Management Accounting Report: Cash Budget and Financial Position

VerifiedAdded on 2023/01/11

|14

|3935

|33

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Lets Grow Ltd. It begins with an introduction to management accounting, emphasizing its role in providing financial information for decision-making. The main body of the report explores various management accounting systems, including inventory management, price optimization, and cost accounting systems, detailing their requirements and benefits. It also examines different management accounting reports, such as budget reports, performance reports, and cost accounting reports, and evaluates how these systems and reports support organizational functions. A significant portion of the report focuses on a cash budget for the coming six months, providing detailed calculations and a working note. The report then discusses the use of the cash budget in preparing and forecasting the financial position of Lets Grow Ltd. Finally, it addresses how the company can adapt its management accounting system to handle financial problems and offers a critical evaluation of the company's financial position based on the forecasted cash budget. The report concludes with a summary of the key findings and a list of references.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

LO 1.................................................................................................................................................3

(a) Management accounting system and its requirements:..........................................................3

Various of reports of Management Accounting:.........................................................................5

(b) Evaluation of how Management accounting system and its report support respective

organisation:................................................................................................................................6

LO 3.................................................................................................................................................6

(c) Cash budget for the coming six months ending in August 2020:..........................................6

(d) Use of cash budget and its application for preparing and forecasting the financial position:7

LO 4.................................................................................................................................................9

(e) Discussion about how Lets Grow Ltd can adapt its management accounting system to deal

with financial problems:..............................................................................................................9

(f). Critical evaluation of financial position of Lets Grow Ltd based on the forecasted cash

budget prepared:........................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

LO 1.................................................................................................................................................3

(a) Management accounting system and its requirements:..........................................................3

Various of reports of Management Accounting:.........................................................................5

(b) Evaluation of how Management accounting system and its report support respective

organisation:................................................................................................................................6

LO 3.................................................................................................................................................6

(c) Cash budget for the coming six months ending in August 2020:..........................................6

(d) Use of cash budget and its application for preparing and forecasting the financial position:7

LO 4.................................................................................................................................................9

(e) Discussion about how Lets Grow Ltd can adapt its management accounting system to deal

with financial problems:..............................................................................................................9

(f). Critical evaluation of financial position of Lets Grow Ltd based on the forecasted cash

budget prepared:........................................................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting term is the combination of accounting reports and managerial reports

used to provide accurate and credible financial information/data to support phase of decision

making. Through managing financial information/details and maintaining earnings, the

administrator decides, records and monitors the financial transactions and events. Additionally,

MA is broader term which actually makes creative strategic decisions through handling

acceptable bookkeeping and financial information (Dauth, Pronobis and Schmid, 2017). This

study is focused on manufacturing company named Lets grow Ltd. The study report comprises

of multiple frameworks/systems and core reports of MA which aid in decision-making phase. In

addition, the use of the cash budget approach for predicting company

operational performance and the use of MA systems to address financial issues/problems.

MAIN BODY

LO 1

(a) Management accounting system and its requirements:

Management accounting can be defined as collection of different elements, conceptual

frameworks, requirements and concepts that assist management in taking effective financial as

well as managerial decisions. They make effective planning with help of these concepts and

provisions relating to use of their funds/resources (Galinova, 2017).

Management Accounting systems are essential in all businesses, as it enables businesses to functi

on effectively by providing financial information on internal functions. The Lets Grow Ltd is

also using the MA system to make right decisions about investments. Additionally, by

implementing management accounting structure that increases productivity, it manages

accounting adequately. Here following is a discussion on the different systems and their specific

requirements in context of Lets Grow Ltd, as follows:

Inventory management system: This system is important for any and all

companies/corporations that are trying to manage and properly track appropriate inventory

records. It's used largely for the tracking of the manufacturing sector facilities

and production of items which have large range of stock items. Lets grow 's manager is

also using this system to identify and classify inventories with the help of classification of

productions and commercial operations. This is used to handle the productivity improvements

Management accounting term is the combination of accounting reports and managerial reports

used to provide accurate and credible financial information/data to support phase of decision

making. Through managing financial information/details and maintaining earnings, the

administrator decides, records and monitors the financial transactions and events. Additionally,

MA is broader term which actually makes creative strategic decisions through handling

acceptable bookkeeping and financial information (Dauth, Pronobis and Schmid, 2017). This

study is focused on manufacturing company named Lets grow Ltd. The study report comprises

of multiple frameworks/systems and core reports of MA which aid in decision-making phase. In

addition, the use of the cash budget approach for predicting company

operational performance and the use of MA systems to address financial issues/problems.

MAIN BODY

LO 1

(a) Management accounting system and its requirements:

Management accounting can be defined as collection of different elements, conceptual

frameworks, requirements and concepts that assist management in taking effective financial as

well as managerial decisions. They make effective planning with help of these concepts and

provisions relating to use of their funds/resources (Galinova, 2017).

Management Accounting systems are essential in all businesses, as it enables businesses to functi

on effectively by providing financial information on internal functions. The Lets Grow Ltd is

also using the MA system to make right decisions about investments. Additionally, by

implementing management accounting structure that increases productivity, it manages

accounting adequately. Here following is a discussion on the different systems and their specific

requirements in context of Lets Grow Ltd, as follows:

Inventory management system: This system is important for any and all

companies/corporations that are trying to manage and properly track appropriate inventory

records. It's used largely for the tracking of the manufacturing sector facilities

and production of items which have large range of stock items. Lets grow 's manager is

also using this system to identify and classify inventories with the help of classification of

productions and commercial operations. This is used to handle the productivity improvements

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

from the production to the distribution, material storage, manufacturing to shipment/delivery.

