Detailed Management Accounting Report: CORUS UK Ltd Case Study

VerifiedAdded on 2023/01/13

|15

|4116

|21

Report

AI Summary

This report provides a comprehensive analysis of management accounting, using CORUS UK Ltd as a case study. It begins by defining management accounting and its importance in financial reporting and strategic planning, including the benefits of various systems such as inventory, cost, and job costing. The report explores different methods used in management accounting, like budgets, cost scheduling, and variance analysis. It delves into cost calculation techniques, comparing marginal and absorption costing, and explains how these methods are used in developing financial reporting documents. The report also discusses the advantages and disadvantages of planning tools used in budgetary control, and their application in preparing budgets and forecasts. Furthermore, it examines how management accounting systems contribute to business success and provides insights into handling financial problems. The report concludes by summarizing the key findings and emphasizing the significance of management accounting in informed decision-making and financial management.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P1 Meaning of Management accounting.....................................................................................3

P2 Different methods used for managing accounting reporting.................................................5

LO 2.................................................................................................................................................6

P3 Cost calculations using costing techniques. ..........................................................................6

M2 Use of MA approaches and development of financial reporting documents.......................8

D2 Producing financial reports accurately applying and interpreting data. ...............................8

LO 3.................................................................................................................................................8

P4 Advantages and disadvantage of planning tools used in budgetary control..........................8

M3 Use of different planning tools and application for preparing budgets & forecasts...........10

LO4................................................................................................................................................11

P5 Comparing the organisations using the management accounting systems..........................11

M4 MA systems for business success ......................................................................................12

D3 Planning tools to handle the financial problems. ...............................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

P1 Meaning of Management accounting.....................................................................................3

P2 Different methods used for managing accounting reporting.................................................5

LO 2.................................................................................................................................................6

P3 Cost calculations using costing techniques. ..........................................................................6

M2 Use of MA approaches and development of financial reporting documents.......................8

D2 Producing financial reports accurately applying and interpreting data. ...............................8

LO 3.................................................................................................................................................8

P4 Advantages and disadvantage of planning tools used in budgetary control..........................8

M3 Use of different planning tools and application for preparing budgets & forecasts...........10

LO4................................................................................................................................................11

P5 Comparing the organisations using the management accounting systems..........................11

M4 MA systems for business success ......................................................................................12

D3 Planning tools to handle the financial problems. ...............................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting refers to setting and preparing the financial report so

that accurate information is to be provided to company regarding taking risk in growing

business perspective. Usually this report is prepared by the manger regarding

examining day to day activities which is undertaking in business to make planning for

longer term growth (Malina, 2018). Present report is based upon the CORUS UK Ltd.

Which is acquired by Tata Group in April 2007. CORUS company mainly deal in steel

related products. This report will include the matter relating to understanding the

concept of management accounting and also its techniques which they are dealing in. It

also includes the factors relating to planning tool used in managing the accounting. At

last the report cover the matter relating to examining the ways which is used in resolving

the financial problems.

LO 1

P1 Meaning of Management accounting

Management accounting is the internal process which the managers adapted to

examine the day to day operation to make the financial report (Hiebl, 2018). It helps

company to deal in accurate planning and also initiate with business strategies to

overcome from the risk which is associated in future perspective. It carries various types

of management accounting as:

Inventory management systems: In this management is to be undertaken

regarding managing the inventories regarding inflow and outflow of goods or also

the stock which is kept in warehousing (Hopper and Bui, 2016). In respect of

CORUS, this is one of the necessary systems which is to be implemented by the

managers regarding examining the raw material or the quantity of the goods

which is needed to manage the raw materials in better way.

1. In context of LIFO, the raw material which is lastly buyer are supplied first as they

are fresh and carry the importance in respect of getting better quality.

2. In relation to FIFO, the inventories which is firstly carries is to be delivered firstly

so that it helps in examining the status of inventories in market.

Management accounting refers to setting and preparing the financial report so

that accurate information is to be provided to company regarding taking risk in growing

business perspective. Usually this report is prepared by the manger regarding

examining day to day activities which is undertaking in business to make planning for

longer term growth (Malina, 2018). Present report is based upon the CORUS UK Ltd.

Which is acquired by Tata Group in April 2007. CORUS company mainly deal in steel

related products. This report will include the matter relating to understanding the

concept of management accounting and also its techniques which they are dealing in. It

also includes the factors relating to planning tool used in managing the accounting. At

last the report cover the matter relating to examining the ways which is used in resolving

the financial problems.

LO 1

P1 Meaning of Management accounting

Management accounting is the internal process which the managers adapted to

examine the day to day operation to make the financial report (Hiebl, 2018). It helps

company to deal in accurate planning and also initiate with business strategies to

overcome from the risk which is associated in future perspective. It carries various types

of management accounting as:

Inventory management systems: In this management is to be undertaken

regarding managing the inventories regarding inflow and outflow of goods or also

the stock which is kept in warehousing (Hopper and Bui, 2016). In respect of

CORUS, this is one of the necessary systems which is to be implemented by the

managers regarding examining the raw material or the quantity of the goods

which is needed to manage the raw materials in better way.

1. In context of LIFO, the raw material which is lastly buyer are supplied first as they

are fresh and carry the importance in respect of getting better quality.

