Management Accounting Report: XLG Business and Variance Analysis

VerifiedAdded on 2023/01/09

|14

|3460

|98

Report

AI Summary

This report delves into the core principles of management accounting, focusing on variance analysis within the context of the XLG business case. It examines sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance, providing detailed calculations and interpretations. The report critically analyzes the merits and demerits of using variances to assess manager performance, discussing the advantages of identifying deviations from planned outcomes, controlling costs, and improving budget projections, alongside the disadvantages of delayed information and potential inaccuracies. Furthermore, the report explores the competitive advantages of FamaQ for XLG, considering the impact of increased demand and production costs. The report also acknowledges the assignment brief's requirement for a report format, which is reflected in the structured presentation of the analysis and findings. The conclusion summarizes the key insights and recommendations derived from the analysis, reinforcing the importance of variance analysis in managerial decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

1. Sales price variance and sales volume contribution variance...............................................................3

2. Material price planning variance and material price operational variance...........................................5

3. Critically analyzing key merits and demerits in relation to use of variances in assessing manager’s

performance:............................................................................................................................................7

PART B.......................................................................................................................................................10

1. FamaQ gives XLG competitive advantage........................................................................................10

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to market

research.................................................................................................................................................10

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15 working

days.......................................................................................................................................................11

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................13

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

1. Sales price variance and sales volume contribution variance...............................................................3

2. Material price planning variance and material price operational variance...........................................5

3. Critically analyzing key merits and demerits in relation to use of variances in assessing manager’s

performance:............................................................................................................................................7

PART B.......................................................................................................................................................10

1. FamaQ gives XLG competitive advantage........................................................................................10

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to market

research.................................................................................................................................................10

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15 working

days.......................................................................................................................................................11

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................13

INTRODUCTION

Managerial accounting is the method of establishing organizational objectives by defining,

evaluating, analyzing, presenting and transmitting guidance to stakeholders. Accounting

management reports on all accounts designed to remind managers of operating business

processes. This includes information related to the prices of the corporation's goods and services.

Budgeting is also used to measure organizational planning decisions (Agrawal and Cooper,

2017). Accounting firms in the administration use annual reviews to note differences from total

budget outcomes. The study deals with the key elements of managerial accounting required to

quantify the renewable growth of the event. The whole study is composed of 2 parts: A and B.

The first element covers realistic sums linked to various variability estimates are based on the

XLG Business case study. It also includes thorough assessment of the benefits and disadvantages

of incorporating variability in the examination of the results of time management. Whereas the

other component concerns risk, importation of Farma Q and how this can impact XLG Company

throughout lock-down based on the aforementioned study given can result.

