Management Accounting Systems and Techniques Report for XYZ Ltd

VerifiedAdded on 2023/01/04

|19

|4394

|39

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques, focusing on their application within XYZ Ltd, a manufacturing industry. It defines management accounting, differentiating it from financial accounting, and details various systems like cost management, price optimization, inventory management, and job costing. The report further examines the benefits of these systems and the importance of aligning management accounting reporting with the overall business goals. It delves into specific techniques such as marginal and absorption costing, presenting related statements and analyses. The report also explores the use of planning tools, including their advantages and disadvantages, and their relevance in budgeting and forecasting, as well as methods for addressing financial problems and ensuring sustainable success.

Management Accounting Systems &

Techniques

Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Definition of management accounting and explanation of various system of this technique 1

P2 About managing accounting report........................................................................................1

M1 Benefits of management accounting system.........................................................................1

D1 Importance of alignment of management accounting reporting with system........................2

TASK 2........................................................................................................................................2

P3 Marginal costing and absorption costing statement...............................................................2

M2 Range of management accounting techniques......................................................................2

D2 Financial report which define management accounting techniques......................................2

TASK 3........................................................................................................................................2

P4 Planning tools and its advantage as well as disadvantage......................................................2

M3 Brief explanation of management accounting planning tools and its relevance in budgeting

forecasting....................................................................................................................................3

TASK 4........................................................................................................................................3

Explanation of financial problem and techniques use for solve this issue..................................3

M4 Use of management accounting tool for responding financial issue.....................................3

D3 Evaluation of how planning tools for accounting respond appropriately to solving

financial problems to lead organisations to sustainable success.................................................3

CONCLUSION................................................................................................................................3

REFRENCES...................................................................................................................................3

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Definition of management accounting and explanation of various system of this technique 1

P2 About managing accounting report........................................................................................1

M1 Benefits of management accounting system.........................................................................1

D1 Importance of alignment of management accounting reporting with system........................2

TASK 2........................................................................................................................................2

P3 Marginal costing and absorption costing statement...............................................................2

M2 Range of management accounting techniques......................................................................2

D2 Financial report which define management accounting techniques......................................2

TASK 3........................................................................................................................................2

P4 Planning tools and its advantage as well as disadvantage......................................................2

M3 Brief explanation of management accounting planning tools and its relevance in budgeting

forecasting....................................................................................................................................3

TASK 4........................................................................................................................................3

Explanation of financial problem and techniques use for solve this issue..................................3

M4 Use of management accounting tool for responding financial issue.....................................3

D3 Evaluation of how planning tools for accounting respond appropriately to solving

financial problems to lead organisations to sustainable success.................................................3

CONCLUSION................................................................................................................................3

REFRENCES...................................................................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting this term is used to provide accounting information in systematic

way which help in taken future business decision. To understand this concept XYZ limited has

been taken it is a manufacturing industry. This report has been contain specific information

regarding relevance of various Management Accounting system and their use of former dating of

accounting reports it is a country in usefulness of marginal as well as absorption costing method

to calculate the value of profit and cost this report also define use of planning tool for taking

business decisions as well as various methods which help in overcoming financial problem.

TASK 1

P1 Definition of management accounting and explanation of various system of this technique

Management accounting: Accounting it is essential part of every business organisation.

On the basis of using techniques in system of accounting business organisation able to record

their transaction related with business activities Management Accounting is a part of accounting

this term has been combination of two words one is management and the other one is accounting

the term management define planning organising running controlling and monitoring business

activities and on the other hand accounting is the procedure of recording collecting and represent

entering financial transaction for relevant stakeholders (Fiondella, Macchioni, Maffei, and

Spanò, 2016).

Management Accounting is the procedure which help in represent information in

systematically wave which help in attending business objective within given time period this is

useful for take decisions there will be various branches of accounting financial branch is also

important.

Difference between financial and management accounting

Financial accounting Management accounting

Financial accounting is related with recording

transaction which only affected by cash related

transaction.

Management Accounting on the other side

record cash as well as other than cash

transactions for example depreciation and

amortization and adjustment of intangible

assets.

