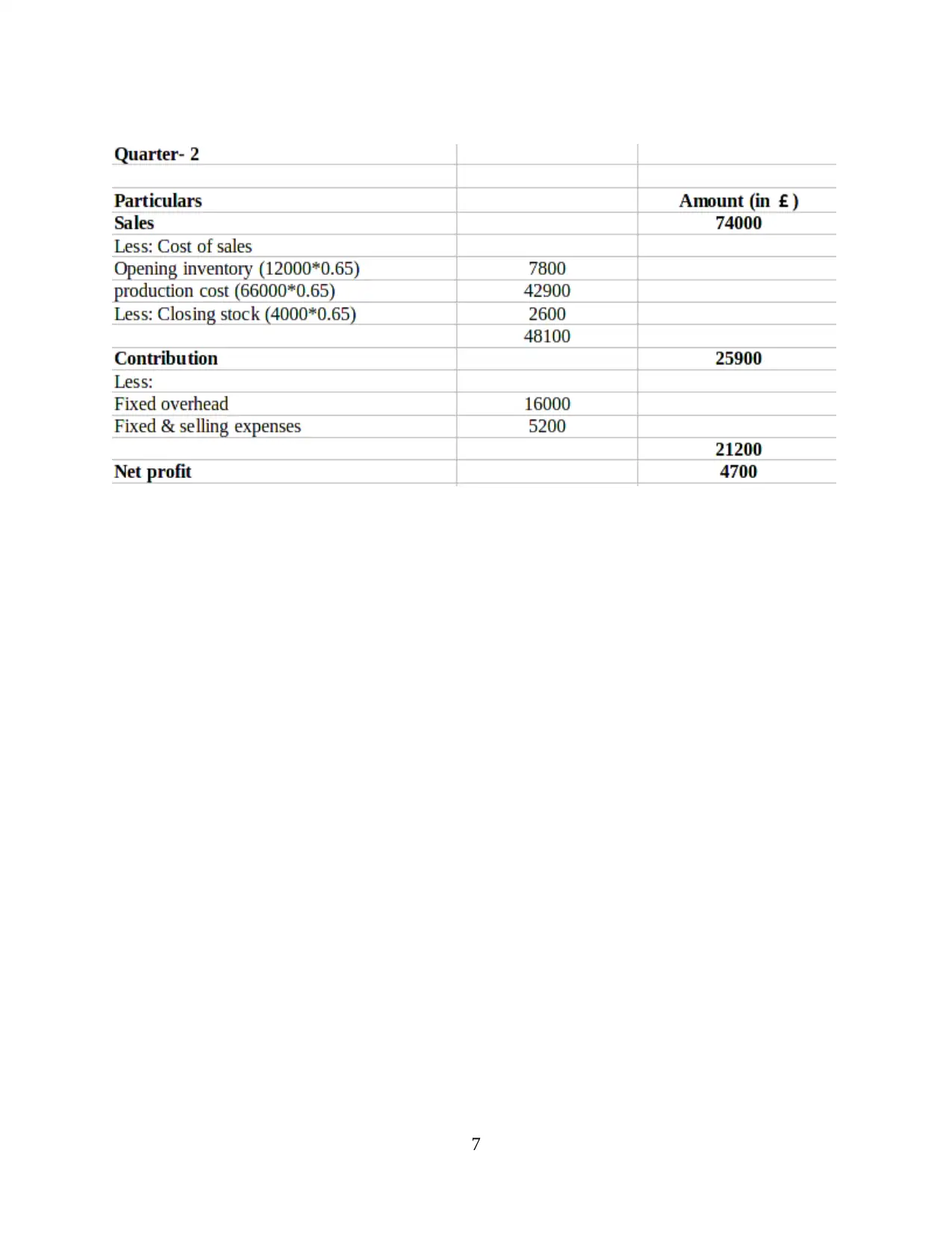

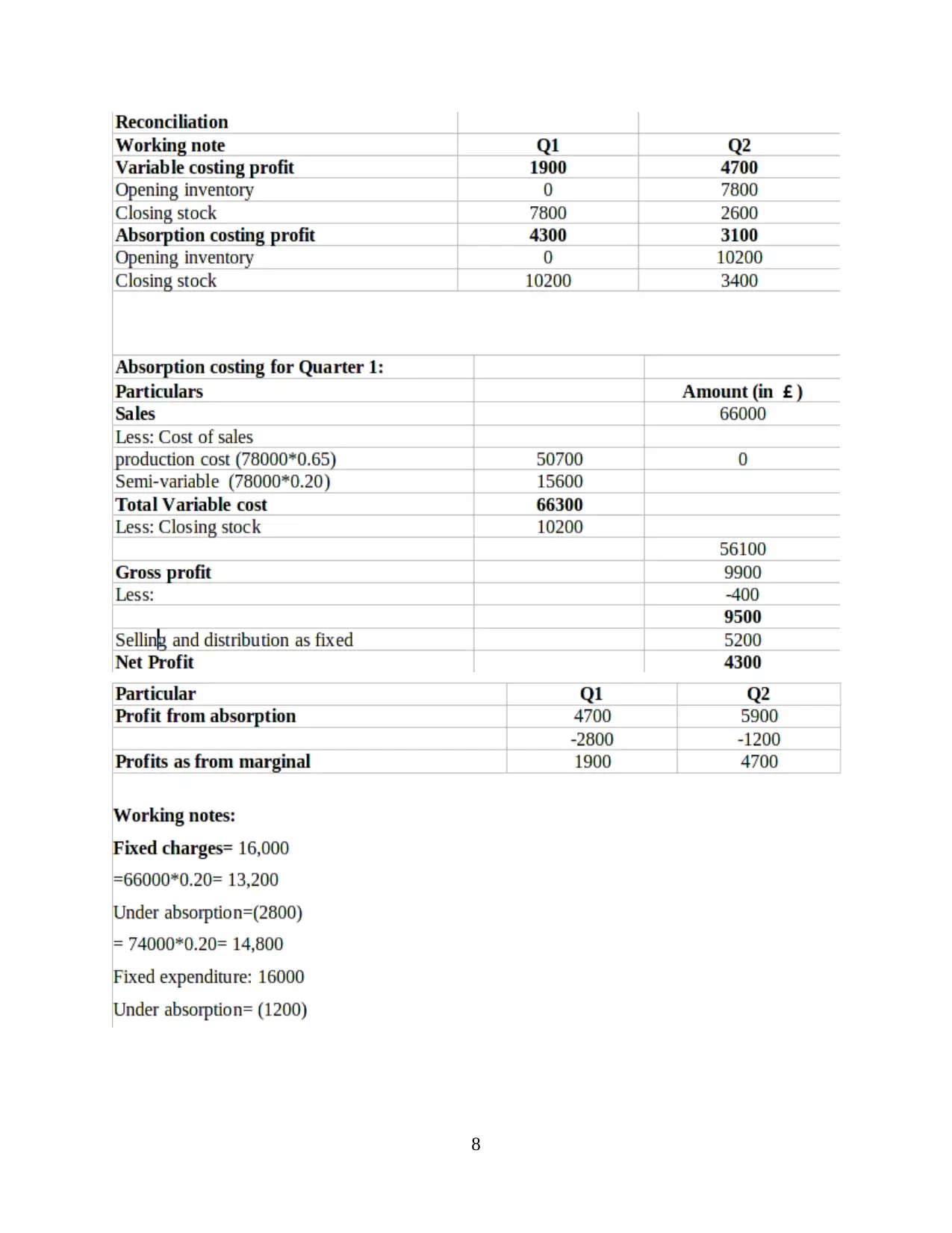

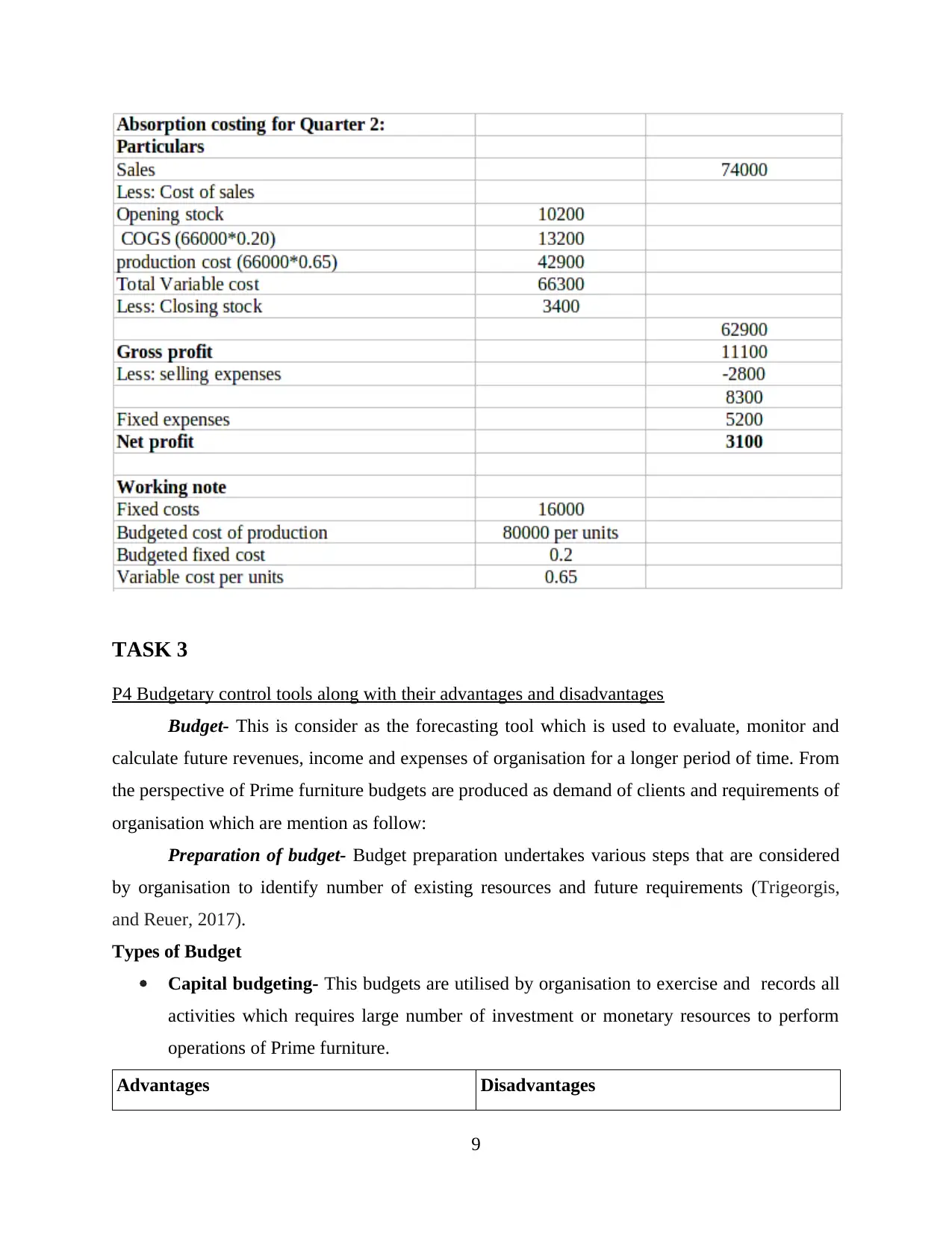

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost : This is termed as the total sum which is supposed to be paid by the purchaser to

the seller in the lieu of the product. As to attract huge amount of customer prime furniture set

suitable cost for their furniture.

Various types of cost are explained as under:

Direct cost: The costs are which are directly allocated to the manufacturing of a product

is known as direct cost such as material cost etc (Hanson and et. al., 2016).

Indirect cost: The cost which are not directly related to the manufacturing but still

essential in manufacturing process is known as indirect cost such as rent, salaries etc.

Cost analysis: This may be outlined as the procedure which is utilised in order to analyse

the numerous functions which are adopted by the business to generate maximum profit. Prime

furniture uses this aspect so that to formulate appropriate decisions to get long term profitability.

Cost volume profit: This method is adopted by management team of prime furniture in

order to recognise the key changes in profit due to change in cost and sales (Hill, 2017).