PART A

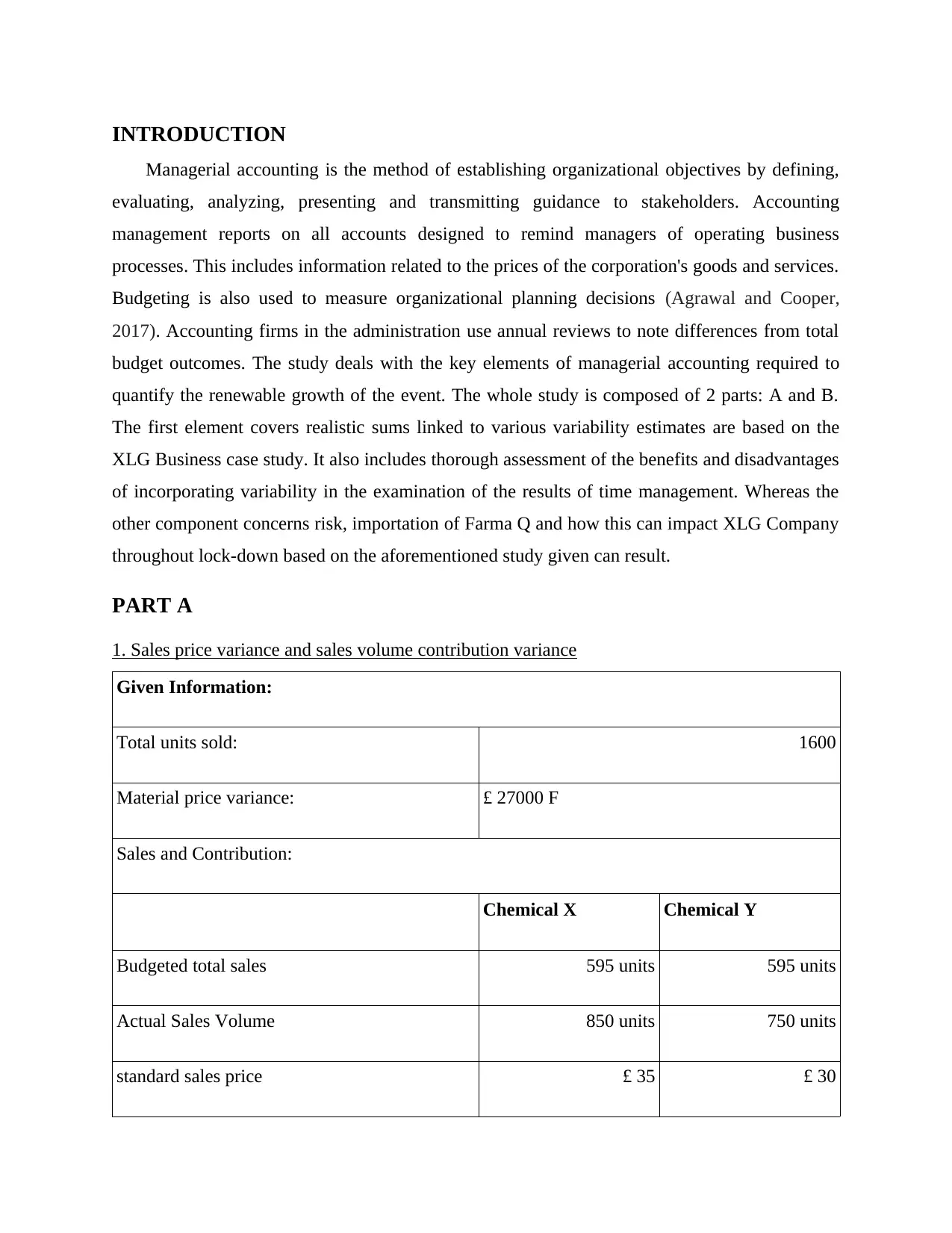

1. Sales price variance and sales volume contribution variance

Given Information:

Total units sold: 1600

Material price variance: £ 27000 F

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

standard sales price £ 35 £ 30

Managerial accounting is the method of establishing organizational objectives by defining,

evaluating, analyzing, presenting and transmitting guidance to stakeholders. Accounting

management reports on all accounts designed to remind managers of operating business

processes. This includes information related to the prices of the corporation's goods and services.

Budgeting is also used to measure organizational planning decisions (Agrawal and Cooper,

2017). Accounting firms in the administration use annual reviews to note differences from total

budget outcomes. The study deals with the key elements of managerial accounting required to

quantify the renewable growth of the event. The whole study is composed of 2 parts: A and B.

The first element covers realistic sums linked to various variability estimates are based on the

XLG Business case study. It also includes thorough assessment of the benefits and disadvantages

of incorporating variability in the examination of the results of time management. Whereas the

other component concerns risk, importation of Farma Q and how this can impact XLG Company

throughout lock-down based on the aforementioned study given can result.

PART A

1. Sales price variance and sales volume contribution variance

Given Information:

Total units sold: 1600

Material price variance: £ 27000 F

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

standard sales price £ 35 £ 30

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

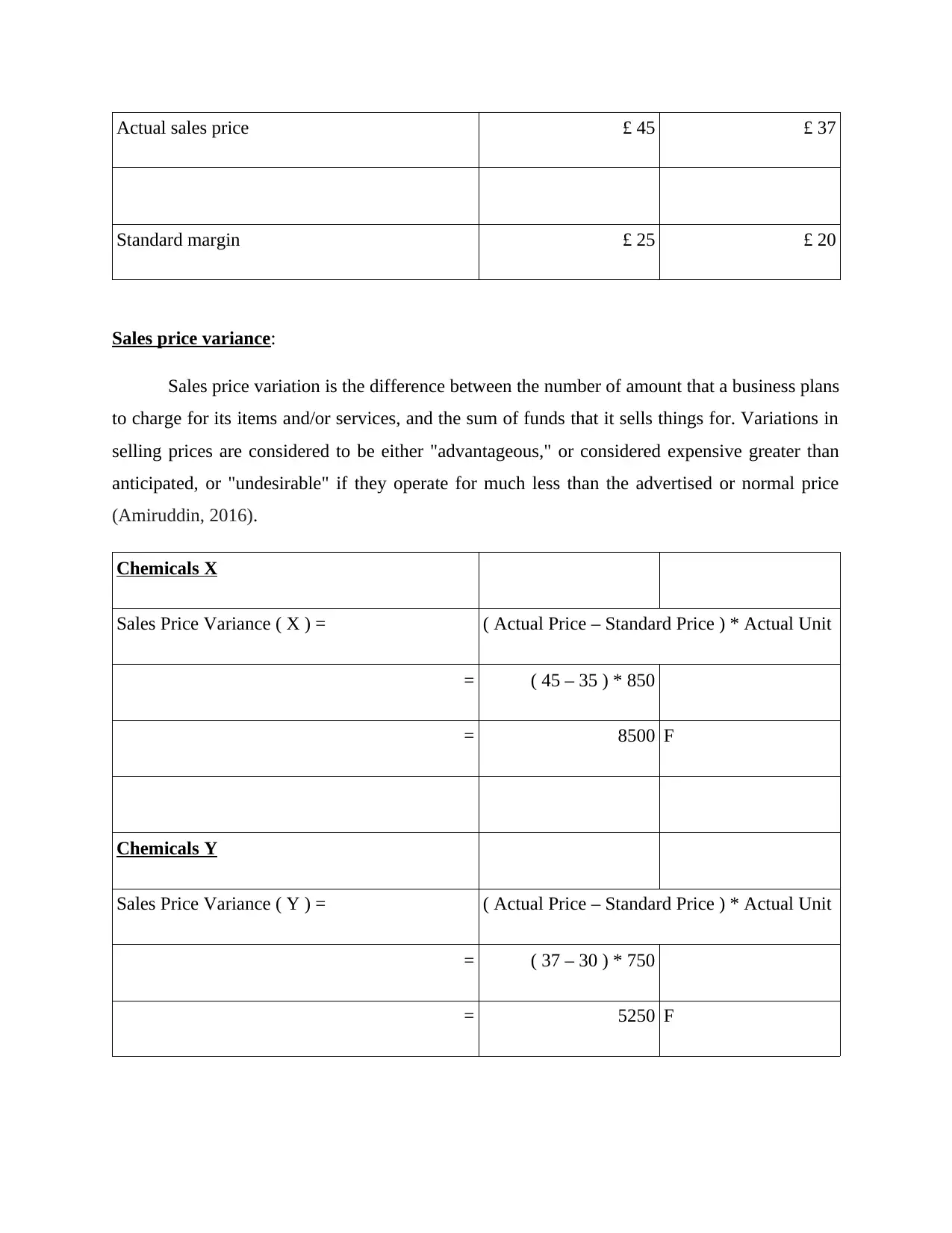

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

Sales price variance:

Sales price variation is the difference between the number of amount that a business plans

to charge for its items and/or services, and the sum of funds that it sells things for. Variations in

selling prices are considered to be either "advantageous," or considered expensive greater than

anticipated, or "undesirable" if they operate for much less than the advertised or normal price

(Amiruddin, 2016).

