Management Accounting Report: Analysis of Creams Ltd's Financials

VerifiedAdded on 2023/01/11

|20

|5529

|85

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on their application within Creams Ltd. It begins with an introduction to management accounting and its essential requirements, followed by an explanation of different reporting methods used. The report then delves into various management accounting systems such as cost accounting, inventory management, job order costing, and price optimization systems, highlighting their benefits and integration within the organization. The second task involves the calculation of costs using different techniques to prepare income statements, including marginal and absorption costing. Furthermore, it explores planning tools, their advantages, and disadvantages, alongside their importance in budgeting and forecasting. The report concludes with a comparison of organizations based on their use of management accounting to address financial issues and the role of management accounting in fostering sustainable development. Overall, the report offers a detailed exploration of the subject, supported by specific examples from Creams Ltd and recommendations for effective financial management.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P.1 Explanation of MA and essential requirements of numerous type of MAS....................3

P2 Explanation of Different reporting used in management accounting...............................5

M1 Benefits of adopting management accounting system.....................................................6

D1 Integration of management report and accounting system...............................................6

TASK 2............................................................................................................................................7

P3 Calculation of costs with various techniques to draw income statement..........................7

Marginal Costing Method: Income Statement.................................................................................7

M2 Apply a range of management accounting techniques....................................................9

D2 Analysis of data by financial report..................................................................................9

TASK 3............................................................................................................................................9

P4. Different planning tools with its advantages and disadvantages.....................................9

M3 Importance of planning tools for budgeting and forecasting process............................12

TASK 4..........................................................................................................................................13

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues......................................................................................................................13

M4 Respond to financial problems, MA lead to sustainable development..........................14

D3 Evaluation of planning tools to overcome financial problems.......................................15

CONCLUSION..............................................................................................................................15

REEFRENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P.1 Explanation of MA and essential requirements of numerous type of MAS....................3

P2 Explanation of Different reporting used in management accounting...............................5

M1 Benefits of adopting management accounting system.....................................................6

D1 Integration of management report and accounting system...............................................6

TASK 2............................................................................................................................................7

P3 Calculation of costs with various techniques to draw income statement..........................7

Marginal Costing Method: Income Statement.................................................................................7

M2 Apply a range of management accounting techniques....................................................9

D2 Analysis of data by financial report..................................................................................9

TASK 3............................................................................................................................................9

P4. Different planning tools with its advantages and disadvantages.....................................9

M3 Importance of planning tools for budgeting and forecasting process............................12

TASK 4..........................................................................................................................................13

P5 Comparison of organisations on the basis of use of management accounting to respond

financial issues......................................................................................................................13

M4 Respond to financial problems, MA lead to sustainable development..........................14

D3 Evaluation of planning tools to overcome financial problems.......................................15

CONCLUSION..............................................................................................................................15

REEFRENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a wider and much more complex term or idea which state that all

management workers ought to understand they need of MA to boost the productivity of the

organization (Cooper, Ezzamel and Qu, 2017). It is a technique that allows the internal manager

to decide whether the enterprise functions successfully or not. This is important for

every organization to guarantee that they give attention to while managing internal operation and

framework which support to achieve all of the defined objectives and goals. In order to fully

understand, the importance of MA and the application of its various reports, system, planning

tool etc. Creams Ltd have been selected.

In this report, the MA system and report with their essential requirement are discussed,

several cost techniques are used to prepare income statement. In addition, various planning tool

for controlling budgets and use of MAS in order to detect and resolve financial problems is also

elaborated.

TASK 1

P.1 Explanation of MA and essential requirements of numerous type of MAS.

Managerial accounting is a system that seeks to interpret reporting data in order to devise

financial strategies to achieve company organization's potential targets (Hopper and Bui, 2016).

Within Cream Limited, MA is used to support the executive department within determining the

real progress of the company. Cream Ltd administration pays heed to various aspects of them,

such as cost accounting system, price control, inventory tracking system and costing of job

orders. Through the help of both, management produces internal assessments that determine the

overall success of organisations. All these are defined in detailed in the sense of Cream Limited,

as follows:

Price Optimising System: This MAS is used to discuss different forms of pricing structures

which an company could use to market its goods. Managers will determine on certain retail

pricing based on the demands of their companies and the costs accrued throughout the whole

procedure of turning raw material into finished goods. Companies can use price retraction,

product skimming, and competitive prices, discounting demand tactics as per the analyses

of their rival markets, external variables and institution's potential target.

Essential requirement:

Management accounting is a wider and much more complex term or idea which state that all

management workers ought to understand they need of MA to boost the productivity of the

organization (Cooper, Ezzamel and Qu, 2017). It is a technique that allows the internal manager

to decide whether the enterprise functions successfully or not. This is important for

every organization to guarantee that they give attention to while managing internal operation and

framework which support to achieve all of the defined objectives and goals. In order to fully

understand, the importance of MA and the application of its various reports, system, planning

tool etc. Creams Ltd have been selected.

