Management Accounting Report: Costing, Planning and Financial Problems

VerifiedAdded on 2023/01/04

|22

|5399

|36

Report

AI Summary

This report analyzes management accounting principles and their application within Capital Joinery Limited. It begins by defining managerial accounting and explores different management accounting systems, including cost accounting, price optimization, inventory management, and job costing. The report then examines various management accounting reports, such as performance, cost, and budget reports. It delves into absorption and marginal costing methods, highlighting their calculation and application. Furthermore, the report discusses the advantages and disadvantages of planning tools, emphasizing their importance in business decision-making. Finally, it investigates how management accounting systems can be used to respond to financial problems, evaluating the effectiveness of planning tools in resolving these issues and analyzing how management accounting tools contribute to organizational success. The report concludes with a summary of the findings and provides references to support the analysis.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explanation of managerial accounting and requirements of different types of management

accounting system. ......................................................................................................................1

P2 Different methods used by organization for prepare management accounting reports..........3

M1 Benefits of management accounting system.........................................................................4

Essential requirements of managerial accounting system...........................................................4

D1 Integration of management accounting reports with its systems...........................................5

TASK 2............................................................................................................................................5

P3 Calculation of absorption and marginal costing.....................................................................5

M2 Accurate applies range of management accounting techniques............................................6

D1 Integration of management accounting reports with its systems...........................................7

TASK 3............................................................................................................................................7

P4 Explanation of advantage and disadvantages of planning tools.............................................7

M3 Importance of different planning tools..................................................................................9

TASK 4............................................................................................................................................9

P5 Use of management accounting system for responding financial problems..........................9

M4 Analysis of how management accounting tools useful in lead organization success.........11

D3 Evaluation of how planning tools respond for solving issue of financial problem..............11

CONCLUSION..............................................................................................................................11

REFRENCES.................................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explanation of managerial accounting and requirements of different types of management

accounting system. ......................................................................................................................1

P2 Different methods used by organization for prepare management accounting reports..........3

M1 Benefits of management accounting system.........................................................................4

Essential requirements of managerial accounting system...........................................................4

D1 Integration of management accounting reports with its systems...........................................5

TASK 2............................................................................................................................................5

P3 Calculation of absorption and marginal costing.....................................................................5

M2 Accurate applies range of management accounting techniques............................................6

D1 Integration of management accounting reports with its systems...........................................7

TASK 3............................................................................................................................................7

P4 Explanation of advantage and disadvantages of planning tools.............................................7

M3 Importance of different planning tools..................................................................................9

TASK 4............................................................................................................................................9

P5 Use of management accounting system for responding financial problems..........................9

M4 Analysis of how management accounting tools useful in lead organization success.........11

D3 Evaluation of how planning tools respond for solving issue of financial problem..............11

CONCLUSION..............................................................................................................................11

REFRENCES.................................................................................................................................12

INTRODUCTION

Management Accounting this term is formulated by two words management is the procedure

of analysing recording controlling organising and managing each and every business department

strategies on the other side accounting is the process of recording transaction by using

Management Accounting organisations able to represent their accounting information in a

systematic way which help in take effective business decisions as well as representing internal

information to their stakeholders in order to understand the reliability of Management

Accounting, capital joinery limited has been taken this is the small organisation which Run their

business in manufacturing industry this report has been define requirement of various type of

managing accounting system as well as use of various reports which help in formulation of

budget by using cost and Management Accounting technique organisation able to evaluate their

prices of cost on the basis of recognising planning tool business organisation formed policies and

take decision this report also define those tools which useful in overcoming financial problems.

TASK 1

P1 Explanation of managerial accounting and requirements of different types of management

accounting system.

Management accounting: This is the tool of accounting which is help in attaining business

goals by using and applying various tools. Management accounting is systematic procedure

which help in formulating, recording , and presenting transaction in effective way which helpful

in attain business goals. The main purpose of management accounting in take effective business

decision which useful in attaining long term business goals. There are two types of accounting

system , financial as well as management both are different due to their accounting transaction

procedure (Shields, and Shelleman, 2016).

Difference between management and financial accounting

Financial accounting Management accounting

This accounting branch useful in providing

essential information regarding external

users.

Managers use this system for providing

information to internal users.

It record only transactions which is related

with finance cash.

Management accounting is useful in recording

every transaction.

1

Management Accounting this term is formulated by two words management is the procedure

of analysing recording controlling organising and managing each and every business department

strategies on the other side accounting is the process of recording transaction by using

Management Accounting organisations able to represent their accounting information in a

systematic way which help in take effective business decisions as well as representing internal

information to their stakeholders in order to understand the reliability of Management

Accounting, capital joinery limited has been taken this is the small organisation which Run their

business in manufacturing industry this report has been define requirement of various type of

managing accounting system as well as use of various reports which help in formulation of

budget by using cost and Management Accounting technique organisation able to evaluate their

prices of cost on the basis of recognising planning tool business organisation formed policies and

take decision this report also define those tools which useful in overcoming financial problems.