This system substantially requires the wide range of comprehensive details about inventories and

related processes (Grabner, Posch and Wabnegg, 2018).

Price optimization system: Pricing system in booming industry is key factor or variable that

decides about technology that will be employed to determine the price of the produced items.

This relates to use of quantitative method that states how an organization should

implement pricing strategy or policy to optimize profitability. This mechanism usually helps to

make direction in setting prices that will be justifiable to both entity and customers. As in Lets

grow, managing official use this system to evaluate the relation of price changes and demand of

items to determine the most efficient price for different products. This system requires thorough

study of response of customers in relation to a product item and relative of changes in prices of

such product items.

Cost Accounting System: It is also a form of management accounting system/framework, that

used quantify accurate and precise costs of each aspect within an organisation. It entails the

procedure of classifying, collecting, evaluating, identifying, summarizing and allocating

different costs to regulate costs and maintain accountability. In fact, this could be used to

assess actual costs of the product item and services offered by an organisation. This framework,

as in the Lets Grow Ltd, is used to measure costs of its different products as well as processes

related to production of product. Managers also monitor and control costs to ensure a certain

level of profitability. By applying cost accounting framework corporation can put strict control

over the costs which can help company to identity unproductive costs as to enhance operational

performance. A cost accounting system within an organisation require comprehensive and

detailed data/information of costs and expenses as well as proper classification of these

costs/expenses as pet their nature and use within corporation (Horvat and Mojzer, 2019).

Evaluation of Benefits of MA systems:

Systems Benefits

Inventory Management System In Lets Grow such system is advantageous to

minimise the overall stock-handling costs and

minimise normal losses of inventory/stock

(Kostyukova and et. al, 2018).

Cost Accounting System This is beneficial in business, as it facilitates

This system substantially requires the wide range of comprehensive details about inventories and

related processes (Grabner, Posch and Wabnegg, 2018).

Price optimization system: Pricing system in booming industry is key factor or variable that

decides about technology that will be employed to determine the price of the produced items.

This relates to use of quantitative method that states how an organization should

implement pricing strategy or policy to optimize profitability. This mechanism usually helps to

make direction in setting prices that will be justifiable to both entity and customers. As in Lets

grow, managing official use this system to evaluate the relation of price changes and demand of

items to determine the most efficient price for different products. This system requires thorough

study of response of customers in relation to a product item and relative of changes in prices of

such product items.

Cost Accounting System: It is also a form of management accounting system/framework, that

used quantify accurate and precise costs of each aspect within an organisation. It entails the

procedure of classifying, collecting, evaluating, identifying, summarizing and allocating

different costs to regulate costs and maintain accountability. In fact, this could be used to

assess actual costs of the product item and services offered by an organisation. This framework,

as in the Lets Grow Ltd, is used to measure costs of its different products as well as processes

related to production of product. Managers also monitor and control costs to ensure a certain

level of profitability. By applying cost accounting framework corporation can put strict control

over the costs which can help company to identity unproductive costs as to enhance operational

performance. A cost accounting system within an organisation require comprehensive and

detailed data/information of costs and expenses as well as proper classification of these

costs/expenses as pet their nature and use within corporation (Horvat and Mojzer, 2019).

