Financial Analysis and Management Accounting Report for Zylla Company

VerifiedAdded on 2020/12/29

|14

|4219

|164

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Zylla Company. It begins with an introduction to management accounting, outlining its essential requirements and various reporting methods. The report delves into specific costing techniques, including absorption and marginal costing, demonstrating their application through detailed calculations and interpretations of financial data. Furthermore, it explores planning and budgetary control systems, evaluating their merits and demerits. The report also addresses the adaptation of management accounting systems to enhance organizational performance. The financial analysis covers income statements, cost analyses, and the distribution of income across different functional areas within the company. The report emphasizes the importance of cost accounting systems, inventory management, and job costing systems. The report includes job cost reports, inventory management reports, operating budget reports, and performance reports to analyze the financial data of the company. In addition, the report covers the impact of price optimization and the significance of accounts receivable aging reports. The report concludes with an overview of the key findings and recommendations for improving financial management within Zylla Company.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1 Management accounting and essential requirements............................................................1

P.2 Different methods used for management accounting reporting............................................2

TASK 2............................................................................................................................................4

P.3 Calculating costing by using marginal and absorption costing............................................4

TASK 3............................................................................................................................................6

P.4 Planning and budgetary control system with their merits and demerits...............................6

TASK 4............................................................................................................................................7

P.5 Adapting management accounting systems..........................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1 Management accounting and essential requirements............................................................1

P.2 Different methods used for management accounting reporting............................................2

TASK 2............................................................................................................................................4

P.3 Calculating costing by using marginal and absorption costing............................................4

TASK 3............................................................................................................................................6

P.4 Planning and budgetary control system with their merits and demerits...............................6

TASK 4............................................................................................................................................7

P.5 Adapting management accounting systems..........................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is a process to manage financial factor in working environment.

In this context, future decision-making is based on financial sector. On the other hand, proper

financial management is the most necessary with activity of some methods acting to be used in

working situation. This report is based on Zylla. Further, it covered income statement and cost

analyses management is help to distribution of income in different field internal working

environment (Banerjee, 2014). The cost and tax write-off of the explanation scheme. As the

calculation cost to set up the commercial enterprise gain statement of the cited organisations.

TASK 1

P1. Management Accounting and essential requirements

Management system is also known as cost system of rules and social control system. It is

a cognitive process used for examine business operations and costs to gear up records, internal

fiscal reports and making known to aid decision maker, conclusion making administration goals.

In simple spoken communication, act of ready cost accounting and financial data and translating

it to useful subject matter for administration federal agency within Zylla firm (Bloomfield,

2015). Management explanation also assistance to accomplish better preparation and

powerfulness over the firm.

Cost Accounting System: In this context, Cost account scheme estimates and measure

expenditure of employment and goods as well as outlay of business concern units and

beginning, such as section. It supply applicable and of import cost data to the managing

director, which assist them to impotence business concern enterprise action and make

thought of activity and thought for forthcoming within Zylla firm effectively and with

efficiency.

Benefits:

In this context, cost accounting determination of cost of product and services, which is

helpful for manager?

This is also helped at the time of set selling price of the product. In addition, cost is help

to increase customer in demand and profitability.

Inventory Management System: In this context, stock of any resources or product which is

used to improve internal environment of business activity (De, 2015). Inventory administration

grouping is a set of programme and argumentation which pull off and powerfulness the

1

Management accounting is a process to manage financial factor in working environment.

In this context, future decision-making is based on financial sector. On the other hand, proper

financial management is the most necessary with activity of some methods acting to be used in

working situation. This report is based on Zylla. Further, it covered income statement and cost

analyses management is help to distribution of income in different field internal working

environment (Banerjee, 2014). The cost and tax write-off of the explanation scheme. As the

calculation cost to set up the commercial enterprise gain statement of the cited organisations.

TASK 1

P1. Management Accounting and essential requirements

Management system is also known as cost system of rules and social control system. It is

a cognitive process used for examine business operations and costs to gear up records, internal

fiscal reports and making known to aid decision maker, conclusion making administration goals.

In simple spoken communication, act of ready cost accounting and financial data and translating

it to useful subject matter for administration federal agency within Zylla firm (Bloomfield,

2015). Management explanation also assistance to accomplish better preparation and

powerfulness over the firm.

Cost Accounting System: In this context, Cost account scheme estimates and measure

expenditure of employment and goods as well as outlay of business concern units and

beginning, such as section. It supply applicable and of import cost data to the managing

director, which assist them to impotence business concern enterprise action and make

thought of activity and thought for forthcoming within Zylla firm effectively and with

efficiency.

Benefits:

In this context, cost accounting determination of cost of product and services, which is

helpful for manager?

This is also helped at the time of set selling price of the product. In addition, cost is help

to increase customer in demand and profitability.

Inventory Management System: In this context, stock of any resources or product which is

used to improve internal environment of business activity (De, 2015). Inventory administration

grouping is a set of programme and argumentation which pull off and powerfulness the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

monitoring device levels of stock list and also determines what commonplace should be fill

again, what flat should be managed and kept up and measure which arrangement should order

efficaciously and with efficiency.

Benefits:

To be provide protraction against uncertainties, shortage of raw material.

To be focus on strategies planning and take advantages of economic scale. This is help to

manage work and improve production level.

Job Costing System:-

Occupation costing framework is a procedure of cost recording and gathering where the

ID of employment or any gathering is nearness for which the cost can be gathered or overseen.

