Management Accounting Report: Cost Analysis for Airdri Ltd.

VerifiedAdded on 2023/01/19

|17

|4707

|62

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within a business context, specifically using Airdri Ltd. as a case study. The report explores different types of management accounting systems, including job costing, price optimizing, cost accounting, and inventory management systems, and how these systems are used by Airdri Ltd. It also examines various management accounting reporting methods, such as budget reports, accounts receivable ageing reports, job cost reports, and inventory reports, highlighting their benefits. Furthermore, the report delves into cost analysis techniques, particularly marginal and absorption costing, and their application in preparing income statements and making informed financial decisions. It discusses the integration of management accounting systems within organizational processes. The report also covers planning tools for budgetary control, comparing their advantages and disadvantages and evaluating how management accounting systems and planning tools can help organizations respond to financial problems and achieve sustainable success. Overall, the report offers a detailed understanding of management accounting practices and their significance in driving business performance and profitability.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

LO1..................................................................................................................................................5

Management accounting and different types of management accounting systems...................5

Different methods used for management accounting reporting..................................................6

Benefits of management accounting systems and their application............................................7

Integration of management accounting systems and management accounting reporting within

organisational processes..............................................................................................................8

LO 2.................................................................................................................................................9

Calculation of costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs.....................................................................................................9

Application of management accounting techniques to produce appropriate financial reporting

documents.................................................................................................................................12

Application and interpretation of financial reports for a range of business activities...............12

LO 3...............................................................................................................................................13

Advantages and disadvantages of different types of planning tools used for budgetary control

...................................................................................................................................................13

Different planning tools and their application for preparing and forecasting budgets.............14

LO 4...............................................................................................................................................15

Comparison of how organisations are adopting management accounting systems to respond to

financial problems.....................................................................................................................15

Analysis of how in responding to financial problems, management accounting can lead

organisations to sustainable success .........................................................................................17

Evaluation of how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success..............................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................4

LO1..................................................................................................................................................5

Management accounting and different types of management accounting systems...................5

Different methods used for management accounting reporting..................................................6

Benefits of management accounting systems and their application............................................7

Integration of management accounting systems and management accounting reporting within

organisational processes..............................................................................................................8

LO 2.................................................................................................................................................9

Calculation of costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs.....................................................................................................9

Application of management accounting techniques to produce appropriate financial reporting

documents.................................................................................................................................12

Application and interpretation of financial reports for a range of business activities...............12

LO 3...............................................................................................................................................13

Advantages and disadvantages of different types of planning tools used for budgetary control

...................................................................................................................................................13

Different planning tools and their application for preparing and forecasting budgets.............14

LO 4...............................................................................................................................................15

Comparison of how organisations are adopting management accounting systems to respond to

financial problems.....................................................................................................................15

Analysis of how in responding to financial problems, management accounting can lead

organisations to sustainable success .........................................................................................17

Evaluation of how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success..............................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................18

INTRODUCTION

Managerial accounting consider collection, examine and coverage information about the

dealing and funds of a business concern. These reports are specifically meant for the use of

managers of the business and are not meant for external stakeholders. Objective of management

accounting is to use these reports and help managers in taking accurate decisions about

controlling business activities to aid in growth and profitability of the business. The Berkeley

Partnership is a financial consultancy organisation which provides it's clients with crucial

information they need for managerial decision-making. To understand various concepts of

management accounting Airdri Ltd. which is located in Technology House, Eynsham OX29

4AQ, UK is taken. It is a provider of sustainable hand dryers which are designed to dry hands

quickly and are recognised for their reliability, low energy consumption, longevity, reduced

noise and ease of service. In this report different methods of management accounting reporting

and techniques to prepare financial statements, planning tools for budgetary control and how

management accounting systems help in responding to financial problems are discussed

(Amiram, Bozanic and Rouen, 2015).

LO1

Management accounting and different types of management accounting systems

According to the Institute of Management Accountants (IMA) : “Management accounting is

a occupation that affect relation in management decision-making, devising preparation and

execution establishment systems, and render skillfulness in financial reporting and control to

assist management in the preparation and execution of an administration strategy”.

According to Chartered Institute of Management Accountants (CIMA) : “Management

accounting is analysing information to advise business strategy and drive sustainable business

success.”

