Management Accounting Report: Continental Clothing Company, Sept 2019

VerifiedAdded on 2023/01/19

|23

|5757

|64

Report

AI Summary

This report provides a detailed analysis of management accounting practices, focusing on their application within Continental Clothing Company Ltd. The report covers various management accounting systems, including job costing, price optimization, cost accounting, and inventory management, highlighting their benefits and applications. It explores different methods used for management accounting reporting, such as budget reports, accounts receivable aging reports, job cost reports, and inventory and manufacturing reports. Furthermore, the report examines the integration of management accounting systems and reporting within organizational processes, emphasizing their role in strategic decision-making. The report also delves into cost analysis techniques, including marginal and absorption costing, and their application in preparing financial statements. Finally, it discusses the advantages and disadvantages of budgetary control tools and the role of management accounting systems in responding to financial problems to achieve sustainable success. The report uses financial data to demonstrate practical applications and insights.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Session: September 2019

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

Different methods used for management accounting reporting.............................................4

M1 Benefits of management accounting systems and their application within Continental

Clothing Company Ltd...........................................................................................................6

Evaluation of how management accounting systems and management accounting reporting is

integrated within organisational processes.............................................................................7

LO 2.................................................................................................................................................7

Application of management accounting techniques and produce appropriate financial

reporting documents.............................................................................................................13

Financial reports that accurately apply and interpret data for a range of business activities13

LO 3...............................................................................................................................................14

Advantages and disadvantages of different types of tools used for budgetary control........14

LO 4...............................................................................................................................................16

Adoption of management accounting systems to respond to financial problems................16

Role of MAS in responding to financial problems that can lead organisations to sustainable

success..................................................................................................................................19

Planning tools used in solving financial problems to lead organisations to sustainable success

..............................................................................................................................................19

CONCLUSION..............................................................................................................................20

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

Different methods used for management accounting reporting.............................................4

M1 Benefits of management accounting systems and their application within Continental

Clothing Company Ltd...........................................................................................................6

Evaluation of how management accounting systems and management accounting reporting is

integrated within organisational processes.............................................................................7

LO 2.................................................................................................................................................7

Application of management accounting techniques and produce appropriate financial

reporting documents.............................................................................................................13

Financial reports that accurately apply and interpret data for a range of business activities13

LO 3...............................................................................................................................................14

Advantages and disadvantages of different types of tools used for budgetary control........14

LO 4...............................................................................................................................................16

Adoption of management accounting systems to respond to financial problems................16

Role of MAS in responding to financial problems that can lead organisations to sustainable

success..................................................................................................................................19

Planning tools used in solving financial problems to lead organisations to sustainable success

..............................................................................................................................................19

CONCLUSION..............................................................................................................................20

INTRODUCTION

Management Accounting is a technique used to analyse different costs and operational

aspects of the business and helps in preparation of financial statements, reporting and recording

different transactions which supports the managers in better decision making to achieve the

goals of the business. This method also helps in making decisions related to competition by

gathering information and processing them which helps top level in deciding he strategies of the

business and evaluate them on timely basis. In this study Continental Clothing Company Ltd.

which is UK's one of the largest manufacture of cloths and has a significant position in clothing

industry. The company has grown to become the world market leading designer and

manufacturer of cloths and offering customers wider range of quality clothing. In this report the

following topics are discussed in detail which includes various techniques used in reporting of

management accounting, methods of cost accounting which are used to make the profit and loss

statement, tools to plan for controlling the budget and the ways in which management accounting

helps in resolving monetary issues. (Angelone and Neopost, 2015).

LO 1

Management accounting and requirement of different types of management accounting systems

Any accounting that helps the corporations in working more effectively can be terms as

Management Accounting. As per one of the well-known institutes, if management accounting is

applied in the companies by the skilled professionals then it can help the top management in

formulating good strategies and policies which can be used for the smooth operations of the

business.

For Continental Clothing Company Ltd. management accounting systems help in analysing costs

associated with production of cloths, determining ways of reducing prices and providing better

products to the customers, measurement of performance which increases efficiency of business

and hence leads to maximisation of profits. Below mentioned are few systems used in

management accounting:

Job costing Technique: It is a method wherein production costs of every product is allocated

with simultaneously keeping watch on the expenses incurred. Continental Clothing Company

Ltd. can make use of this method to calculate the costs related to every product can use this

Management Accounting is a technique used to analyse different costs and operational

aspects of the business and helps in preparation of financial statements, reporting and recording

different transactions which supports the managers in better decision making to achieve the

goals of the business. This method also helps in making decisions related to competition by

gathering information and processing them which helps top level in deciding he strategies of the

business and evaluate them on timely basis. In this study Continental Clothing Company Ltd.

which is UK's one of the largest manufacture of cloths and has a significant position in clothing

industry. The company has grown to become the world market leading designer and

manufacturer of cloths and offering customers wider range of quality clothing. In this report the

following topics are discussed in detail which includes various techniques used in reporting of

management accounting, methods of cost accounting which are used to make the profit and loss

statement, tools to plan for controlling the budget and the ways in which management accounting

helps in resolving monetary issues. (Angelone and Neopost, 2015).

LO 1

Management accounting and requirement of different types of management accounting systems

Any accounting that helps the corporations in working more effectively can be terms as

Management Accounting. As per one of the well-known institutes, if management accounting is

applied in the companies by the skilled professionals then it can help the top management in

formulating good strategies and policies which can be used for the smooth operations of the

business.

For Continental Clothing Company Ltd. management accounting systems help in analysing costs

associated with production of cloths, determining ways of reducing prices and providing better

products to the customers, measurement of performance which increases efficiency of business

and hence leads to maximisation of profits. Below mentioned are few systems used in

management accounting:

Job costing Technique: It is a method wherein production costs of every product is allocated

with simultaneously keeping watch on the expenses incurred. Continental Clothing Company

Ltd. can make use of this method to calculate the costs related to every product can use this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

system to determine the cost of each of its product that it offers to its clients according to their

needs and preferences. As there are lot of differences in the items that are produced, this method

needs a complete segregation of cost for every product and they are also recorded separately. It

gives details regarding the variable costs like direct material which are used. (Gupta, 2017).