Main purpose of financial accounting is Information relevant regarding with

1

Management Accounting this term is used to provide accounting information in systematic

way which help in taken future business decision. To understand this concept XYZ limited has

been taken it is a manufacturing industry. This report has been contain specific information

regarding relevance of various Management Accounting system and their use of former dating of

accounting reports it is a country in usefulness of marginal as well as absorption costing method

to calculate the value of profit and cost this report also define use of planning tool for taking

business decisions as well as various methods which help in overcoming financial problem.

TASK 1

P1 Definition of management accounting and explanation of various system of this technique

Management accounting: Accounting it is essential part of every business organisation.

On the basis of using techniques in system of accounting business organisation able to record

their transaction related with business activities Management Accounting is a part of accounting

this term has been combination of two words one is management and the other one is accounting

the term management define planning organising running controlling and monitoring business

activities and on the other hand accounting is the procedure of recording collecting and represent

entering financial transaction for relevant stakeholders (Fiondella, Macchioni, Maffei, and

Spanò, 2016).

Management Accounting is the procedure which help in represent information in

systematically wave which help in attending business objective within given time period this is

useful for take decisions there will be various branches of accounting financial branch is also

important.

Difference between financial and management accounting

Financial accounting Management accounting

Financial accounting is related with recording

transaction which only affected by cash related

transaction.

Management Accounting on the other side

record cash as well as other than cash

transactions for example depreciation and

amortization and adjustment of intangible

assets.

Main purpose of financial accounting is Information relevant regarding with

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

providing information to external stakeholders. Management Accounting for internal users.

It is essential as per the accounting standards to

formulate financial statement at the year

ending on the basis of that manager able to

recognise their off energy performance.

It is not required to formulate Management

Accounting statement and use management

Accounting techniques for organisation.

Financial accounting is useful for managing

cash assets.

Management department use this technique for

take decision and control their cost.

There will be various type of system which is used by organisation to record their transaction

management department of XYZ Limited following systems.

Cost management system: This system is used by organisation to recognise cost of each unit

there will be various type of techniques which is implementing and related with Management

Accounting it in Cruise absorption costing standard costing SLS marginal costing by using this

technique management department able to understand relevance cost as well as those transaction

which may become the reason of generating higher cost. These tools directly impacted any

useful for take decision regarding these formulation policies of maximum minimises station of

cost.

Price optimization system: This system is useful to formulate policies related with price it is

considered as most essential at the moment which help in generating of profit by formulating

policies regarding with prise organisation able change. Price related policies there will be various

type of policies regarding with prize which included price skimming price discounting

penetration pricing policies different kind of strategies for calculating a price on the basis of

applying particular strategy organisation able to take their decisions it will help in satisfying

customer with attaining goal of organisation within a given time period by generating revenues

Inventory management system: This is also essential tool of Management Accounting

inventory is the most essential tool for organisation managing stock isn't ask for organisations as

it will be useful in minimising cost related with maintaining of stocks and effectively manage

stock within a given time period there will be various type of methods and technologies which is

used to maintain balance of inventory which include ABC analysis as well as other stock

management technique by applying LIFO,FIFO, method organisation formulate policies and able

to recognise number of maximum as well as minimum level required for relevant organisation

2

It is essential as per the accounting standards to

formulate financial statement at the year

ending on the basis of that manager able to

recognise their off energy performance.

It is not required to formulate Management

Accounting statement and use management

Accounting techniques for organisation.

Financial accounting is useful for managing

cash assets.

Management department use this technique for

take decision and control their cost.

There will be various type of system which is used by organisation to record their transaction

management department of XYZ Limited following systems.

Cost management system: This system is used by organisation to recognise cost of each unit

there will be various type of techniques which is implementing and related with Management

Accounting it in Cruise absorption costing standard costing SLS marginal costing by using this

technique management department able to understand relevance cost as well as those transaction

which may become the reason of generating higher cost. These tools directly impacted any

useful for take decision regarding these formulation policies of maximum minimises station of

cost.