Flexible budgeting: This type of budget is used when any alterations and adjustments

are introduced in the level of activities in the organisation. This is adopted by prime furniture for

the aim to making any modification as according to fluctuating sales or cost.

Cost variance: This is defined as a functional tool which is used by prime furniture in

order to get analysis of actual and budgeted cost of manufacturing. This is majorly adopted in

business with the view to make decision strategically.

Marginal costing: This method of costing includes that per unit cost will always be

constant as it divided into fixed and variable costs. The under and over adsorption difficulties is

sorted with the help of using marginal costing. Management opt this method to plan their profits,

determination of break even point i.e. BEP and in fixation of prices.

Adsorption costing: This is a method which is used to prepare all the financial records in

order to get actual profit and transparent view of company's financial performance.

Fixed cost: The type of cost which remains constant irrespective of the level of

production such as factory rent, insurance etc.

5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost : This is termed as the total sum which is supposed to be paid by the purchaser to

the seller in the lieu of the product. As to attract huge amount of customer prime furniture set

suitable cost for their furniture.

Various types of cost are explained as under:

Direct cost: The costs are which are directly allocated to the manufacturing of a product

is known as direct cost such as material cost etc (Hanson and et. al., 2016).

Indirect cost: The cost which are not directly related to the manufacturing but still

essential in manufacturing process is known as indirect cost such as rent, salaries etc.

Cost analysis: This may be outlined as the procedure which is utilised in order to analyse

the numerous functions which are adopted by the business to generate maximum profit. Prime

furniture uses this aspect so that to formulate appropriate decisions to get long term profitability.

Cost volume profit: This method is adopted by management team of prime furniture in

order to recognise the key changes in profit due to change in cost and sales (Hill, 2017).

Flexible budgeting: This type of budget is used when any alterations and adjustments

are introduced in the level of activities in the organisation. This is adopted by prime furniture for

the aim to making any modification as according to fluctuating sales or cost.

Cost variance: This is defined as a functional tool which is used by prime furniture in

order to get analysis of actual and budgeted cost of manufacturing. This is majorly adopted in

business with the view to make decision strategically.

Marginal costing: This method of costing includes that per unit cost will always be

constant as it divided into fixed and variable costs. The under and over adsorption difficulties is

sorted with the help of using marginal costing. Management opt this method to plan their profits,

determination of break even point i.e. BEP and in fixation of prices.

Adsorption costing: This is a method which is used to prepare all the financial records in

order to get actual profit and transparent view of company's financial performance.

Fixed cost: The type of cost which remains constant irrespective of the level of

production such as factory rent, insurance etc.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable cost: The type of cost which continue to change with increasing sales and

production such as cost of direct materials etc.

Cost allocation: This may be defined as the procedure of identification of the different

activities and assigning costs to them. As in prime furnitures this is used to assigning cost to all

the departments.

Standard costing: The method of standard costing is used to ascertain the variances

between actual and standards cost in prime furnitures.

Normal costing: This method is used to calculate variances of standard and actual

overhead occurred in prime furniture so that to measure performance.

Activity based costing: This is defined as bifurcation of cost on the basis of different

functional activities in prime furnitures. This is used by them so that to analyse actual

performance.

Role of costing in setting prices: Costing is essential in setting prices for furniture of

prime furnitures as it give clear picture of all the cost so that it become easy to determine actual

performance.

Cost variances: Various type of variances are assessed so that to determine the

variations between actual and standard activities (Hitt and Duane Ireland, 2017). In prime

furniture this method is used to ascertain variations between various actual and budgeted

activities.

Overhead costs: overall expenses incurred by prime furniture while manufacturing

furniture are termed as overhead cost such as taxation, depreciation etc.

6

production such as cost of direct materials etc.

Cost allocation: This may be defined as the procedure of identification of the different

activities and assigning costs to them. As in prime furnitures this is used to assigning cost to all

the departments.

Standard costing: The method of standard costing is used to ascertain the variances

between actual and standards cost in prime furnitures.

Normal costing: This method is used to calculate variances of standard and actual

overhead occurred in prime furniture so that to measure performance.

