Management Accounting Report: Financial Analysis and Costing Methods

VerifiedAdded on 2020/06/03

|15

|4879

|88

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices, focusing on the case of TECH IMDA Ltd. It explores various types of management accounting, including cost accounting and inventory management, and their effectiveness in recording financial transactions. The report delves into different reporting systems like performance reports and job cost reports, emphasizing their role in analyzing and communicating financial data. Furthermore, it examines various costing methods such as cost-volume-profit analysis and flexible budgeting, used for calculating net profit and interpreting data for business activities. The report also discusses the advantages and disadvantages of using planning tools in budgeting and the utilization of planning tools to overcome financial issues. Finally, it touches upon the balance scorecard and its effective use in resolving financial problems, offering a critical analysis of financial performance and providing insights into effective business management. This report provides a detailed analysis of accounting principles and practices, offering valuable insights for students.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Different types of management accounting and its effectiveness....................................1

P2: Different types of reporting systems................................................................................3

M1: Benefits of using accounting system..............................................................................4

D1: Critical evaluation of reporting system...........................................................................4

TASK 3............................................................................................................................................5

P3: Various types of costing methods use for calculating net profit......................................5

M2: Use of various techniques...............................................................................................9

D2: Interpretation of data for the business activities..............................................................9

TASK 3............................................................................................................................................9

P4: Advantage and disadvantage of using planning tools in budget......................................9

M3: Utilisation and analysis of planning tools.....................................................................11

D3: Critical analysis to overcomes financial issues.............................................................11

TASK 4..........................................................................................................................................11

P5: Balance scorecard and their effective use to resolve financial issues............................11

M4: Evaluation of different financial problems...................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Different types of management accounting and its effectiveness....................................1

P2: Different types of reporting systems................................................................................3

M1: Benefits of using accounting system..............................................................................4

D1: Critical evaluation of reporting system...........................................................................4

TASK 3............................................................................................................................................5

P3: Various types of costing methods use for calculating net profit......................................5

M2: Use of various techniques...............................................................................................9

D2: Interpretation of data for the business activities..............................................................9

TASK 3............................................................................................................................................9

P4: Advantage and disadvantage of using planning tools in budget......................................9

M3: Utilisation and analysis of planning tools.....................................................................11

D3: Critical analysis to overcomes financial issues.............................................................11

TASK 4..........................................................................................................................................11

P5: Balance scorecard and their effective use to resolve financial issues............................11

M4: Evaluation of different financial problems...................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

In recent time, different types of business organisation are using effective management

accounting systems that can assists in recoding financial transaction in their respective

statements. The primary aims of doing so is to attain maximum profit by utilising resources in

more effective manner. By the help of this management can attain their long and short term goals

in more quick time. As mentioned in the case about TECH IMDA Ltd which is dealing

electronic mobile and charges so they need to manage their everyday transaction through using

various system (Gates, Nicolas and Walker, 2012).

Those are being discussed under this report. Such as accounting and reporting systems.

Other than this, certain costing methods are also being illustrated to determine net profitability of

the company. Further, these reports analyse various planning tools use in budget preparation and

those financial issues those are affecting profitability of an organisation. It also covers some

effective measures that can assists in resolving those financial issues that are present in an

organisation

TASK 1

P1: Different types of management accounting and its effectiveness

This seems to be determine that every part of department that are working for the purpose of

increase maximum gain in short span of time. In order to reach at that position, they are using

various aspects which are related with management accounting. It has been seen that

management of every business organisation is always in search of identifying all those effective

ways those are essential for enhancing productivity of “Tech Imda Ltd”. Although this happens

to be important functions of every small and large business organisation in order to make

effective plan, organise and analyse their future needs and wants. While, accounting is a

systematic detail process of summarising, recording and evaluating various transactions those are

essential for the generating maximum earning during the time (Suomala and Lyly-Yrjänäinen,

2012).

Management accounting is said to be crucial profession that included partnering in

effective decision making, devising planning and deliver expertise in proper financial reporting.

This is utmost techniques of evaluating overall business costs and operations to make proper

accounting of reports, records and assist managers to take important decision in near future. This

1

In recent time, different types of business organisation are using effective management

accounting systems that can assists in recoding financial transaction in their respective

statements. The primary aims of doing so is to attain maximum profit by utilising resources in

more effective manner. By the help of this management can attain their long and short term goals

in more quick time. As mentioned in the case about TECH IMDA Ltd which is dealing

electronic mobile and charges so they need to manage their everyday transaction through using

various system (Gates, Nicolas and Walker, 2012).

Those are being discussed under this report. Such as accounting and reporting systems.

Other than this, certain costing methods are also being illustrated to determine net profitability of

the company. Further, these reports analyse various planning tools use in budget preparation and

those financial issues those are affecting profitability of an organisation. It also covers some

effective measures that can assists in resolving those financial issues that are present in an

organisation

TASK 1

P1: Different types of management accounting and its effectiveness

This seems to be determine that every part of department that are working for the purpose of

increase maximum gain in short span of time. In order to reach at that position, they are using

various aspects which are related with management accounting. It has been seen that

management of every business organisation is always in search of identifying all those effective

ways those are essential for enhancing productivity of “Tech Imda Ltd”. Although this happens

to be important functions of every small and large business organisation in order to make

effective plan, organise and analyse their future needs and wants. While, accounting is a

systematic detail process of summarising, recording and evaluating various transactions those are

essential for the generating maximum earning during the time (Suomala and Lyly-Yrjänäinen,

2012).

