Management Accounting Report: Connect Catering Services, UK Operations

VerifiedAdded on 2022/12/28

|16

|4474

|75

Report

AI Summary

This report provides a comprehensive analysis of management accounting, focusing on Connect Catering Services, a UK-based firm. It begins with an introduction to management accounting, emphasizing its role in decision-making and resource optimization. The report elaborates on the essential requirements of different management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems. It evaluates various reporting methods like budget reports, job cost reports, and performance reports. The report identifies the benefits of management accounting systems, such as improved decision-making and efficiency. It also examines the integration of management accounting reporting with the overall management accounting system. The report delves into cost calculations, preparing income statements using absorption and marginal costing methods, and analyzing fixed and variable costs. It examines different management accounting techniques and produces relevant financial reporting documents. Furthermore, the report evaluates planning tools used in budgetary control and compares different organizations' responses to financial problems, including how management accounting can help solve these problems. The report concludes with an overall evaluation of the planning tools and a summary of the key findings.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

P1. Detailed elaboration of management accounting and essential requirements of different

type of management accounting systems....................................................................................1

P2. Evaluation of the various methods that are used in the reporting of management

accounting....................................................................................................................................3

M1. Detailed identification of the benefits of the system of management accounting...............4

D1. Examination of the integration of management accounting reporting with management

accounting system........................................................................................................................4

TASK 2............................................................................................................................................4

P3. Calculation of different types of costs using techniques that are appropriate and also

preparing an income statement using absorption and marginal costing methods.......................4

M2. Examination of different techniques of management accounting and producing

appropriate documents that are related with financial reporting.................................................8

D2. Analysis of reports that are related with the finances...........................................................9

TASK 3............................................................................................................................................9

P4. Evaluation, analysis, and examination of different planning tools that are used in

budgetary control.........................................................................................................................9

M3. Examination of different planning tools and its uses.........................................................10

P5. Comparison of different organizations and their methods of responding to the financial

problems....................................................................................................................................11

M4. Analysis and examination of the response that organisation gives to financial problems

and how management accounting can help to solve them in an effective and efficient manner

...................................................................................................................................................12

D3. Evaluation of the planning tools.........................................................................................12

CONCLUSION..............................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

P1. Detailed elaboration of management accounting and essential requirements of different

type of management accounting systems....................................................................................1

P2. Evaluation of the various methods that are used in the reporting of management

accounting....................................................................................................................................3

M1. Detailed identification of the benefits of the system of management accounting...............4

D1. Examination of the integration of management accounting reporting with management

accounting system........................................................................................................................4

TASK 2............................................................................................................................................4

P3. Calculation of different types of costs using techniques that are appropriate and also

preparing an income statement using absorption and marginal costing methods.......................4

M2. Examination of different techniques of management accounting and producing

appropriate documents that are related with financial reporting.................................................8

D2. Analysis of reports that are related with the finances...........................................................9

TASK 3............................................................................................................................................9

P4. Evaluation, analysis, and examination of different planning tools that are used in

budgetary control.........................................................................................................................9

M3. Examination of different planning tools and its uses.........................................................10

P5. Comparison of different organizations and their methods of responding to the financial

problems....................................................................................................................................11

M4. Analysis and examination of the response that organisation gives to financial problems

and how management accounting can help to solve them in an effective and efficient manner

...................................................................................................................................................12

D3. Evaluation of the planning tools.........................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is one of the most important as well as crucial aspect since it

helps the managers of the company to take appropriate and necessary decisions so that it can add

value to the firm in the long term so that the enterprise can beat the competition and can stand

above from all the rivals that are prevailing in the similar industry (Andarwati, Nirwanto and

Darsono, 2018). In the concept of management accounting efficacy and optimum utilisation of

the available resources is the prime aim and the decisions that are taken in it are also taken

accordingly so that it can carter the needs, requirements, and demands of the organisation so that

the company can grow and prosper in the industry. Connect Catering Services is a firm that is

geographically located in the UK and is operational in the market of providing its services since

a long time period and thus as a result it has captured a larger share in the market too because of

its working. In this report there is a detailed analysis and evaluation of management accounting

and its related aspects that possess a lot of value in the present time and its essential

requirements. Apart from that the report covers different management accounting reporting

methods, different costs that has to be calculated by using appropriate technique like marginal

and absorption costing, advantages and disadvantages of different tools that are used in

budgetary control, and comparison of different firms and the financial problems that they face

while operating in the industry.

TASK 1

P1. Detailed elaboration of management accounting and essential requirements of different type

of management accounting systems

Management accounting is mainly the using of the information that is related with

management so as to make and implement appropriate decisions that can help the company to

take steps which can improve its efficiency in the market in which it is operational. In it

information that is of high importance is identified, analyzed, evaluated, recorded, and

summarized in an accurate and precise manner so that it can help the firm to work in a smooth

manner so as to operate in an effective way in the industry that can help it to improve its

performance in the long run (Brierley, 2017). It is a system that helps the company to grow and

foster in the current market situation that is highly competitive as well as dynamic in nature.

