Management Accounting Report: Analysis of Cambridge Manufacturing Ltd.

VerifiedAdded on 2021/02/19

|21

|4783

|303

Report

AI Summary

This report delves into the realm of management accounting, also known as cost or managerial accounting, and its crucial role in analyzing business costs and operations. Focusing on Cambridge Manufacturing Ltd., a medium-scale organization, the report examines various management accounting systems, including price optimization, inventory management, and cost accounting systems. It explores different types of management accounting reports, such as cost managerial accounting reports, aging reports, budget reports, and performance reports, highlighting their importance in decision-making. Furthermore, the report discusses the benefits and applications of these systems, providing critical evaluations of various reporting and accounting methods. It also addresses cost calculation techniques, including marginal and absorption costing, and explores planning tools used in budgetary control, along with strategies to overcome financial issues. The report concludes with a comprehensive analysis of the role of management accounting in achieving sustainable success in addressing financial problems.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting system and their essential requirement..........................................1

P2 Type of management accounting reports and its importance to management.......................3

M1 Benefits and application of management accounting system...............................................4

D1 Critical evaluation of various reporting and accounting system............................................5

TASK 2............................................................................................................................................5

P3 Calculation of cost by using appropriate technique...............................................................5

M2 Type of accounting techniques............................................................................................10

D2 Data interpretation...............................................................................................................10

TASK 3..........................................................................................................................................10

P4 Merits and Demerits of using planning tools used in budgetary control..............................10

M3 Different planning tools and their applications...................................................................12

TASK 4..........................................................................................................................................12

P5 Comparison with other organisation to overcome financial issues......................................12

M4 Management accounting can lead organisation to sustainable success in responding

financial problems.....................................................................................................................14

D3 Planning respond appropriately to resolve financial problem.............................................15

CONCLUSION..............................................................................................................................15

REFRENCES.................................................................................................................................17

TASK 1............................................................................................................................................1

P1 Management accounting system and their essential requirement..........................................1

P2 Type of management accounting reports and its importance to management.......................3

M1 Benefits and application of management accounting system...............................................4

D1 Critical evaluation of various reporting and accounting system............................................5

TASK 2............................................................................................................................................5

P3 Calculation of cost by using appropriate technique...............................................................5

M2 Type of accounting techniques............................................................................................10

D2 Data interpretation...............................................................................................................10

TASK 3..........................................................................................................................................10

P4 Merits and Demerits of using planning tools used in budgetary control..............................10

M3 Different planning tools and their applications...................................................................12

TASK 4..........................................................................................................................................12

P5 Comparison with other organisation to overcome financial issues......................................12

M4 Management accounting can lead organisation to sustainable success in responding

financial problems.....................................................................................................................14

D3 Planning respond appropriately to resolve financial problem.............................................15

CONCLUSION..............................................................................................................................15

REFRENCES.................................................................................................................................17

INTRODUCTION

Management accounting is also known as cost accounting as well as managerial

accounting. It is the procedure utilise for analysing business cost or operations for preparing

internal financial report and account which help manager within decision making process for

accomplishing business goals. Management accounting help in conducting business activities

within effective manner like planning, organising, staffing, directing and controlling. For

understanding this overall concept medium scale organisation which is named as Cambridge

manufacturing Ltd. This organisation manufacture variety of specialist dietary products as well

as offers nutritional assurance. Respective manufacturing organisation conduct its operation

within United Kingdom. This report will going help in understanding concept of management

accounting, type and their requirement in organisation. Along with this, calculation of cost

through suitable technique has been done and various type of accounting technique will discuss.

Furthermore, merits and demerits of using planning tools in budgetary control will explain as

well majors to overcome financial issues.

TASK 1

P1 Management accounting system and their essential requirement

Management accounting system is related to collecting, analysing and presenting

monetary as well as non-monetary information to its end user according to requirement. It is

Management accounting is also known as cost accounting as well as managerial

accounting. It is the procedure utilise for analysing business cost or operations for preparing

internal financial report and account which help manager within decision making process for

accomplishing business goals. Management accounting help in conducting business activities

within effective manner like planning, organising, staffing, directing and controlling. For

understanding this overall concept medium scale organisation which is named as Cambridge

manufacturing Ltd. This organisation manufacture variety of specialist dietary products as well

as offers nutritional assurance. Respective manufacturing organisation conduct its operation

within United Kingdom. This report will going help in understanding concept of management

accounting, type and their requirement in organisation. Along with this, calculation of cost

through suitable technique has been done and various type of accounting technique will discuss.

Furthermore, merits and demerits of using planning tools in budgetary control will explain as

well majors to overcome financial issues.

TASK 1

P1 Management accounting system and their essential requirement

Management accounting system is related to collecting, analysing and presenting

monetary as well as non-monetary information to its end user according to requirement. It is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

crucial part of an organisation because it is implemented in internal system for controlling

organisational activities within proper manner. This system help in keeping financial record and

help in making effective accounts. There are different type of management accounting system

which help in growth of company as well as in building market image.