Management accounting is said to be crucial profession that included partnering in

effective decision making, devising planning and deliver expertise in proper financial reporting.

This is utmost techniques of evaluating overall business costs and operations to make proper

accounting of reports, records and assist managers to take important decision in near future. This

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

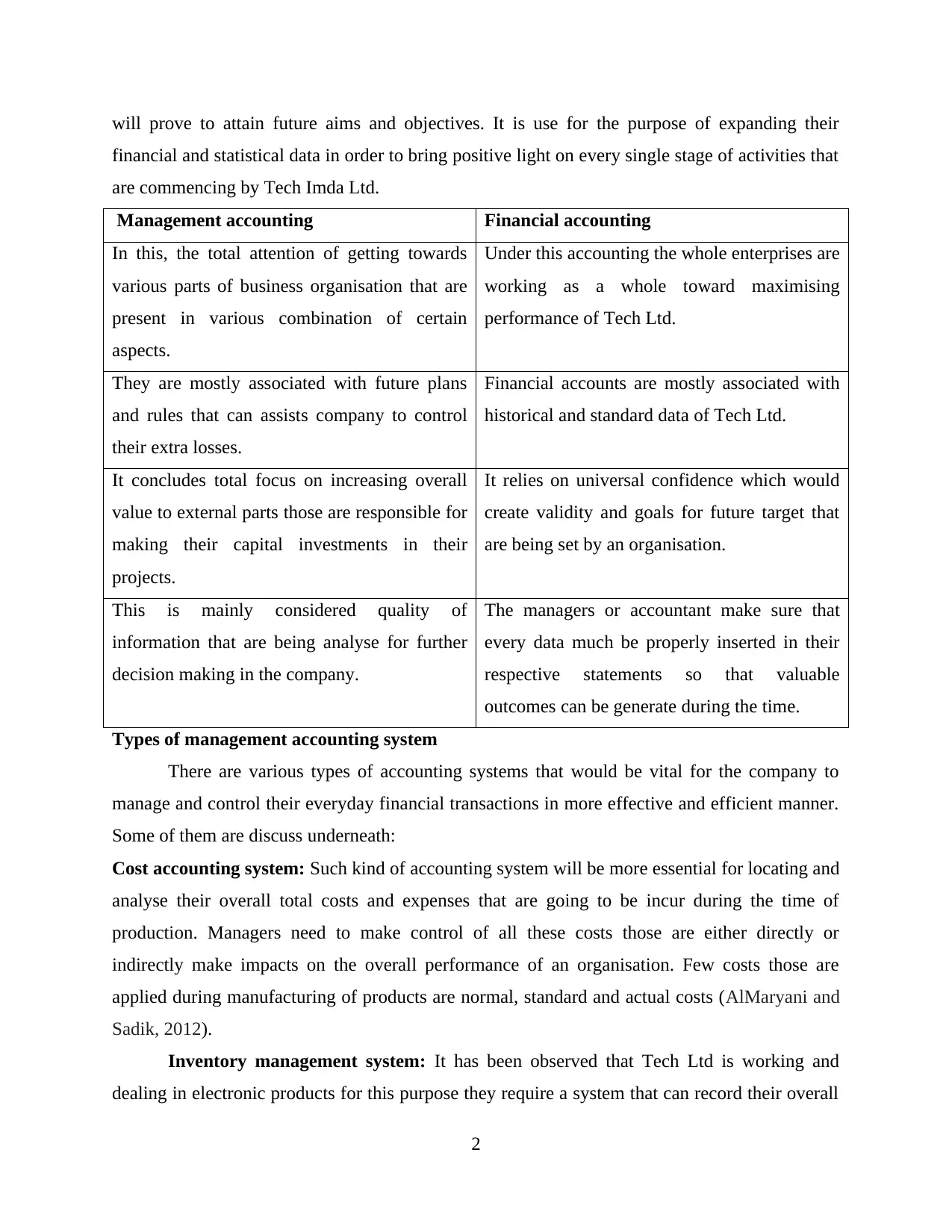

will prove to attain future aims and objectives. It is use for the purpose of expanding their

financial and statistical data in order to bring positive light on every single stage of activities that

are commencing by Tech Imda Ltd.

Management accounting Financial accounting

In this, the total attention of getting towards

various parts of business organisation that are

present in various combination of certain

aspects.

Under this accounting the whole enterprises are

working as a whole toward maximising

performance of Tech Ltd.

They are mostly associated with future plans

and rules that can assists company to control

their extra losses.

Financial accounts are mostly associated with

historical and standard data of Tech Ltd.

It concludes total focus on increasing overall

value to external parts those are responsible for

making their capital investments in their

projects.

It relies on universal confidence which would

create validity and goals for future target that

are being set by an organisation.

This is mainly considered quality of

information that are being analyse for further

decision making in the company.

The managers or accountant make sure that

every data much be properly inserted in their

respective statements so that valuable

outcomes can be generate during the time.