Management accounting is one of the most important as well as crucial aspect since it

helps the managers of the company to take appropriate and necessary decisions so that it can add

value to the firm in the long term so that the enterprise can beat the competition and can stand

above from all the rivals that are prevailing in the similar industry (Andarwati, Nirwanto and

Darsono, 2018). In the concept of management accounting efficacy and optimum utilisation of

the available resources is the prime aim and the decisions that are taken in it are also taken

accordingly so that it can carter the needs, requirements, and demands of the organisation so that

the company can grow and prosper in the industry. Connect Catering Services is a firm that is

geographically located in the UK and is operational in the market of providing its services since

a long time period and thus as a result it has captured a larger share in the market too because of

its working. In this report there is a detailed analysis and evaluation of management accounting

and its related aspects that possess a lot of value in the present time and its essential

requirements. Apart from that the report covers different management accounting reporting

methods, different costs that has to be calculated by using appropriate technique like marginal

and absorption costing, advantages and disadvantages of different tools that are used in

budgetary control, and comparison of different firms and the financial problems that they face

while operating in the industry.

TASK 1

P1. Detailed elaboration of management accounting and essential requirements of different type

of management accounting systems

Management accounting is mainly the using of the information that is related with

management so as to make and implement appropriate decisions that can help the company to

take steps which can improve its efficiency in the market in which it is operational. In it

information that is of high importance is identified, analyzed, evaluated, recorded, and

summarized in an accurate and precise manner so that it can help the firm to work in a smooth

manner so as to operate in an effective way in the industry that can help it to improve its

performance in the long run (Brierley, 2017). It is a system that helps the company to grow and

foster in the current market situation that is highly competitive as well as dynamic in nature.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting system is a system that is of internal in nature which an

enterprise uses to measure the progress of its management so as to implement measures

that can improve its performance if it is not up to the standards that has been expected by

the higher management. While financial management is related with the management of

the finances of the firm so as to allocate the available resources of the company in an

effective and efficient way so that it can helps the company to grow in the market and

differentiation of management and financial accounting is done below in an elaborated

manner-

S. No. Basis of Comparison Management Accounting Financial Accounting

1 Content It is a wide concept and thus

carriers all the information that

is related to financial as well as

non-financial.

It is a narrow concept and thus

only involves financial aspect

of the company.

2 Motive and Uses The main aim of this type of

accounting is to facilitate the

internal management in

decision making so that all the

decisions can be made in an

impactful way.

The motive behind preparation

of this is to provide

information which is related

with finances so that it can

help the stakeholders which are

interested in the working of the

firm.

3 Rules, Regulations

and laws to be

followed

There are no such rules in it to

be followed and it is just

prepared for the sake of

internal management (Daniel,

Persson and Sandorf, 2018).

There are many things that has

to be followed in it and all the

standards of accounting must

also be followed so that it can

help in the smooth functioning

of the company.

There are a number of different management accounting systems that are explained

below-

Cost Accounting System- It is a system that helps in analysing and evaluating all the

costs that are incurring in the business so that unnecessary expenditures can be reduced

enterprise uses to measure the progress of its management so as to implement measures

that can improve its performance if it is not up to the standards that has been expected by

the higher management. While financial management is related with the management of

the finances of the firm so as to allocate the available resources of the company in an

effective and efficient way so that it can helps the company to grow in the market and

differentiation of management and financial accounting is done below in an elaborated

manner-

S. No. Basis of Comparison Management Accounting Financial Accounting

1 Content It is a wide concept and thus

carriers all the information that

is related to financial as well as

non-financial.

It is a narrow concept and thus

only involves financial aspect

of the company.

2 Motive and Uses The main aim of this type of

accounting is to facilitate the

internal management in

decision making so that all the

decisions can be made in an

impactful way.

The motive behind preparation

of this is to provide

information which is related

with finances so that it can

help the stakeholders which are

interested in the working of the

firm.

3 Rules, Regulations

and laws to be

followed

There are no such rules in it to

be followed and it is just

prepared for the sake of

internal management (Daniel,

Persson and Sandorf, 2018).

There are many things that has

to be followed in it and all the

standards of accounting must

also be followed so that it can

help in the smooth functioning

of the company.

There are a number of different management accounting systems that are explained

below-

Cost Accounting System- It is a system that helps in analysing and evaluating all the

costs that are incurring in the business so that unnecessary expenditures can be reduced