Price optimization system: This system is useful to formulate policies related with price it is

considered as most essential at the moment which help in generating of profit by formulating

policies regarding with prise organisation able change. Price related policies there will be various

type of policies regarding with prize which included price skimming price discounting

penetration pricing policies different kind of strategies for calculating a price on the basis of

applying particular strategy organisation able to take their decisions it will help in satisfying

customer with attaining goal of organisation within a given time period by generating revenues

Inventory management system: This is also essential tool of Management Accounting

inventory is the most essential tool for organisation managing stock isn't ask for organisations as

it will be useful in minimising cost related with maintaining of stocks and effectively manage

stock within a given time period there will be various type of methods and technologies which is

used to maintain balance of inventory which include ABC analysis as well as other stock

management technique by applying LIFO,FIFO, method organisation formulate policies and able

to recognise number of maximum as well as minimum level required for relevant organisation

2

stock is essential part of organisation that by using Management Accounting business

cooperation able to sustainability e manage their inventory

Job costing system: this is term is implemented by organisation to recognise value and cause

realise for running particular business activities on the basis of activities recorded from

customers business organisation record order of their job this will help in in managing inventory

as well as record jobs system in effective for efficient way bi formulating job costing system

organisation able to have base regarding with formulation of report and take decisions regarding

with job costing.

P2 About managing accounting report

Budgetary report: This will also useful for formulating policies regarding with future business

decisions on the basis of that manager take decision which project is beneficial for them by

calculating cost of each alternative.

Inventory management report: Inventory report this report has been formulated to record or the

information related with maximum minimum and normal level of stock required this report

contains all the essential information regarding with each month and use of various technique for

maintain stock management and its balance on the basis of formulation of this report

management department of exaggerate Limited able to recognise the number of customer.

Performance report: Performance report this report has been formulated for or collect

information with each department on the basis of that manageable to recognise performance

within a given time period every department which include sales marketing finance as well as

manufacturing and production department it is very essential to formulating performance Report

as on the basis of that management department take decision regarding formulating of policies

for providing reward promotion as well as given recognition on the basis of performance and

skills of human resources (Alabdullah, 2019).

Cost report: Cost report this report has been formulated by data collection from cost accounting

system various statement has been useful for formulating the report cost is essential element does

it is really required to formulate the port which define each cost element as well as impact of

various business activities related with quotes on the basis of formulating cost record

management department of XYZ able to recognise all those activities which may become the

reason of generating risk regarding with hi cash outflows.

3

cooperation able to sustainability e manage their inventory

Job costing system: this is term is implemented by organisation to recognise value and cause

realise for running particular business activities on the basis of activities recorded from

customers business organisation record order of their job this will help in in managing inventory

as well as record jobs system in effective for efficient way bi formulating job costing system

organisation able to have base regarding with formulation of report and take decisions regarding

with job costing.

P2 About managing accounting report

Budgetary report: This will also useful for formulating policies regarding with future business

decisions on the basis of that manager take decision which project is beneficial for them by

calculating cost of each alternative.

Inventory management report: Inventory report this report has been formulated to record or the

information related with maximum minimum and normal level of stock required this report

contains all the essential information regarding with each month and use of various technique for

maintain stock management and its balance on the basis of formulation of this report

management department of exaggerate Limited able to recognise the number of customer.

Performance report: Performance report this report has been formulated for or collect

information with each department on the basis of that manageable to recognise performance

within a given time period every department which include sales marketing finance as well as

manufacturing and production department it is very essential to formulating performance Report

as on the basis of that management department take decision regarding formulating of policies

for providing reward promotion as well as given recognition on the basis of performance and

skills of human resources (Alabdullah, 2019).

Cost report: Cost report this report has been formulated by data collection from cost accounting

system various statement has been useful for formulating the report cost is essential element does

it is really required to formulate the port which define each cost element as well as impact of

various business activities related with quotes on the basis of formulating cost record

management department of XYZ able to recognise all those activities which may become the

reason of generating risk regarding with hi cash outflows.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Account receivables report: Account receivable report this report useful in maintaining balance

between amount received from debtors as there are various customer which are not able to fulfil

their death reliability for given time period these type of debtors considered and non performing

assets it is very essential for our organisation to formulate policies and report on the basis of that

they can able to recognise number of customer which may consider as non performing asset

management department of XYZ use accounts receivable report for recognise these type of

customer and on the basis of that they formulate policies which help in in controlling and reduce

the number of nonperforming assets by providing offer which influence customer to pay their

cash reliability with given time period.