Price optimising technique: This method is used to set optimal prices of all kind of products the

company offers. It helps in controlling the price level and also used to find out that what will be

the demand at each price point. Continental Clothing must use this method to set the prices

which are acceptable to different target customers and to see that how will they respond at each

price level. Company can also decide different structures related to pricing like pricing for

promotions, discounts and the market entry pricing. To decide the prices, company make use of

various factors like benchmarking the competitors, the product life cycle of the all the products

and the vision and objectives of the company as a whole.

Cost accounting technique: This method is used to determine the costs for the purpose of

analysis of the profitability of the business, valuation of its inventory and to control the overall

cost. There are two methods under this: Job and Process costing. The first one i.e. Job Costing

helps in identifying the production costs that are attached to each job in the case where the firms

have different products and different manufacturing for all. On the other side, process costs are

those that identify separate costs for every process and can be used where production go through

different processes. Continental Clothing Company Ltd. have an option to choose this method

they can identify the costs of customized products which are designed as per the requirements of

the clients. (Kaplan and Atkinson, 2015).

Inventory management technique: This method helps in the proper maintenance of stock level

and managing them. It helps in better management of inventory while focusing on procurement

and better inventory turnover. Continental Clothing Company Ltd. If uses this method, then they

can effectively manage all their stock levels, can replenish their raw materials on time and can

satisfy their consumers by proper availability of goods on the retail stores. It enables managing

officials to have a physical record of all inventories within the firm.

Different methods used for management accounting reporting

Companies can become extremely efficient and productive if they do proper reporting

and make management accounting reports. These reports can be used to do proper planning, in

needs and preferences. As there are lot of differences in the items that are produced, this method

needs a complete segregation of cost for every product and they are also recorded separately. It

gives details regarding the variable costs like direct material which are used. (Gupta, 2017).

Price optimising technique: This method is used to set optimal prices of all kind of products the

company offers. It helps in controlling the price level and also used to find out that what will be

the demand at each price point. Continental Clothing must use this method to set the prices

which are acceptable to different target customers and to see that how will they respond at each

price level. Company can also decide different structures related to pricing like pricing for

promotions, discounts and the market entry pricing. To decide the prices, company make use of

various factors like benchmarking the competitors, the product life cycle of the all the products

and the vision and objectives of the company as a whole.

Cost accounting technique: This method is used to determine the costs for the purpose of

analysis of the profitability of the business, valuation of its inventory and to control the overall

cost. There are two methods under this: Job and Process costing. The first one i.e. Job Costing

helps in identifying the production costs that are attached to each job in the case where the firms

have different products and different manufacturing for all. On the other side, process costs are

those that identify separate costs for every process and can be used where production go through

different processes. Continental Clothing Company Ltd. have an option to choose this method

they can identify the costs of customized products which are designed as per the requirements of

the clients. (Kaplan and Atkinson, 2015).

Inventory management technique: This method helps in the proper maintenance of stock level

and managing them. It helps in better management of inventory while focusing on procurement

and better inventory turnover. Continental Clothing Company Ltd. If uses this method, then they

can effectively manage all their stock levels, can replenish their raw materials on time and can

satisfy their consumers by proper availability of goods on the retail stores. It enables managing

officials to have a physical record of all inventories within the firm.

Different methods used for management accounting reporting

Companies can become extremely efficient and productive if they do proper reporting

and make management accounting reports. These reports can be used to do proper planning, in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

making regulations for the companies and to measure the performance both financially and

operationally. Through these reports, relevant figures and statistics are produced which make

decisions better and help in making better long-term strategies for the organization. This

information is important for internal users that help in making decision making for reducing

costs or directing funds in more beneficial product lines. Continental Clothing Company Ltd.

also prepare various reports that are discussed below:

Budget reports: To measure the performance of the organization, budget reports are very

important. A budget helps a company in forecasting the future sales and expenses which are

going to be incurred based on the historical trends of the companies. It is also helpful in

forecasting unusual circumstances. Budget helps the company in achieving the set targets and

goals set. This report supports Continental Clothing Company Ltd. To meet their revenue targets

in an efficient way. (Karadag, 2015).

Accounts receivable ageing reports: This report gives detail information about each and every

debtor of the organization. It also tells the accounts receivables turnover of the company and the

duration in which they are paying back to the company. Here, the company also gets to know

that whether there is a need to tighten the policies of collection and is very useful in monitoring

the doubtful debtors who keeps on extending the dates of payment. It also identifies the bad

debts of the company and helps in managing the liquidity position of the company. Continental

Clothing Company Ltd. Make use of this report to effectively manage its policies related to

accounts receivables which needs to be monitored on a regular basis.

Job cost report: This report mentions different costs related to every activity or job of the

organisation. This report analyses that which activity is less profitable and where the efforts of

the business can be reduced or eliminated. This also examines the costs related to each project

and the wastage if any is occurring in the project is identified so that project can become very

profitable. Continental Clothing Company Ltd. can use these reports to determine the best

pricing for the products and to decrease the costs for each product to generate revenues. (Maas,

Schaltegger and Crutzen, 2016).

Inventory and manufacturing reports: The main motive of this report is to make inventory

management better and production processes more worthy. The report contents include different

costs related to labour, overhead costs and the unnecessary wastages of stock. It also helps

operationally. Through these reports, relevant figures and statistics are produced which make

decisions better and help in making better long-term strategies for the organization. This

information is important for internal users that help in making decision making for reducing

costs or directing funds in more beneficial product lines. Continental Clothing Company Ltd.

also prepare various reports that are discussed below:

Budget reports: To measure the performance of the organization, budget reports are very

important. A budget helps a company in forecasting the future sales and expenses which are

going to be incurred based on the historical trends of the companies. It is also helpful in

forecasting unusual circumstances. Budget helps the company in achieving the set targets and

goals set. This report supports Continental Clothing Company Ltd. To meet their revenue targets

in an efficient way. (Karadag, 2015).

Accounts receivable ageing reports: This report gives detail information about each and every

debtor of the organization. It also tells the accounts receivables turnover of the company and the

duration in which they are paying back to the company. Here, the company also gets to know

that whether there is a need to tighten the policies of collection and is very useful in monitoring

the doubtful debtors who keeps on extending the dates of payment. It also identifies the bad

debts of the company and helps in managing the liquidity position of the company. Continental

Clothing Company Ltd. Make use of this report to effectively manage its policies related to

accounts receivables which needs to be monitored on a regular basis.