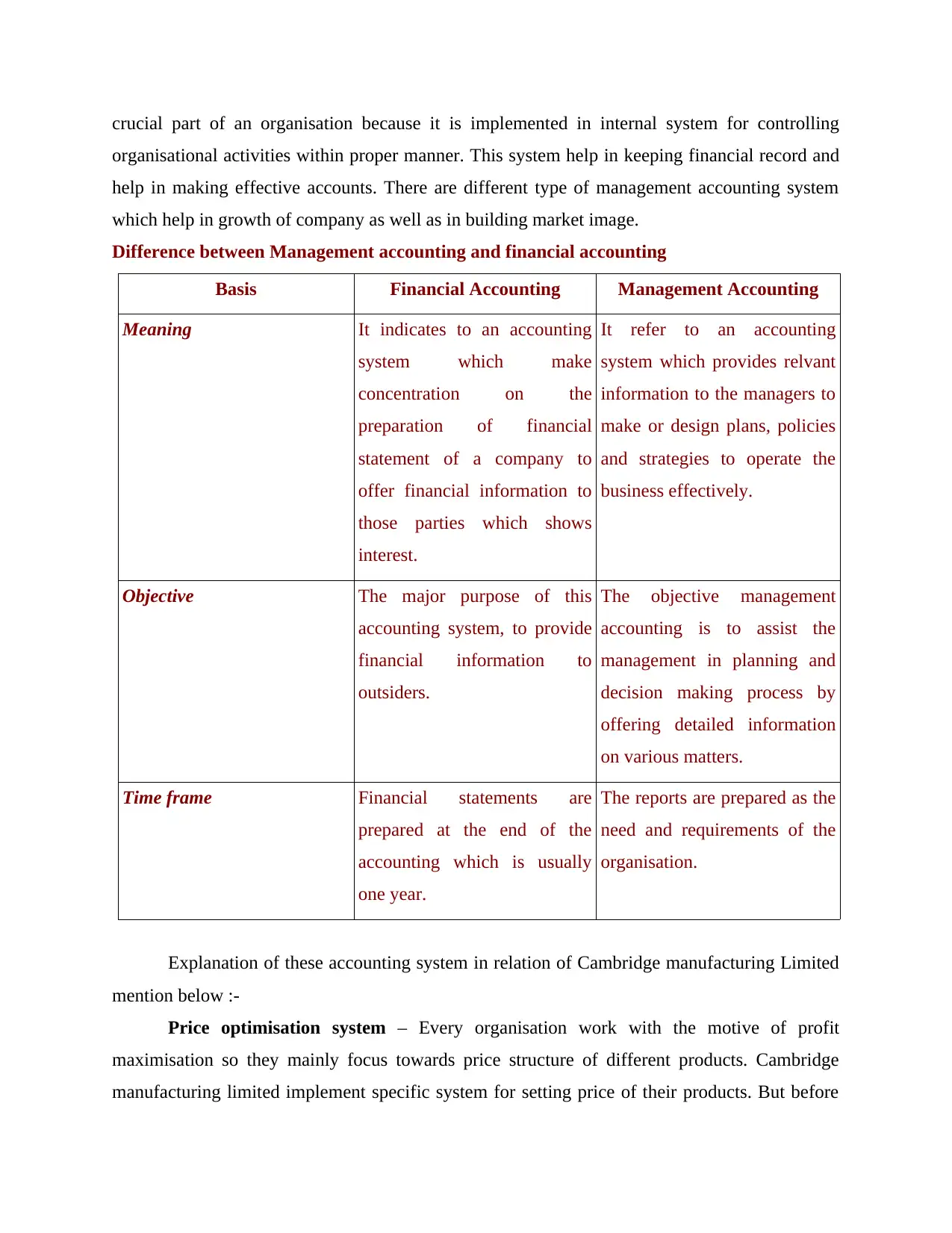

Difference between Management accounting and financial accounting

Basis Financial Accounting Management Accounting

Meaning It indicates to an accounting

system which make

concentration on the

preparation of financial

statement of a company to

offer financial information to

those parties which shows

interest.

It refer to an accounting

system which provides relvant

information to the managers to

make or design plans, policies

and strategies to operate the

business effectively.

Objective The major purpose of this

accounting system, to provide

financial information to

outsiders.

The objective management

accounting is to assist the

management in planning and

decision making process by

offering detailed information

on various matters.

Time frame Financial statements are

prepared at the end of the

accounting which is usually

one year.

The reports are prepared as the

need and requirements of the

organisation.

Explanation of these accounting system in relation of Cambridge manufacturing Limited

mention below :-

Price optimisation system – Every organisation work with the motive of profit

maximisation so they mainly focus towards price structure of different products. Cambridge

manufacturing limited implement specific system for setting price of their products. But before

organisational activities within proper manner. This system help in keeping financial record and

help in making effective accounts. There are different type of management accounting system

which help in growth of company as well as in building market image.

Difference between Management accounting and financial accounting

Basis Financial Accounting Management Accounting

Meaning It indicates to an accounting

system which make

concentration on the

preparation of financial

statement of a company to

offer financial information to

those parties which shows

interest.

It refer to an accounting

system which provides relvant

information to the managers to

make or design plans, policies

and strategies to operate the

business effectively.

Objective The major purpose of this

accounting system, to provide

financial information to

outsiders.

The objective management

accounting is to assist the

management in planning and

decision making process by

offering detailed information

on various matters.

Time frame Financial statements are

prepared at the end of the

accounting which is usually

one year.

The reports are prepared as the

need and requirements of the

organisation.

Explanation of these accounting system in relation of Cambridge manufacturing Limited

mention below :-

Price optimisation system – Every organisation work with the motive of profit

maximisation so they mainly focus towards price structure of different products. Cambridge

manufacturing limited implement specific system for setting price of their products. But before

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

setting price of offering company conduct market research for identifying perception of

customers related to particular product and services. The main requirement of this system to

Cambridge manufacturing Ltd is about ascertainment of the price in respect of the demands they

have in market.