Types of management accounting system

There are various types of accounting systems that would be vital for the company to

manage and control their everyday financial transactions in more effective and efficient manner.

Some of them are discuss underneath:

Cost accounting system: Such kind of accounting system will be more essential for locating and

analyse their overall total costs and expenses that are going to be incur during the time of

production. Managers need to make control of all these costs those are either directly or

indirectly make impacts on the overall performance of an organisation. Few costs those are

applied during manufacturing of products are normal, standard and actual costs (AlMaryani and

Sadik, 2012).

Inventory management system: It has been observed that Tech Ltd is working and

dealing in electronic products for this purpose they require a system that can record their overall

2

financial and statistical data in order to bring positive light on every single stage of activities that

are commencing by Tech Imda Ltd.

Management accounting Financial accounting

In this, the total attention of getting towards

various parts of business organisation that are

present in various combination of certain

aspects.

Under this accounting the whole enterprises are

working as a whole toward maximising

performance of Tech Ltd.

They are mostly associated with future plans

and rules that can assists company to control

their extra losses.

Financial accounts are mostly associated with

historical and standard data of Tech Ltd.

It concludes total focus on increasing overall

value to external parts those are responsible for

making their capital investments in their

projects.

It relies on universal confidence which would

create validity and goals for future target that

are being set by an organisation.

This is mainly considered quality of

information that are being analyse for further

decision making in the company.

The managers or accountant make sure that

every data much be properly inserted in their

respective statements so that valuable

outcomes can be generate during the time.

Types of management accounting system

There are various types of accounting systems that would be vital for the company to

manage and control their everyday financial transactions in more effective and efficient manner.

Some of them are discuss underneath:

Cost accounting system: Such kind of accounting system will be more essential for locating and

analyse their overall total costs and expenses that are going to be incur during the time of

production. Managers need to make control of all these costs those are either directly or

indirectly make impacts on the overall performance of an organisation. Few costs those are

applied during manufacturing of products are normal, standard and actual costs (AlMaryani and

Sadik, 2012).

Inventory management system: It has been observed that Tech Ltd is working and

dealing in electronic products for this purpose they require a system that can record their overall

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production detail of raw materials. By the help of this, managers can easily make analysis of all

those costs are helpful in keeping their overall bills, record of invoice other warehouses.

Job costing system: This accounting system is more effective systems which will be

utilised to measure total allotted products costs to a single products and team group. Basically,

this could be more crucial in order to manufacture goods in more effectively different from one

another.

Price optimisation: This would guide accounting system which will be identifying

different types of customer’s perceptions about various prices of products that are being set by an

organisation. It would be assists them in order to determine price set which will useful in

increase their operation costs of manufacturing.

Benefits of using accounting system

All those above mentioned accounting systems are providing more crucial outcomes for

the company by offering maximum chances of increase their profit as well as efficiency at the

same time (Mistry, Sharma and Low, 2014).

P2: Different types of reporting systems

In every manufacturing business whether operating as small or large scale need to prepare

a well structure report out of their overall performance from the entire year. For this purpose,

they are using various types of accounting systems reporting. The primary motive of using such

kind of reports is to analyse, record, communicate and make proper evaluation of the collected

data from various departments. There are various vital sources from which accounting data can

be gathered. Some of them are taken from internal as well as few of them are taken from

external. These sources would provide valuable information about the current and past year

financial position of the company (Evans, Burritt and Guthrie, 2013). On this basis, investors

could make their various capital investment decisions in order to gain maximum advantage over

other companies. There are various types of accounting reports that are helpful in recording

crucial financial information in their respective set format. There are various types of accounting

system reports which are helpful in recording financial transactions. Some of them are discuss

underneath:

Performance report: According to this specific report, overall performance and financial

condition of the company can be easily identified. This can be prepared by using past and

current year data for the purpose of making actual and standard financial position of the

3

those costs are helpful in keeping their overall bills, record of invoice other warehouses.

Job costing system: This accounting system is more effective systems which will be

utilised to measure total allotted products costs to a single products and team group. Basically,

this could be more crucial in order to manufacture goods in more effectively different from one

another.

Price optimisation: This would guide accounting system which will be identifying

different types of customer’s perceptions about various prices of products that are being set by an

organisation. It would be assists them in order to determine price set which will useful in

increase their operation costs of manufacturing.

Benefits of using accounting system

All those above mentioned accounting systems are providing more crucial outcomes for

the company by offering maximum chances of increase their profit as well as efficiency at the

same time (Mistry, Sharma and Low, 2014).

P2: Different types of reporting systems

In every manufacturing business whether operating as small or large scale need to prepare

a well structure report out of their overall performance from the entire year. For this purpose,

they are using various types of accounting systems reporting. The primary motive of using such

kind of reports is to analyse, record, communicate and make proper evaluation of the collected

data from various departments. There are various vital sources from which accounting data can

be gathered. Some of them are taken from internal as well as few of them are taken from

external. These sources would provide valuable information about the current and past year

financial position of the company (Evans, Burritt and Guthrie, 2013). On this basis, investors

could make their various capital investment decisions in order to gain maximum advantage over

other companies. There are various types of accounting reports that are helpful in recording

crucial financial information in their respective set format. There are various types of accounting

system reports which are helpful in recording financial transactions. Some of them are discuss

underneath:

Performance report: According to this specific report, overall performance and financial

condition of the company can be easily identified. This can be prepared by using past and

current year data for the purpose of making actual and standard financial position of the

3

company. In order to determine any critical issues some crucial techniques such as Key

performance indicators would be more reliable.