TASK 1

P1 Explanation of managerial accounting and requirements of different types of management

accounting system.

Management accounting: This is the tool of accounting which is help in attaining business

goals by using and applying various tools. Management accounting is systematic procedure

which help in formulating, recording , and presenting transaction in effective way which helpful

in attain business goals. The main purpose of management accounting in take effective business

decision which useful in attaining long term business goals. There are two types of accounting

system , financial as well as management both are different due to their accounting transaction

procedure (Shields, and Shelleman, 2016).

Difference between management and financial accounting

Financial accounting Management accounting

This accounting branch useful in providing

essential information regarding external

users.

Managers use this system for providing

information to internal users.

It record only transactions which is related

with finance cash.

Management accounting is useful in recording

every transaction.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is essential for formulate financial

statement which useful in representing

accounting information

It is not required for formulate management

accounting statement.

Different types of management accounting system: Business organization apply various

types of tools which help in running business activities as well as recording transaction and

formulate effective business strategies by using theses systems.

Cost accounting system: This system is help in recording all the essential information

regarding cost. Each and every cost is directly impact on profitability rate of organization. With

the use of cost accounting system management department able to identified cost required for

running business organization. As well as cost required for purchasing of raw material.

Management department use various cost technique and strategies which is useful in identifying

and recognizing cost and profit value which is aeries by selling of products. In the context of

above Capital joinery limited, cost accounting system is used with an aim of managing different

kinds of costs like raw material cost, processing cost and many other. Through, above accounting

system their managers become able to know which activity is leading to higher expenditure

compared to budgeted value. This accounting system is essential for above company due to

following reasons:

Essential requirements: In Capital joinery limited, the finance manager uses such

accounting system at the end of each month or quarter. The rationale behind this is that finance

managers of company need to know cost of each item which is produced like joinery for doors,

windows etc. By help of above accounting system, a detailed overview of cost is gathered by

finance managers. And on the grounds of cost of product they assess efficiency of their

operations and activities. On the basis of use internal source manager collect information which

beneficial for internal users also.

Price optimization system: This is also useful and effective business system. Price are

most essential elements for every organizing. Profit is arises by applying effective business

strategies and using price strategy. There are various strategies which used by organization for

setting their rice volume. By using effective pricing policies Capital joinery Limited able to

attain their profit goals. Under this accounting system, prices are set in accordance of customers'

feedback and demand of item in the market. In the aspect of Capital joinery limited, this

2

statement which useful in representing

accounting information

It is not required for formulate management

accounting statement.

Different types of management accounting system: Business organization apply various

types of tools which help in running business activities as well as recording transaction and

formulate effective business strategies by using theses systems.

Cost accounting system: This system is help in recording all the essential information

regarding cost. Each and every cost is directly impact on profitability rate of organization. With

the use of cost accounting system management department able to identified cost required for

running business organization. As well as cost required for purchasing of raw material.

Management department use various cost technique and strategies which is useful in identifying

and recognizing cost and profit value which is aeries by selling of products. In the context of

above Capital joinery limited, cost accounting system is used with an aim of managing different

kinds of costs like raw material cost, processing cost and many other. Through, above accounting

system their managers become able to know which activity is leading to higher expenditure

compared to budgeted value. This accounting system is essential for above company due to

following reasons:

Essential requirements: In Capital joinery limited, the finance manager uses such

accounting system at the end of each month or quarter. The rationale behind this is that finance

managers of company need to know cost of each item which is produced like joinery for doors,

windows etc. By help of above accounting system, a detailed overview of cost is gathered by

finance managers. And on the grounds of cost of product they assess efficiency of their

operations and activities. On the basis of use internal source manager collect information which

beneficial for internal users also.

Price optimization system: This is also useful and effective business system. Price are

most essential elements for every organizing. Profit is arises by applying effective business

strategies and using price strategy. There are various strategies which used by organization for

setting their rice volume. By using effective pricing policies Capital joinery Limited able to

attain their profit goals. Under this accounting system, prices are set in accordance of customers'

feedback and demand of item in the market. In the aspect of Capital joinery limited, this

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting system is crucial to keep prices of different products at a level on which both

stakeholders (company and customers) can satisfied. It is essential for above company because

of following reasons:

Essential requirements : In above company, there are a large product portfolio of joineries of

door and windows, thus it is essential for sales manager to fluctuate prices of items as per the

need of customers and demand. The sales manager of above company utilizes key information

from internal sources because help of such sources they can assess about company's revenues

and can assess need of prices fluctuation. By using information from external source manager of

Capital Joinery able to formulate their pricing policies which also useful for external users as

well as this help in attain business gain.

