Analysis of Management Accounting: London Beer Factory Report

VerifiedAdded on 2023/01/18

|16

|4315

|99

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on the London Beer Factory as a case study. It begins with an introduction to management accounting and its significance, followed by an examination of various management accounting systems such as cost accounting, price optimization, inventory management, and job costing. The report then delves into different types of management accounting reports, including cost reports, stock reports, and accounts receivable reports, highlighting their benefits and integration within organizational processes. Furthermore, the report explores financial statement preparation using marginal and absorption costing methods, presenting income statements and their interpretations. Finally, it discusses the limitations and benefits of planning tools for budgetary control, providing a well-rounded overview of management accounting principles and applications.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3..........................................................................................................................................10

TASK 4..........................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

APPENDIX....................................................................................................................................18

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3..........................................................................................................................................10

TASK 4..........................................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

APPENDIX....................................................................................................................................18

INTRODUCTION

In the aspect of finance there are various accounting method that are applied by

corporations and management accounting is one of them. This can be understood as an

accounting method in which accountants analyse financial and anti-financial information for

producing internal reports for managerial aspects (Gray III, 2015). This accounting has different

number of features and roles for business entities. Basically, the objective of report is to

analysing about MA in a broad sense. Under the report a company selected which is London beer

factory, headquartered in London, United Kingdom. The company operates in production and

supply of beer into different segments of United Kingdom.

The report covers about different types of MAS and role for corporations. As well as

about various kinds of MA reports and planning tools of budgetary control. In addition, financial

statements are also produced in report along with contribution of MAS in sorting financial

problems faced by business entities.

MAIN BODY

TASK 1

MA- It can be understood as a type of accounting method in which systematic way of managing

quantitative and qualitative information in applied with an aim of creating internal reports. This

accounting plays a significant role for business entities that are as follows:

Better planning- This accounting contributes in effective planning for companies. It is so

because management department of businesses utilise key information from prepared

internal reports under this accounting.

Better controlling- As well as MA is beneficial for effective controlling of various

aspects. Such as in the above company, their managerial aspect keep control over

different departments by gathering important from this accounting (Smith, 2015).

Effective decision making- Along with above benefits, this accounting is beneficial for

better decision making at different stages. It becomes possible only because of

availability of relevant data at the moment of decision making.

In the aspect of finance there are various accounting method that are applied by

corporations and management accounting is one of them. This can be understood as an

accounting method in which accountants analyse financial and anti-financial information for

producing internal reports for managerial aspects (Gray III, 2015). This accounting has different

number of features and roles for business entities. Basically, the objective of report is to

analysing about MA in a broad sense. Under the report a company selected which is London beer

factory, headquartered in London, United Kingdom. The company operates in production and

supply of beer into different segments of United Kingdom.

The report covers about different types of MAS and role for corporations. As well as

about various kinds of MA reports and planning tools of budgetary control. In addition, financial

statements are also produced in report along with contribution of MAS in sorting financial

problems faced by business entities.

MAIN BODY

TASK 1

MA- It can be understood as a type of accounting method in which systematic way of managing

quantitative and qualitative information in applied with an aim of creating internal reports. This

accounting plays a significant role for business entities that are as follows:

Better planning- This accounting contributes in effective planning for companies. It is so

because management department of businesses utilise key information from prepared

internal reports under this accounting.

Better controlling- As well as MA is beneficial for effective controlling of various

aspects. Such as in the above company, their managerial aspect keep control over

different departments by gathering important from this accounting (Smith, 2015).

Effective decision making- Along with above benefits, this accounting is beneficial for

better decision making at different stages. It becomes possible only because of

availability of relevant data at the moment of decision making.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Different MAS:

Cost accounting system- It is understood as a system that is linked with procedure of

projection of futuristic expenses of business entities in a better manner. The role of this

accounting is not limited till estimation, it also helps in finding variation of expenses. In

the companies, this accounting is essential for better management of monetary activities

so that amount of expenses can be decreased. Under above chosen business entity,

London beer factory this accounting system is applied with an aim of keeping cost of

beer manufacturing lower from the estimation.

Price optimisation system- As accordance of name, this accounting system is associated

with a process of setting prices of products and services as per the demand and quality of

each product (Harrison and Lock, 2017). It becomes possible because under this, data is

collected about customers' demand and price is being set. Such as in regards of above

company, their sales department utilise useful information about demand of their beer

into various market segments on the basis of this price is being set.

Inventory management system- This is a kinds of accounting system which is aligned

with process of keeping control on those goods that are purchased and sold out by

companies during a particular time period. In this, the valuation of stock is done as

accordance of various methods such as LIFO method, FIFO method and weighted

average cost technique. All these techniques play a significant role for companies in order

to track accurate quantity of material at the time when it is needed. Such as in regards of

above business entity, London beer factory their production department utilise key

information about stored raw material for manufacturing of beer.

