Management Accounting Systems, Costing, and Budgetary Control Report

VerifiedAdded on 2023/01/12

|17

|4360

|47

Report

AI Summary

This report examines management accounting principles and their application within Cream Limited, a UK-based food company. It begins by defining management accounting and exploring various systems like inventory management, job order costing, price optimization, and cost accounting. The report then delves into reporting methods such as account receivable, inventory management, performance, and budget reports. A significant portion is dedicated to cost analysis, including calculations using marginal and absorption costing methods, alongside variance analysis. The report further explains budgetary control, planning tools, and their respective advantages and disadvantages. Finally, it compares organizations based on their use of management accounting to address financial issues, culminating in a conclusion and references.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explanation of different types of systems of management accounting along with their

essential requirements..................................................................................................................1

P2 Explanation of various methods that are used for reporting of management accounting......3

TASK 2............................................................................................................................................4

P3 Calculation of costs using cost analysis techniques and formulating of income statement

under absorption and marginal costing........................................................................................4

TASK 3..........................................................................................................................................10

P4 Explanation of budgetary control along with description of planning tools and advantages

and disadvantages of all of them...............................................................................................10

TASK 4..........................................................................................................................................13

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues...........................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explanation of different types of systems of management accounting along with their

essential requirements..................................................................................................................1

P2 Explanation of various methods that are used for reporting of management accounting......3

TASK 2............................................................................................................................................4

P3 Calculation of costs using cost analysis techniques and formulating of income statement

under absorption and marginal costing........................................................................................4

TASK 3..........................................................................................................................................10

P4 Explanation of budgetary control along with description of planning tools and advantages

and disadvantages of all of them...............................................................................................10

TASK 4..........................................................................................................................................13

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues...........................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is a wider concept which is required to be understood by all the

managers so that they can improve performance of company in which they are working. It is a

technique which helps internal stakeholders to determine that the entity is performing

appropriately or not. All the information regarding business execution is recorded with the help

of it. In order to reach all the predetermined goals and objectives it is essential for all the

enterprises to make sure that they are paying attention towards it (Christ and Burritt, 2017).

Maim aim of this report is to understand concept of management accounting and its use within

the organization to carry out operations systematically. This project is based upon Cream

Limited which is one of the medium sized companies of United Kingdom. The entity is selling

different types of food items in the market. Some of them are waffles, ice creams and doughnuts.

This assignment covers various topics such as understanding of management accounting, its

systems and reports, application of various cost analysis techniques to formulate income

statement of the organization. Apart from this, various types of planning tools that are used in

budgetary control and comparison of organizations on the basis of use of management

accounting are also covered in this report.

TASK 1

P1 Explanation of different types of systems of management accounting along with their

essential requirements

In all the organisations a specific technique is used by the managers for the purpose of

analysing that the efforts that are made by them to enhance performance of business are resulting

positively or negatively. It is known as management accounting which helps all the internal

stakeholders to analyse performance of the company (Cooper, Ezzamel and Qu, 2017). In Cream

Limited management accounting is used to assist the board of directors to analyse actual progress

of the entity. With the help of it, employees also determine that the organisation in which they

are working will provide them growth in future or not. While planning to achieve all the long-

term business goals it is very important for the managers to make sure that they are using it as it

will guide them to monitor and control the performance of business.

Most of the business entities are using different types of management accounting systems

to make sure that the planned activities are performed in systematic manner or not. In order to

1

Management accounting is a wider concept which is required to be understood by all the

managers so that they can improve performance of company in which they are working. It is a

technique which helps internal stakeholders to determine that the entity is performing

appropriately or not. All the information regarding business execution is recorded with the help

of it. In order to reach all the predetermined goals and objectives it is essential for all the

enterprises to make sure that they are paying attention towards it (Christ and Burritt, 2017).

Maim aim of this report is to understand concept of management accounting and its use within

the organization to carry out operations systematically. This project is based upon Cream

Limited which is one of the medium sized companies of United Kingdom. The entity is selling

different types of food items in the market. Some of them are waffles, ice creams and doughnuts.

This assignment covers various topics such as understanding of management accounting, its

systems and reports, application of various cost analysis techniques to formulate income

statement of the organization. Apart from this, various types of planning tools that are used in

budgetary control and comparison of organizations on the basis of use of management

accounting are also covered in this report.

TASK 1

P1 Explanation of different types of systems of management accounting along with their

essential requirements

In all the organisations a specific technique is used by the managers for the purpose of

analysing that the efforts that are made by them to enhance performance of business are resulting

positively or negatively. It is known as management accounting which helps all the internal

stakeholders to analyse performance of the company (Cooper, Ezzamel and Qu, 2017). In Cream

Limited management accounting is used to assist the board of directors to analyse actual progress

of the entity. With the help of it, employees also determine that the organisation in which they

are working will provide them growth in future or not. While planning to achieve all the long-

term business goals it is very important for the managers to make sure that they are using it as it

will guide them to monitor and control the performance of business.