Job cost report: This report mentions different costs related to every activity or job of the

organisation. This report analyses that which activity is less profitable and where the efforts of

the business can be reduced or eliminated. This also examines the costs related to each project

and the wastage if any is occurring in the project is identified so that project can become very

profitable. Continental Clothing Company Ltd. can use these reports to determine the best

pricing for the products and to decrease the costs for each product to generate revenues. (Maas,

Schaltegger and Crutzen, 2016).

Inventory and manufacturing reports: The main motive of this report is to make inventory

management better and production processes more worthy. The report contents include different

costs related to labour, overhead costs and the unnecessary wastages of stock. It also helps

managers in comparing various manufacturing plants and where they are lacking so that

improvement can be done. This report can help Continental Clothing Company Ltd. for better

management of inventory levels of cloths with controlling manufacturing costs (Maas,

Schaltegger and Crutzen, 2016).

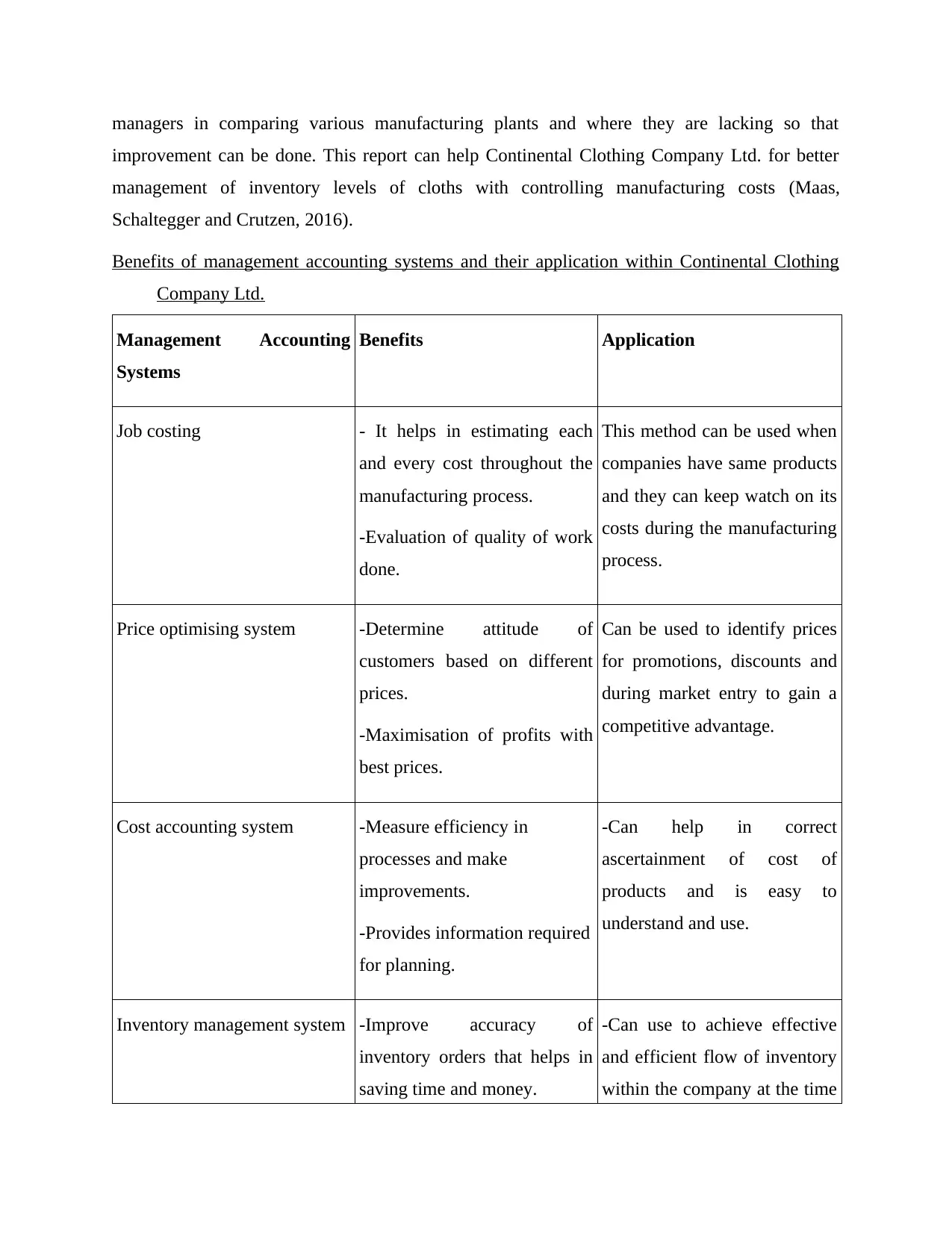

Benefits of management accounting systems and their application within Continental Clothing

Company Ltd.

Management Accounting

Systems

Benefits Application

Job costing - It helps in estimating each

and every cost throughout the

manufacturing process.

-Evaluation of quality of work

done.

This method can be used when

companies have same products

and they can keep watch on its

costs during the manufacturing

process.

Price optimising system -Determine attitude of

customers based on different

prices.

-Maximisation of profits with

best prices.

Can be used to identify prices

for promotions, discounts and

during market entry to gain a

competitive advantage.

Cost accounting system -Measure efficiency in

processes and make

improvements.

-Provides information required

for planning.

-Can help in correct

ascertainment of cost of

products and is easy to

understand and use.

Inventory management system -Improve accuracy of

inventory orders that helps in

saving time and money.

-Can use to achieve effective

and efficient flow of inventory

within the company at the time

improvement can be done. This report can help Continental Clothing Company Ltd. for better

management of inventory levels of cloths with controlling manufacturing costs (Maas,

Schaltegger and Crutzen, 2016).

Benefits of management accounting systems and their application within Continental Clothing

Company Ltd.

Management Accounting

Systems

Benefits Application

Job costing - It helps in estimating each

and every cost throughout the

manufacturing process.

-Evaluation of quality of work

done.

