Management Accounting Report: Essential Requirements and Methods

VerifiedAdded on 2020/06/04

|16

|5423

|104

Report

AI Summary

This report provides a comprehensive overview of management accounting, detailing its essential requirements and various methods used for reporting and analysis. It covers key aspects such as inventory management systems, job costing systems, price optimization, and cost accounting systems, emphasizing their roles in planning, monitoring, and controlling business activities. The report explores the use of both marginal and absorption costing methods to create income statements, highlighting their differences and applications. It also discusses the advantages and disadvantages of planning tools used for budgetary control, and how management accounting is utilized to solve financial problems. The report emphasizes the importance of management accounting in providing financial and statistical information for effective decision-making, and its integration with accounting, finance, and management to improve business understanding. The report concludes with a discussion on the benefits of these management accounting techniques for business performance.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1 Essential Requirements of Management Accounting systems..............................................1

P2: Methods used for management accounting reporting...........................................................3

M1...............................................................................................................................................4

D1................................................................................................................................................5

P3 Use of absorption and marginal costing to make income statements....................................5

P4 Disadvantages and advantages of various planning tools used for budgetary control..........8

M3...............................................................................................................................................9

P5 Use of management accounting in solving financial problems...........................................10

D3..............................................................................................................................................11

M4.............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

P1 Essential Requirements of Management Accounting systems..............................................1

P2: Methods used for management accounting reporting...........................................................3

M1...............................................................................................................................................4

D1................................................................................................................................................5

P3 Use of absorption and marginal costing to make income statements....................................5

P4 Disadvantages and advantages of various planning tools used for budgetary control..........8

M3...............................................................................................................................................9

P5 Use of management accounting in solving financial problems...........................................10

D3..............................................................................................................................................11

M4.............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management Accounting is a statement carrying the financial and statistical information

of the company necessary for the purpose of decision making (Macintosh and Quattrone, 2010).

This process is an integration of accounting, finance and management to develop a better

understanding of the business activities. Planning for the organisation is dependent on this report.

The information gathered is further utilised to perform monitoring and controlling functions by

the management. It is a process which involves analysis, interpretation and presentation of the

information gathered in financial accounting. The activities conducted in this process are carried

out in an efficient manner and information is collected should be the best of knowledge so that

the decisions taken works for the benefit of the company. Management accounting is different

from cost accounting in which reports are only prepared for the stakeholders. The report consist

of information such as available cash, sales revenue, current assets and liabilities of the

organisation. The report is kept strictly confidential and can be accessed by only the internal

member of the company. The various tools and techniques used in this process are mentioned

and along with a planning strategy for the coming period.

P1 Essential Requirements of Management Accounting systems

Management accounting is process which obtains, identifies, analyses and interprets the

information for the planning, monitoring and controlling of the business activities. It is an

amalgamation of accounts, finance and management for the welfare of the business. The report

which is formulated after this process is being sent to the top management which helps them in

formulating policies and deciding the future course of action. The data collected is revenue, cash

flows and debts of the company (Baldvinsdottir, Mitchell and Nørreklit, 2010). The financial and

non financial information obtained is combined to get a better view of the circumstances. This

process is utilized in all the organisation be it public or private limited company.

Management accounting system however is a system responsible for gathering of

financial data across various business operations such as sales, revenue, inventory costs and

prices of raw materials and converting into reports.

The following are the types of management accounting system.

Inventory Management System:

This system is the most preferred accounting system used for tracking inventory levels,

sales and deliveries. The most common technique used in this system is Bar code tracking. This

1

Management Accounting is a statement carrying the financial and statistical information

of the company necessary for the purpose of decision making (Macintosh and Quattrone, 2010).

This process is an integration of accounting, finance and management to develop a better

understanding of the business activities. Planning for the organisation is dependent on this report.

The information gathered is further utilised to perform monitoring and controlling functions by

the management. It is a process which involves analysis, interpretation and presentation of the

information gathered in financial accounting. The activities conducted in this process are carried

out in an efficient manner and information is collected should be the best of knowledge so that

the decisions taken works for the benefit of the company. Management accounting is different

from cost accounting in which reports are only prepared for the stakeholders. The report consist

of information such as available cash, sales revenue, current assets and liabilities of the

organisation. The report is kept strictly confidential and can be accessed by only the internal

member of the company. The various tools and techniques used in this process are mentioned

and along with a planning strategy for the coming period.

P1 Essential Requirements of Management Accounting systems

Management accounting is process which obtains, identifies, analyses and interprets the

information for the planning, monitoring and controlling of the business activities. It is an

amalgamation of accounts, finance and management for the welfare of the business. The report

which is formulated after this process is being sent to the top management which helps them in

formulating policies and deciding the future course of action. The data collected is revenue, cash

flows and debts of the company (Baldvinsdottir, Mitchell and Nørreklit, 2010). The financial and

non financial information obtained is combined to get a better view of the circumstances. This

process is utilized in all the organisation be it public or private limited company.

Management accounting system however is a system responsible for gathering of

financial data across various business operations such as sales, revenue, inventory costs and

prices of raw materials and converting into reports.

The following are the types of management accounting system.