Inventory management system: This system is related with managing inventory.

Business organizations able to attain their success by maintain and managing their stock . It is

really essential to record each limit of storage. By using management inventory technique, JIT,

ABC analyse and using LIFO as well as FIFO method organization able to identifying maximum

as well as minimum of their business transaction. Management department of capital joinery

Limited apply this methodology through which they manage their inventory. This accounting

system is essential for above company as:

Essential requirements :The production manager of Capital joinery limited needs such

accounting system to take corrective actions about production of new joineries. It becomes

possible because under stock management system a detailed report is prepared which contains

information about how much quantity of raw material, finished goods and prepared goods are

available in warehouse. This information is utilized by production department to analyse need of

purchasing raw material or producing new joineries etc. Information has been collected for using

inventory system from external sources they on the basis of using vouchers, credit notes, and

debit note organization can find out the information regarding level of stock required by

organization.

Job costing system: This system is user by organization to find out time required for

each and every job as well as they find out cost required for fulfilling requirement of every job.

Organization on the basis of using job costing system able to fulfil requirement of every business

transaction. Capital joinery Limited uses this methodology which useful in tracking each

business transaction. This accounting system is used to assess cost of each item in a separate

3

stakeholders (company and customers) can satisfied. It is essential for above company because

of following reasons:

Essential requirements : In above company, there are a large product portfolio of joineries of

door and windows, thus it is essential for sales manager to fluctuate prices of items as per the

need of customers and demand. The sales manager of above company utilizes key information

from internal sources because help of such sources they can assess about company's revenues

and can assess need of prices fluctuation. By using information from external source manager of

Capital Joinery able to formulate their pricing policies which also useful for external users as

well as this help in attain business gain.

Inventory management system: This system is related with managing inventory.

Business organizations able to attain their success by maintain and managing their stock . It is

really essential to record each limit of storage. By using management inventory technique, JIT,

ABC analyse and using LIFO as well as FIFO method organization able to identifying maximum

as well as minimum of their business transaction. Management department of capital joinery

Limited apply this methodology through which they manage their inventory. This accounting

system is essential for above company as:

Essential requirements :The production manager of Capital joinery limited needs such

accounting system to take corrective actions about production of new joineries. It becomes

possible because under stock management system a detailed report is prepared which contains

information about how much quantity of raw material, finished goods and prepared goods are

available in warehouse. This information is utilized by production department to analyse need of

purchasing raw material or producing new joineries etc. Information has been collected for using

inventory system from external sources they on the basis of using vouchers, credit notes, and

debit note organization can find out the information regarding level of stock required by

organization.

Job costing system: This system is user by organization to find out time required for

each and every job as well as they find out cost required for fulfilling requirement of every job.

Organization on the basis of using job costing system able to fulfil requirement of every business

transaction. Capital joinery Limited uses this methodology which useful in tracking each

business transaction. This accounting system is used to assess cost of each item in a separate

3

manner because under it cost of each operation is measured with rationale of job cost. It is

essential for above company due to following reasons:

Essential requirements :In the context of above company, their finance department relay on

such accounting system with an aim of analysing cost of each item or joinery. They do so in

accordance of prepared report under this accounting system in which each products' cost is

categorized in separate elements. They collect theses sources from using internal sources of

organization. On the basis of that these information are used to measure as quantitative method.

P2 Different methods used by organization for prepare management accounting reports

Reports are essential through which every information is recorded in particular file

document. These are help in formatting and providing path for creation f budget. On the basis of

report organization able to proved essential business information. Capital joinery limited

formulate following reports which help in attaining their business goals (Maas, Schaltegger, and

Crutzen, 2016).

Performance report: This report has been formulate for identifying performance of each

department generally small business organisation don't have large period is there this is activities

world limited in some departments with the user performance report organisation able to

understand that you off and identify performance of each department which include marketing

financing production as well as capabilities and is case of human exorcist they hired for their

functions this is the submission of all the report management department of sunshine used report

for 4 minutes effectiveness titans on the basis of identify icing performance

Cost report: This report has been used to define it in every element coach price on the

basis of foreman eating this report management apartment able to recognise for particular

business activities rising in various transactions call report cause report cost report. Coach report

useful in identifying kitchen every transition cost to with organisation bell to formally defective

this is policies for controlling and managing court manager road Capital joinery limited use this

policy through with take enable to control there cost.

Budget report: This report is for imitating for providing guidelines regarding for me

letting of budget it is us conclusion of all the report with his prepared by organisations by using

management accounting technique but it report shows future expenses as well as profit and

4

essential for above company due to following reasons:

Essential requirements :In the context of above company, their finance department relay on

such accounting system with an aim of analysing cost of each item or joinery. They do so in

accordance of prepared report under this accounting system in which each products' cost is

categorized in separate elements. They collect theses sources from using internal sources of

organization. On the basis of that these information are used to measure as quantitative method.