M1 Benefits of management accounting system

Particular Management accounting system’s benefits

Job costing system By using job costing system organisation able

to recognise value of the Year each order cost

per unit and time required for converting raw

material into finished good and delivering

order as well as record all this transaction

which help in recording systematic manner

this is useful in measurement of performance.

Cost management system XYZ Limited use cost management system

with through which they can evaluate cost for

running their business activities as well as

identify those business activities which may

become the reason of generating high cost

(Alyousef, and Mickan, 2016).

Inventory management system Xyz Limited using various techniques which

help in managing their stock as well as

recording is level of the stock this will help in

measuring value of stock as well as

controlling and minimising their cost effective

and systematic manner. Level of stock which

4

between amount received from debtors as there are various customer which are not able to fulfil

their death reliability for given time period these type of debtors considered and non performing

assets it is very essential for our organisation to formulate policies and report on the basis of that

they can able to recognise number of customer which may consider as non performing asset

management department of XYZ use accounts receivable report for recognise these type of

customer and on the basis of that they formulate policies which help in in controlling and reduce

the number of nonperforming assets by providing offer which influence customer to pay their

cash reliability with given time period.

M1 Benefits of management accounting system

Particular Management accounting system’s benefits

Job costing system By using job costing system organisation able

to recognise value of the Year each order cost

per unit and time required for converting raw

material into finished good and delivering

order as well as record all this transaction

which help in recording systematic manner

this is useful in measurement of performance.

Cost management system XYZ Limited use cost management system

with through which they can evaluate cost for

running their business activities as well as

identify those business activities which may

become the reason of generating high cost

(Alyousef, and Mickan, 2016).