In this report, the MA system and report with their essential requirement are discussed,

several cost techniques are used to prepare income statement. In addition, various planning tool

for controlling budgets and use of MAS in order to detect and resolve financial problems is also

elaborated.

TASK 1

P.1 Explanation of MA and essential requirements of numerous type of MAS.

Managerial accounting is a system that seeks to interpret reporting data in order to devise

financial strategies to achieve company organization's potential targets (Hopper and Bui, 2016).

Within Cream Limited, MA is used to support the executive department within determining the

real progress of the company. Cream Ltd administration pays heed to various aspects of them,

such as cost accounting system, price control, inventory tracking system and costing of job

orders. Through the help of both, management produces internal assessments that determine the

overall success of organisations. All these are defined in detailed in the sense of Cream Limited,

as follows:

Price Optimising System: This MAS is used to discuss different forms of pricing structures

which an company could use to market its goods. Managers will determine on certain retail

pricing based on the demands of their companies and the costs accrued throughout the whole

procedure of turning raw material into finished goods. Companies can use price retraction,

product skimming, and competitive prices, discounting demand tactics as per the analyses

of their rival markets, external variables and institution's potential target.

Essential requirement:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price Optimization program in Creams Ltd. demands that it enables the boss to determine

the most acceptable rates to maximize revenue. This also promotes the recruitment to additional

consumers who boost the company's well-being positively and thereby gain economic benefits.

This program is incorporate by manager of Creams Ltd, to get the benefit of the most favourable

market policy inside the business and retain an acceptable profit margin. This therefore enables

the correct costs of products to be raised to maximize the loyal consumer base. Price

management is a technique that helps Creams Ltd to achieve a level of operation in specified

productivity by discovering how responsive its current consumers are to commodity price

adjustments. In case if a market volume wants to be connected to income and particularly if it

needs to increase profitability while maintaining the same consumer rates, optimum prices are

required.

Cost Accounting system: This is a mechanism that offers various forms of methodology

for which company can effectively determine costs incurred throughout the production cycle. By

the applications of this system manager may analyse operations that generated high cost levels.

This method covers work costing, operation costing, marginal and normal costing. With the

support of this system, respective company detect the total cost incurred on producing and

managing various operations within specific time frame.

Essential requirement:

The cost accounting system for various operational and non-operational activities is

primarily permitted for Creams Ltd to recognise their overall cost and determine the non-rentable

activities. Good experience of operating managers through profit-making will spend too much

and raise the income for the period being. This also makes developments in emerging operating

strategies that are theoretically profitable for Creams Ltd. This system is advantageous for

company in different ways such as enables management to determine the main selling products

of the business and also benefit to precise price of the goods to be calculated by presenting the

correct cost information. Management of Creams Ltd will have confidence throughout the

costing method and therefore lead to its outcomes and motivation within its operation that

support to increase the overall efficiency of company. By using the analysis method for the

structure implementation, a carefully-phased framework should be implemented.

Inventory management system: Management implement this system to maintain detailed

information about the raw materials level or Stocks Company hold to manufacture items that are

the most acceptable rates to maximize revenue. This also promotes the recruitment to additional

consumers who boost the company's well-being positively and thereby gain economic benefits.

This program is incorporate by manager of Creams Ltd, to get the benefit of the most favourable

market policy inside the business and retain an acceptable profit margin. This therefore enables

the correct costs of products to be raised to maximize the loyal consumer base. Price

management is a technique that helps Creams Ltd to achieve a level of operation in specified

productivity by discovering how responsive its current consumers are to commodity price

adjustments. In case if a market volume wants to be connected to income and particularly if it

needs to increase profitability while maintaining the same consumer rates, optimum prices are

required.

Cost Accounting system: This is a mechanism that offers various forms of methodology

for which company can effectively determine costs incurred throughout the production cycle. By

the applications of this system manager may analyse operations that generated high cost levels.

This method covers work costing, operation costing, marginal and normal costing. With the

support of this system, respective company detect the total cost incurred on producing and

managing various operations within specific time frame.

Essential requirement:

The cost accounting system for various operational and non-operational activities is

primarily permitted for Creams Ltd to recognise their overall cost and determine the non-rentable

activities. Good experience of operating managers through profit-making will spend too much

and raise the income for the period being. This also makes developments in emerging operating

strategies that are theoretically profitable for Creams Ltd. This system is advantageous for

company in different ways such as enables management to determine the main selling products

of the business and also benefit to precise price of the goods to be calculated by presenting the

correct cost information. Management of Creams Ltd will have confidence throughout the

costing method and therefore lead to its outcomes and motivation within its operation that

support to increase the overall efficiency of company. By using the analysis method for the

structure implementation, a carefully-phased framework should be implemented.