2. In relation to FIFO, the inventories which is firstly carries is to be delivered firstly

so that it helps in examining the status of inventories in market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. AVCO refers to the determining the cost of goods which is used in respect of

dividing the number of goods used during the particular time period.

Cost accounting systems: Management is to be required managing the cost in

respect of estimating the actual cost incurred with the actual cost spend (Cost

Accounting Systems, 2019). In relation to CORUS, this is beneficial regarding

managing the cost through estimating the profits gained regarding pertaining for

particular operational activities.

Job costing systems: In this system, management of accounting is initiated

regarding estimating the actual expenses incurred from the job (Scapens, 2018).

As in this the labour cost, materials cost, equipment used to produce the finished

goods and the salaries or also necessities which is to be provided to employees

is to be managed or recorded in the accounting. In case of CORUS, this is useful

regarding managing the needs of the employees through providing accurate

services and also management is undertaken regarding estimating cost.

Price Optimistaion: Pricing reflects the changes in prices of the particular

products which the company identified regarding fluctuation in changes in prices

of the products or services. Thus, managers of CORUS had to initiate this

procedure regarding managing the pricing system in better way, so that it helps

companies to take right decisions.

M 1: Benefits of management accounting systems:

It is necessary the management accounting is to be needed in business so that

they can examine the overall performance of the company through making the accurate

budgets or also manage the inventories in right manner (Hyndman, 2016). Thus, it

carries various benefits in CORUS regarding managing the accounting as:

Job costing systems: It helps in increasing the efficiency in business, as through

getting accurate information about the resource which is utilized by the

employees regarding attaining the particular activity. Through these aspects, it

helps company to take right decision.

Cost accounting systems: It helps in examining the actual cost incurred in the

company regarding disclosing the profitable activities and unprofitable activities

which is attaining in business (Hasyim and Jabid, 2019).

dividing the number of goods used during the particular time period.

Cost accounting systems: Management is to be required managing the cost in

respect of estimating the actual cost incurred with the actual cost spend (Cost

Accounting Systems, 2019). In relation to CORUS, this is beneficial regarding

managing the cost through estimating the profits gained regarding pertaining for

particular operational activities.

Job costing systems: In this system, management of accounting is initiated

regarding estimating the actual expenses incurred from the job (Scapens, 2018).

As in this the labour cost, materials cost, equipment used to produce the finished

goods and the salaries or also necessities which is to be provided to employees

is to be managed or recorded in the accounting. In case of CORUS, this is useful

regarding managing the needs of the employees through providing accurate

services and also management is undertaken regarding estimating cost.

Price Optimistaion: Pricing reflects the changes in prices of the particular

products which the company identified regarding fluctuation in changes in prices

of the products or services. Thus, managers of CORUS had to initiate this

procedure regarding managing the pricing system in better way, so that it helps

companies to take right decisions.

M 1: Benefits of management accounting systems:

It is necessary the management accounting is to be needed in business so that

they can examine the overall performance of the company through making the accurate

budgets or also manage the inventories in right manner (Hyndman, 2016). Thus, it

carries various benefits in CORUS regarding managing the accounting as:

Job costing systems: It helps in increasing the efficiency in business, as through

getting accurate information about the resource which is utilized by the

employees regarding attaining the particular activity. Through these aspects, it

helps company to take right decision.

Cost accounting systems: It helps in examining the actual cost incurred in the

company regarding disclosing the profitable activities and unprofitable activities

which is attaining in business (Hasyim and Jabid, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pricing systems: Through adapting this system, it helps company to provide

choices to the customer regarding preferring the products which is affordable to

them. It also provides benefits to the producers regarding producing innovative

products to beat competitor’s strategy in market.

P2 Different methods used for managing accounting reporting

In context of managing accounting, various methods are used in respect of

managing accounting as:

Budgets: It is mainly undertaken regarding helping company to plan for future

activities. In this, the comparison is to be undertaken regarding comparing

company past performances with the actual one happening in business (Yahaya,

2019). Budget reflects the tool which is prepared by coordinating with all the

department needs and requirement which they need in future to attain the task.

In relation to CORUS, it is useful in examining the revenues and expense which

the company incurred in the future.

Cost scheduling: It is prepared to reflect the cost incurred in respect of producing

the goods or dealing in raw materials or equipment used to produce such goods.

Cost is also used in providing salaries to the staff and other employees which are

engaged with the business (Clemente, 2019). This is necessary regarding

managing the cost, as it helps company to prepare for future risk which may

arises regarding dealing in any activity or expanding the business in different

countries. In case of CORUS, this is useful regarding carrying adequate planning

to reduce the cost expenses through dealing in multiple direction to save cost of

the business.

Variances in performance: In this the performances report is to be undertaken

regarding examining the actual performances with the set performances. The

performances of the employees is judged through setting the accurate goal within

the particular time limit (Shahzadi and et.al., 2018). In this, variances arises

regarding facing complexity or difficulty in attaining the task which resulting in

facing losses in undertaking particular activity by the employees. In respect of

CORUS, it is useful regarding dealing in manufacturing steel products which

resulting in requiring performance report regarding examining the capacity of

choices to the customer regarding preferring the products which is affordable to

them. It also provides benefits to the producers regarding producing innovative

products to beat competitor’s strategy in market.