Inventory Management System:

This system is the most preferred accounting system used for tracking inventory levels,

sales and deliveries. The most common technique used in this system is Bar code tracking. This

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

technique helps in tracking the inventories. Each inventory is provided with a bar code . The bar

codes are scanned whenever the inventories move in or out of the facility or can be used for

moving the inventory within the storage facility as well. The another common tool used is RFID.

This tool has a feature of advanced bar coding as every item consists a device which emits signal

any movement of the same can be tracked in no time. Both the tools help in maintaining

inventories at a appropriate level so that the company does not have to bear extra costs for

storing the same.

Job costing system

This accounting system focuses on accumulation of manufacturing cost independently for

each job. This system is beneficial in the company producing diversified products or niche

commodities (Lukka and Modell, 2010). The costs are categorised into overhead, direct and

indirect costs and lastly labour cost. The sole purpose of this system is to control the

manufacturing costs for each unit and enhancing the profitability.

Price Optimisation system

As the name suggests this system focuses on optimising the cost incurred by the company

on producing a product. This system helps a company by increasing the level of profitability.

The price charged from the consumers need to be maintained at a profitable level so that there is

an increase in the per product margin of the company. The crucial part is the price is to be

decided keeping in mind the competition, market and the purchasing power of the consumers so

that they are able to afford the product.

Cost accounting system

Cost accounting system is a tool used by the business houses to estimate the cost of

pricing of products for profitability analysis and cost control. This system is used to identify

what products are profitable for the company and which one are incurring losses. The various

elements which are involved in cost are to analysed while calculation of cost and ensuring that

problems shall not arise due to the non performing elements. This ensures the company that the

goals will be achieved in an effortless manner.

The essential requirement of Management accounting which are to be fulfilled by managers are: Traditional accounting techniques: these techniques are often used enterprises which

operate at a small or medium scale due to the less finance. The technique takes into

account the cost and profit on the forecasting basis. The need of management accounting

2

codes are scanned whenever the inventories move in or out of the facility or can be used for

moving the inventory within the storage facility as well. The another common tool used is RFID.

This tool has a feature of advanced bar coding as every item consists a device which emits signal

any movement of the same can be tracked in no time. Both the tools help in maintaining

inventories at a appropriate level so that the company does not have to bear extra costs for

storing the same.

Job costing system

This accounting system focuses on accumulation of manufacturing cost independently for

each job. This system is beneficial in the company producing diversified products or niche

commodities (Lukka and Modell, 2010). The costs are categorised into overhead, direct and

indirect costs and lastly labour cost. The sole purpose of this system is to control the

manufacturing costs for each unit and enhancing the profitability.

Price Optimisation system

As the name suggests this system focuses on optimising the cost incurred by the company

on producing a product. This system helps a company by increasing the level of profitability.

The price charged from the consumers need to be maintained at a profitable level so that there is

an increase in the per product margin of the company. The crucial part is the price is to be

decided keeping in mind the competition, market and the purchasing power of the consumers so

that they are able to afford the product.

Cost accounting system

Cost accounting system is a tool used by the business houses to estimate the cost of

pricing of products for profitability analysis and cost control. This system is used to identify

what products are profitable for the company and which one are incurring losses. The various

elements which are involved in cost are to analysed while calculation of cost and ensuring that

problems shall not arise due to the non performing elements. This ensures the company that the

goals will be achieved in an effortless manner.

The essential requirement of Management accounting which are to be fulfilled by managers are: Traditional accounting techniques: these techniques are often used enterprises which

operate at a small or medium scale due to the less finance. The technique takes into

account the cost and profit on the forecasting basis. The need of management accounting

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is realised as cost plays one of the most important function of organisation. It helps the

organisation in calculating the cost which is linked to the upcoming projects.

Lean accounting: this process focuses on eliminating the unnecessary activites and

processes in an organisation. This techniques is mostly applied in the manufacturing

sector or in streamlining design or in service processes (Bodie, 2013). The biggest

drawback of lean accounting is that it requires a total change in the cultural environment

of the company. This process is very costly and time consuming.

P2: Methods used for management accounting reporting

In an organisation, the financial information are recorded with the help of using

appropriate accounting system. Because most of the valuable decisions are taken on the basis of

these systems. All the necessary data those are collected by the firm are need to be reported in

the designed format so that it would be used at the time of decision making. To get maximum

competitive advantages these prove to be useful for the entire department. The reports which are

prepared from the collected data are implemented in proper manner by the managers in the

context of future forecasted. With the effective reporting of accounting system a cited company

determine its stock position and availability of cash to meet out its debts and outstanding

liabilities. The reporting can be filled according to the set policies which are made by the

company. It is mainly prepared at the end of the year. The most of he effective decisions are rely

on the reporting of financial statements. The managers of the company need to organise and

collect each information with financial transactions from concern department are recorded in it.

The management need to maintain balance between various departments so the future

goals can be achieved. The collected data are categorised into a summarised form in order to

prepare a annual report. Some of them are:

Job costing report: In the production process, there are various jobs which need to be

performed by the managers according to the set plan. So that total estimation of possible

outcomes can be determine. Because under this report, an individual products are not

considered but the lot of product segments are taken into consideration. By the help of

this report all the necessary activities which are carried in an organisation if no use to the

businesses are identified and valuable steps are taken against them. This support the

manager of firm to eliminate the jobs which create no profit for the company and can

3

organisation in calculating the cost which is linked to the upcoming projects.