Inventory management system: Management implement this system to maintain detailed

information about the raw materials level or Stocks Company hold to manufacture items that are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

offered to end customers. All goods needed by buyers are produced at Creams Ltd by preserving

the materials according to their requirements (Hall, 2016). These are all classified as follows:

• AVCO (Average Cost Method): In this process, the overall cost related to closing stock is

calculated.

• FIFO (First in First Out): Although this assesses the expense of closing stock on the basis of

the principle that first-place products bought are priced first in a given sequence.

• LIFO (Last in First Out): When the closing stock is priced within this strategy according to the

principle that perhaps the latest bought products are sold at the first spot.

Essential requirement:

In Creams Ltd the program is mainly important for the inventory management and ensuring

that the manufactured products are still able to fulfil changing demand requirements. It further

includes maintaining accurate accounts of any commodity in stores, the overall inventory used in

manufacturing, and the real final goods that can be marketed at every point of purchase. The

system help in various organisation process of creams ltd such as support manager to maximize

efficiency and performance of Creams Ltd by maintaining sufficient stocks. The company has

the specific and comprehensive stock level understanding assisted by this process. In addition,

Creams ltd is involved in consumables, thus this system is particularly more important which

help to choose to call back a particular commodity, compliance review to just call back the

impacted goods. The risk involved within to retrieve at all products without any traceability,

whether or not impacted and missing significant sales numbers.

Job order costing system: It is one of the major MA system used in all companies that

operate several forms of operation. This would be specifically meant to document detailed

details about all events and job happening within company during a specific time (Hirsch,

Seubert, & Sohn, 2015).

Essential requirement:

Creams Limited explicitly applies to the basic provision of the Work Costing Framework

as any employee needs to function with absolute productivity that results in consumer loyalty

and an increased client base. The support business achieves the long-term goals, such as

increased client satisfaction, strong income revenue, improved market image and low staff

turnover. Furthermore, there is no better role in contributing to the success of the business this

program helps remove the same and allows it easier to choose the best choice for the ideal task.

the materials according to their requirements (Hall, 2016). These are all classified as follows:

• AVCO (Average Cost Method): In this process, the overall cost related to closing stock is

calculated.

• FIFO (First in First Out): Although this assesses the expense of closing stock on the basis of

the principle that first-place products bought are priced first in a given sequence.

• LIFO (Last in First Out): When the closing stock is priced within this strategy according to the

principle that perhaps the latest bought products are sold at the first spot.

Essential requirement:

In Creams Ltd the program is mainly important for the inventory management and ensuring

that the manufactured products are still able to fulfil changing demand requirements. It further

includes maintaining accurate accounts of any commodity in stores, the overall inventory used in

manufacturing, and the real final goods that can be marketed at every point of purchase. The

system help in various organisation process of creams ltd such as support manager to maximize

efficiency and performance of Creams Ltd by maintaining sufficient stocks. The company has

the specific and comprehensive stock level understanding assisted by this process. In addition,

Creams ltd is involved in consumables, thus this system is particularly more important which

help to choose to call back a particular commodity, compliance review to just call back the

impacted goods. The risk involved within to retrieve at all products without any traceability,

whether or not impacted and missing significant sales numbers.

Job order costing system: It is one of the major MA system used in all companies that

operate several forms of operation. This would be specifically meant to document detailed

details about all events and job happening within company during a specific time (Hirsch,

Seubert, & Sohn, 2015).

Essential requirement:

Creams Limited explicitly applies to the basic provision of the Work Costing Framework

as any employee needs to function with absolute productivity that results in consumer loyalty

and an increased client base. The support business achieves the long-term goals, such as

increased client satisfaction, strong income revenue, improved market image and low staff

turnover. Furthermore, there is no better role in contributing to the success of the business this

program helps remove the same and allows it easier to choose the best choice for the ideal task.

It benefits and support manager of creams ltd to maximize efficiency and performance of Creams

Ltd by maintaining sufficient stocks. The company has the specific and comprehensive stock

level understanding assisted by this process.

P2 Explanation of Different reporting used in management accounting.

In the current market situation, in several companies the basic method for generating

internal records and analyses is followed, known as MA reporting. Concentration is necessary to

determine whether the organization performs favourably or adversely in certain time frame

(Šiška, 2016). In Creams Ltd, the managers often take various reports into consideration to

guarantee that all the company's goals are accomplished. Some of these are listed under:

Inventory management report: It is really is important to documenting all the materials

that an enterprise needs to carry out all the operational activities. Manager of Creams

Ltd undertakes this report to assess whether they have sufficient products to market different

goods to customers according to their requirements. It is beneficial for the company, as it can

help supply of goods on time and reduce the possibility of unsatisfied purchasers.

Budget report: It is largely related with plans that businesses have made to allocate

resources to all departments as per their requirements so that administrators can carry out

every operations. Creams Ltd also needs this report to ensure planned activities are held within

the same budget previously decided upon or not. This is beneficial for the organization and with

the assistance of this report; the necessary money will be allocated to the departments to perform

all of their tasks.