Management Accounting systems help Airdri Ltd. in analysing costs associated with

manufacturing of hand dryers that provide fast hand drying services to it's customers, preparation

of plans, determining ways of reducing prices, decision making, organising and understanding

financial data, identifying business problem areas and strategies of solving them etc. so that

performance of the business can be improved and sustainable profits can be gained for successful

Managerial accounting consider collection, examine and coverage information about the

dealing and funds of a business concern. These reports are specifically meant for the use of

managers of the business and are not meant for external stakeholders. Objective of management

accounting is to use these reports and help managers in taking accurate decisions about

controlling business activities to aid in growth and profitability of the business. The Berkeley

Partnership is a financial consultancy organisation which provides it's clients with crucial

information they need for managerial decision-making. To understand various concepts of

management accounting Airdri Ltd. which is located in Technology House, Eynsham OX29

4AQ, UK is taken. It is a provider of sustainable hand dryers which are designed to dry hands

quickly and are recognised for their reliability, low energy consumption, longevity, reduced

noise and ease of service. In this report different methods of management accounting reporting

and techniques to prepare financial statements, planning tools for budgetary control and how

management accounting systems help in responding to financial problems are discussed

(Amiram, Bozanic and Rouen, 2015).

LO1

Management accounting and different types of management accounting systems

According to the Institute of Management Accountants (IMA) : “Management accounting is

a occupation that affect relation in management decision-making, devising preparation and

execution establishment systems, and render skillfulness in financial reporting and control to

assist management in the preparation and execution of an administration strategy”.

According to Chartered Institute of Management Accountants (CIMA) : “Management

accounting is analysing information to advise business strategy and drive sustainable business

success.”

Management Accounting systems help Airdri Ltd. in analysing costs associated with

manufacturing of hand dryers that provide fast hand drying services to it's customers, preparation

of plans, determining ways of reducing prices, decision making, organising and understanding

financial data, identifying business problem areas and strategies of solving them etc. so that

performance of the business can be improved and sustainable profits can be gained for successful

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

running of the business. Some management accounting systems used by Airdri Ltd. are as

follows :

Different management accounting systems

Job costing system : This system is used to assign manufacturing cost to each individual

product while keeping track on expense monitoring. The products provided by Airdri Ltd. are

sufficiently different from each other and each has a significant cost. Various types of hand

dryers based on the customer requirements are manufactured so as to satisfy different needs.

Whether a robust, cast iron dryer is needed to sustain high usage, or a quiet, contemporary dryer

is preferred by the customer, Airdri has a dryer to fit every wash room environment (Bogsnes,

2016).

Price optimising system : This system is used to take control of the prices of resources

and help in deciding prices of multiple products at a time. This helps in determining how demand

will fluctuate at different price levels. Airdri Ltd. use this system to tailor prices for different

products based on the demand of the customers. It also helps in determining pricing structures

for promotional pricing, initial pricing and discount pricing. Before determining the prices

product life cycle, category goals of different products and competitors pricing strategies are

considered.

Cost accounting system : It is a framework used by firms to estimate the cost of their

products for profitability analysis, inventory valuation and cost control. Airdri Ltd. uses this

system to track the flow of inventory continually through the various stages of hand dryer

production. It allows the company to maintain just-in-time inventory system where materials are

ordered from vendors and suppliers on an as needed basis. It helps production managers and cost

accountants to check the inventory at every stage of production (Chenhall and Moers, 2015).

Inventory management system : This system is a combination of technology and

processes and procedures that oversee the monitoring and maintenance of stocked products and

determine if they are assets or raw materials or finished goods ready to be delivered to the end

consumers. It helps the managers of Airdri Ltd. to map the complete journey of the product.

Through accurate tracking of goods, the company can minimize waste, analyse trends and make

better investment decisions.

Vital role of management accounting in Airdri Ltd

follows :

Different management accounting systems

Job costing system : This system is used to assign manufacturing cost to each individual

product while keeping track on expense monitoring. The products provided by Airdri Ltd. are

sufficiently different from each other and each has a significant cost. Various types of hand

dryers based on the customer requirements are manufactured so as to satisfy different needs.

Whether a robust, cast iron dryer is needed to sustain high usage, or a quiet, contemporary dryer

is preferred by the customer, Airdri has a dryer to fit every wash room environment (Bogsnes,

2016).

Price optimising system : This system is used to take control of the prices of resources

and help in deciding prices of multiple products at a time. This helps in determining how demand

will fluctuate at different price levels. Airdri Ltd. use this system to tailor prices for different

products based on the demand of the customers. It also helps in determining pricing structures

for promotional pricing, initial pricing and discount pricing. Before determining the prices

product life cycle, category goals of different products and competitors pricing strategies are

considered.

Cost accounting system : It is a framework used by firms to estimate the cost of their

products for profitability analysis, inventory valuation and cost control. Airdri Ltd. uses this

system to track the flow of inventory continually through the various stages of hand dryer

production. It allows the company to maintain just-in-time inventory system where materials are

ordered from vendors and suppliers on an as needed basis. It helps production managers and cost

accountants to check the inventory at every stage of production (Chenhall and Moers, 2015).

Inventory management system : This system is a combination of technology and

processes and procedures that oversee the monitoring and maintenance of stocked products and

determine if they are assets or raw materials or finished goods ready to be delivered to the end

consumers. It helps the managers of Airdri Ltd. to map the complete journey of the product.

Through accurate tracking of goods, the company can minimize waste, analyse trends and make

better investment decisions.