Employment costing framework is utilized as a part of organizations, where the creation of an

item is 'one off' that is diverse for an individual client proficiently (Otley, 2015). It is appropriate

and solid for associations where work is embraced towards a unique prerequisite of a client and

each request take brief term similarly.

Benefits:

In this context, cost control planning and decision making process is to be involve to

improve internal environment performance.

This is to be determination of different types of profit and loss in organisation. In

addition, selling price must be inculcated in financial carrying into action.

Price Optimising System: In this context, program of activity which allows a steadfast to know

the old customer' sensitiveness to modification the commodity monetary value according to the

profitableness levels within Zylla firm effectual (Altawati, 2018). Price optimising grouping use

by business organization to tailor evaluation for various customized based on their response to

modification in different pricing. This is focus on how the customer will be respond from

different price on similar products.

Benefits :

It is to be focus on increase the level of profitability and change level of customer.

To be defining the profitability based on existing clients.

2

again, what flat should be managed and kept up and measure which arrangement should order

efficaciously and with efficiency.

Benefits:

To be provide protraction against uncertainties, shortage of raw material.

To be focus on strategies planning and take advantages of economic scale. This is help to

manage work and improve production level.

Job Costing System:-

Occupation costing framework is a procedure of cost recording and gathering where the

ID of employment or any gathering is nearness for which the cost can be gathered or overseen.

Employment costing framework is utilized as a part of organizations, where the creation of an

item is 'one off' that is diverse for an individual client proficiently (Otley, 2015). It is appropriate

and solid for associations where work is embraced towards a unique prerequisite of a client and

each request take brief term similarly.

Benefits:

In this context, cost control planning and decision making process is to be involve to

improve internal environment performance.

This is to be determination of different types of profit and loss in organisation. In

addition, selling price must be inculcated in financial carrying into action.

Price Optimising System: In this context, program of activity which allows a steadfast to know

the old customer' sensitiveness to modification the commodity monetary value according to the

profitableness levels within Zylla firm effectual (Altawati, 2018). Price optimising grouping use

by business organization to tailor evaluation for various customized based on their response to

modification in different pricing. This is focus on how the customer will be respond from

different price on similar products.

Benefits :

It is to be focus on increase the level of profitability and change level of customer.

To be defining the profitability based on existing clients.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

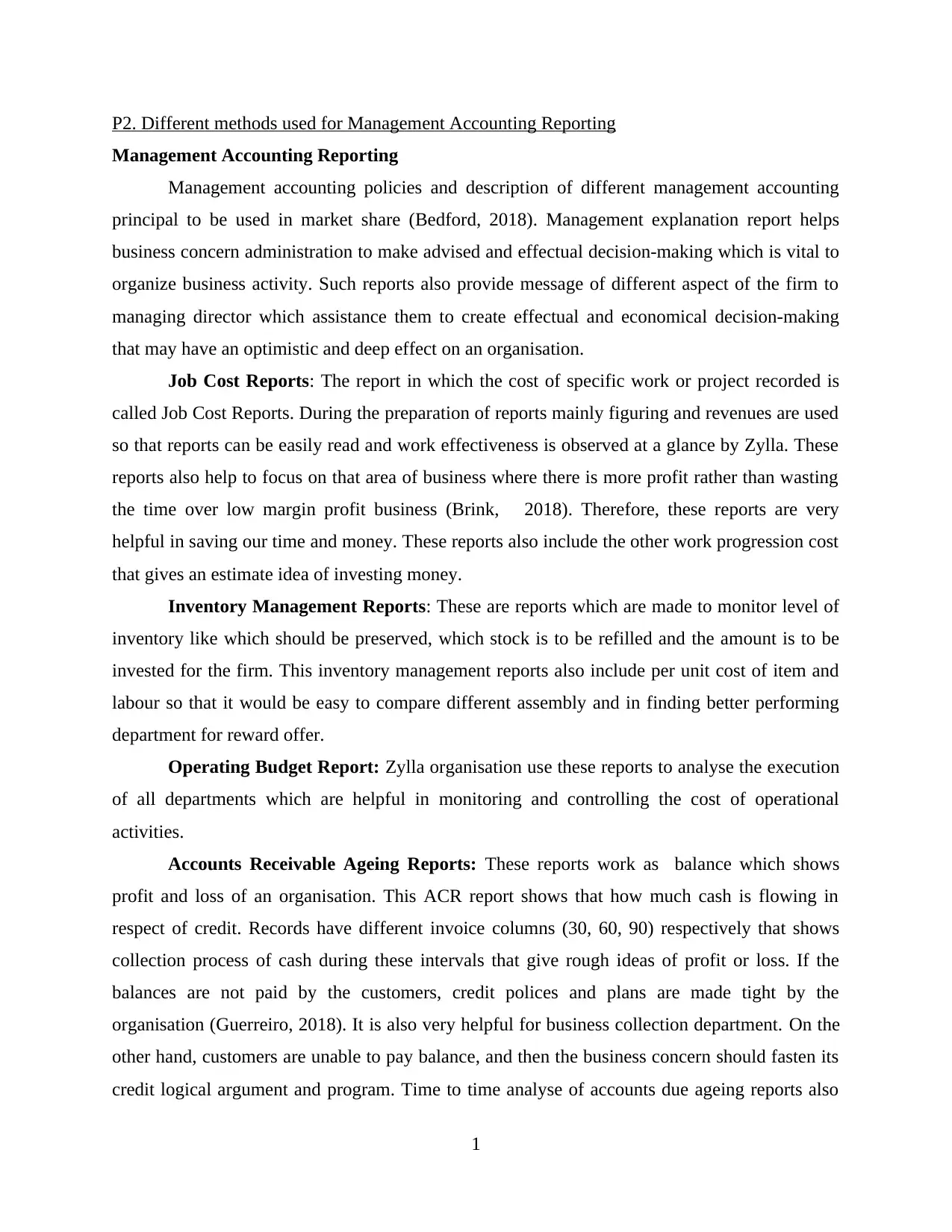

P2. Different methods used for Management Accounting Reporting

Management Accounting Reporting

Management accounting policies and description of different management accounting