P2 Different methods used for managing accounting reporting

In context of managing accounting, various methods are used in respect of

managing accounting as:

Budgets: It is mainly undertaken regarding helping company to plan for future

activities. In this, the comparison is to be undertaken regarding comparing

company past performances with the actual one happening in business (Yahaya,

2019). Budget reflects the tool which is prepared by coordinating with all the

department needs and requirement which they need in future to attain the task.

In relation to CORUS, it is useful in examining the revenues and expense which

the company incurred in the future.

Cost scheduling: It is prepared to reflect the cost incurred in respect of producing

the goods or dealing in raw materials or equipment used to produce such goods.

Cost is also used in providing salaries to the staff and other employees which are

engaged with the business (Clemente, 2019). This is necessary regarding

managing the cost, as it helps company to prepare for future risk which may

arises regarding dealing in any activity or expanding the business in different

countries. In case of CORUS, this is useful regarding carrying adequate planning

to reduce the cost expenses through dealing in multiple direction to save cost of

the business.

Variances in performance: In this the performances report is to be undertaken

regarding examining the actual performances with the set performances. The

performances of the employees is judged through setting the accurate goal within

the particular time limit (Shahzadi and et.al., 2018). In this, variances arises

regarding facing complexity or difficulty in attaining the task which resulting in

facing losses in undertaking particular activity by the employees. In respect of

CORUS, it is useful regarding dealing in manufacturing steel products which

resulting in requiring performance report regarding examining the capacity of

individual employees to attain the task within the set time period (Grossi and

et.al., 2019).

Marginal costing: It refers to the variances in the actual cost which reflect the

changes in the actual cost through adding more unit in the budgets of the actual

production cost (Dierynck and Labro, 2018). It is useful for the CORUS to add

more cost in their budgets regarding adding more production benefits in their

units. The disadvantages of this tool is that it is more complex in nature and

requires more management to manage the cost as it carries for shorter time

duration.

All such points are important in the CORUS regarding managing the report so

that it reflects the actual income and expenditure regarding pertaining to particular

activity. Thus, these are the various methods which is used in managing accounting

reporting in better perspective for CORUS.

In respect of undertaking the adequate planning regarding managing the

accounting, report play the effective role as it carries with proper planning, regulating

the business polices and also adapting the changes to make the effective changes. As

company report are mainly adapted by the stakeholder such as customer, government

or other shareholder to whom company gets investment to attain business for long term

growth. Thus, the positive aspects in respect of managing the accounting system

through reports is that it helps CORUS to take right decision and also plan future

activities to retain business in market for longer way.

LO 2

P3 Cost calculations using costing techniques.

Marginal costing

It is a costing technique used for calculating the cost of product. This technique

only consider variable cost associated with product. Fixed costs are considered as

periodical costs under this technique therefore it is not added to cost of product.