Most of the business entities are using different types of management accounting systems

to make sure that the planned activities are performed in systematic manner or not. In order to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

conduct all the operations properly it is essential for managers to use different types of systems.

Management in Cream Limited are paying attention towards various types of them such as cost

accounting, price optimisation, inventory management and job order costing (Granlund and

Lukka, 2017). With the help of all of them internal records are generated by managers to analyse

actual performance of organisations. All of them are described below in detail in context of

Cream Limited:

Inventory management system: In most of the companies it is used by managers to

keep detailed information of all the items that are used by them to produce products which are

sold to clients. In Creams Limited it is implemented to make sure that all the items that are

required by customers are made according to their choices by keeping all the ingredients. It helps

managers to make sure that they are having all the goods to make ice creams, waffles, doughnuts

etc. according to requirement of consumers. There are various types of inventory management

systems which could be used by the organisation to manage goods. Description of all of them is

as follows:

AVCO (Average Cost Method): In this method of inventory management all the goods

are used or production by taking average cost as a basis (Hall, 2016).

FIFO (First in First Out): While using FIFO all the entities use previously undertaken

stocks for performing operational activities.

LIFO (Last in First Out): Under this method of inventory management system newly

bought items are used for manufacturing products.

From all the above described methods of inventory management systems FIFO is used in

Creams Limited so that the managers can utilise all the ingredients properly before they

become expired.

Essential requirements: It is very important for the organisation because it helps to perform

all the operations properly by managing the goods in systematic manner. It also helps to make

sure that all the ingredients are kept by the entity to meet requirements of customers (Hopper and

Bui, 2016).

Job order costing system: It is one of the main systems which is used in all the

companies that are performing different types of activities. Main purpose of it is to record

information of all the operations separately. In Creams Limited it is used to record requirements

of all the customers distinctly so that all their demand could be made. With the help of it,

2

Management in Cream Limited are paying attention towards various types of them such as cost

accounting, price optimisation, inventory management and job order costing (Granlund and

Lukka, 2017). With the help of all of them internal records are generated by managers to analyse

actual performance of organisations. All of them are described below in detail in context of

Cream Limited:

Inventory management system: In most of the companies it is used by managers to

keep detailed information of all the items that are used by them to produce products which are

sold to clients. In Creams Limited it is implemented to make sure that all the items that are

required by customers are made according to their choices by keeping all the ingredients. It helps

managers to make sure that they are having all the goods to make ice creams, waffles, doughnuts

etc. according to requirement of consumers. There are various types of inventory management

systems which could be used by the organisation to manage goods. Description of all of them is

as follows:

AVCO (Average Cost Method): In this method of inventory management all the goods

are used or production by taking average cost as a basis (Hall, 2016).

FIFO (First in First Out): While using FIFO all the entities use previously undertaken

stocks for performing operational activities.

LIFO (Last in First Out): Under this method of inventory management system newly

bought items are used for manufacturing products.

From all the above described methods of inventory management systems FIFO is used in

Creams Limited so that the managers can utilise all the ingredients properly before they

become expired.

Essential requirements: It is very important for the organisation because it helps to perform

all the operations properly by managing the goods in systematic manner. It also helps to make

sure that all the ingredients are kept by the entity to meet requirements of customers (Hopper and

Bui, 2016).

Job order costing system: It is one of the main systems which is used in all the

companies that are performing different types of activities. Main purpose of it is to record

information of all the operations separately. In Creams Limited it is used to record requirements

of all the customers distinctly so that all their demand could be made. With the help of it,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation meet its long-term goals such as higher satisfaction level of clients. It guides the

managers to make sure that they are able to perform all the activities according to specification

of consumers.

Essential requirements: Job order costing system is very important for Creams Limited

because with the help of it all the expectations of clients could be met properly. Apart from this,

it will be also beneficial to achieve business goals such as higher profits and highly satisfied

consumers (Hirsch, Seubert, and Sohn, 2015).

Price optimisation system: This management accounting system is mainly focused with

setting right price for all the items that are sold by an organisation. Managers of Creams Limited

are using it to analyse that the price which is set by them for all their products are able to attract

large number of customers. It is beneficial for the organisation to determine responses of

consumers upon the prices that are decided by them to set for all the stuff that are sold by it to

them.

Essential requirements: It is required by Creams Limited because by using it the

managers will be able to enhance sales by setting right price for all the items that are sold by it.

This system can also help the enterprise to analyse that it will be able to meet all its goals by

deciding right rates for all the items that are sold by it.

Cost accounting system: It is the last management accounting system which is mainly

used for the purpose of analysing cost of each and every activity which is performed by an

organisation to meet all its business objectives (Järvenpää and Länsiluoto, 2016). In Creams

Limited it is used by managers to analyse all the expenses that are required to be met by it to

achieve all the predetermined goals. By using it the management get aware of all the costs that

are taking place which executing operations.

Essential requirements: Cost accounting system is vital to be used by Creams Limited as

it can help the managers to determine actual cost of all the operations that are performed by it.