Job costing system- This can be understood as a kinds of accounting system that is linked

to procedure of computing cost of each produced unit in a correct manner. The objective

of this accounting system is to minimise overall cost of job in a better way. This is not

suitable for small businesses because of small product portfolio. It is suitable for

companies whose product portfolio is wider. In regards of above company, this

accounting system is applied in order to address cost of each produced unit of beer.

Various method of MA reports

Cost accounting system- It is understood as a system that is linked with procedure of

projection of futuristic expenses of business entities in a better manner. The role of this

accounting is not limited till estimation, it also helps in finding variation of expenses. In

the companies, this accounting is essential for better management of monetary activities

so that amount of expenses can be decreased. Under above chosen business entity,

London beer factory this accounting system is applied with an aim of keeping cost of

beer manufacturing lower from the estimation.

Price optimisation system- As accordance of name, this accounting system is associated

with a process of setting prices of products and services as per the demand and quality of

each product (Harrison and Lock, 2017). It becomes possible because under this, data is

collected about customers' demand and price is being set. Such as in regards of above

company, their sales department utilise useful information about demand of their beer

into various market segments on the basis of this price is being set.

Inventory management system- This is a kinds of accounting system which is aligned

with process of keeping control on those goods that are purchased and sold out by

companies during a particular time period. In this, the valuation of stock is done as

accordance of various methods such as LIFO method, FIFO method and weighted

average cost technique. All these techniques play a significant role for companies in order

to track accurate quantity of material at the time when it is needed. Such as in regards of

above business entity, London beer factory their production department utilise key

information about stored raw material for manufacturing of beer.

Job costing system- This can be understood as a kinds of accounting system that is linked

to procedure of computing cost of each produced unit in a correct manner. The objective

of this accounting system is to minimise overall cost of job in a better way. This is not

suitable for small businesses because of small product portfolio. It is suitable for

companies whose product portfolio is wider. In regards of above company, this

accounting system is applied in order to address cost of each produced unit of beer.

Various method of MA reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MA reports may be understood as those written notes which consists information regards

to monetary and anti monetary segments in an systematic manner. This recorded data is widely

used by managerial department of business entities in order to take suitable correct action at right

time. In the above chosen business entity London beer factory, their accountant produces below

mentioned reports that are as followings:

Cost report- This report is being prepared by integration of cost accounting system. The

report consists information regards to expenses which occur in performing vital range of

business activities and operations (Kure and Raffnsøe-Møller, 2017). Along with this

report categorise activities as according to their level of expenses. The objective of

producing this report is to focusing on those elements and aspects which consume higher

amount of cost. In regards of above London beer factory, their finance department utilise

key information by this report that helps them in minimising total amount of cost.

Stock report- This can be understood as a type of report which contains information about

valued quantity of material that is stored in warehouses. Same as the above accounting

report, this report also prepared by help of inventory management system. The main

objective of this report is to help manufacturing department in order to consider right

steps about how much number of units are required to be manufactured. In the context of

above company, their manufacturing department produce beers in a cost effective manner

by consumption of key information through this report.

Accounts receivable report- It is a report which arranges information about number of

debtors who are liable for business entities with date of transaction in a proper manner.

The role of preparing this report is to help finance department in order to make accurate

policies and strategies. In above company, their finance department utilise key

information by help of this report which help in order to make strategies to gather debt

amount from various debtors.

Benefit of MAS:

Name of MAS Benefit

Cost accounting system It is aligned with aspect of controlling overall expenses of

different operations by analysing accurate level of variances. In

the aspect of above London beer factory, they use this accounting

to monetary and anti monetary segments in an systematic manner. This recorded data is widely

used by managerial department of business entities in order to take suitable correct action at right

time. In the above chosen business entity London beer factory, their accountant produces below

mentioned reports that are as followings:

Cost report- This report is being prepared by integration of cost accounting system. The

report consists information regards to expenses which occur in performing vital range of

business activities and operations (Kure and Raffnsøe-Møller, 2017). Along with this

report categorise activities as according to their level of expenses. The objective of

producing this report is to focusing on those elements and aspects which consume higher

amount of cost. In regards of above London beer factory, their finance department utilise

key information by this report that helps them in minimising total amount of cost.

Stock report- This can be understood as a type of report which contains information about

valued quantity of material that is stored in warehouses. Same as the above accounting

report, this report also prepared by help of inventory management system. The main

objective of this report is to help manufacturing department in order to consider right

steps about how much number of units are required to be manufactured. In the context of

above company, their manufacturing department produce beers in a cost effective manner

by consumption of key information through this report.

Accounts receivable report- It is a report which arranges information about number of

debtors who are liable for business entities with date of transaction in a proper manner.

The role of preparing this report is to help finance department in order to make accurate

policies and strategies. In above company, their finance department utilise key

information by help of this report which help in order to make strategies to gather debt

amount from various debtors.