Lean accounting: this process focuses on eliminating the unnecessary activites and

processes in an organisation. This techniques is mostly applied in the manufacturing

sector or in streamlining design or in service processes (Bodie, 2013). The biggest

drawback of lean accounting is that it requires a total change in the cultural environment

of the company. This process is very costly and time consuming.

P2: Methods used for management accounting reporting

In an organisation, the financial information are recorded with the help of using

appropriate accounting system. Because most of the valuable decisions are taken on the basis of

these systems. All the necessary data those are collected by the firm are need to be reported in

the designed format so that it would be used at the time of decision making. To get maximum

competitive advantages these prove to be useful for the entire department. The reports which are

prepared from the collected data are implemented in proper manner by the managers in the

context of future forecasted. With the effective reporting of accounting system a cited company

determine its stock position and availability of cash to meet out its debts and outstanding

liabilities. The reporting can be filled according to the set policies which are made by the

company. It is mainly prepared at the end of the year. The most of he effective decisions are rely

on the reporting of financial statements. The managers of the company need to organise and

collect each information with financial transactions from concern department are recorded in it.

The management need to maintain balance between various departments so the future

goals can be achieved. The collected data are categorised into a summarised form in order to

prepare a annual report. Some of them are:

Job costing report: In the production process, there are various jobs which need to be

performed by the managers according to the set plan. So that total estimation of possible

outcomes can be determine. Because under this report, an individual products are not

considered but the lot of product segments are taken into consideration. By the help of

this report all the necessary activities which are carried in an organisation if no use to the

businesses are identified and valuable steps are taken against them. This support the

manager of firm to eliminate the jobs which create no profit for the company and can

3

invest these funds on the other profitable activities. In this way profitability of company

can be increased and efficiency can be achieve. Variance analysis report: Under this process of different activities there are variances

which are analysed from various sales done by the company during the year. It is mostly

required to determine the effects and problems which are related with revenues incurred

by the company during the year (Parker, 2012). Variances are generally comes out from

the standard and actual sales comparison. This report can make the company to control its

losses from the total sales of their products. Inventory management system: This system is used by the enterprises to manage the

stock in an effective manner. Economic order quantity is identify to maintain the stock at

an appropriate level so that company can achieve efficiency in its storage process. This

help the firm eliminate other problems like shortage of funds and many more. Cost accounting system: Cost is a broad concept which include various elements. Main

factor which affect the overall cost of enterprise in order to maintain the efficiency and to

achieve the goals in an effective manner.

Price optimisation system: This system is used by the companies to identify and set an

optimum price for the company's product so that company can maintain its profitability.

Cost price and various other methods are there which can be used by the firm to set an

optimum price for its product.

All these are the main methods of management accounting for reporting. By using this manager

of Nero Ltd can provide various benefits to the firm and can maintain the effectiveness of

various business activities (Otley and Emmanuel, 2013). By using these firm can set an

optimum and right prices for its products and can attract more number of customers. With the

help of these methods company can maintain an optimum level of stock so additional cost of

firm can be saved.

M1

To carry out all the business activities and processes in an effective way it is very

necessary that a firm should have all the information required. For this various systems are there

through which a company can get support. Important aspects of a business such as employee's

performance, cost of business operations can be maintained. This not only reduce the risk of

business operation but also increase their effectiveness. Further it help the company to maintain a

4

can be increased and efficiency can be achieve. Variance analysis report: Under this process of different activities there are variances

which are analysed from various sales done by the company during the year. It is mostly

required to determine the effects and problems which are related with revenues incurred

by the company during the year (Parker, 2012). Variances are generally comes out from

the standard and actual sales comparison. This report can make the company to control its

losses from the total sales of their products. Inventory management system: This system is used by the enterprises to manage the

stock in an effective manner. Economic order quantity is identify to maintain the stock at

an appropriate level so that company can achieve efficiency in its storage process. This

help the firm eliminate other problems like shortage of funds and many more. Cost accounting system: Cost is a broad concept which include various elements. Main

factor which affect the overall cost of enterprise in order to maintain the efficiency and to

achieve the goals in an effective manner.

Price optimisation system: This system is used by the companies to identify and set an

optimum price for the company's product so that company can maintain its profitability.

Cost price and various other methods are there which can be used by the firm to set an

optimum price for its product.

All these are the main methods of management accounting for reporting. By using this manager

of Nero Ltd can provide various benefits to the firm and can maintain the effectiveness of

various business activities (Otley and Emmanuel, 2013). By using these firm can set an

optimum and right prices for its products and can attract more number of customers. With the

help of these methods company can maintain an optimum level of stock so additional cost of

firm can be saved.

M1

To carry out all the business activities and processes in an effective way it is very

necessary that a firm should have all the information required. For this various systems are there

through which a company can get support. Important aspects of a business such as employee's

performance, cost of business operations can be maintained. This not only reduce the risk of

business operation but also increase their effectiveness. Further it help the company to maintain a

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

optimum level of stock which decrease the cost of business operation and help the company to

achieve competitive advantage. Overall the concept of management accounting provide various

benefits to an enterprise.

