Management Accounting Report: Techniques and Analysis for Creams Ltd.

VerifiedAdded on 2023/01/11

|18

|4600

|69

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their practical application within Creams Ltd., a company selling ice-creams, doughnuts and waffles. The report begins by defining management accounting and its essential systems, including cost accounting, inventory management, job costing, and price optimization. It then explores various management accounting reporting methods such as job cost reports, departmental reports, performance reports, and product/service profitability reports. The core of the report delves into the application of management accounting techniques, specifically marginal costing and absorption costing, evaluating their advantages and disadvantages. The report further examines the benefits of management accounting systems and offers a critical evaluation of their effectiveness. It also touches on the advantages and disadvantages of planning tools, and compares how organizations adapt management accounting systems to address financial challenges. Overall, the report provides a practical understanding of how management accounting supports decision-making and improves operational efficiency within a business context.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

TASK 1..........................................................................................................................................................3

P1: Explanation of management accounting and the essential requirement of its systems....................3

P2: Management accounting reporting methods....................................................................................4

M1: Benefits of management accounting systems..................................................................................5

D1: Critical evaluation of management accounting systems...................................................................6

TASK 2..........................................................................................................................................................6

P3: Application of various techniques of management accounting.........................................................6

M2: Accurate application of techniques................................................................................................13

D2: Producing of financial reports.........................................................................................................13

TASK 3........................................................................................................................................................13

P4: Advantages and disadvantages of planning tools............................................................................13

M3: Analysis of planning tools...............................................................................................................15

TASK 4........................................................................................................................................................15

P5: Comparison of organizations in adapting to management accounting systems to solve financial

problems...............................................................................................................................................15

M4: Analysis of organizations dealing with financial problems.............................................................16

D3: Evaluation of planning tools............................................................................................................16

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

TASK 1..........................................................................................................................................................3

P1: Explanation of management accounting and the essential requirement of its systems....................3

P2: Management accounting reporting methods....................................................................................4

M1: Benefits of management accounting systems..................................................................................5

D1: Critical evaluation of management accounting systems...................................................................6

TASK 2..........................................................................................................................................................6

P3: Application of various techniques of management accounting.........................................................6

M2: Accurate application of techniques................................................................................................13

D2: Producing of financial reports.........................................................................................................13

TASK 3........................................................................................................................................................13

P4: Advantages and disadvantages of planning tools............................................................................13

M3: Analysis of planning tools...............................................................................................................15

TASK 4........................................................................................................................................................15

P5: Comparison of organizations in adapting to management accounting systems to solve financial

problems...............................................................................................................................................15

M4: Analysis of organizations dealing with financial problems.............................................................16

D3: Evaluation of planning tools............................................................................................................16

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

INTRODUCTION

Management accounting refers to the use of financial provisions, data and information

effectively and efficiently by the managers in order to help in decision-making process

(Alawattage, Wickramasinghe and Uddin, 2017). It is a technique which helps the managers to

take the required decisions at the right time for the enterprise. It helps the managers to better

inform themselves before they take the required decisions which can impact the operations of an

enterprise both in the short-run as well as the long-run. Thus it is quite a helpful tool for the

managers. This report is based on Creams Ltd. which sells ice-creams, doughnuts and waffles in

the market. In this project, specific focus will be made on demonstration of understanding of

management accounting systems, application of a range of techniques. Additionally, analysis on

use of planning tools and comparison of ways in which firms can use management accounting

data will be analyzed.

TASK 1

P1: Explanation of management accounting and the essential requirement of its

systems

Management accounting refers to use of various types of techniques in order to help in

taking of various types of decisions for the benefit of the management of the enterprise

(Alsharari and Youssef, 2017). It is used by the managers of Creams Ltd. in order to help them in

raising the overall efficiency, effectiveness and productivity of the enterprise.

Management accounting systems-

Cost accounting system- Cost accounting system is used for identification of various

types of costs which can incur within an organization such as fixed costs, semi-variable costs and

variable costs. The managers of Creams Ltd. can make use of this system to identify and

segregate their costs in order to reduce it. This will help them in maximizing their level of profits

and achieving their short-term and long-term objectives in the future.

Essential requirements-

Cost accounting system must be able to identify various types of costs which are

incurring within an enterprise.

Cost accounting system must be able to identify the overheads and should be able to

provide different techniques to absorb them.

Inventory management system- Inventory management system is used for the purpose

of management of items in the inventory of the enterprise. It can be used by the managers

of Creams Ltd. to better track the stock items and properly manage them so that there is

no mismanagement of stock occurring within the organization. The managers of Creams

Management accounting refers to the use of financial provisions, data and information

effectively and efficiently by the managers in order to help in decision-making process

(Alawattage, Wickramasinghe and Uddin, 2017). It is a technique which helps the managers to

take the required decisions at the right time for the enterprise. It helps the managers to better

inform themselves before they take the required decisions which can impact the operations of an

enterprise both in the short-run as well as the long-run. Thus it is quite a helpful tool for the

managers. This report is based on Creams Ltd. which sells ice-creams, doughnuts and waffles in

the market. In this project, specific focus will be made on demonstration of understanding of

management accounting systems, application of a range of techniques. Additionally, analysis on

use of planning tools and comparison of ways in which firms can use management accounting

data will be analyzed.