P2 Explanation of various methods that are used for reporting of management accounting

In most of the entities specific procedure is followed to generate internal records and reports

which is known as management accounting reporting (Kaplan and Atkinson, 2015). In order to

determine that organisation performing favourably or adversely it is required to be focused. In

Creams Limited it is also taken in to consideration by the managers to make sure that they meet

3

managers to make sure that they are able to perform all the activities according to specification

of consumers.

Essential requirements: Job order costing system is very important for Creams Limited

because with the help of it all the expectations of clients could be met properly. Apart from this,

it will be also beneficial to achieve business goals such as higher profits and highly satisfied

consumers (Hirsch, Seubert, and Sohn, 2015).

Price optimisation system: This management accounting system is mainly focused with

setting right price for all the items that are sold by an organisation. Managers of Creams Limited

are using it to analyse that the price which is set by them for all their products are able to attract

large number of customers. It is beneficial for the organisation to determine responses of

consumers upon the prices that are decided by them to set for all the stuff that are sold by it to

them.

Essential requirements: It is required by Creams Limited because by using it the

managers will be able to enhance sales by setting right price for all the items that are sold by it.

This system can also help the enterprise to analyse that it will be able to meet all its goals by

deciding right rates for all the items that are sold by it.

Cost accounting system: It is the last management accounting system which is mainly

used for the purpose of analysing cost of each and every activity which is performed by an

organisation to meet all its business objectives (Järvenpää and Länsiluoto, 2016). In Creams

Limited it is used by managers to analyse all the expenses that are required to be met by it to

achieve all the predetermined goals. By using it the management get aware of all the costs that

are taking place which executing operations.

Essential requirements: Cost accounting system is vital to be used by Creams Limited as

it can help the managers to determine actual cost of all the operations that are performed by it.

P2 Explanation of various methods that are used for reporting of management accounting

In most of the entities specific procedure is followed to generate internal records and reports

which is known as management accounting reporting (Kaplan and Atkinson, 2015). In order to

determine that organisation performing favourably or adversely it is required to be focused. In

Creams Limited it is also taken in to consideration by the managers to make sure that they meet

3

all the business objectives. There are various methods that are used for reporting management

accounting information. All of them are described below:

Account receivable report: It is mainly related to the record of the details of such clients

who will make payment in future and bought goods on credit. In Creams Limited it is used by

management to keep detailed information of owed amount which will be recovered from the

customers in future on a due date. It is beneficial for the entity because it can help to analyse

actual outstanding that will be received in future (Maas, Schaltegger and Crutzen, 2016).

Inventory management report: It is related to the recording information of all the

goods that are used by an organisation to perform all the operational activities. In Creams

Limited this report is created by managers to analyse that they are having sufficient ingredients

to offer different items to the customers according to their requirements. It is advantageous for

the entity as it can help to order goods on time so that possibility of unsatisfied clients could be

ignored.

Performance report: In most of the companies this report is generated for the purpose of

analysing actual performance of whole entity and the employees who are working within it.

Manager of Creams Limited are also formulating it so that they can analyse the progress of entity

and determine that staff members are making appropriate efforts to contribute in growth of

business. It is beneficial for the organisation because it can help the management to allow

bonuses and compensation to all the employees according to their performance (Malina, 2017).

Budget report: It is mainly related to the records that are made by organisations to

allocate funding to all the divisions according to their requirements so that they can perform all

their operations. Creams Limited is also using this report to make sure that all the planned

activities are performed in the specific budget which was decided for them previously. It is

beneficial for the entity as with the help of it appropriate funding could be assigned to the

departments so that they are perform all their duties.

TASK 2

P3 Calculation of costs using cost analysis techniques and formulating of income statement