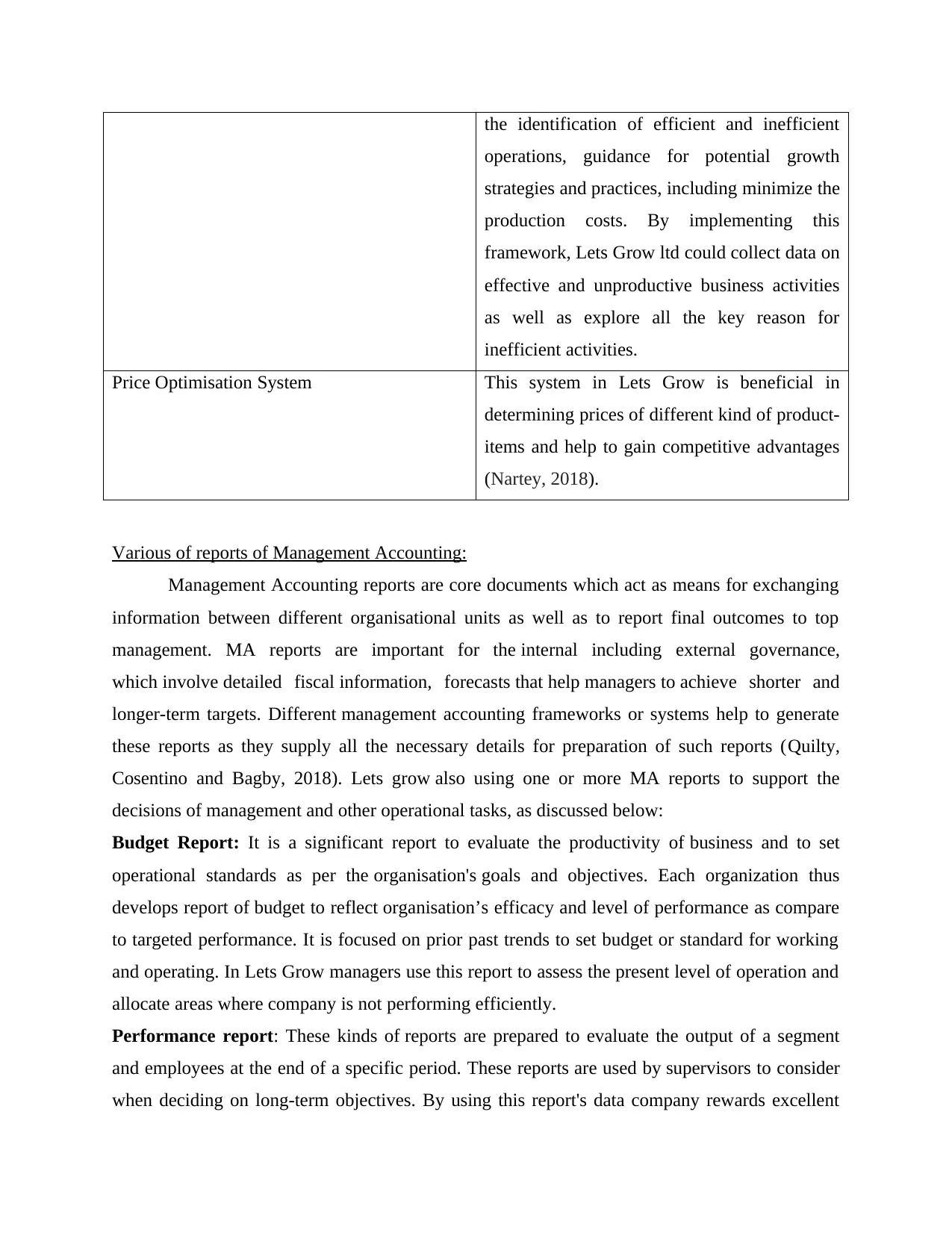

Evaluation of Benefits of MA systems:

Systems Benefits

Inventory Management System In Lets Grow such system is advantageous to

minimise the overall stock-handling costs and

minimise normal losses of inventory/stock

(Kostyukova and et. al, 2018).

Cost Accounting System This is beneficial in business, as it facilitates

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the identification of efficient and inefficient

operations, guidance for potential growth

strategies and practices, including minimize the

production costs. By implementing this

framework, Lets Grow ltd could collect data on

effective and unproductive business activities

as well as explore all the key reason for

inefficient activities.

Price Optimisation System This system in Lets Grow is beneficial in

determining prices of different kind of product-

items and help to gain competitive advantages

(Nartey, 2018).

Various of reports of Management Accounting:

Management Accounting reports are core documents which act as means for exchanging

information between different organisational units as well as to report final outcomes to top

management. MA reports are important for the internal including external governance,

which involve detailed fiscal information, forecasts that help managers to achieve shorter and

longer-term targets. Different management accounting frameworks or systems help to generate

these reports as they supply all the necessary details for preparation of such reports (Quilty,

Cosentino and Bagby, 2018). Lets grow also using one or more MA reports to support the

decisions of management and other operational tasks, as discussed below:

Budget Report: It is a significant report to evaluate the productivity of business and to set

operational standards as per the organisation's goals and objectives. Each organization thus

develops report of budget to reflect organisation’s efficacy and level of performance as compare

to targeted performance. It is focused on prior past trends to set budget or standard for working

and operating. In Lets Grow managers use this report to assess the present level of operation and

allocate areas where company is not performing efficiently.

Performance report: These kinds of reports are prepared to evaluate the output of a segment

and employees at the end of a specific period. These reports are used by supervisors to consider

when deciding on long-term objectives. By using this report's data company rewards excellent

operations, guidance for potential growth

strategies and practices, including minimize the

production costs. By implementing this

framework, Lets Grow ltd could collect data on

effective and unproductive business activities

as well as explore all the key reason for

inefficient activities.

Price Optimisation System This system in Lets Grow is beneficial in

determining prices of different kind of product-

items and help to gain competitive advantages

(Nartey, 2018).

Various of reports of Management Accounting:

Management Accounting reports are core documents which act as means for exchanging

information between different organisational units as well as to report final outcomes to top

management. MA reports are important for the internal including external governance,

which involve detailed fiscal information, forecasts that help managers to achieve shorter and

longer-term targets. Different management accounting frameworks or systems help to generate

these reports as they supply all the necessary details for preparation of such reports (Quilty,

Cosentino and Bagby, 2018). Lets grow also using one or more MA reports to support the

decisions of management and other operational tasks, as discussed below:

Budget Report: It is a significant report to evaluate the productivity of business and to set

operational standards as per the organisation's goals and objectives. Each organization thus

develops report of budget to reflect organisation’s efficacy and level of performance as compare

to targeted performance. It is focused on prior past trends to set budget or standard for working

and operating. In Lets Grow managers use this report to assess the present level of operation and

allocate areas where company is not performing efficiently.