Account receivable report: This kind of reports is more vital for making analysis of total

lists of unpaid customer’s invoices and credits amounts. Through this, company can easily be

able to make essential evaluation of credit amount recovery those are being due from so many

times (Van der Stede, 2015).

Inventory management report: It has been determined that plenty of useful information

are associated with companies stock positions are easily be analyse by using various techniques.

Some of them inventory turnover ratios by which total rotation of inventories can be examined.

ABC costing and EOQ is valuable techniques of making proper analysis opening and closing

stock during the time are recorded as per their mentioned data of occurrence.

Operational budgets: Such kind of reports includes various information regarding their

overall cost and expenses those are being invested for the production of one unit of products and

services. This would be summarising by analysing, sales, production and other raw material

budgets in an accounting period of time.

Job cost report: According to this specific reports production department in order to determine

total cost that are going to be utilised during manufacturing of products and services. With this

Tech Imda Ltd can manage and control their everyday costs and extra expenses those increase

burden on the company (Sisaye and Birnberg, 2012).

M1: Benefits of using accounting system

As per the above mentioned various accounting systems those are helpful for the company

in order to planning for controlling their daily operations. It has been found that all of them are

having their own benefits and limitations. Use of inventory management system can provide safe

and security to their stock for longer period of time. Whereas, job costing and cost accounting

are two of the main systems by the help of this company can increase their productivity and

growth in more quick time. Moreover, this can lead to increase efficiency and future growth for

the company in very limited period of time.

D1: Critical evaluation of reporting system

To generate more specific outcomes in an accounting period by using limited resources of

the company they need to make use of various recording techniques. It is necessary to make use

of various accounting system reporting which will be helpful in recoding various financial

4

performance indicators would be more reliable.

Account receivable report: This kind of reports is more vital for making analysis of total

lists of unpaid customer’s invoices and credits amounts. Through this, company can easily be

able to make essential evaluation of credit amount recovery those are being due from so many

times (Van der Stede, 2015).

Inventory management report: It has been determined that plenty of useful information

are associated with companies stock positions are easily be analyse by using various techniques.

Some of them inventory turnover ratios by which total rotation of inventories can be examined.

ABC costing and EOQ is valuable techniques of making proper analysis opening and closing

stock during the time are recorded as per their mentioned data of occurrence.

Operational budgets: Such kind of reports includes various information regarding their

overall cost and expenses those are being invested for the production of one unit of products and

services. This would be summarising by analysing, sales, production and other raw material

budgets in an accounting period of time.

Job cost report: According to this specific reports production department in order to determine

total cost that are going to be utilised during manufacturing of products and services. With this

Tech Imda Ltd can manage and control their everyday costs and extra expenses those increase

burden on the company (Sisaye and Birnberg, 2012).

M1: Benefits of using accounting system

As per the above mentioned various accounting systems those are helpful for the company

in order to planning for controlling their daily operations. It has been found that all of them are

having their own benefits and limitations. Use of inventory management system can provide safe

and security to their stock for longer period of time. Whereas, job costing and cost accounting

are two of the main systems by the help of this company can increase their productivity and

growth in more quick time. Moreover, this can lead to increase efficiency and future growth for

the company in very limited period of time.

D1: Critical evaluation of reporting system

To generate more specific outcomes in an accounting period by using limited resources of

the company they need to make use of various recording techniques. It is necessary to make use

of various accounting system reporting which will be helpful in recoding various financial

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information in appropriate manner. By the help of all those reports which are made by taking

information from each department can assists investors to make their necessary capital

investment decision under their projects. Some crucial techniques are inventory management

reports which are more reliable sources to record stock information in more systematic manner.

TASK 3

P3: Various types of costing methods use for calculating net profit

In every business organisation costs is utmost important aspects that can increase of

decrease their percentage of growth and performance at the same point of time. These costs are

either directly or indirectly associated with the production of products and services. As costs is

said to be value of money invested by Tech Imda Ltd in accordance to get something in return.

Normal, standard and actual are few costs those are been keen to be determined by the company

before taking any other decision (Moser, 2012). There are various types of costs use as

microeconomic techniques in the manufacturing process. Some of them are discuss underneath:

Cost volume profit (CVP): This technique is mainly used to determine total changes in

costs and volume that affects a company's operating income and their total earning. In

order to perform these types of analysis, there is various assumption which are needed to

be taken into consideration such as sales price per units is to be remain constant.

Flexible budgeting: Such kind of budgets would be adjusted or flexes for making

alternation in total volume of mentioned activity. This budget is more reliable and useful

than a static budget which would be remains at one individual amount of entire capacity

of an activity (Archives, 2018).

Cost variances: It is known as total difference among actual costs value and its estimated

budgeted value. Company uses this cost variances to make use to data analysis and track

their ongoing work (Cost variance, 2018).

Cost of inventory: This consists of all those costs which are related with holding or

storing stock for sales. This would be considered as opportunities cost of total money

utilised during the time of production.