under absorption and marginal costing

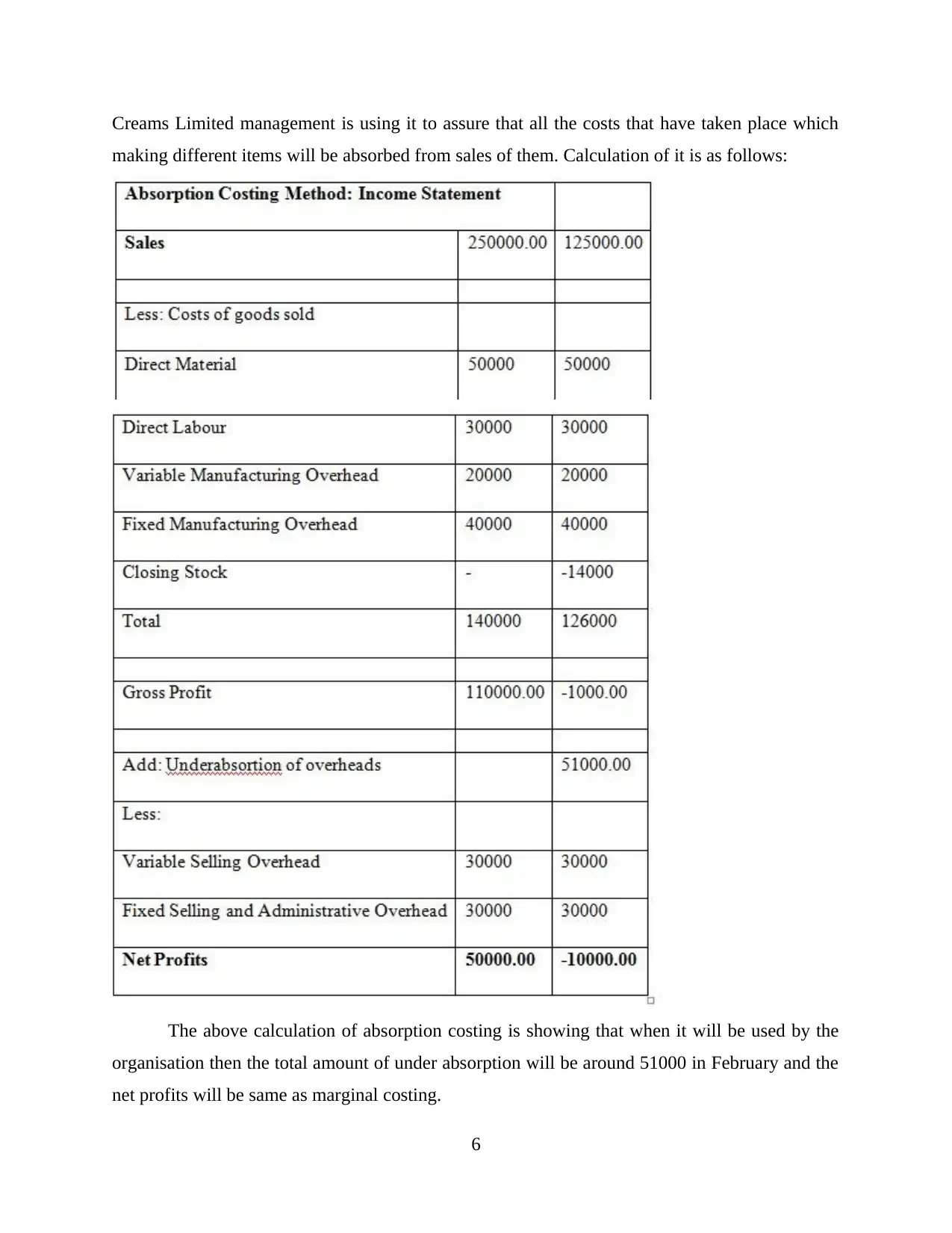

Marginal costing: It can be defined as a costing technique which is used by companies to

determine cost of each and every additional unit which is made by the organisation along with

4

accounting information. All of them are described below:

Account receivable report: It is mainly related to the record of the details of such clients

who will make payment in future and bought goods on credit. In Creams Limited it is used by

management to keep detailed information of owed amount which will be recovered from the

customers in future on a due date. It is beneficial for the entity because it can help to analyse

actual outstanding that will be received in future (Maas, Schaltegger and Crutzen, 2016).

Inventory management report: It is related to the recording information of all the

goods that are used by an organisation to perform all the operational activities. In Creams

Limited this report is created by managers to analyse that they are having sufficient ingredients

to offer different items to the customers according to their requirements. It is advantageous for

the entity as it can help to order goods on time so that possibility of unsatisfied clients could be

ignored.

Performance report: In most of the companies this report is generated for the purpose of

analysing actual performance of whole entity and the employees who are working within it.

Manager of Creams Limited are also formulating it so that they can analyse the progress of entity

and determine that staff members are making appropriate efforts to contribute in growth of

business. It is beneficial for the organisation because it can help the management to allow

bonuses and compensation to all the employees according to their performance (Malina, 2017).

Budget report: It is mainly related to the records that are made by organisations to

allocate funding to all the divisions according to their requirements so that they can perform all

their operations. Creams Limited is also using this report to make sure that all the planned

activities are performed in the specific budget which was decided for them previously. It is

beneficial for the entity as with the help of it appropriate funding could be assigned to the

departments so that they are perform all their duties.

TASK 2

P3 Calculation of costs using cost analysis techniques and formulating of income statement

under absorption and marginal costing

Marginal costing: It can be defined as a costing technique which is used by companies to

determine cost of each and every additional unit which is made by the organisation along with

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the predetermined production units. In Creams Limited it is used by managers to analyse cost of

all the additional items that are made by it according to the requirements of customers (Malmi,

2016). All the calculation of it are as follows:

From the above calculations it has been determined that while calculating profits from

marginal costing the entity will generate profits of 50000 for January month and loss of 10000

for February month.