Account receivable report: It is mainly related to monitoring these customers' data which

will allow future sales and on credit transactions of goods. In Creams Limited, it is achieved by

management to maintain correct information about the volume owed and, in the meantime, the

customers will recover on a timeline. It is beneficial to the department as it will assist in

determining the actual exception which will be given in the upcoming time.

Performance document: This study is generated in most companies as the total

performance of the whole enterprise and its employees is measured (van Helden and Uddin,

2016). The manager of Creams Ltd often establishes it to determine the company's success as

well as to ascertain whether employees are making adequate objectives to contribute to the

growth of the business. This is really good for the business and therefore will allow the managers

to give bonuses and benefits to the employees because of their performance.

Ltd by maintaining sufficient stocks. The company has the specific and comprehensive stock

level understanding assisted by this process.

P2 Explanation of Different reporting used in management accounting.

In the current market situation, in several companies the basic method for generating

internal records and analyses is followed, known as MA reporting. Concentration is necessary to

determine whether the organization performs favourably or adversely in certain time frame

(Šiška, 2016). In Creams Ltd, the managers often take various reports into consideration to

guarantee that all the company's goals are accomplished. Some of these are listed under:

Inventory management report: It is really is important to documenting all the materials

that an enterprise needs to carry out all the operational activities. Manager of Creams

Ltd undertakes this report to assess whether they have sufficient products to market different

goods to customers according to their requirements. It is beneficial for the company, as it can

help supply of goods on time and reduce the possibility of unsatisfied purchasers.

Budget report: It is largely related with plans that businesses have made to allocate

resources to all departments as per their requirements so that administrators can carry out

every operations. Creams Ltd also needs this report to ensure planned activities are held within

the same budget previously decided upon or not. This is beneficial for the organization and with

the assistance of this report; the necessary money will be allocated to the departments to perform

all of their tasks.

Account receivable report: It is mainly related to monitoring these customers' data which

will allow future sales and on credit transactions of goods. In Creams Limited, it is achieved by

management to maintain correct information about the volume owed and, in the meantime, the

customers will recover on a timeline. It is beneficial to the department as it will assist in

determining the actual exception which will be given in the upcoming time.

Performance document: This study is generated in most companies as the total

performance of the whole enterprise and its employees is measured (van Helden and Uddin,

2016). The manager of Creams Ltd often establishes it to determine the company's success as

well as to ascertain whether employees are making adequate objectives to contribute to the

growth of the business. This is really good for the business and therefore will allow the managers

to give bonuses and benefits to the employees because of their performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1 Benefits of adopting management accounting system

System Benefits

Cost accounting system These system Enables executives in a manner which

helps to evaluate the company's biggest consumer

goods.

It also allows determining the exact prices for the

products by having the right cost details.

Inventory management

system

This aid manager to improve Creams Ltd productivity

and profitability by retaining adequate stock.

Supported by this method, the business has the detail

and accurate knowledge about stock level.

Job costing system Managers assess the efficiency of a firm's specific work.

It offers maximum charge details such as wages, content

and other operating costs that are expanded within the

business in various occupations.

Price optimisation system This system support to implement the most beneficial

pricing strategy within company so that proper profit

margin can be maintained.

It also enables to fix the suitable prices of goods so that

loyal customer base can be increased.

D1 Integration of management report and accounting system

This is really important for the manager of Creams, to implement different system and

reports within organisation process in order to attain the company goals within specific time

frame. Such as cost accounting system is use to detect the total cost involved in within various

operation and activities and on the other side the cost reporting system to record the total cost

used in these operation. Similarly, budget report records the allocated funds on different

operation and actual cost spend over these activities.

System Benefits

Cost accounting system These system Enables executives in a manner which

helps to evaluate the company's biggest consumer

goods.

It also allows determining the exact prices for the

products by having the right cost details.

Inventory management

system

This aid manager to improve Creams Ltd productivity

and profitability by retaining adequate stock.

Supported by this method, the business has the detail

and accurate knowledge about stock level.

Job costing system Managers assess the efficiency of a firm's specific work.

It offers maximum charge details such as wages, content

and other operating costs that are expanded within the

business in various occupations.

Price optimisation system This system support to implement the most beneficial

pricing strategy within company so that proper profit

margin can be maintained.

It also enables to fix the suitable prices of goods so that

loyal customer base can be increased.

