Management Accounting Report: Financial Analysis of Airdri (BTEC)

VerifiedAdded on 2023/01/13

|15

|3799

|1

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, using the Airdri organization as a case study. The report begins with an introduction to management accounting, defining its role in analyzing and recording financial and non-financial decisions. It then explores various management accounting techniques, including cost analysis (fixed, variable, and semi-variable costs), cost-volume-profit analysis, flexible budgeting, and different costing methods like absorption and marginal costing, with relevant calculations and examples. The report also delves into the use of planning tools, such as budgeting (master, static, cash flow, operating, and financial budgets), pricing strategies, and the impact of supply and demand. Finally, the report examines how organizations can respond to financial difficulties, including benchmarking, key performance indicators (KPIs), and budgetary control to identify variances and improve financial stability. The report concludes with a summary of key findings and references.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

P3 Application for range of management accounting techniques..............................................1

M2. Application of management accounting technique for appropriate financial reporting

document......................................................................................................................................5

TASK 3............................................................................................................................................6

P4. Various uses of planning tools for managerial accounting..................................................6

M3 Analysing different uses of planning tools and their implication in predicting budget.......8

TASK 4............................................................................................................................................8

P5 Various methods which organisation can use in managerial accounting to respond business

difficulties....................................................................................................................................8

M4 Analysing solutions to financial difficulties which can lead organisation in its stability. .11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

P3 Application for range of management accounting techniques..............................................1

M2. Application of management accounting technique for appropriate financial reporting

document......................................................................................................................................5

TASK 3............................................................................................................................................6

P4. Various uses of planning tools for managerial accounting..................................................6

M3 Analysing different uses of planning tools and their implication in predicting budget.......8

TASK 4............................................................................................................................................8

P5 Various methods which organisation can use in managerial accounting to respond business

difficulties....................................................................................................................................8

M4 Analysing solutions to financial difficulties which can lead organisation in its stability. .11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is also known as managerial accounting or cost accounting. It is

referred as the process of analysing and recording financial and non-financial decisions by

managers. It is the systematic presentation of accounting data to transform its policies which are

to be adopted by managers in their daily activities. According to this project Airdri organisation

has been selected for its management accounting. This organisation was introduced by

Oxfordshire in 1974. It is the first manufacturer of hand dryer. There are various types of range

for management accounting techniques applied in the organisation. It also implement some

planning tools used for the controlling and direction of business(Alyousef and Alnasser, 2015).

Additionally, it can respond financial problems by using benchmarking, key performance

indicators and budgetary targets which helps organisation to achieve success.

TASK 2

P3 Application for range of management accounting techniques

Management accounting is the analysis for business decision-making. There are various

range of these techniques which are described as under:-

Cost:- A cost is an expense done on production of products which is to be recovered on

sale by earning profits.

Types of cost:- The cost is further classified in various categories which are:-

Fixed Cost:- It is the cost which remains constant and stable, which don't fluctuate on

change in mass of production.

Variable cost:- It vary with change in volume of production.

Semi- Variable cost:- It is the cost which are partially fixed and partially variable.

Cost Analysis:- It is considered as the measurement of expense incurred in

manufacturing as compared to output generated.

Cost Volume profit:- This analysis is used to determine the changes taking place in cost

and volume affects the operating profit of an organisation.

Flexible Budgeting:- It is a flexible budget which predicts production with changing

level of business activity (Elmassri, Harris and Carter, 2016).

Cost Variances:- It is the variation between expected expenses and actual expense done

by an organisation.

1

Management accounting is also known as managerial accounting or cost accounting. It is

referred as the process of analysing and recording financial and non-financial decisions by

managers. It is the systematic presentation of accounting data to transform its policies which are

to be adopted by managers in their daily activities. According to this project Airdri organisation

has been selected for its management accounting. This organisation was introduced by

Oxfordshire in 1974. It is the first manufacturer of hand dryer. There are various types of range

for management accounting techniques applied in the organisation. It also implement some

planning tools used for the controlling and direction of business(Alyousef and Alnasser, 2015).