TASK 1

P1: Explanation of management accounting and the essential requirement of its

systems

Management accounting refers to use of various types of techniques in order to help in

taking of various types of decisions for the benefit of the management of the enterprise

(Alsharari and Youssef, 2017). It is used by the managers of Creams Ltd. in order to help them in

raising the overall efficiency, effectiveness and productivity of the enterprise.

Management accounting systems-

Cost accounting system- Cost accounting system is used for identification of various

types of costs which can incur within an organization such as fixed costs, semi-variable costs and

variable costs. The managers of Creams Ltd. can make use of this system to identify and

segregate their costs in order to reduce it. This will help them in maximizing their level of profits

and achieving their short-term and long-term objectives in the future.

Essential requirements-

Cost accounting system must be able to identify various types of costs which are

incurring within an enterprise.

Cost accounting system must be able to identify the overheads and should be able to

provide different techniques to absorb them.

Inventory management system- Inventory management system is used for the purpose

of management of items in the inventory of the enterprise. It can be used by the managers

of Creams Ltd. to better track the stock items and properly manage them so that there is

no mismanagement of stock occurring within the organization. The managers of Creams

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ltd. can make use of this system so that the stock can be effectively managed within the

organization.

Essential requirements-

Inventory management system should be able to facilitate better management of

inventory.

Inventory management system must be able to facilitate the use of techniques like LIFO,

FIFO etc. which help in tracking of inflows and outflows of stock items.

Job costing system- Job costing system is used in order to maintain a track record of job

orders received and job orders given within the enterprise (Alsharari, 2019). It is most

commonly used by manufacturing organizations. As Creams Ltd. deals in manufacturing

it can use this system. This system will help the company to properly manage its job

orders. By proper management of job orders and tracking those from starting till

completion the company can raise its efficiency, effectiveness and productivity level in

the future.

Essential requirements-

Job costing system should enable checking of status of job orders from receiving the

orders till their completion.

Job costing system should enable to maintain a proper track of the job orders received in

the company.

Price optimization system- Price optimization system is used in order to facilitate the

setting up of the right price of a product or a service within the organization. It can be

used to revise the strategies related to pricing. The managers of Creams Ltd. can make

use of it in order to set a right price.

Essential requirements-

Price optimization system must facilitate setting up of a right price.

Price optimization system should be able to identify the change in price so that profits

can be maximized by changing price.

P2: Management accounting reporting methods

There are plenty of methods which can be used for management accounting reporting

(Aouni, McGillis and Abdulkarim, 2017). The managers of Creams Ltd. make use of the

following methods which are explained as follows in the context of the company-

Job cost reports- These reports can be used for identifying the various types of costs

associated with the job orders. These reports are prepared on the basis of job costing accounts

within the organization. These reports summarize the overall job orders on the basis of orders

received and orders given. The managers of Creams Ltd. can use these reports to identify

organization.

Essential requirements-

Inventory management system should be able to facilitate better management of

inventory.

Inventory management system must be able to facilitate the use of techniques like LIFO,

FIFO etc. which help in tracking of inflows and outflows of stock items.

Job costing system- Job costing system is used in order to maintain a track record of job

orders received and job orders given within the enterprise (Alsharari, 2019). It is most

commonly used by manufacturing organizations. As Creams Ltd. deals in manufacturing

it can use this system. This system will help the company to properly manage its job

orders. By proper management of job orders and tracking those from starting till

completion the company can raise its efficiency, effectiveness and productivity level in

the future.

Essential requirements-

Job costing system should enable checking of status of job orders from receiving the

orders till their completion.

Job costing system should enable to maintain a proper track of the job orders received in

the company.

Price optimization system- Price optimization system is used in order to facilitate the

setting up of the right price of a product or a service within the organization. It can be

used to revise the strategies related to pricing. The managers of Creams Ltd. can make

use of it in order to set a right price.

Essential requirements-

Price optimization system must facilitate setting up of a right price.

Price optimization system should be able to identify the change in price so that profits

can be maximized by changing price.

P2: Management accounting reporting methods

There are plenty of methods which can be used for management accounting reporting

(Aouni, McGillis and Abdulkarim, 2017). The managers of Creams Ltd. make use of the

following methods which are explained as follows in the context of the company-

Job cost reports- These reports can be used for identifying the various types of costs

associated with the job orders. These reports are prepared on the basis of job costing accounts

within the organization. These reports summarize the overall job orders on the basis of orders

received and orders given. The managers of Creams Ltd. can use these reports to identify

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

whether excessive expenditure is being done in completion of job orders in the enterprise. If

excessive expenses are being incurred rectification steps can be taken with the help of these

reports so that the level of profits can be maximized within the organization.

Departmental reports- In a big company there are different types of departments and

segments such as production, finance, HR, marketing, sales etc. These reports are prepared in

order to identify the problems which are there in different departments of an enterprise.