Benefit of MAS:

Name of MAS Benefit

Cost accounting system It is aligned with aspect of controlling overall expenses of

different operations by analysing accurate level of variances. In

the aspect of above London beer factory, they use this accounting

system for tracking actual cost of production and managing those

activities whose cost is above estimation.

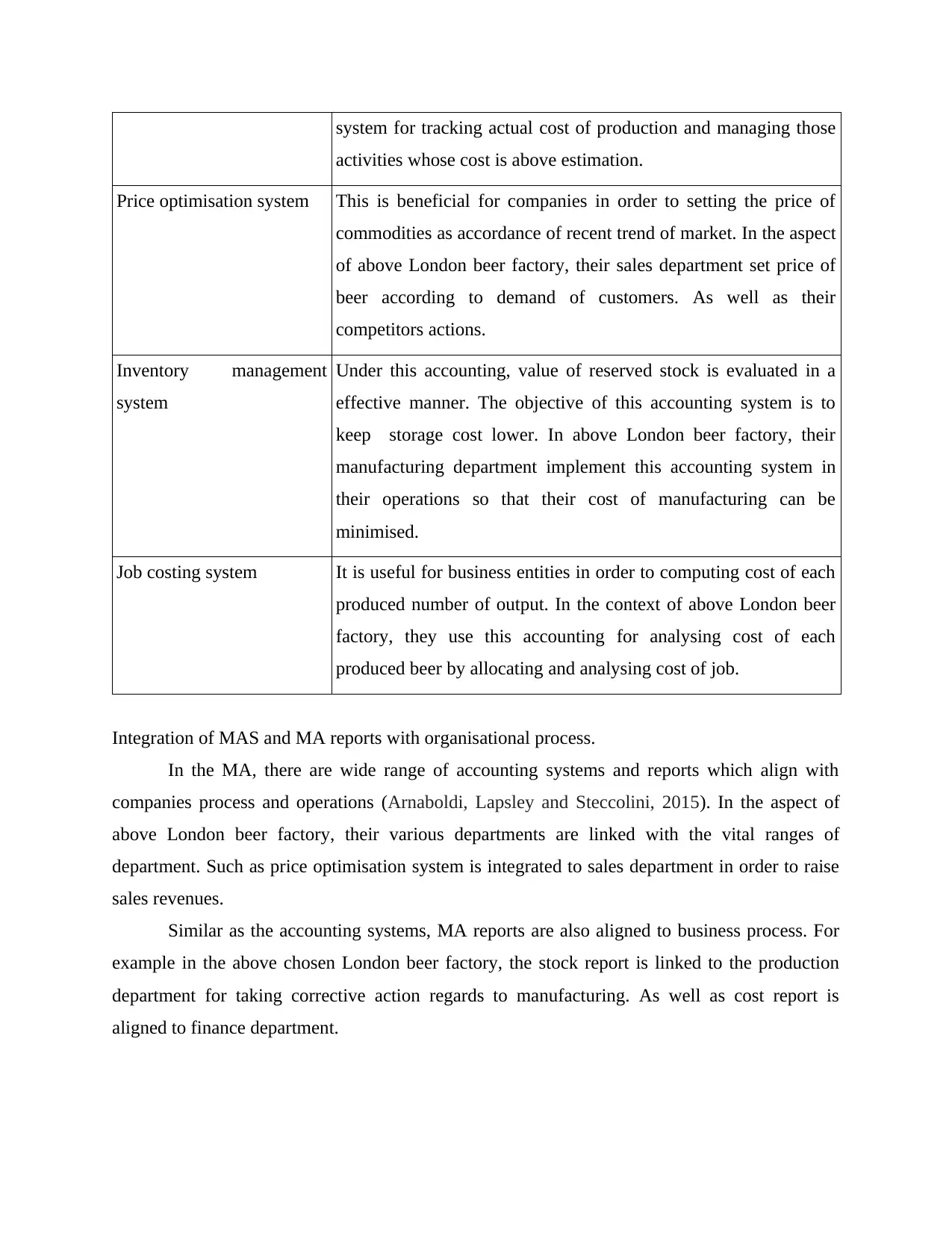

Price optimisation system This is beneficial for companies in order to setting the price of

commodities as accordance of recent trend of market. In the aspect

of above London beer factory, their sales department set price of

beer according to demand of customers. As well as their

competitors actions.

Inventory management

system

Under this accounting, value of reserved stock is evaluated in a

effective manner. The objective of this accounting system is to

keep storage cost lower. In above London beer factory, their

manufacturing department implement this accounting system in

their operations so that their cost of manufacturing can be

minimised.

Job costing system It is useful for business entities in order to computing cost of each

produced number of output. In the context of above London beer

factory, they use this accounting for analysing cost of each

produced beer by allocating and analysing cost of job.

Integration of MAS and MA reports with organisational process.

