Management Accounting Report: Flying Airline Company Proposal

VerifiedAdded on 2020/05/28

|7

|1052

|84

Report

AI Summary

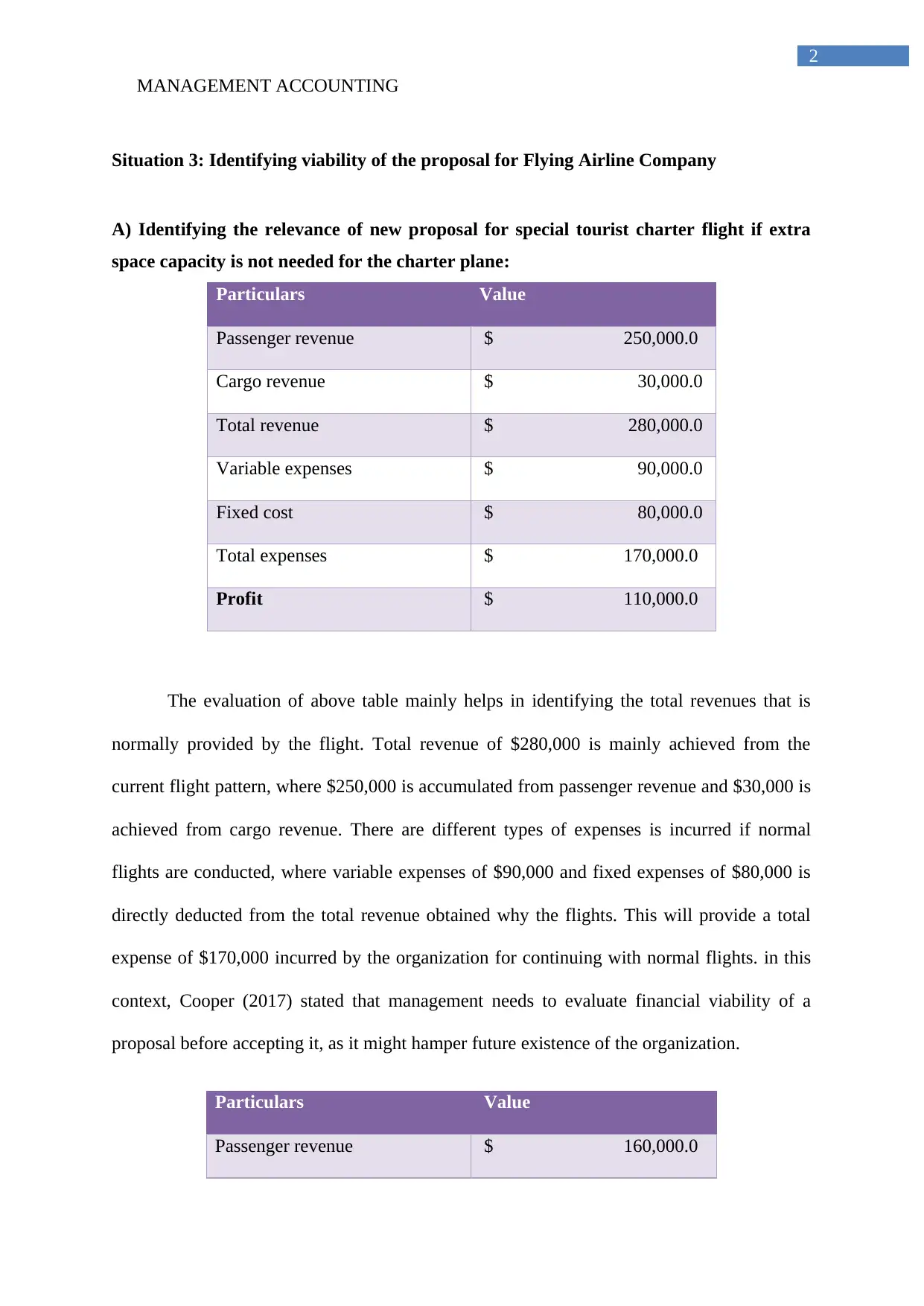

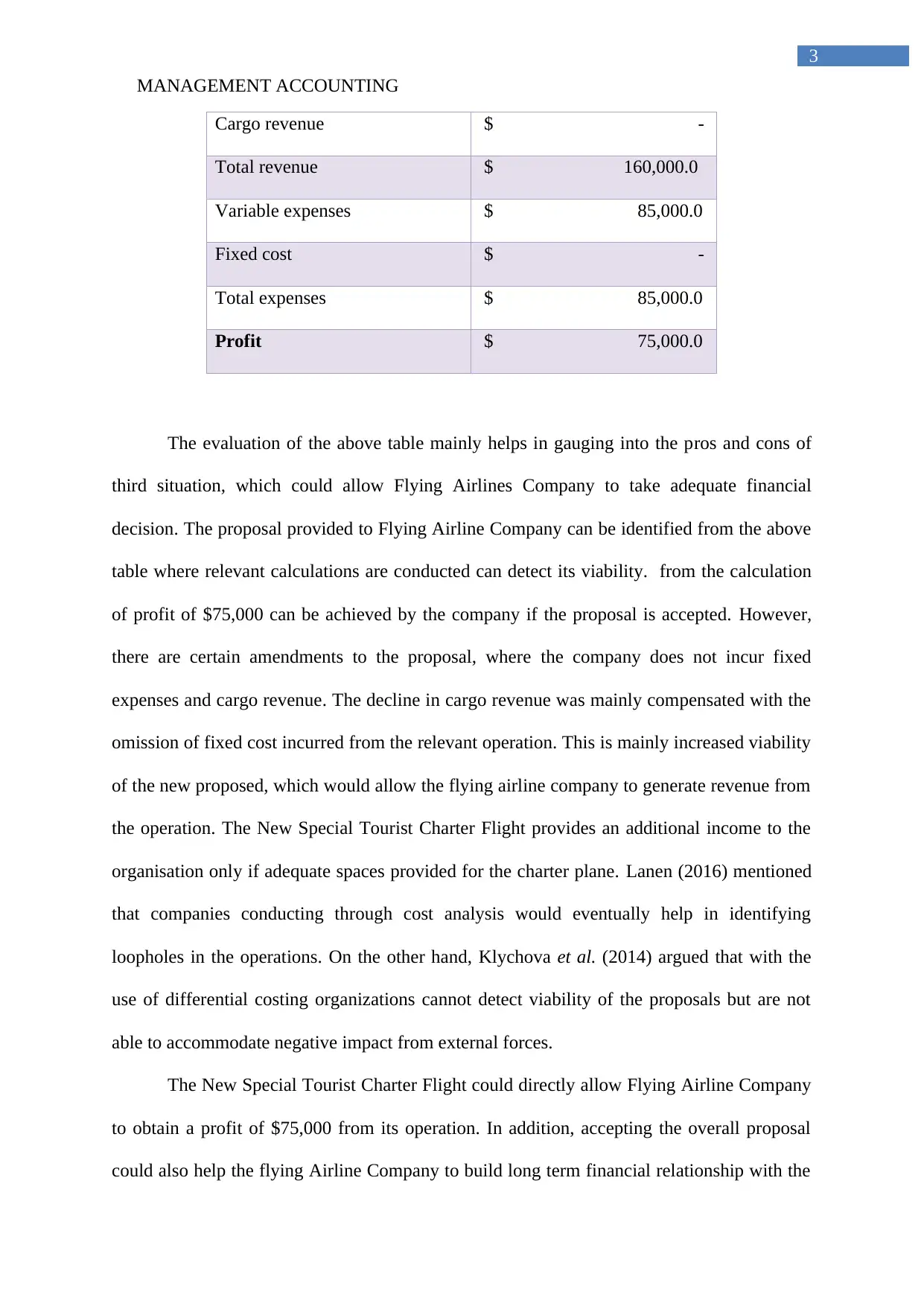

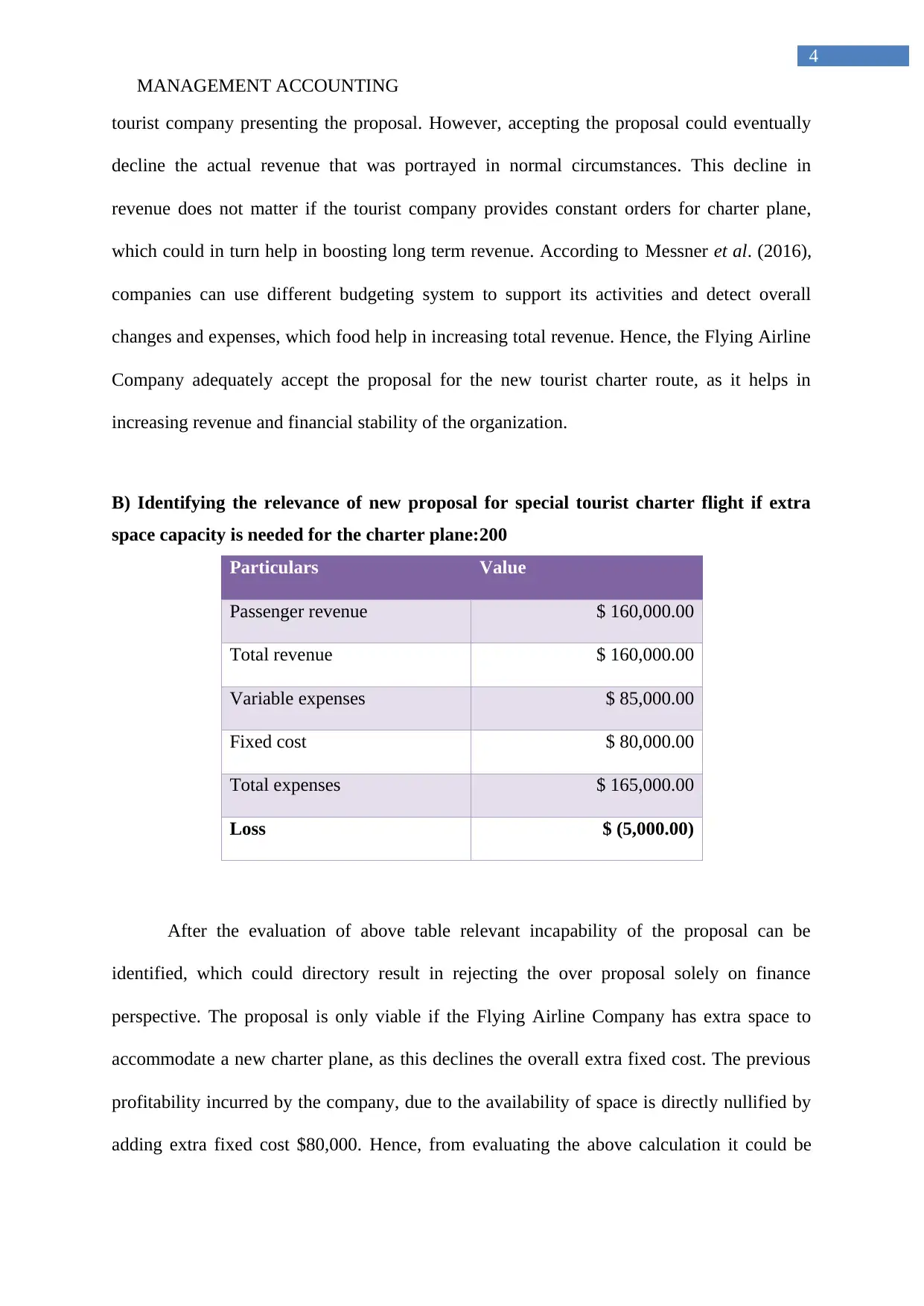

This report provides a comprehensive financial analysis of a proposal for Flying Airline Company regarding a new special tourist charter flight. The analysis evaluates the viability of the proposal under two scenarios: one where extra space capacity is not needed and another where it is required. The report assesses passenger and cargo revenue, variable and fixed expenses, and calculates the resulting profit or loss for each scenario. It references relevant accounting literature and considers the implications of accepting or rejecting the proposal, including its impact on the company's financial stability and potential for long-term revenue. The report highlights the importance of cost analysis and differential costing in making informed financial decisions, ultimately recommending whether the airline should accept the proposal based on its potential profitability and impact on the company's overall financial performance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.