Management Accounting Report: Financial Planning and Analysis

VerifiedAdded on 2020/06/05

|17

|4891

|153

Report

AI Summary

This report delves into the core principles of management accounting, focusing on its application within Tech (UK) Ltd., a company specializing in mobile phone chargers. It begins by differentiating between management and financial accounting, emphasizing the role of management accounting in strategic planning, performance management, and risk control. The report then explores various management accounting systems, including cost management, inventory management, and job costing, highlighting their significance in cost determination, inventory control, and production management. It further examines different types of managerial accounting reports, such as budget reports, accounts receivable reports, and job cost reports, and their importance in decision-making, cost reduction, and financial returns. The report also covers cost calculation methods, including marginal costing and absorption costing, and provides an overview of budgeting techniques, discussing their merits and demerits. Finally, the report addresses the use of management accounting in responding to financial problems. The report incorporates key concepts and provides practical examples relevant to the business operations of Tech (UK) Ltd., offering a comprehensive analysis of management accounting tools and techniques for effective financial management.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and essential requirements of management accounting systems..1

P2: Different types of managerial accounting reports and their importance..............................3

TASK 2............................................................................................................................................5

P3: Calculation of cost and preparation of income statement.....................................................5

TASK 3............................................................................................................................................7

P4: Different kind of Budgets and their merits and demerits......................................................7

TASK 4..........................................................................................................................................10

P5: Use of management accounting to respond financial problem...........................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and essential requirements of management accounting systems..1

P2: Different types of managerial accounting reports and their importance..............................3

TASK 2............................................................................................................................................5

P3: Calculation of cost and preparation of income statement.....................................................5

TASK 3............................................................................................................................................7

P4: Different kind of Budgets and their merits and demerits......................................................7

TASK 4..........................................................................................................................................10

P5: Use of management accounting to respond financial problem...........................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting enables an organisation to make an effective decision with the

help of information collected from different departments with a motive of achieving competitive

advantage. This allows managers2_1525961397 (1) to perform specific functions such as

strategic management, performance appraisal and risk control. It helps in formulating policies

and strategies through which they can direct the employees to work in the best possible way.

Tech (UK) Ltd. which deals in providing special charger for mobile telephones and other gadgets

foe the retail outlets in the UK. The project covers the difference between management and

financial accounting as well as the importance of management accounting and reporting system

in the growth of business organisation. Moreover, the benefits and drawbacks of different

financial tools to control budgets are also discussed under this report (Garrison and et. al., 2010).

.

TASK 1

P1: Management accounting and essential requirements of management accounting systems

Management accounting:

It refers to the process of preparing and maintaining financial reports and documents

containing all financial and non-financial information which is helpful in making effective plans

and strategies for future business activities. Such documents help company and its stakeholders

in identifying the actual financial position on the basis of which the decision has been taken by

them for the betterment of an organisation.

The main functions which need to be performed by managers of Tech (UK) company are

described as below:

Strategic management: The accountant manager can make effective planning and

strategies with the help of using data available through management accounting and reporting

systems (Fullerton, Kennedy and Widener, 2014).

Performance management: The performance of company depends on the performance

of employees therefore, it is essentially required for manager to analyse the performance of

employees on the basis of their past year performance so that they can motivate them by

providing rewards, compensation etc.

1

Management accounting enables an organisation to make an effective decision with the

help of information collected from different departments with a motive of achieving competitive

advantage. This allows managers2_1525961397 (1) to perform specific functions such as

strategic management, performance appraisal and risk control. It helps in formulating policies

and strategies through which they can direct the employees to work in the best possible way.

Tech (UK) Ltd. which deals in providing special charger for mobile telephones and other gadgets

foe the retail outlets in the UK. The project covers the difference between management and

financial accounting as well as the importance of management accounting and reporting system

in the growth of business organisation. Moreover, the benefits and drawbacks of different

financial tools to control budgets are also discussed under this report (Garrison and et. al., 2010).

.

TASK 1

P1: Management accounting and essential requirements of management accounting systems

Management accounting:

It refers to the process of preparing and maintaining financial reports and documents

containing all financial and non-financial information which is helpful in making effective plans

and strategies for future business activities. Such documents help company and its stakeholders

in identifying the actual financial position on the basis of which the decision has been taken by

them for the betterment of an organisation.

The main functions which need to be performed by managers of Tech (UK) company are

described as below:

Strategic management: The accountant manager can make effective planning and

strategies with the help of using data available through management accounting and reporting

systems (Fullerton, Kennedy and Widener, 2014).

Performance management: The performance of company depends on the performance

of employees therefore, it is essentially required for manager to analyse the performance of

employees on the basis of their past year performance so that they can motivate them by

providing rewards, compensation etc.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk management: With the help of accounting and reporting system, the manager can

identify the risk which can affect the performance of company and accordingly, make corrective

measures in order to overcome such risk.

Difference between management and financial accounting

Management accounting Financial accounting

Its main purpose is to make effective plans and

policies to operate business activities more

smoothly.

Its main focus is to show true and fair financial

position of company through preparing

financial reports such as P&L a/c and Balance

sheet.

It provides financial as well as non-financial

information to the management of company.

It only provides financial information to

company.

Its main aim is to provide relevant data to the

internal management of company so that they

can make an effective decisions.

Its main objective is to provide the financial

data to the outsiders which includes investors,

stakeholders etc.

It is prepared as per the needs of the

organisation.

