Management Accounting Report: Costing Techniques and Budgetary Control

VerifiedAdded on 2023/01/23

|22

|5822

|69

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Equilibrium Asset Management, a financial consultancy firm, and its client, Ryder Architecture, a construction company. The report explores the core principles of management accounting, emphasizing its role in internal decision-making and strategic planning. It examines various management accounting systems, including cost accounting, inventory management, price optimization, and job order costing, highlighting their benefits and applications. Furthermore, the report analyzes different management accounting reporting methods, such as performance reports, budget reports, and accounts receivable reports, and discusses their integration into organizational processes. The report also covers costing techniques, including direct and indirect costs, cost analysis, and cost-volume-profit analysis, providing a comprehensive understanding of cost management. Finally, the report explores the advantages and disadvantages of different planning tools used for budgetary control and concludes with an overview of how organizations adapt their management accounting systems to respond to financial challenges.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of its systems.......................................1

P2 Different methods used for management accounting reporting.............................................4

TASK 2............................................................................................................................................5

P3 Calculation of cost using different costing techniques...........................................................5

........................................................................................................................................................10

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different planning tool used for budgetary control........10

TASK 4..........................................................................................................................................13

P5 Comparison of the way in which organisations are adapting management accounting

systems.......................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of its systems.......................................1

P2 Different methods used for management accounting reporting.............................................4

TASK 2............................................................................................................................................5

P3 Calculation of cost using different costing techniques...........................................................5

........................................................................................................................................................10

TASK 3..........................................................................................................................................10

P4 Advantages and disadvantages of different planning tool used for budgetary control........10

TASK 4..........................................................................................................................................13

P5 Comparison of the way in which organisations are adapting management accounting

systems.......................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is can be defined as the process of keeping record of internal

information of the company so that strategic decision for betterment of organisation can be

formulated. With the help of it, internal stakeholders such as managers, employees etc. analyse

that business entity is performing well or not in the market (Chenhall and Moers, 2015). It also

helps external stakeholders to determine actual status of the enterprise. This report is based upon

medium sized financial consultancy firm Equilibrium Asset Management that is having different

clients such as Ryder Architecture which is a construction company established in UK.

This assignment covers various topics such as management accounting, its reporting,

systems, use of different costing methods to calculate costs, advantages and disadvantages of

planning tools used in budgetary control. Along with this, the way in which management

accounting systems are used by companies to respond financial problems is also covered under

this report.

TASK 1

P1 Management accounting and essential requirements of its systems

Management accounting: It is a process of analysing and communicating organisational

data with managers so that they can observe performance of company and form strategies to

enhance it. Equilibrium Asset Management helps Ryder Architecture to conduct it on regular

basis so that actual performance of organisation can be measured.

Origin and evolution of management accounting: Management accounting was firstly

emerged as a significant activity during the earlier industrial revolution. It was originated after

financial accounting which can trace its origin to its stewardship role in different trading

ventures. Two major industries which has played an important role in the evolution of it were

textile and railroad.

Management accounting systems: Management accounting systems are such types of

systems which are used by managers of enterprises for the purpose of keeping track record of

different functional and operational departments of business. There are various types of systems

that are used by Equilibrium Asset Management in order to help stakeholders of Ryder

Architecture to determine actual status of organisation (Fullerton, Kennedy and Widener, 2014).

1

Management accounting is can be defined as the process of keeping record of internal

information of the company so that strategic decision for betterment of organisation can be

formulated. With the help of it, internal stakeholders such as managers, employees etc. analyse

that business entity is performing well or not in the market (Chenhall and Moers, 2015). It also

helps external stakeholders to determine actual status of the enterprise. This report is based upon

medium sized financial consultancy firm Equilibrium Asset Management that is having different

clients such as Ryder Architecture which is a construction company established in UK.

This assignment covers various topics such as management accounting, its reporting,

systems, use of different costing methods to calculate costs, advantages and disadvantages of

planning tools used in budgetary control. Along with this, the way in which management

accounting systems are used by companies to respond financial problems is also covered under

this report.

TASK 1

P1 Management accounting and essential requirements of its systems

Management accounting: It is a process of analysing and communicating organisational

data with managers so that they can observe performance of company and form strategies to

enhance it. Equilibrium Asset Management helps Ryder Architecture to conduct it on regular

basis so that actual performance of organisation can be measured.