In the MA, there are wide range of accounting systems and reports which align with

companies process and operations (Arnaboldi, Lapsley and Steccolini, 2015). In the aspect of

above London beer factory, their various departments are linked with the vital ranges of

department. Such as price optimisation system is integrated to sales department in order to raise

sales revenues.

Similar as the accounting systems, MA reports are also aligned to business process. For

example in the above chosen London beer factory, the stock report is linked to the production

department for taking corrective action regards to manufacturing. As well as cost report is

aligned to finance department.

activities whose cost is above estimation.

Price optimisation system This is beneficial for companies in order to setting the price of

commodities as accordance of recent trend of market. In the aspect

of above London beer factory, their sales department set price of

beer according to demand of customers. As well as their

competitors actions.

Inventory management

system

Under this accounting, value of reserved stock is evaluated in a

effective manner. The objective of this accounting system is to

keep storage cost lower. In above London beer factory, their

manufacturing department implement this accounting system in

their operations so that their cost of manufacturing can be

minimised.

Job costing system It is useful for business entities in order to computing cost of each

produced number of output. In the context of above London beer

factory, they use this accounting for analysing cost of each

produced beer by allocating and analysing cost of job.

Integration of MAS and MA reports with organisational process.

In the MA, there are wide range of accounting systems and reports which align with

companies process and operations (Arnaboldi, Lapsley and Steccolini, 2015). In the aspect of

above London beer factory, their various departments are linked with the vital ranges of

department. Such as price optimisation system is integrated to sales department in order to raise

sales revenues.

Similar as the accounting systems, MA reports are also aligned to business process. For

example in the above chosen London beer factory, the stock report is linked to the production

department for taking corrective action regards to manufacturing. As well as cost report is

aligned to finance department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