Additionally, it can respond financial problems by using benchmarking, key performance

indicators and budgetary targets which helps organisation to achieve success.

TASK 2

P3 Application for range of management accounting techniques

Management accounting is the analysis for business decision-making. There are various

range of these techniques which are described as under:-

Cost:- A cost is an expense done on production of products which is to be recovered on

sale by earning profits.

Types of cost:- The cost is further classified in various categories which are:-

Fixed Cost:- It is the cost which remains constant and stable, which don't fluctuate on

change in mass of production.

Variable cost:- It vary with change in volume of production.

Semi- Variable cost:- It is the cost which are partially fixed and partially variable.

Cost Analysis:- It is considered as the measurement of expense incurred in

manufacturing as compared to output generated.

Cost Volume profit:- This analysis is used to determine the changes taking place in cost

and volume affects the operating profit of an organisation.

Flexible Budgeting:- It is a flexible budget which predicts production with changing

level of business activity (Elmassri, Harris and Carter, 2016).

Cost Variances:- It is the variation between expected expenses and actual expense done

by an organisation.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption Costing:- It is also known as inventory valuation method. It involves direct

cost which consists of material, labour, overhead, etc., are the manufacturing expense assigned to

produce a product.

Marginal Costing:- It is the change in total production cost which increases on every

additional unit of variable cost whereas fixed cost remains constant.

Cost Allocation:- It is considered as the cost allocation on every department, production

process in forming a product.

Activity-based Costing:- This is implied by organisation to improve cost accuracy on

every business activity.

Inventory Cost:- It's the cost originated by business on its procurement, storage, and

management of inventory in business (Fallan and Opstad, 2014).

Types of Inventory cost:- There are three types of inventory cost,which are as follows:-

Ordering cost:- These are those expense incurred on storing inventory until it is sold

which are placing an order, handling paper work, etc.

Carrying Cost:- This is the cost implied on storage of finished product, insurance,

obsolete, loss by theft, etc. which leads to increase the price of product.

Shortage Cost:- This is the cost which are generated on out of stock product by

disrupted production, emergency shipments, customer loyalty.

Benefits of reducing inventory cost:- The owner of organisation are benefited with the

inventory cost control by earning more profit on least expense incurred. This also leads in

reduction of obsolescence of products, cost shortage as it produce more to meet the demand of

consumers.

Valuation method:- This method determines current worth and identifying monetary

terms to quantify its benefits. It involves three types of valuation method such as asset based,

market value and earning value approach.

Overhead Cost:- It is referred as an ongoing expense of operating business. This

expense is done by entities for its stability and to achieve success in future (Holm, Kumar and

Plenborg, 2016)

Absorption costing technique

Quarter 1

Particulars Amount

2

cost which consists of material, labour, overhead, etc., are the manufacturing expense assigned to

produce a product.

Marginal Costing:- It is the change in total production cost which increases on every

additional unit of variable cost whereas fixed cost remains constant.

Cost Allocation:- It is considered as the cost allocation on every department, production

process in forming a product.

Activity-based Costing:- This is implied by organisation to improve cost accuracy on

every business activity.

Inventory Cost:- It's the cost originated by business on its procurement, storage, and

management of inventory in business (Fallan and Opstad, 2014).

Types of Inventory cost:- There are three types of inventory cost,which are as follows:-

Ordering cost:- These are those expense incurred on storing inventory until it is sold

which are placing an order, handling paper work, etc.

Carrying Cost:- This is the cost implied on storage of finished product, insurance,

obsolete, loss by theft, etc. which leads to increase the price of product.

Shortage Cost:- This is the cost which are generated on out of stock product by

disrupted production, emergency shipments, customer loyalty.