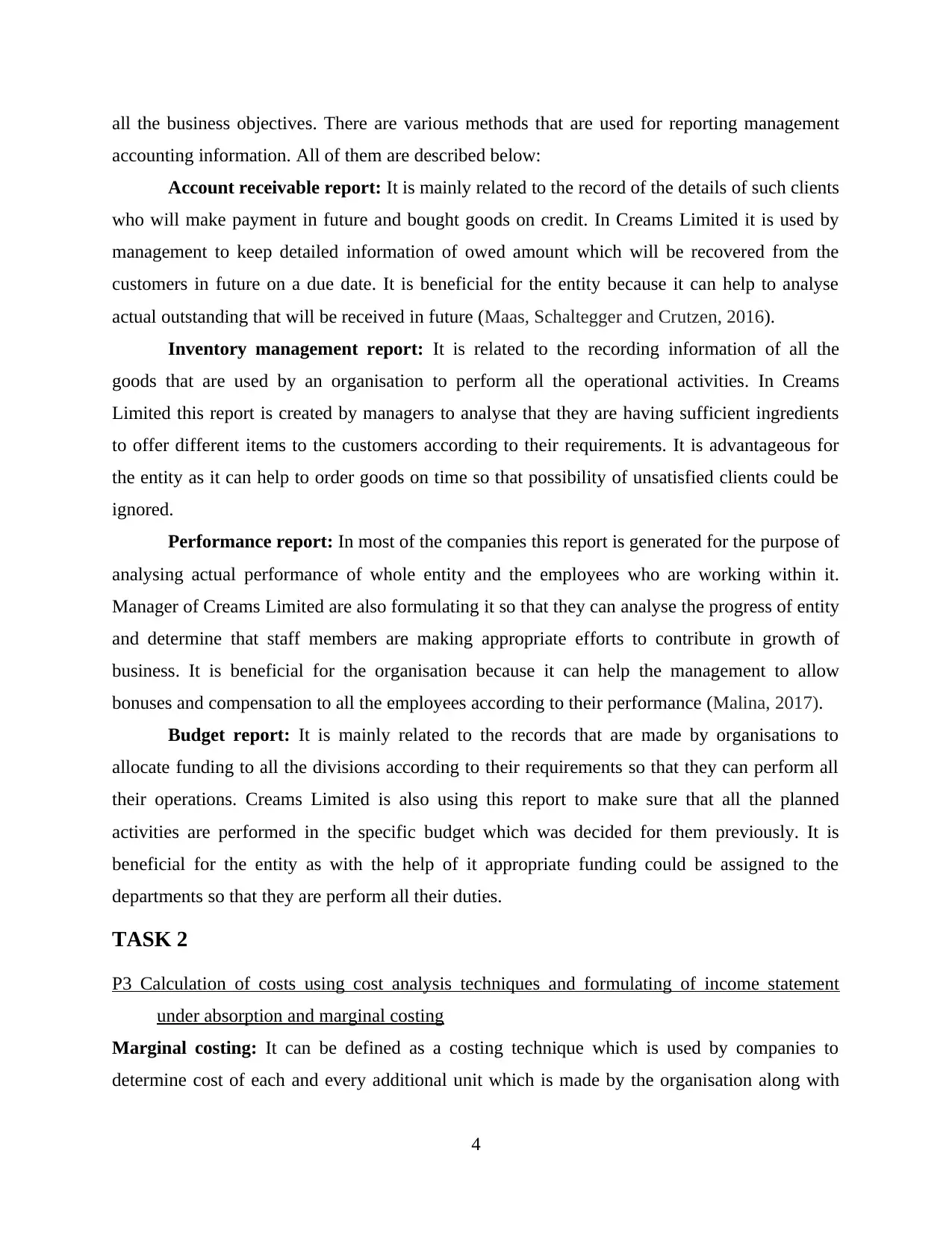

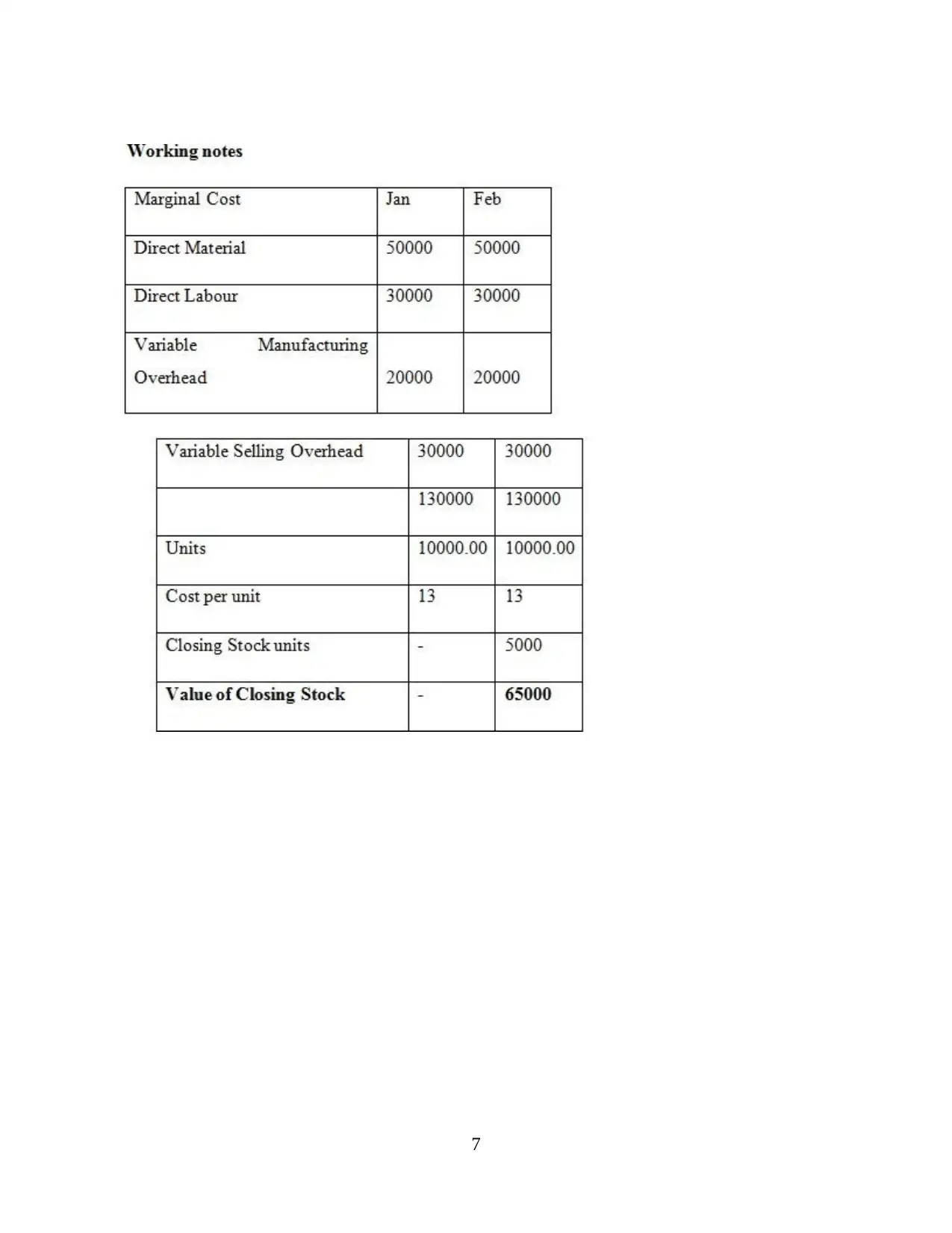

Absorption costing: This costing technique is mainly related to the absorption of cost of

all the produced items from the revenues that are generated by selling them (Messner, 2016). In

5

all the additional items that are made by it according to the requirements of customers (Malmi,

2016). All the calculation of it are as follows:

From the above calculations it has been determined that while calculating profits from

marginal costing the entity will generate profits of 50000 for January month and loss of 10000

for February month.

Absorption costing: This costing technique is mainly related to the absorption of cost of

all the produced items from the revenues that are generated by selling them (Messner, 2016). In

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Creams Limited management is using it to assure that all the costs that have taken place which

making different items will be absorbed from sales of them. Calculation of it is as follows:

The above calculation of absorption costing is showing that when it will be used by the

organisation then the total amount of under absorption will be around 51000 in February and the

net profits will be same as marginal costing.

6

making different items will be absorbed from sales of them. Calculation of it is as follows:

The above calculation of absorption costing is showing that when it will be used by the

organisation then the total amount of under absorption will be around 51000 in February and the

net profits will be same as marginal costing.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