Vital role of management accounting in Airdri Ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It help the company to make control on the business activities and actions. It is also

though using key information from internal report, managers become competent to focus

on that activities which are outcome into low profitability or high costs.

MA plays a vital role in developing effective planning of different type of available

resources. It is only possible as per the accumulated information, managers of the

company can competent to monitor future activities that help in efficacious planning.

Different methods used for management accounting reporting

Management accounting reporting includes collection of data that provides useful

information to the managers for planning, regulating, decision-making and measuring

performance of the business. These reports provide information needed to cut costs, cut product

lines that are not profitable and invest in goods that offer best financial returns. The various

reports prepared by management and their benefits for Airdri Ltd. are as follows : Budget report : Financial data is documented and recorded in a budget report which is

used by management to compare the estimated, budgeted projections with actual

performance achieved during a period. Budget report lists all the sources of earnings and

expenditures that are required to achieve organisational goals and objectives. Airdri Ltd.

can use these reports to limit the expenses during production and complete the work

within the estimated budget amount (Dent and Barry, 2017). Accounts receivable ageing reports : It is a periodic report that categorizes a company's

accounts receivable according to the length of time an invoice has been outstanding. It

helps in determining the financial health of company's customers and their ability to pay

their debts. Airdri Ltd. can use these reports so as to monitor its collection policies to

reduce old bad debts and maintain liquidity of the company. Job cost reports : These reports are used to identify cost, expenses and financial

efficiency and profitability of each particular job. These reports help in evaluating the

projects that are more profitable than others and focusing efforts on such jobs. Costs of

each job can be evaluated and waste areas can be identified to reduce overall costs. Airdri

Ltd. can use these reports to decide the pricing strategies of the company and reduce

production costs with providing good quality products (Khan and Jain, 2018).

Inventory and manufacturing reports : The proper reporting and accounting of

inventory increase the usefulness of financial statements for potential and actual

though using key information from internal report, managers become competent to focus

on that activities which are outcome into low profitability or high costs.

MA plays a vital role in developing effective planning of different type of available

resources. It is only possible as per the accumulated information, managers of the

company can competent to monitor future activities that help in efficacious planning.

Different methods used for management accounting reporting

Management accounting reporting includes collection of data that provides useful

information to the managers for planning, regulating, decision-making and measuring

performance of the business. These reports provide information needed to cut costs, cut product

lines that are not profitable and invest in goods that offer best financial returns. The various

reports prepared by management and their benefits for Airdri Ltd. are as follows : Budget report : Financial data is documented and recorded in a budget report which is

used by management to compare the estimated, budgeted projections with actual

performance achieved during a period. Budget report lists all the sources of earnings and

expenditures that are required to achieve organisational goals and objectives. Airdri Ltd.

can use these reports to limit the expenses during production and complete the work

within the estimated budget amount (Dent and Barry, 2017). Accounts receivable ageing reports : It is a periodic report that categorizes a company's

accounts receivable according to the length of time an invoice has been outstanding. It

helps in determining the financial health of company's customers and their ability to pay

their debts. Airdri Ltd. can use these reports so as to monitor its collection policies to

reduce old bad debts and maintain liquidity of the company. Job cost reports : These reports are used to identify cost, expenses and financial

efficiency and profitability of each particular job. These reports help in evaluating the

projects that are more profitable than others and focusing efforts on such jobs. Costs of

each job can be evaluated and waste areas can be identified to reduce overall costs. Airdri

Ltd. can use these reports to decide the pricing strategies of the company and reduce

production costs with providing good quality products (Khan and Jain, 2018).

Inventory and manufacturing reports : The proper reporting and accounting of

inventory increase the usefulness of financial statements for potential and actual

investors. These reports help in maintaining a balance between inventory investment and

customer service. They contain labour cost, per unit overhead cost and wastages

concerned with inventory which helps the managers to establish a comparison between

different processes of inventory management and introduce improvement if required.

Airdri Ltd. can use this system to manage the inventory levels of hand dryers and control

their manufacturing costs.

Benefits of management accounting systems and their application

Management

Accounting

Systems

Benefits Application

Job costing

system

Help the managers to

calculate the profit earned on

individual jobs and ascertain

if it should be pursued in

future.

Evaluation of quality of work

done.

Airdri Ltd. can use this

system to determine the costs

of different types of hand

dryers it produces based on

their requirements (Lin and

et. al., 2018).

Price optimising

system

Evaluate the customer

behaviour based on prices of

the products.

Helps in determining prices

that maximizes profits.

Airdri Ltd. can use this

system to reduce cost of

operations and set

competitive prices for

products/services.

Cost accounting

system

Helps in controlling and

managing costs of materials,

labour and overhead costs.

Correct business policies can

be formulated based on cost

information.

Airdri Ltd. can use this

system in correct

ascertainment of cost of

products and control them by

formulating appropriate

policies.