Types of inventory cost:

Holding or carrying cost

Ordering cost

5

information from each department can assists investors to make their necessary capital

investment decision under their projects. Some crucial techniques are inventory management

reports which are more reliable sources to record stock information in more systematic manner.

TASK 3

P3: Various types of costing methods use for calculating net profit

In every business organisation costs is utmost important aspects that can increase of

decrease their percentage of growth and performance at the same point of time. These costs are

either directly or indirectly associated with the production of products and services. As costs is

said to be value of money invested by Tech Imda Ltd in accordance to get something in return.

Normal, standard and actual are few costs those are been keen to be determined by the company

before taking any other decision (Moser, 2012). There are various types of costs use as

microeconomic techniques in the manufacturing process. Some of them are discuss underneath:

Cost volume profit (CVP): This technique is mainly used to determine total changes in

costs and volume that affects a company's operating income and their total earning. In

order to perform these types of analysis, there is various assumption which are needed to

be taken into consideration such as sales price per units is to be remain constant.

Flexible budgeting: Such kind of budgets would be adjusted or flexes for making

alternation in total volume of mentioned activity. This budget is more reliable and useful

than a static budget which would be remains at one individual amount of entire capacity

of an activity (Archives, 2018).

Cost variances: It is known as total difference among actual costs value and its estimated

budgeted value. Company uses this cost variances to make use to data analysis and track

their ongoing work (Cost variance, 2018).

Cost of inventory: This consists of all those costs which are related with holding or

storing stock for sales. This would be considered as opportunities cost of total money

utilised during the time of production.

Types of inventory cost:

Holding or carrying cost

Ordering cost

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stock out cost.

Benefits of reducing inventory cost:

It would help in spending less income on material frees up costs for other uses. It will

control and overcome shopping expense, lower insurances and so on.

Price competitive is other important benefits that can individual would get from using

correct inventory control system.

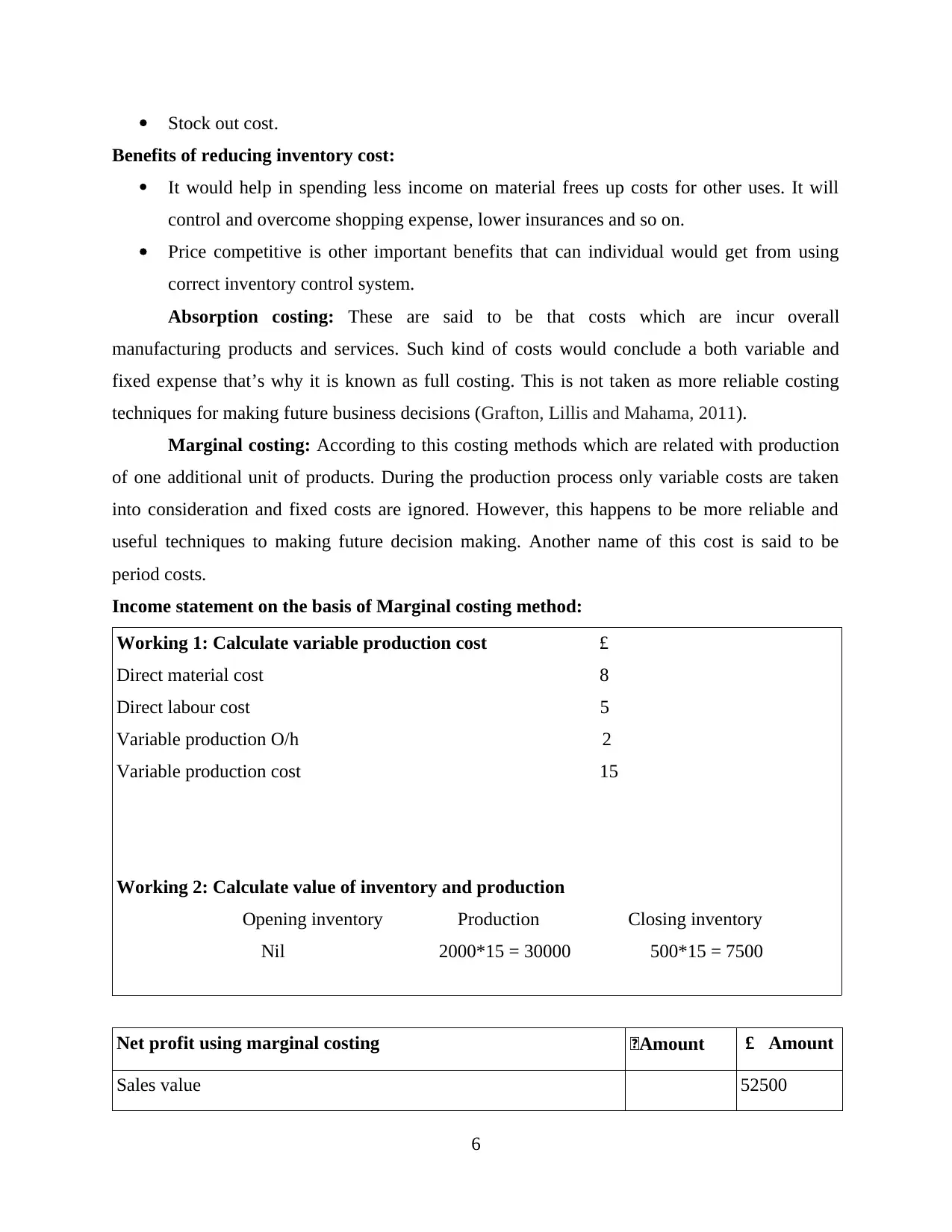

Absorption costing: These are said to be that costs which are incur overall

manufacturing products and services. Such kind of costs would conclude a both variable and

fixed expense that’s why it is known as full costing. This is not taken as more reliable costing

techniques for making future business decisions (Grafton, Lillis and Mahama, 2011).