D1

Every organisation set some objectives and goals to achieve in the near future so that

desire mount of profit can be generated by the company. Reports which are prepared by the firm

provide useful facts and information to manager working at top level and guide them in taking

decision about the company (Tucker and Parker, 2014). Both the process are integrated with

each other without completion of one other can not be executed working of both in an effective

manner is necessary.

P3 Use of absorption and marginal costing to make income statements

Production process of an organisation include various number of costs which need to be

identify by the organisation. For this there are various methods which can be used by the

company. Expenses which occur during the production process are mainly divided into two

categories called fixed and variable. Treatment of these expense remain different as per the

situation. Main methods of this are explained below: Marginal costing: This is the cost which get affected by the number of units produce by

the company in a given time frame. Variation in quantity produce directly affect the total

amount of expenditure of production process (Malmi, 2010). All expenditure such as

labour and material cost are allocated to the production process as per the units produced.

In this expenses are not divided as per the category of fixed cost but they are incorporated

in the income statement with the heading of total amount. After calculation of variable

costs this amount deduct to attain the contribution.

Absorption costing: Under this, fixed cost treated differently, it included as per the basis

of productions which take place in the organisation. A different approach is adopted by

the company to calculate the profits (Vakalfotis, Ballantine and Wall, 2013). In this all

overheads are incorporated for calculating the gross income and then both selling and

administration expenses are included. After that addition and deduction take place in

order to find out the over or under absorption in order to calculate the final profit made

by the company.

Main difference between absorption and marginal costing can be understood by the table given

5

achieve competitive advantage. Overall the concept of management accounting provide various

benefits to an enterprise.

D1

Every organisation set some objectives and goals to achieve in the near future so that

desire mount of profit can be generated by the company. Reports which are prepared by the firm

provide useful facts and information to manager working at top level and guide them in taking

decision about the company (Tucker and Parker, 2014). Both the process are integrated with

each other without completion of one other can not be executed working of both in an effective

manner is necessary.

P3 Use of absorption and marginal costing to make income statements

Production process of an organisation include various number of costs which need to be

identify by the organisation. For this there are various methods which can be used by the

company. Expenses which occur during the production process are mainly divided into two

categories called fixed and variable. Treatment of these expense remain different as per the

situation. Main methods of this are explained below: Marginal costing: This is the cost which get affected by the number of units produce by

the company in a given time frame. Variation in quantity produce directly affect the total

amount of expenditure of production process (Malmi, 2010). All expenditure such as

labour and material cost are allocated to the production process as per the units produced.

In this expenses are not divided as per the category of fixed cost but they are incorporated

in the income statement with the heading of total amount. After calculation of variable

costs this amount deduct to attain the contribution.

Absorption costing: Under this, fixed cost treated differently, it included as per the basis

of productions which take place in the organisation. A different approach is adopted by

the company to calculate the profits (Vakalfotis, Ballantine and Wall, 2013). In this all

overheads are incorporated for calculating the gross income and then both selling and

administration expenses are included. After that addition and deduction take place in

order to find out the over or under absorption in order to calculate the final profit made

by the company.

Main difference between absorption and marginal costing can be understood by the table given