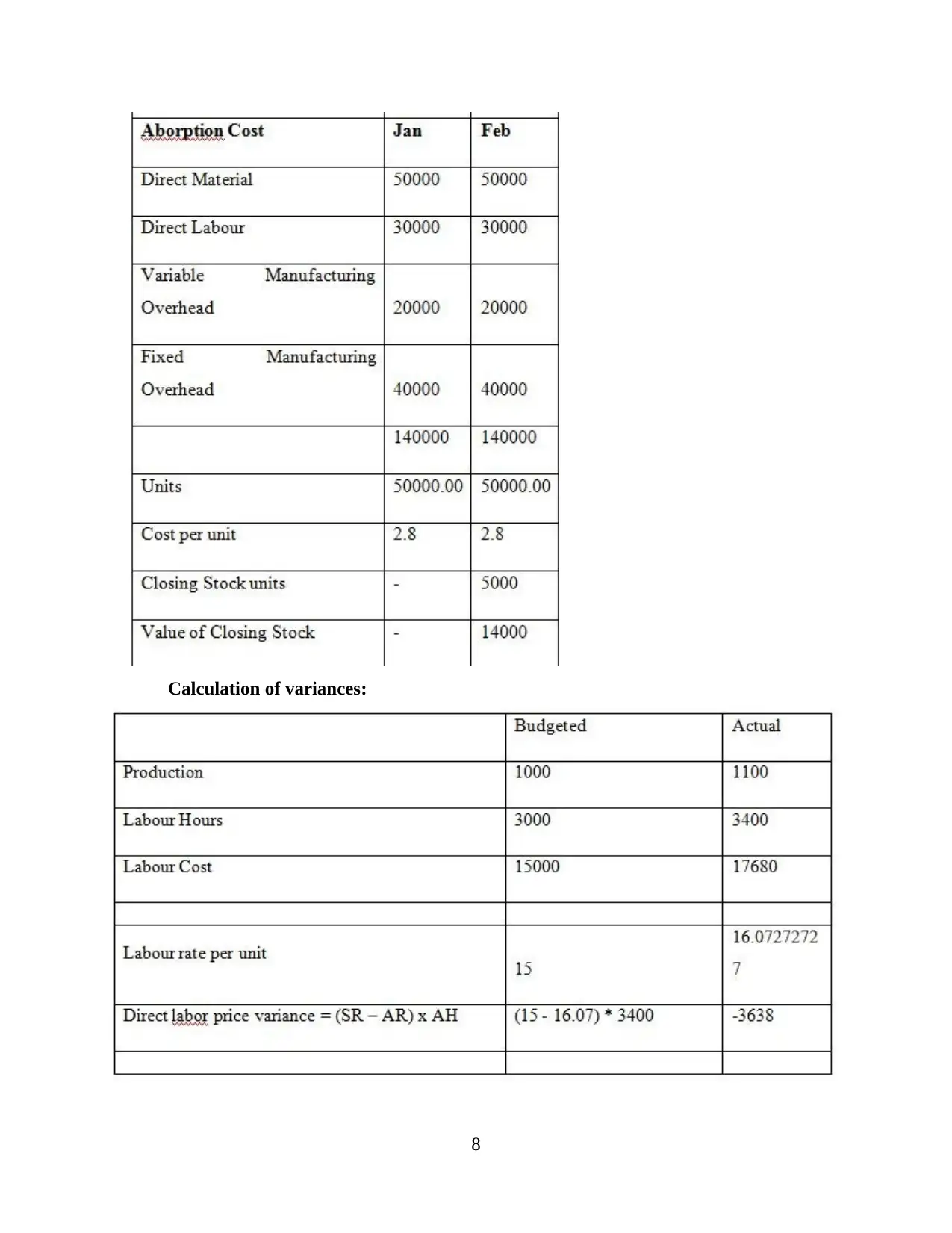

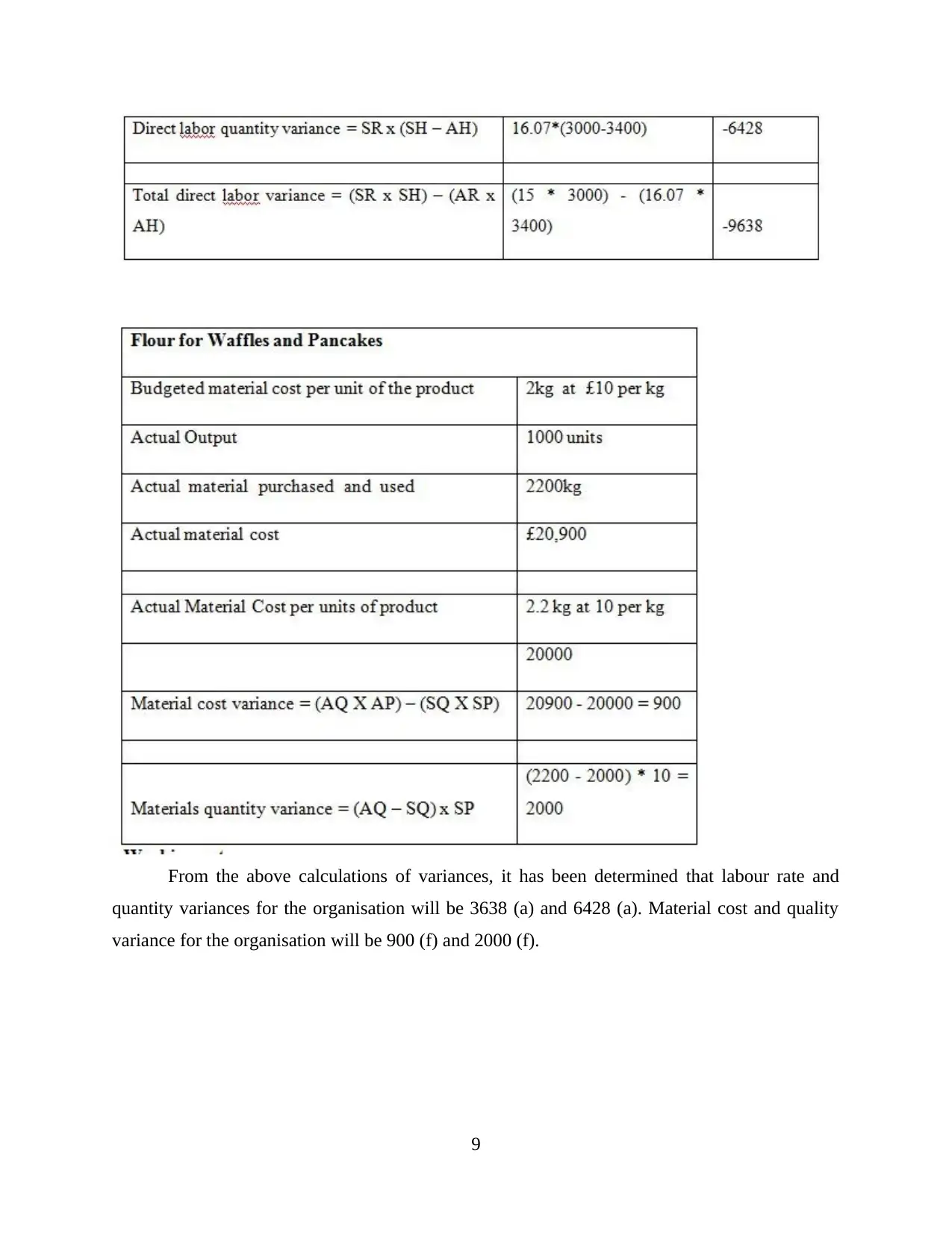

Calculation of variances:

8

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above calculations of variances, it has been determined that labour rate and

quantity variances for the organisation will be 3638 (a) and 6428 (a). Material cost and quality

variance for the organisation will be 900 (f) and 2000 (f).

9

quantity variances for the organisation will be 3638 (a) and 6428 (a). Material cost and quality

variance for the organisation will be 900 (f) and 2000 (f).

9

TASK 3

P4 Explanation of budgetary control along with description of planning tools and advantages and

disadvantages of all of them

Budgetary control is referred as the process through which organizations prepare budget

for future and compare that budget from actual performance in order to find out the variances, if

any exist. By comparing the budgeted figures with actual ones, the management of an

organisation enable to find out variances and accordingly take corrective actions immediately

without any delay (Nitzl, 2016). It is the mechanism through which senior managers of Creams

Limited make sure that the spending limits are appropriate. This control is crucial as spending

excesses have an adverse influence on corporate profits. Budgetary control is used as a system in

organisation to control cost that includes development of budget, coordinating different

departments and establishing responsibilities and duties, comparison of performance with

budgeted and act upon outcomes to accomplish the maximum beneficial or profitable.

The main objective of using budgetary control in Creams Limited is that it is an effective

system that plays vital role in success of business entity. This helps in improving efficiency and

effectiveness of company. In planning and controlling, budgeting plays crucial role as it supports

in directing the resources which are restricted in quantity to the most productive utilization and

therefore, ensure efficiency within firm. An effective budgetary control system facilitates in

planning different activities and make sure smooth and systematic working in organisation. It

also combines the ideas of different management levels in preparation of budget as well as

facilitate coordination among various departments (Otley, 2016). As budgetary control system is

an effective means of planning, thus make sure enough availability of working capital as well as

other resources within firm.

There are some conditions required for good budgetary control system. These conditions

include support from upper level management, creation of responsibility center, quantification of

goal of an organisation, realistic targets, state of organizational goals, participation of employees,

coverage of all areas of organisation, good accounting system etc. In budgetary control within

Creams Limited, different types of planning tools are required (Quattrone, 2016). Some of the