D1 Integration of management report and accounting system

This is really important for the manager of Creams, to implement different system and

reports within organisation process in order to attain the company goals within specific time

frame. Such as cost accounting system is use to detect the total cost involved in within various

operation and activities and on the other side the cost reporting system to record the total cost

used in these operation. Similarly, budget report records the allocated funds on different

operation and actual cost spend over these activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

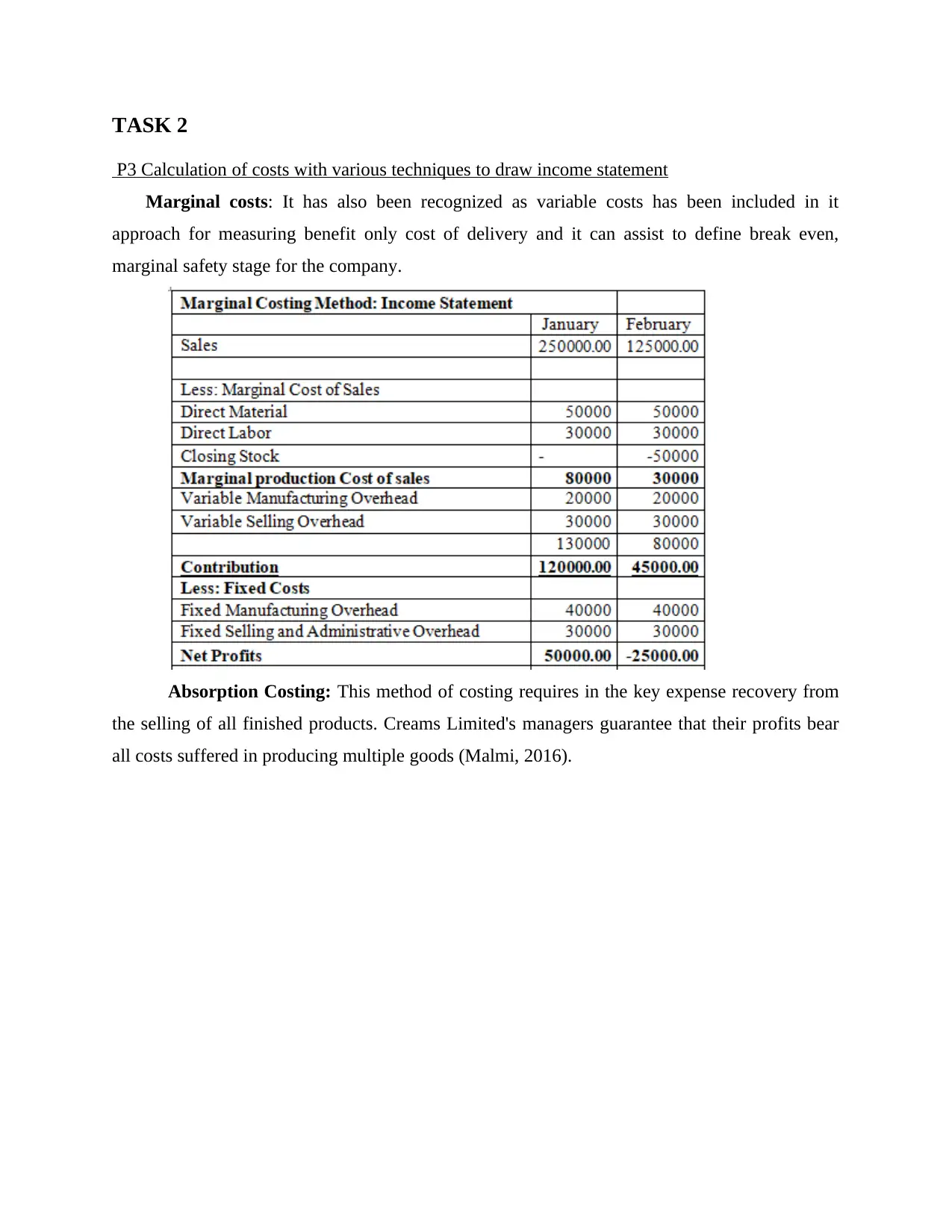

P3 Calculation of costs with various techniques to draw income statement

Marginal costs: It has also been recognized as variable costs has been included in it

approach for measuring benefit only cost of delivery and it can assist to define break even,

marginal safety stage for the company.