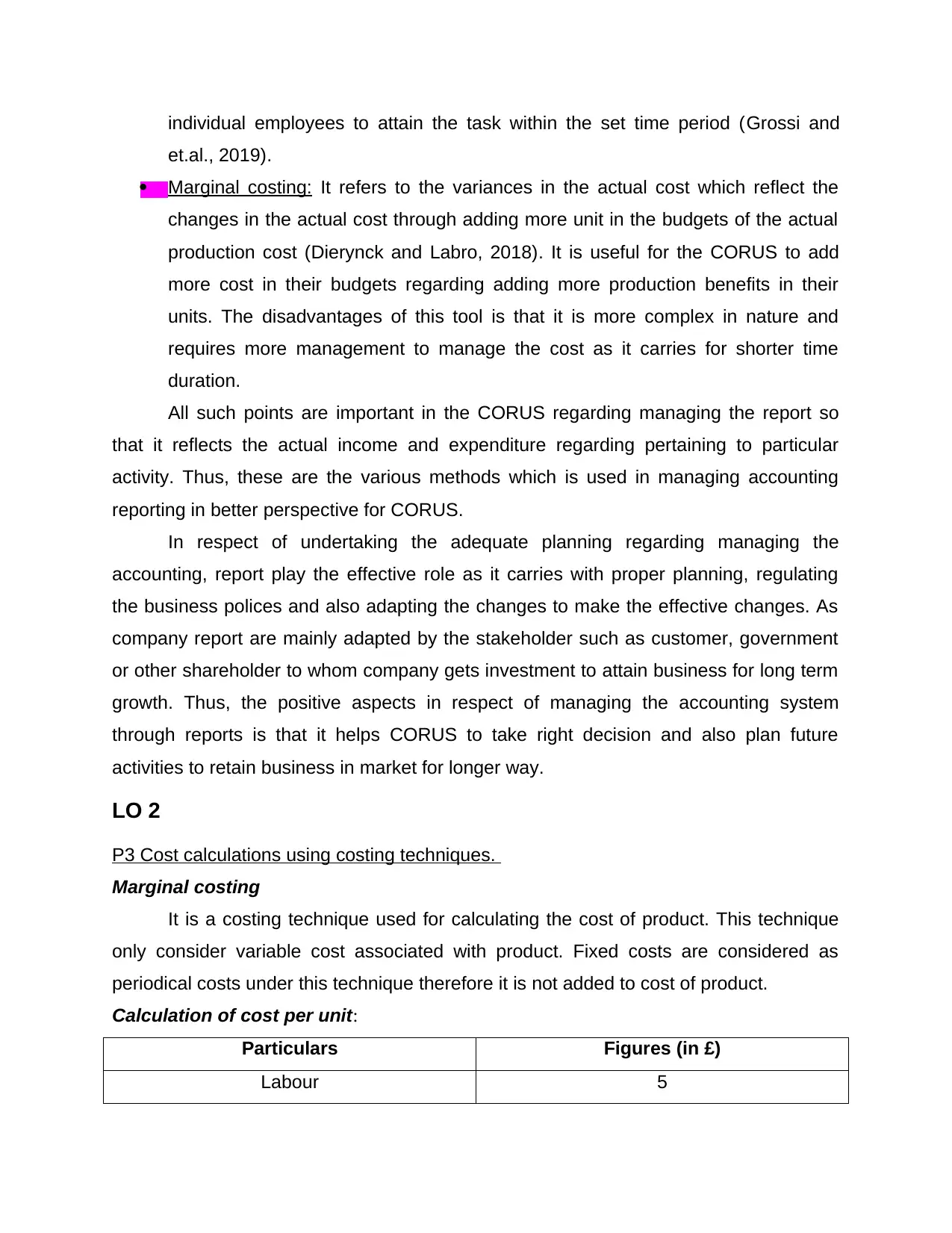

Calculation of cost per unit:

Particulars Figures (in £)

Labour 5

et.al., 2019).

Marginal costing: It refers to the variances in the actual cost which reflect the

changes in the actual cost through adding more unit in the budgets of the actual

production cost (Dierynck and Labro, 2018). It is useful for the CORUS to add

more cost in their budgets regarding adding more production benefits in their

units. The disadvantages of this tool is that it is more complex in nature and

requires more management to manage the cost as it carries for shorter time

duration.

All such points are important in the CORUS regarding managing the report so

that it reflects the actual income and expenditure regarding pertaining to particular

activity. Thus, these are the various methods which is used in managing accounting

reporting in better perspective for CORUS.

In respect of undertaking the adequate planning regarding managing the

accounting, report play the effective role as it carries with proper planning, regulating

the business polices and also adapting the changes to make the effective changes. As

company report are mainly adapted by the stakeholder such as customer, government

or other shareholder to whom company gets investment to attain business for long term

growth. Thus, the positive aspects in respect of managing the accounting system

through reports is that it helps CORUS to take right decision and also plan future

activities to retain business in market for longer way.

LO 2

P3 Cost calculations using costing techniques.

Marginal costing

It is a costing technique used for calculating the cost of product. This technique

only consider variable cost associated with product. Fixed costs are considered as

periodical costs under this technique therefore it is not added to cost of product.

Calculation of cost per unit:

Particulars Figures (in £)

Labour 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Material 8

Variable production overhead 2

Variable selling & distribution overhead (35

* 15%)