planning tools are mentioned below along with their advantages and disadvantages:

Cost budget: It is defined as a financial plan regarding identified expenses of company for

the next period. It details all the expenses related to activities and operations of business. It is the

10

P4 Explanation of budgetary control along with description of planning tools and advantages and

disadvantages of all of them

Budgetary control is referred as the process through which organizations prepare budget

for future and compare that budget from actual performance in order to find out the variances, if

any exist. By comparing the budgeted figures with actual ones, the management of an

organisation enable to find out variances and accordingly take corrective actions immediately

without any delay (Nitzl, 2016). It is the mechanism through which senior managers of Creams

Limited make sure that the spending limits are appropriate. This control is crucial as spending

excesses have an adverse influence on corporate profits. Budgetary control is used as a system in

organisation to control cost that includes development of budget, coordinating different

departments and establishing responsibilities and duties, comparison of performance with

budgeted and act upon outcomes to accomplish the maximum beneficial or profitable.

The main objective of using budgetary control in Creams Limited is that it is an effective

system that plays vital role in success of business entity. This helps in improving efficiency and

effectiveness of company. In planning and controlling, budgeting plays crucial role as it supports

in directing the resources which are restricted in quantity to the most productive utilization and

therefore, ensure efficiency within firm. An effective budgetary control system facilitates in

planning different activities and make sure smooth and systematic working in organisation. It

also combines the ideas of different management levels in preparation of budget as well as

facilitate coordination among various departments (Otley, 2016). As budgetary control system is

an effective means of planning, thus make sure enough availability of working capital as well as

other resources within firm.

There are some conditions required for good budgetary control system. These conditions

include support from upper level management, creation of responsibility center, quantification of

goal of an organisation, realistic targets, state of organizational goals, participation of employees,

coverage of all areas of organisation, good accounting system etc. In budgetary control within

Creams Limited, different types of planning tools are required (Quattrone, 2016). Some of the

planning tools are mentioned below along with their advantages and disadvantages:

Cost budget: It is defined as a financial plan regarding identified expenses of company for

the next period. It details all the expenses related to activities and operations of business. It is the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.