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

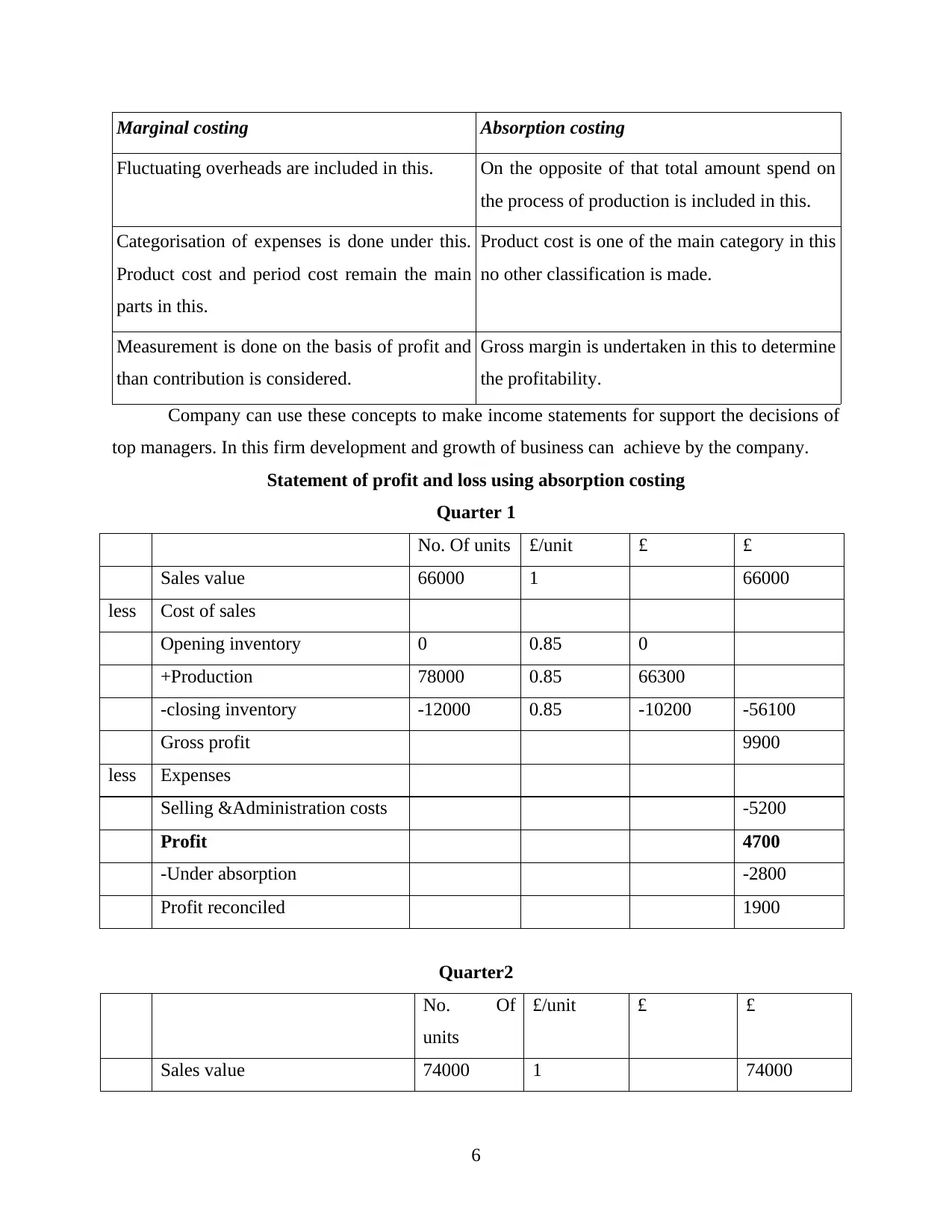

Marginal costing Absorption costing

Fluctuating overheads are included in this. On the opposite of that total amount spend on

the process of production is included in this.

Categorisation of expenses is done under this.

Product cost and period cost remain the main

parts in this.

Product cost is one of the main category in this

no other classification is made.

Measurement is done on the basis of profit and

than contribution is considered.

Gross margin is undertaken in this to determine

the profitability.

Company can use these concepts to make income statements for support the decisions of

top managers. In this firm development and growth of business can achieve by the company.