Chemicals X

Sales Price Variance ( X ) = ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850

= 8500 F

Chemicals Y

Sales Price Variance ( Y ) = ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750

= 5250 F

Standard margin £ 25 £ 20

Sales price variance:

Sales price variation is the difference between the number of amount that a business plans

to charge for its items and/or services, and the sum of funds that it sells things for. Variations in

selling prices are considered to be either "advantageous," or considered expensive greater than

anticipated, or "undesirable" if they operate for much less than the advertised or normal price

(Amiruddin, 2016).

Chemicals X

Sales Price Variance ( X ) = ( Actual Price – Standard Price ) * Actual Unit

= ( 45 – 35 ) * 850

= 8500 F

Chemicals Y

Sales Price Variance ( Y ) = ( Actual Price – Standard Price ) * Actual Unit

= ( 37 – 30 ) * 750

= 5250 F

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

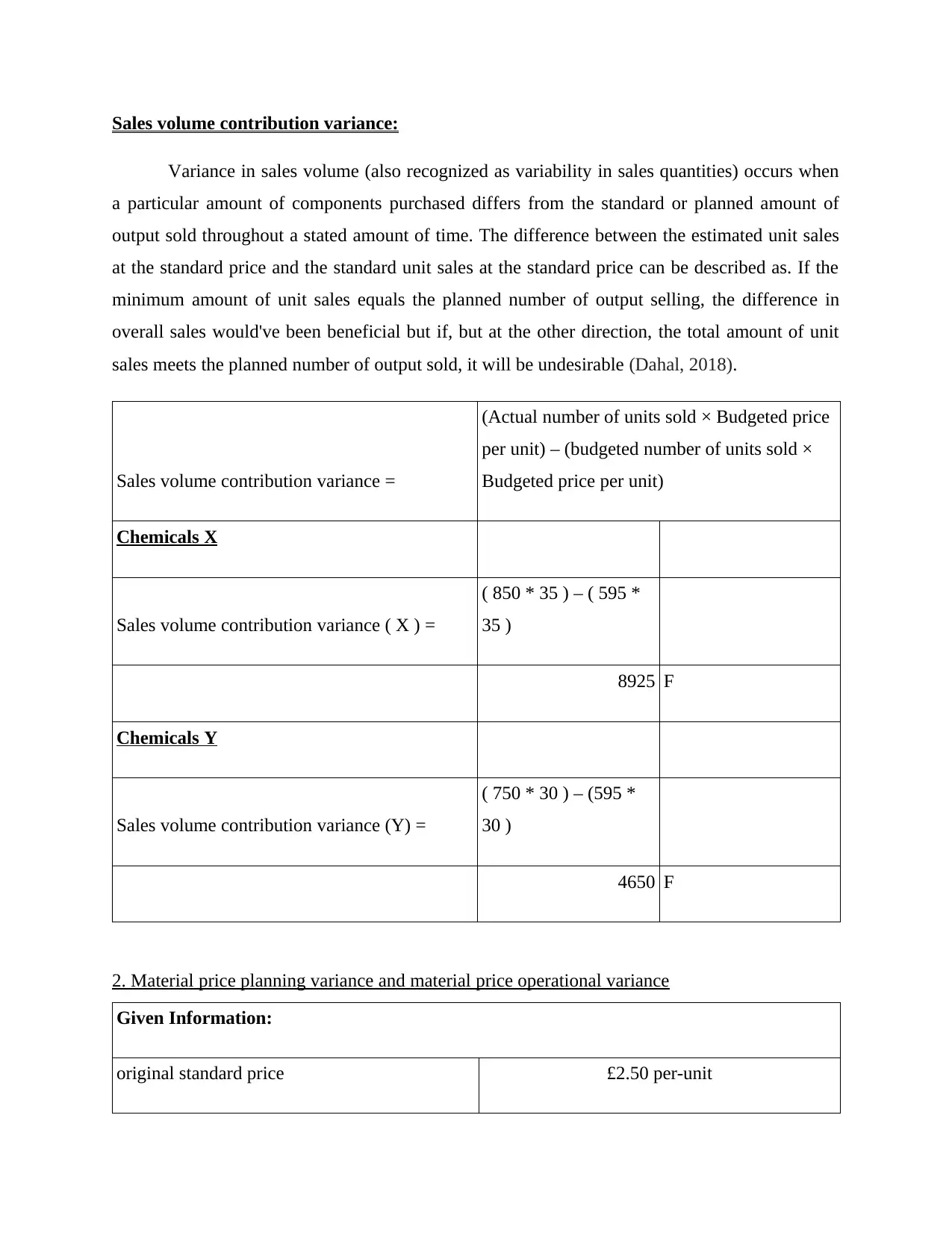

Sales volume contribution variance:

Variance in sales volume (also recognized as variability in sales quantities) occurs when

a particular amount of components purchased differs from the standard or planned amount of

output sold throughout a stated amount of time. The difference between the estimated unit sales

at the standard price and the standard unit sales at the standard price can be described as. If the

minimum amount of unit sales equals the planned number of output selling, the difference in

overall sales would've been beneficial but if, but at the other direction, the total amount of unit

sales meets the planned number of output sold, it will be undesirable (Dahal, 2018).