It is prepared annually.

Importance of management accounting in decision making process

Determination of aim: With the help of information available through management

accounting system, the managers can easily determine the target which needs to be achieve in

near future (Dillard and Roslender, 2011).

Helps in formulation of plans: After analysing the financial and non-financial

information, the managers of different departments can mutually make an effective decision and

plans for the betterment of an organisation.

Measurement of performance: The accounting systems provides all information related

with financial transactions, employee's performance etc. which help management to identify the

actual performance of company. Analysing the performance through comparing actual with

standard help in determining and removing deviation if any.

2

identify the risk which can affect the performance of company and accordingly, make corrective

measures in order to overcome such risk.

Difference between management and financial accounting

Management accounting Financial accounting

Its main purpose is to make effective plans and

policies to operate business activities more

smoothly.

Its main focus is to show true and fair financial

position of company through preparing

financial reports such as P&L a/c and Balance

sheet.

It provides financial as well as non-financial

information to the management of company.

It only provides financial information to

company.

Its main aim is to provide relevant data to the

internal management of company so that they

can make an effective decisions.

Its main objective is to provide the financial

data to the outsiders which includes investors,

stakeholders etc.

It is prepared as per the needs of the

organisation.

It is prepared annually.

Importance of management accounting in decision making process

Determination of aim: With the help of information available through management

accounting system, the managers can easily determine the target which needs to be achieve in

near future (Dillard and Roslender, 2011).

Helps in formulation of plans: After analysing the financial and non-financial

information, the managers of different departments can mutually make an effective decision and

plans for the betterment of an organisation.

Measurement of performance: The accounting systems provides all information related

with financial transactions, employee's performance etc. which help management to identify the

actual performance of company. Analysing the performance through comparing actual with

standard help in determining and removing deviation if any.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different management accounting systems

There are various management accounting systems which are listed below:

Cost management system: This system helps management of Tech (UK) Limited to

determine cost which is used in manufacturing products so that they can recover it from their

customers along with margins. Addition of labour cost, material cost, overhead expenses etc.

brings total product cost. The management is also required to determine what the customers

think about the price the company charged while buying product. The queries regarding level of

satisfaction of customers related with prices of products need to be analysed and solved as

quickly as possible (Cinquini and Tenucci, 2010). For example, if the demand of mobile charger

are increased then in order to grab such opportunity the company should required to increase the

prices of their products and generate huge revenues.

Actual Costing Standard costing Normal costing

Under this, cost of job is

properly evaluated with the

help of using actual direct

material and applied overhead.

In this, cost of the job is

properly analyses through

budgeting of direct and

standard cost at the time of

production.

The actual price are

determined after analysing the

direct labour and direct

material cost incurred in future

production process.

Inventory management system: This system is useful in maintain minimum level of

stock with company which ensures them in meeting the needs and demands of targeted

customers. The managers have to ensure about proper allocation of resources to each department

on the basis of assuming outcome received in future. This help company in fulfilling the

demands of customers through ordering raw materials whenever they feel shortage. For example,

if the manager find that the company have insufficient products to fulfil demand of customers

then they should required to ordered products in advances so as to meet the demand.

Types of inventory valuation techniques:

FIFO: According to this, the materials comes first in warehouses will used first in

production process. Using FIFO, the oldest cost of goods are identified as cost first. No GAAP

restrictions are followed while using FIFO at the time of reporting financial outcomes.

3

There are various management accounting systems which are listed below:

Cost management system: This system helps management of Tech (UK) Limited to

determine cost which is used in manufacturing products so that they can recover it from their

customers along with margins. Addition of labour cost, material cost, overhead expenses etc.

brings total product cost. The management is also required to determine what the customers

think about the price the company charged while buying product. The queries regarding level of

satisfaction of customers related with prices of products need to be analysed and solved as

quickly as possible (Cinquini and Tenucci, 2010). For example, if the demand of mobile charger

are increased then in order to grab such opportunity the company should required to increase the

prices of their products and generate huge revenues.

Actual Costing Standard costing Normal costing

Under this, cost of job is

properly evaluated with the

help of using actual direct

material and applied overhead.

In this, cost of the job is

properly analyses through

budgeting of direct and

standard cost at the time of

production.

The actual price are

determined after analysing the

direct labour and direct

material cost incurred in future

production process.

Inventory management system: This system is useful in maintain minimum level of

stock with company which ensures them in meeting the needs and demands of targeted

customers. The managers have to ensure about proper allocation of resources to each department

on the basis of assuming outcome received in future. This help company in fulfilling the

demands of customers through ordering raw materials whenever they feel shortage. For example,

if the manager find that the company have insufficient products to fulfil demand of customers

then they should required to ordered products in advances so as to meet the demand.

Types of inventory valuation techniques:

FIFO: According to this, the materials comes first in warehouses will used first in

production process. Using FIFO, the oldest cost of goods are identified as cost first. No GAAP

restrictions are followed while using FIFO at the time of reporting financial outcomes.