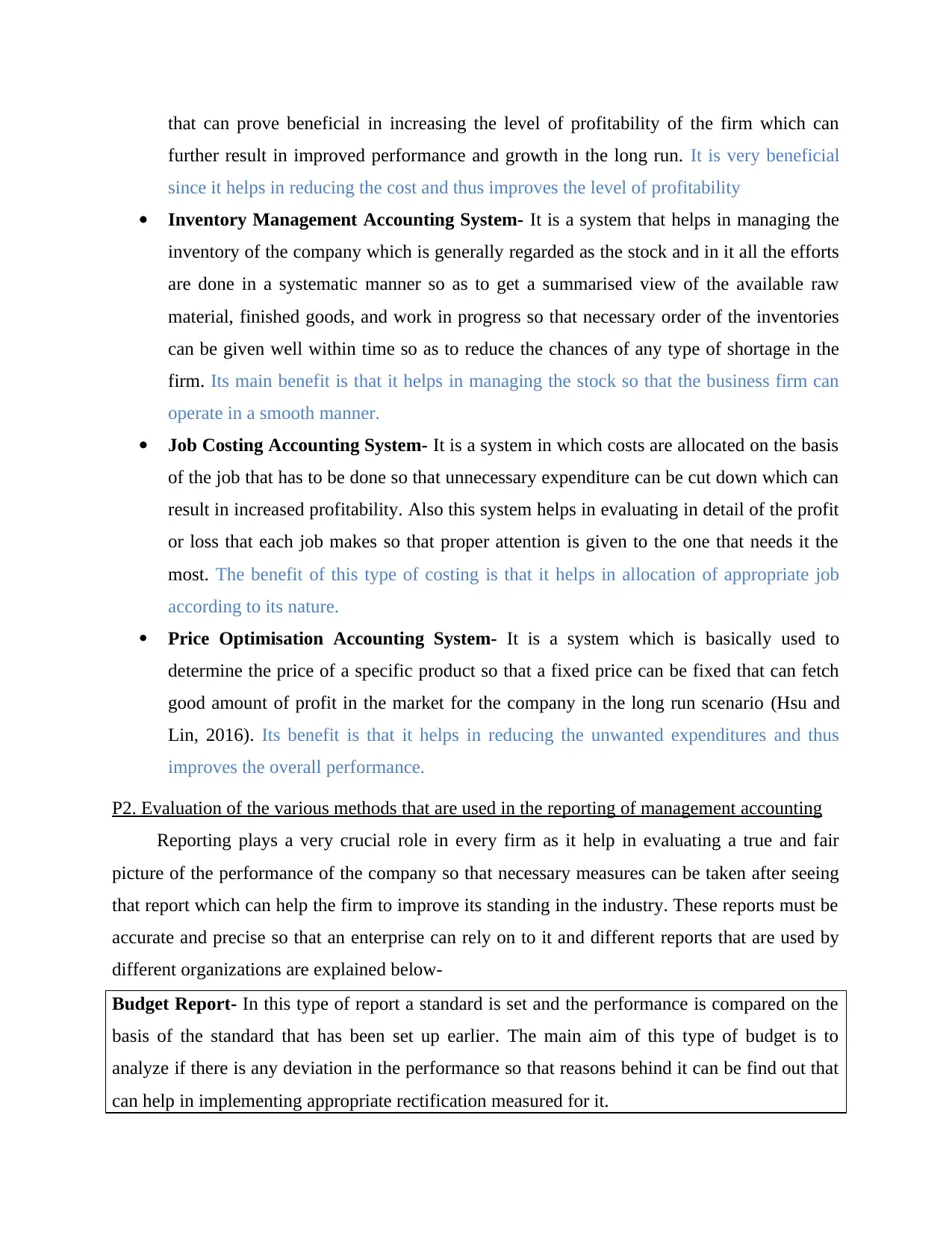

that can prove beneficial in increasing the level of profitability of the firm which can

further result in improved performance and growth in the long run. It is very beneficial

since it helps in reducing the cost and thus improves the level of profitability

Inventory Management Accounting System- It is a system that helps in managing the

inventory of the company which is generally regarded as the stock and in it all the efforts

are done in a systematic manner so as to get a summarised view of the available raw

material, finished goods, and work in progress so that necessary order of the inventories

can be given well within time so as to reduce the chances of any type of shortage in the

firm. Its main benefit is that it helps in managing the stock so that the business firm can

operate in a smooth manner.

Job Costing Accounting System- It is a system in which costs are allocated on the basis

of the job that has to be done so that unnecessary expenditure can be cut down which can

result in increased profitability. Also this system helps in evaluating in detail of the profit

or loss that each job makes so that proper attention is given to the one that needs it the

most. The benefit of this type of costing is that it helps in allocation of appropriate job

according to its nature.

Price Optimisation Accounting System- It is a system which is basically used to

determine the price of a specific product so that a fixed price can be fixed that can fetch

good amount of profit in the market for the company in the long run scenario (Hsu and

Lin, 2016). Its benefit is that it helps in reducing the unwanted expenditures and thus

improves the overall performance.

P2. Evaluation of the various methods that are used in the reporting of management accounting

Reporting plays a very crucial role in every firm as it help in evaluating a true and fair

picture of the performance of the company so that necessary measures can be taken after seeing

that report which can help the firm to improve its standing in the industry. These reports must be

accurate and precise so that an enterprise can rely on to it and different reports that are used by

different organizations are explained below-

Budget Report- In this type of report a standard is set and the performance is compared on the

basis of the standard that has been set up earlier. The main aim of this type of budget is to

analyze if there is any deviation in the performance so that reasons behind it can be find out that

can help in implementing appropriate rectification measured for it.

further result in improved performance and growth in the long run. It is very beneficial

since it helps in reducing the cost and thus improves the level of profitability

Inventory Management Accounting System- It is a system that helps in managing the

inventory of the company which is generally regarded as the stock and in it all the efforts

are done in a systematic manner so as to get a summarised view of the available raw

material, finished goods, and work in progress so that necessary order of the inventories

can be given well within time so as to reduce the chances of any type of shortage in the

firm. Its main benefit is that it helps in managing the stock so that the business firm can

operate in a smooth manner.