Sales volume contribution variance =

(Actual number of units sold × Budgeted price

per unit) – (budgeted number of units sold ×

Budgeted price per unit)

Chemicals X

Sales volume contribution variance ( X ) =

( 850 * 35 ) – ( 595 *

35 )

8925 F

Chemicals Y

Sales volume contribution variance (Y) =

( 750 * 30 ) – (595 *

30 )

4650 F

2. Material price planning variance and material price operational variance

Given Information:

original standard price £2.50 per-unit

Variance in sales volume (also recognized as variability in sales quantities) occurs when

a particular amount of components purchased differs from the standard or planned amount of

output sold throughout a stated amount of time. The difference between the estimated unit sales

at the standard price and the standard unit sales at the standard price can be described as. If the

minimum amount of unit sales equals the planned number of output selling, the difference in

overall sales would've been beneficial but if, but at the other direction, the total amount of unit

sales meets the planned number of output sold, it will be undesirable (Dahal, 2018).

Sales volume contribution variance =

(Actual number of units sold × Budgeted price

per unit) – (budgeted number of units sold ×

Budgeted price per unit)

Chemicals X

Sales volume contribution variance ( X ) =

( 850 * 35 ) – ( 595 *

35 )

8925 F

Chemicals Y

Sales volume contribution variance (Y) =

( 750 * 30 ) – (595 *

30 )

4650 F

2. Material price planning variance and material price operational variance

Given Information:

original standard price £2.50 per-unit

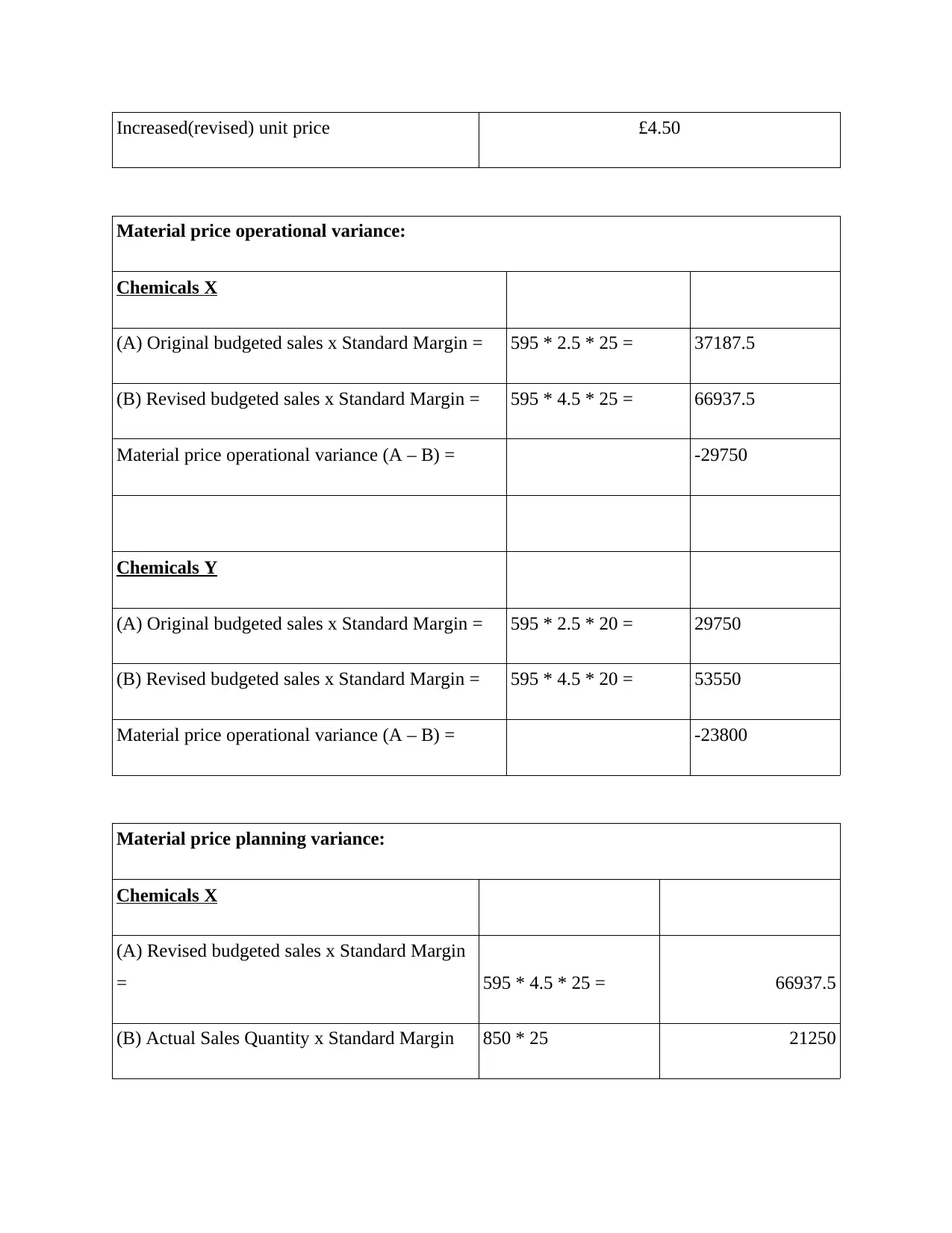

Increased(revised) unit price £4.50

Material price operational variance:

Chemicals X

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 25 = 37187.5

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 25 = 66937.5

Material price operational variance (A – B) = -29750

Chemicals Y

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 20 = 29750

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 20 = 53550

Material price operational variance (A – B) = -23800

Material price planning variance:

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 25 = 66937.5

(B) Actual Sales Quantity x Standard Margin 850 * 25 21250

Material price operational variance:

Chemicals X

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 25 = 37187.5

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 25 = 66937.5

Material price operational variance (A – B) = -29750

Chemicals Y

(A) Original budgeted sales x Standard Margin = 595 * 2.5 * 20 = 29750

(B) Revised budgeted sales x Standard Margin = 595 * 4.5 * 20 = 53550

Material price operational variance (A – B) = -23800

Material price planning variance:

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 25 = 66937.5

(B) Actual Sales Quantity x Standard Margin 850 * 25 21250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

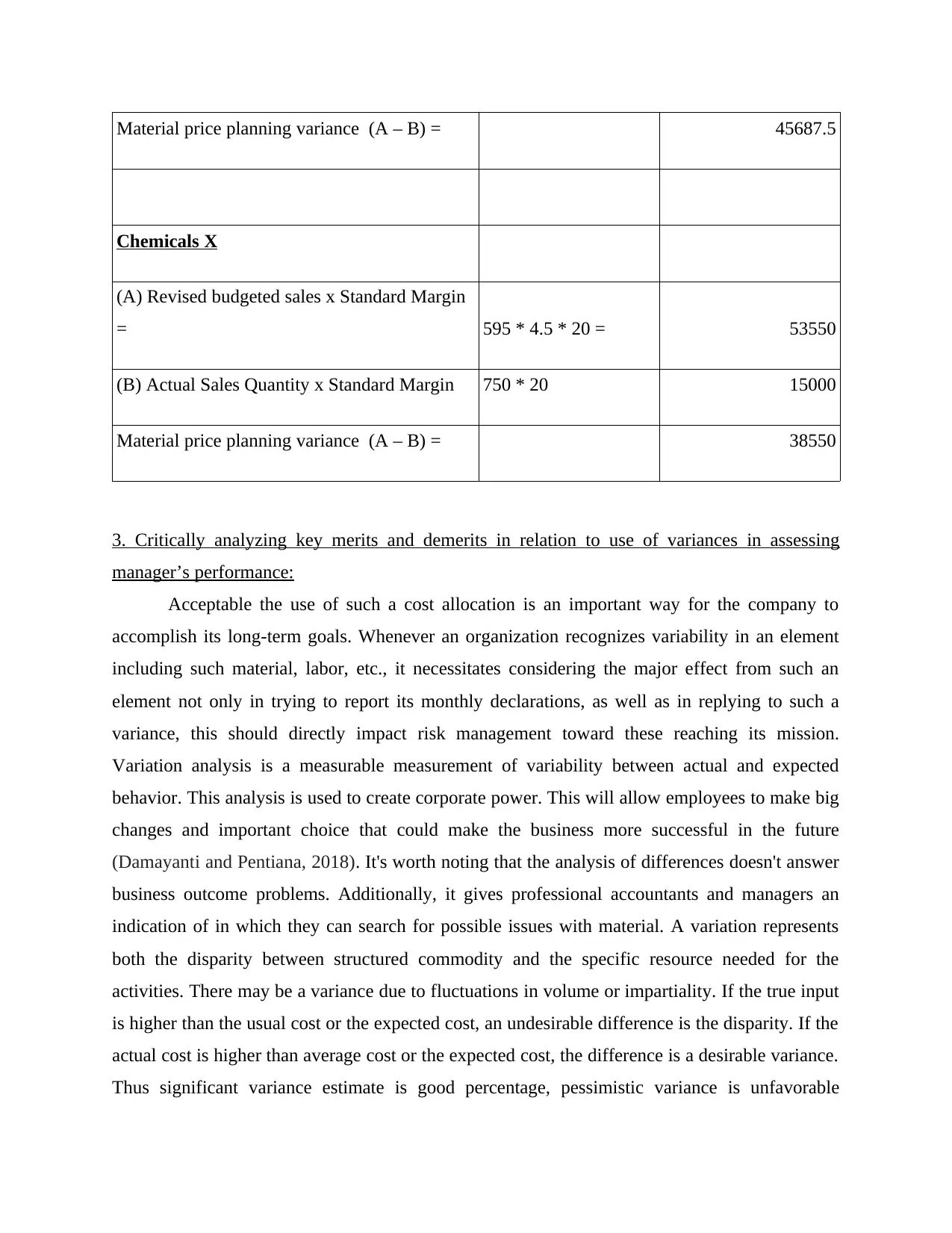

Material price planning variance (A – B) = 45687.5

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 20 = 53550

(B) Actual Sales Quantity x Standard Margin 750 * 20 15000

Material price planning variance (A – B) = 38550

3. Critically analyzing key merits and demerits in relation to use of variances in assessing

manager’s performance:

Acceptable the use of such a cost allocation is an important way for the company to

accomplish its long-term goals. Whenever an organization recognizes variability in an element

including such material, labor, etc., it necessitates considering the major effect from such an

element not only in trying to report its monthly declarations, as well as in replying to such a

variance, this should directly impact risk management toward these reaching its mission.

Variation analysis is a measurable measurement of variability between actual and expected

behavior. This analysis is used to create corporate power. This will allow employees to make big

changes and important choice that could make the business more successful in the future

(Damayanti and Pentiana, 2018). It's worth noting that the analysis of differences doesn't answer

business outcome problems. Additionally, it gives professional accountants and managers an

indication of in which they can search for possible issues with material. A variation represents

both the disparity between structured commodity and the specific resource needed for the

activities. There may be a variance due to fluctuations in volume or impartiality. If the true input

is higher than the usual cost or the expected cost, an undesirable difference is the disparity. If the

actual cost is higher than average cost or the expected cost, the difference is a desirable variance.