Inventory

management

-Improves the accuracy of inventory -Airdri Ltd. can use this system to

maintain sufficient stock of the

customer service. They contain labour cost, per unit overhead cost and wastages

concerned with inventory which helps the managers to establish a comparison between

different processes of inventory management and introduce improvement if required.

Airdri Ltd. can use this system to manage the inventory levels of hand dryers and control

their manufacturing costs.

Benefits of management accounting systems and their application

Management

Accounting

Systems

Benefits Application

Job costing

system

Help the managers to

calculate the profit earned on

individual jobs and ascertain

if it should be pursued in

future.

Evaluation of quality of work

done.

Airdri Ltd. can use this

system to determine the costs

of different types of hand

dryers it produces based on

their requirements (Lin and

et. al., 2018).

Price optimising

system

Evaluate the customer

behaviour based on prices of

the products.

Helps in determining prices

that maximizes profits.

Airdri Ltd. can use this

system to reduce cost of

operations and set

competitive prices for

products/services.

Cost accounting

system

Helps in controlling and

managing costs of materials,

labour and overhead costs.

Correct business policies can

be formulated based on cost

information.

Airdri Ltd. can use this

system in correct

ascertainment of cost of

products and control them by

formulating appropriate

policies.

Inventory

management

-Improves the accuracy of inventory -Airdri Ltd. can use this system to

maintain sufficient stock of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

system orders.

- Costs of warehousing extra

products can be reduced.

products on need basis of the

customers.

Integration of management accounting systems and management accounting reporting within

organisational processes

Type of reporting Integration with Airdri Ltd. processes

Budget report Helps in concentrating of business activities on targeted

results and objectives in a better way.

Accounts receivable ageing

report

Helps in making efforts towards timely collection of accounts

receivable and creation of proper collection policy.

Job cost report Helps in determining prices and reducing overall costs of the

product.

Inventory and manufacturing

report

Helps in better management of inventory levels and

manufacturing cost and accurately estimating the required

level of inventory level.