This method can be used when

companies have same products

and they can keep watch on its

costs during the manufacturing

process.

Price optimising system -Determine attitude of

customers based on different

prices.

-Maximisation of profits with

best prices.

Can be used to identify prices

for promotions, discounts and

during market entry to gain a

competitive advantage.

Cost accounting system -Measure efficiency in

processes and make

improvements.

-Provides information required

for planning.

-Can help in correct

ascertainment of cost of

products and is easy to

understand and use.

Inventory management system -Improve accuracy of

inventory orders that helps in

saving time and money.

-Can use to achieve effective

and efficient flow of inventory

within the company at the time

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of sale.

Evaluation of how management accounting systems and management accounting reporting is

integrated within organisational processes

The reports prepared in management accounting reflects the current order with the

company, sales revenue, cash in hand, other current assets like debtors or accounts receivable,

stock, current liabilities like accounts payable or creditors and outstanding debts. Some more

information about variance analysis and necessary statistical data are also there which enables

managers in better decision making. Continental Clothing Company Ltd prepare all these reports

for the strategic decisions. Job cost method is useful in making reports related to job costs which

includes calculation of costs, expenses and profitability of every activities happening in the

company. Cost accounting method is helpful in preparing budget report so as to analyse

company performance, control costs and determine actual expenditures incurred in past.

Inventory management system helps in preparing inventory and management report to determine

various costs related to labour, overhead costs and the unnecessary wastages of stock. Price

optimising system helps in determining strategies of pricing of different range of clothing based

on client's preference and need (Mack and Goretzki, 2017).

LO 2

Techniques of cost analysis to prepare an income statement using marginal and absorption costs

for Continental Clothing Company Ltd.

Costs reflects to value which has been put to produce goods and services. It includes all

those costs starting from the procurement of raw materials, labour used, the time and resources

utilised, other fixed and variable costs used to manufacture a product. There are two main

methods used in costing i.e. Absorption and Marginal or variable.

Marginal costing: Marginal costing refers to the method where all the variables costs are fixed

costs are treated separately and are segregated as per product and period costs respectively. Here,

segregation only happens based on variable and fixed and not on the basis of manufacturing and

non-manufacturing costs. It is an easy technique to estimate the costs and net profit and loss and

the changes due to change in the production level. (Maskell, Baggaley and Grasso, 2017).

Evaluation of how management accounting systems and management accounting reporting is

integrated within organisational processes

The reports prepared in management accounting reflects the current order with the

company, sales revenue, cash in hand, other current assets like debtors or accounts receivable,

stock, current liabilities like accounts payable or creditors and outstanding debts. Some more

information about variance analysis and necessary statistical data are also there which enables

managers in better decision making. Continental Clothing Company Ltd prepare all these reports

for the strategic decisions. Job cost method is useful in making reports related to job costs which

includes calculation of costs, expenses and profitability of every activities happening in the

company. Cost accounting method is helpful in preparing budget report so as to analyse

company performance, control costs and determine actual expenditures incurred in past.

Inventory management system helps in preparing inventory and management report to determine

various costs related to labour, overhead costs and the unnecessary wastages of stock. Price

optimising system helps in determining strategies of pricing of different range of clothing based

on client's preference and need (Mack and Goretzki, 2017).

LO 2

Techniques of cost analysis to prepare an income statement using marginal and absorption costs

for Continental Clothing Company Ltd.

Costs reflects to value which has been put to produce goods and services. It includes all

those costs starting from the procurement of raw materials, labour used, the time and resources

utilised, other fixed and variable costs used to manufacture a product. There are two main

methods used in costing i.e. Absorption and Marginal or variable.

Marginal costing: Marginal costing refers to the method where all the variables costs are fixed

costs are treated separately and are segregated as per product and period costs respectively. Here,

segregation only happens based on variable and fixed and not on the basis of manufacturing and

non-manufacturing costs. It is an easy technique to estimate the costs and net profit and loss and

the changes due to change in the production level. (Maskell, Baggaley and Grasso, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