3

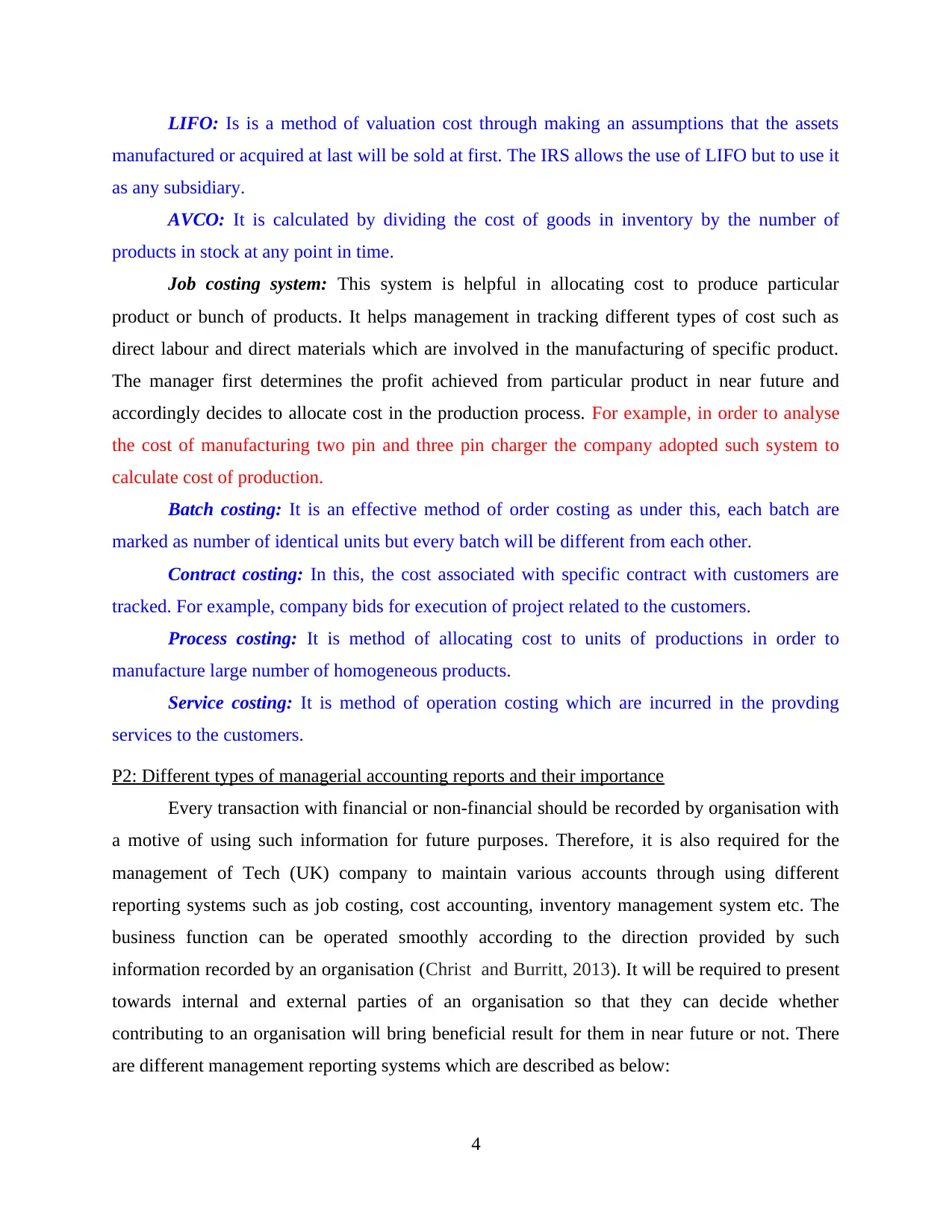

LIFO: Is is a method of valuation cost through making an assumptions that the assets

manufactured or acquired at last will be sold at first. The IRS allows the use of LIFO but to use it

as any subsidiary.

AVCO: It is calculated by dividing the cost of goods in inventory by the number of

products in stock at any point in time.

Job costing system: This system is helpful in allocating cost to produce particular

product or bunch of products. It helps management in tracking different types of cost such as

direct labour and direct materials which are involved in the manufacturing of specific product.

The manager first determines the profit achieved from particular product in near future and

accordingly decides to allocate cost in the production process. For example, in order to analyse

the cost of manufacturing two pin and three pin charger the company adopted such system to

calculate cost of production.

Batch costing: It is an effective method of order costing as under this, each batch are

marked as number of identical units but every batch will be different from each other.

Contract costing: In this, the cost associated with specific contract with customers are

tracked. For example, company bids for execution of project related to the customers.

Process costing: It is method of allocating cost to units of productions in order to

manufacture large number of homogeneous products.

Service costing: It is method of operation costing which are incurred in the provding

services to the customers.

P2: Different types of managerial accounting reports and their importance

Every transaction with financial or non-financial should be recorded by organisation with

a motive of using such information for future purposes. Therefore, it is also required for the

management of Tech (UK) company to maintain various accounts through using different

reporting systems such as job costing, cost accounting, inventory management system etc. The

business function can be operated smoothly according to the direction provided by such

information recorded by an organisation (Christ and Burritt, 2013). It will be required to present

towards internal and external parties of an organisation so that they can decide whether

contributing to an organisation will bring beneficial result for them in near future or not. There

are different management reporting systems which are described as below:

4

manufactured or acquired at last will be sold at first. The IRS allows the use of LIFO but to use it

as any subsidiary.

AVCO: It is calculated by dividing the cost of goods in inventory by the number of

products in stock at any point in time.

Job costing system: This system is helpful in allocating cost to produce particular

product or bunch of products. It helps management in tracking different types of cost such as

direct labour and direct materials which are involved in the manufacturing of specific product.