Benefits of reducing inventory cost:- The owner of organisation are benefited with the

inventory cost control by earning more profit on least expense incurred. This also leads in

reduction of obsolescence of products, cost shortage as it produce more to meet the demand of

consumers.

Valuation method:- This method determines current worth and identifying monetary

terms to quantify its benefits. It involves three types of valuation method such as asset based,

market value and earning value approach.

Overhead Cost:- It is referred as an ongoing expense of operating business. This

expense is done by entities for its stability and to achieve success in future (Holm, Kumar and

Plenborg, 2016)

Absorption costing technique

Quarter 1

Particulars Amount

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales 66000

Less: Cost of sales

Production Cost (78000*

0.65) 50700

Semi variable (78000 *

0.20) 15600

Total variable cost 66300

Less: Closing stock 10200 56100

Gross Profit 9900

Less: Expenses 400

9500

Selling and distribution as

fixed 5200

Net Profit 4300

Quarter 2

Particular Amount

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*.20) 13200

Production cost

(66000*0.20) 42900

Total variable cost 66300

Less: Closing stock 3400 62900

Gross Profit 11100

Less: Selling expenses 2800

8300

3

Less: Cost of sales

Production Cost (78000*

0.65) 50700

Semi variable (78000 *

0.20) 15600

Total variable cost 66300

Less: Closing stock 10200 56100

Gross Profit 9900

Less: Expenses 400

9500

Selling and distribution as

fixed 5200

Net Profit 4300

Quarter 2

Particular Amount

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*.20) 13200

Production cost

(66000*0.20) 42900

Total variable cost 66300

Less: Closing stock 3400 62900

Gross Profit 11100

Less: Selling expenses 2800

8300

3

Fixed expenses 5200

Net profit 3100

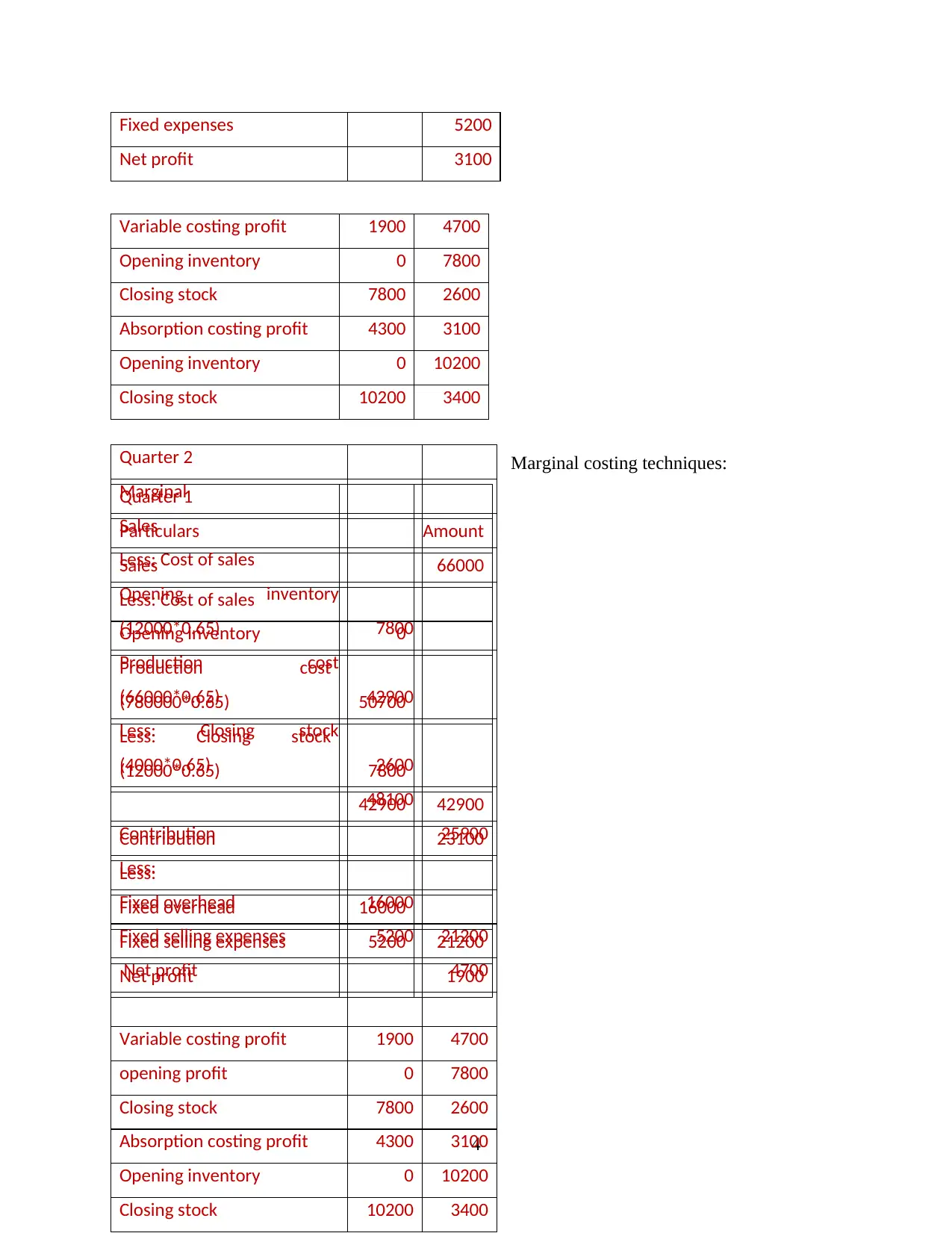

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Marginal costing techniques:

Quarter 1

Particulars Amount

Sales 66000

Less: Cost of sales

Opening inventory 0

Production cost

(780000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

Net profit 1900

4

Quarter 2

Marginal

Sales

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

Production cost

(66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

Net profit 4700

Variable costing profit 1900 4700

opening profit 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Net profit 3100

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Marginal costing techniques:

Quarter 1

Particulars Amount

Sales 66000

Less: Cost of sales

Opening inventory 0

Production cost

(780000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

Net profit 1900

4

Quarter 2

Marginal

Sales

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

Production cost

(66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

Net profit 4700

Variable costing profit 1900 4700

opening profit 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2. Application of management accounting technique for appropriate financial reporting

document

Normal Costing:- It is the cost which identifies the expense incurred on every particular

product based on its material, labour, overhead, etc. to produce. It is easier to determine accurate

production cost (Luft, Shields and Thomas, 2016).

Standard Costing:- This costing method is used to compare standard cost and revenue

with actual results for determining the deviation to take correct measures for its improvement. It

5

document

Normal Costing:- It is the cost which identifies the expense incurred on every particular

product based on its material, labour, overhead, etc. to produce. It is easier to determine accurate

production cost (Luft, Shields and Thomas, 2016).

Standard Costing:- This costing method is used to compare standard cost and revenue

with actual results for determining the deviation to take correct measures for its improvement. It

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps managers to identify about business production, profit and issues. It provides more useful

information for managerial planning and decision-making.

TASK 3

P4. Various uses of planning tools for managerial accounting

The planning instruments used in management accounting are to prepare budget with

different pricing strategies to compete with rivalries from demand and supply, which helps

managers of Airdri in cost-accounting management are:-

Budget:- It is a formal document with the estimated income and expense for the basis of

future plans and objectives. Managers of Airdri must estimate budget to meet its future

requirements for its success (Ojua, 2016).

Different types of budget:- There are different types of budget prepared by an

organisation to have direction and control on management accounting are:-

Master Budget:- This budget provides the accurate information of its financial activity

and its position as compared to its competitors. Managers of Airdri use this budget to

maintain particular record of sales, operating expense, etc., to accomplish its goals.