principal to be used in market share (Bedford, 2018). Management explanation report helps

business concern administration to make advised and effectual decision-making which is vital to

organize business activity. Such reports also provide message of different aspect of the firm to

managing director which assistance them to create effectual and economical decision-making

that may have an optimistic and deep effect on an organisation.

Job Cost Reports: The report in which the cost of specific work or project recorded is

called Job Cost Reports. During the preparation of reports mainly figuring and revenues are used

so that reports can be easily read and work effectiveness is observed at a glance by Zylla. These

reports also help to focus on that area of business where there is more profit rather than wasting

the time over low margin profit business (Brink, 2018). Therefore, these reports are very

helpful in saving our time and money. These reports also include the other work progression cost

that gives an estimate idea of investing money.

Inventory Management Reports: These are reports which are made to monitor level of

inventory like which should be preserved, which stock is to be refilled and the amount is to be

invested for the firm. This inventory management reports also include per unit cost of item and

labour so that it would be easy to compare different assembly and in finding better performing

department for reward offer.

Operating Budget Report: Zylla organisation use these reports to analyse the execution

of all departments which are helpful in monitoring and controlling the cost of operational

activities.

Accounts Receivable Ageing Reports: These reports work as balance which shows

profit and loss of an organisation. This ACR report shows that how much cash is flowing in

respect of credit. Records have different invoice columns (30, 60, 90) respectively that shows

collection process of cash during these intervals that give rough ideas of profit or loss. If the

balances are not paid by the customers, credit polices and plans are made tight by the

organisation (Guerreiro, 2018). It is also very helpful for business collection department. On the

other hand, customers are unable to pay balance, and then the business concern should fasten its

credit logical argument and program. Time to time analyse of accounts due ageing reports also

1

Management Accounting Reporting

Management accounting policies and description of different management accounting

principal to be used in market share (Bedford, 2018). Management explanation report helps

business concern administration to make advised and effectual decision-making which is vital to

organize business activity. Such reports also provide message of different aspect of the firm to

managing director which assistance them to create effectual and economical decision-making

that may have an optimistic and deep effect on an organisation.

Job Cost Reports: The report in which the cost of specific work or project recorded is

called Job Cost Reports. During the preparation of reports mainly figuring and revenues are used

so that reports can be easily read and work effectiveness is observed at a glance by Zylla. These

reports also help to focus on that area of business where there is more profit rather than wasting

the time over low margin profit business (Brink, 2018). Therefore, these reports are very

helpful in saving our time and money. These reports also include the other work progression cost

that gives an estimate idea of investing money.

Inventory Management Reports: These are reports which are made to monitor level of

inventory like which should be preserved, which stock is to be refilled and the amount is to be

invested for the firm. This inventory management reports also include per unit cost of item and

labour so that it would be easy to compare different assembly and in finding better performing

department for reward offer.

Operating Budget Report: Zylla organisation use these reports to analyse the execution

of all departments which are helpful in monitoring and controlling the cost of operational

activities.

Accounts Receivable Ageing Reports: These reports work as balance which shows

profit and loss of an organisation. This ACR report shows that how much cash is flowing in

respect of credit. Records have different invoice columns (30, 60, 90) respectively that shows

collection process of cash during these intervals that give rough ideas of profit or loss. If the

balances are not paid by the customers, credit polices and plans are made tight by the

organisation (Guerreiro, 2018). It is also very helpful for business collection department. On the

other hand, customers are unable to pay balance, and then the business concern should fasten its

credit logical argument and program. Time to time analyse of accounts due ageing reports also

1

assistance enterprise collection department to topographic point its old debts efficaciously and

with efficiency.

Performance Report: In performance report is help to internal department of

organisation about product and services are performed of group services. This also helps

production department inside organisation as well as marketing segmentation. It also activity

system to attempt gainfulness analytic thinking for commodity lines, market portion and go away

so that they gain their performance and profits efficaciously and expeditiously (Mussati, 2018).

These reports enable firms to restorative mensuration at place in order to bring off and relation

the costs which brings efficiency in the business trading operations effectively.

All such methods of management accounting are helping to take new decision-making

policies in organisation. Some changes are made to increase current market performance as per

needs of current market network. On the other hand, to make new strategies and plans for

increase the number of profitability and managing resources for future accomplishment. To

manage inventory level, account receivable report and operation management in organisation.