Segregation of departments becomes quite essential for preparation of these reports

(Arunruangsirilert and Chonglerttham, 2017). The managers of Creams Ltd. can make use of

these reports which will help in raising the level of efficiency, effectiveness and productivity in

the departments. This will lead to increase in the profits of the company and will provide it with

strategic advantage against its various competitors in the market. Thus these reports are quite

useful from the point of view of management of an organization.

Performance reports- Performance report is an important activity in project

communication management. It involves collection of information and dissemination of

information, utilization of resources and forecasting of future data (Project Management

Concepts: Defining Performance Reporting, 2019). The managers of Creams Ltd. can make use

of these reports which will help in measurement and comparison of performance to identify the

deviations and variances which are occurring in the performance of the organization. This can

help in quickly taking of measures to improve the overall performance so that strategic

advantage which is gained by the company can be maintained.

Product/service profitability report- Product/service profitability report can be used in

order to identify the prospects of earning of profits on a particular product or a service (Bolt-Lee

and Monte Swain, 2016). This is especially very helpful when a firm has to earn higher profits in

the future by innovating new products and services. This report can be used by the managers of

Creams Ltd. to identify the prospects of launching a new product or a service within the market.

It can be used to identify the problems or issues which are related with launching a new product

or service. Thus if the company is able to use this report effectively then it will allow it to

innovate in the market which gives it an excellent opportunity for maximizing its level of profits

in the future time period.

M1: Benefits of management accounting systems

Management accounting systems have their benefits. Cost accounting system is

beneficial as it helps in reducing the excessive costs. Inventory management system helps in

better tracking of stock items in the inventory. Job costing system helps in better tracking of the

job orders within the organization. Price optimization system helps in setting of the right price in

the organization so that the profits can be maximized. Thus the managers of Creams Ltd. can

benefit from using each of these systems.

excessive expenses are being incurred rectification steps can be taken with the help of these

reports so that the level of profits can be maximized within the organization.

Departmental reports- In a big company there are different types of departments and

segments such as production, finance, HR, marketing, sales etc. These reports are prepared in

order to identify the problems which are there in different departments of an enterprise.

Segregation of departments becomes quite essential for preparation of these reports

(Arunruangsirilert and Chonglerttham, 2017). The managers of Creams Ltd. can make use of

these reports which will help in raising the level of efficiency, effectiveness and productivity in

the departments. This will lead to increase in the profits of the company and will provide it with

strategic advantage against its various competitors in the market. Thus these reports are quite

useful from the point of view of management of an organization.

Performance reports- Performance report is an important activity in project

communication management. It involves collection of information and dissemination of

information, utilization of resources and forecasting of future data (Project Management

Concepts: Defining Performance Reporting, 2019). The managers of Creams Ltd. can make use

of these reports which will help in measurement and comparison of performance to identify the

deviations and variances which are occurring in the performance of the organization. This can

help in quickly taking of measures to improve the overall performance so that strategic

advantage which is gained by the company can be maintained.

Product/service profitability report- Product/service profitability report can be used in

order to identify the prospects of earning of profits on a particular product or a service (Bolt-Lee

and Monte Swain, 2016). This is especially very helpful when a firm has to earn higher profits in

the future by innovating new products and services. This report can be used by the managers of

Creams Ltd. to identify the prospects of launching a new product or a service within the market.

It can be used to identify the problems or issues which are related with launching a new product

or service. Thus if the company is able to use this report effectively then it will allow it to

innovate in the market which gives it an excellent opportunity for maximizing its level of profits

in the future time period.

M1: Benefits of management accounting systems

Management accounting systems have their benefits. Cost accounting system is

beneficial as it helps in reducing the excessive costs. Inventory management system helps in

better tracking of stock items in the inventory. Job costing system helps in better tracking of the

job orders within the organization. Price optimization system helps in setting of the right price in

the organization so that the profits can be maximized. Thus the managers of Creams Ltd. can

benefit from using each of these systems.

D1: Critical evaluation of management accounting systems

The management accounting systems can be effectively used within the organization.

Cost accounting system can be used for monitoring and controlling of costs. Inventory

management system can be used to track the movement of inventory within the organization. Job

costing system can be used for the purpose of management of job orders. Price optimization

system helps in choosing a right price for the products and services. Thus all of them can be

effectively used by the managers of Creams Ltd.

TASK 2

P3: Application of various techniques of management accounting

The management accounting systems can be effectively used within the organization.

Cost accounting system can be used for monitoring and controlling of costs. Inventory

management system can be used to track the movement of inventory within the organization. Job

costing system can be used for the purpose of management of job orders. Price optimization

system helps in choosing a right price for the products and services. Thus all of them can be

effectively used by the managers of Creams Ltd.