Static Budget:- It is fixed budget which remain same even after changes in sales takes

place. Managers of Airdri use it for warehousing and storage of inventory.

Cash Flow Budget:- It is used to determine inflow and outflow of cash within particular

duration of business. Managers of Airdri use it to manage cash wisely, to earn profits by

more of cash inflow.

Operating Budget:- This budget forecast and analyse expected income and expenses in

specified period of time. Managers of Airdri use this budget for monthly basis to

determine the over expense on supply.

Financial Budget:- This budget represents the managing assets, income, cash flow and

expenses of an organisation. Managers of Airdri use it to evaluate their business financial

position of profit and loss, determine its value on public stock offering or merger.

Alternative methods of budget:- This budget involves four alternative budgeting

methods which are traditional historic, priority basis, zero- based and activity based budgeting.

Behavioural implications of budget:- The budget create positivity in behaviour of

human beings as the managers are about to achieve their desired set goal of business.

6

information for managerial planning and decision-making.

TASK 3

P4. Various uses of planning tools for managerial accounting

The planning instruments used in management accounting are to prepare budget with

different pricing strategies to compete with rivalries from demand and supply, which helps

managers of Airdri in cost-accounting management are:-

Budget:- It is a formal document with the estimated income and expense for the basis of

future plans and objectives. Managers of Airdri must estimate budget to meet its future

requirements for its success (Ojua, 2016).

Different types of budget:- There are different types of budget prepared by an

organisation to have direction and control on management accounting are:-

Master Budget:- This budget provides the accurate information of its financial activity

and its position as compared to its competitors. Managers of Airdri use this budget to

maintain particular record of sales, operating expense, etc., to accomplish its goals.

Static Budget:- It is fixed budget which remain same even after changes in sales takes

place. Managers of Airdri use it for warehousing and storage of inventory.

Cash Flow Budget:- It is used to determine inflow and outflow of cash within particular

duration of business. Managers of Airdri use it to manage cash wisely, to earn profits by

more of cash inflow.

Operating Budget:- This budget forecast and analyse expected income and expenses in

specified period of time. Managers of Airdri use this budget for monthly basis to

determine the over expense on supply.

Financial Budget:- This budget represents the managing assets, income, cash flow and

expenses of an organisation. Managers of Airdri use it to evaluate their business financial

position of profit and loss, determine its value on public stock offering or merger.

Alternative methods of budget:- This budget involves four alternative budgeting

methods which are traditional historic, priority basis, zero- based and activity based budgeting.

Behavioural implications of budget:- The budget create positivity in behaviour of

human beings as the managers are about to achieve their desired set goal of business.

6

Pricing strategies:- It is the strategy which determines best decision planning for price

of product to compete with its rivalries. Managers of Airdri plan pricing strategy to produce

products on least price with increase in number of sale to achieve success (Orelli, Padovani and

Katsikas, 2016).

Competitors determine their prices:- Competitors of Airdri organisation are World

Dryer Corporation, Kallerians, American Dryer Corporation, etc. They estimate pricing on the

basis of cost-plus evaluation, competitory rating, value-based pricing, penetration price and

skimming valuation.

Supply and demand considerations:- The fluctuation in supply and demand by rise and

fall until the price reaches consumer equilibrium of organisation. Managers of Airdri focus on

the price for consumer satisfaction with its equilibrium.

Actual Costing:- This costing measures actual cost of direct material, labour, etc., on

particular accounting period. Managers of Airdri use this concept of costing to determine actual

costing of inventory through weighted average cost on accounting period.

Cost system differ on costing activity:- This difference is explained on the basis of

costing described as under:-

Job costing:- It is the method of identifying, recording and analysing the manufacturing

job instead of process. Managers of Airdri use this system to examine each job for

achievement of organisation objectives.