Origin and evolution of management accounting: Management accounting was firstly

emerged as a significant activity during the earlier industrial revolution. It was originated after

financial accounting which can trace its origin to its stewardship role in different trading

ventures. Two major industries which has played an important role in the evolution of it were

textile and railroad.

Management accounting systems: Management accounting systems are such types of

systems which are used by managers of enterprises for the purpose of keeping track record of

different functional and operational departments of business. There are various types of systems

that are used by Equilibrium Asset Management in order to help stakeholders of Ryder

Architecture to determine actual status of organisation (Fullerton, Kennedy and Widener, 2014).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Explanation of management accounting: It can be defined as the process of generating

different management reports and accounts in order to analyse actual status of the company.

With the help of it, managers of Ryder Architecture can form strategic decisions for day to day

activities of organisation.

Difference between management and financial accounting:

Management accounting Financial accounting

It provides information of organisation's

performance to the internal stakeholders.

With the help of it, external stakeholders get

information regarding organisation's actual

financial status.

There are no specific standards and principles

to conduct management accounting.

While conducting financial accounting, it is

very important to comply with specific

accounting standards and principles.

Different management accounting systems are as follows:

Cost accounting system: With the help of it managers of companies analyse different

costs that are related to various activities such as manufacturing. It is used by financial advisers

in Equilibrium Asset Management for Ryder Architecture in order to keep detailed information

of all the expenses that are related to building construction and other services. It is required for

the organisation as it helps to keep track record of direct and indirect cost of business. It helps to

add value to the enterprise because with the help of it, information regarding all the expenses can

be gathered (Englund and Gerdin, 2014).

Inventory management system: It is mainly used in manufacturing companies in order

to manage inventory in appropriate manner. This system is used by Equilibrium Asset

Management for its client Ryder Architecture for the purpose of keeping track record of all the

items that are used for the purpose of preparation of goods. There are three different types of

inventory management systems LIFO, FIFO and AVCO.

In LIFO recently received stock is used for production activities first. In FIFO system,

earlier bought items are used for manufacturing activities. In AVCO, goods are used in average

cost basis for production. In Ryder Architecture FIFO is used for the purpose of constructing

buildings. This system is required for all the business entities as it can help to keep detailed

2

different management reports and accounts in order to analyse actual status of the company.

With the help of it, managers of Ryder Architecture can form strategic decisions for day to day

activities of organisation.

Difference between management and financial accounting:

Management accounting Financial accounting

It provides information of organisation's

performance to the internal stakeholders.

With the help of it, external stakeholders get

information regarding organisation's actual

financial status.

There are no specific standards and principles

to conduct management accounting.

While conducting financial accounting, it is

very important to comply with specific

accounting standards and principles.

Different management accounting systems are as follows:

Cost accounting system: With the help of it managers of companies analyse different

costs that are related to various activities such as manufacturing. It is used by financial advisers

in Equilibrium Asset Management for Ryder Architecture in order to keep detailed information

of all the expenses that are related to building construction and other services. It is required for

the organisation as it helps to keep track record of direct and indirect cost of business. It helps to

add value to the enterprise because with the help of it, information regarding all the expenses can

be gathered (Englund and Gerdin, 2014).

Inventory management system: It is mainly used in manufacturing companies in order

to manage inventory in appropriate manner. This system is used by Equilibrium Asset

Management for its client Ryder Architecture for the purpose of keeping track record of all the

items that are used for the purpose of preparation of goods. There are three different types of

inventory management systems LIFO, FIFO and AVCO.

In LIFO recently received stock is used for production activities first. In FIFO system,

earlier bought items are used for manufacturing activities. In AVCO, goods are used in average

cost basis for production. In Ryder Architecture FIFO is used for the purpose of constructing

buildings. This system is required for all the business entities as it can help to keep detailed

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information of stock which is used for business operations (Honggowati and et.al., 2017). It add

value to the organisation by helping managers to maintaining inventory according to the

requirements.

Price optimisation system: As its name states, it is mainly used to set optimum prices

for all the products that are manufactured by the organisation. It is utilised by Equilibrium Asset

Management which preparing record of Ryder Architecture for the purpose of helping managers

to set appropriate prices for all the buildings sold to customers. It is important and also add value

to the organisation as it helps to analyse that the price which is set by the company for building is

able to meet expectation of customers or not (Smith, 2017).