The manager first determines the profit achieved from particular product in near future and

accordingly decides to allocate cost in the production process. For example, in order to analyse

the cost of manufacturing two pin and three pin charger the company adopted such system to

calculate cost of production.

Batch costing: It is an effective method of order costing as under this, each batch are

marked as number of identical units but every batch will be different from each other.

Contract costing: In this, the cost associated with specific contract with customers are

tracked. For example, company bids for execution of project related to the customers.

Process costing: It is method of allocating cost to units of productions in order to

manufacture large number of homogeneous products.

Service costing: It is method of operation costing which are incurred in the provding

services to the customers.

P2: Different types of managerial accounting reports and their importance

Every transaction with financial or non-financial should be recorded by organisation with

a motive of using such information for future purposes. Therefore, it is also required for the

management of Tech (UK) company to maintain various accounts through using different

reporting systems such as job costing, cost accounting, inventory management system etc. The

business function can be operated smoothly according to the direction provided by such

information recorded by an organisation (Christ and Burritt, 2013). It will be required to present

towards internal and external parties of an organisation so that they can decide whether

contributing to an organisation will bring beneficial result for them in near future or not. There

are different management reporting systems which are described as below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report: These reports are helpful in analysing the performance of different

departments and reduce cost incurred in future business activities. It is prepared on the basis of

estimation of cost incurred after making proper analysis of cost incurred in previous years. This

will help in making scenario of doing future business activities in front of their employees so that

they can perform in right direction (Baldvinsdottir, Mitchell and Nørreklit, 2010).

Accounts Receivable report: This report helps in representing the information about the

list of debtors whose payment are due to company. Its supports management in reminding the

name of unpaid debtors for the purpose of recovery on particular date. Such report ensures

company about having sufficient funds which can be called anytime. For this, it is important for

the manager to understand about the credit policies and need to focus on adopting various

measures to recover of dues from their customers.

Job cost reports: This report provides information about the cost and revenue incurred in

producing specific product or group of products. It is important for manager to identify such area

where they get profitable outcome and accordingly, decide what percentage of amount should be

invested in such areas. Thus, all actions related with allocation of cost are depend on the

profitable result received in future.

Inventory and manufacturing: These reports provides the details of resources available

with them at the time of operating business functions. It helps management to know the

requirements of inventory which forces them to order adequate inventory from suppliers in order

to run production process without any interruptions and are able to meet customer's needs and

demands (Macintosh and Quattrone, 2010).

Importance of managerial accounting reports:

Decision making: Availability of information related with financial as well as non-

financial which help them in knowing their actual financial position thus all the necessary steps

for execution of business activities are taken accordingly. This helps management in formulating

planning, performance management and risk management which enhances their productivity and

profitability.

Reduces cost: These information helps the management of company to anticipate the

future problems and make an effective plans for the purpose of eliminating such problems as

quickly as possible. This will help in reducing cost of production process through which they

able to provide quality products at an affordable price.

5

departments and reduce cost incurred in future business activities. It is prepared on the basis of

estimation of cost incurred after making proper analysis of cost incurred in previous years. This

will help in making scenario of doing future business activities in front of their employees so that

they can perform in right direction (Baldvinsdottir, Mitchell and Nørreklit, 2010).

Accounts Receivable report: This report helps in representing the information about the

list of debtors whose payment are due to company. Its supports management in reminding the

name of unpaid debtors for the purpose of recovery on particular date. Such report ensures

company about having sufficient funds which can be called anytime. For this, it is important for

the manager to understand about the credit policies and need to focus on adopting various

measures to recover of dues from their customers.

Job cost reports: This report provides information about the cost and revenue incurred in

producing specific product or group of products. It is important for manager to identify such area

where they get profitable outcome and accordingly, decide what percentage of amount should be

invested in such areas. Thus, all actions related with allocation of cost are depend on the

profitable result received in future.

Inventory and manufacturing: These reports provides the details of resources available

with them at the time of operating business functions. It helps management to know the

requirements of inventory which forces them to order adequate inventory from suppliers in order

to run production process without any interruptions and are able to meet customer's needs and

demands (Macintosh and Quattrone, 2010).

Importance of managerial accounting reports:

Decision making: Availability of information related with financial as well as non-

financial which help them in knowing their actual financial position thus all the necessary steps

for execution of business activities are taken accordingly. This helps management in formulating

planning, performance management and risk management which enhances their productivity and

profitability.

Reduces cost: These information helps the management of company to anticipate the

future problems and make an effective plans for the purpose of eliminating such problems as

quickly as possible. This will help in reducing cost of production process through which they

able to provide quality products at an affordable price.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Increase financial returns: As all the actions and procedures are implemented which

required to be followed by management of company. Thus It requires to conduct training

programs to their employees so as to perform better and achieve best possible outcomes in near

future (Nandan, 2010).