Process Costing:- This system accumulates cost when large number of diversified units

are produced. Managers of Airdri implement this system to aggregate large batch of

products and then allocate them for one individual unit produced.

Contract Costing:- This cost system is associated with specialised written agreement

with customer. Managers of Airdri use this to track the cost of that contract which

satisfies the desire of consumers.

Strategic Planning:- It is the process of identifying and analysing the business strategies

by implementing them for evaluation of achievement of organisational objectives. It is very

essential for managers of Airdri for their business growth and its stability in competitive market

as it inform about possible opportunities and solution of challenges.

7

of product to compete with its rivalries. Managers of Airdri plan pricing strategy to produce

products on least price with increase in number of sale to achieve success (Orelli, Padovani and

Katsikas, 2016).

Competitors determine their prices:- Competitors of Airdri organisation are World

Dryer Corporation, Kallerians, American Dryer Corporation, etc. They estimate pricing on the

basis of cost-plus evaluation, competitory rating, value-based pricing, penetration price and

skimming valuation.

Supply and demand considerations:- The fluctuation in supply and demand by rise and

fall until the price reaches consumer equilibrium of organisation. Managers of Airdri focus on

the price for consumer satisfaction with its equilibrium.

Actual Costing:- This costing measures actual cost of direct material, labour, etc., on

particular accounting period. Managers of Airdri use this concept of costing to determine actual

costing of inventory through weighted average cost on accounting period.

Cost system differ on costing activity:- This difference is explained on the basis of

costing described as under:-

Job costing:- It is the method of identifying, recording and analysing the manufacturing

job instead of process. Managers of Airdri use this system to examine each job for

achievement of organisation objectives.

Process Costing:- This system accumulates cost when large number of diversified units

are produced. Managers of Airdri implement this system to aggregate large batch of

products and then allocate them for one individual unit produced.

Contract Costing:- This cost system is associated with specialised written agreement

with customer. Managers of Airdri use this to track the cost of that contract which

satisfies the desire of consumers.

Strategic Planning:- It is the process of identifying and analysing the business strategies

by implementing them for evaluation of achievement of organisational objectives. It is very

essential for managers of Airdri for their business growth and its stability in competitive market

as it inform about possible opportunities and solution of challenges.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M3 Analysing different uses of planning tools and their implication in predicting budget

These planing instruments are used to achieve organisational objective for its stability in

competitive market. Every business aims to direct and control its cost to increase large number of

sales with consumer satisfaction and maximisation of profits. These tools are applicable in

forecasting the budget by estimating accuracy in forecasting, cost-benefit analysis on particular

time period. Managers of Airdri use these planning tools to ascertain expected budget and to

compare the actual result by estimating corrective measures.

TASK 4

P5 Various methods which organisation can use in managerial accounting to respond business

difficulties

Financial Problems:- It is the biggest issue faced by managers of an organisation while

running a business. This is mandatory for an organisation to maintain its monetary terms.

Managers of Airdri focus on these major issues which affect the steadiness of company in global

marketplace.

Unnecessary expenditure:- The high expenditure done on various activities such as

advertisements, promotional activities, etc., which increase cost of product. Managers of

Airdri are adversely affected by this issue as it lacks in accomplishment of aims and

intentions to attain success.

Lack of cash inflow:- It is described as capability of managers to restrict its cash outflow

by managing cash transaction for controlling expenditure. Managers of Airdri further

develop various strategies to increase cash inflow in business that leads to attain high

profit-margin by minimising this cash outflow.

The financial problems can be solved by using benchmarking, key performance

indicators (KPI) and budgetary contrrol to identify variances. Managers of Airdri have developed

effective strategies and systems for accomplishment of its project on particular time, full

disclosure of financial positions which leads to achieve success.