Job order costing system: It is a system which is used to assign and accumulate cost of

each manufactured unit of organisation. With the help of this system, Equilibrium Asset

Management helps its client Ryder Architecture to assign cost to each and every building

constructed by the enterprise which is going to be sold to customers. It is very important for the

entity as it helps to analyse cost of different items that are manufactured according to

specification of consumers. With the helps of it value can be added to the organisation because it

helps to determine cost of each and every building constructed by the enterprise.

Benefits of management accounting systems

Management accounting system Benefit

Cost accounting system It is used in Ryder Architecture as it helps to keep track

record of different costs involved in the business

operations.

Inventory management system It is applied within Ryder Architecture because with the

helps of it managers analyse requirements of inventory

for business.

Price optimisation system In Ryder Architecture this system is used to set

appropriate price for the buildings as it helps to meet

client's expectations.

Job costing system This system is used in Ryder Architecture for the

purpose of analysing cost of different activities that are

3

value to the organisation by helping managers to maintaining inventory according to the

requirements.

Price optimisation system: As its name states, it is mainly used to set optimum prices

for all the products that are manufactured by the organisation. It is utilised by Equilibrium Asset

Management which preparing record of Ryder Architecture for the purpose of helping managers

to set appropriate prices for all the buildings sold to customers. It is important and also add value

to the organisation as it helps to analyse that the price which is set by the company for building is

able to meet expectation of customers or not (Smith, 2017).

Job order costing system: It is a system which is used to assign and accumulate cost of

each manufactured unit of organisation. With the help of this system, Equilibrium Asset

Management helps its client Ryder Architecture to assign cost to each and every building

constructed by the enterprise which is going to be sold to customers. It is very important for the

entity as it helps to analyse cost of different items that are manufactured according to

specification of consumers. With the helps of it value can be added to the organisation because it

helps to determine cost of each and every building constructed by the enterprise.

Benefits of management accounting systems

Management accounting system Benefit

Cost accounting system It is used in Ryder Architecture as it helps to keep track

record of different costs involved in the business

operations.

Inventory management system It is applied within Ryder Architecture because with the

helps of it managers analyse requirements of inventory

for business.

Price optimisation system In Ryder Architecture this system is used to set

appropriate price for the buildings as it helps to meet

client's expectations.

Job costing system This system is used in Ryder Architecture for the

purpose of analysing cost of different activities that are

3

performed according to specifications of clients.

P2 Different methods used for management accounting reporting

Management accounting reporting: It can be defined as the process of generating

different management accounting reports which covers different information regarding

organisation's performance. There are different methods of generating them that are used by

Equilibrium Asset Management to form various reports for its client Ryder Architecture.

Characteristics of good information systems:

Reliability: Good information system provide reliable information to the users which

helps them to analyse actual status of the company.

Accuracy: With the help of good information systems accurate data regarding

performance of the organisation can be gathered which can guide stakeholders to form

strategic decisions (Badolato, Donelson and Ege, 2014).

Reasons behind understanding and overall easy to comprehensive of reports: For

consultants in Equilibrium Asset Management, it is very important to generate understandable

and comprehensive reports for Ryder Architecture so that it can guide top executives of

organisation to form strategic decision. Some of the reasons behind it are as follows:

It is vital that the reports obtained from management accounting systems must be

understandable and comprehensive because with the help of it managers can assess actual

status of the organisation.

Management accounting reports guide managers to formulate innovative strategies for

betterment of organisation and if these are not understandable and comprehensive, then it

is not possible for managers to perform this activity.

Different methods of management accounting reporting are described below in detail:

Performance report: This report is mainly generated for the purpose of keeping track

record of performance of all the operations of the company. It is used by Equilibrium Asset

Management for Ryder Architecture so that data regarding employee's and business's

performance can be recorded. It is used within the organisation to provide bonus and incentives

to staff members according to their efforts to accomplish tasks that are allotted to them. This

report is beneficial for the company as it helps to form effective strategies for the company to in

order to enhance its performance (Kaplan and Atkinson, 2015).

4

P2 Different methods used for management accounting reporting

Management accounting reporting: It can be defined as the process of generating

different management accounting reports which covers different information regarding

organisation's performance. There are different methods of generating them that are used by

Equilibrium Asset Management to form various reports for its client Ryder Architecture.