Performance report: These kinds of reports are prepared to evaluate the output of a segment

and employees at the end of a specific period. These reports are used by supervisors to consider

when deciding on long-term objectives. By using this report's data company rewards excellent

working employees and good performers, helps the staff to be motivated. There is, thus, a need

to track results and acts of employees in a performance reports that managers prepare. Company

executives in the Lets grow Ltd are using this report for setting rewards and other benefits for

employees/workers to encourage. employee to put their efforts towards organisation's goals

(Robalo and Gago, 2017).

Cost accounting report: The cost of different products or services are defined and determined

under this report. This specifics of all the costs involved in production of a products and costs

incurred to specific organisational processes. This report is mainly linked with cost accounting

system of MA which require delayed costs information. In Lets grow Ltd, this report is used by

managing officials to assess the costs of processes and products as well as to enable managers to

track the areas which are responsible for increasing overall costs.

(b) Evaluation of how Management accounting system and its report support respective

organisation:

Management accounting systems as discussed above and its different reports are interconnected.

Reports offers key data and information to managers and here such information in reports are

obtained through multiple systems of MA. Reports and Systems are integral part of the entire

managerial accounting structure. Aim of reports and systems is to provide extensive support to

managerial as well as operational/organisational tasks. In the relevant company manager, the

stock management method is applied as well as reports are prepared to make products and

services conveniently accessible. With the assistance of such reports and processes, an

administrator collects all relevant information that contributes to making decisions (Schmidt,

2017). The inventory management system allows to determine how much materials are required

for processing and tracking to significantly lessen wasting. This also leads to the efficient usage

of resources. The company could collect the necessary costs details and budget it through cost

reports through obeying cost accounting system. In addition, the price-optimization system is

always coupled with reports, as company can decide which rate the customer must be influenced

by reporting, in long this can provide competitive advantages to company.

to track results and acts of employees in a performance reports that managers prepare. Company

executives in the Lets grow Ltd are using this report for setting rewards and other benefits for

employees/workers to encourage. employee to put their efforts towards organisation's goals

(Robalo and Gago, 2017).

Cost accounting report: The cost of different products or services are defined and determined

under this report. This specifics of all the costs involved in production of a products and costs

incurred to specific organisational processes. This report is mainly linked with cost accounting

system of MA which require delayed costs information. In Lets grow Ltd, this report is used by

managing officials to assess the costs of processes and products as well as to enable managers to

track the areas which are responsible for increasing overall costs.

(b) Evaluation of how Management accounting system and its report support respective

organisation:

Management accounting systems as discussed above and its different reports are interconnected.

Reports offers key data and information to managers and here such information in reports are

obtained through multiple systems of MA. Reports and Systems are integral part of the entire

managerial accounting structure. Aim of reports and systems is to provide extensive support to

managerial as well as operational/organisational tasks. In the relevant company manager, the

stock management method is applied as well as reports are prepared to make products and

services conveniently accessible. With the assistance of such reports and processes, an

administrator collects all relevant information that contributes to making decisions (Schmidt,

2017). The inventory management system allows to determine how much materials are required

for processing and tracking to significantly lessen wasting. This also leads to the efficient usage

of resources. The company could collect the necessary costs details and budget it through cost

reports through obeying cost accounting system. In addition, the price-optimization system is

always coupled with reports, as company can decide which rate the customer must be influenced

by reporting, in long this can provide competitive advantages to company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 3