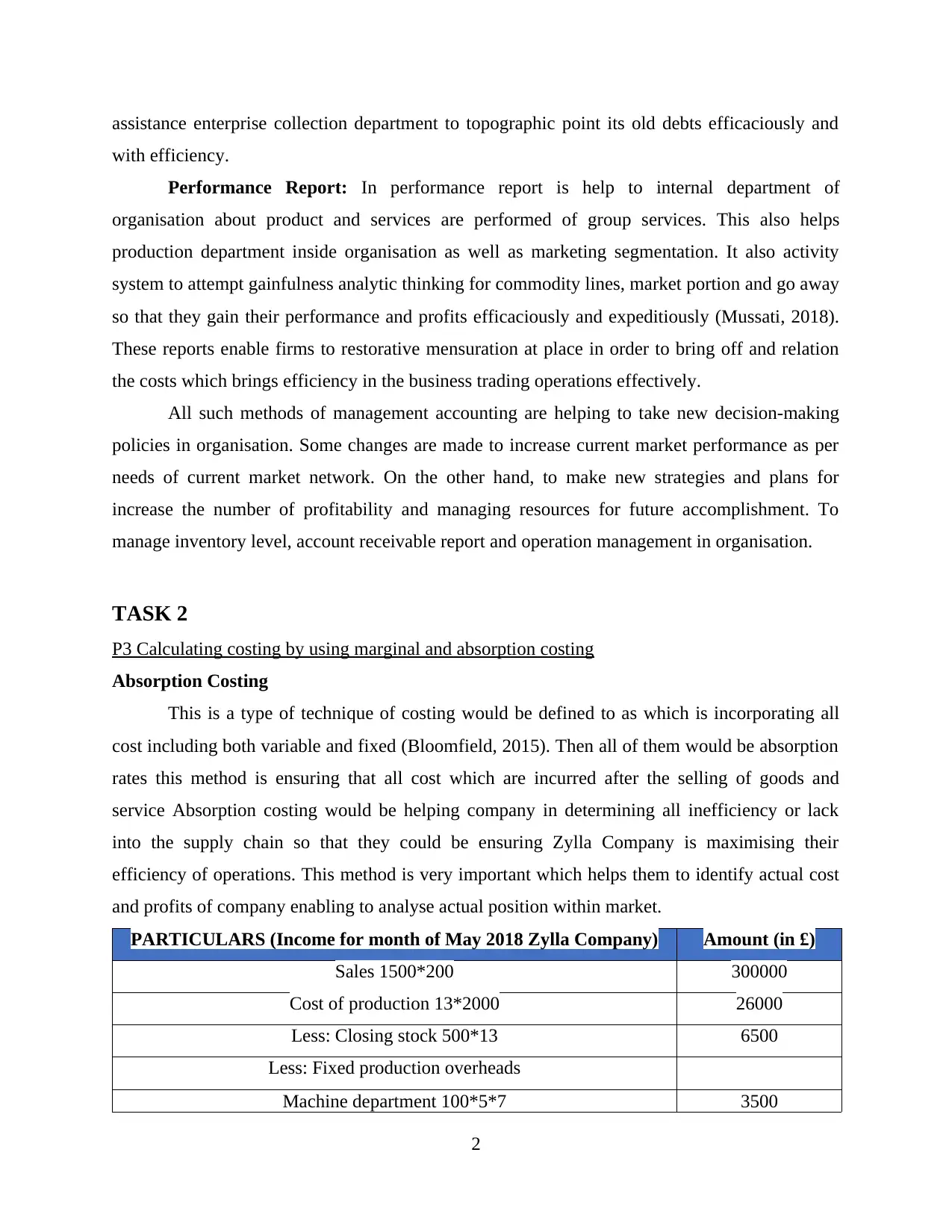

TASK 2

P3 Calculating costing by using marginal and absorption costing

Absorption Costing

This is a type of technique of costing would be defined to as which is incorporating all

cost including both variable and fixed (Bloomfield, 2015). Then all of them would be absorption

rates this method is ensuring that all cost which are incurred after the selling of goods and

service Absorption costing would be helping company in determining all inefficiency or lack

into the supply chain so that they could be ensuring Zylla Company is maximising their

efficiency of operations. This method is very important which helps them to identify actual cost

and profits of company enabling to analyse actual position within market.

PARTICULARS (Income for month of May 2018 Zylla Company) Amount (in £)

Sales 1500*200 300000

Cost of production 13*2000 26000

Less: Closing stock 500*13 6500

Less: Fixed production overheads

Machine department 100*5*7 3500

2

with efficiency.

Performance Report: In performance report is help to internal department of

organisation about product and services are performed of group services. This also helps

production department inside organisation as well as marketing segmentation. It also activity

system to attempt gainfulness analytic thinking for commodity lines, market portion and go away

so that they gain their performance and profits efficaciously and expeditiously (Mussati, 2018).

These reports enable firms to restorative mensuration at place in order to bring off and relation

the costs which brings efficiency in the business trading operations effectively.

All such methods of management accounting are helping to take new decision-making

policies in organisation. Some changes are made to increase current market performance as per

needs of current market network. On the other hand, to make new strategies and plans for

increase the number of profitability and managing resources for future accomplishment. To

manage inventory level, account receivable report and operation management in organisation.

TASK 2

P3 Calculating costing by using marginal and absorption costing

Absorption Costing

This is a type of technique of costing would be defined to as which is incorporating all

cost including both variable and fixed (Bloomfield, 2015). Then all of them would be absorption

rates this method is ensuring that all cost which are incurred after the selling of goods and

service Absorption costing would be helping company in determining all inefficiency or lack

into the supply chain so that they could be ensuring Zylla Company is maximising their

efficiency of operations. This method is very important which helps them to identify actual cost

and profits of company enabling to analyse actual position within market.

PARTICULARS (Income for month of May 2018 Zylla Company) Amount (in £)

Sales 1500*200 300000

Cost of production 13*2000 26000

Less: Closing stock 500*13 6500

Less: Fixed production overheads

Machine department 100*5*7 3500

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finishing department 5*20*4/6 150

Dispatch department 1*20*1/5 4

Gross profit 315846

Less: Packing box 0.50*2000 1000

Net Profit 314846

Interpretation:

In the above table which is depicting the actual cost of Zylla company would be enabling

them to recognise financial condition within markets including both fixed and variable expense.