TASK 2

P3: Application of various techniques of management accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

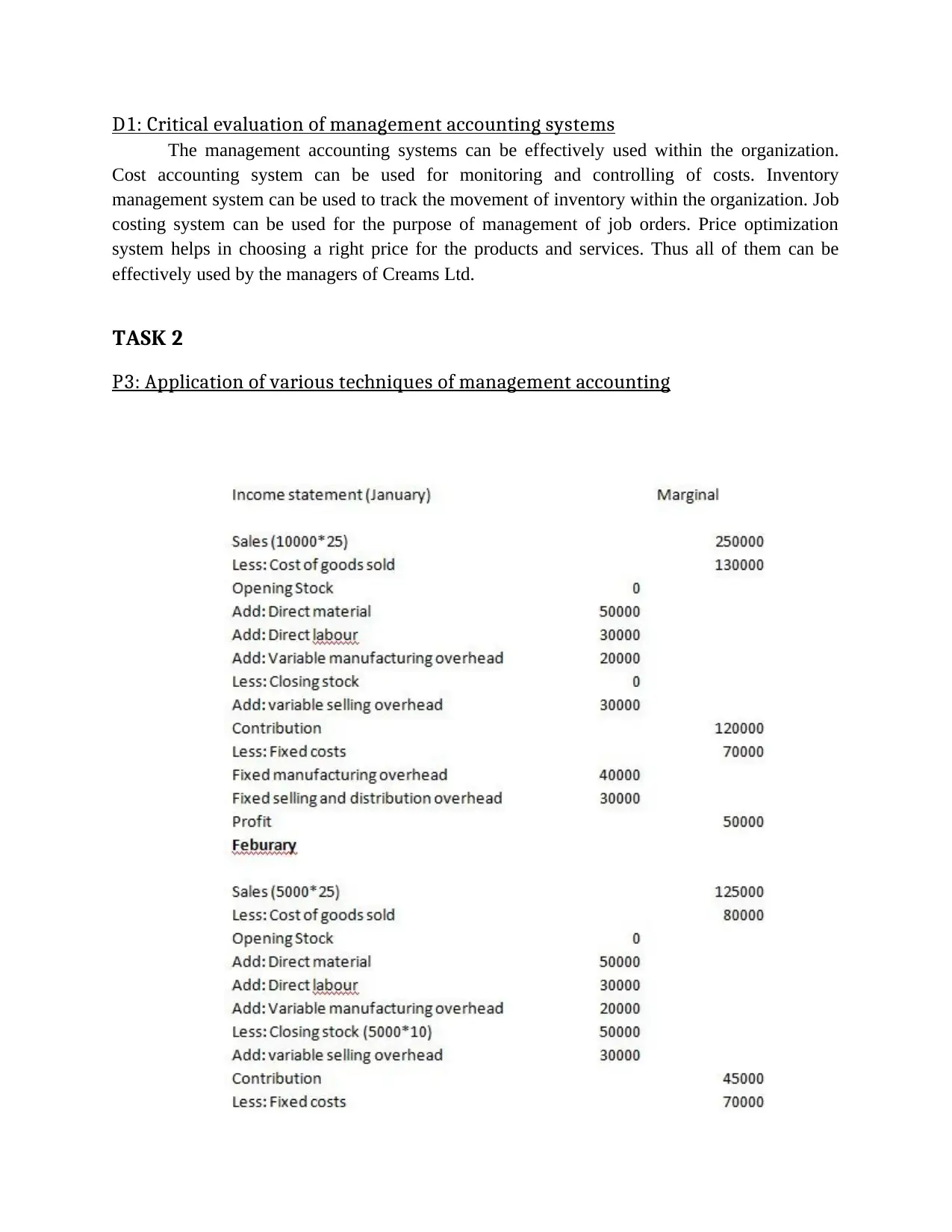

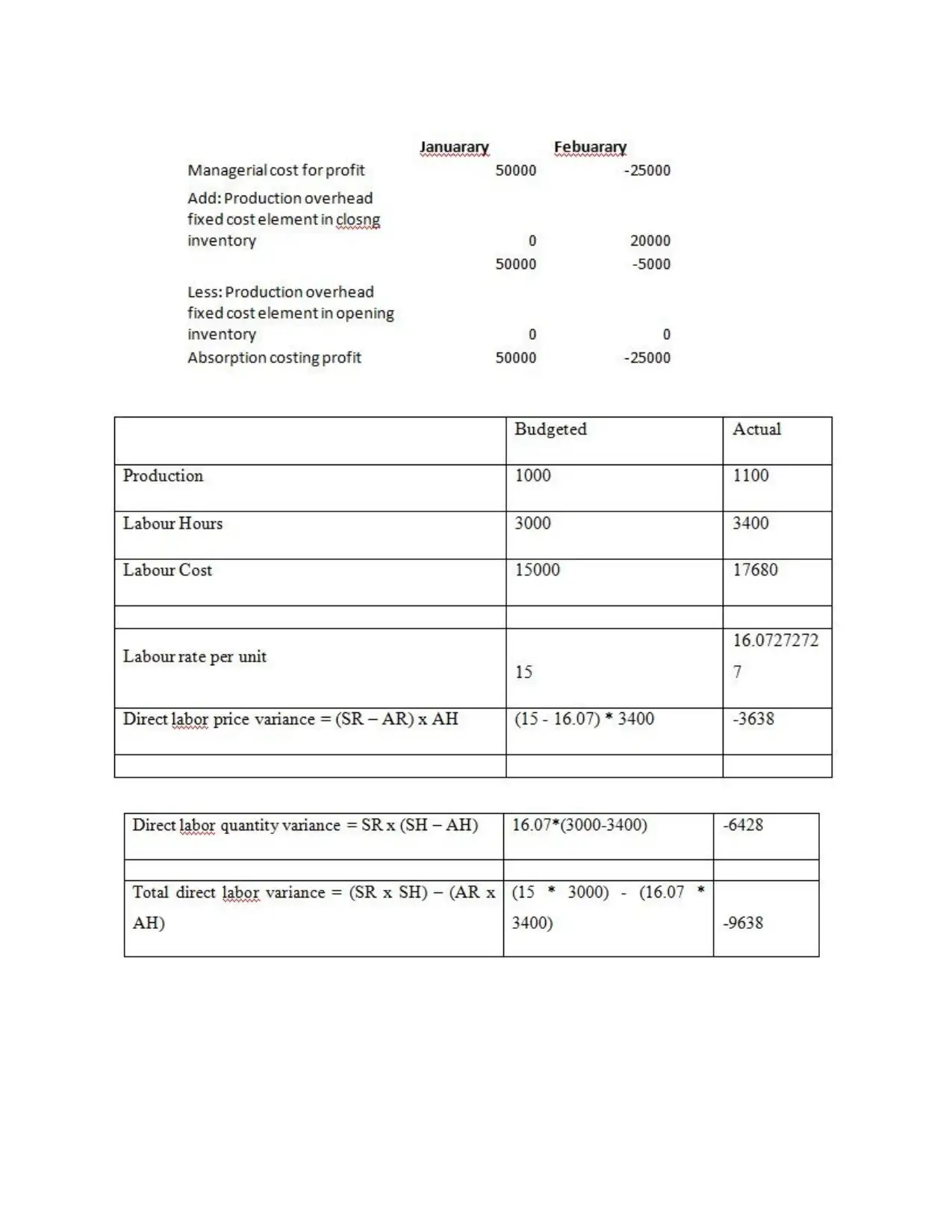

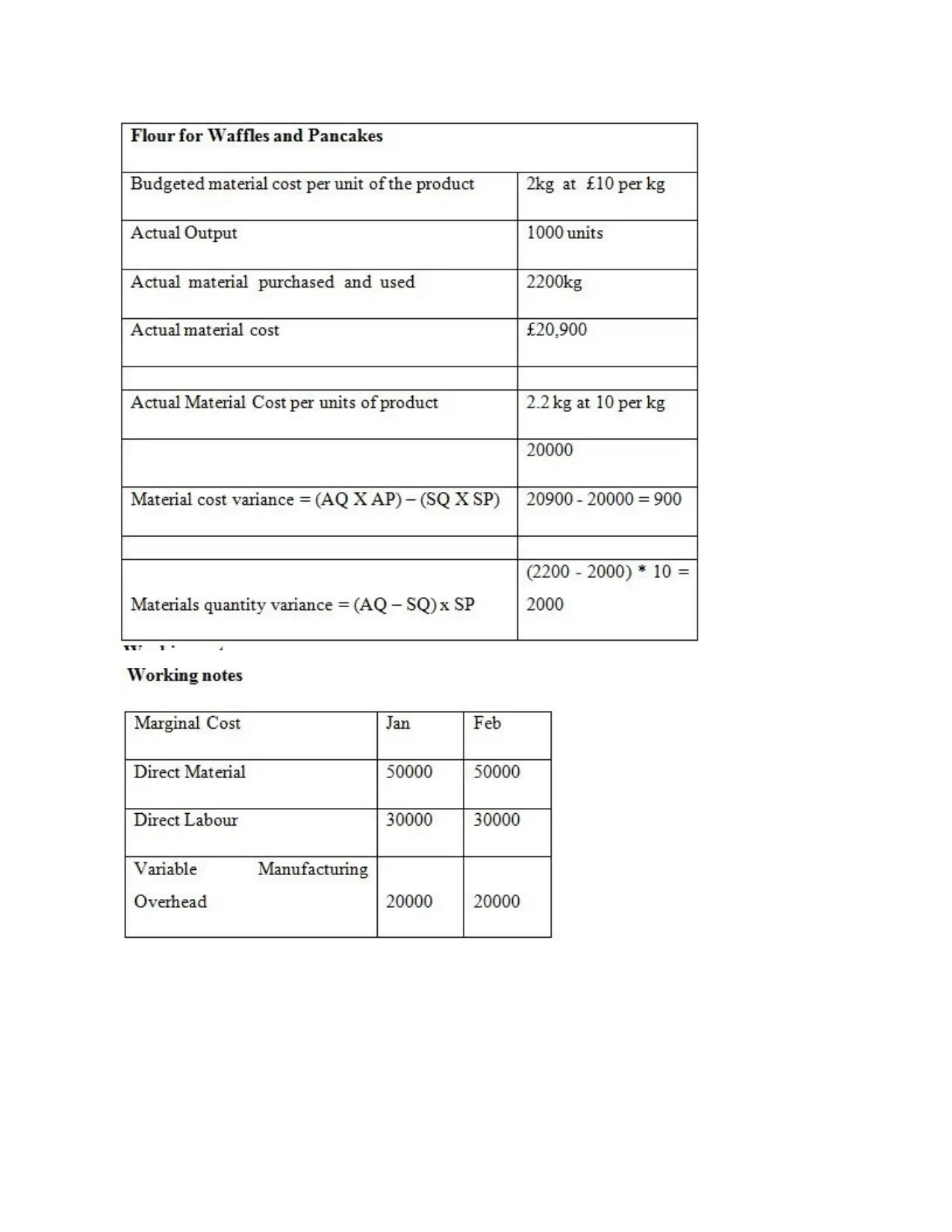

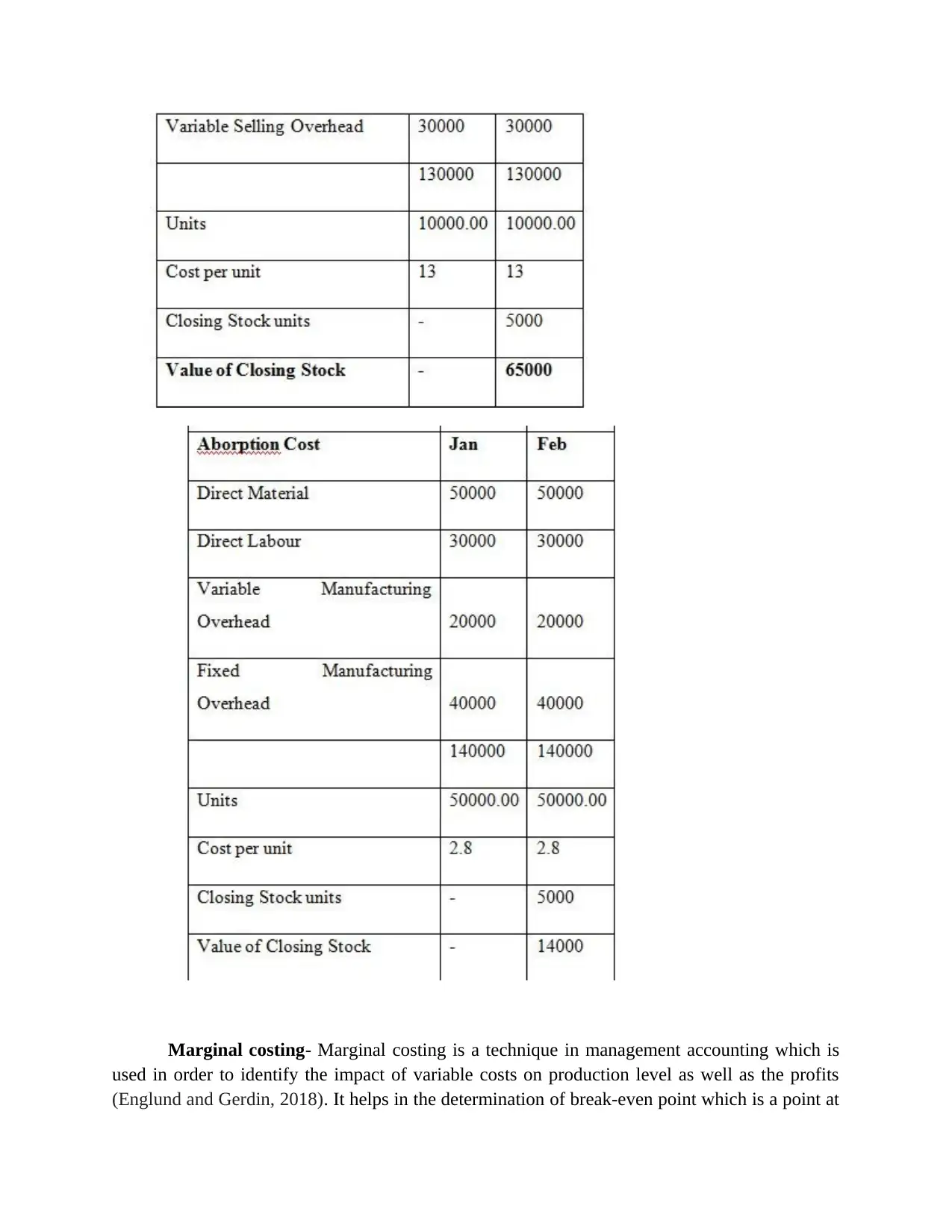

Marginal costing- Marginal costing is a technique in management accounting which is

used in order to identify the impact of variable costs on production level as well as the profits

(Englund and Gerdin, 2018). It helps in the determination of break-even point which is a point at

used in order to identify the impact of variable costs on production level as well as the profits

(Englund and Gerdin, 2018). It helps in the determination of break-even point which is a point at

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which a company neither earns profits nor incurs loss. The management of Creams Ltd. has

made use of this technique in its calculations as stated above.

Advantages-

Marginal costing is quite effective in controlling of various costs within the organization.

Thus by controlling the costs the profits of the enterprise can be easily maximized.

Therefore in this manner this technique is highly useful for the management of any

organization.

Marginal costing is quite helpful in maximizing the outputs of the production process and

enhances the companies to make use of their full capacity. Therefore, in this manner this

technique is quite helpful for the managers of an organization. It can help in maximizing

the overall level of profits which leads to strategic advantage over competitors.