Job Costing Accounting System- It is a system in which costs are allocated on the basis

of the job that has to be done so that unnecessary expenditure can be cut down which can

result in increased profitability. Also this system helps in evaluating in detail of the profit

or loss that each job makes so that proper attention is given to the one that needs it the

most. The benefit of this type of costing is that it helps in allocation of appropriate job

according to its nature.

Price Optimisation Accounting System- It is a system which is basically used to

determine the price of a specific product so that a fixed price can be fixed that can fetch

good amount of profit in the market for the company in the long run scenario (Hsu and

Lin, 2016). Its benefit is that it helps in reducing the unwanted expenditures and thus

improves the overall performance.

P2. Evaluation of the various methods that are used in the reporting of management accounting

Reporting plays a very crucial role in every firm as it help in evaluating a true and fair

picture of the performance of the company so that necessary measures can be taken after seeing

that report which can help the firm to improve its standing in the industry. These reports must be

accurate and precise so that an enterprise can rely on to it and different reports that are used by

different organizations are explained below-

Budget Report- In this type of report a standard is set and the performance is compared on the

basis of the standard that has been set up earlier. The main aim of this type of budget is to

analyze if there is any deviation in the performance so that reasons behind it can be find out that

can help in implementing appropriate rectification measured for it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

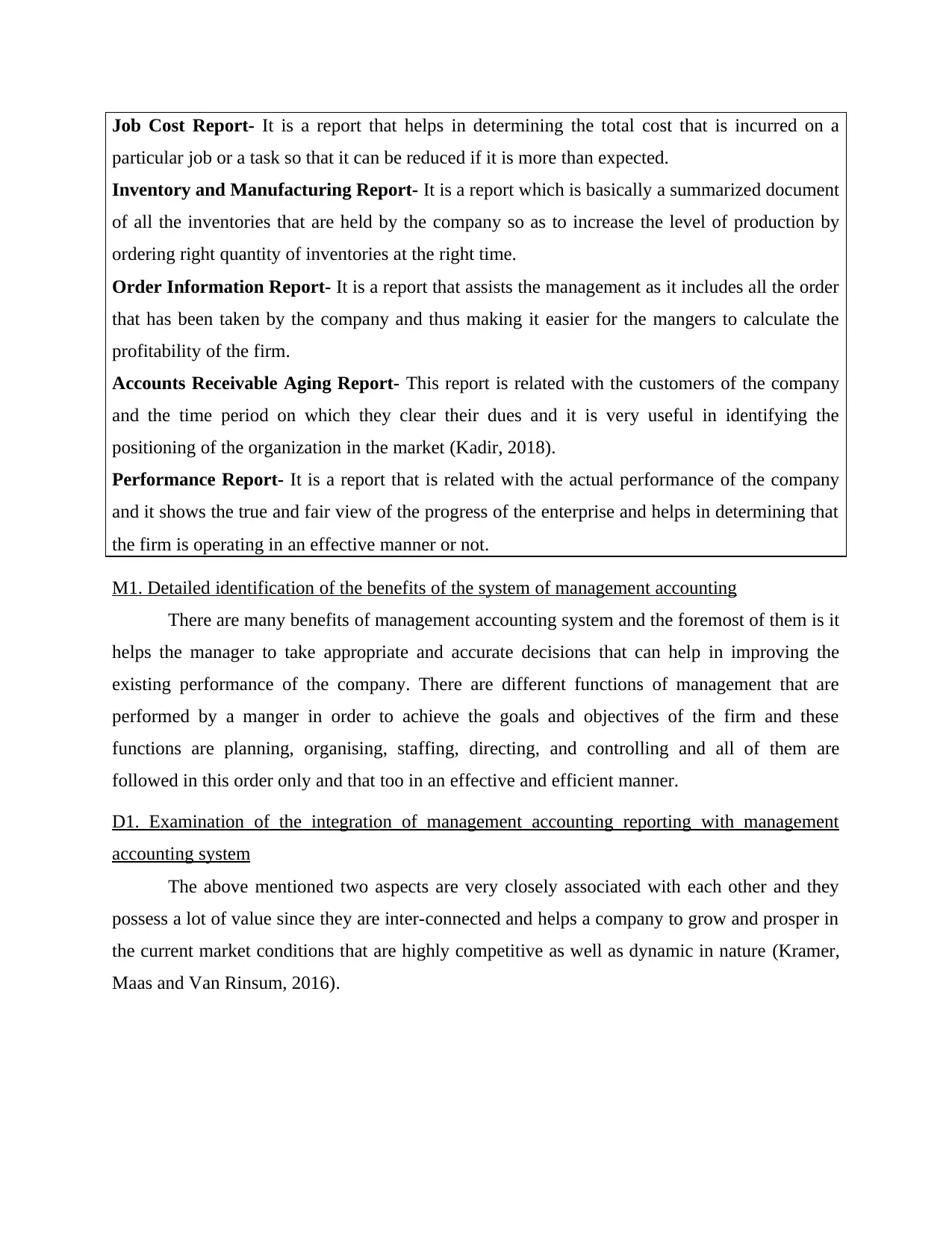

Job Cost Report- It is a report that helps in determining the total cost that is incurred on a

particular job or a task so that it can be reduced if it is more than expected.