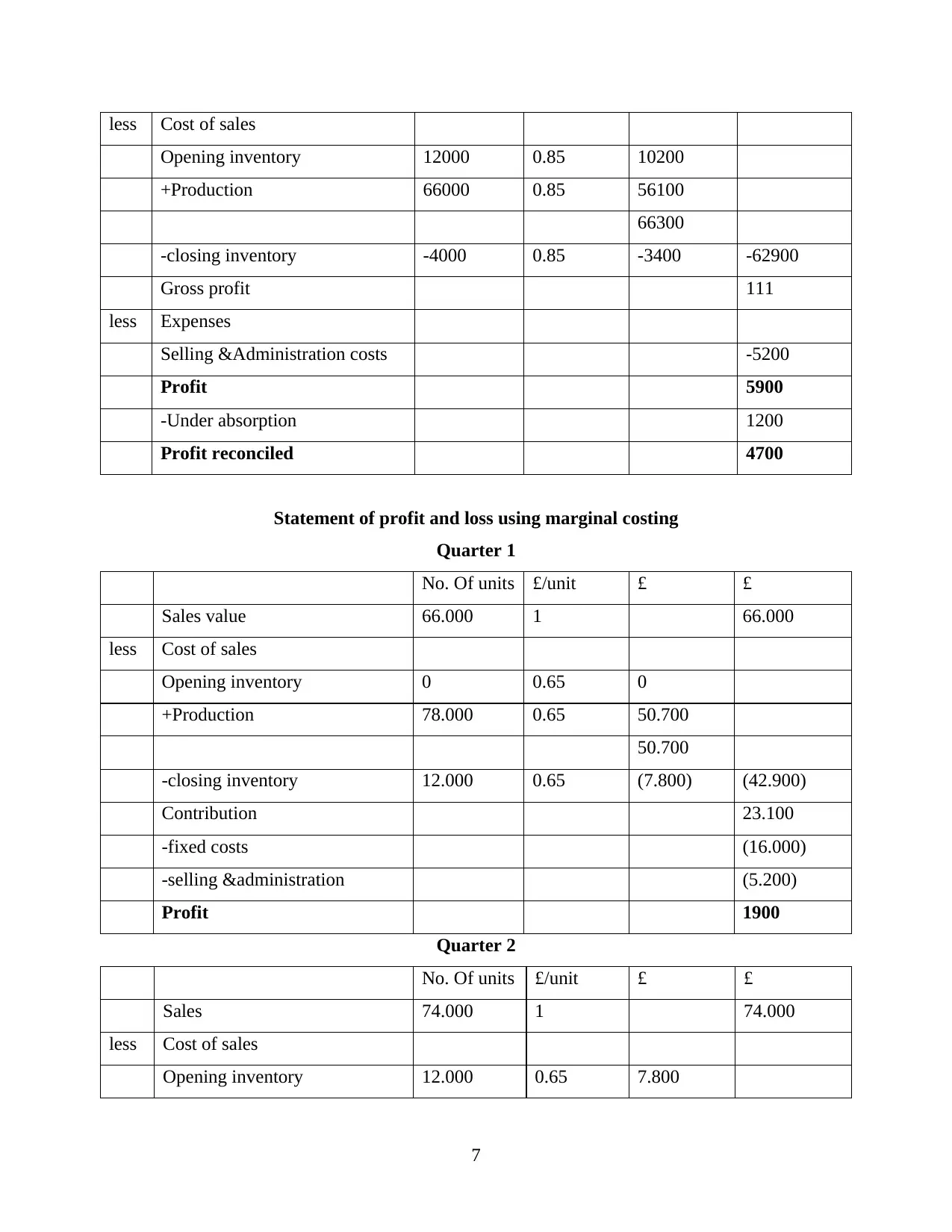

Statement of profit and loss using absorption costing

Quarter 1

No. Of units £/unit £ £

Sales value 66000 1 66000

less Cost of sales

Opening inventory 0 0.85 0

+Production 78000 0.85 66300

-closing inventory -12000 0.85 -10200 -56100

Gross profit 9900

less Expenses

Selling &Administration costs -5200

Profit 4700

-Under absorption -2800

Profit reconciled 1900

Quarter2

No. Of

units

£/unit £ £

Sales value 74000 1 74000

6

Fluctuating overheads are included in this. On the opposite of that total amount spend on

the process of production is included in this.

Categorisation of expenses is done under this.

Product cost and period cost remain the main

parts in this.

Product cost is one of the main category in this

no other classification is made.

Measurement is done on the basis of profit and

than contribution is considered.

Gross margin is undertaken in this to determine

the profitability.

Company can use these concepts to make income statements for support the decisions of

top managers. In this firm development and growth of business can achieve by the company.

Statement of profit and loss using absorption costing

Quarter 1

No. Of units £/unit £ £

Sales value 66000 1 66000

less Cost of sales

Opening inventory 0 0.85 0

+Production 78000 0.85 66300

-closing inventory -12000 0.85 -10200 -56100

Gross profit 9900

less Expenses

Selling &Administration costs -5200

Profit 4700

-Under absorption -2800

Profit reconciled 1900

Quarter2

No. Of

units

£/unit £ £

Sales value 74000 1 74000

6

less Cost of sales

Opening inventory 12000 0.85 10200

+Production 66000 0.85 56100

66300

-closing inventory -4000 0.85 -3400 -62900

Gross profit 111

less Expenses

Selling &Administration costs -5200

Profit 5900

-Under absorption 1200

Profit reconciled 4700

Statement of profit and loss using marginal costing

Quarter 1

No. Of units £/unit £ £

Sales value 66.000 1 66.000

less Cost of sales

Opening inventory 0 0.65 0

+Production 78.000 0.65 50.700

50.700

-closing inventory 12.000 0.65 (7.800) (42.900)

Contribution 23.100

-fixed costs (16.000)

-selling &administration (5.200)

Profit 1900

Quarter 2

No. Of units £/unit £ £

Sales 74.000 1 74.000

less Cost of sales

Opening inventory 12.000 0.65 7.800

7

Opening inventory 12000 0.85 10200

+Production 66000 0.85 56100

66300

-closing inventory -4000 0.85 -3400 -62900

Gross profit 111

less Expenses

Selling &Administration costs -5200

Profit 5900

-Under absorption 1200

Profit reconciled 4700

Statement of profit and loss using marginal costing

Quarter 1

No. Of units £/unit £ £

Sales value 66.000 1 66.000

less Cost of sales

Opening inventory 0 0.65 0

+Production 78.000 0.65 50.700

50.700

-closing inventory 12.000 0.65 (7.800) (42.900)

Contribution 23.100

-fixed costs (16.000)

-selling &administration (5.200)