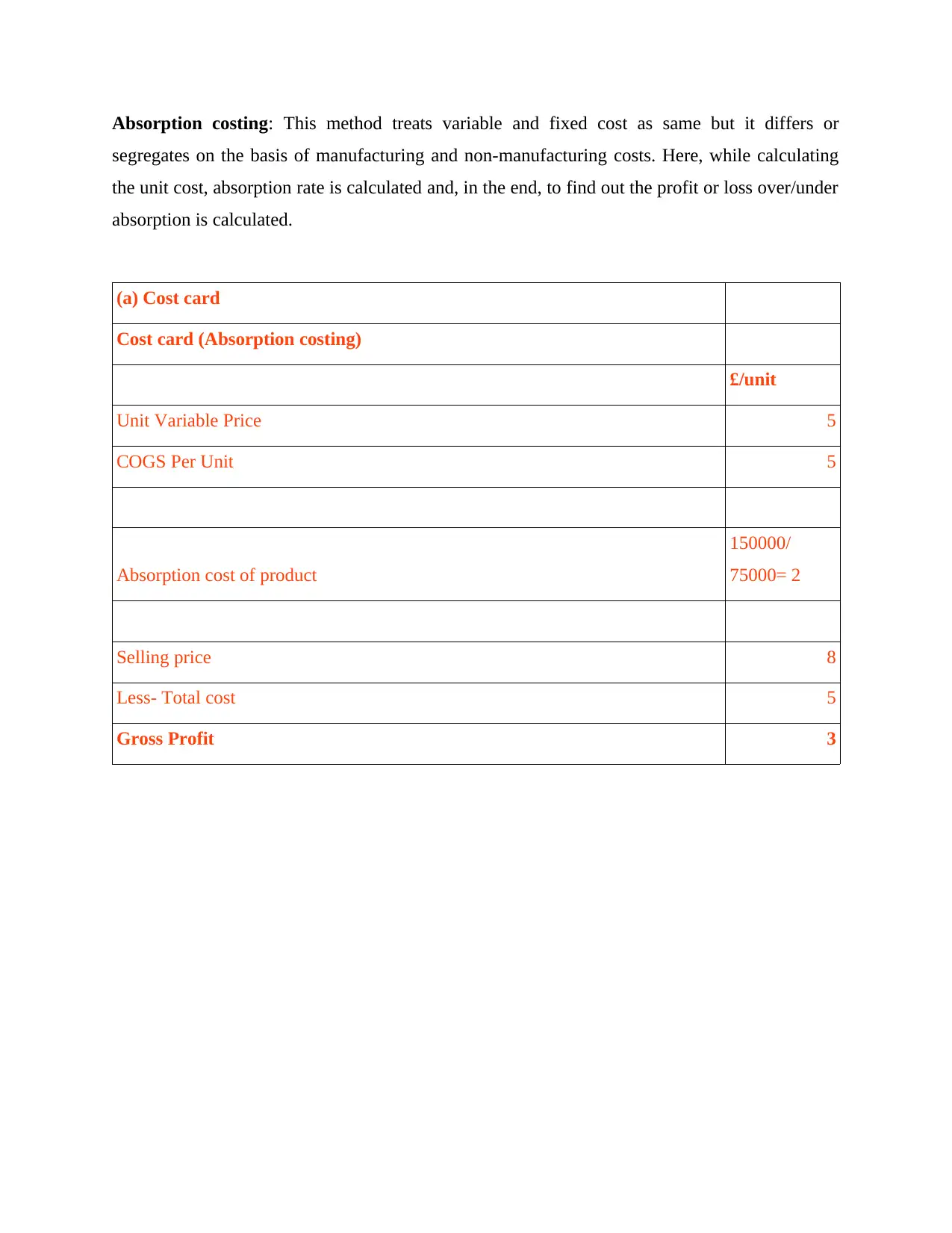

Absorption costing: This method treats variable and fixed cost as same but it differs or

segregates on the basis of manufacturing and non-manufacturing costs. Here, while calculating

the unit cost, absorption rate is calculated and, in the end, to find out the profit or loss over/under

absorption is calculated.

(a) Cost card

Cost card (Absorption costing)

£/unit

Unit Variable Price 5

COGS Per Unit 5

Absorption cost of product

150000/

75000= 2

Selling price 8

Less- Total cost 5

Gross Profit 3

segregates on the basis of manufacturing and non-manufacturing costs. Here, while calculating

the unit cost, absorption rate is calculated and, in the end, to find out the profit or loss over/under

absorption is calculated.

(a) Cost card

Cost card (Absorption costing)

£/unit

Unit Variable Price 5

COGS Per Unit 5

Absorption cost of product

150000/

75000= 2

Selling price 8

Less- Total cost 5

Gross Profit 3

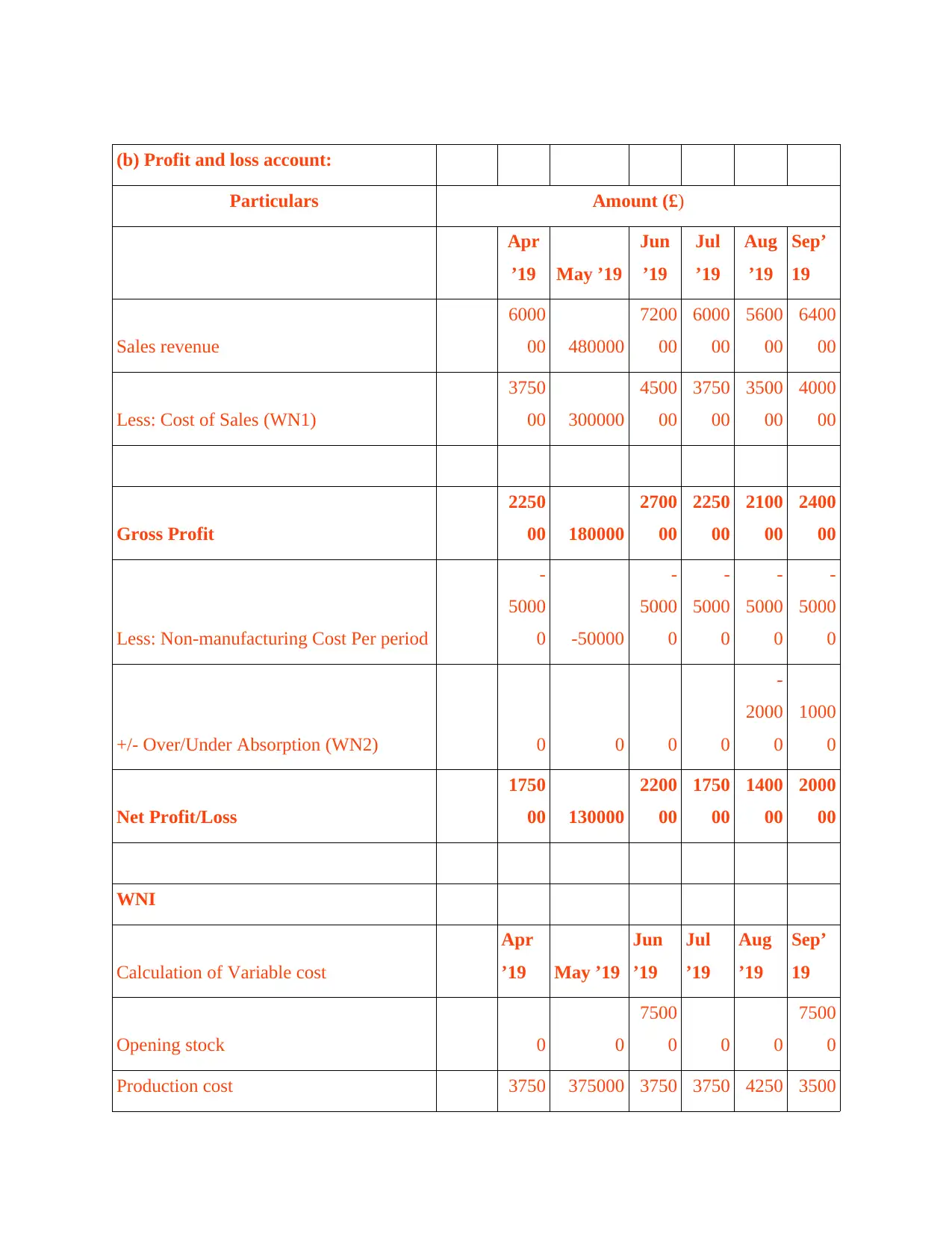

(b) Profit and loss account:

Particulars Amount (£)

Apr

’19 May ’19

Jun

’19

Jul

’19

Aug

’19

Sep’

19

Sales revenue

6000

00 480000

7200

00

6000

00

5600

00

6400

00

Less: Cost of Sales (WN1)

3750

00 300000

4500

00

3750

00

3500

00

4000

00

Gross Profit

2250

00 180000

2700

00

2250

00

2100

00

2400

00

Less: Non-manufacturing Cost Per period

-

5000

0 -50000

-

5000

0

-

5000

0

-

5000

0

-

5000

0

+/- Over/Under Absorption (WN2) 0 0 0 0

-

2000

0

1000

0

Net Profit/Loss

1750

00 130000

2200

00

1750

00

1400

00

2000

00

WNI

Calculation of Variable cost

Apr

’19 May ’19

Jun

’19

Jul

’19

Aug

’19

Sep’

19

Opening stock 0 0

7500

0 0 0

7500

0

Production cost 3750 375000 3750 3750 4250 3500

Particulars Amount (£)

Apr

’19 May ’19

Jun

’19

Jul

’19

Aug

’19

Sep’

19

Sales revenue

6000

00 480000

7200

00

6000

00

5600

00

6400

00

Less: Cost of Sales (WN1)

3750

00 300000

4500

00

3750

00

3500

00

4000

00

Gross Profit

2250

00 180000

2700

00

2250

00

2100

00

2400

00

Less: Non-manufacturing Cost Per period

-

5000

0 -50000

-

5000

0

-

5000

0

-

5000

0

-

5000

0

+/- Over/Under Absorption (WN2) 0 0 0 0

-

2000

0

1000

0

Net Profit/Loss

1750

00 130000

2200

00

1750

00

1400

00

2000

00

WNI

Calculation of Variable cost

Apr

’19 May ’19

Jun

’19

Jul

’19

Aug

’19

Sep’

19

Opening stock 0 0

7500

0 0 0

7500

0

Production cost 3750 375000 3750 3750 4250 3500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

00 00 00 00 00

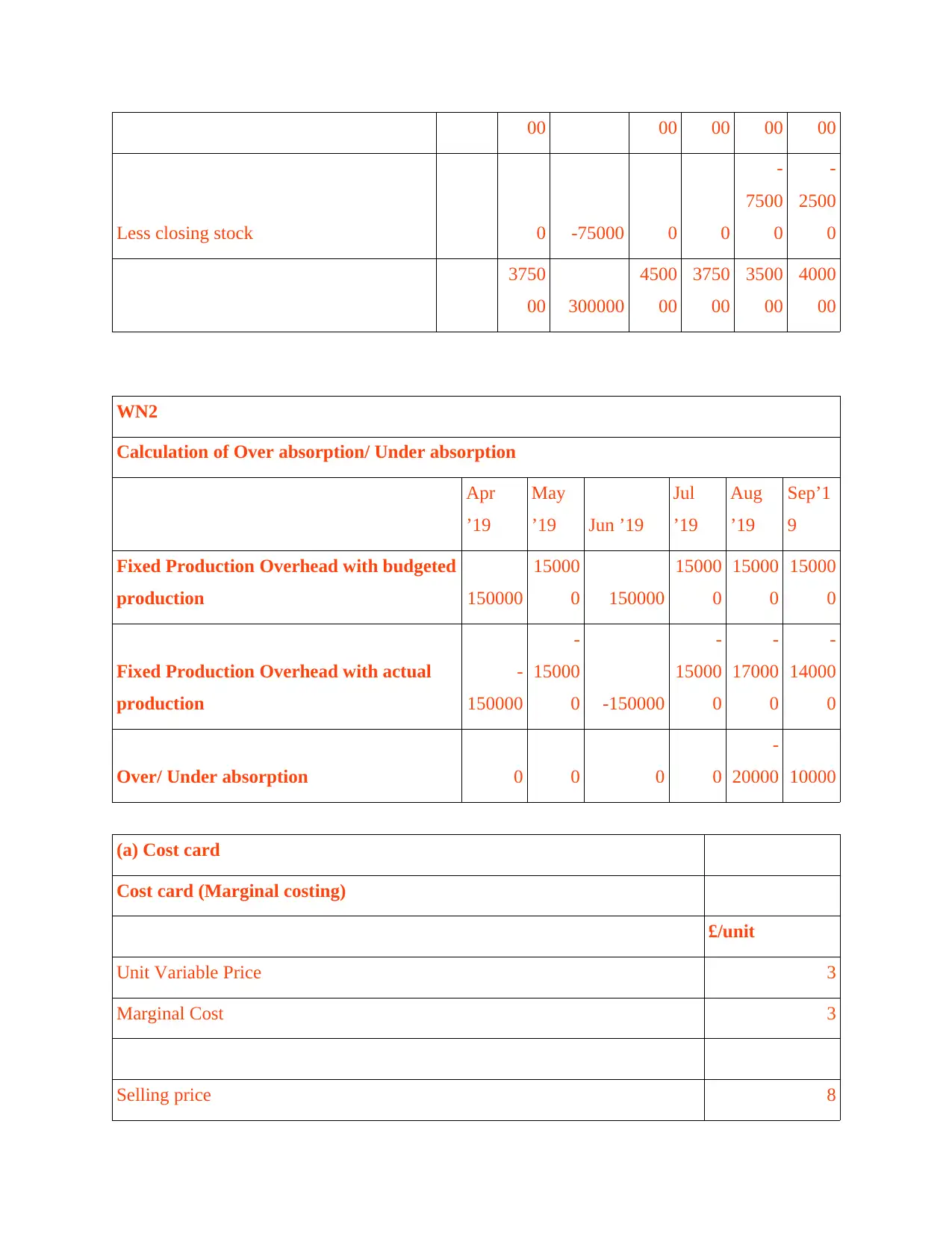

Less closing stock 0 -75000 0 0

-

7500

0

-

2500

0

3750

00 300000

4500

00

3750

00

3500

00

4000

00

WN2

Calculation of Over absorption/ Under absorption

Apr

’19

May

’19 Jun ’19

Jul

’19

Aug

’19

Sep’1

9

Fixed Production Overhead with budgeted

production 150000

15000

0 150000

15000

0

15000

0

15000

0

Fixed Production Overhead with actual

production

-

150000

-

15000

0 -150000

-

15000

0

-

17000

0

-

14000

0

Over/ Under absorption 0 0 0 0

-

20000 10000

(a) Cost card

Cost card (Marginal costing)