Inventory management system - The particular system major part of manufacturing

company to track record and manage stocks within organisation. Mainly manufacturing

organisation can use inventory management system for keeping proper records analysis of stock

on every production level. This method can assist respective manufacturing company within

their activities as well as assist in identifying need of material at different level. This system will

help an organisation to manage their inventory and achieve better better outcomes within given

time period. Respective method will be advantageous for business firm in maintaining proper

stock within proper manner and use resources in production procedure. As a result it can reduce

wastages and help to place next order of goods and services. There are various techniques of

inventory explanation of these are as follows :-

LIFO – As per this method stock which come last will goes out first. Thus, LIFO is

simply last in first out.

FIFO – There are stock coming first and sale out first. Thus, it depends that in FIFO

method first in first out take place.

AVOC – It is calculating cost of inventory on average basis.

Cost accounting system – This accounting system gives direction to organisation by

concentrating on cost and increasing profitability. Cost accounting system involve systematic set

of activities such as understanding, analysing, entering, summarizing cost of goods as well as

services. In relation of Cambridge manufacturing Ltd implement specific system for analysing

variance by comparing within actual as well as estimated cost. Cost accounting system is

generally utilise by Cambridge manufacturing Ltd with the motive of improving their production

level as well as profitability.

Job costing system – This is kind of accounting system which help in analysing

expenditure which occur for particular job. With the assistance of job accounting system detail

information related to cost will be gained which is connected to accounting period. In respective

Cambridge manufacturing Ltd, this costing system is implemented for gaining knowledge about

customers related to particular product and services. The main requirement of this system to

Cambridge manufacturing Ltd is about ascertainment of the price in respect of the demands they

have in market.

Inventory management system - The particular system major part of manufacturing

company to track record and manage stocks within organisation. Mainly manufacturing

organisation can use inventory management system for keeping proper records analysis of stock

on every production level. This method can assist respective manufacturing company within

their activities as well as assist in identifying need of material at different level. This system will

help an organisation to manage their inventory and achieve better better outcomes within given

time period. Respective method will be advantageous for business firm in maintaining proper

stock within proper manner and use resources in production procedure. As a result it can reduce

wastages and help to place next order of goods and services. There are various techniques of

inventory explanation of these are as follows :-

LIFO – As per this method stock which come last will goes out first. Thus, LIFO is

simply last in first out.

FIFO – There are stock coming first and sale out first. Thus, it depends that in FIFO

method first in first out take place.

AVOC – It is calculating cost of inventory on average basis.

Cost accounting system – This accounting system gives direction to organisation by

concentrating on cost and increasing profitability. Cost accounting system involve systematic set

of activities such as understanding, analysing, entering, summarizing cost of goods as well as

services. In relation of Cambridge manufacturing Ltd implement specific system for analysing

variance by comparing within actual as well as estimated cost. Cost accounting system is

generally utilise by Cambridge manufacturing Ltd with the motive of improving their production

level as well as profitability.

Job costing system – This is kind of accounting system which help in analysing

expenditure which occur for particular job. With the assistance of job accounting system detail

information related to cost will be gained which is connected to accounting period. In respective

Cambridge manufacturing Ltd, this costing system is implemented for gaining knowledge about

various assigned job. There are several information which gained through job costing system are

as follows :-

Direct material – It is part of variable cost that is related to the production unit as well as

track cost of material within particular job.

Direct labour – In this cost of labour will be track related to specific job and also involve

time card and time sheet.

Overhead - At the end of every accounting period the total amount of each cost to apply

methodology regarding to allocation.

P2 Type of management accounting reports and its importance to management

There are different type of management accounting report which will be use by

Cambridge Manufacturing Limited for keeping record of every transactions. Management

accounting report will help in taking better decision on the basis of provided information which

help in generating profit for business firm in future. Explanation of these reporting system are

mention below :-

Cost managerial accounting report – This type of report is design for identifying cost

of amount spent on manufacturing process. Respective reporting system will give full

detail related to amount invested for conducting business activities. Cambridge

manufacturing Ltd. Have to prepare cost managerial accounting report because it help in

controlling cost which affect profitability of company as well as also help in

understanding actual expenditure. So that, optimum utilisation of available resources

method will be use in company.

Account receivable ageing reports – It is most important tool which help in managing

organisational activities as well account receivable ageing report shows amount which

customer have to pay company. Respective report help Cambridge manufacturing Ltd. In

identifying that finance division is collecting receivable slowly as well as credit policies

also.

Budget report – Motive behind designing this report is to compare actual budget with

its estimated. Financial data of an organisation are recorded within budget report which

is prepared by expertise. It also assist in identifying level of expenditure within an

organisation. Cambridge manufacturing limited prepare budget report foe ensuring that

as follows :-

Direct material – It is part of variable cost that is related to the production unit as well as

track cost of material within particular job.

Direct labour – In this cost of labour will be track related to specific job and also involve

time card and time sheet.

Overhead - At the end of every accounting period the total amount of each cost to apply

methodology regarding to allocation.