Profit 1900

Quarter 2

No. Of units £/unit £ £

Sales 74.000 1 74.000

less Cost of sales

Opening inventory 12.000 0.65 7.800

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

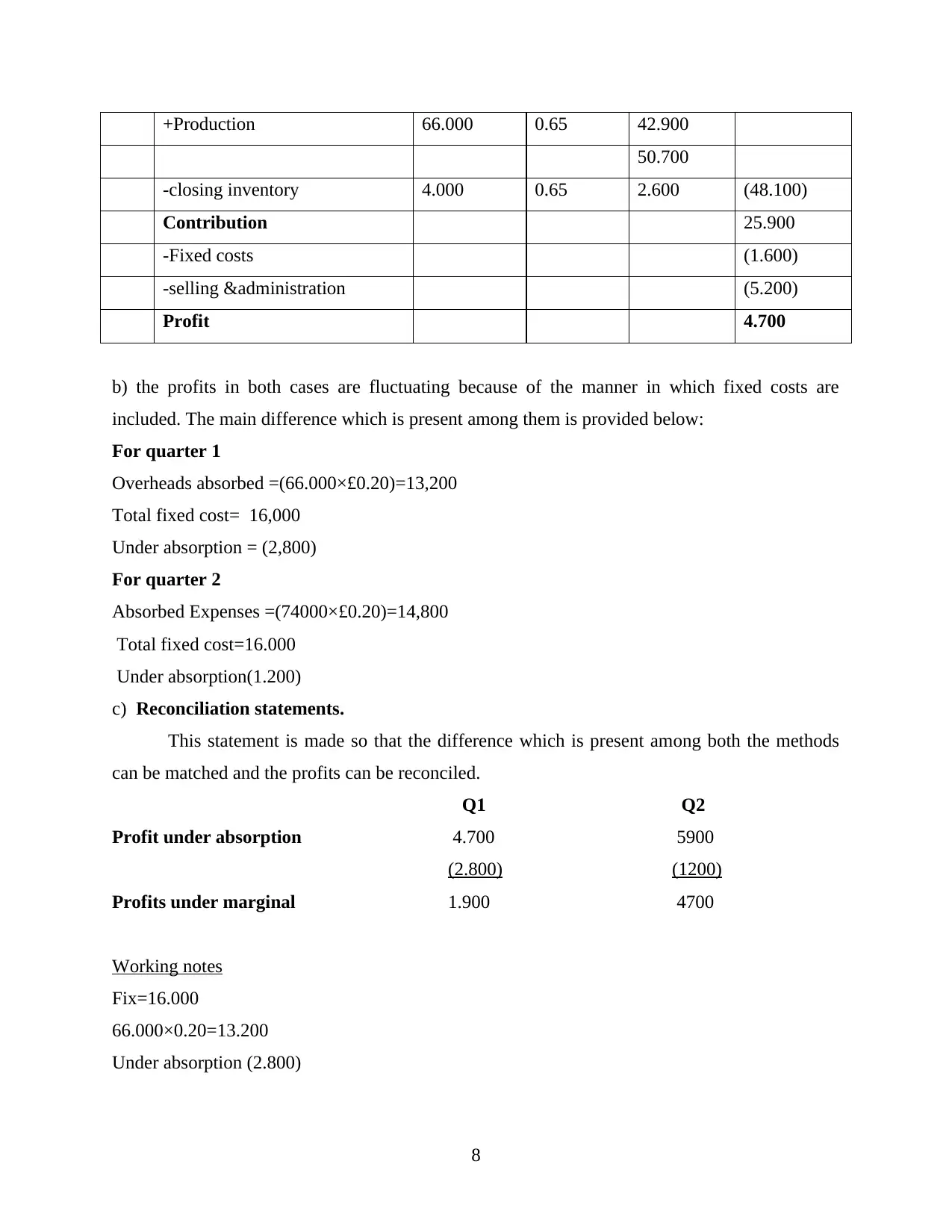

+Production 66.000 0.65 42.900

50.700

-closing inventory 4.000 0.65 2.600 (48.100)

Contribution 25.900

-Fixed costs (1.600)

-selling &administration (5.200)

Profit 4.700

b) the profits in both cases are fluctuating because of the manner in which fixed costs are

included. The main difference which is present among them is provided below:

For quarter 1

Overheads absorbed =(66.000×£0.20)=13,200

Total fixed cost= 16,000

Under absorption = (2,800)

For quarter 2

Absorbed Expenses =(74000×£0.20)=14,800

Total fixed cost=16.000

Under absorption(1.200)

c) Reconciliation statements.

This statement is made so that the difference which is present among both the methods

can be matched and the profits can be reconciled.

Q1 Q2

Profit under absorption 4.700 5900

(2.800) (1200)

Profits under marginal 1.900 4700

Working notes

Fix=16.000

66.000×0.20=13.200

Under absorption (2.800)

8

50.700

-closing inventory 4.000 0.65 2.600 (48.100)

Contribution 25.900

-Fixed costs (1.600)

-selling &administration (5.200)

Profit 4.700

b) the profits in both cases are fluctuating because of the manner in which fixed costs are

included. The main difference which is present among them is provided below:

For quarter 1

Overheads absorbed =(66.000×£0.20)=13,200

Total fixed cost= 16,000

Under absorption = (2,800)

For quarter 2

Absorbed Expenses =(74000×£0.20)=14,800

Total fixed cost=16.000

Under absorption(1.200)

c) Reconciliation statements.

This statement is made so that the difference which is present among both the methods

can be matched and the profits can be reconciled.

Q1 Q2

Profit under absorption 4.700 5900

(2.800) (1200)

Profits under marginal 1.900 4700

Working notes

Fix=16.000

66.000×0.20=13.200

Under absorption (2.800)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

74.000×0.20=14.800

Fix=16.000

Under absorption=1.200

P4 Disadvantages and advantages of various planning tools used for budgetary control

In an enterprise it is very essential that all the available tools and techniques should be

taken into account before taking any decision and for that it is very necessary to collect all the

relevant data about them. This help the organisation in control all the activities and operation sin

an effective manner which provide both short and long term advantage to the enterprise and

ensure growth of the company (Tayles, 2011). For this various budgets are prepared in every

organisation at various level because this provide support to the organisation activities and help

in achieve various objectives. It is a written plan which assist about the future expenses of an

organisation and give information about the income of company. This provide ground to evaluate

the performance of various departments against the set standards. Identification of all variations

help in future planning of the business.

Proper investigation is done by the firms and data is collected about the past action and

decision of the company to take effective future decisions. Projection and prediction about every

department is done by the organisation for incorporated new business budgets. All the problems

which could occur in the business are also included in the budget to avoid the same in the future.

Merits of budget

This ensure the proper and optimum utilisation of all the available resources and assets to

increase effectiveness of business operations.

This provide an effective control on all the expenditures of business which help reduce

the overall expenses of business. Ensure effective communication among all the departments of firm which ensure the

fulfilment of all business objectives.

Demerits of budget

Lot of amount is spend on the whole process of making budgets, this is an expensive

process because this increase the unnecessary burden of the firm.