Inventory and Manufacturing Report- It is a report which is basically a summarized document

of all the inventories that are held by the company so as to increase the level of production by

ordering right quantity of inventories at the right time.

Order Information Report- It is a report that assists the management as it includes all the order

that has been taken by the company and thus making it easier for the mangers to calculate the

profitability of the firm.

Accounts Receivable Aging Report- This report is related with the customers of the company

and the time period on which they clear their dues and it is very useful in identifying the

positioning of the organization in the market (Kadir, 2018).

Performance Report- It is a report that is related with the actual performance of the company

and it shows the true and fair view of the progress of the enterprise and helps in determining that

the firm is operating in an effective manner or not.

M1. Detailed identification of the benefits of the system of management accounting

There are many benefits of management accounting system and the foremost of them is it

helps the manager to take appropriate and accurate decisions that can help in improving the

existing performance of the company. There are different functions of management that are

performed by a manger in order to achieve the goals and objectives of the firm and these

functions are planning, organising, staffing, directing, and controlling and all of them are

followed in this order only and that too in an effective and efficient manner.

D1. Examination of the integration of management accounting reporting with management

accounting system

The above mentioned two aspects are very closely associated with each other and they

possess a lot of value since they are inter-connected and helps a company to grow and prosper in

the current market conditions that are highly competitive as well as dynamic in nature (Kramer,

Maas and Van Rinsum, 2016).

particular job or a task so that it can be reduced if it is more than expected.

Inventory and Manufacturing Report- It is a report which is basically a summarized document

of all the inventories that are held by the company so as to increase the level of production by

ordering right quantity of inventories at the right time.

Order Information Report- It is a report that assists the management as it includes all the order

that has been taken by the company and thus making it easier for the mangers to calculate the

profitability of the firm.

Accounts Receivable Aging Report- This report is related with the customers of the company

and the time period on which they clear their dues and it is very useful in identifying the

positioning of the organization in the market (Kadir, 2018).

Performance Report- It is a report that is related with the actual performance of the company

and it shows the true and fair view of the progress of the enterprise and helps in determining that

the firm is operating in an effective manner or not.

M1. Detailed identification of the benefits of the system of management accounting

There are many benefits of management accounting system and the foremost of them is it

helps the manager to take appropriate and accurate decisions that can help in improving the

existing performance of the company. There are different functions of management that are

performed by a manger in order to achieve the goals and objectives of the firm and these

functions are planning, organising, staffing, directing, and controlling and all of them are

followed in this order only and that too in an effective and efficient manner.

D1. Examination of the integration of management accounting reporting with management

accounting system

The above mentioned two aspects are very closely associated with each other and they

possess a lot of value since they are inter-connected and helps a company to grow and prosper in

the current market conditions that are highly competitive as well as dynamic in nature (Kramer,

Maas and Van Rinsum, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

P3. Calculation of different types of costs using techniques that are appropriate and also