P2 Type of management accounting reports and its importance to management

There are different type of management accounting report which will be use by

Cambridge Manufacturing Limited for keeping record of every transactions. Management

accounting report will help in taking better decision on the basis of provided information which

help in generating profit for business firm in future. Explanation of these reporting system are

mention below :-

Cost managerial accounting report – This type of report is design for identifying cost

of amount spent on manufacturing process. Respective reporting system will give full

detail related to amount invested for conducting business activities. Cambridge

manufacturing Ltd. Have to prepare cost managerial accounting report because it help in

controlling cost which affect profitability of company as well as also help in

understanding actual expenditure. So that, optimum utilisation of available resources

method will be use in company.

Account receivable ageing reports – It is most important tool which help in managing

organisational activities as well account receivable ageing report shows amount which

customer have to pay company. Respective report help Cambridge manufacturing Ltd. In

identifying that finance division is collecting receivable slowly as well as credit policies

also.

Budget report – Motive behind designing this report is to compare actual budget with

its estimated. Financial data of an organisation are recorded within budget report which

is prepared by expertise. It also assist in identifying level of expenditure within an

organisation. Cambridge manufacturing limited prepare budget report foe ensuring that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

resources are allocated within proper manner as well it help in reducing operational cost

and assist in determining availability of sufficient funds.

Performance report – This report is design on the performance of any particular

activity and help in measuring, evaluating as well as analysing performance of company

and staff members. Performance report help in identifying difference between actual and

standard performance of Cambridge manufacturing limited and also staff working with

them. In addition to this, respective business firm have to make performance report on

regular basis so that present performance will be identified, future forecast will be

conducted as well as difference within actual and baseline will be fined.

M1 Benefits and application of management accounting system

There are several management accounting system which play important role in every type

of business firm. Thus, Cambridge manufacturing Ltd. Will implement several type of

accounting system within their working which are advantageous for them as well as client also.

Advantages of accounting system are as follows :-

Type of accounting system Benefits

Inventory management system This accounting system is beneficial

for organisation because it help in

identifying how much inventory

exactly required for conducting work.

Inventory management system will

assist Cambridge manufacturing in

proper planning and also in tracking

inventory.

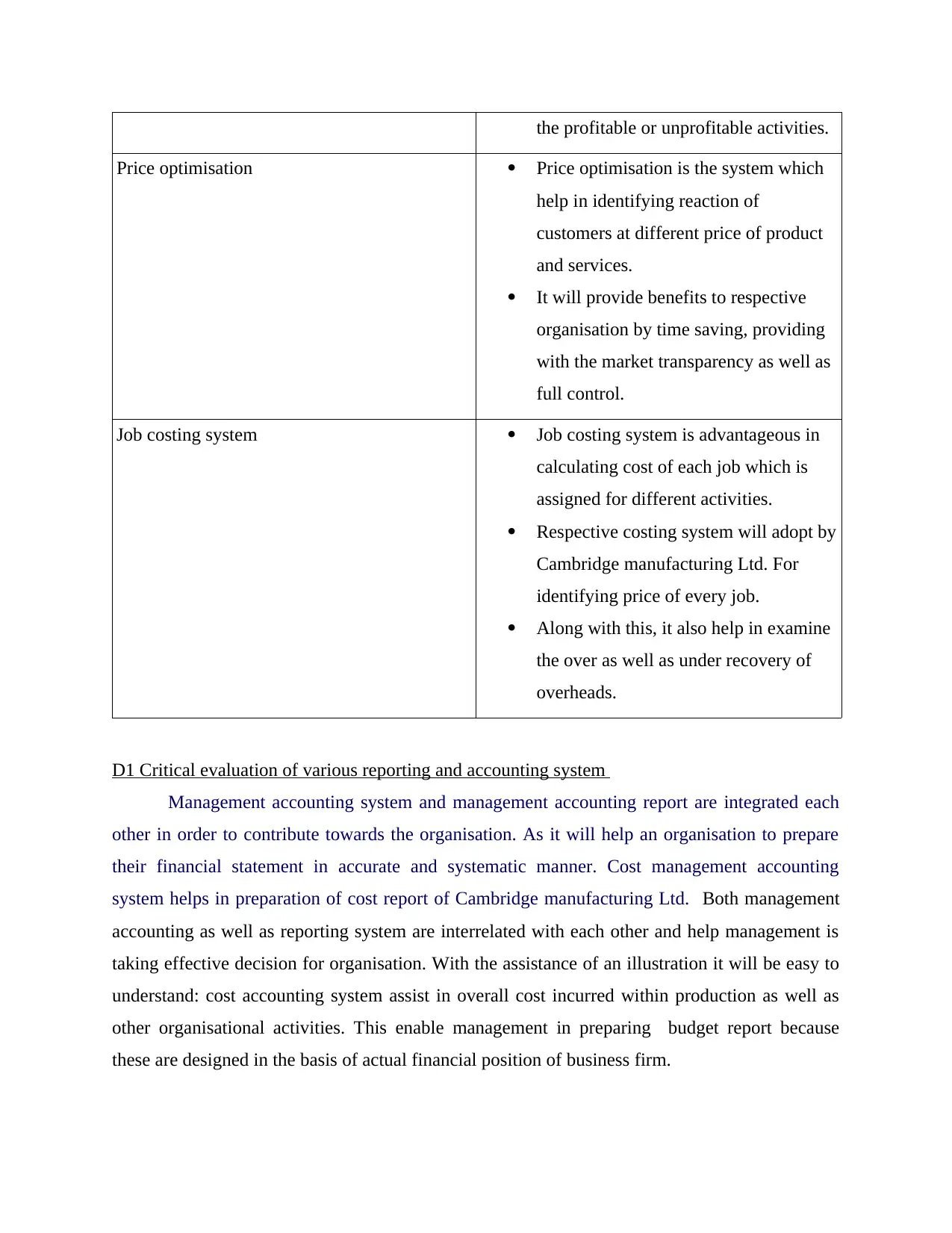

Cost accounting system Cost accounting system help

calculating overall cost of various

operations as well as activities.