TASK 2

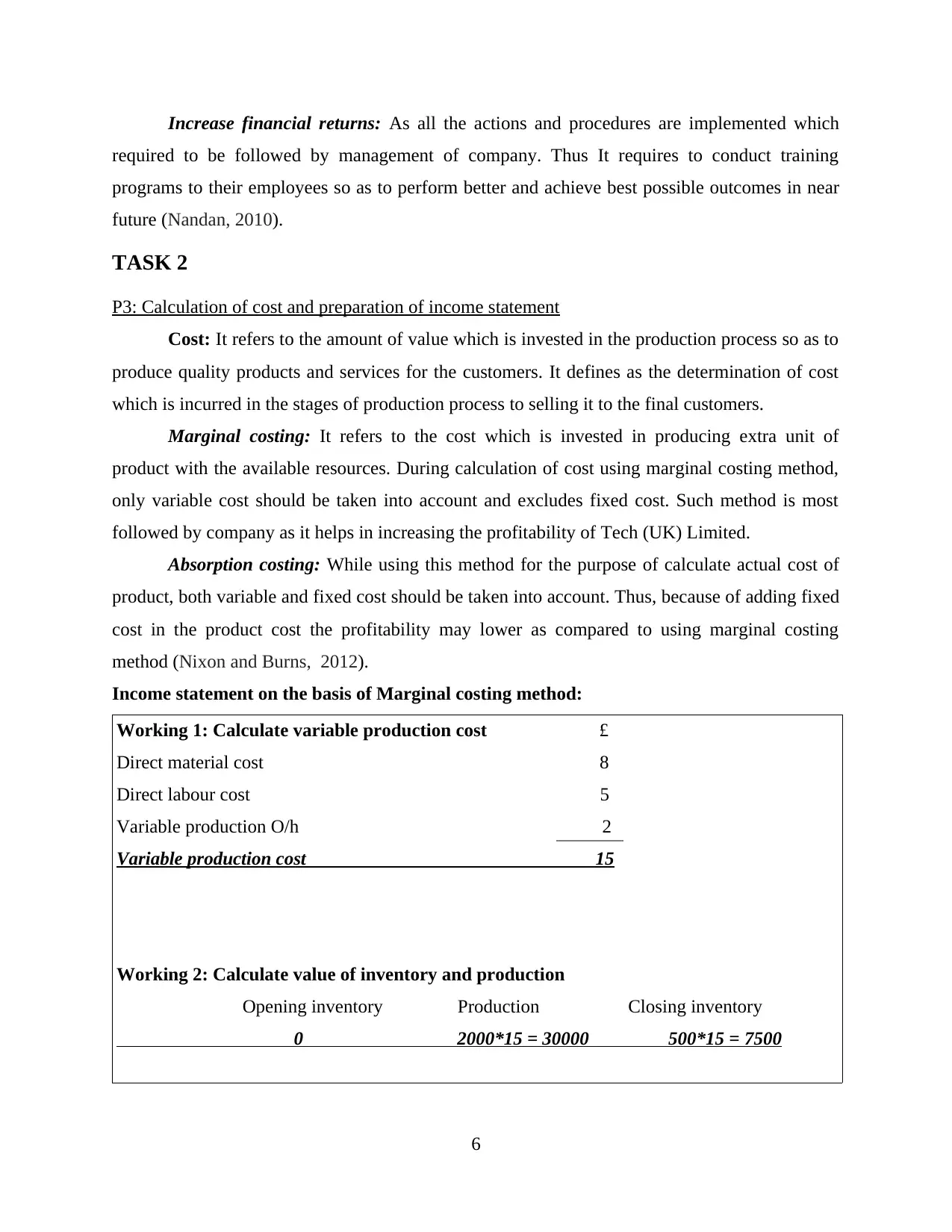

P3: Calculation of cost and preparation of income statement

Cost: It refers to the amount of value which is invested in the production process so as to

produce quality products and services for the customers. It defines as the determination of cost

which is incurred in the stages of production process to selling it to the final customers.

Marginal costing: It refers to the cost which is invested in producing extra unit of

product with the available resources. During calculation of cost using marginal costing method,

only variable cost should be taken into account and excludes fixed cost. Such method is most

followed by company as it helps in increasing the profitability of Tech (UK) Limited.

Absorption costing: While using this method for the purpose of calculate actual cost of

product, both variable and fixed cost should be taken into account. Thus, because of adding fixed

cost in the product cost the profitability may lower as compared to using marginal costing

method (Nixon and Burns, 2012).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

6

required to be followed by management of company. Thus It requires to conduct training

programs to their employees so as to perform better and achieve best possible outcomes in near

future (Nandan, 2010).

TASK 2

P3: Calculation of cost and preparation of income statement

Cost: It refers to the amount of value which is invested in the production process so as to

produce quality products and services for the customers. It defines as the determination of cost

which is incurred in the stages of production process to selling it to the final customers.

Marginal costing: It refers to the cost which is invested in producing extra unit of

product with the available resources. During calculation of cost using marginal costing method,

only variable cost should be taken into account and excludes fixed cost. Such method is most

followed by company as it helps in increasing the profitability of Tech (UK) Limited.

Absorption costing: While using this method for the purpose of calculate actual cost of

product, both variable and fixed cost should be taken into account. Thus, because of adding fixed

cost in the product cost the profitability may lower as compared to using marginal costing

method (Nixon and Burns, 2012).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