Marginal costing: According to this costing methods which are related with production

of one additional unit of products. During the production process only variable costs are taken

into consideration and fixed costs are ignored. However, this happens to be more reliable and

useful techniques to making future decision making. Another name of this cost is said to be

period costs.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value 52500

6

Benefits of reducing inventory cost:

It would help in spending less income on material frees up costs for other uses. It will

control and overcome shopping expense, lower insurances and so on.

Price competitive is other important benefits that can individual would get from using

correct inventory control system.

Absorption costing: These are said to be that costs which are incur overall

manufacturing products and services. Such kind of costs would conclude a both variable and

fixed expense that’s why it is known as full costing. This is not taken as more reliable costing

techniques for making future business decisions (Grafton, Lillis and Mahama, 2011).

Marginal costing: According to this costing methods which are related with production

of one additional unit of products. During the production process only variable costs are taken

into consideration and fixed costs are ignored. However, this happens to be more reliable and

useful techniques to making future decision making. Another name of this cost is said to be

period costs.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value 52500

6

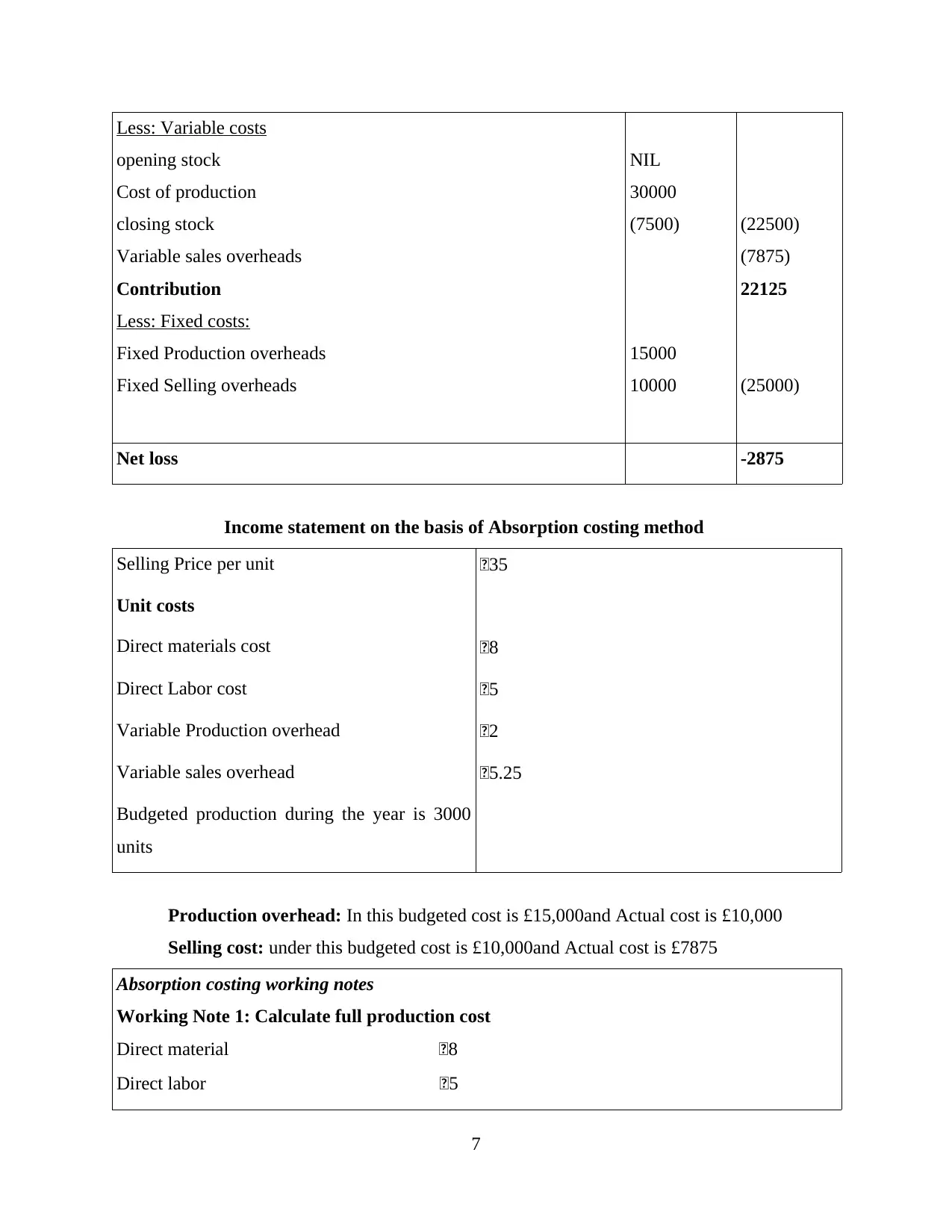

Less: Variable costs

opening stock

Cost of production

closing stock

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labor cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labor £5