Activity based costing: This is defined as bifurcation of cost on the basis of different

functional activities in prime furnitures. This is used by them so that to analyse actual

performance.

Role of costing in setting prices: Costing is essential in setting prices for furniture of

prime furnitures as it give clear picture of all the cost so that it become easy to determine actual

performance.

Cost variances: Various type of variances are assessed so that to determine the

variations between actual and standard activities (Hitt and Duane Ireland, 2017). In prime

furniture this method is used to ascertain variations between various actual and budgeted

activities.

Overhead costs: overall expenses incurred by prime furniture while manufacturing

furniture are termed as overhead cost such as taxation, depreciation etc.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

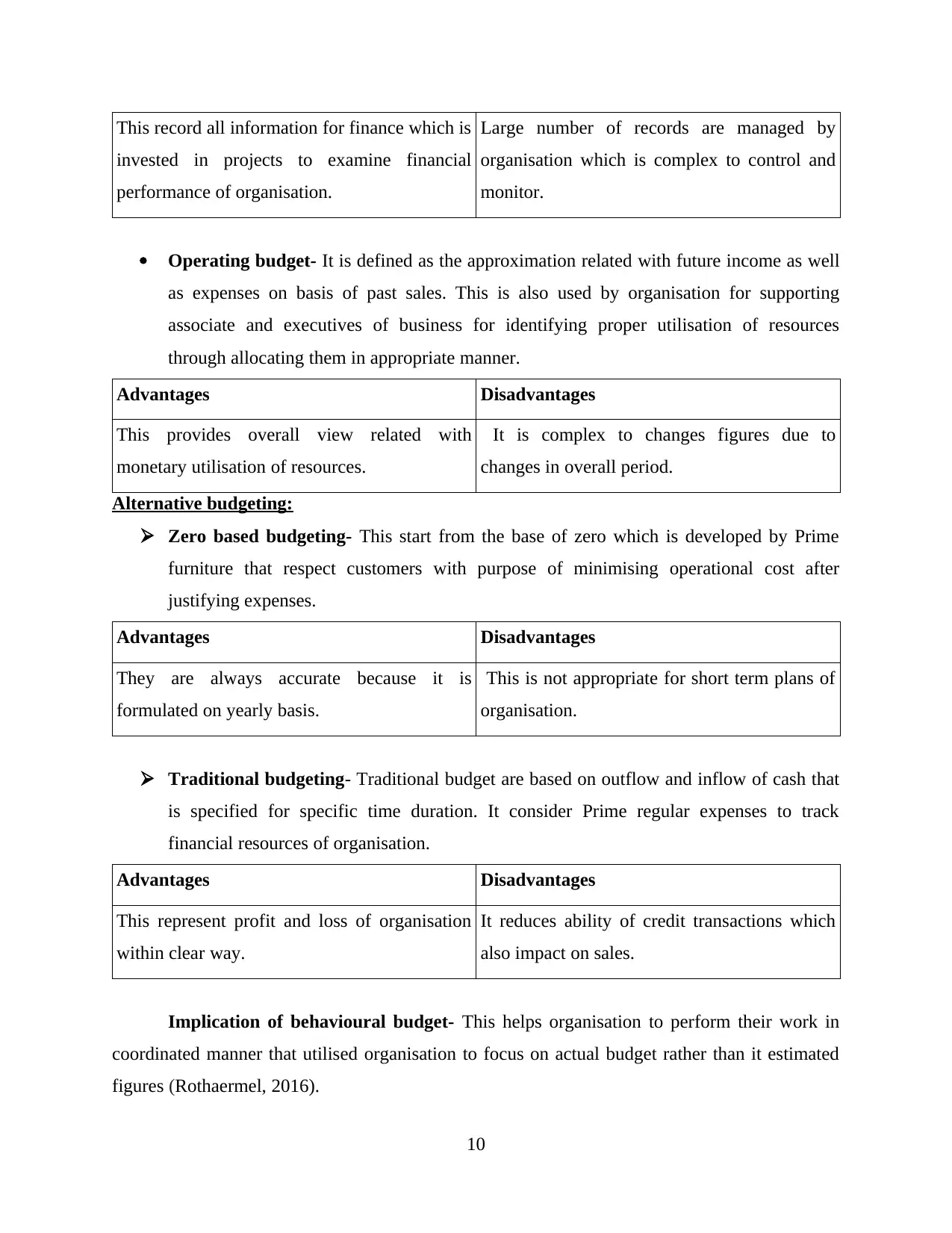

P4 Budgetary control tools along with their advantages and disadvantages

Budget- This is consider as the forecasting tool which is used to evaluate, monitor and