Disadvantages-

Marginal costing fixed overheads in a separate category which is disadvantageous for an

organization. This is so because their controllability is reduced. This can create problems

as this will lead to increase in the overheads of the company.

Marginal costing technique is not as effective as standard costing and budgetary control

in controlling of costs. Thus it many not result in as effective outcomes in controlling of

costs as compared to standard costing and budgetary control.

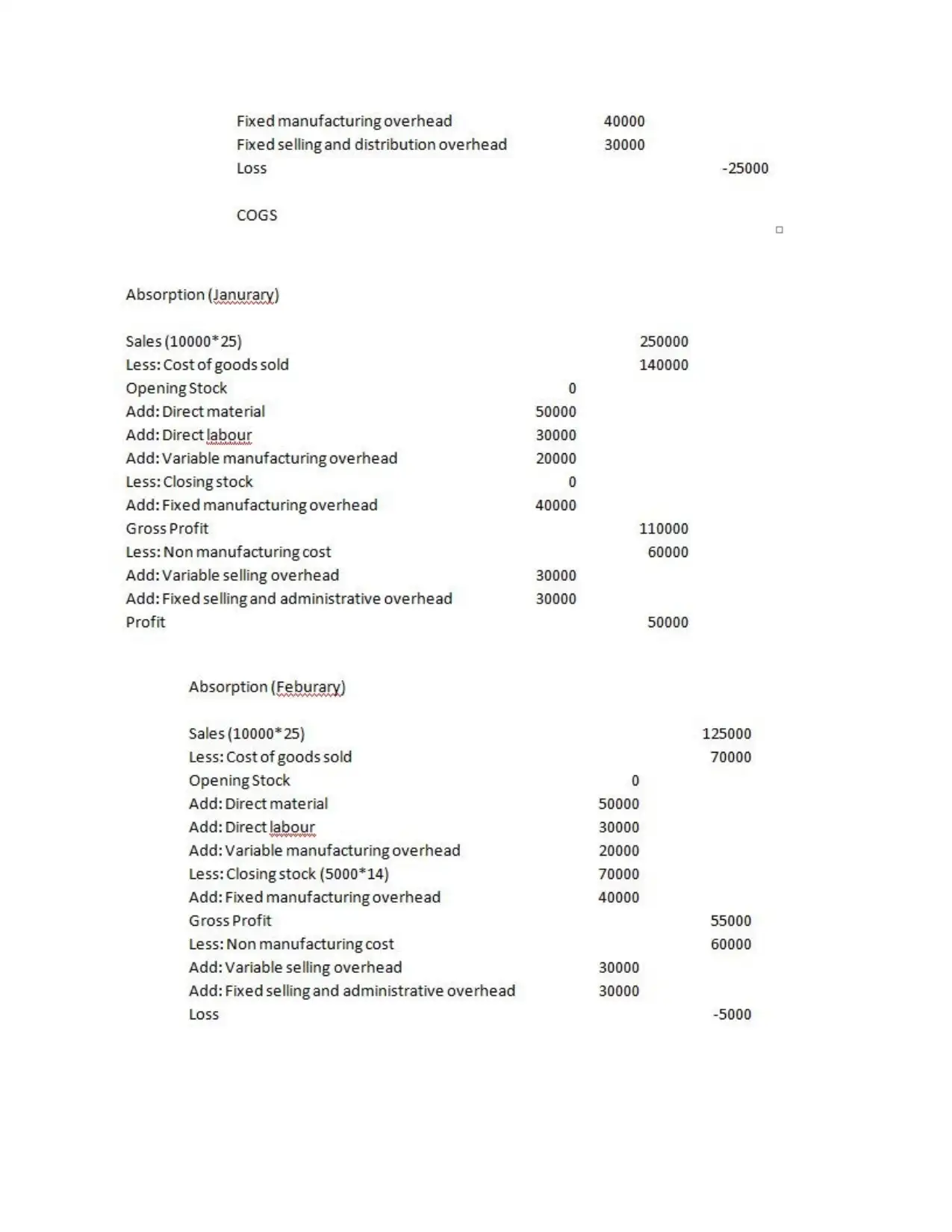

Absorption costing- Absorption costing is a technique which is used in

management accounting which leads to calculation of the overall costs being incurred

within an organization (Ghasemi and et.al., 2016). This leads to absorption of different

overheads which are incurring within a company. The managers of Creams Ltd. have

made use of this technique which has led to absorption of different overheads of the

company.

Advantages-

Absorption costing takes into account all the costs which are related with the production

unlike marginal costing. Thus it becomes quite advantageous for the organization.

Absorption costing helps in absorption of different overheads within an organization.

This helps a lot in determination of the exact level of profitability within the organization.

Disadvantages-

Absorption costing can skew the profitability level of a company and thus is not very

useful if the management has to perform a detailed analysis on the level of profits of the

company.

Absorption costing does not help in comparison purposes. Thus it can be quite

disadvantageous for an enterprise if the managers have to compare the data of the current

made use of this technique in its calculations as stated above.

Advantages-

Marginal costing is quite effective in controlling of various costs within the organization.

Thus by controlling the costs the profits of the enterprise can be easily maximized.