It is a time consuming process which create delays in the other operation of enterprise.

By save this time an enterprise can create additional benefits form its activities.

9

Fix=16.000

Under absorption=1.200

P4 Disadvantages and advantages of various planning tools used for budgetary control

In an enterprise it is very essential that all the available tools and techniques should be

taken into account before taking any decision and for that it is very necessary to collect all the

relevant data about them. This help the organisation in control all the activities and operation sin

an effective manner which provide both short and long term advantage to the enterprise and

ensure growth of the company (Tayles, 2011). For this various budgets are prepared in every

organisation at various level because this provide support to the organisation activities and help

in achieve various objectives. It is a written plan which assist about the future expenses of an

organisation and give information about the income of company. This provide ground to evaluate

the performance of various departments against the set standards. Identification of all variations

help in future planning of the business.

Proper investigation is done by the firms and data is collected about the past action and

decision of the company to take effective future decisions. Projection and prediction about every

department is done by the organisation for incorporated new business budgets. All the problems

which could occur in the business are also included in the budget to avoid the same in the future.

Merits of budget

This ensure the proper and optimum utilisation of all the available resources and assets to

increase effectiveness of business operations.

This provide an effective control on all the expenditures of business which help reduce

the overall expenses of business. Ensure effective communication among all the departments of firm which ensure the

fulfilment of all business objectives.

Demerits of budget

Lot of amount is spend on the whole process of making budgets, this is an expensive

process because this increase the unnecessary burden of the firm.

It is a time consuming process which create delays in the other operation of enterprise.

By save this time an enterprise can create additional benefits form its activities.

9

As whole process is based on the estimation and prediction and it is not necessary that all

the prediction proof right and in this a business enterprise fail to achieve the set results.

Cash budget: Under this budget, all the activities of business which undertaken with the

help of cash, are included in this (Lukka and Vinnari, 2014). This provide an opportunity to the

organisation to manage the funds effectively in a proper manner which leads and improve the

financial position of a company. This budget aids effectiveness in the planning activity of a

manager and assist him to collect all the funds required to execute the activities.

Operation budget: This budget is made by thee organisations to specify the way in which

all the operation of company will be executed (Tappura and et. al., 2015). This ensure effective

implementation of all the activities and help the company to achieve the set criteria. This budget

help in implemented all the complex tasks of a business firm.

M3

It is very necessary for a business manager to first identify the problems and issues exist

in the business environment. This can be done by him by evaluating the financial statements of

the company. In this way efficiency and effectiveness in all the business operation can be

managed and enhanced. Various methods are and tools are are available to an enterprise for this.

Estimation help the business managers to identify the issues and problems which can rise in

future and also recommend the effective ways for completing the business operations. Further it

help the top manager to make effective budgets for all the department and utilise all the available

resources of the company.

P5 Use of management accounting in solving financial problems

There can be numerous problems which can arise in business over a period of time. But a

organisation have to solve them in order to achieve the objectives smoothly. For instance a

business is having problems with communication so the business have to formulate policies in

such a manner that the hurdle should be crossed and ensures coordination among the employees.

The formulated policies should be cross examined so that there are no loopholes during the

course of strategy formulation (Quinn, 2011). This ensures that the business conducts its

operations in a effective manner and the finance saved can be utilised further in business.

Key performance Indicators

KPI is a value that clearly shows how effectively a business is fulfilling its goals. They

help in measuring the effectiveness of a function in an organisation. It demonstrates how the core

10

the prediction proof right and in this a business enterprise fail to achieve the set results.

Cash budget: Under this budget, all the activities of business which undertaken with the

help of cash, are included in this (Lukka and Vinnari, 2014). This provide an opportunity to the

organisation to manage the funds effectively in a proper manner which leads and improve the

financial position of a company. This budget aids effectiveness in the planning activity of a

manager and assist him to collect all the funds required to execute the activities.

Operation budget: This budget is made by thee organisations to specify the way in which

all the operation of company will be executed (Tappura and et. al., 2015). This ensure effective

implementation of all the activities and help the company to achieve the set criteria. This budget

help in implemented all the complex tasks of a business firm.

M3

It is very necessary for a business manager to first identify the problems and issues exist

in the business environment. This can be done by him by evaluating the financial statements of

the company. In this way efficiency and effectiveness in all the business operation can be

managed and enhanced. Various methods are and tools are are available to an enterprise for this.

Estimation help the business managers to identify the issues and problems which can rise in

future and also recommend the effective ways for completing the business operations. Further it

help the top manager to make effective budgets for all the department and utilise all the available

resources of the company.

P5 Use of management accounting in solving financial problems

There can be numerous problems which can arise in business over a period of time. But a

organisation have to solve them in order to achieve the objectives smoothly. For instance a

business is having problems with communication so the business have to formulate policies in

such a manner that the hurdle should be crossed and ensures coordination among the employees.

The formulated policies should be cross examined so that there are no loopholes during the

course of strategy formulation (Quinn, 2011). This ensures that the business conducts its

operations in a effective manner and the finance saved can be utilised further in business.

Key performance Indicators

KPI is a value that clearly shows how effectively a business is fulfilling its goals. They

help in measuring the effectiveness of a function in an organisation. It demonstrates how the core

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.