Inventory management system Xyz Limited using various techniques which

help in managing their stock as well as

recording is level of the stock this will help in

measuring value of stock as well as

controlling and minimising their cost effective

and systematic manner. Level of stock which

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

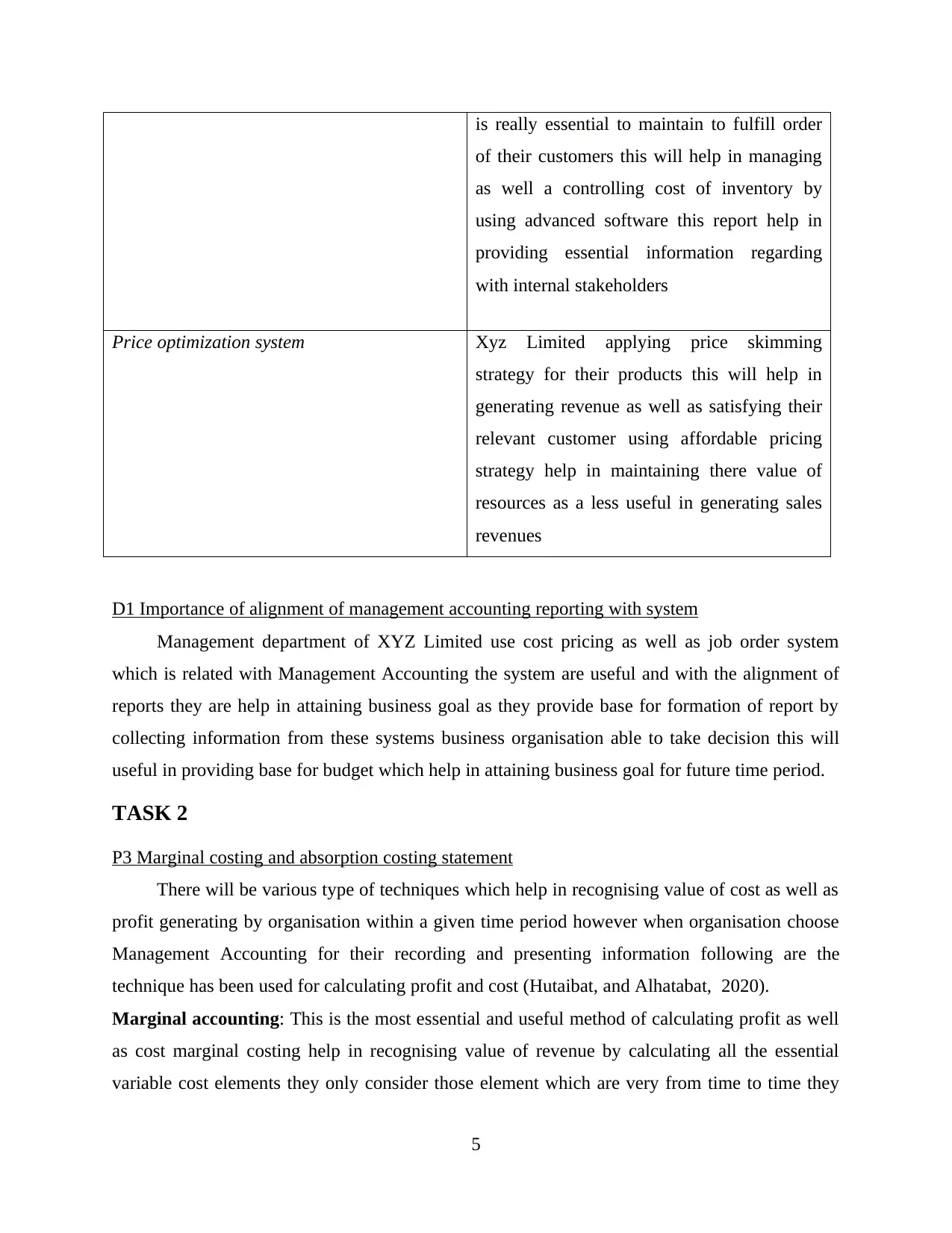

is really essential to maintain to fulfill order

of their customers this will help in managing

as well a controlling cost of inventory by

using advanced software this report help in

providing essential information regarding

with internal stakeholders

Price optimization system Xyz Limited applying price skimming

strategy for their products this will help in

generating revenue as well as satisfying their

relevant customer using affordable pricing

strategy help in maintaining there value of

resources as a less useful in generating sales

revenues

D1 Importance of alignment of management accounting reporting with system

Management department of XYZ Limited use cost pricing as well as job order system

which is related with Management Accounting the system are useful and with the alignment of

reports they are help in attaining business goal as they provide base for formation of report by

collecting information from these systems business organisation able to take decision this will

useful in providing base for budget which help in attaining business goal for future time period.

TASK 2

P3 Marginal costing and absorption costing statement

There will be various type of techniques which help in recognising value of cost as well as

profit generating by organisation within a given time period however when organisation choose

Management Accounting for their recording and presenting information following are the

technique has been used for calculating profit and cost (Hutaibat, and Alhatabat, 2020).

Marginal accounting: This is the most essential and useful method of calculating profit as well

as cost marginal costing help in recognising value of revenue by calculating all the essential

variable cost elements they only consider those element which are very from time to time they

5

of their customers this will help in managing

as well a controlling cost of inventory by

using advanced software this report help in

providing essential information regarding

with internal stakeholders

Price optimization system Xyz Limited applying price skimming

strategy for their products this will help in

generating revenue as well as satisfying their

relevant customer using affordable pricing

strategy help in maintaining there value of

resources as a less useful in generating sales

revenues

D1 Importance of alignment of management accounting reporting with system

Management department of XYZ Limited use cost pricing as well as job order system

which is related with Management Accounting the system are useful and with the alignment of

reports they are help in attaining business goal as they provide base for formation of report by

collecting information from these systems business organisation able to take decision this will

useful in providing base for budget which help in attaining business goal for future time period.

TASK 2

P3 Marginal costing and absorption costing statement

There will be various type of techniques which help in recognising value of cost as well as

profit generating by organisation within a given time period however when organisation choose

Management Accounting for their recording and presenting information following are the

technique has been used for calculating profit and cost (Hutaibat, and Alhatabat, 2020).