So from total sales of company which is about 1500 units are sold with the per unit cost of about

200 which is about 300000 so this becomes the most important step in taking out the actual sales

per unit. Then the cost of production for company which is around £13 on 2000 total production

of about 26000. From this, we have to subtract the closing stock which is 500 multiplied by cost

per production of units £13 this will be about 6500. Then all fixed production overheads are to be

subtracted like that of cost of machinery, finishing and that related to dispatching of goods. With

the help of all these, gross profits for that period would be £315846 from this all variable

expense which is of packing around 1000 would be subtracted. From this whole calculation, net

profits for the month of May 2018 for Zylla Company would be £314846.

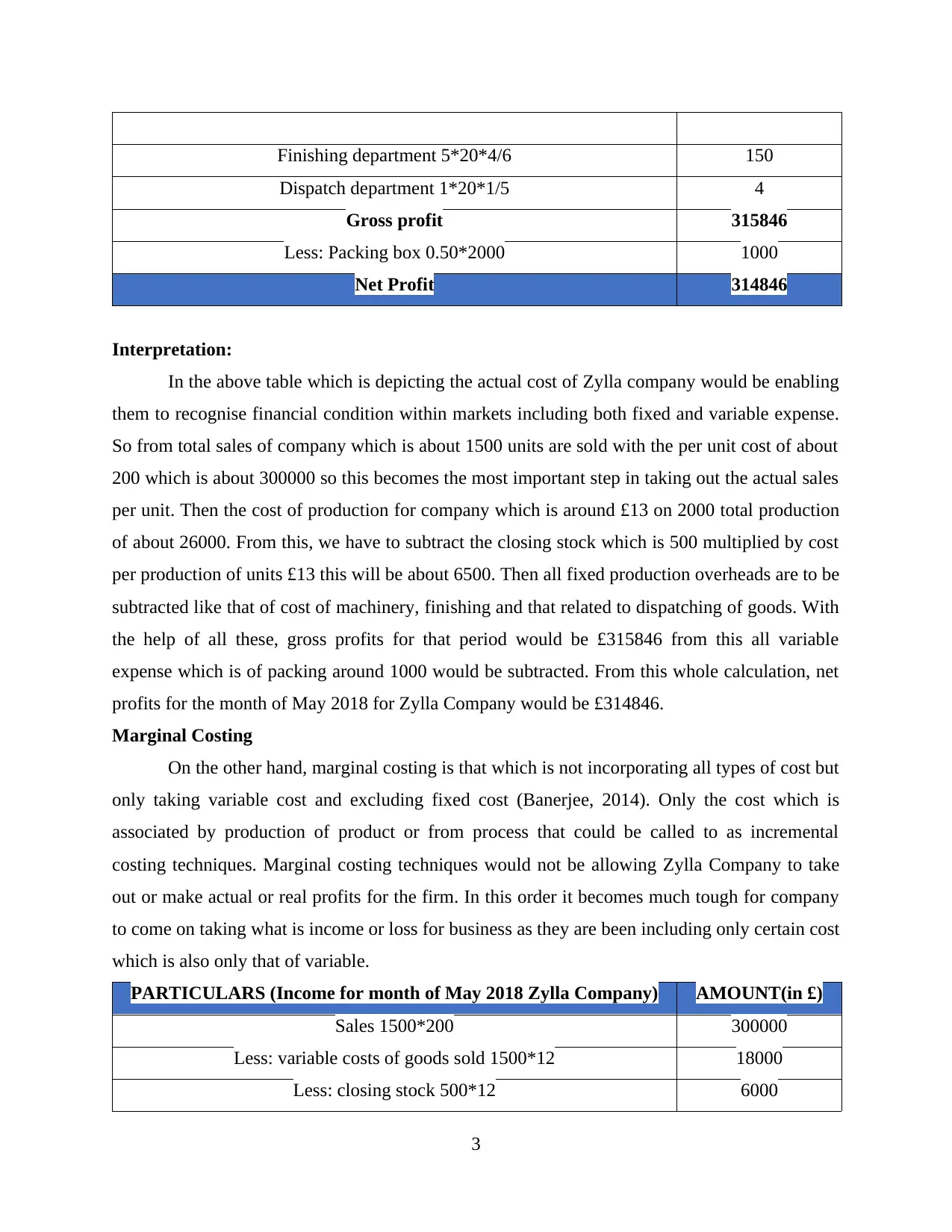

Marginal Costing

On the other hand, marginal costing is that which is not incorporating all types of cost but

only taking variable cost and excluding fixed cost (Banerjee, 2014). Only the cost which is

associated by production of product or from process that could be called to as incremental

costing techniques. Marginal costing techniques would not be allowing Zylla Company to take

out or make actual or real profits for the firm. In this order it becomes much tough for company

to come on taking what is income or loss for business as they are been including only certain cost

which is also only that of variable.

PARTICULARS (Income for month of May 2018 Zylla Company) AMOUNT(in £)

Sales 1500*200 300000

Less: variable costs of goods sold 1500*12 18000

Less: closing stock 500*12 6000

3

Dispatch department 1*20*1/5 4

Gross profit 315846

Less: Packing box 0.50*2000 1000

Net Profit 314846

Interpretation:

In the above table which is depicting the actual cost of Zylla company would be enabling

them to recognise financial condition within markets including both fixed and variable expense.