6

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

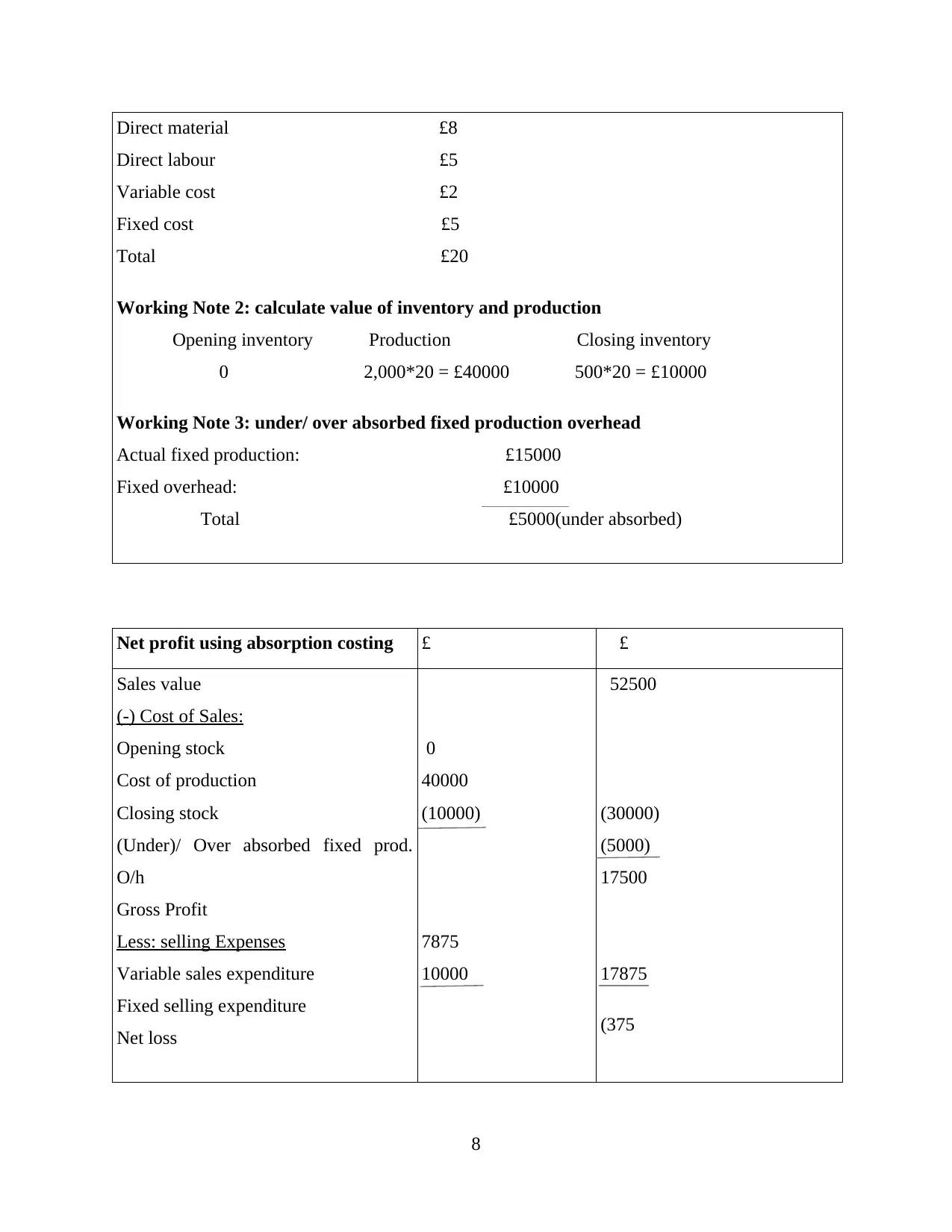

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000 and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

7

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000 and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375