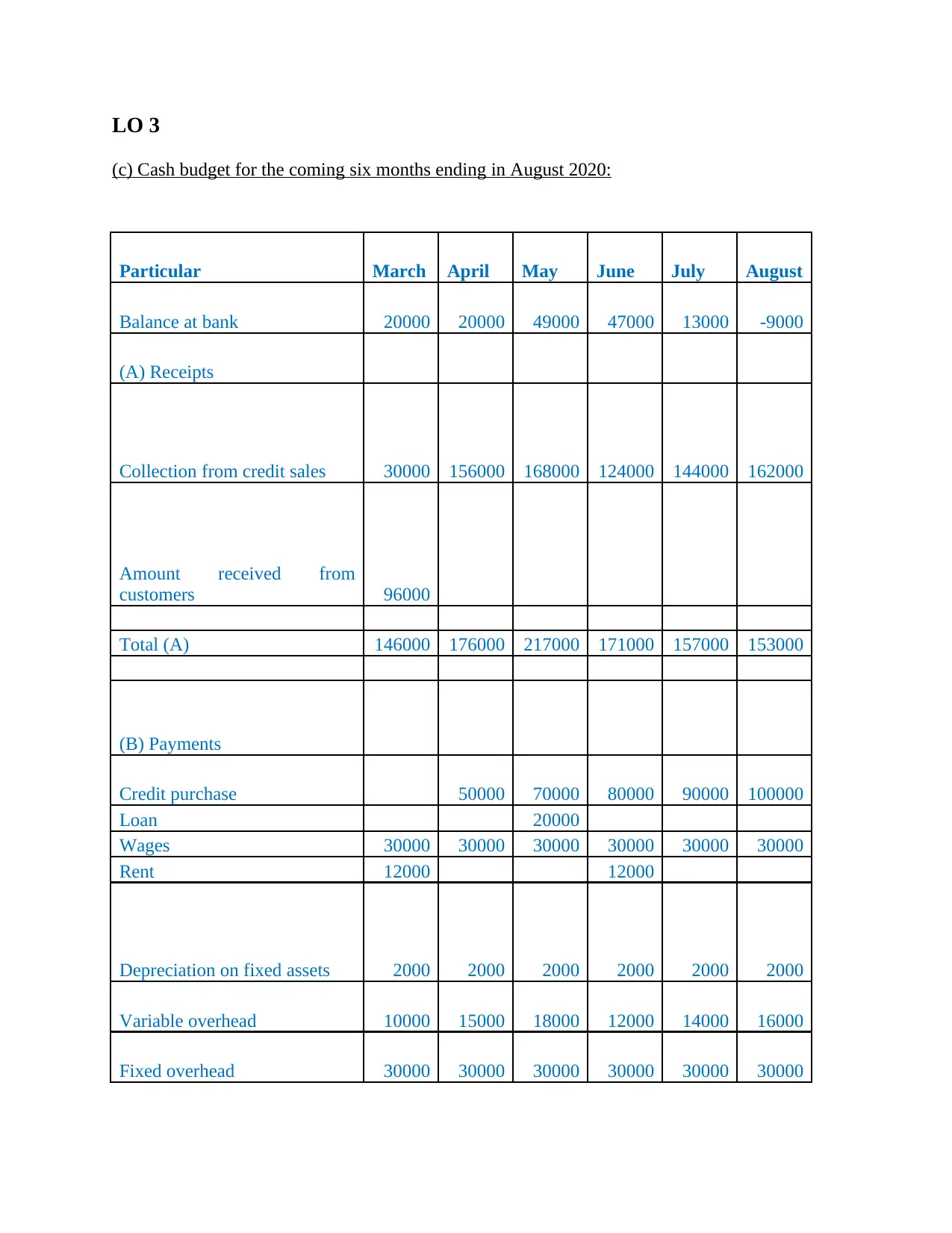

(c) Cash budget for the coming six months ending in August 2020:

Particular March April May June July August

Balance at bank 20000 20000 49000 47000 13000 -9000

(A) Receipts

Collection from credit sales 30000 156000 168000 124000 144000 162000

Amount received from

customers 96000

Total (A) 146000 176000 217000 171000 157000 153000

(B) Payments

Credit purchase 50000 70000 80000 90000 100000

Loan 20000

Wages 30000 30000 30000 30000 30000 30000

Rent 12000 12000

Depreciation on fixed assets 2000 2000 2000 2000 2000 2000

Variable overhead 10000 15000 18000 12000 14000 16000

Fixed overhead 30000 30000 30000 30000 30000 30000

(c) Cash budget for the coming six months ending in August 2020:

Particular March April May June July August

Balance at bank 20000 20000 49000 47000 13000 -9000

(A) Receipts

Collection from credit sales 30000 156000 168000 124000 144000 162000

Amount received from

customers 96000

Total (A) 146000 176000 217000 171000 157000 153000

(B) Payments

Credit purchase 50000 70000 80000 90000 100000

Loan 20000

Wages 30000 30000 30000 30000 30000 30000

Rent 12000 12000

Depreciation on fixed assets 2000 2000 2000 2000 2000 2000

Variable overhead 10000 15000 18000 12000 14000 16000

Fixed overhead 30000 30000 30000 30000 30000 30000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