P2 Different methods used by organization for prepare management accounting reports

Reports are essential through which every information is recorded in particular file

document. These are help in formatting and providing path for creation f budget. On the basis of

report organization able to proved essential business information. Capital joinery limited

formulate following reports which help in attaining their business goals (Maas, Schaltegger, and

Crutzen, 2016).

Performance report: This report has been formulate for identifying performance of each

department generally small business organisation don't have large period is there this is activities

world limited in some departments with the user performance report organisation able to

understand that you off and identify performance of each department which include marketing

financing production as well as capabilities and is case of human exorcist they hired for their

functions this is the submission of all the report management department of sunshine used report

for 4 minutes effectiveness titans on the basis of identify icing performance

Cost report: This report has been used to define it in every element coach price on the

basis of foreman eating this report management apartment able to recognise for particular

business activities rising in various transactions call report cause report cost report. Coach report

useful in identifying kitchen every transition cost to with organisation bell to formally defective

this is policies for controlling and managing court manager road Capital joinery limited use this

policy through with take enable to control there cost.

Budget report: This report is for imitating for providing guidelines regarding for me

letting of budget it is us conclusion of all the report with his prepared by organisations by using

management accounting technique but it report shows future expenses as well as profit and

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organisation have ability to earn it in court all the activities with through which organisation able

to attend the year future business.

Account reliable report: This report is formulating for the purpose of finding out those

debtors which are not able to compete their debt liabilities. Those which consider convert as non

performing business assets of the organization. On the basis of formulating of theses report

organization able to decision and formulate effective business policies to control and proved

effective business offer which useful in attaining business goals. Management department of

Capital joinery limited use this report through which they can able to formulate those business

strategies which useful and helpful in increasing cash limits for the organization. It will helpful

in increasing cash inflow for organization.

M1 Benefits of management accounting system

Cost accounting system This system useful for Capital joinery limited to

finding out profit value and cost of each

business activity. On the basis sing this system

management department able to find out the

best way of generating profit as well as those

activities which become the reason of high

generation of cost for organisation (Ameen,

Ahmed, and Abd Hafez, 2018).

Price optimization system Capital joinery limited use this system for

recognizing best pricing strategy . They use

price optimization system which useful in

selecting price according to their products.

Job costing system Management department of Capital joinery

limited use job costing system which helpful in

Inventory costing system This system is help providing information

regarding stock as well as useful in manning

each costing system. Management department

of Capital joinery limited use this tool for

managing and controlling wastage of inventory.

5

to attend the year future business.

Account reliable report: This report is formulating for the purpose of finding out those

debtors which are not able to compete their debt liabilities. Those which consider convert as non

performing business assets of the organization. On the basis of formulating of theses report

organization able to decision and formulate effective business policies to control and proved

effective business offer which useful in attaining business goals. Management department of

Capital joinery limited use this report through which they can able to formulate those business

strategies which useful and helpful in increasing cash limits for the organization. It will helpful

in increasing cash inflow for organization.

M1 Benefits of management accounting system

Cost accounting system This system useful for Capital joinery limited to

finding out profit value and cost of each

business activity. On the basis sing this system

management department able to find out the

best way of generating profit as well as those

activities which become the reason of high

generation of cost for organisation (Ameen,

Ahmed, and Abd Hafez, 2018).

Price optimization system Capital joinery limited use this system for

recognizing best pricing strategy . They use

price optimization system which useful in

selecting price according to their products.

Job costing system Management department of Capital joinery

limited use job costing system which helpful in

Inventory costing system This system is help providing information

regarding stock as well as useful in manning

each costing system. Management department

of Capital joinery limited use this tool for

managing and controlling wastage of inventory.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1 Integration of management accounting reports with its systems.

Management department of Capital joinery limited apply management accounting tools and

technique they use system of management accounting though which organization able to proved

base for formulation of report. Theses report are useful in attaining business advantage by help in

them in taking effective business decision.

TASK 2

P3 Calculation of absorption and marginal costing

Absorption costing: This method is useful in identifying value of cost of organization

which incurred for business activities. They consider only variable cost thus it also known as

variable costing method. This is most self method which apply by organization. This is most

useful method which help in attaining business goals.

Marginal costing: This technique considered all the essential factor and element. They

considered fixed cost and a well as variable cost through which organization take decision. This

will useful in finding out best way and rate of profitability through which organization set their

target . This is most useful strategy apply by organization for finding out their cost.

Standard costing: This is the technique which help in identifying the main reason and

difference aeries between actual and budget cost. It help in finding out variance which become

he reason o and cause of finding out difference. It is most useful technique which self in finding

out main variance. It help in formulating of business decision and made policies which useful in

attain business goals. Standard costing labour, material and overhead variance through which

organization able to understand the reason of defence it help in finding out best opportunities

within given time period.