Along with this, respective accounting

system will assist Cambridge

manufacturing Ltd. in fixation of prices,

decreasing prices as well as in identify

and assist in determining availability of sufficient funds.

Performance report – This report is design on the performance of any particular

activity and help in measuring, evaluating as well as analysing performance of company

and staff members. Performance report help in identifying difference between actual and

standard performance of Cambridge manufacturing limited and also staff working with

them. In addition to this, respective business firm have to make performance report on

regular basis so that present performance will be identified, future forecast will be

conducted as well as difference within actual and baseline will be fined.

M1 Benefits and application of management accounting system

There are several management accounting system which play important role in every type

of business firm. Thus, Cambridge manufacturing Ltd. Will implement several type of

accounting system within their working which are advantageous for them as well as client also.

Advantages of accounting system are as follows :-

Type of accounting system Benefits

Inventory management system This accounting system is beneficial

for organisation because it help in

identifying how much inventory

exactly required for conducting work.

Inventory management system will

assist Cambridge manufacturing in

proper planning and also in tracking

inventory.

Cost accounting system Cost accounting system help

calculating overall cost of various

operations as well as activities.

Along with this, respective accounting

system will assist Cambridge

manufacturing Ltd. in fixation of prices,

decreasing prices as well as in identify

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the profitable or unprofitable activities.

Price optimisation Price optimisation is the system which

help in identifying reaction of

customers at different price of product

and services.

It will provide benefits to respective

organisation by time saving, providing

with the market transparency as well as

full control.

Job costing system Job costing system is advantageous in

calculating cost of each job which is

assigned for different activities.

Respective costing system will adopt by

Cambridge manufacturing Ltd. For

identifying price of every job.

Along with this, it also help in examine

the over as well as under recovery of

overheads.

D1 Critical evaluation of various reporting and accounting system

Management accounting system and management accounting report are integrated each

other in order to contribute towards the organisation. As it will help an organisation to prepare

their financial statement in accurate and systematic manner. Cost management accounting

system helps in preparation of cost report of Cambridge manufacturing Ltd. Both management

accounting as well as reporting system are interrelated with each other and help management is

taking effective decision for organisation. With the assistance of an illustration it will be easy to

understand: cost accounting system assist in overall cost incurred within production as well as

other organisational activities. This enable management in preparing budget report because

these are designed in the basis of actual financial position of business firm.

Price optimisation Price optimisation is the system which

help in identifying reaction of

customers at different price of product

and services.

It will provide benefits to respective

organisation by time saving, providing

with the market transparency as well as

full control.

Job costing system Job costing system is advantageous in

calculating cost of each job which is

assigned for different activities.

Respective costing system will adopt by

Cambridge manufacturing Ltd. For

identifying price of every job.

Along with this, it also help in examine

the over as well as under recovery of

overheads.

D1 Critical evaluation of various reporting and accounting system

Management accounting system and management accounting report are integrated each

other in order to contribute towards the organisation. As it will help an organisation to prepare

their financial statement in accurate and systematic manner. Cost management accounting

system helps in preparation of cost report of Cambridge manufacturing Ltd. Both management

accounting as well as reporting system are interrelated with each other and help management is

taking effective decision for organisation. With the assistance of an illustration it will be easy to

understand: cost accounting system assist in overall cost incurred within production as well as

other organisational activities. This enable management in preparing budget report because

these are designed in the basis of actual financial position of business firm.