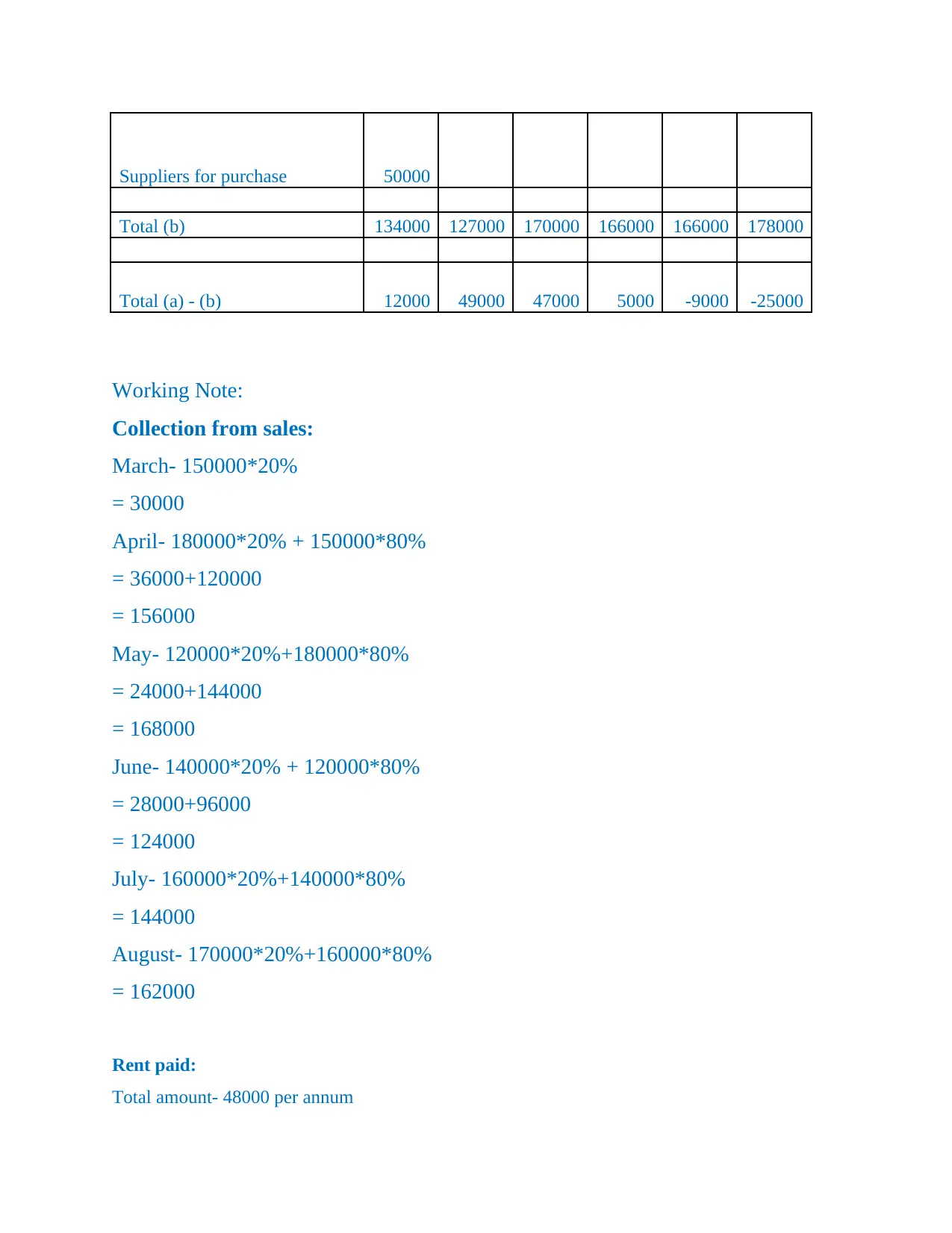

Suppliers for purchase 50000

Total (b) 134000 127000 170000 166000 166000 178000

Total (a) - (b) 12000 49000 47000 5000 -9000 -25000

Working Note:

Collection from sales:

March- 150000*20%

= 30000

April- 180000*20% + 150000*80%

= 36000+120000

= 156000

May- 120000*20%+180000*80%

= 24000+144000

= 168000

June- 140000*20% + 120000*80%

= 28000+96000

= 124000

July- 160000*20%+140000*80%

= 144000

August- 170000*20%+160000*80%

= 162000

Rent paid:

Total amount- 48000 per annum

Total (b) 134000 127000 170000 166000 166000 178000

Total (a) - (b) 12000 49000 47000 5000 -9000 -25000

Working Note:

Collection from sales:

March- 150000*20%

= 30000

April- 180000*20% + 150000*80%

= 36000+120000

= 156000

May- 120000*20%+180000*80%

= 24000+144000

= 168000

June- 140000*20% + 120000*80%

= 28000+96000

= 124000

July- 160000*20%+140000*80%

= 144000

August- 170000*20%+160000*80%

= 162000

Rent paid:

Total amount- 48000 per annum

Per quarter- 48000/4

= 12000

Depreciation:

Total- 24000 per annum

Per month- 24000/12

= 2000

(d) Use of cash budget and its application for preparing and forecasting the financial position:

Budget: Budgets are structured for an assessment of future profits and costs for benefits of

business. The budget is valuable in creating estimates while considering an organization's goals.

In attempt to produce profits and increase customer numbers, accountant Lets Grow Ltd prepares

numerous types of budgets which assist in the utilization of funds and other financial resources

by setting financial targets. In company managers prepare budgets based on past data and

information while considering short term as well as long term objectives with aim to improve

exiting performance level (Singh and Verma, 2018).

Cash budget: Cash budgets are inflow and outflows of cash forecasts planned for a certain set

period by managers in an organization. It allows credit risk management as well as decides

whether funds for projects are sufficiently available. A cash budget provides estimation of cash

inflows and outflows, act as an accounting instrument for tracking and control of specific short-

term cash flows operations of an entity, a prediction of the expected cash revenues of an

organization, and payments over a period typically of weeks and months. The cash estimate, a

prediction of cash receipts as well as cash payments for year, is all in line with budgets,

and importance of making a financial forecast could not be over-emphasized, because sufficient

cash is necessary if enterprise is to succeed. Staff must also be paying in cash, taxes payable in

cash, including vendors may withhold products until they have been payed promptly. For most

situations a month end cash budget would be appropriate, since payments are usually made

at beginning of each month between lenders and debtors.

Importance of Cash Budget: Most companies in the modern financial world have to create a

cash budget before investment on any expected growth or awareness of new assets is made.

A cash budget dictates the ability of the company to cover its obligations and expenses.

= 12000

Depreciation:

Total- 24000 per annum

Per month- 24000/12

= 2000

(d) Use of cash budget and its application for preparing and forecasting the financial position:

Budget: Budgets are structured for an assessment of future profits and costs for benefits of

business. The budget is valuable in creating estimates while considering an organization's goals.

In attempt to produce profits and increase customer numbers, accountant Lets Grow Ltd prepares

numerous types of budgets which assist in the utilization of funds and other financial resources

by setting financial targets. In company managers prepare budgets based on past data and

information while considering short term as well as long term objectives with aim to improve

exiting performance level (Singh and Verma, 2018).