Marginal accounting: This is the most essential and useful method of calculating profit as well

as cost marginal costing help in recognising value of revenue by calculating all the essential

variable cost elements they only consider those element which are very from time to time they

5

are not consider fixed elements does it is also known as variable cost accounting by applying

marginal costing and provide base to evaluate value of break even analysis as well as value of

margin of safety which directly impact on and give information regarding how these tools are

relatable with each item of income statement

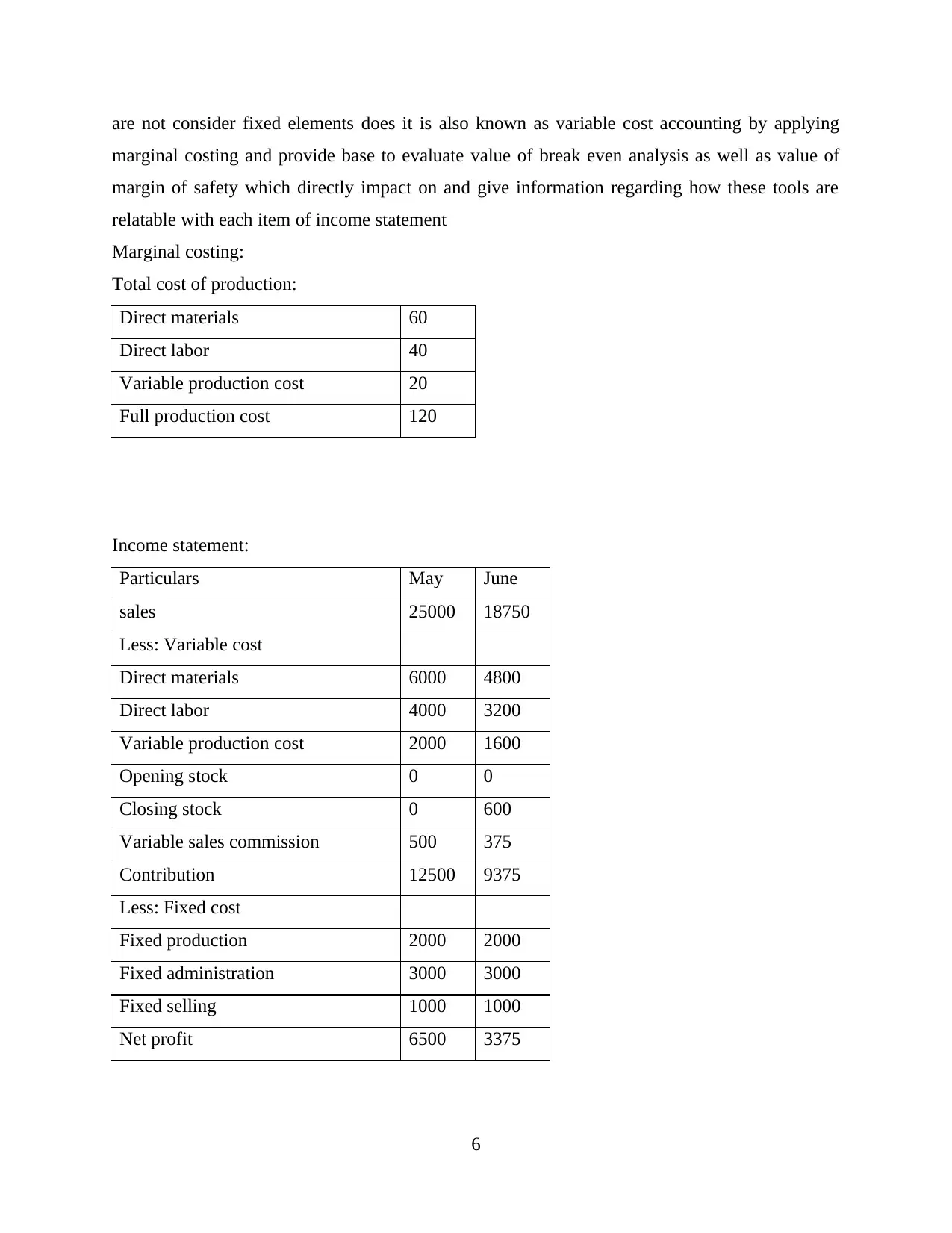

Marginal costing:

Total cost of production:

Direct materials 60

Direct labor 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labor 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

6

marginal costing and provide base to evaluate value of break even analysis as well as value of

margin of safety which directly impact on and give information regarding how these tools are

relatable with each item of income statement

Marginal costing:

Total cost of production:

Direct materials 60

Direct labor 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labor 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