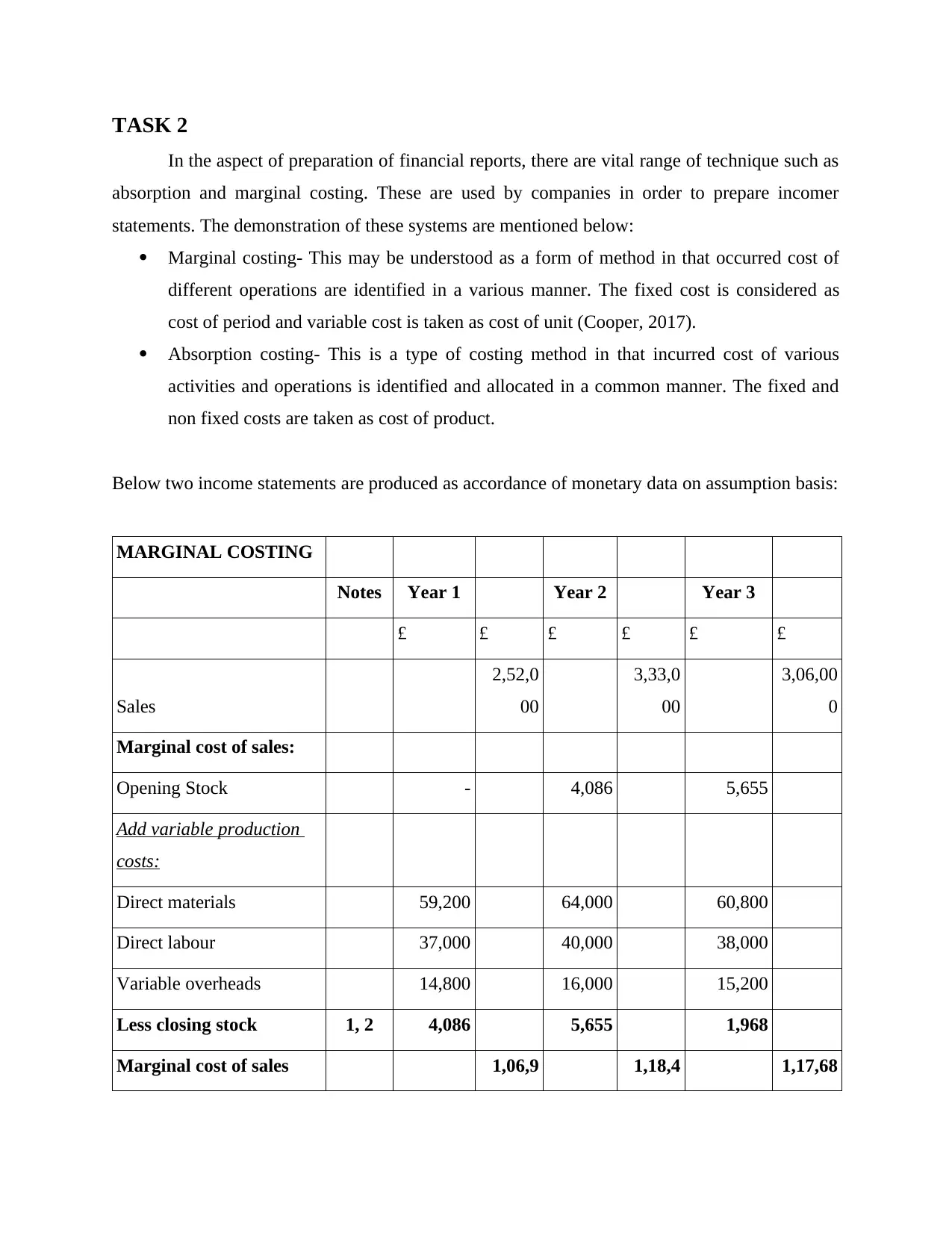

TASK 2

In the aspect of preparation of financial reports, there are vital range of technique such as

absorption and marginal costing. These are used by companies in order to prepare incomer

statements. The demonstration of these systems are mentioned below:

Marginal costing- This may be understood as a form of method in that occurred cost of

different operations are identified in a various manner. The fixed cost is considered as

cost of period and variable cost is taken as cost of unit (Cooper, 2017).

Absorption costing- This is a type of costing method in that incurred cost of various

activities and operations is identified and allocated in a common manner. The fixed and

non fixed costs are taken as cost of product.

Below two income statements are produced as accordance of monetary data on assumption basis:

MARGINAL COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,00

0

Marginal cost of sales:

Opening Stock - 4,086 5,655

Add variable production

costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Less closing stock 1, 2 4,086 5,655 1,968

Marginal cost of sales 1,06,9 1,18,4 1,17,68

In the aspect of preparation of financial reports, there are vital range of technique such as

absorption and marginal costing. These are used by companies in order to prepare incomer

statements. The demonstration of these systems are mentioned below:

Marginal costing- This may be understood as a form of method in that occurred cost of

different operations are identified in a various manner. The fixed cost is considered as

cost of period and variable cost is taken as cost of unit (Cooper, 2017).

Absorption costing- This is a type of costing method in that incurred cost of various

activities and operations is identified and allocated in a common manner. The fixed and

non fixed costs are taken as cost of product.

Below two income statements are produced as accordance of monetary data on assumption basis:

MARGINAL COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,00

0

Marginal cost of sales:

Opening Stock - 4,086 5,655

Add variable production

costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Less closing stock 1, 2 4,086 5,655 1,968