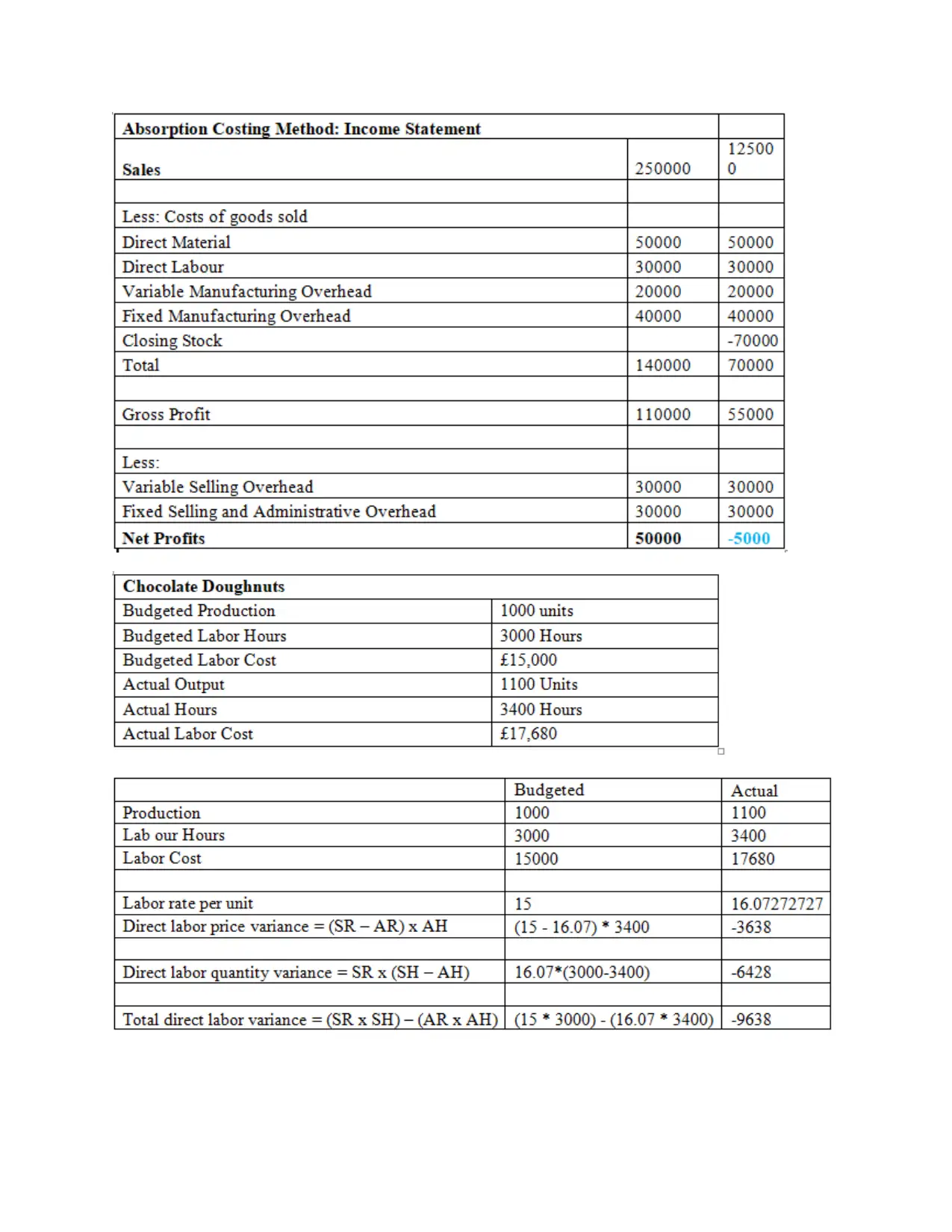

Absorption Costing: This method of costing requires in the key expense recovery from

the selling of all finished products. Creams Limited's managers guarantee that their profits bear

all costs suffered in producing multiple goods (Malmi, 2016).

P3 Calculation of costs with various techniques to draw income statement

Marginal costs: It has also been recognized as variable costs has been included in it

approach for measuring benefit only cost of delivery and it can assist to define break even,

marginal safety stage for the company.

Absorption Costing: This method of costing requires in the key expense recovery from

the selling of all finished products. Creams Limited's managers guarantee that their profits bear

all costs suffered in producing multiple goods (Malmi, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 Apply a range of management accounting techniques

Cost-volume profit analysis: Cost volume profit evaluation is really a cost accounting

approach that looks at the effect on net revenue that different rates of cost as well as volume have

in specific time. The CVP model, also widely recognized as break-even model, tries to calculate

the break-even point for various revenue levels and expense structures which can be helpful for

management making short-term economic decisions.

Cost-volume profit analysis: Cost volume profit evaluation is really a cost accounting

approach that looks at the effect on net revenue that different rates of cost as well as volume have

in specific time. The CVP model, also widely recognized as break-even model, tries to calculate

the break-even point for various revenue levels and expense structures which can be helpful for

management making short-term economic decisions.

Activity-based costing: Activity-based costing (ABC) is a system of costing related goods

and services which assigns overhead and administration costs. This costly accounting approach

considers the association between prices, operating operations and manufactured goods, applying

indirect costs to goods less objectively than conventional costing approaches.