preparing an income statement using absorption and marginal costing methods

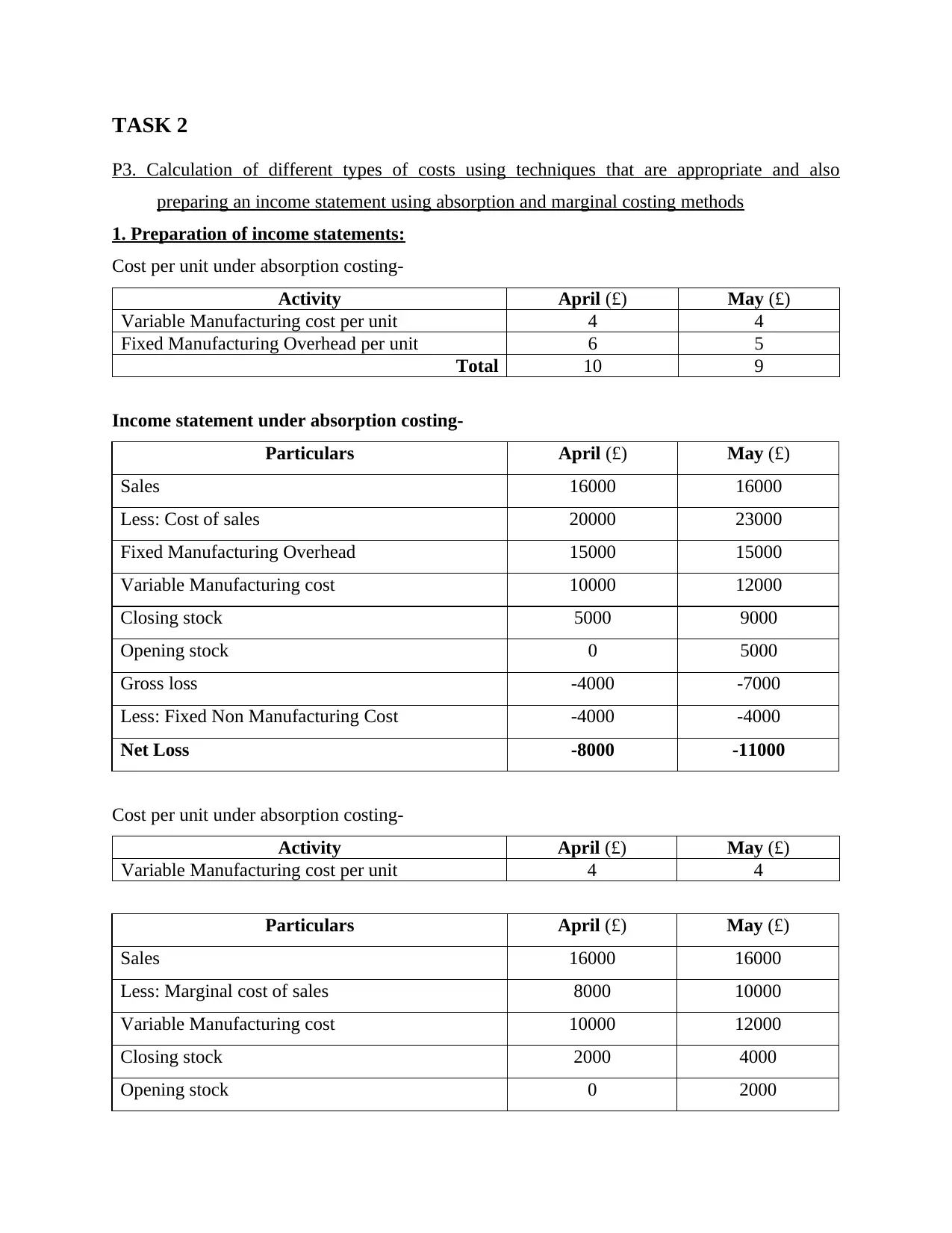

1. Preparation of income statements:

Cost per unit under absorption costing-

Activity April (£) May (£)

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

Total 10 9

Income statement under absorption costing-

Particulars April (£) May (£)

Sales 16000 16000

Less: Cost of sales 20000 23000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost 10000 12000

Closing stock 5000 9000

Opening stock 0 5000

Gross loss -4000 -7000

Less: Fixed Non Manufacturing Cost -4000 -4000

Net Loss -8000 -11000

Cost per unit under absorption costing-

Activity April (£) May (£)

Variable Manufacturing cost per unit 4 4

Particulars April (£) May (£)

Sales 16000 16000

Less: Marginal cost of sales 8000 10000

Variable Manufacturing cost 10000 12000

Closing stock 2000 4000

Opening stock 0 2000

P3. Calculation of different types of costs using techniques that are appropriate and also

preparing an income statement using absorption and marginal costing methods

1. Preparation of income statements:

Cost per unit under absorption costing-

Activity April (£) May (£)

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

Total 10 9

Income statement under absorption costing-

Particulars April (£) May (£)

Sales 16000 16000

Less: Cost of sales 20000 23000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost 10000 12000

Closing stock 5000 9000

Opening stock 0 5000

Gross loss -4000 -7000

Less: Fixed Non Manufacturing Cost -4000 -4000

Net Loss -8000 -11000

Cost per unit under absorption costing-

Activity April (£) May (£)

Variable Manufacturing cost per unit 4 4

Particulars April (£) May (£)