Characteristics of good information systems:

Reliability: Good information system provide reliable information to the users which

helps them to analyse actual status of the company.

Accuracy: With the help of good information systems accurate data regarding

performance of the organisation can be gathered which can guide stakeholders to form

strategic decisions (Badolato, Donelson and Ege, 2014).

Reasons behind understanding and overall easy to comprehensive of reports: For

consultants in Equilibrium Asset Management, it is very important to generate understandable

and comprehensive reports for Ryder Architecture so that it can guide top executives of

organisation to form strategic decision. Some of the reasons behind it are as follows:

It is vital that the reports obtained from management accounting systems must be

understandable and comprehensive because with the help of it managers can assess actual

status of the organisation.

Management accounting reports guide managers to formulate innovative strategies for

betterment of organisation and if these are not understandable and comprehensive, then it

is not possible for managers to perform this activity.

Different methods of management accounting reporting are described below in detail:

Performance report: This report is mainly generated for the purpose of keeping track

record of performance of all the operations of the company. It is used by Equilibrium Asset

Management for Ryder Architecture so that data regarding employee's and business's

performance can be recorded. It is used within the organisation to provide bonus and incentives

to staff members according to their efforts to accomplish tasks that are allotted to them. This

report is beneficial for the company as it helps to form effective strategies for the company to in

order to enhance its performance (Kaplan and Atkinson, 2015).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report: It is an internal report used by entities to assign budget to different

functional and operational department of the organisation. It is used by managers in Equilibrium

Asset Management to compare actual and standard spendings of Ryder Architecture in order to

measure its performance. It is beneficial for the enterprise as it helps to execute all the business

activities in allotted budget. With the help of it, companies can determine that they are able to

meet the projections that were made previously.

Account receivable report: This type of report is created to list owed amount of

different clients. It is mainly generated by such companies that are offering products to the

customers on credit. In Equilibrium Asset Management, it is used by employees to keep track

record of all the outstanding amount of clients of Ryder Architecture. It is beneficial for the

organisation as it helps to determine actual unpaid amount by customers. With the help of it,

enterprise can tighten its credit policies so that situation of late payment from clients can be

ignored.

Inventory management report: Main purpose of this report is to keep track record of

inventory which is kept by manufacturing companies. It is created by Equilibrium Asset

Management for Ryder Architecture so that the organisation can keep track record of material

which is used to construct building for customers. It is advantageous for the entity as it helps to

check status of stock whether it is in warehouse, transit or delivered to clients (Lindholm, Laine

and Suomala, 2017).Integration of management accounting systems and report in

organisation process

There are various management accounting systems and reports that are integrated with

organisational process. Price optimisation system is used by Ryder Architecture for the purpose

of setting appropriate prices for the buildings constructed by it. Accounting receivable reports are

used to tighten credit policies by analysing total owed amount of different clients.

TASK 2

P3 Calculation of cost using different costing techniques

Cost: It is the total amount which is required to be paid by a buyer to the seller of the

product. In order to attract large number of customers, Ryder Architecture set appropriate cost

for all the building constructed by it.

5

functional and operational department of the organisation. It is used by managers in Equilibrium

Asset Management to compare actual and standard spendings of Ryder Architecture in order to

measure its performance. It is beneficial for the enterprise as it helps to execute all the business

activities in allotted budget. With the help of it, companies can determine that they are able to

meet the projections that were made previously.

Account receivable report: This type of report is created to list owed amount of

different clients. It is mainly generated by such companies that are offering products to the

customers on credit. In Equilibrium Asset Management, it is used by employees to keep track

record of all the outstanding amount of clients of Ryder Architecture. It is beneficial for the

organisation as it helps to determine actual unpaid amount by customers. With the help of it,

enterprise can tighten its credit policies so that situation of late payment from clients can be

ignored.

Inventory management report: Main purpose of this report is to keep track record of

inventory which is kept by manufacturing companies. It is created by Equilibrium Asset

Management for Ryder Architecture so that the organisation can keep track record of material

which is used to construct building for customers. It is advantageous for the entity as it helps to

check status of stock whether it is in warehouse, transit or delivered to clients (Lindholm, Laine

and Suomala, 2017).Integration of management accounting systems and report in

organisation process

There are various management accounting systems and reports that are integrated with

organisational process. Price optimisation system is used by Ryder Architecture for the purpose

of setting appropriate prices for the buildings constructed by it. Accounting receivable reports are

used to tighten credit policies by analysing total owed amount of different clients.