8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

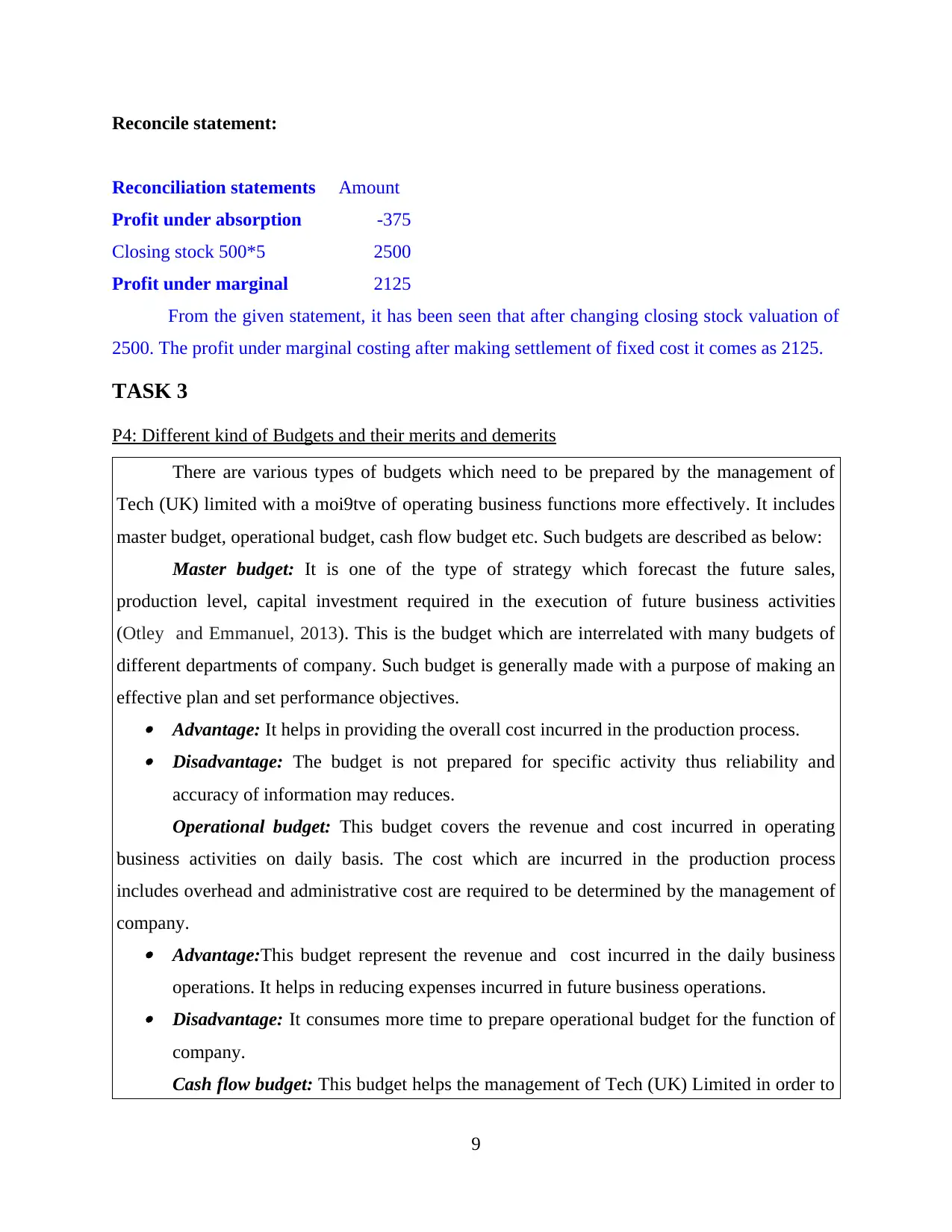

Reconcile statement:

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

From the given statement, it has been seen that after changing closing stock valuation of

2500. The profit under marginal costing after making settlement of fixed cost it comes as 2125.

TASK 3

P4: Different kind of Budgets and their merits and demerits

There are various types of budgets which need to be prepared by the management of

Tech (UK) limited with a moi9tve of operating business functions more effectively. It includes

master budget, operational budget, cash flow budget etc. Such budgets are described as below:

Master budget: It is one of the type of strategy which forecast the future sales,

production level, capital investment required in the execution of future business activities

(Otley and Emmanuel, 2013). This is the budget which are interrelated with many budgets of

different departments of company. Such budget is generally made with a purpose of making an

effective plan and set performance objectives. Advantage: It helps in providing the overall cost incurred in the production process. Disadvantage: The budget is not prepared for specific activity thus reliability and

accuracy of information may reduces.

Operational budget: This budget covers the revenue and cost incurred in operating

business activities on daily basis. The cost which are incurred in the production process

includes overhead and administrative cost are required to be determined by the management of

company. Advantage:This budget represent the revenue and cost incurred in the daily business

operations. It helps in reducing expenses incurred in future business operations. Disadvantage: It consumes more time to prepare operational budget for the function of

company.