Cash budget: Cash budgets are inflow and outflows of cash forecasts planned for a certain set

period by managers in an organization. It allows credit risk management as well as decides

whether funds for projects are sufficiently available. A cash budget provides estimation of cash

inflows and outflows, act as an accounting instrument for tracking and control of specific short-

term cash flows operations of an entity, a prediction of the expected cash revenues of an

organization, and payments over a period typically of weeks and months. The cash estimate, a

prediction of cash receipts as well as cash payments for year, is all in line with budgets,

and importance of making a financial forecast could not be over-emphasized, because sufficient

cash is necessary if enterprise is to succeed. Staff must also be paying in cash, taxes payable in

cash, including vendors may withhold products until they have been payed promptly. For most

situations a month end cash budget would be appropriate, since payments are usually made

at beginning of each month between lenders and debtors.

Importance of Cash Budget: Most companies in the modern financial world have to create a

cash budget before investment on any expected growth or awareness of new assets is made.

A cash budget dictates the ability of the company to cover its obligations and expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Furthermore, it assists management in decision-taking on its cash reserves for furthering

operations, moreover it assists management in achievement of its goals over a defined period,

and finally, it makes it possible to calculate actual financial activity against the market forecast

(Suljović and Meta, 2017).

Application of cash budget: The cash budgets can be applied by the organization to better

prepare and provide direction and emphasis on business’s sensitive areas. Furthermore, the

corporation and its managerial benefit from cash budgets through proper

allocations and utilization of funds for investments, divestments and current projects that also

generate greater revenues for the Respective company. This means that company employees

receive bonuses and other economic advantages from the corporation's budgetary revenues. It

must be stressed that a business with sufficient budgets will schedule its development and

growth.

Advantages: This budget approach helps us to determine whether cash reserves are sufficient to

meet every day obligations or whether minimum liquidity and cash status requirements stated in

the business or external governance of the business are retained. This also allows a company to

make the decision whether it has so much cash-funds to be spent on financially viable activity or

not.

Disadvantages: Main demerit of this budget is that it consumes more time and a minor error can

lead to adverse financial risks for business. This Budget includes the generation of

budgeted figures, reporting of costs estimates and the forwarding of such information to

management. Such statistics do not change until they have been released. Thus, further

modification in cash budget is not possible generally which make it rigid (Disadvantage of cash

budget. 2019).

LO 4

(e) Discussion about how Lets Grow Ltd can adapt its management accounting system to deal

with financial problems:

Each and every business organisation like Lets Grow ltd face Financial problems at

different stage of operations and at different business segments. Financial problems can lead to

direct impact on organisation’s performance and profitability. Ignorance of financial problems

operations, moreover it assists management in achievement of its goals over a defined period,

and finally, it makes it possible to calculate actual financial activity against the market forecast

(Suljović and Meta, 2017).

Application of cash budget: The cash budgets can be applied by the organization to better

prepare and provide direction and emphasis on business’s sensitive areas. Furthermore, the

corporation and its managerial benefit from cash budgets through proper

allocations and utilization of funds for investments, divestments and current projects that also

generate greater revenues for the Respective company. This means that company employees

receive bonuses and other economic advantages from the corporation's budgetary revenues. It

must be stressed that a business with sufficient budgets will schedule its development and

growth.

Advantages: This budget approach helps us to determine whether cash reserves are sufficient to

meet every day obligations or whether minimum liquidity and cash status requirements stated in

the business or external governance of the business are retained. This also allows a company to

make the decision whether it has so much cash-funds to be spent on financially viable activity or

not.

Disadvantages: Main demerit of this budget is that it consumes more time and a minor error can

lead to adverse financial risks for business. This Budget includes the generation of

budgeted figures, reporting of costs estimates and the forwarding of such information to

management. Such statistics do not change until they have been released. Thus, further

modification in cash budget is not possible generally which make it rigid (Disadvantage of cash

budget. 2019).

LO 4

(e) Discussion about how Lets Grow Ltd can adapt its management accounting system to deal

with financial problems:

Each and every business organisation like Lets Grow ltd face Financial problems at

different stage of operations and at different business segments. Financial problems can lead to

direct impact on organisation’s performance and profitability. Ignorance of financial problems

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

may lead to financial risks and adverse financial performance. Here following is discussion on

major financial problems that company is facing:

Increasing Inventories costs: In recent period company’s aggregate inventory handing and

storage costs have been substantially increased and continuously going on. This financial

problem affecting company’s operating profits and gross productivity level.

Decreasing sales: There is major decline in company’s sales after making changes in prices of its

different products. This financial problem affecting company’s overall profitability level.

In attempt to respond to these financial problems and recognising key cause of such

problems company can use following techniques of MA, as discussed below:

Benchmarking: It is method of contrasting one's business operations and performance measures

to industry standards. Usually measured aspects are of performance, time, and costs.

In benchmarking process, management recognizes best organizations in their sector, in another

sector where similar mechanisms occur, and compares the outcomes and procedures of those

evaluated (the "benchmarks") to results of one's own. Benchmarking is being used to calculate

performance by means of a particular variable (cost each unit of measurement, efficiency per-

unit of measurement, cycle period of per-unit of measurement or faults per unit of measurement)

leading in performance metric which is then contrasted with others.