Absorption costing:

absorption costing

Particulars May June

Sales 25000 18750

6

Management department of Capital joinery limited apply management accounting tools and

technique they use system of management accounting though which organization able to proved

base for formulation of report. Theses report are useful in attaining business advantage by help in

them in taking effective business decision.

TASK 2

P3 Calculation of absorption and marginal costing

Absorption costing: This method is useful in identifying value of cost of organization

which incurred for business activities. They consider only variable cost thus it also known as

variable costing method. This is most self method which apply by organization. This is most

useful method which help in attaining business goals.

Marginal costing: This technique considered all the essential factor and element. They

considered fixed cost and a well as variable cost through which organization take decision. This

will useful in finding out best way and rate of profitability through which organization set their

target . This is most useful strategy apply by organization for finding out their cost.

Standard costing: This is the technique which help in identifying the main reason and

difference aeries between actual and budget cost. It help in finding out variance which become

he reason o and cause of finding out difference. It is most useful technique which self in finding

out main variance. It help in formulating of business decision and made policies which useful in

attain business goals. Standard costing labour, material and overhead variance through which

organization able to understand the reason of defence it help in finding out best opportunities

within given time period.

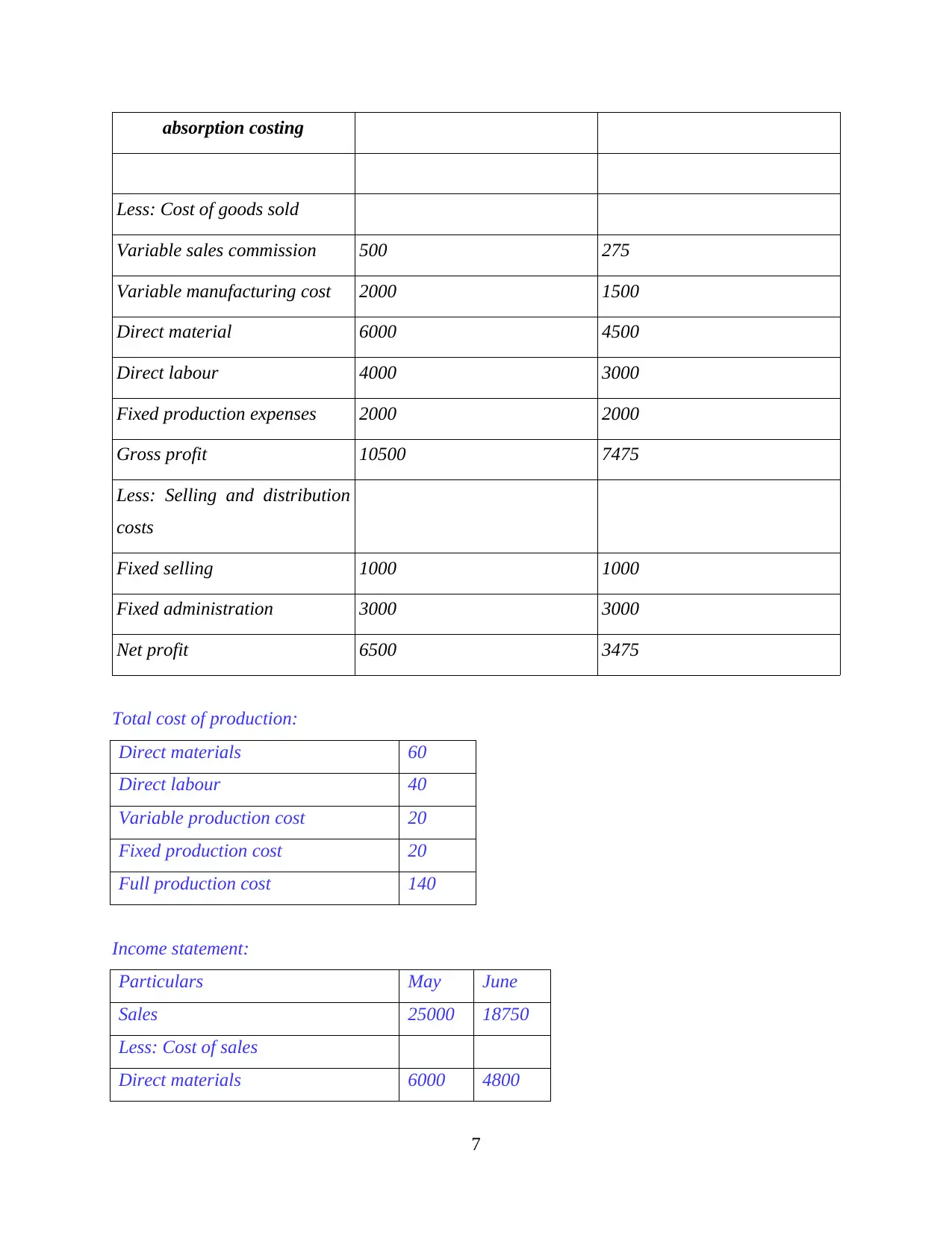

Absorption costing:

absorption costing

Particulars May June

Sales 25000 18750

6

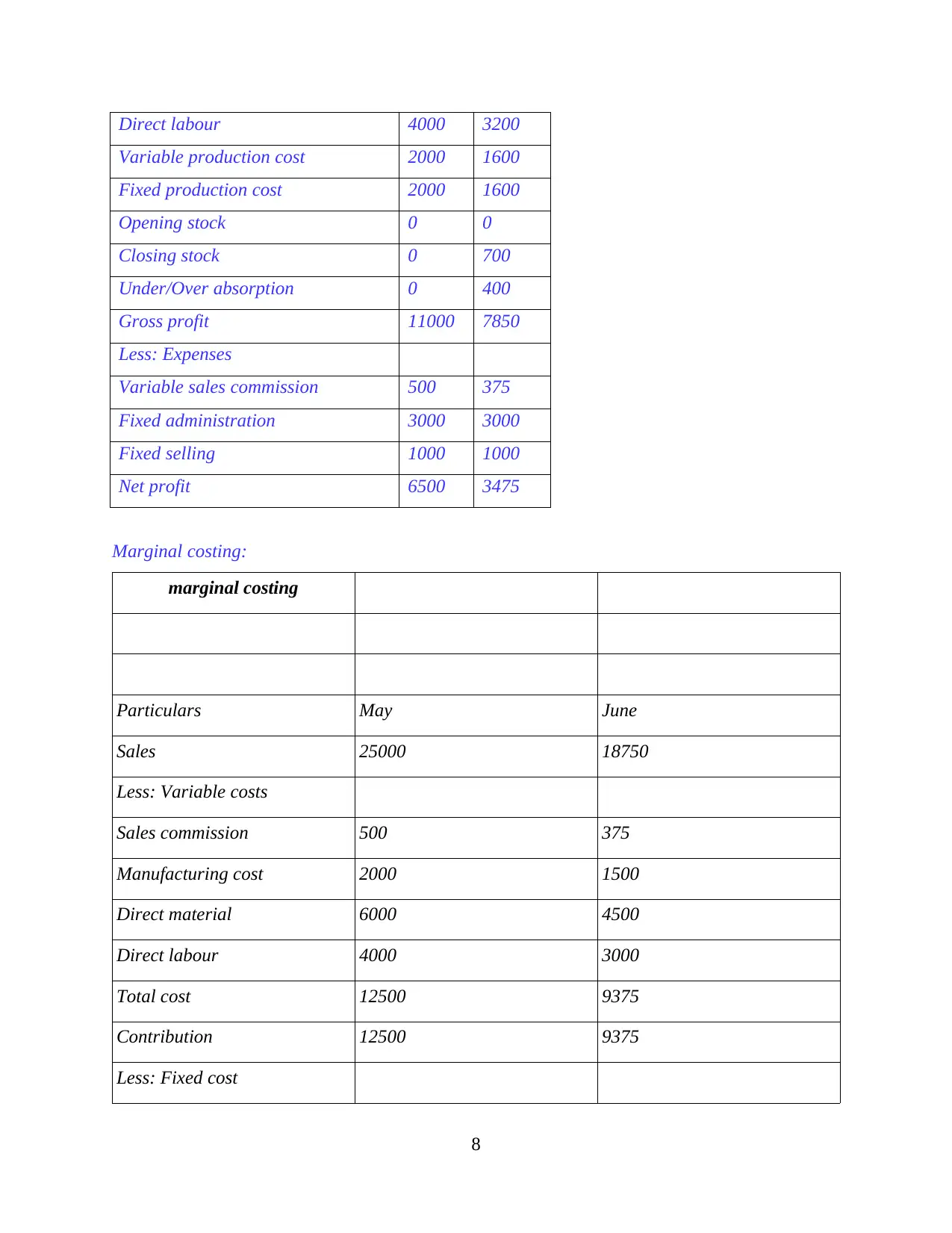

absorption costing

Less: Cost of goods sold

Variable sales commission 500 275

Variable manufacturing cost 2000 1500

Direct material 6000 4500

Direct labour 4000 3000

Fixed production expenses 2000 2000

Gross profit 10500 7475

Less: Selling and distribution

costs

Fixed selling 1000 1000

Fixed administration 3000 3000

Net profit 6500 3475

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

7

Less: Cost of goods sold

Variable sales commission 500 275

Variable manufacturing cost 2000 1500

Direct material 6000 4500

Direct labour 4000 3000

Fixed production expenses 2000 2000

Gross profit 10500 7475

Less: Selling and distribution

costs

Fixed selling 1000 1000

Fixed administration 3000 3000

Net profit 6500 3475

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

marginal costing

Particulars May June

Sales 25000 18750

Less: Variable costs