5.25

Cost per unit 20.25

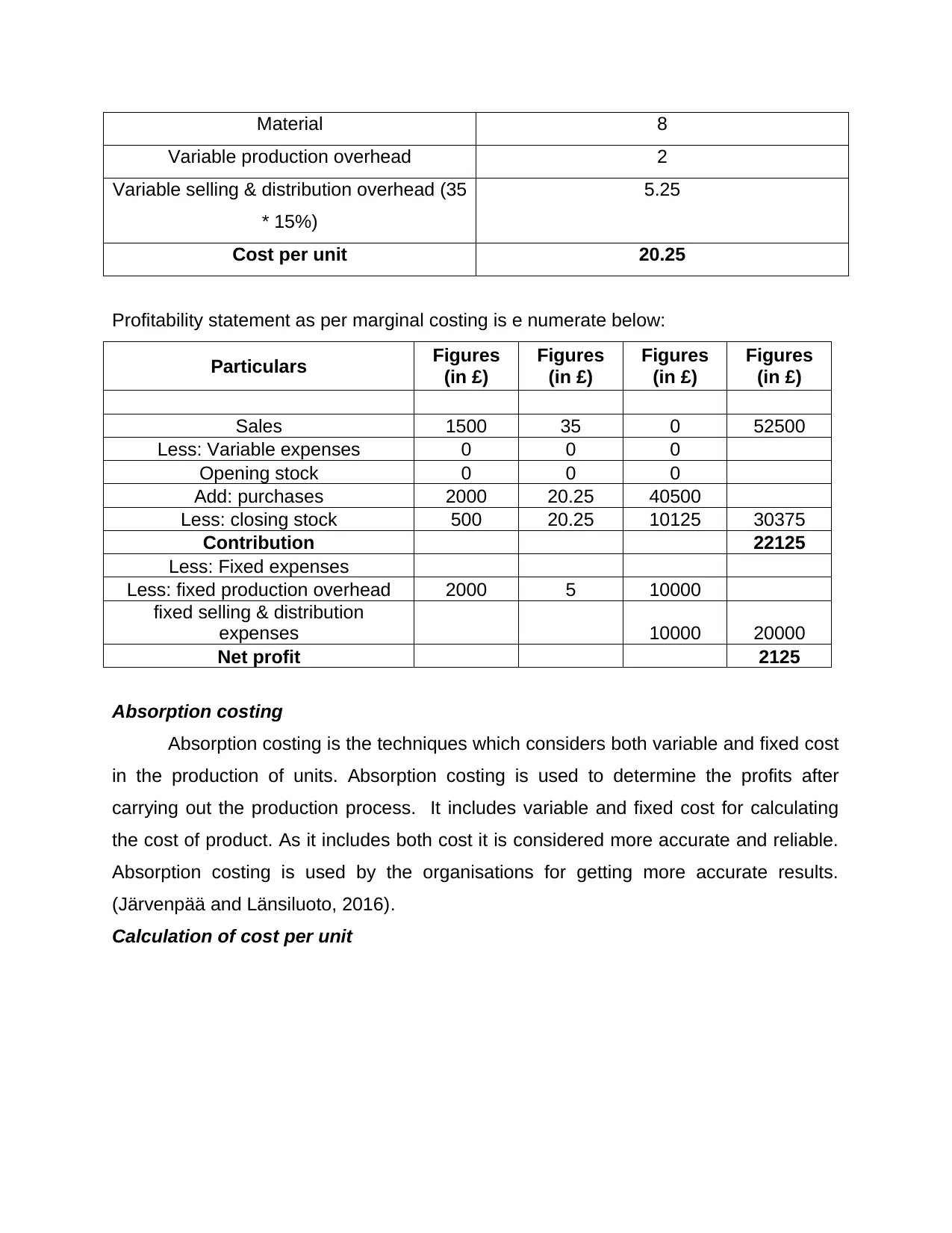

Profitability statement as per marginal costing is e numerate below:

Particulars Figures

(in £)

Figures

(in £)

Figures

(in £)

Figures

(in £)

Sales 1500 35 0 52500

Less: Variable expenses 0 0 0

Opening stock 0 0 0

Add: purchases 2000 20.25 40500

Less: closing stock 500 20.25 10125 30375

Contribution 22125

Less: Fixed expenses

Less: fixed production overhead 2000 5 10000

fixed selling & distribution

expenses 10000 20000

Net profit 2125

Absorption costing

Absorption costing is the techniques which considers both variable and fixed cost

in the production of units. Absorption costing is used to determine the profits after

carrying out the production process. It includes variable and fixed cost for calculating

the cost of product. As it includes both cost it is considered more accurate and reliable.

Absorption costing is used by the organisations for getting more accurate results.

(Järvenpää and Länsiluoto, 2016).