TASK 2

P3 Calculation of cost using different costing techniques

Cost: It is the total amount which is required to be paid by a buyer to the seller of the

product. In order to attract large number of customers, Ryder Architecture set appropriate cost

for all the building constructed by it.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are various types of costs that are faced by business entities. All of them are as

follows:

Direct cost: All such type of costs that are directly related to construction of buildings

are known as direct costs. Example of them are depreciation, insurance, salaries to

experts etc.

Indirect cost: All the expenses that are not directly accountable for the construction

activities of the organisation are considered as the part of indirect costs. It includes rent,

office utilities etc.

Cost analysis: It can be defined as the process which is used to measure the benefits of

different actions that are taken by the organisation for the purpose of generating profits. It is also

used in Ryder Architecture for the purpose of analysing that the decisions that were formulated

by the organisation in order to attain long term business objectives.

Cost volume profit: It is a method of cost accounting which is used by managers of

Ryder Architecture for the purpose of analysing impact of changes in cost and volume on

organisational profit.

Flexible budgeting: It is a type of method of formulating budgets in which modifications

or adjustments could be made according to changes in organisation's activities. It is used in

Ryder Architecture for the purpose of making alteration in budget according to varying volume

or cost (Bryson, Crosby and Bloomberg, 2014).

Cost variance: It can be defined as a tool which is used in Ryder Architecture to analyse

different between actual and budgeted cost of construction. It is mainly used in the organisation

for the purpose of formulating strategic decisions.

Marginal costing: In this costing method, cost per unit will always remain same and it

will be divided into fixed and variable. The problem of over and under absorption can be sorted

out with the help of marginal costing. This method is also used by the management in fixing the

price, profit planning, calculating the BEP and other important decisions.

Absorption costing: This method is used for preparing financial records. By using this

method, company presents a clear view of its gross profit and net profit. It helps the

management to allocate the fixed overheads to particular department.

Fixed cost: All the costs that remains constant with the constructed buildings is known as

fixed cost. For Ryder Architecture such type of costs are taxation, interest, insurance etc.

6

follows:

Direct cost: All such type of costs that are directly related to construction of buildings

are known as direct costs. Example of them are depreciation, insurance, salaries to

experts etc.

Indirect cost: All the expenses that are not directly accountable for the construction

activities of the organisation are considered as the part of indirect costs. It includes rent,

office utilities etc.

Cost analysis: It can be defined as the process which is used to measure the benefits of

different actions that are taken by the organisation for the purpose of generating profits. It is also

used in Ryder Architecture for the purpose of analysing that the decisions that were formulated

by the organisation in order to attain long term business objectives.

Cost volume profit: It is a method of cost accounting which is used by managers of

Ryder Architecture for the purpose of analysing impact of changes in cost and volume on

organisational profit.

Flexible budgeting: It is a type of method of formulating budgets in which modifications

or adjustments could be made according to changes in organisation's activities. It is used in

Ryder Architecture for the purpose of making alteration in budget according to varying volume

or cost (Bryson, Crosby and Bloomberg, 2014).

Cost variance: It can be defined as a tool which is used in Ryder Architecture to analyse

different between actual and budgeted cost of construction. It is mainly used in the organisation

for the purpose of formulating strategic decisions.

Marginal costing: In this costing method, cost per unit will always remain same and it

will be divided into fixed and variable. The problem of over and under absorption can be sorted

out with the help of marginal costing. This method is also used by the management in fixing the

price, profit planning, calculating the BEP and other important decisions.

Absorption costing: This method is used for preparing financial records. By using this

method, company presents a clear view of its gross profit and net profit. It helps the

management to allocate the fixed overheads to particular department.

Fixed cost: All the costs that remains constant with the constructed buildings is known as

fixed cost. For Ryder Architecture such type of costs are taxation, interest, insurance etc.

6

Variable cost: The cost which changes with the increment or decrement in the number of

constructed buildings is known as variable cost. Example of such costs for Ryder Architecture

are material, wages for labour etc. (Maas, Schaltegger and Crutzen, 2016).