7

opening stock

Cost of production

closing stock

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labor cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labor £5

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

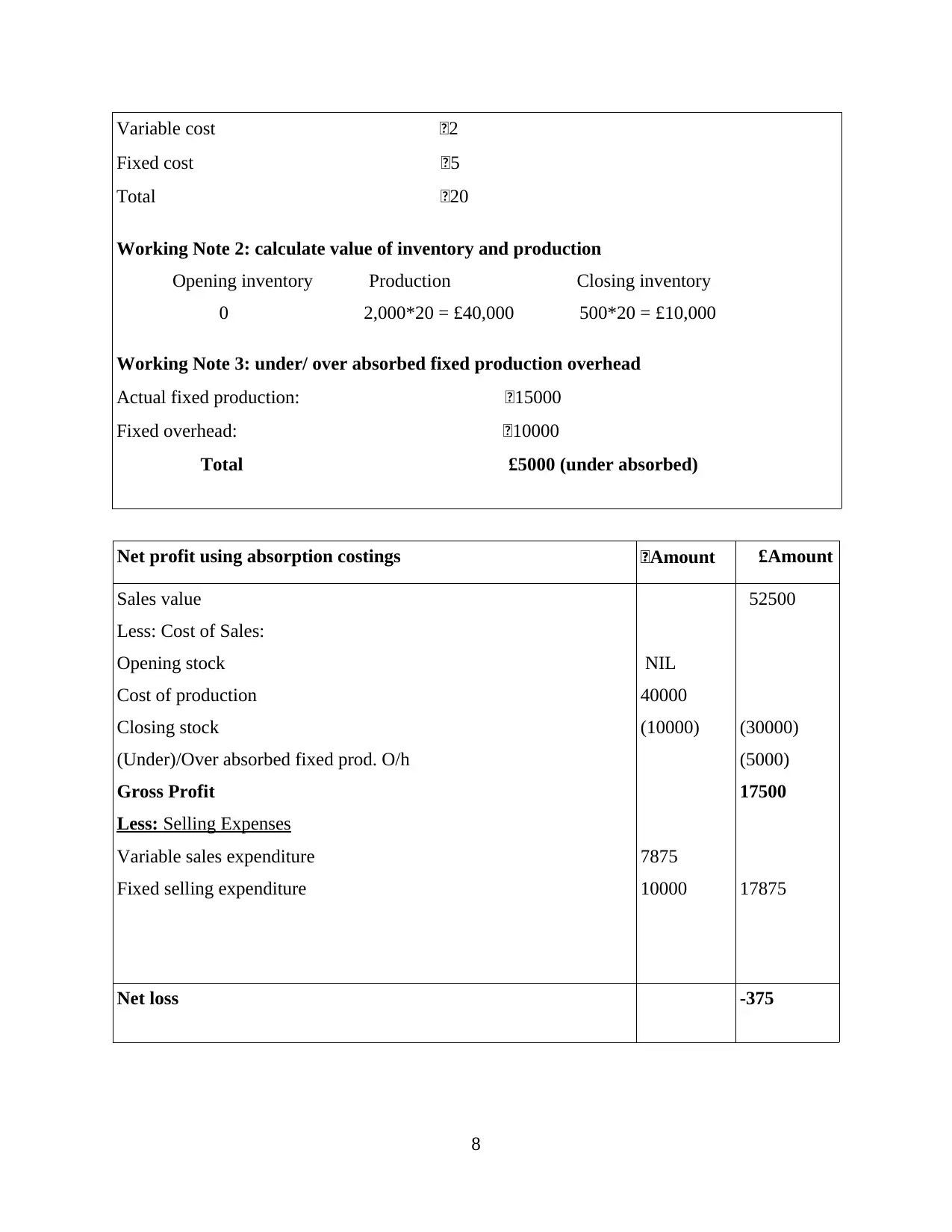

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

8

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2: Use of various techniques

There are various other costing techniques those are helpful in collecting more effective

outcomes in more quick time. Such as fixed and variable cost which is varies as per the

percentage change in total units produce during that time. Cost allocation is another reliable

costing technique which will assist in allocating cost at right places so that maximum growth can

be attained. Normal and standard costing is the one which is use to make comparison between

actual and estimated costs a company in investing in their projects.

D2: Interpretation of data for the business activities

For the purpose of generating maximum benefits from their total investment, it is

necessary to have right management techniques or costing methods. The Tech Imda Ltd need to

make use of both absorption and marginal costing to analyse their overall profit and loss. From

the above calculation, it has been found that they are getting different results from both costing

techniques. In spite of this, they need to select that one which is more effective and reliable for

making crucial decision making in coming time.