£/unit

Unit Variable Price 3

Marginal Cost 3

Selling price 8

Less closing stock 0 -75000 0 0

-

7500

0

-

2500

0

3750

00 300000

4500

00

3750

00

3500

00

4000

00

WN2

Calculation of Over absorption/ Under absorption

Apr

’19

May

’19 Jun ’19

Jul

’19

Aug

’19

Sep’1

9

Fixed Production Overhead with budgeted

production 150000

15000

0 150000

15000

0

15000

0

15000

0

Fixed Production Overhead with actual

production

-

150000

-

15000

0 -150000

-

15000

0

-

17000

0

-

14000

0

Over/ Under absorption 0 0 0 0

-

20000 10000

(a) Cost card

Cost card (Marginal costing)

£/unit

Unit Variable Price 3

Marginal Cost 3

Selling price 8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

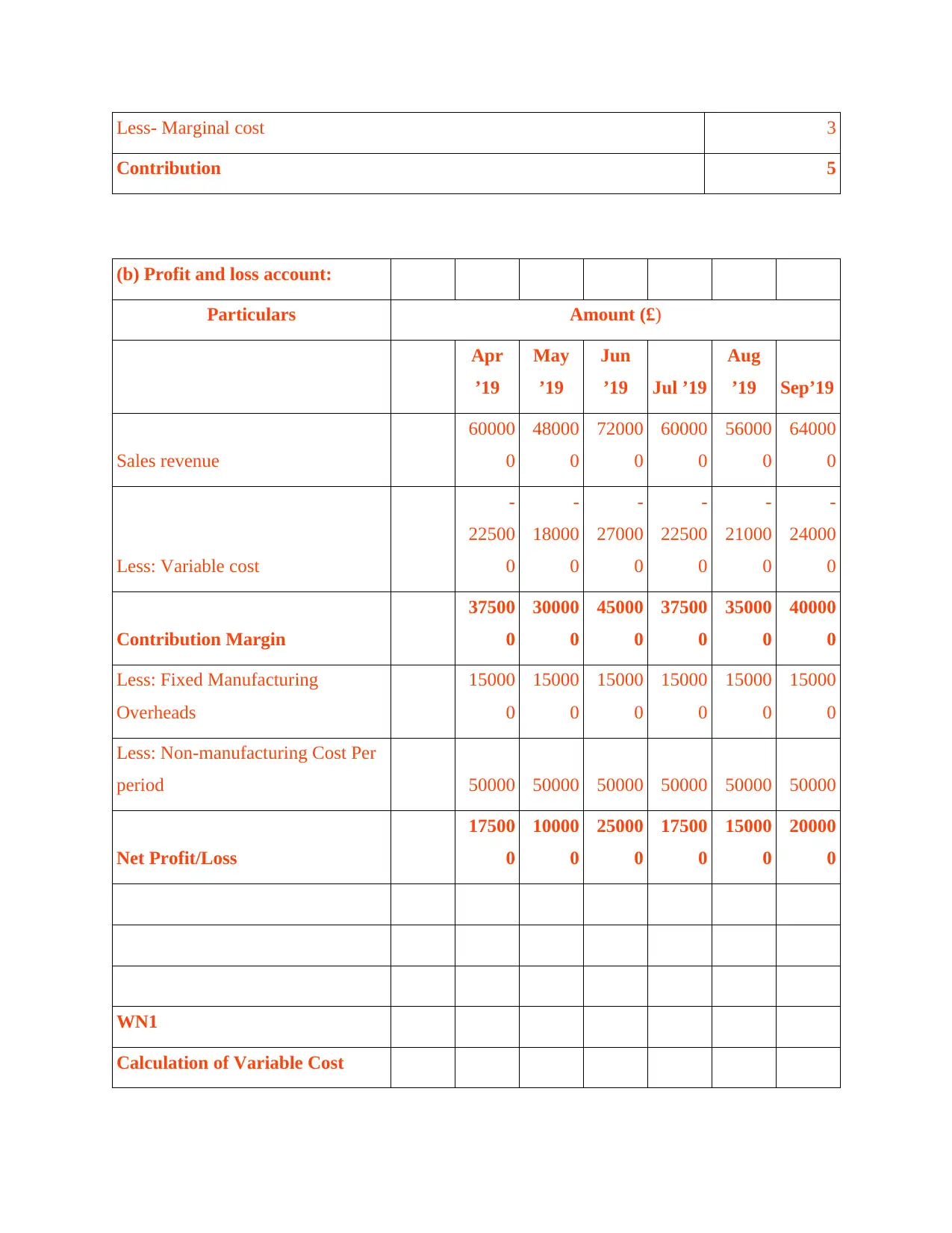

Less- Marginal cost 3

Contribution 5

(b) Profit and loss account:

Particulars Amount (£)

Apr

’19

May

’19

Jun

’19 Jul ’19

Aug

’19 Sep’19

Sales revenue

60000

0

48000

0

72000

0

60000

0

56000

0

64000

0

Less: Variable cost

-

22500

0

-

18000

0

-

27000

0

-

22500

0

-

21000

0

-

24000

0

Contribution Margin

37500

0

30000

0

45000

0

37500

0

35000

0

40000

0

Less: Fixed Manufacturing

Overheads

15000

0

15000

0

15000

0

15000

0

15000

0

15000

0

Less: Non-manufacturing Cost Per

period 50000 50000 50000 50000 50000 50000

Net Profit/Loss

17500

0

10000

0

25000

0

17500

0

15000

0

20000

0

WN1

Calculation of Variable Cost

Contribution 5

(b) Profit and loss account:

Particulars Amount (£)