LO 2

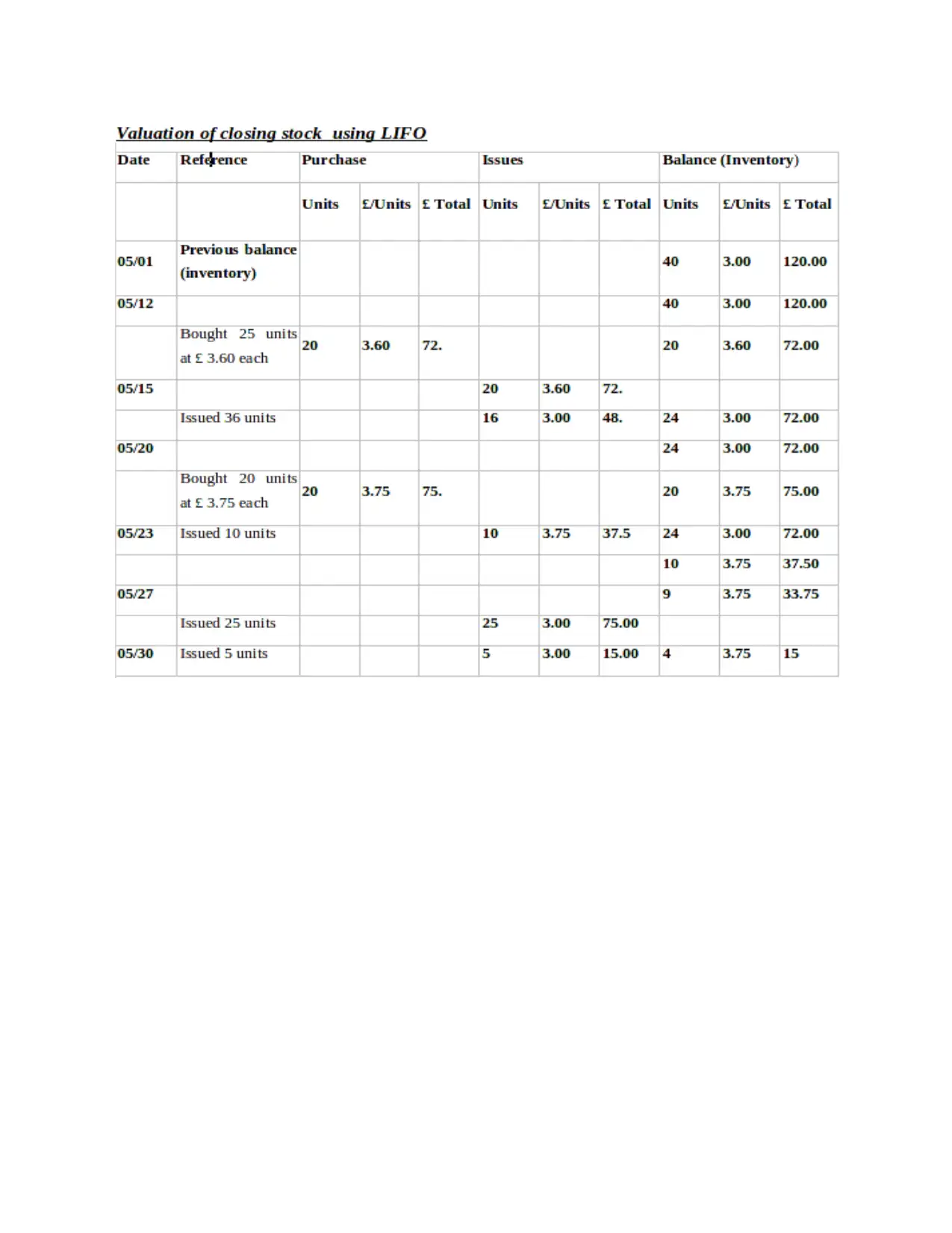

Calculation of costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs

Cost is the monetary valuation of effort, material, origins, time and substitute consumed,

risk incurred and opportunity forgone in production and delivery of a good or service. For the

preparation of income statement marginal and absorption costings can be used which are

explained as follows :

Marginal costing : It is the cost of one additional unit of output. This concept is used to

determine the optimum production quantity for a company where it costs the least amount to

produce additional units. Variable cost is charged to units of cost, while fixed costs for the period

is completely written off against the contribution (Mokhtar, Jusoh and Zulkifli, 2016).

- Costs of warehousing extra

products can be reduced.

products on need basis of the

customers.

Integration of management accounting systems and management accounting reporting within

organisational processes

Type of reporting Integration with Airdri Ltd. processes

Budget report Helps in concentrating of business activities on targeted

results and objectives in a better way.

Accounts receivable ageing

report

Helps in making efforts towards timely collection of accounts

receivable and creation of proper collection policy.

Job cost report Helps in determining prices and reducing overall costs of the

product.

Inventory and manufacturing

report

Helps in better management of inventory levels and

manufacturing cost and accurately estimating the required

level of inventory level.

LO 2

Calculation of costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs

Cost is the monetary valuation of effort, material, origins, time and substitute consumed,

risk incurred and opportunity forgone in production and delivery of a good or service. For the

preparation of income statement marginal and absorption costings can be used which are

explained as follows :

Marginal costing : It is the cost of one additional unit of output. This concept is used to

determine the optimum production quantity for a company where it costs the least amount to

produce additional units. Variable cost is charged to units of cost, while fixed costs for the period

is completely written off against the contribution (Mokhtar, Jusoh and Zulkifli, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing : It is a method of calculating the cost of a particular product by

taking into account indirect expenses as well as direct costs. Both variable and fixed costs are

included. A portion of fixed overhead is allocated to each unit of product along with

manufacturing cost.