KPIs: A performance indicator or also recognized as key-performance indicator (KPI) is kind of

tool used by an agency or corporation to assess performance. This is often used to track an

activity or to evaluate specific components of corporate performance that are most important for

currents and potential success of enterprise. A performance indicator or also recognized as the

key-performance indicator (KPI) is kind of tool used by agency or corporation to assess

performance. This is often used to track an activity or to evaluate specific components of

corporate performance that are most important for currents and potential success of enterprise.

KPIs are being used to evaluate performance of company in its the business segments, divisions,

departments, and workers. This is very useful in demonstrating that certain results/outcomes

have been obtained or hasn't been accomplished, in enabling decision-makers to attain the

intended outputs, results, aims and priorities, in helping to perceive distinctions, enhancements or

innovations that are connected to desired change in particular context as well as in information

showing adjustments like factors or variations.

major financial problems that company is facing:

Increasing Inventories costs: In recent period company’s aggregate inventory handing and

storage costs have been substantially increased and continuously going on. This financial

problem affecting company’s operating profits and gross productivity level.

Decreasing sales: There is major decline in company’s sales after making changes in prices of its

different products. This financial problem affecting company’s overall profitability level.

In attempt to respond to these financial problems and recognising key cause of such

problems company can use following techniques of MA, as discussed below:

Benchmarking: It is method of contrasting one's business operations and performance measures

to industry standards. Usually measured aspects are of performance, time, and costs.

In benchmarking process, management recognizes best organizations in their sector, in another

sector where similar mechanisms occur, and compares the outcomes and procedures of those

evaluated (the "benchmarks") to results of one's own. Benchmarking is being used to calculate

performance by means of a particular variable (cost each unit of measurement, efficiency per-

unit of measurement, cycle period of per-unit of measurement or faults per unit of measurement)

leading in performance metric which is then contrasted with others.

KPIs: A performance indicator or also recognized as key-performance indicator (KPI) is kind of

tool used by an agency or corporation to assess performance. This is often used to track an

activity or to evaluate specific components of corporate performance that are most important for

currents and potential success of enterprise. A performance indicator or also recognized as the

key-performance indicator (KPI) is kind of tool used by agency or corporation to assess

performance. This is often used to track an activity or to evaluate specific components of

corporate performance that are most important for currents and potential success of enterprise.

KPIs are being used to evaluate performance of company in its the business segments, divisions,

departments, and workers. This is very useful in demonstrating that certain results/outcomes

have been obtained or hasn't been accomplished, in enabling decision-makers to attain the

intended outputs, results, aims and priorities, in helping to perceive distinctions, enhancements or

innovations that are connected to desired change in particular context as well as in information

showing adjustments like factors or variations.

Financial Governance: This corresponds to way financial information is gathered, handled,

tracked and regulated by a corporation. Financial governance encompasses how companies

monitor business transactions, handle data on efficiency and monitoring, compliance, activities

and reporting. This approach should be used regularly and efficiently to allow the organizations

to make greater long-term results because it can generate sustainable productivity and leaving

behind its competitors in industry. This will help it achieve the long-term objective of optimizing

profit (Weetman, 2019).

Comparison between organizations that how to resolve financial issues:

Basis Letts Grow Ltd Hope constructions ltd

Financial Issues Corporation is facing issue of

increasing stock/inventory

costs. Another issue is decline

in sales after changes in prices

of its products.

This corporation is facing issue of

increasing costs of its construction

projects.

MA system For responding to above 2

issues company adopt

inventory management system

and price optimization system

respectively. As inventory MS

can help company to

minimize inventories costs

and price optimization system

can help to set optimum price

of its products without leading

to decline in sales.

Company should adopt cost

accounting systems to control cost

of its various construction projects

and allocate areas which can lead

to increase in overall project costs.

Technique Company should use

Benchmarking and financial

governance to assess the

reason and identify the main

cause of increase in stock

costs and decline in sales.

Hope construction should adopt

KPIs technique to recognize all the

root factors which are responsible

of increasing project costs (Welsh,

2018).

tracked and regulated by a corporation. Financial governance encompasses how companies

monitor business transactions, handle data on efficiency and monitoring, compliance, activities

and reporting. This approach should be used regularly and efficiently to allow the organizations

to make greater long-term results because it can generate sustainable productivity and leaving

behind its competitors in industry. This will help it achieve the long-term objective of optimizing

profit (Weetman, 2019).

Comparison between organizations that how to resolve financial issues:

Basis Letts Grow Ltd Hope constructions ltd

Financial Issues Corporation is facing issue of

increasing stock/inventory

costs. Another issue is decline

in sales after changes in prices

of its products.

This corporation is facing issue of

increasing costs of its construction

projects.

MA system For responding to above 2

issues company adopt

inventory management system

and price optimization system

respectively. As inventory MS

can help company to

minimize inventories costs

and price optimization system

can help to set optimum price

of its products without leading

to decline in sales.

Company should adopt cost

accounting systems to control cost

of its various construction projects

and allocate areas which can lead

to increase in overall project costs.

Technique Company should use

Benchmarking and financial

governance to assess the

reason and identify the main

cause of increase in stock

costs and decline in sales.

Hope construction should adopt

KPIs technique to recognize all the

root factors which are responsible

of increasing project costs (Welsh,

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.