TASK 2

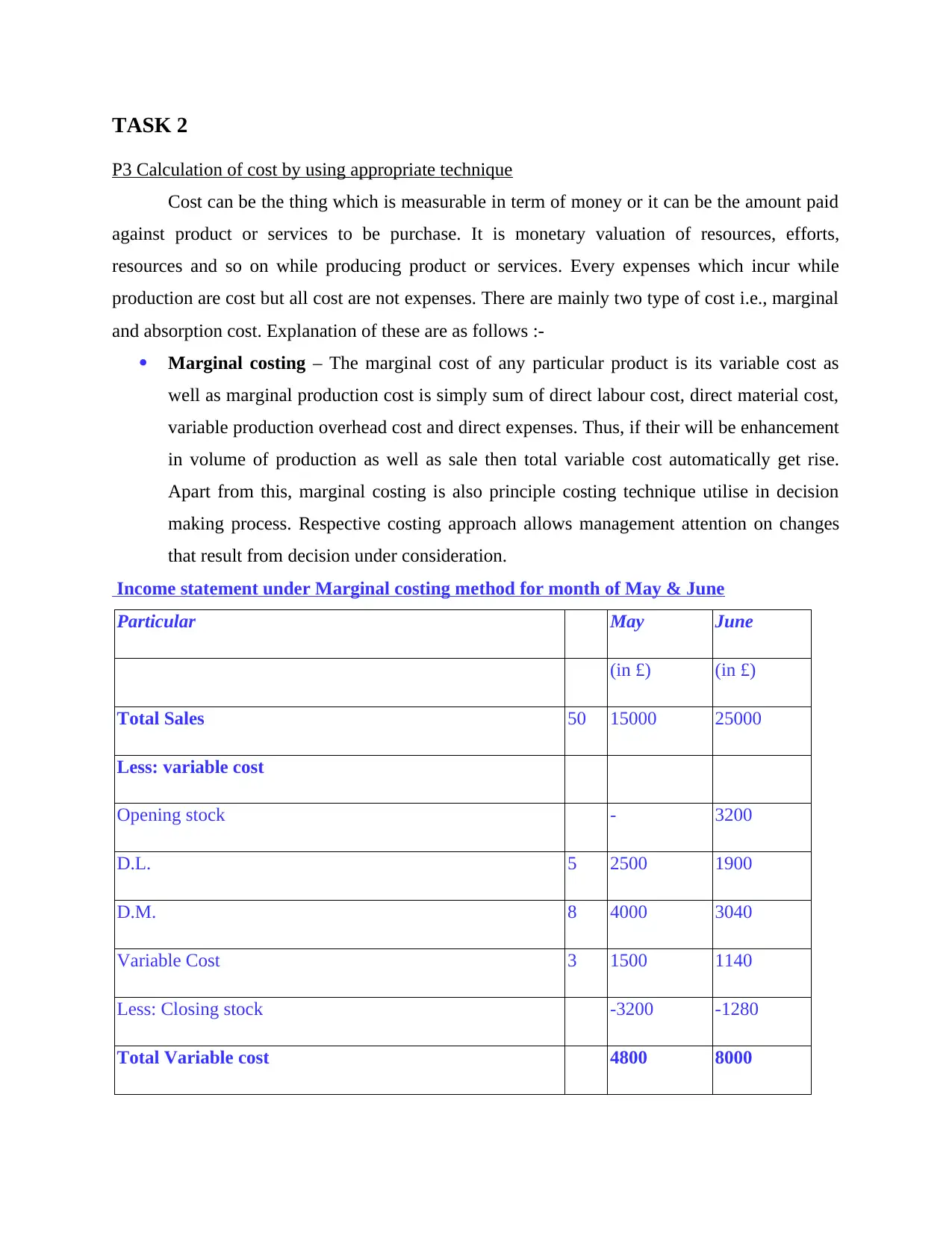

P3 Calculation of cost by using appropriate technique

Cost can be the thing which is measurable in term of money or it can be the amount paid

against product or services to be purchase. It is monetary valuation of resources, efforts,

resources and so on while producing product or services. Every expenses which incur while

production are cost but all cost are not expenses. There are mainly two type of cost i.e., marginal

and absorption cost. Explanation of these are as follows :-

Marginal costing – The marginal cost of any particular product is its variable cost as

well as marginal production cost is simply sum of direct labour cost, direct material cost,

variable production overhead cost and direct expenses. Thus, if their will be enhancement

in volume of production as well as sale then total variable cost automatically get rise.

Apart from this, marginal costing is also principle costing technique utilise in decision

making process. Respective costing approach allows management attention on changes

that result from decision under consideration.

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

P3 Calculation of cost by using appropriate technique

Cost can be the thing which is measurable in term of money or it can be the amount paid

against product or services to be purchase. It is monetary valuation of resources, efforts,

resources and so on while producing product or services. Every expenses which incur while

production are cost but all cost are not expenses. There are mainly two type of cost i.e., marginal

and absorption cost. Explanation of these are as follows :-

Marginal costing – The marginal cost of any particular product is its variable cost as

well as marginal production cost is simply sum of direct labour cost, direct material cost,

variable production overhead cost and direct expenses. Thus, if their will be enhancement

in volume of production as well as sale then total variable cost automatically get rise.

Apart from this, marginal costing is also principle costing technique utilise in decision

making process. Respective costing approach allows management attention on changes

that result from decision under consideration.