Identification of Financial problems:- These problems can be identified by the

following are:-

Benchmarking:- It's the process of measuring organisation performance on the basis of

evaluating business production as compared to its rivalries. Managers of Airdri use it to identify

8

These planing instruments are used to achieve organisational objective for its stability in

competitive market. Every business aims to direct and control its cost to increase large number of

sales with consumer satisfaction and maximisation of profits. These tools are applicable in

forecasting the budget by estimating accuracy in forecasting, cost-benefit analysis on particular

time period. Managers of Airdri use these planning tools to ascertain expected budget and to

compare the actual result by estimating corrective measures.

TASK 4

P5 Various methods which organisation can use in managerial accounting to respond business

difficulties

Financial Problems:- It is the biggest issue faced by managers of an organisation while

running a business. This is mandatory for an organisation to maintain its monetary terms.

Managers of Airdri focus on these major issues which affect the steadiness of company in global

marketplace.

Unnecessary expenditure:- The high expenditure done on various activities such as

advertisements, promotional activities, etc., which increase cost of product. Managers of

Airdri are adversely affected by this issue as it lacks in accomplishment of aims and

intentions to attain success.

Lack of cash inflow:- It is described as capability of managers to restrict its cash outflow

by managing cash transaction for controlling expenditure. Managers of Airdri further

develop various strategies to increase cash inflow in business that leads to attain high

profit-margin by minimising this cash outflow.

The financial problems can be solved by using benchmarking, key performance

indicators (KPI) and budgetary contrrol to identify variances. Managers of Airdri have developed

effective strategies and systems for accomplishment of its project on particular time, full

disclosure of financial positions which leads to achieve success.

Identification of Financial problems:- These problems can be identified by the

following are:-

Benchmarking:- It's the process of measuring organisation performance on the basis of

evaluating business production as compared to its rivalries. Managers of Airdri use it to identify

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

their financial position in this competitive market (Prencipe, Bar-Yosef and Dekker, 2014). The

managers further plans to solve the financial problem of unnecessary expenditure by minimising

through preparing various schemes to manage their monetary transactions.

Key Performance Indicator (KPI):- It demonstrates the company effectiveness in

achieving its organisation goal. Managers of Airdri use this to evaluate their task at multiple

level for achievement of success. The Airdri Company focus on minimising cash outflow with

maintaining budget that aims to equalise business revenue and expenditure from estimated to

actual financial plan.

Budgetary targets:- The organisation set budgetary targets to identify the variance and

problems taking place which delays in organisational objective. Managers of Airdri focus on

budgetary targets as it directs and control the task of company with its effectiveness and

efficiency.

Financial governance:- It is referred as different methods for collection of information,

managing, monitoring and controlling. It includes the measurement to track company

performance for achievement of goal. Managers of Airdri use this financial governance to

manage activity and control information, compliance, transaction and disclosures.

Application of financial administration for preventing from financial difficulty:-

These application of financial governance in prevention from financial governance are as

follows:-

Control environment:- It is the main purpose of organisation to maintain its control on

people performance. Managers of Airdri imply it to manage and control on activities of

organisation, providing discipline and structure for ethical values to compete with

competitors.

Risk Assessment:- Every organisation targets to examine the risk which are either

controllable or uncontrollable. Managers of Airdri imply risk assessment for the

corrective measures to control risk (Sokolov and Giniatullin, 2015).

Control Activities:- These are the activities for policies and procedures that helps to

ensure management about major directions to control task on track. Managers of Airdri

are benefited with segregation of duties which focus on particular area for proper control

to achieve success.

9

managers further plans to solve the financial problem of unnecessary expenditure by minimising

through preparing various schemes to manage their monetary transactions.

Key Performance Indicator (KPI):- It demonstrates the company effectiveness in

achieving its organisation goal. Managers of Airdri use this to evaluate their task at multiple

level for achievement of success. The Airdri Company focus on minimising cash outflow with

maintaining budget that aims to equalise business revenue and expenditure from estimated to

actual financial plan.