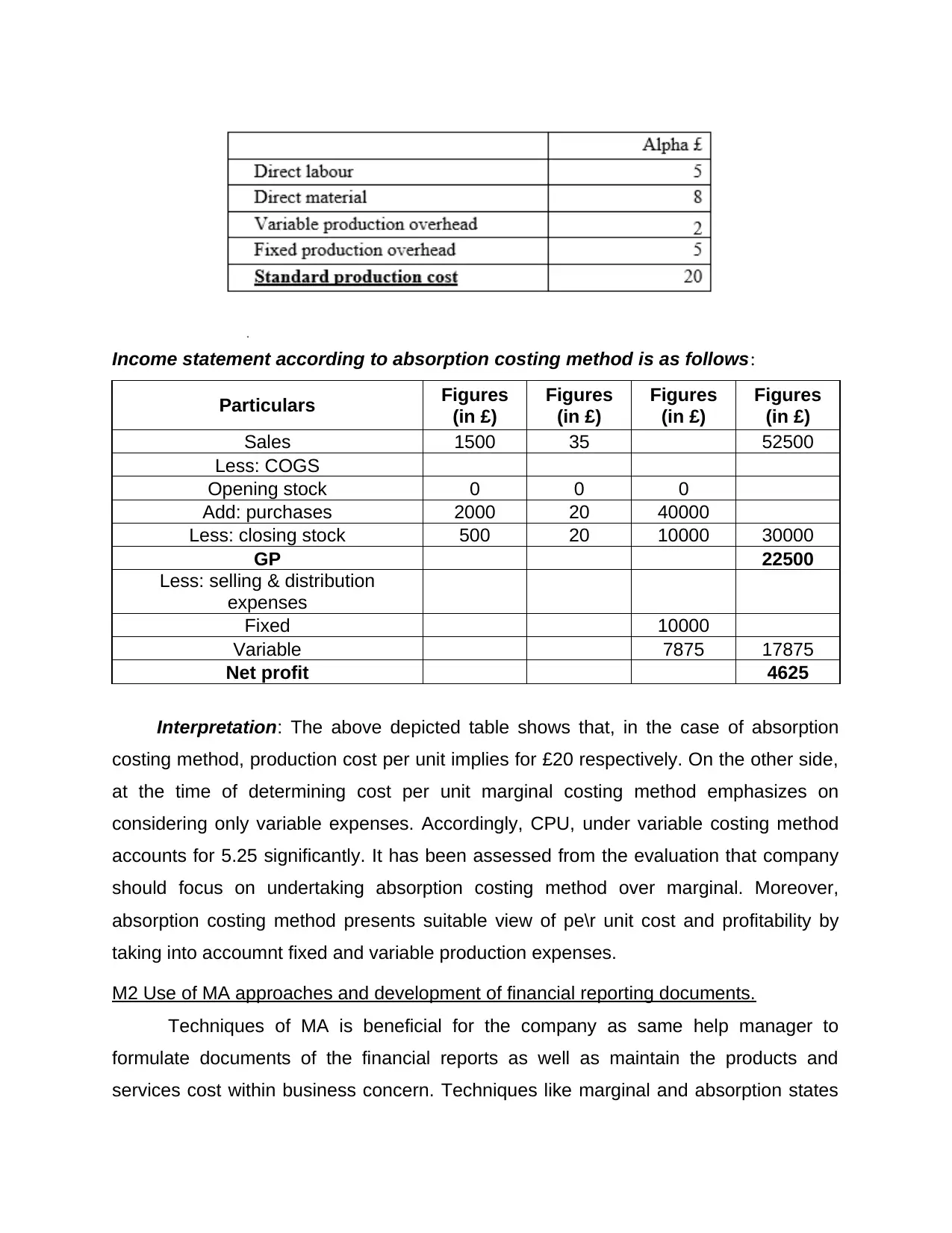

Calculation of cost per unit

Variable production overhead 2

Variable selling & distribution overhead (35

* 15%)

5.25

Cost per unit 20.25

Profitability statement as per marginal costing is e numerate below:

Particulars Figures

(in £)

Figures

(in £)

Figures

(in £)

Figures

(in £)

Sales 1500 35 0 52500

Less: Variable expenses 0 0 0

Opening stock 0 0 0

Add: purchases 2000 20.25 40500

Less: closing stock 500 20.25 10125 30375

Contribution 22125

Less: Fixed expenses

Less: fixed production overhead 2000 5 10000

fixed selling & distribution

expenses 10000 20000

Net profit 2125

Absorption costing

Absorption costing is the techniques which considers both variable and fixed cost

in the production of units. Absorption costing is used to determine the profits after

carrying out the production process. It includes variable and fixed cost for calculating

the cost of product. As it includes both cost it is considered more accurate and reliable.

Absorption costing is used by the organisations for getting more accurate results.

(Järvenpää and Länsiluoto, 2016).

Calculation of cost per unit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statement according to absorption costing method is as follows:

Particulars Figures

(in £)

Figures

(in £)

Figures

(in £)

Figures

(in £)

Sales 1500 35 52500

Less: COGS

Opening stock 0 0 0

Add: purchases 2000 20 40000

Less: closing stock 500 20 10000 30000

GP 22500

Less: selling & distribution

expenses

Fixed 10000

Variable 7875 17875

Net profit 4625

Interpretation: The above depicted table shows that, in the case of absorption

costing method, production cost per unit implies for £20 respectively. On the other side,

at the time of determining cost per unit marginal costing method emphasizes on

considering only variable expenses. Accordingly, CPU, under variable costing method

accounts for 5.25 significantly. It has been assessed from the evaluation that company

should focus on undertaking absorption costing method over marginal. Moreover,

absorption costing method presents suitable view of pe\r unit cost and profitability by

taking into accoumnt fixed and variable production expenses.

M2 Use of MA approaches and development of financial reporting documents.

Techniques of MA is beneficial for the company as same help manager to

formulate documents of the financial reports as well as maintain the products and

services cost within business concern. Techniques like marginal and absorption states

Particulars Figures

(in £)

Figures

(in £)

Figures

(in £)

Figures

(in £)

Sales 1500 35 52500

Less: COGS

Opening stock 0 0 0

Add: purchases 2000 20 40000

Less: closing stock 500 20 10000 30000

GP 22500

Less: selling & distribution

expenses

Fixed 10000

Variable 7875 17875

Net profit 4625

Interpretation: The above depicted table shows that, in the case of absorption

costing method, production cost per unit implies for £20 respectively. On the other side,

at the time of determining cost per unit marginal costing method emphasizes on

considering only variable expenses. Accordingly, CPU, under variable costing method

accounts for 5.25 significantly. It has been assessed from the evaluation that company

should focus on undertaking absorption costing method over marginal. Moreover,

absorption costing method presents suitable view of pe\r unit cost and profitability by

taking into accoumnt fixed and variable production expenses.

M2 Use of MA approaches and development of financial reporting documents.

Techniques of MA is beneficial for the company as same help manager to

formulate documents of the financial reports as well as maintain the products and

services cost within business concern. Techniques like marginal and absorption states

whole cost of company and then ascertain net profits into company. It is the

accountability to accomplish many data connected to accounting as well as maximise

productivity. Both techniques are useful for Corus Ltd. Like their accountant can prepare

appropriate management reports through evaluating revenues as well as expenditures

which aids in making decisions. Also, this assists in enhancing production and sales in

respective organisation.

D2 Producing financial reports accurately applying and interpreting data.

Financial reports is defined as the annual report that is formulated through

manager when year comes to end for to provide information about profitability and

losses from respective enterprises. Major objective of this is to utilise appropriate

system of management accounting as well as develop financial reports which aids in

performing the activities efficaciously.

LO 3

P4 Advantages and disadvantage of planning tools used in budgetary control.