Marginal cost of sales 1,06,9 1,18,4 1,17,68

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

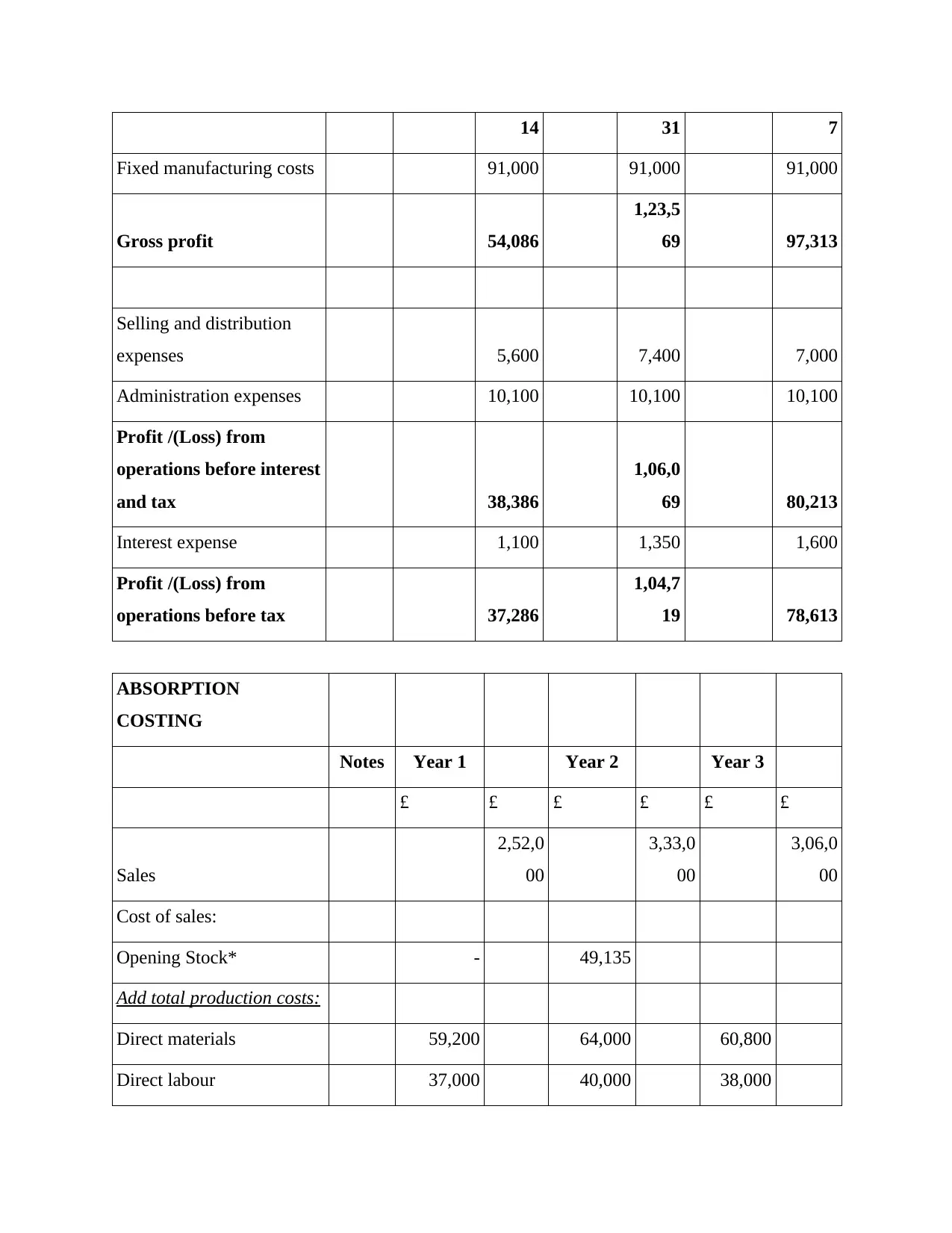

14 31 7

Fixed manufacturing costs 91,000 91,000 91,000

Gross profit 54,086

1,23,5

69 97,313

Selling and distribution

expenses 5,600 7,400 7,000

Administration expenses 10,100 10,100 10,100

Profit /(Loss) from

operations before interest

and tax 38,386

1,06,0

69 80,213

Interest expense 1,100 1,350 1,600

Profit /(Loss) from

operations before tax 37,286

1,04,7

19 78,613

ABSORPTION

COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,0

00

Cost of sales:

Opening Stock* - 49,135

Add total production costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Fixed manufacturing costs 91,000 91,000 91,000

Gross profit 54,086

1,23,5

69 97,313

Selling and distribution

expenses 5,600 7,400 7,000

Administration expenses 10,100 10,100 10,100

Profit /(Loss) from

operations before interest

and tax 38,386

1,06,0

69 80,213

Interest expense 1,100 1,350 1,600

Profit /(Loss) from

operations before tax 37,286

1,04,7

19 78,613

ABSORPTION

COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,0

00

Cost of sales:

Opening Stock* - 49,135

Add total production costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Fixed manufacturing costs 91,000 91,000 91,000

Less closing stock** 1,2 49,135 63,300 21,579

Cost of sales

1,52,8

65

1,96,8

35

1,83,4

21

Gross profit

99,13

5

1,36,1

65

1,22,5

79

Distribution expenses 5,600 7,400 7,000

Administration expenses

10,10

0

10,10

0 10,100

Profit /(Loss) from

operations before interest

and tax

83,43

5

1,18,6

65

1,05,4

79

Interest 1,100 1,350 1,600

Profit /(Loss) from

operations before tax

82,33

5

1,17,3

15

1,03,8

79

Interpretation of prepared financial statements.

As accordance of above produced financial statements, it may be interpreted that amount

of net profit is different in three years. The income statements are prepared as according to

absorption and marginal costing techniques (Hoque, 2017). In the aspect of marginal costing

method, the amount of calculated net profit is of £37286, £104719 and £78613 for year one, two

and three. Apart from it, under absorption costing method the amount of computed net profit is

of £82335, £117315 and £103879 for year one, two and three. Herein, this analysis it is

important to know that value of financial data is similar in both of the methods but amount of net

Fixed manufacturing costs 91,000 91,000 91,000

Less closing stock** 1,2 49,135 63,300 21,579

Cost of sales

1,52,8

65

1,96,8

35

1,83,4

21

Gross profit

99,13

5

1,36,1

65

1,22,5

79

Distribution expenses 5,600 7,400 7,000

Administration expenses

10,10

0

10,10

0 10,100

Profit /(Loss) from

operations before interest

and tax

83,43

5

1,18,6

65

1,05,4

79

Interest 1,100 1,350 1,600

Profit /(Loss) from

operations before tax

82,33

5

1,17,3

15

1,03,8

79

Interpretation of prepared financial statements.

As accordance of above produced financial statements, it may be interpreted that amount

of net profit is different in three years. The income statements are prepared as according to

absorption and marginal costing techniques (Hoque, 2017). In the aspect of marginal costing

method, the amount of calculated net profit is of £37286, £104719 and £78613 for year one, two

and three. Apart from it, under absorption costing method the amount of computed net profit is

of £82335, £117315 and £103879 for year one, two and three. Herein, this analysis it is

important to know that value of financial data is similar in both of the methods but amount of net

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profit is different. It is so because of consideration of total cost of operations under absorption

and marginal costing.