TASK 3

P4: Advantage and disadvantage of using planning tools in budget

Budget is known as estimation for future cost and expenditure that a company is going to

be incurring during the time of production process. It is a kind of financial plan for defined

period. It is mainly consists of planned sales volume and revenue, resources quantity and various

costs and expenses detail. In every business organisation, it is necessary to have proper control

over their production or costs. This can only be helpful in controlling extra costs which were

incurred during that period of time (Schaltegger and Csutora, 2012). There are various types of

budgets which are prepared by an organisation. Some of them are discuss underneath:

Operational budgets: This seems to be financial budget of any given activities which is

categories into cost account or function units. It consists of estimation of total cost of resources.

Advantages: It uses to track entire business operations by continuous monitoring and

recording of transactions.

Disadvantage: Inaccuracy is primary aspect which affects business under certain

situations.

9

There are various other costing techniques those are helpful in collecting more effective

outcomes in more quick time. Such as fixed and variable cost which is varies as per the

percentage change in total units produce during that time. Cost allocation is another reliable

costing technique which will assist in allocating cost at right places so that maximum growth can

be attained. Normal and standard costing is the one which is use to make comparison between

actual and estimated costs a company in investing in their projects.

D2: Interpretation of data for the business activities

For the purpose of generating maximum benefits from their total investment, it is

necessary to have right management techniques or costing methods. The Tech Imda Ltd need to

make use of both absorption and marginal costing to analyse their overall profit and loss. From

the above calculation, it has been found that they are getting different results from both costing

techniques. In spite of this, they need to select that one which is more effective and reliable for

making crucial decision making in coming time.

TASK 3

P4: Advantage and disadvantage of using planning tools in budget

Budget is known as estimation for future cost and expenditure that a company is going to

be incurring during the time of production process. It is a kind of financial plan for defined

period. It is mainly consists of planned sales volume and revenue, resources quantity and various

costs and expenses detail. In every business organisation, it is necessary to have proper control

over their production or costs. This can only be helpful in controlling extra costs which were

incurred during that period of time (Schaltegger and Csutora, 2012). There are various types of

budgets which are prepared by an organisation. Some of them are discuss underneath:

Operational budgets: This seems to be financial budget of any given activities which is

categories into cost account or function units. It consists of estimation of total cost of resources.

Advantages: It uses to track entire business operations by continuous monitoring and

recording of transactions.

Disadvantage: Inaccuracy is primary aspect which affects business under certain

situations.

9

Master budget: It is known as one of the major budgets which is summaries with all detail

information about total production and costs that is related in an accounting process. These are

prepared by using monthly, quarterly and yearly basis.

Advantage: The main positive aspect of this budget is not to make any additional budget

because all detail is mentioned on a single sheet.

Disadvantage: Such types of budgets are dynamic and costly.

Cash budget: These types of cost budget are mainly used to make use of all cash transaction

from associate activities. Such as operating, investing and financing (Zaleha Abdul Rasid and et.

al.,2014).

Advantage: To determine total cash inflow and outflow in an accounting period of time.

Disadvantage: These restricted to certain limitations as well as tool economical.

Process of budget:

In order to estimate detail idea about preparing budget for the company it is necessary to

collected various information. This information gather from each department can leads to take

action about formulating new budget for the cited company. Some crucial steps involve under

this projects are:

Before making any new plan, a proper estimation of budget needs can be analyse by the

company.

In the next step, company’s total forecasted of all income and expenses of various

departments are needed to be submitted to higher level.

After collecting permission from upper department, process of budget formulation gets

begun.

Then the next processes are to completed budget and resend it to top management to take

permission for publishing.

At the end, it is ready to be shown in front of various internal or external parties.

Pricing system: There are various pricing systems those are helpful in setting prices for their

products. Some of the crucial methods are discuss underneath:

Price skimming: According to this pricing policies which is being charged for increasing

demand of a new products. In the earlier stages, company used to set much higher prices.

Economic pricing: Under this pricing method, an organisation can set the costs as low

of their different products in accordance to attract maximum customers.

10

information about total production and costs that is related in an accounting process. These are

prepared by using monthly, quarterly and yearly basis.

Advantage: The main positive aspect of this budget is not to make any additional budget

because all detail is mentioned on a single sheet.

Disadvantage: Such types of budgets are dynamic and costly.

Cash budget: These types of cost budget are mainly used to make use of all cash transaction

from associate activities. Such as operating, investing and financing (Zaleha Abdul Rasid and et.

al.,2014).

Advantage: To determine total cash inflow and outflow in an accounting period of time.

Disadvantage: These restricted to certain limitations as well as tool economical.

Process of budget:

In order to estimate detail idea about preparing budget for the company it is necessary to

collected various information. This information gather from each department can leads to take

action about formulating new budget for the cited company. Some crucial steps involve under

this projects are:

Before making any new plan, a proper estimation of budget needs can be analyse by the

company.

In the next step, company’s total forecasted of all income and expenses of various

departments are needed to be submitted to higher level.

After collecting permission from upper department, process of budget formulation gets

begun.

Then the next processes are to completed budget and resend it to top management to take

permission for publishing.

At the end, it is ready to be shown in front of various internal or external parties.

Pricing system: There are various pricing systems those are helpful in setting prices for their

products. Some of the crucial methods are discuss underneath:

Price skimming: According to this pricing policies which is being charged for increasing

demand of a new products. In the earlier stages, company used to set much higher prices.

Economic pricing: Under this pricing method, an organisation can set the costs as low

of their different products in accordance to attract maximum customers.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.