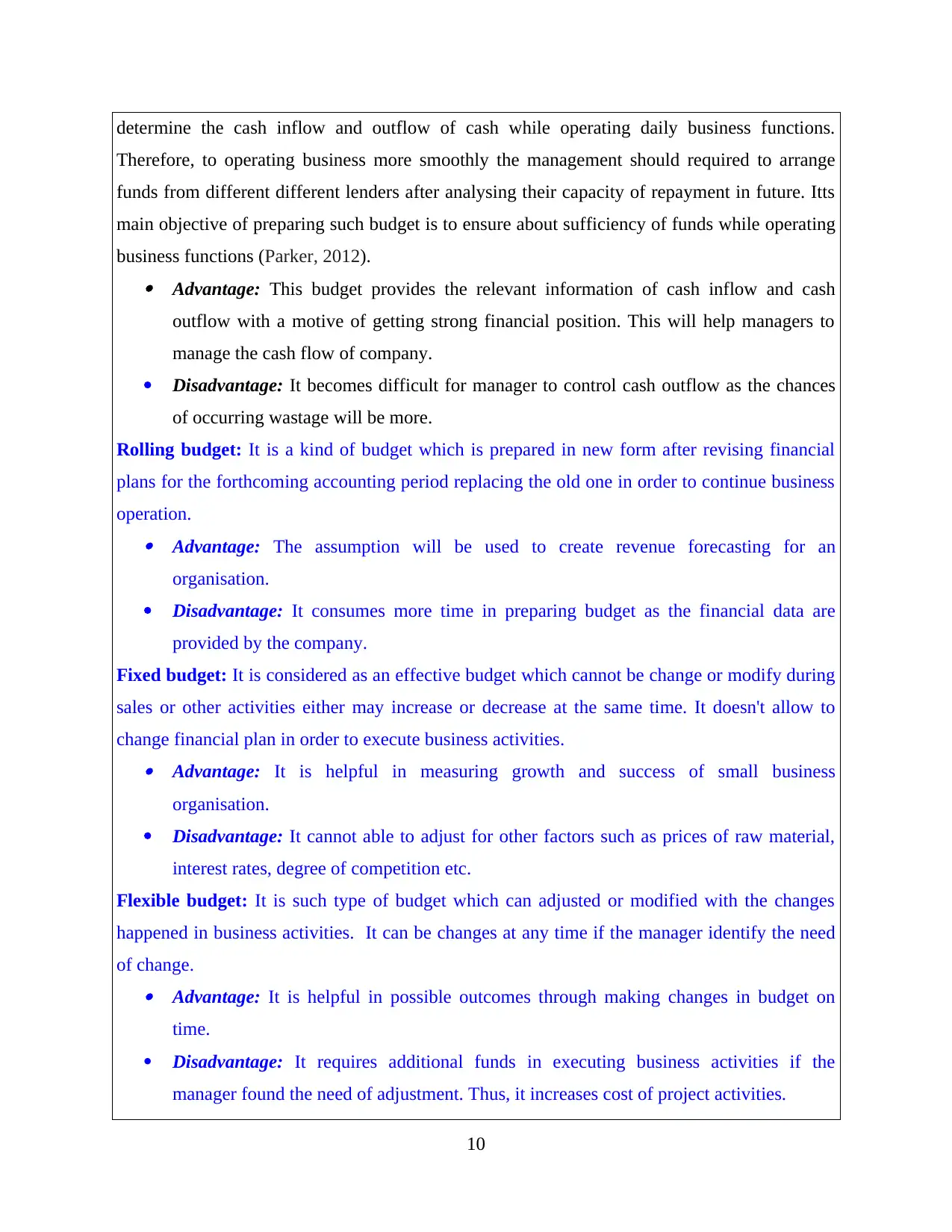

Cash flow budget: This budget helps the management of Tech (UK) Limited in order to

9

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

From the given statement, it has been seen that after changing closing stock valuation of

2500. The profit under marginal costing after making settlement of fixed cost it comes as 2125.

TASK 3

P4: Different kind of Budgets and their merits and demerits

There are various types of budgets which need to be prepared by the management of

Tech (UK) limited with a moi9tve of operating business functions more effectively. It includes

master budget, operational budget, cash flow budget etc. Such budgets are described as below:

Master budget: It is one of the type of strategy which forecast the future sales,

production level, capital investment required in the execution of future business activities

(Otley and Emmanuel, 2013). This is the budget which are interrelated with many budgets of

different departments of company. Such budget is generally made with a purpose of making an

effective plan and set performance objectives. Advantage: It helps in providing the overall cost incurred in the production process. Disadvantage: The budget is not prepared for specific activity thus reliability and

accuracy of information may reduces.

Operational budget: This budget covers the revenue and cost incurred in operating

business activities on daily basis. The cost which are incurred in the production process

includes overhead and administrative cost are required to be determined by the management of

company. Advantage:This budget represent the revenue and cost incurred in the daily business

operations. It helps in reducing expenses incurred in future business operations. Disadvantage: It consumes more time to prepare operational budget for the function of

company.

Cash flow budget: This budget helps the management of Tech (UK) Limited in order to

9

determine the cash inflow and outflow of cash while operating daily business functions.

Therefore, to operating business more smoothly the management should required to arrange

funds from different different lenders after analysing their capacity of repayment in future. Itts

main objective of preparing such budget is to ensure about sufficiency of funds while operating

business functions (Parker, 2012). Advantage: This budget provides the relevant information of cash inflow and cash

outflow with a motive of getting strong financial position. This will help managers to

manage the cash flow of company.

Disadvantage: It becomes difficult for manager to control cash outflow as the chances

of occurring wastage will be more.

Rolling budget: It is a kind of budget which is prepared in new form after revising financial

plans for the forthcoming accounting period replacing the old one in order to continue business

operation. Advantage: The assumption will be used to create revenue forecasting for an

organisation.

Disadvantage: It consumes more time in preparing budget as the financial data are

provided by the company.

Fixed budget: It is considered as an effective budget which cannot be change or modify during

sales or other activities either may increase or decrease at the same time. It doesn't allow to

change financial plan in order to execute business activities. Advantage: It is helpful in measuring growth and success of small business

organisation.

Disadvantage: It cannot able to adjust for other factors such as prices of raw material,

interest rates, degree of competition etc.

Flexible budget: It is such type of budget which can adjusted or modified with the changes

happened in business activities. It can be changes at any time if the manager identify the need

of change. Advantage: It is helpful in possible outcomes through making changes in budget on

time.

Disadvantage: It requires additional funds in executing business activities if the

manager found the need of adjustment. Thus, it increases cost of project activities.

10

Therefore, to operating business more smoothly the management should required to arrange

funds from different different lenders after analysing their capacity of repayment in future. Itts

main objective of preparing such budget is to ensure about sufficiency of funds while operating

business functions (Parker, 2012). Advantage: This budget provides the relevant information of cash inflow and cash

outflow with a motive of getting strong financial position. This will help managers to

manage the cash flow of company.

Disadvantage: It becomes difficult for manager to control cash outflow as the chances

of occurring wastage will be more.

Rolling budget: It is a kind of budget which is prepared in new form after revising financial

plans for the forthcoming accounting period replacing the old one in order to continue business

operation. Advantage: The assumption will be used to create revenue forecasting for an

organisation.

Disadvantage: It consumes more time in preparing budget as the financial data are

provided by the company.

Fixed budget: It is considered as an effective budget which cannot be change or modify during

sales or other activities either may increase or decrease at the same time. It doesn't allow to

change financial plan in order to execute business activities. Advantage: It is helpful in measuring growth and success of small business

organisation.

Disadvantage: It cannot able to adjust for other factors such as prices of raw material,

interest rates, degree of competition etc.

Flexible budget: It is such type of budget which can adjusted or modified with the changes

happened in business activities. It can be changes at any time if the manager identify the need

of change. Advantage: It is helpful in possible outcomes through making changes in budget on

time.

Disadvantage: It requires additional funds in executing business activities if the

manager found the need of adjustment. Thus, it increases cost of project activities.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.