Thus significant variance estimate is good percentage, pessimistic variance is unfavorable

Chemicals X

(A) Revised budgeted sales x Standard Margin

= 595 * 4.5 * 20 = 53550

(B) Actual Sales Quantity x Standard Margin 750 * 20 15000

Material price planning variance (A – B) = 38550

3. Critically analyzing key merits and demerits in relation to use of variances in assessing

manager’s performance:

Acceptable the use of such a cost allocation is an important way for the company to

accomplish its long-term goals. Whenever an organization recognizes variability in an element

including such material, labor, etc., it necessitates considering the major effect from such an

element not only in trying to report its monthly declarations, as well as in replying to such a

variance, this should directly impact risk management toward these reaching its mission.

Variation analysis is a measurable measurement of variability between actual and expected

behavior. This analysis is used to create corporate power. This will allow employees to make big

changes and important choice that could make the business more successful in the future

(Damayanti and Pentiana, 2018). It's worth noting that the analysis of differences doesn't answer

business outcome problems. Additionally, it gives professional accountants and managers an

indication of in which they can search for possible issues with material. A variation represents

both the disparity between structured commodity and the specific resource needed for the

activities. There may be a variance due to fluctuations in volume or impartiality. If the true input

is higher than the usual cost or the expected cost, an undesirable difference is the disparity. If the

actual cost is higher than average cost or the expected cost, the difference is a desirable variance.

Thus significant variance estimate is good percentage, pessimistic variance is unfavorable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

variance. Variability interconnects with certain variances. Distinctions between variations,

whether negatively or positively, are important in strategic thinking (Datar and Rajan, 2018). A

detailed debate on the main benefits and demerit points of the use of differences in the evaluation

of organizational results follows in this respect:

Merits

• Verification of divergence from norm or planned seems to be the first value of the study of the

differences. Such arrival will start concentrating the evaluation on the management teams. The

relevant details for this withdrawal shall be given to the management, in particular for incorrect

decision (cost is beyond anticipated).

• The second benefit of the variation would be its value in spending controls. In case of adverse

variance management takes fair critically assess. When sufficient descriptions are not given and

reasonable control actions are implemented, rationale of an unfavorable variation is assessed in

first place (Egan and Tweedie, 2018).

• Future adjustment of budget projections is the third value of variance or variability

assessments. Unless, in addition to an incorrect budget estimate, there is no logical explanation

for uncertainty, the outlook for capacity should be updated or revised.

• The fourth value of this variation is to assess the output of the administrators and, in specific,

the supervisor controller. Favorable sign indicates stronger manger efficiency, whereas

unfavorable variance means poor performance.

• The fifth benefit of variance development is to examine a system of responsibilities and

functions inside the corporation. Defining obligations and roles improves the efficiency and

control mechanism in regard the organisation.

• The simulation of differences or the examination of differences creates an accountability

structure inside the firm. All are liable for the results of unfavorable variances (Eisenberg, 2016)

(Feger and Mermet, 2017).

• In some circumstances, budget vs. actual differences may suggest that the company's business

variety or directed consumer market needs to be reassessed. There's now a lot of exaggeration

whether negatively or positively, are important in strategic thinking (Datar and Rajan, 2018). A

detailed debate on the main benefits and demerit points of the use of differences in the evaluation

of organizational results follows in this respect:

Merits

• Verification of divergence from norm or planned seems to be the first value of the study of the

differences. Such arrival will start concentrating the evaluation on the management teams. The

relevant details for this withdrawal shall be given to the management, in particular for incorrect

decision (cost is beyond anticipated).

• The second benefit of the variation would be its value in spending controls. In case of adverse

variance management takes fair critically assess. When sufficient descriptions are not given and

reasonable control actions are implemented, rationale of an unfavorable variation is assessed in

first place (Egan and Tweedie, 2018).

• Future adjustment of budget projections is the third value of variance or variability

assessments. Unless, in addition to an incorrect budget estimate, there is no logical explanation

for uncertainty, the outlook for capacity should be updated or revised.

• The fourth value of this variation is to assess the output of the administrators and, in specific,

the supervisor controller. Favorable sign indicates stronger manger efficiency, whereas

unfavorable variance means poor performance.

• The fifth benefit of variance development is to examine a system of responsibilities and

functions inside the corporation. Defining obligations and roles improves the efficiency and

control mechanism in regard the organisation.

• The simulation of differences or the examination of differences creates an accountability

structure inside the firm. All are liable for the results of unfavorable variances (Eisenberg, 2016)

(Feger and Mermet, 2017).

• In some circumstances, budget vs. actual differences may suggest that the company's business

variety or directed consumer market needs to be reassessed. There's now a lot of exaggeration

regarding preparing a budget. If such assumptions contribute to expenditure blow-up, this could

be because the fundamental projections for a variety of variables are entirely inaccurate. This can

be as simple as an economic crisis or as complicated as issues when it comes to delivering goods

out again to customers. The necessary changes inside the business could be seen at the

conclusion from each day.

• Assists the company in achieving its strategic objectives and ensuring the effective utilization

of the capital of the organization. This also helps to create standards for the concerned parties. If

the multiple regression analysis presents a set of results that produce large differences in the

study, it may indicate there have been significant issues with the budget preparation. Problems

may lead to the use of inaccurate information or details, or software inaccurate data when used to

prepare either expenditure or a specific analysis reports that occur (Grabner, Posch and

Wabnegg, 2018). Variance evaluation is also a valuable way of checking the costing method of

the company. By making efforts to strengthen the financial planning system, the company needs

to get to be a lot more effective.