D2 Analysis of data by financial report

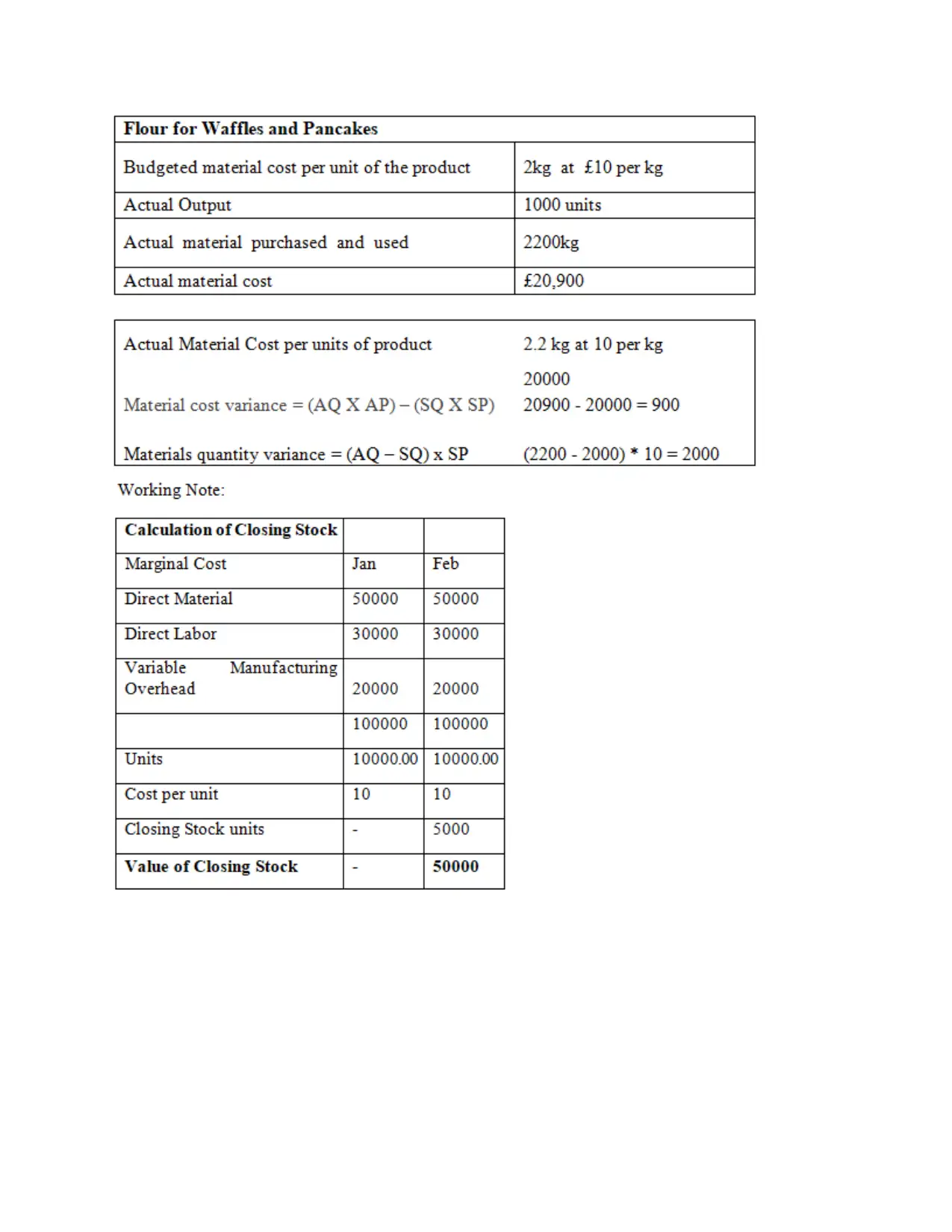

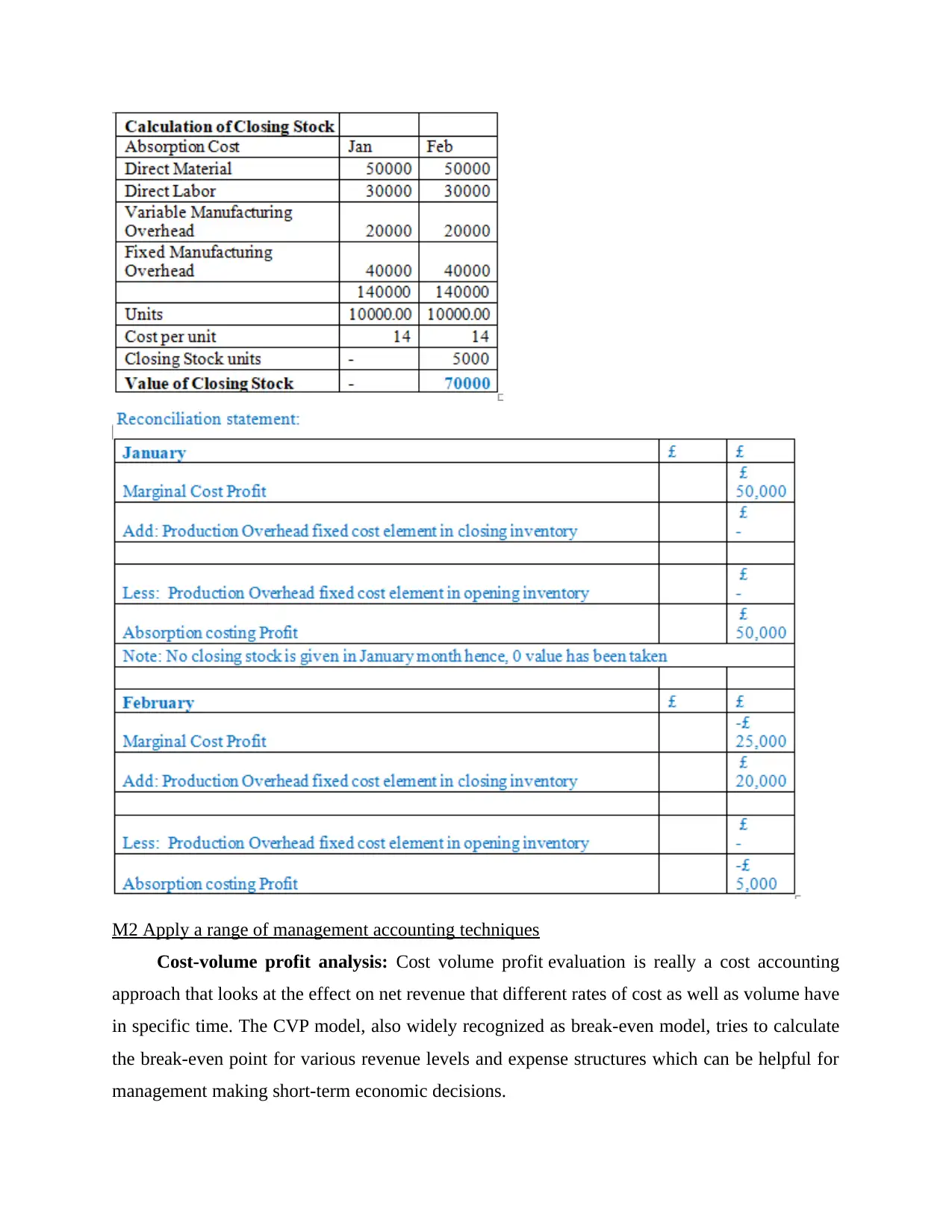

The annual report reflects organisation's income and expenses over a specified period of

time. Creams Ltd manager will use both marginal and absorption costing financial statements to

define product amount and benefit connection with the factor consequence it already have in

specific period. From the above figures it has been determined that labour rate and volume

differences will be 3638(a) and 6428(a) for the company. The client will be paid 900(f) and

2000(f) in terms of manufacturing costs and demand fluctuations.

TASK 3

P4. Different planning tools with its advantages and disadvantages.

Budgetary management is referred to as the mechanism by which companies plan their

budget for upcoming time and equate the same with current results in order to assess any

difference. The managers of a company can quickly spot discrepancies and make necessary

adjustments by comparing the predicted forecasts to the real figures. This mechanism ensures

that management of Creams Ltd recognize the spending limits of different operation within a

time frame. This control is important because excessive spending has an adverse impact towards

corporate revenue.

The main goal of Creams Ltd by using the budgetary control is to evaluate the gap

between the actual and budgeted figures which is vital to the success of the organization. This

contributes to improved efficiency and output of the companies within appropriate time manner.

Budgeting performs a vital role in planning and handling, since it promotes resource distribution

that is distributed for most effective purpose, while retaining market efficiency (Quattrone,

2016). A effective process of budgetary management encourages the planning of different

activities and ensures productive and systematic activity of the company. This also combines

recommendations from rising management levels to prepare the budget as well as encourage

cooperation across divisions. Some of the crucial planning tools are defined underneath in the

context of Creams Ltd:

and services which assigns overhead and administration costs. This costly accounting approach