Sales 16000 16000

Less: Marginal cost of sales 8000 10000

Variable Manufacturing cost 10000 12000

Closing stock 2000 4000

Opening stock 0 2000

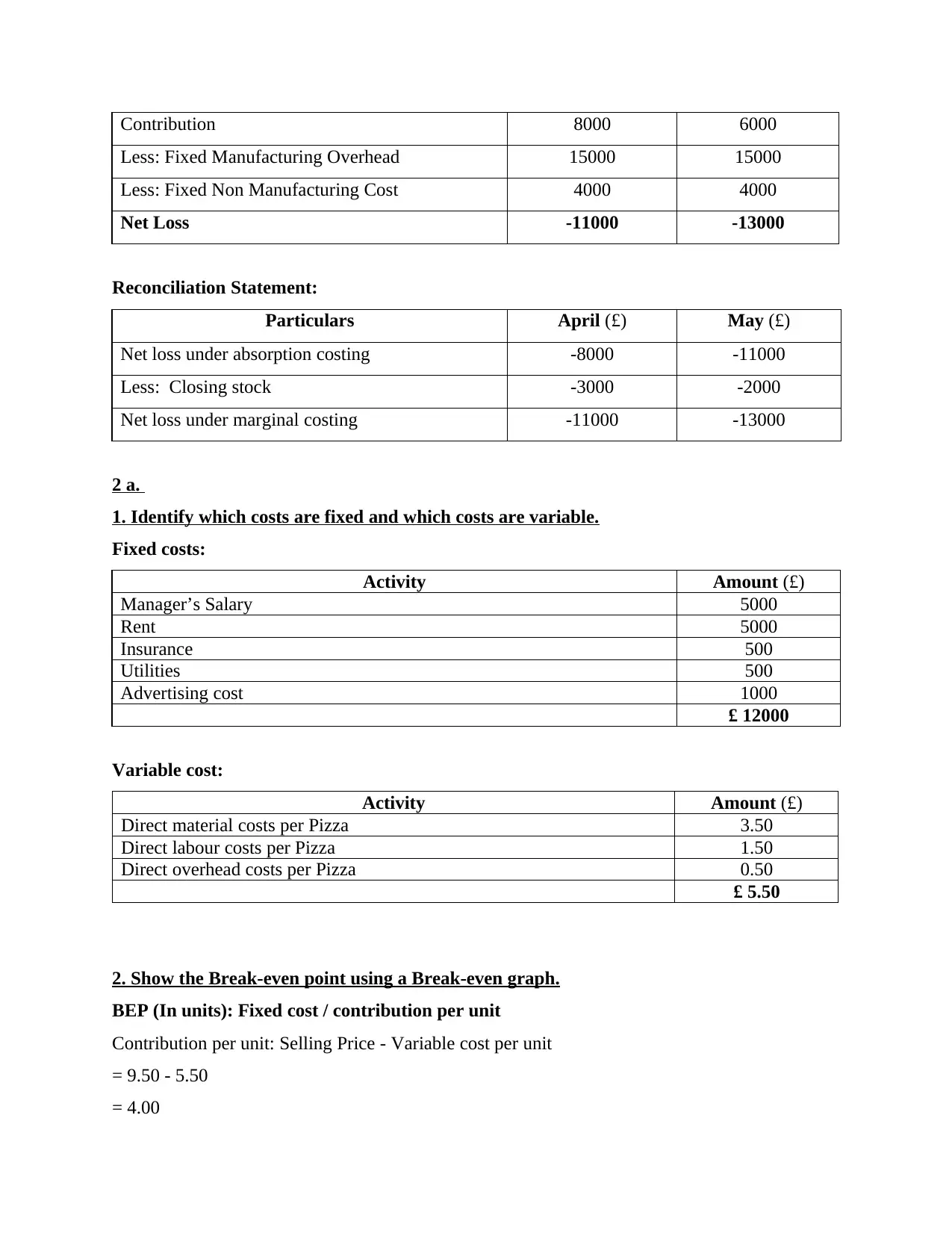

Contribution 8000 6000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non Manufacturing Cost 4000 4000

Net Loss -11000 -13000

Reconciliation Statement:

Particulars April (£) May (£)

Net loss under absorption costing -8000 -11000

Less: Closing stock -3000 -2000

Net loss under marginal costing -11000 -13000

2 a.

1. Identify which costs are fixed and which costs are variable.

Fixed costs:

Activity Amount (£)

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£ 12000

Variable cost:

Activity Amount (£)

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£ 5.50

2. Show the Break-even point using a Break-even graph.

BEP (In units): Fixed cost / contribution per unit

Contribution per unit: Selling Price - Variable cost per unit

= 9.50 - 5.50

= 4.00

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non Manufacturing Cost 4000 4000

Net Loss -11000 -13000

Reconciliation Statement:

Particulars April (£) May (£)

Net loss under absorption costing -8000 -11000

Less: Closing stock -3000 -2000

Net loss under marginal costing -11000 -13000

2 a.

1. Identify which costs are fixed and which costs are variable.

Fixed costs:

Activity Amount (£)

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£ 12000

Variable cost:

Activity Amount (£)

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£ 5.50

2. Show the Break-even point using a Break-even graph.

BEP (In units): Fixed cost / contribution per unit

Contribution per unit: Selling Price - Variable cost per unit

= 9.50 - 5.50

= 4.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BEP: 12000 / 4

= 3000 Units

BEP (In revenues): Fixed cost / PV ratio

PV ratio: Contribution / selling price* 100

= 4/ 9.50*100

= 42.10 %

BEP (In revenues) = 12000 / 42.10 %

= £ 28503

3. What would be the Margin of Safety if the organization managed to sell 2500 Pizzas?

Margin of safety = Sales units - BEP in Units

= 2500 - 3000

= - 500 Units

4. If the manager’s salary is increased to £6,000, how will this affect the BEP in units and in

sales value?

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000 / 4

= 3250 Units

New BEP (In revenues): 13000 / 42.10 %

= £ 30878

2 b. Preparation of graph:

Activity Amount (£)

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed Cost 12000

BEP point 28503

= 3000 Units

BEP (In revenues): Fixed cost / PV ratio

PV ratio: Contribution / selling price* 100

= 4/ 9.50*100

= 42.10 %

BEP (In revenues) = 12000 / 42.10 %

= £ 28503

3. What would be the Margin of Safety if the organization managed to sell 2500 Pizzas?

Margin of safety = Sales units - BEP in Units

= 2500 - 3000

= - 500 Units

4. If the manager’s salary is increased to £6,000, how will this affect the BEP in units and in

sales value?