Budgetary targets:- The organisation set budgetary targets to identify the variance and

problems taking place which delays in organisational objective. Managers of Airdri focus on

budgetary targets as it directs and control the task of company with its effectiveness and

efficiency.

Financial governance:- It is referred as different methods for collection of information,

managing, monitoring and controlling. It includes the measurement to track company

performance for achievement of goal. Managers of Airdri use this financial governance to

manage activity and control information, compliance, transaction and disclosures.

Application of financial administration for preventing from financial difficulty:-

These application of financial governance in prevention from financial governance are as

follows:-

Control environment:- It is the main purpose of organisation to maintain its control on

people performance. Managers of Airdri imply it to manage and control on activities of

organisation, providing discipline and structure for ethical values to compete with

competitors.

Risk Assessment:- Every organisation targets to examine the risk which are either

controllable or uncontrollable. Managers of Airdri imply risk assessment for the

corrective measures to control risk (Sokolov and Giniatullin, 2015).

Control Activities:- These are the activities for policies and procedures that helps to

ensure management about major directions to control task on track. Managers of Airdri

are benefited with segregation of duties which focus on particular area for proper control

to achieve success.

9

Information and communication:- Organisation should pertain information for

effective communication that creates success of organisation. Managers of Airdri must

take note of proper decoding and feedback of messages with each other.

Monitoring:- It is the process of accessing the quality of performance over time.

Managers of Airdri impose monitoring to control the task to be accomplished with

efficiency.

Using financial administration to monitor strategy:- The financial governance is used

to monitor strategy for cash inflow, economic valuation, asset management, growth, risk

assessment and measurement, profitability ratios, optimizing taxation, etc.

The comparison between Airdri and Excel dryers:-

Basis of Difference Airdri Excel Dryers

Financial Problem The manager of Airdri faces

issue of unnecessary

expenditure by spending their

money undoubtedly with high

usage on promotional

activities.

The managers of Excel Dryers

challenge the financial

problem of lack in cash inflow

by increasing their cash

outflow with high expenses on

increasing bad debts.

Management Accounting

System

The Airdri managers adopt

inventory management system

for selling their products

through marginal and

absorption costing with FIFO

and LIFO.

The Excel Dryers implements

optimising pricing strategy for

maintain the cost of their

products at low price for

enlarging sales to attain profit-

margins.

System usage This system is implied in

business operation for proper

management of inventory in

order to ascertain actual

production and output.

The managers of Excel Dryers

use this system for selling

products at least-cost effective

price for maximisation of

wealth and profits in order to

increase market share.

10

effective communication that creates success of organisation. Managers of Airdri must

take note of proper decoding and feedback of messages with each other.

Monitoring:- It is the process of accessing the quality of performance over time.

Managers of Airdri impose monitoring to control the task to be accomplished with

efficiency.

Using financial administration to monitor strategy:- The financial governance is used

to monitor strategy for cash inflow, economic valuation, asset management, growth, risk

assessment and measurement, profitability ratios, optimizing taxation, etc.

The comparison between Airdri and Excel dryers:-

Basis of Difference Airdri Excel Dryers

Financial Problem The manager of Airdri faces

issue of unnecessary

expenditure by spending their

money undoubtedly with high

usage on promotional

activities.

The managers of Excel Dryers

challenge the financial

problem of lack in cash inflow

by increasing their cash

outflow with high expenses on

increasing bad debts.

Management Accounting

System

The Airdri managers adopt

inventory management system

for selling their products

through marginal and

absorption costing with FIFO

and LIFO.

The Excel Dryers implements

optimising pricing strategy for

maintain the cost of their

products at low price for

enlarging sales to attain profit-

margins.

System usage This system is implied in

business operation for proper

management of inventory in

order to ascertain actual

production and output.

The managers of Excel Dryers

use this system for selling

products at least-cost effective

price for maximisation of

wealth and profits in order to

increase market share.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.