Demerits

• Accounting staff records discrepancies at the end of every season before sending the reports to

managers. Company needs information much faster for most circumstances so it chooses to

concentrate on automatic indications or on-site actions.

• Many variance / variance variables are not included in accounting records, and accounting

departments will study and evaluate information such as routing research, spending on supplies

and payroll records to examine the causes of such differences. This bring-on procedure is cost-

effective only if the supervisors have been able to solve the problems effectively on the grounds

of the data obtained.

• Where budgeting does not take place on the basis of a detailed analysis of each element, the

annual budget can be treated broadly, that may vary from the exact statistics. With such a

situation it cannot make much sense to evaluate differences (Kosov, Mashinistova, and

Kharakoz, 2016).

be because the fundamental projections for a variety of variables are entirely inaccurate. This can

be as simple as an economic crisis or as complicated as issues when it comes to delivering goods

out again to customers. The necessary changes inside the business could be seen at the

conclusion from each day.

• Assists the company in achieving its strategic objectives and ensuring the effective utilization

of the capital of the organization. This also helps to create standards for the concerned parties. If

the multiple regression analysis presents a set of results that produce large differences in the

study, it may indicate there have been significant issues with the budget preparation. Problems

may lead to the use of inaccurate information or details, or software inaccurate data when used to

prepare either expenditure or a specific analysis reports that occur (Grabner, Posch and

Wabnegg, 2018). Variance evaluation is also a valuable way of checking the costing method of

the company. By making efforts to strengthen the financial planning system, the company needs

to get to be a lot more effective.

Demerits

• Accounting staff records discrepancies at the end of every season before sending the reports to

managers. Company needs information much faster for most circumstances so it chooses to

concentrate on automatic indications or on-site actions.

• Many variance / variance variables are not included in accounting records, and accounting

departments will study and evaluate information such as routing research, spending on supplies

and payroll records to examine the causes of such differences. This bring-on procedure is cost-

effective only if the supervisors have been able to solve the problems effectively on the grounds

of the data obtained.

• Where budgeting does not take place on the basis of a detailed analysis of each element, the

annual budget can be treated broadly, that may vary from the exact statistics. With such a

situation it cannot make much sense to evaluate differences (Kosov, Mashinistova, and

Kharakoz, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• A variation study has a major drawback in that it takes far longer to evaluate the effect of the

variability and it may therefore prolong the corrective behavior. The monitoring method leads to

a considerable reduction in time-frame and thus will significantly hinder the implementation of

prevention measures.

PART B

1. FamaQ gives XLG competitive advantage

It is accurate that Fama Q provides the XLG company a competitive advantage as it is the

corporation's dominant cleaning agent and XLG takes protection to protect its UK dominant

market position from its rivals. For the Chemical X, the selling price difference is £8500 that is

in a favorable situation and for Chemical Y it is £5250 that is also in support. Chemical X and

Y's market volume output variation is £8925 and £4650 separately so both are in the XLG

Corporation’s favorable situation. From the other extreme, the commodity price operating

difference for the Chemical X is detrimental which again is -£29750 and for Chemical Y is -

£23800 which is also unfavorable as implies it is not advantageous to the companies and also

some competitive (Machado, 2016). Additionally, the difference in the commodity price

preparation is £45687.5 and £38550 accordingly for Chemical X and Y. XLG Company can

avoid sourcing from Brazil and instead concentrate on manufacturing through-house save the

shipping costs. XLG Business will concentrate on digital shopping because of the corona virus

that is distributed around the country.

Fama Q provides the XLG strong competitive edge, although in the lockdown cost per

share tends to increase to £4.50 and XLG has to pay Fama Q £3.70, which is becoming

expensive to them. Because of elevated air travel fees which also boost the sales price of

cleaning items, companies have to start shipping from Brazil. It has been established from the

prices of sales and commodity aspects that perhaps the importation of commodity through Brazil

by air transformation raises the average cost of every product.

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to

market research

Demand for Chemical X and Y is growing by 45 percent, so companies can start their

development according to consumer research that they require to avoid purchasing Brazilian

variability and it may therefore prolong the corrective behavior. The monitoring method leads to

a considerable reduction in time-frame and thus will significantly hinder the implementation of

prevention measures.

PART B

1. FamaQ gives XLG competitive advantage

It is accurate that Fama Q provides the XLG company a competitive advantage as it is the

corporation's dominant cleaning agent and XLG takes protection to protect its UK dominant

market position from its rivals. For the Chemical X, the selling price difference is £8500 that is

in a favorable situation and for Chemical Y it is £5250 that is also in support. Chemical X and

Y's market volume output variation is £8925 and £4650 separately so both are in the XLG

Corporation’s favorable situation. From the other extreme, the commodity price operating

difference for the Chemical X is detrimental which again is -£29750 and for Chemical Y is -

£23800 which is also unfavorable as implies it is not advantageous to the companies and also

some competitive (Machado, 2016). Additionally, the difference in the commodity price

preparation is £45687.5 and £38550 accordingly for Chemical X and Y. XLG Company can

avoid sourcing from Brazil and instead concentrate on manufacturing through-house save the

shipping costs. XLG Business will concentrate on digital shopping because of the corona virus

that is distributed around the country.