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000 / 4

= 3250 Units

New BEP (In revenues): 13000 / 42.10 %

= £ 30878

2 b. Preparation of graph:

Activity Amount (£)

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed Cost 12000

BEP point 28503

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Variance Analysis Report:

Actual units sold = 12000

Budgeted units sold = 10000

Budgeted price per unit = 9.50

Sales volume variance = (Actual units sold - Budgeted units sold) x Budgeted price per unit

= (12000 - 10000) * 9.50

= 2000 * 9.50

= 19000 Favourable

Flexible budget

Items Actual (£) Budgeted (£) Variance (£)

Sales price 10 9.50 0.50 Fav.

Sales units 12000 10000 2000 Fav.

Revenues 120000 95000 25000 Fav.

Fixed cost 15000 12000 3000 Adv.

Variable cost 5 5.50 0.50 Fav.

M2. Examination of different techniques of management accounting and producing appropriate

documents that are related with financial reporting

There are a number of different techniques that are related with management accounting as

it helps in analysing the performance of the company so as to take appropriate decisions if

performance is not up to the expectations of higher authorities of management. It becomes much

more important as it helps in determining the loop holes of the business and then rectifies it

Actual units sold = 12000

Budgeted units sold = 10000

Budgeted price per unit = 9.50

Sales volume variance = (Actual units sold - Budgeted units sold) x Budgeted price per unit

= (12000 - 10000) * 9.50

= 2000 * 9.50

= 19000 Favourable

Flexible budget

Items Actual (£) Budgeted (£) Variance (£)

Sales price 10 9.50 0.50 Fav.

Sales units 12000 10000 2000 Fav.

Revenues 120000 95000 25000 Fav.

Fixed cost 15000 12000 3000 Adv.

Variable cost 5 5.50 0.50 Fav.

M2. Examination of different techniques of management accounting and producing appropriate

documents that are related with financial reporting

There are a number of different techniques that are related with management accounting as

it helps in analysing the performance of the company so as to take appropriate decisions if

performance is not up to the expectations of higher authorities of management. It becomes much

more important as it helps in determining the loop holes of the business and then rectifies it

accordingly so that it does not hamper the functioning of the company in the long run (Lai, Leoni

and Stacchezzini, 2019).

D2. Analysis of reports that are related with the finances

Financial statement is one of the most important aspect for every firm that is operational in the

market as it helps in evaluating the true positioning of the firm in the profitability terms so that

profit or loss aspect can be studied in detail which can prove beneficial in improving the overall

performance of the enterprise in the long term.

TASK 3

P4. Evaluation, analysis, and examination of different planning tools that are used in budgetary

control

Planning is one of the most essential aspect as it is the first function and all the other

activities and functions depends on it since it bridges the gap between the present situation that is

the present positioning of the company with that of the future prospects at which the firm wants

to be in the near future. There are a number of different planning tools that are used under

budgetary control since it helps in evaluating the performance with the set standards and

planning also does the same thing. There are different types of budget that are used by different

organizations so as to cater the needs, requirements, and demands of the company and all of

them are discussed below in detail with their advantages as well as disadvantages with context to

Connect Catering services-

Cash Budget- It is one of the most crucial type of budget as it is related with the receipts

and expenditure of cash and its related aspects that is inflow and outflow of cash. This budget

helps in determining the allocation of cash so that it can be used in an accurate manner leaving

no scope of error in between which can prove useful from the company’s point of view. Its

advantages and disadvantages are illustrated below- Advantages- It is very easy to formulate and helps in reducing the unnecessary

expenditure at times which results in improved profitability of the company (Miles and

Miles, 2019).

Disadvantage- It is very rigid and does not leave any scope for innovation and spending

in new areas that can fetch good returns in the near future and also the data can be used

against the company if it gets into the wrong hands.

and Stacchezzini, 2019).

D2. Analysis of reports that are related with the finances

Financial statement is one of the most important aspect for every firm that is operational in the

market as it helps in evaluating the true positioning of the firm in the profitability terms so that

profit or loss aspect can be studied in detail which can prove beneficial in improving the overall

performance of the enterprise in the long term.

TASK 3

P4. Evaluation, analysis, and examination of different planning tools that are used in budgetary

control

Planning is one of the most essential aspect as it is the first function and all the other

activities and functions depends on it since it bridges the gap between the present situation that is

the present positioning of the company with that of the future prospects at which the firm wants

to be in the near future. There are a number of different planning tools that are used under

budgetary control since it helps in evaluating the performance with the set standards and

planning also does the same thing. There are different types of budget that are used by different

organizations so as to cater the needs, requirements, and demands of the company and all of

them are discussed below in detail with their advantages as well as disadvantages with context to

Connect Catering services-

Cash Budget- It is one of the most crucial type of budget as it is related with the receipts

and expenditure of cash and its related aspects that is inflow and outflow of cash. This budget

helps in determining the allocation of cash so that it can be used in an accurate manner leaving

no scope of error in between which can prove useful from the company’s point of view. Its

advantages and disadvantages are illustrated below- Advantages- It is very easy to formulate and helps in reducing the unnecessary

expenditure at times which results in improved profitability of the company (Miles and

Miles, 2019).

Disadvantage- It is very rigid and does not leave any scope for innovation and spending

in new areas that can fetch good returns in the near future and also the data can be used

against the company if it gets into the wrong hands.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.