Therefore in this manner this technique is highly useful for the management of any

organization.

Marginal costing is quite helpful in maximizing the outputs of the production process and

enhances the companies to make use of their full capacity. Therefore, in this manner this

technique is quite helpful for the managers of an organization. It can help in maximizing

the overall level of profits which leads to strategic advantage over competitors.

Disadvantages-

Marginal costing fixed overheads in a separate category which is disadvantageous for an

organization. This is so because their controllability is reduced. This can create problems

as this will lead to increase in the overheads of the company.

Marginal costing technique is not as effective as standard costing and budgetary control

in controlling of costs. Thus it many not result in as effective outcomes in controlling of

costs as compared to standard costing and budgetary control.

Absorption costing- Absorption costing is a technique which is used in

management accounting which leads to calculation of the overall costs being incurred

within an organization (Ghasemi and et.al., 2016). This leads to absorption of different

overheads which are incurring within a company. The managers of Creams Ltd. have

made use of this technique which has led to absorption of different overheads of the

company.

Advantages-

Absorption costing takes into account all the costs which are related with the production

unlike marginal costing. Thus it becomes quite advantageous for the organization.

Absorption costing helps in absorption of different overheads within an organization.

This helps a lot in determination of the exact level of profitability within the organization.

Disadvantages-

Absorption costing can skew the profitability level of a company and thus is not very

useful if the management has to perform a detailed analysis on the level of profits of the

company.

Absorption costing does not help in comparison purposes. Thus it can be quite

disadvantageous for an enterprise if the managers have to compare the data of the current

year with the previous year for comparison. This will lead to creation of problems and

issues within the organization for the management.

Justification- Both the techniques of marginal costing and absorption costing can be

used by the management of the organization. The managers of Creams Ltd. have used

both of these techniques as stated above in the calculations. This has helped the

management of the company to take better decisions for the future.

M2: Accurate application of techniques

The techniques of marginal and absorption costing have been applied by the management

of Creams Ltd. in their calculations. These techniques have resulted in better calculation of level

of profits. Marginal costing has helped the company in finding out its break-even point.

Absorption costing has helped in absorbing the various overheads of the company. Thus by using

both of these techniques for calculation purposes the managers have made sure that they achieve

a higher level of efficiency, effectiveness and productivity within the different processes of the

organization. Also they hope to attain a distinct strategic advantage against the competitors to

facilitate better growth rate in the future.

D2: Producing of financial reports

Financial reports like Income statement, Balance Sheet etc. are quite helpful for any

organization. The managers of Creams Ltd. can make use of these financial reports to report

about what is happening in the business. It can be used for the satisfaction of various

stakeholders who are associated with the organization such as government, employees, suppliers

and customers. This will help the company in comparison of its performance with the previous

year to identify and deviations and variances. Also analysis of the financial strength of the

company can be easily prepared using these reports.

TASK 3

P4: Advantages and disadvantages of planning tools

Budgetary control is a process through which budgets are prepared within an organization

(Golyagina and Valuckas, 2016). Budgets are prepared to find out whether there are any

deviations and variances in the performance of the organization. It is a tool which can be

effectively used by the management of Creams Ltd. to plan for the future. The planning tools of

budgetary control which are used by its management are as follows-

Sales budget-

A sales budget is one of the most common budgets which are prepared within an

organization (Lapsley and Rekers, 2017). The management of Creams Ltd. makes use of this

issues within the organization for the management.

Justification- Both the techniques of marginal costing and absorption costing can be

used by the management of the organization. The managers of Creams Ltd. have used

both of these techniques as stated above in the calculations. This has helped the

management of the company to take better decisions for the future.

M2: Accurate application of techniques

The techniques of marginal and absorption costing have been applied by the management

of Creams Ltd. in their calculations. These techniques have resulted in better calculation of level

of profits. Marginal costing has helped the company in finding out its break-even point.

Absorption costing has helped in absorbing the various overheads of the company. Thus by using

both of these techniques for calculation purposes the managers have made sure that they achieve

a higher level of efficiency, effectiveness and productivity within the different processes of the

organization. Also they hope to attain a distinct strategic advantage against the competitors to

facilitate better growth rate in the future.

D2: Producing of financial reports

Financial reports like Income statement, Balance Sheet etc. are quite helpful for any

organization. The managers of Creams Ltd. can make use of these financial reports to report

about what is happening in the business. It can be used for the satisfaction of various

stakeholders who are associated with the organization such as government, employees, suppliers

and customers. This will help the company in comparison of its performance with the previous

year to identify and deviations and variances. Also analysis of the financial strength of the

company can be easily prepared using these reports.

TASK 3

P4: Advantages and disadvantages of planning tools

Budgetary control is a process through which budgets are prepared within an organization

(Golyagina and Valuckas, 2016). Budgets are prepared to find out whether there are any

deviations and variances in the performance of the organization. It is a tool which can be

effectively used by the management of Creams Ltd. to plan for the future. The planning tools of

budgetary control which are used by its management are as follows-

Sales budget-

A sales budget is one of the most common budgets which are prepared within an

organization (Lapsley and Rekers, 2017). The management of Creams Ltd. makes use of this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.