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

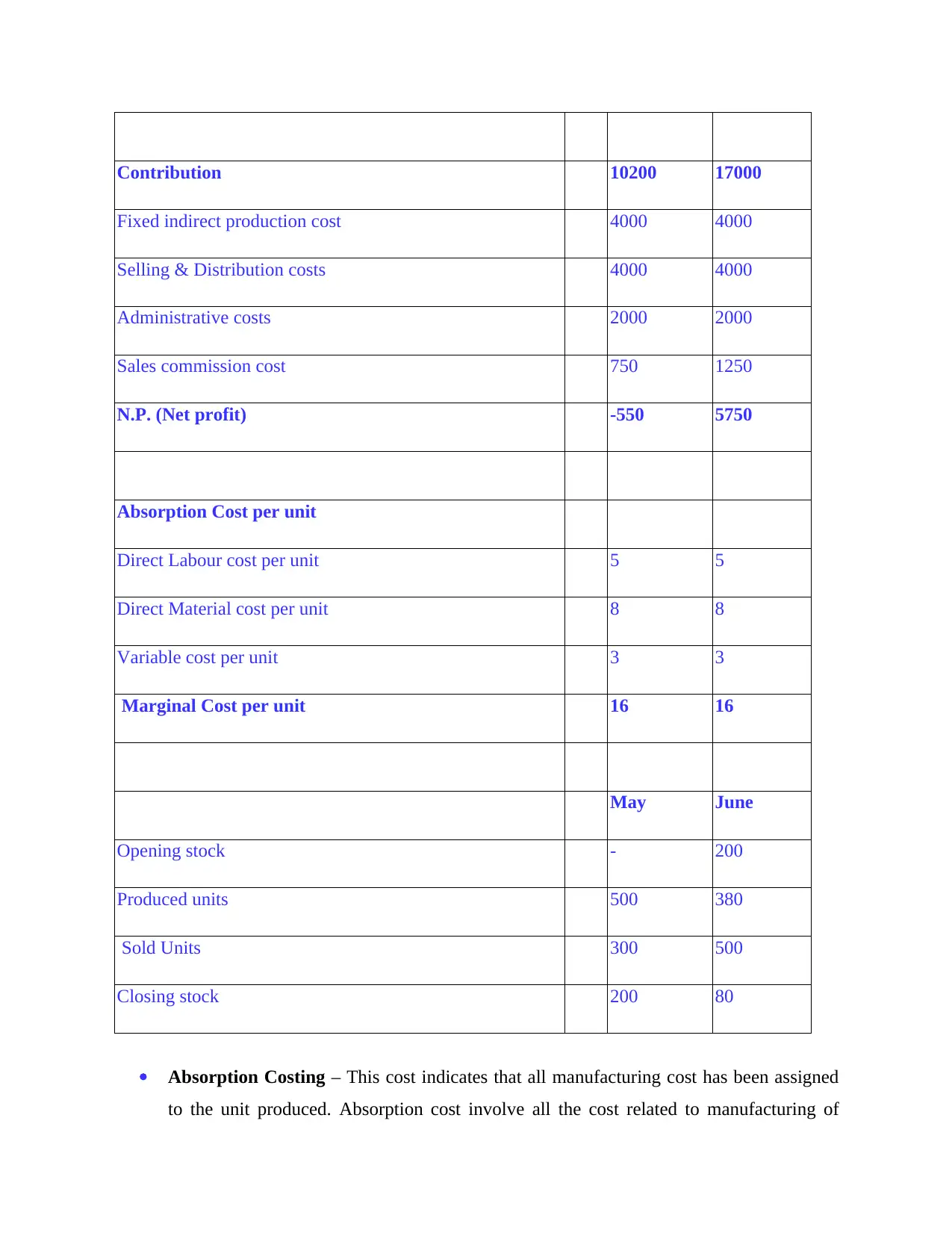

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Absorption Costing – This cost indicates that all manufacturing cost has been assigned

to the unit produced. Absorption cost involve all the cost related to manufacturing of

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Absorption Costing – This cost indicates that all manufacturing cost has been assigned

to the unit produced. Absorption cost involve all the cost related to manufacturing of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