Accounting techniques to produce financial statements.

In the context of financial accounting, most of the income statements are prepared as

according to absorption and marginal costing method. Like in the context of London beer

factory, their income statements are prepared by help of absorption and marginal costing

techniques. These both techniques have some benefits and drawbacks.

Except from these techniques, there are some other methods also to prepare financial

statements such as standard costing method, activity based costing method etc. In the aspect of

standard costing this can be stated that it is related with projection of futuristic cost which is

being used as framework fork for making comparison. While in the activity based costing, cost

of different types of activities are allocated and analysed as per each activity.

TASK 3

Limitations and benefits of planning tools of budgetary control.

Budgetary control- This may be understood as a kinds of approach in order to controlling of

financial and anti-financial performance by help of wide ranges of budget. In this aspect of role

of budgets is essential because by help of these financial plans managers of companies take

corrective actions for setting further outcomes. There are vital range of budgets and some of

them are as follows:

Sales budget- As name assists, it is a budget in which activities related to possible sales

revenues and cost of sales are projected by help of past budget data. The main objective

of preparation of this budget is to help sales department in order to take corrective action

regards to allocation of funds and for increasing total sales revenues (Gullberg, 2016). In

the context of above London beer factory, their accountants prepare this budget for

helping to their sales department. The sales department of above company track actual

performance by calculating variances between actual sales and estimated sales.

Advantages- This budget plays a significant role for business entities in order to align available

funds into different kinds of sales activities. Due to it, maximum utilisation of financial resources

become possible.

and marginal costing.

Accounting techniques to produce financial statements.

In the context of financial accounting, most of the income statements are prepared as

according to absorption and marginal costing method. Like in the context of London beer

factory, their income statements are prepared by help of absorption and marginal costing

techniques. These both techniques have some benefits and drawbacks.

Except from these techniques, there are some other methods also to prepare financial

statements such as standard costing method, activity based costing method etc. In the aspect of

standard costing this can be stated that it is related with projection of futuristic cost which is

being used as framework fork for making comparison. While in the activity based costing, cost

of different types of activities are allocated and analysed as per each activity.

TASK 3

Limitations and benefits of planning tools of budgetary control.

Budgetary control- This may be understood as a kinds of approach in order to controlling of

financial and anti-financial performance by help of wide ranges of budget. In this aspect of role

of budgets is essential because by help of these financial plans managers of companies take

corrective actions for setting further outcomes. There are vital range of budgets and some of

them are as follows:

Sales budget- As name assists, it is a budget in which activities related to possible sales

revenues and cost of sales are projected by help of past budget data. The main objective

of preparation of this budget is to help sales department in order to take corrective action

regards to allocation of funds and for increasing total sales revenues (Gullberg, 2016). In

the context of above London beer factory, their accountants prepare this budget for

helping to their sales department. The sales department of above company track actual

performance by calculating variances between actual sales and estimated sales.

Advantages- This budget plays a significant role for business entities in order to align available

funds into different kinds of sales activities. Due to it, maximum utilisation of financial resources

become possible.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages- Along with the benefit, this budget has limitations too. Such as under this budget

estimation is done as per the previous financial data not as per the research. Due to it, this budget

gets fail in some cases when current years’ sale fluctuates by huge gape.

Production budget- Similar as to above sales budget, this budget is produced by business

entities in order to help their manufacturing department. Under this budget activity

regards to production such as projected production units, cost and many more are

estimated. This budget contributes to business entities in an effective manner by keeping

cost of production in an effective manner. Like in the above London beer factory, this

budget is prepared by accountants in order to help production department. It becomes

possible because they assist key information throughout this budget and make plan

accordingly.

Advantages- This budget makes possible to effective utilisation of available quantity of raw

material. It is so because as per the estimated value of quantity, the production managers allocate

their materials into different operations.

Disadvantage- Though, this budget has multiple number of roles but it has some limitations too

that are faced by companies. It consumes higher amount of costs as well as time in order to

accomplish process of budget making. Due to this drawback, the small business entities cannot

apply it in their operations and activities of production.

Cash budget- This budget has variant number of features and roles for companies except

from above budgets (Monden, 2019). It consists information about estimated value of

cash inflow and outflows. In simple words, this budget estimates the possible activities

which may lead to generation of cash as well as those activities which may become cause

of expenses. In the context of above London beer factory, this budget is widely used by

their finance department for taking corrective action regards to proper management of

available financial resources. Along with for ensuring better liquidity position in order to

make payment of short term debts.

Advantage-This budget helps to companies in order to take better decision for increasing total

value of liquid assets.

Drawback- Key drawback of this budget is that, this is totally based on the assumption and due

to this companies cannot rely on its assumptions.

estimation is done as per the previous financial data not as per the research. Due to it, this budget

gets fail in some cases when current years’ sale fluctuates by huge gape.