So from total sales of company which is about 1500 units are sold with the per unit cost of about

200 which is about 300000 so this becomes the most important step in taking out the actual sales

per unit. Then the cost of production for company which is around £13 on 2000 total production

of about 26000. From this, we have to subtract the closing stock which is 500 multiplied by cost

per production of units £13 this will be about 6500. Then all fixed production overheads are to be

subtracted like that of cost of machinery, finishing and that related to dispatching of goods. With

the help of all these, gross profits for that period would be £315846 from this all variable

expense which is of packing around 1000 would be subtracted. From this whole calculation, net

profits for the month of May 2018 for Zylla Company would be £314846.

Marginal Costing

On the other hand, marginal costing is that which is not incorporating all types of cost but

only taking variable cost and excluding fixed cost (Banerjee, 2014). Only the cost which is

associated by production of product or from process that could be called to as incremental

costing techniques. Marginal costing techniques would not be allowing Zylla Company to take

out or make actual or real profits for the firm. In this order it becomes much tough for company

to come on taking what is income or loss for business as they are been including only certain cost

which is also only that of variable.

PARTICULARS (Income for month of May 2018 Zylla Company) AMOUNT(in £)

Sales 1500*200 300000

Less: variable costs of goods sold 1500*12 18000

Less: closing stock 500*12 6000

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Add: cost of production 2000*12 24000

Production contribution 300000

Less: Variable non- manufacturing costs

Packing boxes 0.50* 2000 1000

Total contribution expenses 299000

Less: Expenses

Fixed manufacturing costs 100*7*5 3500

Finishing department 2500

Dispatch department 1000

Net Profit 292000

Interpretation:

From the above table, it could be concluded that if a company is taking cost by using

marginal costing they would be arriving at profits which is not actual. If Zylla Company is

selling about 1500 units in the month of May 2018, each at £200 so their total sales for that

month will be around 300000 which is same as that of absorption costing. Then they would be

subtracting variable cost of goods sold of 1500 units at £12 each and is coming to about 18000.

After this if they are to less closing stock during that period which is about 6000 and

adding cost of production around 24000 they would be getting production contribution to about

300000. Then they have to subtract variable non- manufacturing cost or packing of all boxes to

about 1000 but in this we would also be including total contribution expense which was not done

in above absorption costing techniques. Then in last stage, all expenses would be subtracted

which are fixed manufacturing cost, finishing and dispatch department so the net profits would

be around £292000.

TASK 3

P4 Planning and budgetary control system with their merits and demerits

Activity Based Budgeting

This type of budgeting techniques would be calling for taking out cost of all different

types of activities which are been operated within company. Activities like manufacturing,

packaging, finance, production or that related to marketing which company need to operate on

daily bases (Gooneratne and Hoque, 2016). All these activities need to be allotted cost so that it

4

Production contribution 300000

Less: Variable non- manufacturing costs

Packing boxes 0.50* 2000 1000

Total contribution expenses 299000

Less: Expenses

Fixed manufacturing costs 100*7*5 3500

Finishing department 2500

Dispatch department 1000

Net Profit 292000

Interpretation:

From the above table, it could be concluded that if a company is taking cost by using

marginal costing they would be arriving at profits which is not actual. If Zylla Company is

selling about 1500 units in the month of May 2018, each at £200 so their total sales for that

month will be around 300000 which is same as that of absorption costing. Then they would be

subtracting variable cost of goods sold of 1500 units at £12 each and is coming to about 18000.

After this if they are to less closing stock during that period which is about 6000 and

adding cost of production around 24000 they would be getting production contribution to about

300000. Then they have to subtract variable non- manufacturing cost or packing of all boxes to

about 1000 but in this we would also be including total contribution expense which was not done

in above absorption costing techniques. Then in last stage, all expenses would be subtracted

which are fixed manufacturing cost, finishing and dispatch department so the net profits would

be around £292000.

TASK 3

P4 Planning and budgetary control system with their merits and demerits

Activity Based Budgeting

This type of budgeting techniques would be calling for taking out cost of all different

types of activities which are been operated within company. Activities like manufacturing,

packaging, finance, production or that related to marketing which company need to operate on

daily bases (Gooneratne and Hoque, 2016). All these activities need to be allotted cost so that it

4

becomes easy for firm to identify which task is including how much cost. Activity based

budgeting technique is the best suited for that company which is manufacturing products or

having many different types of activities or task.

Merits

This type of technique would be helping in managing all cost related to each type of cost

so the operational efficiency could be enhanced.

Activity based budgeting would also be helping firm to optimally allocate overall cost to

firm based on activities done by them.

Demerits

This technique would be requiring highly experienced or skilled manager or accountant

who is having full and correct knowledge of identifying and allocating funds or cost

(Otley, 2015).

Time taken in identification and allocation would also be very high so there is a chance of

wasting time would be done by managers.

Zero Base Budgeting

This is the most used and widely accepted type of budgeting technique which is helping

manager in lowering down their burden by not incorporating last year’s budget or left over cost

to this current year (De Baerdemaeker and Bruggeman, 2015). Zero Base Budgeting or ZBB is a

technique used by firm in order to prepare new budget included in this year only and avoiding

last year cost. However, it is required on the part of manager of Zylla Company that they are

identifying merits and demerits of ZBB before using or applying it.