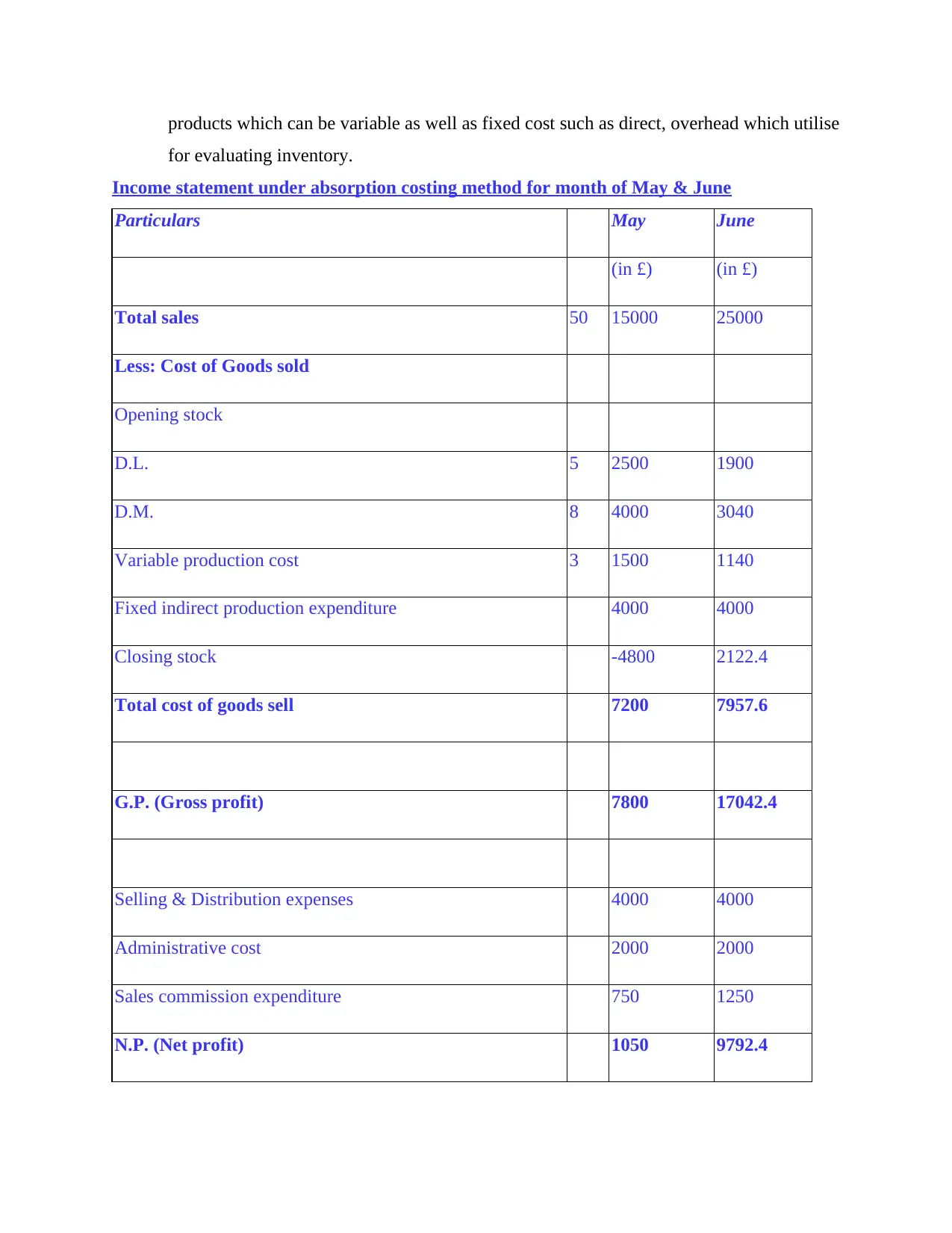

products which can be variable as well as fixed cost such as direct, overhead which utilise

for evaluating inventory.

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

for evaluating inventory.

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

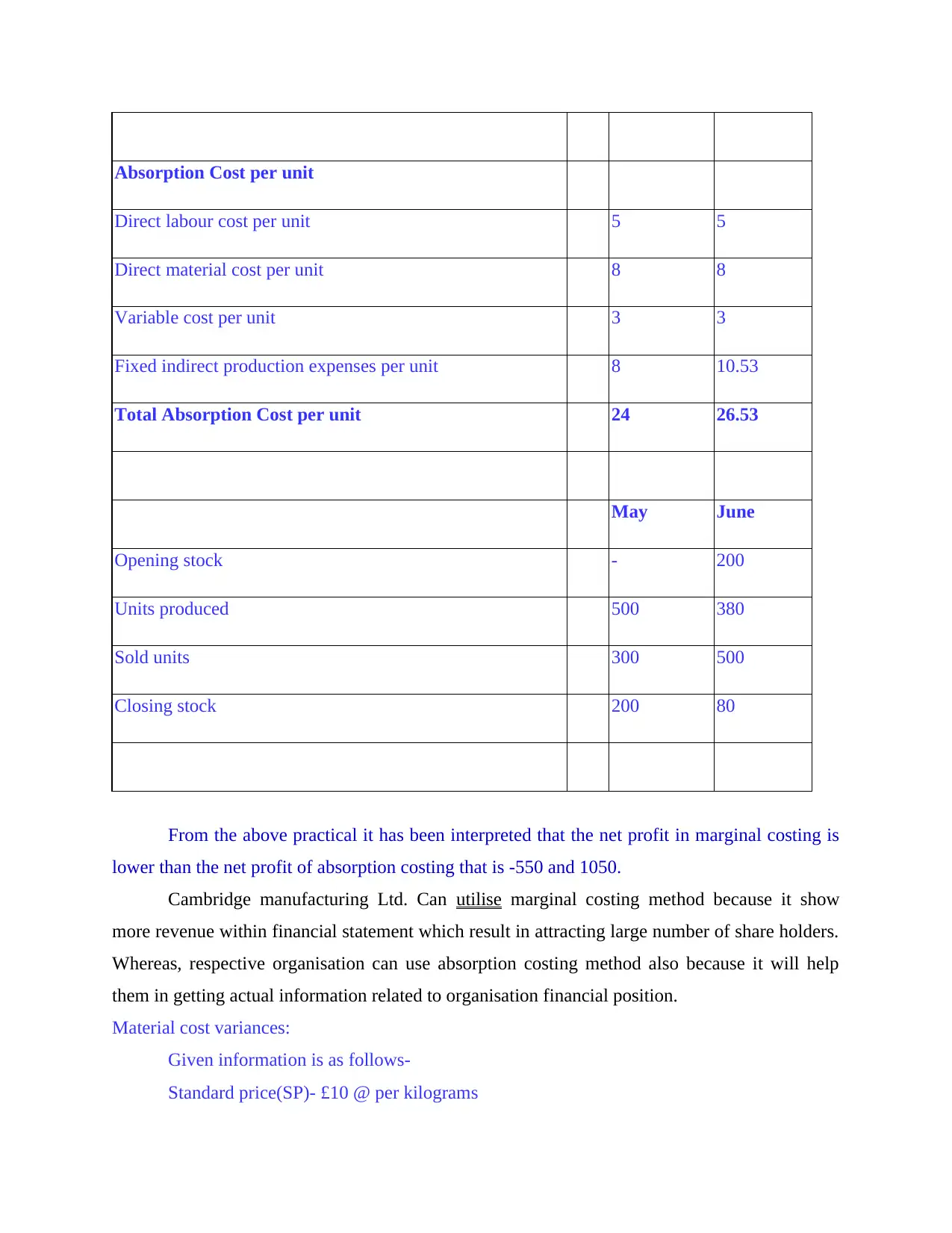

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

From the above practical it has been interpreted that the net profit in marginal costing is

lower than the net profit of absorption costing that is -550 and 1050.

Cambridge manufacturing Ltd. Can utilise marginal costing method because it show

more revenue within financial statement which result in attracting large number of share holders.

Whereas, respective organisation can use absorption costing method also because it will help

them in getting actual information related to organisation financial position.

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

From the above practical it has been interpreted that the net profit in marginal costing is

lower than the net profit of absorption costing that is -550 and 1050.

Cambridge manufacturing Ltd. Can utilise marginal costing method because it show

more revenue within financial statement which result in attracting large number of share holders.

Whereas, respective organisation can use absorption costing method also because it will help

them in getting actual information related to organisation financial position.

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.