Apr

’19

May

’19

Jun

’19 Jul ’19

Aug

’19 Sep’19

Sales revenue

60000

0

48000

0

72000

0

60000

0

56000

0

64000

0

Less: Variable cost

-

22500

0

-

18000

0

-

27000

0

-

22500

0

-

21000

0

-

24000

0

Contribution Margin

37500

0

30000

0

45000

0

37500

0

35000

0

40000

0

Less: Fixed Manufacturing

Overheads

15000

0

15000

0

15000

0

15000

0

15000

0

15000

0

Less: Non-manufacturing Cost Per

period 50000 50000 50000 50000 50000 50000

Net Profit/Loss

17500

0

10000

0

25000

0

17500

0

15000

0

20000

0

WN1

Calculation of Variable Cost

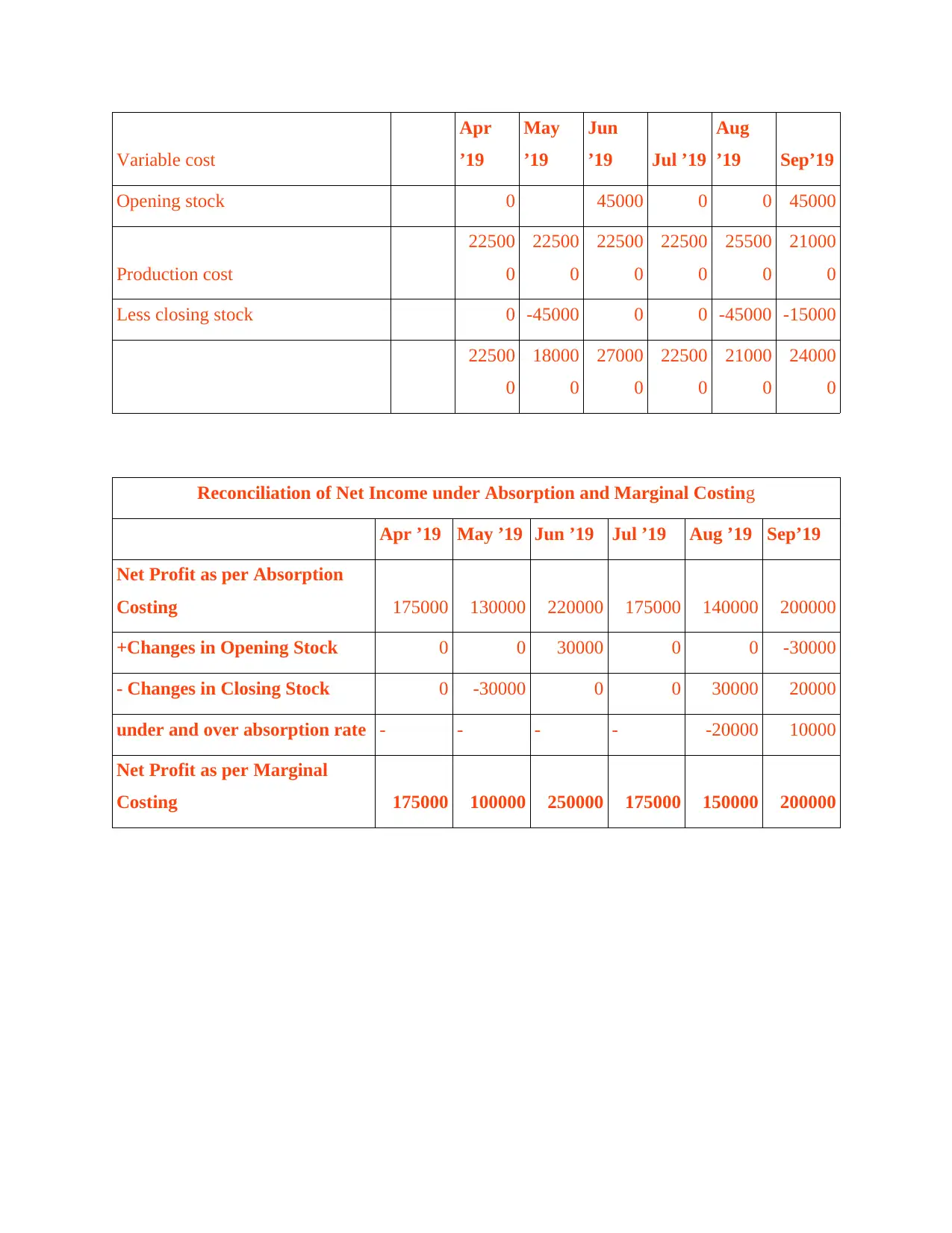

Variable cost

Apr

’19

May

’19

Jun

’19 Jul ’19

Aug

’19 Sep’19

Opening stock 0 45000 0 0 45000

Production cost

22500

0

22500

0

22500

0

22500

0

25500

0

21000

0

Less closing stock 0 -45000 0 0 -45000 -15000

22500

0

18000

0

27000

0

22500

0

21000

0

24000

0

Reconciliation of Net Income under Absorption and Marginal Costing

Apr ’19 May ’19 Jun ’19 Jul ’19 Aug ’19 Sep’19

Net Profit as per Absorption

Costing 175000 130000 220000 175000 140000 200000

+Changes in Opening Stock 0 0 30000 0 0 -30000

- Changes in Closing Stock 0 -30000 0 0 30000 20000

under and over absorption rate - - - - -20000 10000

Net Profit as per Marginal

Costing 175000 100000 250000 175000 150000 200000

Apr

’19

May

’19

Jun

’19 Jul ’19

Aug

’19 Sep’19

Opening stock 0 45000 0 0 45000

Production cost

22500

0

22500

0

22500

0

22500

0

25500

0

21000

0

Less closing stock 0 -45000 0 0 -45000 -15000

22500

0

18000

0

27000

0

22500

0

21000

0

24000

0

Reconciliation of Net Income under Absorption and Marginal Costing

Apr ’19 May ’19 Jun ’19 Jul ’19 Aug ’19 Sep’19

Net Profit as per Absorption

Costing 175000 130000 220000 175000 140000 200000

+Changes in Opening Stock 0 0 30000 0 0 -30000

- Changes in Closing Stock 0 -30000 0 0 30000 20000

under and over absorption rate - - - - -20000 10000

Net Profit as per Marginal

Costing 175000 100000 250000 175000 150000 200000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.