calculate future revenues, income and expenses of organisation for a longer period of time. From

the perspective of Prime furniture budgets are produced as demand of clients and requirements of

organisation which are mention as follow:

Preparation of budget- Budget preparation undertakes various steps that are considered

by organisation to identify number of existing resources and future requirements (Trigeorgis,

and Reuer, 2017).

Types of Budget

Capital budgeting- This budgets are utilised by organisation to exercise and records all

activities which requires large number of investment or monetary resources to perform

operations of Prime furniture.

Advantages Disadvantages

9

P4 Budgetary control tools along with their advantages and disadvantages

Budget- This is consider as the forecasting tool which is used to evaluate, monitor and

calculate future revenues, income and expenses of organisation for a longer period of time. From

the perspective of Prime furniture budgets are produced as demand of clients and requirements of

organisation which are mention as follow:

Preparation of budget- Budget preparation undertakes various steps that are considered

by organisation to identify number of existing resources and future requirements (Trigeorgis,

and Reuer, 2017).

Types of Budget

Capital budgeting- This budgets are utilised by organisation to exercise and records all

activities which requires large number of investment or monetary resources to perform

operations of Prime furniture.

Advantages Disadvantages

9

This record all information for finance which is

invested in projects to examine financial

performance of organisation.

Large number of records are managed by

organisation which is complex to control and

monitor.

Operating budget- It is defined as the approximation related with future income as well

as expenses on basis of past sales. This is also used by organisation for supporting

associate and executives of business for identifying proper utilisation of resources

through allocating them in appropriate manner.

Advantages Disadvantages

This provides overall view related with

monetary utilisation of resources.

It is complex to changes figures due to

changes in overall period.

Alternative budgeting:

Zero based budgeting- This start from the base of zero which is developed by Prime

furniture that respect customers with purpose of minimising operational cost after

justifying expenses.

Advantages Disadvantages

They are always accurate because it is

formulated on yearly basis.

This is not appropriate for short term plans of

organisation.

Traditional budgeting- Traditional budget are based on outflow and inflow of cash that

is specified for specific time duration. It consider Prime regular expenses to track

financial resources of organisation.

Advantages Disadvantages

This represent profit and loss of organisation

within clear way.

It reduces ability of credit transactions which

also impact on sales.

Implication of behavioural budget- This helps organisation to perform their work in

coordinated manner that utilised organisation to focus on actual budget rather than it estimated

figures (Rothaermel, 2016).

10

invested in projects to examine financial

performance of organisation.

Large number of records are managed by

organisation which is complex to control and

monitor.

Operating budget- It is defined as the approximation related with future income as well

as expenses on basis of past sales. This is also used by organisation for supporting

associate and executives of business for identifying proper utilisation of resources

through allocating them in appropriate manner.

Advantages Disadvantages

This provides overall view related with

monetary utilisation of resources.

It is complex to changes figures due to

changes in overall period.

Alternative budgeting:

Zero based budgeting- This start from the base of zero which is developed by Prime

furniture that respect customers with purpose of minimising operational cost after

justifying expenses.

Advantages Disadvantages

They are always accurate because it is

formulated on yearly basis.

This is not appropriate for short term plans of

organisation.

Traditional budgeting- Traditional budget are based on outflow and inflow of cash that

is specified for specific time duration. It consider Prime regular expenses to track

financial resources of organisation.

Advantages Disadvantages

This represent profit and loss of organisation

within clear way.

It reduces ability of credit transactions which

also impact on sales.

Implication of behavioural budget- This helps organisation to perform their work in

coordinated manner that utilised organisation to focus on actual budget rather than it estimated

figures (Rothaermel, 2016).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.