TASK 4

P.5 Adapting management accounting systems

There are some financial problems must be faced by organisation. On the other hand,

organisation becomes successful through completing challenges and facing problems inside as

well outside organisation. Some changes are made from long period as per the need of current

market network. One of this, commercial enterprise difficulty is a state of affairs for every

business concern to grow up and pull off their functional human action. Here are some financial

difficulty which an administration faces during their trading operations are as follows:-

Funding: - In this context, new business is needed more money and capital to start a new

venture in organisation. In addition, many problems are faced at time to take decision of

5

budgeting technique is the best suited for that company which is manufacturing products or

having many different types of activities or task.

Merits

This type of technique would be helping in managing all cost related to each type of cost

so the operational efficiency could be enhanced.

Activity based budgeting would also be helping firm to optimally allocate overall cost to

firm based on activities done by them.

Demerits

This technique would be requiring highly experienced or skilled manager or accountant

who is having full and correct knowledge of identifying and allocating funds or cost

(Otley, 2015).

Time taken in identification and allocation would also be very high so there is a chance of

wasting time would be done by managers.

Zero Base Budgeting

This is the most used and widely accepted type of budgeting technique which is helping

manager in lowering down their burden by not incorporating last year’s budget or left over cost

to this current year (De Baerdemaeker and Bruggeman, 2015). Zero Base Budgeting or ZBB is a

technique used by firm in order to prepare new budget included in this year only and avoiding

last year cost. However, it is required on the part of manager of Zylla Company that they are

identifying merits and demerits of ZBB before using or applying it.

TASK 4

P.5 Adapting management accounting systems

There are some financial problems must be faced by organisation. On the other hand,

organisation becomes successful through completing challenges and facing problems inside as

well outside organisation. Some changes are made from long period as per the need of current

market network. One of this, commercial enterprise difficulty is a state of affairs for every

business concern to grow up and pull off their functional human action. Here are some financial

difficulty which an administration faces during their trading operations are as follows:-

Funding: - In this context, new business is needed more money and capital to start a new

venture in organisation. In addition, many problems are faced at time to take decision of

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business expansion. In this context, organisation focuses on improving current market

network as well as overall development of organisation (Fullerton, 2014). On the other

hand, business necessarily backing option that it can cut down or remove these types of

problems effectively.

Cash flow: Cash flow is deliberate by takeoff expenses from business concern total

financial gain. Positive number of consequent shows the net financial gain of the

establishment and antagonistic Scribe the failure. Modest hard cash flow business interest

find problems to spread out their transaction and arrangement with antagonistic hard

medium of exchange flow have only few derived device for increase. Lack of creating

affirmation cash flow can begin too much liability for a concern interest which can sink it

for good.

Too much level of debt: In this context, there are too much debt is harmful for business

and operational level activity inside organisation. It is help to improve current market

level of organisation (Chenhall, 2018). Too much debt also adjacent the possibility for

approving loans from the banking concern and also financial support as well.

Commercial enterprise debts and possession can affect currency flow and revenues that

firm is hold to be bankrupt.

Poor financial management: - In this context, poor financial problem by commercial

enterprise managing director raise the fiscal monetary fund difficulty for the firm. Poor

social control, no proper research of markets, approximation competition will cause

difficulty which impact revenue content and risk for wellness and property of steadfast.

Budgeting problem: In this context, budgeting is one of the most important parts for

internal and external working environment (Stafford, 2017). A mechanically and bolt

monetary fund can cut down the invention and inaugural at lower berth level. It can also

origin perceptual experience of partiality. Budget difficulty also feeling the enterprise

concern plan of action and programme as asymptomatic as decision-making effectual.

Characteristic of management accounting

Helping in decision-making: It helps to take new decisions in organisation and provide

relevant information from different sources such as financial and cost accounting. This

helps to improve current market network.

6

network as well as overall development of organisation (Fullerton, 2014). On the other

hand, business necessarily backing option that it can cut down or remove these types of

problems effectively.

Cash flow: Cash flow is deliberate by takeoff expenses from business concern total

financial gain. Positive number of consequent shows the net financial gain of the

establishment and antagonistic Scribe the failure. Modest hard cash flow business interest

find problems to spread out their transaction and arrangement with antagonistic hard

medium of exchange flow have only few derived device for increase. Lack of creating

affirmation cash flow can begin too much liability for a concern interest which can sink it

for good.

Too much level of debt: In this context, there are too much debt is harmful for business

and operational level activity inside organisation. It is help to improve current market

level of organisation (Chenhall, 2018). Too much debt also adjacent the possibility for

approving loans from the banking concern and also financial support as well.

Commercial enterprise debts and possession can affect currency flow and revenues that

firm is hold to be bankrupt.

Poor financial management: - In this context, poor financial problem by commercial

enterprise managing director raise the fiscal monetary fund difficulty for the firm. Poor

social control, no proper research of markets, approximation competition will cause

difficulty which impact revenue content and risk for wellness and property of steadfast.

Budgeting problem: In this context, budgeting is one of the most important parts for

internal and external working environment (Stafford, 2017). A mechanically and bolt

monetary fund can cut down the invention and inaugural at lower berth level. It can also

origin perceptual experience of partiality. Budget difficulty also feeling the enterprise

concern plan of action and programme as asymptomatic as decision-making effectual.

Characteristic of management accounting

Helping in decision-making: It helps to take new decisions in organisation and provide

relevant information from different sources such as financial and cost accounting. This

helps to improve current market network.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Provide new data: - An effectual social control accountant renders required information

to the direction of concern. It is up to the social control that how they use and utilise this

data for solving their commercial enterprise and cost difficulty through effectual

decision-making (Klychova, 2018). Some changes are needed for future improvement in

organisation as well as development of overall management.