Cost allocation: It can be defined as the process of identifying, aggregating and

assessing different costs of the company according to different activities. In Ryder Architecture it

is used for the purpose of allocating appropriate costs to all the functional departments.

Standard costing: This costing method is used for recording the variance between actual

costs and standard costs. Within the large organizations, it is difficult to collect the records for all

the activities, so standard costs are used for saving the time.

Normal costing: This method is useful to get the variances between standard and actual

overheads. It is also helpful for the management for an understanding and maintaining the

performance in completing a project (Melnyk and et.al., 2014).

Activity based costing: It can be defined as a costing method which is used in Ryder

Architecture in order to assign cots to different activities performed by the organisation

according to actual expenses which has taken place while performing them.

Role of costing in setting price: Costing helps to set prices for the buildings that are

constructed by Ryder Architecture as with the help of it organisation can determine the actual

costs which has taken place while conducting operations. With the help of it, managers can

analyse costs and then set price for all the buildings.

Inventory cost: All the costs that are related to procurement, management and storage

are known as inventory cost. There are various types of it, which are faced by Ryder Architecture

are as follows:

Ordering cost: The cost which takes place while creating and processing an order to a

supplier of Ryder Architecture is known as ordering cost.

Carrying cost: It is also known as holding cost which is faced by Ryder Architecture

while holding the material in stock.

Shortage cost: When Ryder Architecture do not have any inventory in stock then this

cost takes place.

Benefits of reducing inventory cost:

Reducing inventory cost results in increased profits because the saved amount could be

reinvested in business operations.

7

constructed buildings is known as variable cost. Example of such costs for Ryder Architecture

are material, wages for labour etc. (Maas, Schaltegger and Crutzen, 2016).

Cost allocation: It can be defined as the process of identifying, aggregating and

assessing different costs of the company according to different activities. In Ryder Architecture it

is used for the purpose of allocating appropriate costs to all the functional departments.

Standard costing: This costing method is used for recording the variance between actual

costs and standard costs. Within the large organizations, it is difficult to collect the records for all

the activities, so standard costs are used for saving the time.

Normal costing: This method is useful to get the variances between standard and actual

overheads. It is also helpful for the management for an understanding and maintaining the

performance in completing a project (Melnyk and et.al., 2014).

Activity based costing: It can be defined as a costing method which is used in Ryder

Architecture in order to assign cots to different activities performed by the organisation

according to actual expenses which has taken place while performing them.

Role of costing in setting price: Costing helps to set prices for the buildings that are

constructed by Ryder Architecture as with the help of it organisation can determine the actual

costs which has taken place while conducting operations. With the help of it, managers can

analyse costs and then set price for all the buildings.

Inventory cost: All the costs that are related to procurement, management and storage

are known as inventory cost. There are various types of it, which are faced by Ryder Architecture

are as follows:

Ordering cost: The cost which takes place while creating and processing an order to a

supplier of Ryder Architecture is known as ordering cost.

Carrying cost: It is also known as holding cost which is faced by Ryder Architecture

while holding the material in stock.

Shortage cost: When Ryder Architecture do not have any inventory in stock then this

cost takes place.

Benefits of reducing inventory cost:

Reducing inventory cost results in increased profits because the saved amount could be

reinvested in business operations.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

When inventory cost is reduced by an organisation then it helps to establish competitive

price in the market which helps to attract large number of customers.

Valuation methods:

LIFO: In this type of method recently received material is used for the construction

activities.

FIFO: In this method, earlier received material is used for business operations first.

Ryder Architecture use FIFO method for construction activities (Tucker and Lowe,

2014).

Cost variances: Different types of variances are used for the purpose of determining

difference between actual and budgeted cost of inventory. These are material cost, price, usage

variance etc. With the help of all of them, managers of Ryder Architecture analyse difference

between actual and standard price, cost and usage.

Overhead costs: All the expenses that are faced by Ryder Architecture while

constructing buildings are considered as the part of overhead costs. These are insurance, taxation,

depreciation etc.