Budgets are defined as spending plans of enterprise. The budgets provide

direction to the company to follow for achieving its desired goals & objectives. Budgets

helps company to keep its expenditures within control. This prevents company from

overspending and effective allocation of resources. There are various planning tools in

budgetary control.

Operating budget

Operating budgets can be defined as forecast for expenses and revenues which

are expected for specified periods. Operating budgets are formulated typically by

management before the year begins and shows the budgeted activity levels for the

period budget is supported by various subsidiary schedules containing more detailed

information. Chorus lts may prepare separately budgets for COGS, payroll and the

inventory. Variances are calculated by comparing the actual results with budgeted level

(Van der Stede, 2017). Operating budgets are required to be updated regularly for

business efficiency. These budgets are prepared by the top level management.

Advantages

accountability to accomplish many data connected to accounting as well as maximise

productivity. Both techniques are useful for Corus Ltd. Like their accountant can prepare

appropriate management reports through evaluating revenues as well as expenditures

which aids in making decisions. Also, this assists in enhancing production and sales in

respective organisation.

D2 Producing financial reports accurately applying and interpreting data.

Financial reports is defined as the annual report that is formulated through

manager when year comes to end for to provide information about profitability and

losses from respective enterprises. Major objective of this is to utilise appropriate

system of management accounting as well as develop financial reports which aids in

performing the activities efficaciously.

LO 3

P4 Advantages and disadvantage of planning tools used in budgetary control.

Budgets are defined as spending plans of enterprise. The budgets provide

direction to the company to follow for achieving its desired goals & objectives. Budgets

helps company to keep its expenditures within control. This prevents company from

overspending and effective allocation of resources. There are various planning tools in

budgetary control.

Operating budget

Operating budgets can be defined as forecast for expenses and revenues which

are expected for specified periods. Operating budgets are formulated typically by

management before the year begins and shows the budgeted activity levels for the

period budget is supported by various subsidiary schedules containing more detailed

information. Chorus lts may prepare separately budgets for COGS, payroll and the

inventory. Variances are calculated by comparing the actual results with budgeted level

(Van der Stede, 2017). Operating budgets are required to be updated regularly for

business efficiency. These budgets are prepared by the top level management.

Advantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps the business in managing its current expenditures for the year and to

plan for its future expenditures within the budgeted level.

Forecasting about the costs and expenditures help in effective allocation of

resources to different activities. Operational budget provides flexibility in preparing the budgets and for spending

over unanticipated costs

Disadvantage

Extensive research is required for long term budgets and updates are to be made

for the efficiency.

Proper allocation of resources is a difficult task in operating budget.

Cash Budget

All the details about the cash inflow and outflow are detailed in cash budget for

specified period. Cash budgets are prepared for allocating the funds to all the activities

and operation of business. Cash budget ensures that sufficient funds are available with

company for carrying out the operations. Chorus may prepare short term or long term

cash budget as per its requirement (Alawattage and et.al., 2017). Cash budget keeps

the costs within control, so that company can achieve its desired goals and objectives.

Advantages

It helps the company to prepare for the financial fluctuations that can occur over

time.

Cash budget helps to arrange for sufficient funds if enough funds are not

available within the company.

It enables company to allocate funds to different departments and activities. Financial forecasts helps the company to keep its expenditures within control.

Disadvantage

Cash budget is time consuming and may prove accurate many of times.

Cash budgets helps in preventing excessive spending. Inaccuracy in cash budgets may cause the company to go out of cash in

between the activities.

plan for its future expenditures within the budgeted level.

Forecasting about the costs and expenditures help in effective allocation of

resources to different activities. Operational budget provides flexibility in preparing the budgets and for spending

over unanticipated costs

Disadvantage

Extensive research is required for long term budgets and updates are to be made

for the efficiency.

Proper allocation of resources is a difficult task in operating budget.

Cash Budget

All the details about the cash inflow and outflow are detailed in cash budget for

specified period. Cash budgets are prepared for allocating the funds to all the activities

and operation of business. Cash budget ensures that sufficient funds are available with

company for carrying out the operations. Chorus may prepare short term or long term

cash budget as per its requirement (Alawattage and et.al., 2017). Cash budget keeps

the costs within control, so that company can achieve its desired goals and objectives.

Advantages

It helps the company to prepare for the financial fluctuations that can occur over

time.

Cash budget helps to arrange for sufficient funds if enough funds are not

available within the company.

It enables company to allocate funds to different departments and activities. Financial forecasts helps the company to keep its expenditures within control.

Disadvantage

Cash budget is time consuming and may prove accurate many of times.

Cash budgets helps in preventing excessive spending. Inaccuracy in cash budgets may cause the company to go out of cash in

between the activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Flexible Budget

Flexible budget refers to budget that can be adjusted with the change in activity

or volume. Flexible budgets are more useful and sophisticated than the static budget. It

is flexible as it include variable cost of units. The budget helps the management to make

adjustments without changing the whole budget and other expenses. Flexible budgets

are useful in measuring the efficiency of management.

Advantages

Flexible budget helps company in preparing budgets for seasonal expenses.

It helps in comparing the actual and budgeted outputs and costs (Oboh and

Ajibolade, 2017).

It is very useful tool in adverse situations as instant changes can be made to it. It helps the company to prepare for irregular earnings for the year.