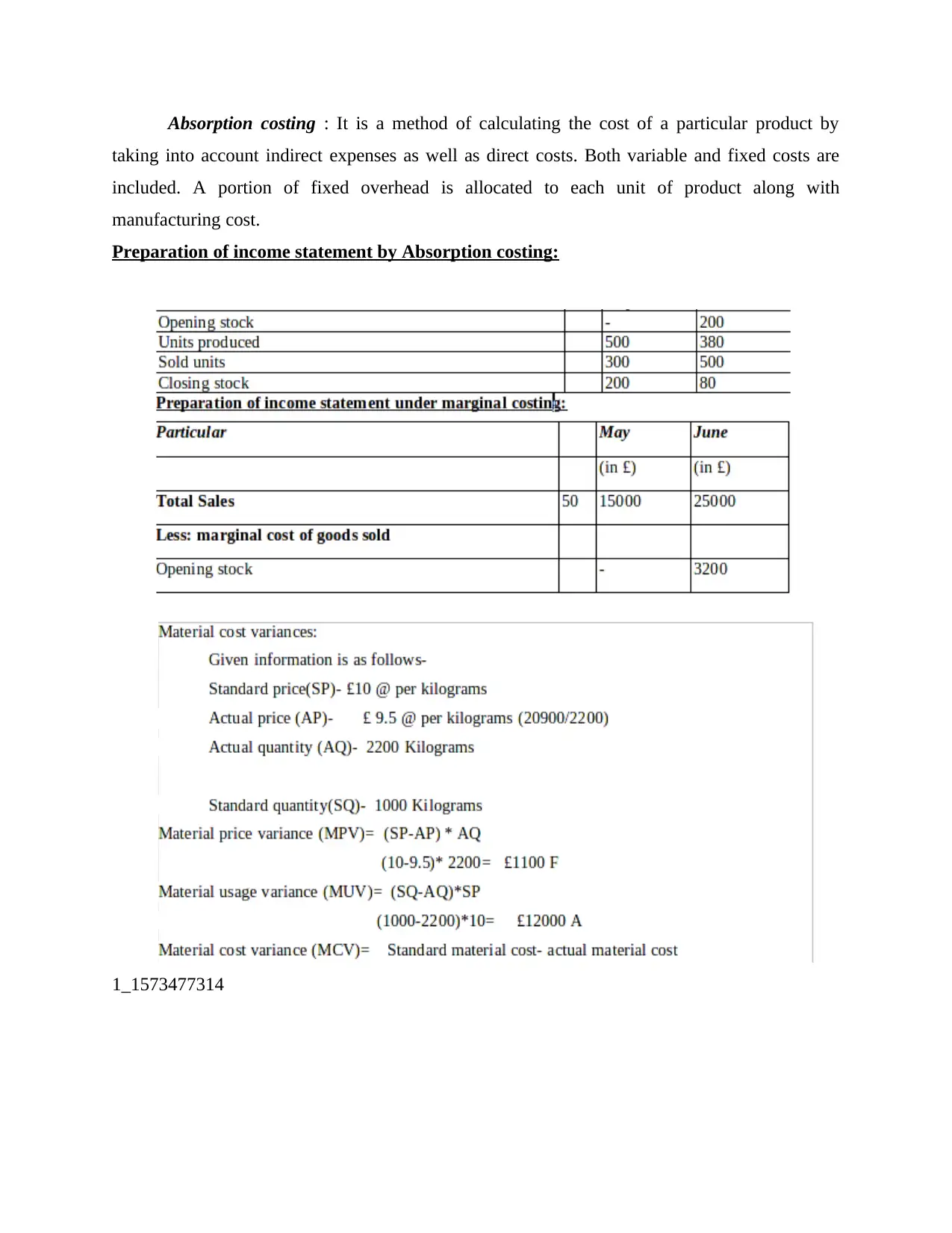

Preparation of income statement by Absorption costing:

1_1573477314

taking into account indirect expenses as well as direct costs. Both variable and fixed costs are

included. A portion of fixed overhead is allocated to each unit of product along with

manufacturing cost.

Preparation of income statement by Absorption costing:

1_1573477314

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

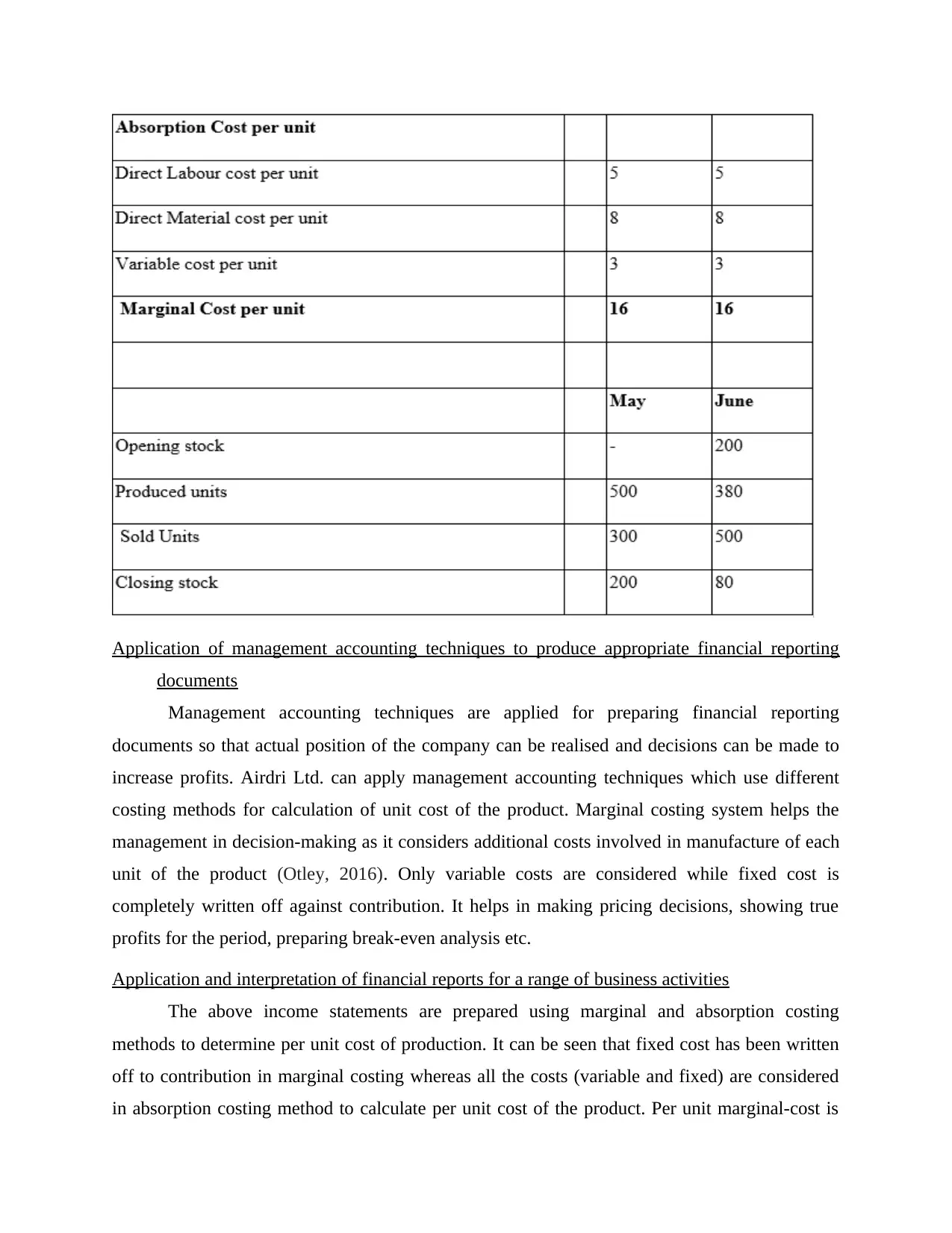

Application of management accounting techniques to produce appropriate financial reporting

documents

Management accounting techniques are applied for preparing financial reporting

documents so that actual position of the company can be realised and decisions can be made to

increase profits. Airdri Ltd. can apply management accounting techniques which use different

costing methods for calculation of unit cost of the product. Marginal costing system helps the

management in decision-making as it considers additional costs involved in manufacture of each

unit of the product (Otley, 2016). Only variable costs are considered while fixed cost is

completely written off against contribution. It helps in making pricing decisions, showing true

profits for the period, preparing break-even analysis etc.

Application and interpretation of financial reports for a range of business activities

The above income statements are prepared using marginal and absorption costing

methods to determine per unit cost of production. It can be seen that fixed cost has been written

off to contribution in marginal costing whereas all the costs (variable and fixed) are considered

in absorption costing method to calculate per unit cost of the product. Per unit marginal-cost is

documents

Management accounting techniques are applied for preparing financial reporting

documents so that actual position of the company can be realised and decisions can be made to

increase profits. Airdri Ltd. can apply management accounting techniques which use different

costing methods for calculation of unit cost of the product. Marginal costing system helps the

management in decision-making as it considers additional costs involved in manufacture of each

unit of the product (Otley, 2016). Only variable costs are considered while fixed cost is

completely written off against contribution. It helps in making pricing decisions, showing true

profits for the period, preparing break-even analysis etc.

Application and interpretation of financial reports for a range of business activities

The above income statements are prepared using marginal and absorption costing

methods to determine per unit cost of production. It can be seen that fixed cost has been written

off to contribution in marginal costing whereas all the costs (variable and fixed) are considered

in absorption costing method to calculate per unit cost of the product. Per unit marginal-cost is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

£16 and per unit absorption-cost is £26.53. Net profit as per marginal costing and absorption

costing are £5750 and £9792.4 respectively for Airdri Ltd. for the month of June. The net profit

of the company has increased in the month of June as compared to May which indicates that the

company is growing in the market.

LO 3

Advantages and disadvantages of different types of planning tools used for budgetary control

Budget is a financial plan for a defined period and includes planned sales volumes and

revenues, resource quantities, costs and expenses, assets, liabilities and cash flows. Budget is an

internal tools that help the management in setting goals, measuring outcomes and planning for

contingencies. These help in projecting sales trend, cost trends and overall economic outlook of

the market (Budgeting and business planning. 2019).

Budgetary control is the process by which budgets are prepared for the future period and

are compared with actual performance to find out out any deviations from the estimated budget

so that corrective actions can be taken by the management.

Different types of planning tools

The types of planning tools used for budgetary control are :

Budget Variance- It is a periodic measure which is used to quantify the difference between

budgeted and actual performance of the business. It can help Airdri Ltd. in identifying causes of

variation in income and expenses from the budgeted amounts and the remedies for reduction of

such variance.

Advantages- Help the managers in making efficient, detailed and forward looking

budgetary decisions. It also helps in identifying the changes that are required in business strategy

so that the costs can be controlled and responsibility can be assigned to make expenses only

according to the estimated budgets.

Disadvantages- The variance can only be realised at the end of a quarter and this may

lead to a delay in remedial actions; a detailed analysis of every factor needs to be done so as to

identify the root cause of such deviation.

Flexible Budget-This budget adjusts or flexes with change in revenue and expenses, based on

the amount of sales activity that actually occurs. Airdri Ltd. can modify the budget during the

year for actual sales levels, changes in cost of production or any change in business operations.

costing are £5750 and £9792.4 respectively for Airdri Ltd. for the month of June. The net profit

of the company has increased in the month of June as compared to May which indicates that the

company is growing in the market.