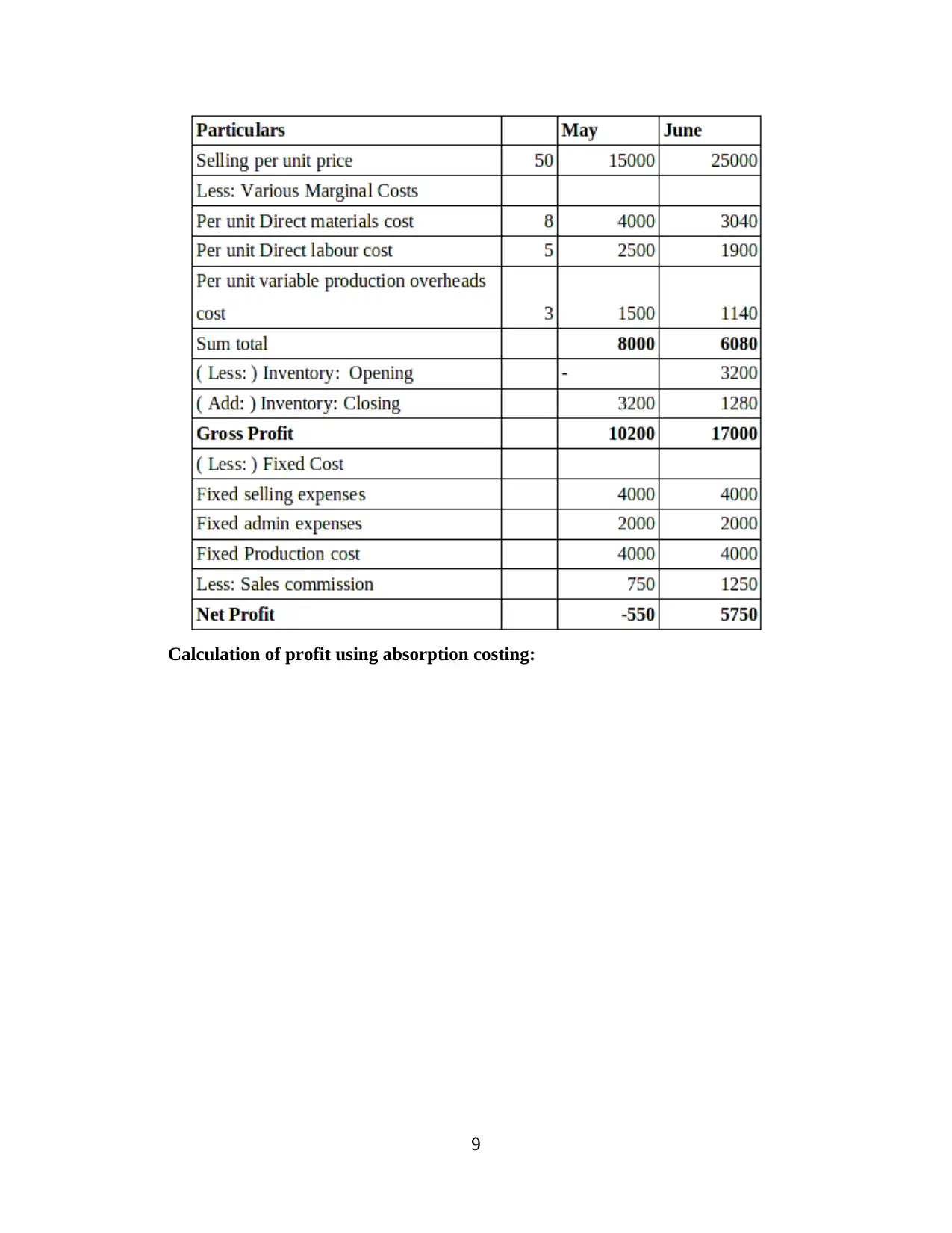

Calculation of profit using marginal costing:

8

price in the market which helps to attract large number of customers.

Valuation methods:

LIFO: In this type of method recently received material is used for the construction

activities.

FIFO: In this method, earlier received material is used for business operations first.

Ryder Architecture use FIFO method for construction activities (Tucker and Lowe,

2014).

Cost variances: Different types of variances are used for the purpose of determining

difference between actual and budgeted cost of inventory. These are material cost, price, usage

variance etc. With the help of all of them, managers of Ryder Architecture analyse difference

between actual and standard price, cost and usage.

Overhead costs: All the expenses that are faced by Ryder Architecture while

constructing buildings are considered as the part of overhead costs. These are insurance, taxation,

depreciation etc.