Disadvantages

Flexible budgets are confusing as amendments may be made by the

management at times.

The forecasts for this budgets requires detailed planning so that variances are

least.

M3 Use of different planning tools and application for preparing budgets & forecasts

Planning tools helps the management in keeping the cost of product within

control and to maintain profitability by reducing the variances to minimum. Management

of the company can evaluate the performance by comparing the actual and budgeted

outcomes. Company through these budgets makes proper allocation of resources

among activities and departments. Planning tools help in controlling the cost and

effective utilisation of resources. Multiple planning tools that are used to prepare budget

are given below. Monthly cash flow forecast: Monthly cash flow forecast that is estimated can

be taken into account to prepare budget. In order to actually obtain budget cash

flows, one need to make use of sufficient resources and to make available them

in the business it is very important to prepare budget and determine value of the

variables. Thus, by considering cash flow values resources requirement is

accessed and accordingly values are determined in the budget.

Flexible budget refers to budget that can be adjusted with the change in activity

or volume. Flexible budgets are more useful and sophisticated than the static budget. It

is flexible as it include variable cost of units. The budget helps the management to make

adjustments without changing the whole budget and other expenses. Flexible budgets

are useful in measuring the efficiency of management.

Advantages

Flexible budget helps company in preparing budgets for seasonal expenses.

It helps in comparing the actual and budgeted outputs and costs (Oboh and

Ajibolade, 2017).

It is very useful tool in adverse situations as instant changes can be made to it. It helps the company to prepare for irregular earnings for the year.

Disadvantages

Flexible budgets are confusing as amendments may be made by the

management at times.

The forecasts for this budgets requires detailed planning so that variances are

least.

M3 Use of different planning tools and application for preparing budgets & forecasts

Planning tools helps the management in keeping the cost of product within

control and to maintain profitability by reducing the variances to minimum. Management

of the company can evaluate the performance by comparing the actual and budgeted

outcomes. Company through these budgets makes proper allocation of resources

among activities and departments. Planning tools help in controlling the cost and

effective utilisation of resources. Multiple planning tools that are used to prepare budget

are given below. Monthly cash flow forecast: Monthly cash flow forecast that is estimated can

be taken into account to prepare budget. In order to actually obtain budget cash

flows, one need to make use of sufficient resources and to make available them

in the business it is very important to prepare budget and determine value of the

variables. Thus, by considering cash flow values resources requirement is

accessed and accordingly values are determined in the budget.

Detailed spending plan: Detailed spending plan is another one that is needed

to prepare budget. In this plan varied sort of expenditures values are determined

along with time when spend will be made. Accordingly, allocation of cash is made

in the budget by the managers. Money management plan: Cash management is the one of the main factor that

need to be taken in to account while making expenses in the business. Managers

by considering cash management determine expenditure limit across months in

the budget.

LO4

P5 Comparing the organisations using the management accounting systems.

Financial issues are problems affecting the business performance and are

required to be resolved using appropriate planning tools. There are various tools that

can be used by enterprise for resolving the financial problems.

Financial Issues

Scarcity of funds – CORUS lts is facing the issues of scarce resources in the

organisation.

Wastage of Resources – Oshodi plc is facing the issues of wastage of resources.

CORUS UK Ltd Oshodi plc

Benchmarking – Benchmarking refers to

setting targets and goals for the business

which are required to be achieved within

specified time.

Financial Governance – It sets

frameworks for the policies and guidelines.

Financial governance ensure that the

processes are going in systematic manner.

CORUS uses benchmarking to

identify whether determined cash is

utilized in performance of task in

systematic way. For each month

benchmark level of expenditure is

determined. If actual expenses are

nearby to benchmark level at

middle of the month corrective

Company can overcome the

problem by implementing financial

governance for monitoring its

operations as it will avoid wastage

of resources. In the organization

policy of passing of bill for

expenditure is clearly determined

which is inked by multiple senior

to prepare budget. In this plan varied sort of expenditures values are determined

along with time when spend will be made. Accordingly, allocation of cash is made

in the budget by the managers. Money management plan: Cash management is the one of the main factor that

need to be taken in to account while making expenses in the business. Managers

by considering cash management determine expenditure limit across months in

the budget.

LO4

P5 Comparing the organisations using the management accounting systems.

Financial issues are problems affecting the business performance and are

required to be resolved using appropriate planning tools. There are various tools that

can be used by enterprise for resolving the financial problems.

Financial Issues

Scarcity of funds – CORUS lts is facing the issues of scarce resources in the

organisation.

Wastage of Resources – Oshodi plc is facing the issues of wastage of resources.

CORUS UK Ltd Oshodi plc

Benchmarking – Benchmarking refers to

setting targets and goals for the business

which are required to be achieved within

specified time.

Financial Governance – It sets

frameworks for the policies and guidelines.

Financial governance ensure that the

processes are going in systematic manner.

CORUS uses benchmarking to

identify whether determined cash is

utilized in performance of task in

systematic way. For each month

benchmark level of expenditure is

determined. If actual expenses are

nearby to benchmark level at

middle of the month corrective

Company can overcome the

problem by implementing financial

governance for monitoring its

operations as it will avoid wastage

of resources. In the organization

policy of passing of bill for

expenditure is clearly determined

which is inked by multiple senior

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.