Selective nature: It is a potential to characteristic of management account that is only

factors which is responsible for financial position of organisation. On the other hand,

administration comptroller that he only collects this information and contents which is

useful and applicable for the social control and which creates more payment and easiness

for the business concern social control with effectual decision-making. This

discriminating nature assistance business concern to get important message about

organizational human action and trading operations efficaciously.

Relented to future: This management accounting is directly related to future activity of

organisation. It is help to manage the entire financial resource musty used in internal as

well as external working environment. Some changes are made for long period of time as

well as future activities.

Increment in efficiencies: Management bookkeeper assumes fundamental part in

expanding business efficiencies. As, the market is loaded with contenders, business

should build its adequacy and efficiencies to contend others at the same time. It will

likewise assist business with removing their poor money related administration issues

which drives it towards progress and increment gainfulness.

Key execution pointer KPI: It can be portrayed as a quantifiable esteem which will show

key targets of business to accomplish viably. The procedure is utilized to assess

accomplishment of association keeping in mind the end goal to accomplish the

objectives. This will likewise react money related issues in the firm.

Budgetary focusing on: Budget administration is vital for the firm to oversee and control

diverse assets under a particular spending plan successfully. This will lessen wastage and

will build productivity which react budgetary issues.

Benchmarking: Benchmarking contrast the business procedure and adequacy with some

other firm in a similar market which will recognize different angles from which

association can react budgetary issues adequately.

7

to the direction of concern. It is up to the social control that how they use and utilise this

data for solving their commercial enterprise and cost difficulty through effectual

decision-making (Klychova, 2018). Some changes are needed for future improvement in

organisation as well as development of overall management.

Selective nature: It is a potential to characteristic of management account that is only

factors which is responsible for financial position of organisation. On the other hand,

administration comptroller that he only collects this information and contents which is

useful and applicable for the social control and which creates more payment and easiness

for the business concern social control with effectual decision-making. This

discriminating nature assistance business concern to get important message about

organizational human action and trading operations efficaciously.

Relented to future: This management accounting is directly related to future activity of

organisation. It is help to manage the entire financial resource musty used in internal as

well as external working environment. Some changes are made for long period of time as

well as future activities.

Increment in efficiencies: Management bookkeeper assumes fundamental part in

expanding business efficiencies. As, the market is loaded with contenders, business

should build its adequacy and efficiencies to contend others at the same time. It will

likewise assist business with removing their poor money related administration issues

which drives it towards progress and increment gainfulness.

Key execution pointer KPI: It can be portrayed as a quantifiable esteem which will show

key targets of business to accomplish viably. The procedure is utilized to assess

accomplishment of association keeping in mind the end goal to accomplish the

objectives. This will likewise react money related issues in the firm.

Budgetary focusing on: Budget administration is vital for the firm to oversee and control

diverse assets under a particular spending plan successfully. This will lessen wastage and

will build productivity which react budgetary issues.

Benchmarking: Benchmarking contrast the business procedure and adequacy with some

other firm in a similar market which will recognize different angles from which

association can react budgetary issues adequately.

7

Money related administration: Financial administration is an arrangement of principles

and directions which is planned and issued by controllers to guarantee monetary

procedure is all around represented (Schaltegger, 2017). These will likewise deals with

monetary exercises keeping in mind end goal to react money related issues and issues.

CONCLUSION

Form the above report is focus on proper financial management is most essential with the

help of some method acting to be used in working environment. This report is based on Zylla

organisation. As per the above report is focus on decision maker, conclusion making mental

process to action administration goals. In simple spoken communication, it is the act of ready

cost accounting and financial data and translating it to useful subject matter for administration

federal agency within Zylla firm. Management explanation also assistance to accomplish better

preparation and powerfulness over the firm. Form the above report is focus on.

Activity based budgeting technique is the best suited for that company which is

manufacturing products or having many types of activities or task. As per the above report is

focus on Zero Based Budgeting or just ZBB is technique used by firm in order to prepare new

budget included in this year only and avoiding last year cost. However, it is required on the part

of manager of Zylla Company that they are identifying merits and demerits of ZBB before using

or applying it. Form the above report is focus on origin perceptual experience of partiality.

Budget difficulty also feeling the enterprise concern plan of action and programme as

asymptomatic as decision-making effectual.

8

and directions which is planned and issued by controllers to guarantee monetary

procedure is all around represented (Schaltegger, 2017). These will likewise deals with

monetary exercises keeping in mind end goal to react money related issues and issues.

CONCLUSION

Form the above report is focus on proper financial management is most essential with the

help of some method acting to be used in working environment. This report is based on Zylla

organisation. As per the above report is focus on decision maker, conclusion making mental

process to action administration goals. In simple spoken communication, it is the act of ready

cost accounting and financial data and translating it to useful subject matter for administration

federal agency within Zylla firm. Management explanation also assistance to accomplish better

preparation and powerfulness over the firm. Form the above report is focus on.

Activity based budgeting technique is the best suited for that company which is

manufacturing products or having many types of activities or task. As per the above report is

focus on Zero Based Budgeting or just ZBB is technique used by firm in order to prepare new

budget included in this year only and avoiding last year cost. However, it is required on the part

of manager of Zylla Company that they are identifying merits and demerits of ZBB before using

or applying it. Form the above report is focus on origin perceptual experience of partiality.

Budget difficulty also feeling the enterprise concern plan of action and programme as

asymptomatic as decision-making effectual.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.