LO 3

Advantages and disadvantages of different types of planning tools used for budgetary control

Budget is a financial plan for a defined period and includes planned sales volumes and

revenues, resource quantities, costs and expenses, assets, liabilities and cash flows. Budget is an

internal tools that help the management in setting goals, measuring outcomes and planning for

contingencies. These help in projecting sales trend, cost trends and overall economic outlook of

the market (Budgeting and business planning. 2019).

Budgetary control is the process by which budgets are prepared for the future period and

are compared with actual performance to find out out any deviations from the estimated budget

so that corrective actions can be taken by the management.

Different types of planning tools

The types of planning tools used for budgetary control are :

Budget Variance- It is a periodic measure which is used to quantify the difference between

budgeted and actual performance of the business. It can help Airdri Ltd. in identifying causes of

variation in income and expenses from the budgeted amounts and the remedies for reduction of

such variance.

Advantages- Help the managers in making efficient, detailed and forward looking

budgetary decisions. It also helps in identifying the changes that are required in business strategy

so that the costs can be controlled and responsibility can be assigned to make expenses only

according to the estimated budgets.

Disadvantages- The variance can only be realised at the end of a quarter and this may

lead to a delay in remedial actions; a detailed analysis of every factor needs to be done so as to

identify the root cause of such deviation.

Flexible Budget-This budget adjusts or flexes with change in revenue and expenses, based on

the amount of sales activity that actually occurs. Airdri Ltd. can modify the budget during the

year for actual sales levels, changes in cost of production or any change in business operations.

Advantages- It can be updated with current data of revenues and expenses for current

operating conditions. It can be adjusted with changing costs and profit margins. Flexible budgets

can help in controlling costs as various costs can be adjusted depending on the needs of the

organisation.

Disadvantages -It maybe confusing to use and requires an expert to mould the budget as

per requirement. It also requires high alertness to the changing conditions that leads to the

change in levels of sales/activities.

Master Budget- It is the sum total of all the divisional budgets that is prepared by all the

divisions. It includes financial planning, cash-flow forecast and budgeted profit and loss account

and balance sheet of the organisation (Yigitbasioglu, 2016).

Advantages - A complete overview of the company's budget can be gained. It reveals

about the earning and spending of the company as a whole. Master budge equals master planning

and helps in identifying problems and plan ahead.

Disadvantages - It is difficult to identify the department that is spending more. A master

budget is also difficult to update as it includes many categories and numbers of different

departments as a whole.

Different planning tools and their application for preparing and forecasting budgets

Organisations use different planning tools to prepare and forecast budgets. These tools

help ensure companies don't overspend and run out of cash. Budgeting and forecasting provides

a specific direction to the business so that it works within a framework and make decisions that

are forward looking. Airdri Ltd. can use budget variance in determining any accounting

discrepancy that led to the variance in estimated and actual amounts of the budget. The causes of

variation in incomes and expenses can be identified which help managers in making strategic

decisions to correct them. Flexible budgets can be used by the company to update its budget

based on unexpected expenses or fluctuations in income. These budgets can be changed with

change in activities of the company within the period for which budget has been prepared.

Master budget helps in integrating the activities of various departments of the company and

coordinating them so that a complete overview of the conditions of the company can be

ascertained (Pandey, 2015).

operating conditions. It can be adjusted with changing costs and profit margins. Flexible budgets

can help in controlling costs as various costs can be adjusted depending on the needs of the

organisation.

Disadvantages -It maybe confusing to use and requires an expert to mould the budget as

per requirement. It also requires high alertness to the changing conditions that leads to the

change in levels of sales/activities.

Master Budget- It is the sum total of all the divisional budgets that is prepared by all the

divisions. It includes financial planning, cash-flow forecast and budgeted profit and loss account

and balance sheet of the organisation (Yigitbasioglu, 2016).

Advantages - A complete overview of the company's budget can be gained. It reveals

about the earning and spending of the company as a whole. Master budge equals master planning

and helps in identifying problems and plan ahead.

Disadvantages - It is difficult to identify the department that is spending more. A master

budget is also difficult to update as it includes many categories and numbers of different

departments as a whole.

Different planning tools and their application for preparing and forecasting budgets

Organisations use different planning tools to prepare and forecast budgets. These tools

help ensure companies don't overspend and run out of cash. Budgeting and forecasting provides

a specific direction to the business so that it works within a framework and make decisions that

are forward looking. Airdri Ltd. can use budget variance in determining any accounting

discrepancy that led to the variance in estimated and actual amounts of the budget. The causes of

variation in incomes and expenses can be identified which help managers in making strategic

decisions to correct them. Flexible budgets can be used by the company to update its budget

based on unexpected expenses or fluctuations in income. These budgets can be changed with

change in activities of the company within the period for which budget has been prepared.

Master budget helps in integrating the activities of various departments of the company and

coordinating them so that a complete overview of the conditions of the company can be

ascertained (Pandey, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.