Calculation of profit using marginal costing:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

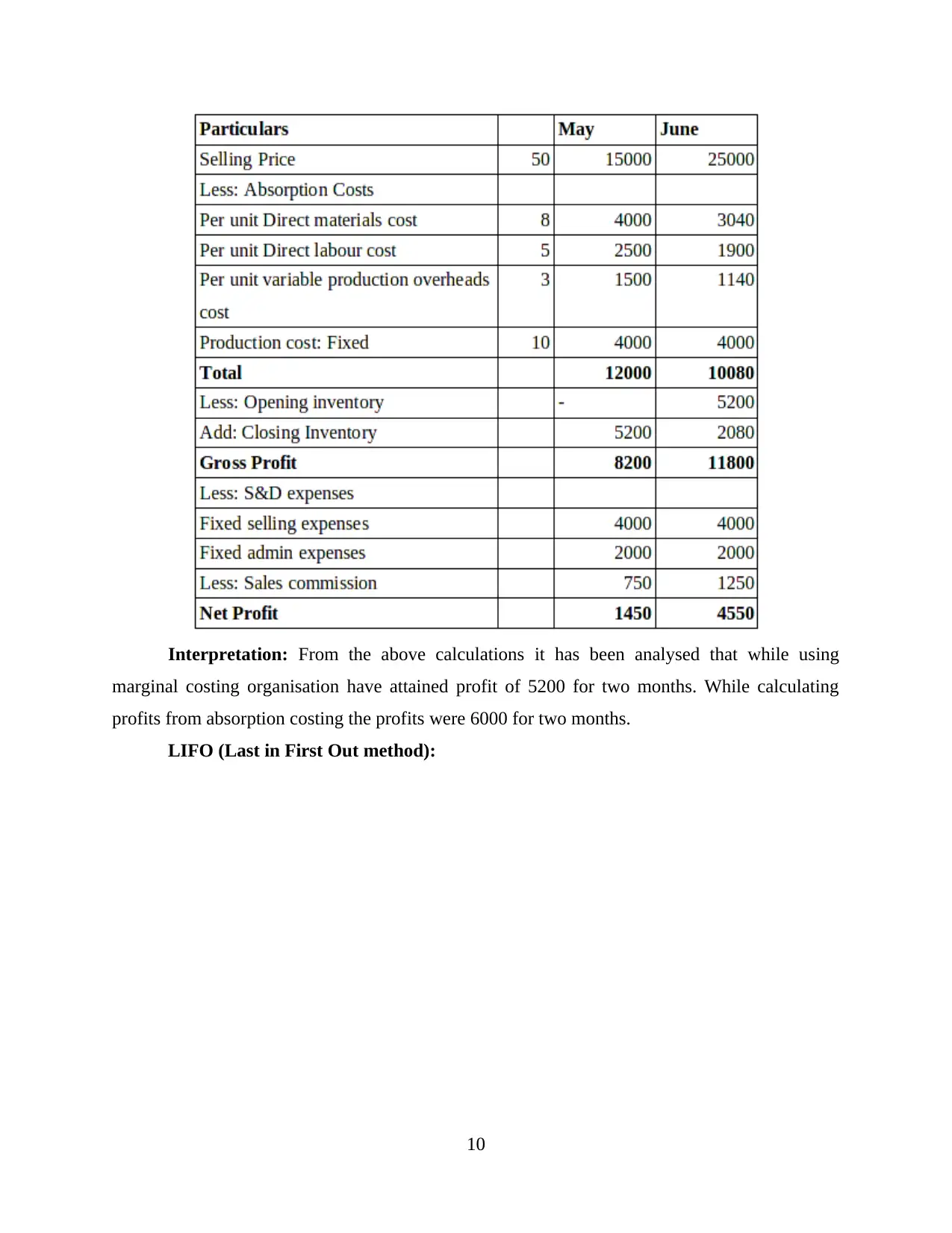

Calculation of profit using absorption costing:

9

9

Interpretation: From the above calculations it has been analysed that while using

marginal costing organisation have attained profit of 5200 for two months. While calculating

profits from absorption costing the profits were 6000 for two months.

LIFO (Last in First Out method):

10

marginal costing organisation have attained profit of 5200 for two months. While calculating

profits from absorption costing the profits were 6000 for two months.

LIFO (Last in First Out method):

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.