considers the association between prices, operating operations and manufactured goods, applying

indirect costs to goods less objectively than conventional costing approaches.

D2 Analysis of data by financial report

The annual report reflects organisation's income and expenses over a specified period of

time. Creams Ltd manager will use both marginal and absorption costing financial statements to

define product amount and benefit connection with the factor consequence it already have in

specific period. From the above figures it has been determined that labour rate and volume

differences will be 3638(a) and 6428(a) for the company. The client will be paid 900(f) and

2000(f) in terms of manufacturing costs and demand fluctuations.

TASK 3

P4. Different planning tools with its advantages and disadvantages.

Budgetary management is referred to as the mechanism by which companies plan their

budget for upcoming time and equate the same with current results in order to assess any

difference. The managers of a company can quickly spot discrepancies and make necessary

adjustments by comparing the predicted forecasts to the real figures. This mechanism ensures

that management of Creams Ltd recognize the spending limits of different operation within a

time frame. This control is important because excessive spending has an adverse impact towards

corporate revenue.

The main goal of Creams Ltd by using the budgetary control is to evaluate the gap

between the actual and budgeted figures which is vital to the success of the organization. This

contributes to improved efficiency and output of the companies within appropriate time manner.

Budgeting performs a vital role in planning and handling, since it promotes resource distribution

that is distributed for most effective purpose, while retaining market efficiency (Quattrone,

2016). A effective process of budgetary management encourages the planning of different

activities and ensures productive and systematic activity of the company. This also combines

recommendations from rising management levels to prepare the budget as well as encourage

cooperation across divisions. Some of the crucial planning tools are defined underneath in the

context of Creams Ltd:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.