Fama Q provides the XLG strong competitive edge, although in the lockdown cost per

share tends to increase to £4.50 and XLG has to pay Fama Q £3.70, which is becoming

expensive to them. Because of elevated air travel fees which also boost the sales price of

cleaning items, companies have to start shipping from Brazil. It has been established from the

prices of sales and commodity aspects that perhaps the importation of commodity through Brazil

by air transformation raises the average cost of every product.

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to

market research

Demand for Chemical X and Y is growing by 45 percent, so companies can start their

development according to consumer research that they require to avoid purchasing Brazilian

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

goods. Due to the nature of a disease outbreak scenario in the country and worldwide, the

organisation and any individual of the nation who has to suffer is affected. Instructional process

cost of the product is £2.50 per product, however owing to this global epidemic circumstance it

will raise the product priced at £ 4.50 per item and as a consequence XLG Corporation will have

to pay £ 3.70 per department to Fama Q. It will reduce the production margin of the business that

is not advantageous caused by air transportation of massive value content (Rybicka, 2018). In

this case, in order to raise their selling price, they must avoid shipping stuff from Brazil and find

their replacement or manufacture themselves in the UK to reduce their costs. Since original

production price rises due to the increased shipping costs, this may reduce demand or decrease

the profitability for XLG Business as well.

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days

Manufacturing goods in the United Kingdom minimizes production costs as well as

reducing delivery schedule that is very significant in helping to attract more customers. Since

consumers favor certain products or companies that supply raw materials at minimal prices. If

industry receives lower costs by producing Fama Q products in the British otherwise businesses

have to maintain this cycle and avoid purchasing from Brazil before the scenario is usual.

XLG Corporation is already charging £3.70 to Fama Q and once they begin manufacturing

in the Kingdom they have £ 3 per product which takes 15 days fewer periods to manufacture

goods (Setiawan, Rahmawati and Widagdo, 2019). The fast turnaround choice falls under the

happiness of the consumer and their purchase process that boosts the image of the organisation

or actually increases their market opportunity. XLG Corporation wants to change its emphasis

and start producing goods in the UK because it minimizes costs by rising shipping and taxation

costs. Shipping goods from out of the UK often takes several workdays that may lead the

consumer to withdraw the request.

By evaluating all the facts and variables that contribute to further cost production and an

immediate rise in the appraised value, executives must define and make sound decisions that

they will implement with regard to the business in order to retain the sustainability and consumer

demand for goods & products in this disease outbreak situation. Lookdown satiations create

tremendous problems for the environment where corporate sustainability is very challenging;

organisation and any individual of the nation who has to suffer is affected. Instructional process

cost of the product is £2.50 per product, however owing to this global epidemic circumstance it

will raise the product priced at £ 4.50 per item and as a consequence XLG Corporation will have

to pay £ 3.70 per department to Fama Q. It will reduce the production margin of the business that

is not advantageous caused by air transportation of massive value content (Rybicka, 2018). In

this case, in order to raise their selling price, they must avoid shipping stuff from Brazil and find

their replacement or manufacture themselves in the UK to reduce their costs. Since original

production price rises due to the increased shipping costs, this may reduce demand or decrease

the profitability for XLG Business as well.

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days

Manufacturing goods in the United Kingdom minimizes production costs as well as

reducing delivery schedule that is very significant in helping to attract more customers. Since

consumers favor certain products or companies that supply raw materials at minimal prices. If

industry receives lower costs by producing Fama Q products in the British otherwise businesses

have to maintain this cycle and avoid purchasing from Brazil before the scenario is usual.

XLG Corporation is already charging £3.70 to Fama Q and once they begin manufacturing

in the Kingdom they have £ 3 per product which takes 15 days fewer periods to manufacture

goods (Setiawan, Rahmawati and Widagdo, 2019). The fast turnaround choice falls under the

happiness of the consumer and their purchase process that boosts the image of the organisation

or actually increases their market opportunity. XLG Corporation wants to change its emphasis

and start producing goods in the UK because it minimizes costs by rising shipping and taxation

costs. Shipping goods from out of the UK often takes several workdays that may lead the

consumer to withdraw the request.

By evaluating all the facts and variables that contribute to further cost production and an

immediate rise in the appraised value, executives must define and make sound decisions that

they will implement with regard to the business in order to retain the sustainability and consumer

demand for goods & products in this disease outbreak situation. Lookdown satiations create

tremendous problems for the environment where corporate sustainability is very challenging;

citizens strive to maintain their employment secure and income producing companies. In this

tough position, it is the institution's best chance to preserve its competitiveness (van Helden,

2019) (Vetrov, Vandina and Galustov, 2017).

CONCLUSION

It has been ascertained from the current conversation that business environment generates so

many problems and also difficulties that also support the growth and profit of the organization.

Utilizing management accounting notions, managers need to make informed business decisions

according to the present situation that the organization is facing. Responsible for setting the

productivity conditions in company activities by recognizing revenue and inventory variances,

and often evaluate what behaviour is in favour in output or not. Each company is affected in the

lockout circumstances, so it is easier to consider the circumstances and find potential ways to

escape from this tough position.

tough position, it is the institution's best chance to preserve its competitiveness (van Helden,

2019) (Vetrov, Vandina and Galustov, 2017).

CONCLUSION

It has been ascertained from the current conversation that business environment generates so

many problems and also difficulties that also support the growth and profit of the organization.

Utilizing management accounting notions, managers need to make informed business decisions

according to the present situation that the organization is facing. Responsible for setting the

productivity conditions in company activities by recognizing revenue and inventory variances,

and often evaluate what behaviour is in favour in output or not. Each company is affected in the

lockout circumstances, so it is easier to consider the circumstances and find potential ways to

escape from this tough position.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.