Production budget- Similar as to above sales budget, this budget is produced by business

entities in order to help their manufacturing department. Under this budget activity

regards to production such as projected production units, cost and many more are

estimated. This budget contributes to business entities in an effective manner by keeping

cost of production in an effective manner. Like in the above London beer factory, this

budget is prepared by accountants in order to help production department. It becomes

possible because they assist key information throughout this budget and make plan

accordingly.

Advantages- This budget makes possible to effective utilisation of available quantity of raw

material. It is so because as per the estimated value of quantity, the production managers allocate

their materials into different operations.

Disadvantage- Though, this budget has multiple number of roles but it has some limitations too

that are faced by companies. It consumes higher amount of costs as well as time in order to

accomplish process of budget making. Due to this drawback, the small business entities cannot

apply it in their operations and activities of production.

Cash budget- This budget has variant number of features and roles for companies except

from above budgets (Monden, 2019). It consists information about estimated value of

cash inflow and outflows. In simple words, this budget estimates the possible activities

which may lead to generation of cash as well as those activities which may become cause

of expenses. In the context of above London beer factory, this budget is widely used by

their finance department for taking corrective action regards to proper management of

available financial resources. Along with for ensuring better liquidity position in order to

make payment of short term debts.

Advantage-This budget helps to companies in order to take better decision for increasing total

value of liquid assets.

Drawback- Key drawback of this budget is that, this is totally based on the assumption and due

to this companies cannot rely on its assumptions.

Use of different planning tools and their application for preparing and forecasting budgets.

There are different kinds of budgets that are used by corporations in order to take better

decisions of financial aspects. These all budgets are useful for effectively management of their

monetary sources as well as for making accurate forecasting of different operations and activities

(Fleischman and Parker, 2017). In the context of above London beer factory, their accountants

are preparing vital range of budgets such as cash budget, production budget and sales budget. All

these budgets play a key role in the aspect of accurate estimation of income and expenses. This

becomes possible because executives of above company, analyse past years budgeted

information for making forecasting of further activities. Thus, it can be stated that planning tools

of budgetary control are too crucial for making accurate projection of different kinds of financial

activities.

TASK 4

Analysis of ways in which management accounting methods help organisation to respond to

financial problems that will have sustainable success.

Monetary issues- In current business scenario, there is cut throat competition which becomes

cause of different kinds of monetary issues (Busco and Quattrone, 2015). These problems raise

due to ineffective planning and strategy implementation. In simple term, financial problems are

those in that companies fail to operate various functions because of lack of financial sources.

Herein, below some common financial issues which are faced by most of the corporations are

demonstrated in such manner:

Lack of sales revenue- It is one of the major issue that occurs in different businesses and

impact in a negative manner. This can be defined as a kinds of problem in that sales

revenues of corporations continuous to fell and due to this total number of production

also fell down. This is so because if sales revenue will be lower than there will be

shortage of funds in order to make purchase of raw materials and due to this total value of

production will decrease. In regards of above London beer factory, they face this issue

and because of it they do not have enough number of funds to complete various activities

on time.

Increased amount of expenses- Under this sort of monetary issue in that total value of

expense start to raise because of ineffective plans and policies. As a result, companies fail

There are different kinds of budgets that are used by corporations in order to take better

decisions of financial aspects. These all budgets are useful for effectively management of their

monetary sources as well as for making accurate forecasting of different operations and activities

(Fleischman and Parker, 2017). In the context of above London beer factory, their accountants

are preparing vital range of budgets such as cash budget, production budget and sales budget. All

these budgets play a key role in the aspect of accurate estimation of income and expenses. This

becomes possible because executives of above company, analyse past years budgeted

information for making forecasting of further activities. Thus, it can be stated that planning tools

of budgetary control are too crucial for making accurate projection of different kinds of financial

activities.

TASK 4

Analysis of ways in which management accounting methods help organisation to respond to

financial problems that will have sustainable success.

Monetary issues- In current business scenario, there is cut throat competition which becomes

cause of different kinds of monetary issues (Busco and Quattrone, 2015). These problems raise

due to ineffective planning and strategy implementation. In simple term, financial problems are

those in that companies fail to operate various functions because of lack of financial sources.

Herein, below some common financial issues which are faced by most of the corporations are

demonstrated in such manner:

Lack of sales revenue- It is one of the major issue that occurs in different businesses and

impact in a negative manner. This can be defined as a kinds of problem in that sales

revenues of corporations continuous to fell and due to this total number of production

also fell down. This is so because if sales revenue will be lower than there will be

shortage of funds in order to make purchase of raw materials and due to this total value of

production will decrease. In regards of above London beer factory, they face this issue

and because of it they do not have enough number of funds to complete various activities

on time.

Increased amount of expenses- Under this sort of monetary issue in that total value of

expense start to raise because of ineffective plans and policies. As a result, companies fail

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.