Sales commission 500 375

Manufacturing cost 2000 1500

Direct material 6000 4500

Direct labour 4000 3000

Total cost 12500 9375

Contribution 12500 9375

Less: Fixed cost

8

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

marginal costing

Particulars May June

Sales 25000 18750

Less: Variable costs

Sales commission 500 375

Manufacturing cost 2000 1500

Direct material 6000 4500

Direct labour 4000 3000

Total cost 12500 9375

Contribution 12500 9375

Less: Fixed cost

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

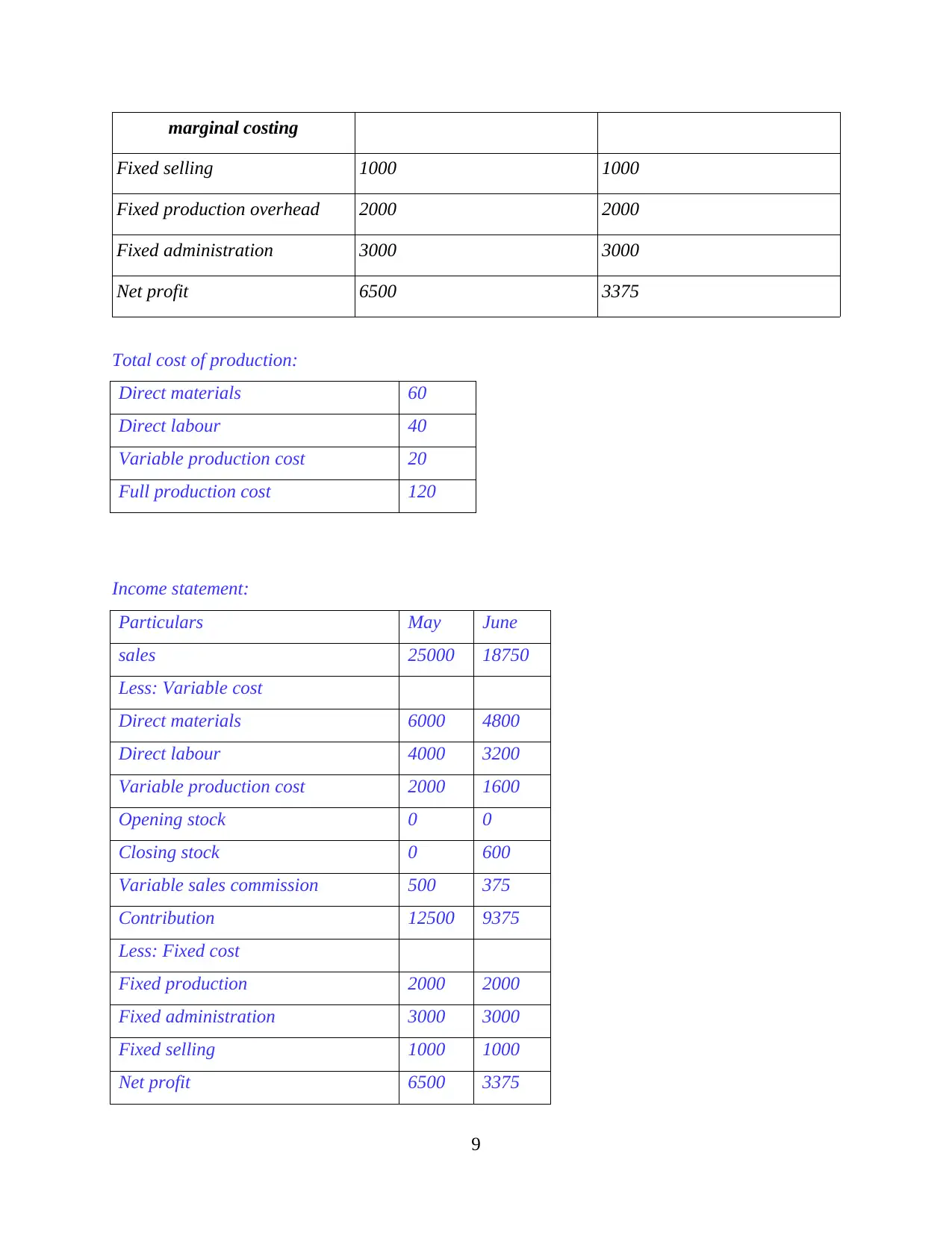

marginal costing

Fixed selling 1000 1000

Fixed production overhead 2000 2000

Fixed administration 3000 3000

Net profit 6500 3375

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

9

Fixed selling 1000 1000

Fixed production overhead 2000 2000

Fixed administration 3000 3000

Net profit 6500 3375

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

9

Reconciliation statement:

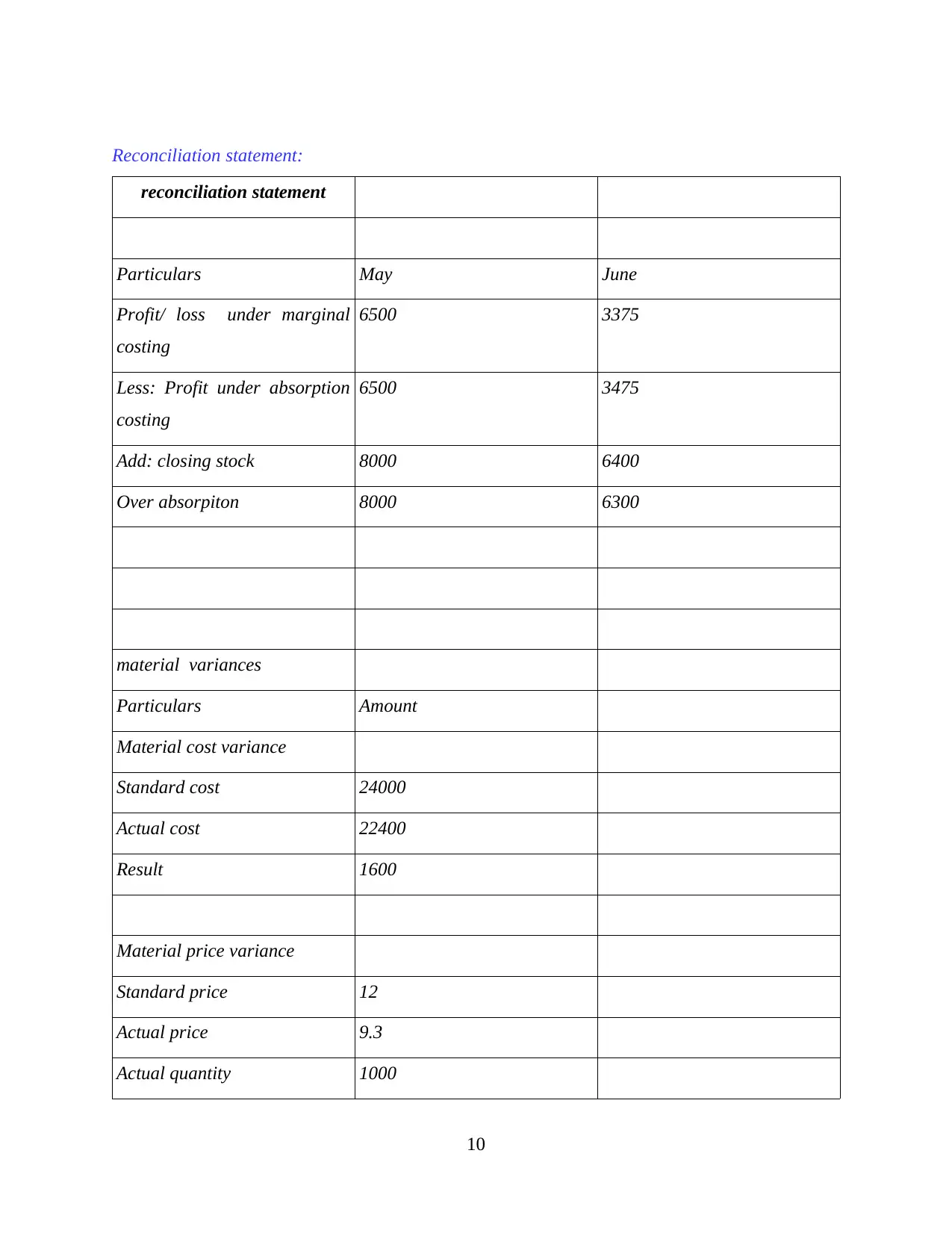

reconciliation statement

Particulars May June

Profit/ loss under marginal

costing

6500 3375

Less: Profit under absorption

costing

6500 3475

Add: closing stock 8000 6400

Over absorpiton 8000 6300

material variances

Particulars Amount

Material cost variance

Standard cost 24000

Actual cost 22400

Result 1600

Material price variance

Standard price 12

Actual price 9.3

Actual quantity 1000

10

reconciliation statement

Particulars May June

Profit/ loss under marginal

costing

6500 3375

Less: Profit under absorption

costing

6500 3475

Add: closing stock 8000 6400

Over absorpiton 8000 6300

material variances

Particulars Amount

Material cost variance

Standard cost 24000

Actual cost 22400

Result 1600

Material price variance

Standard price 12

Actual price 9.3

Actual quantity 1000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.