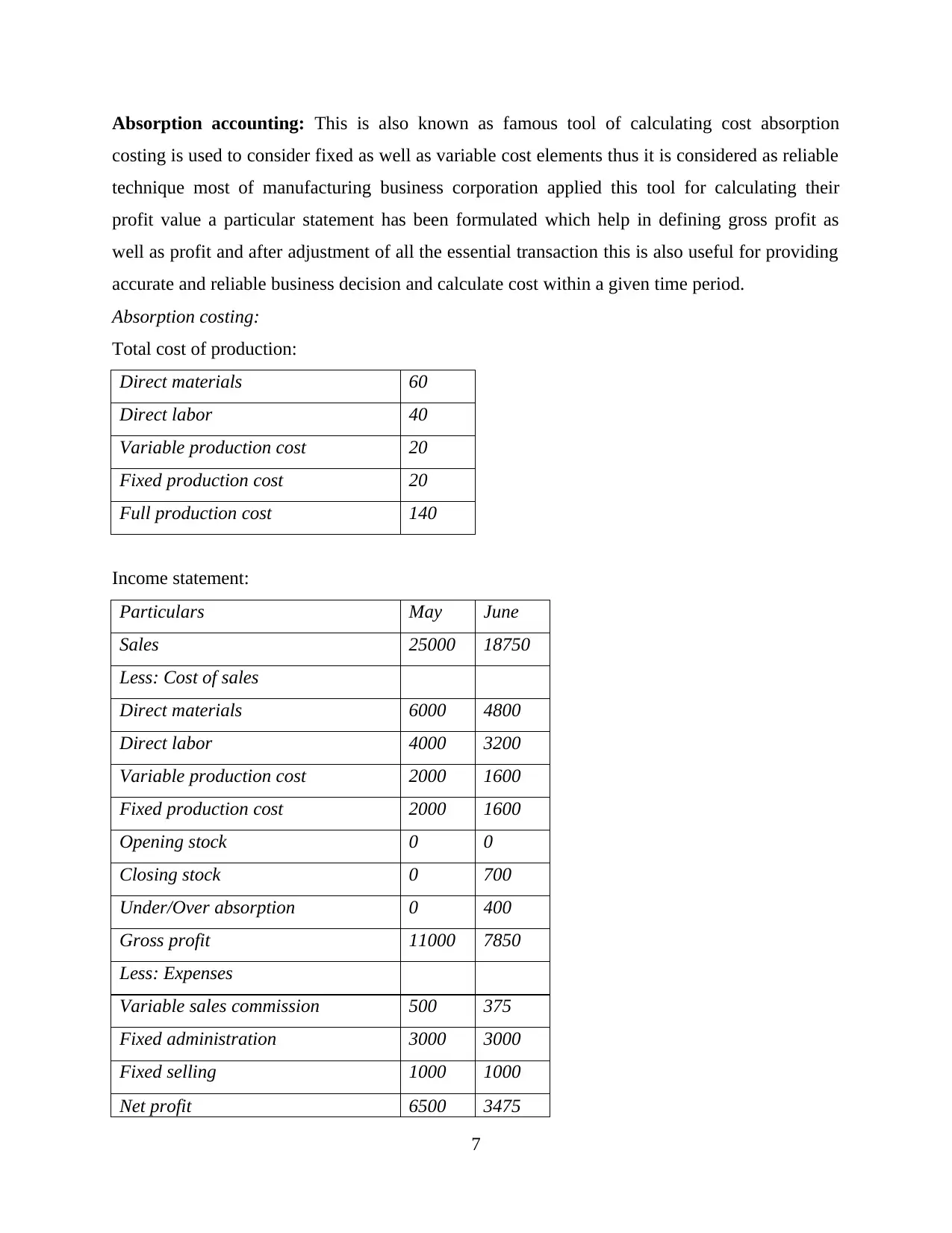

Absorption accounting: This is also known as famous tool of calculating cost absorption

costing is used to consider fixed as well as variable cost elements thus it is considered as reliable

technique most of manufacturing business corporation applied this tool for calculating their

profit value a particular statement has been formulated which help in defining gross profit as

well as profit and after adjustment of all the essential transaction this is also useful for providing

accurate and reliable business decision and calculate cost within a given time period.

Absorption costing:

Total cost of production:

Direct materials 60

Direct labor 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labor 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

7

costing is used to consider fixed as well as variable cost elements thus it is considered as reliable

technique most of manufacturing business corporation applied this tool for calculating their

profit value a particular statement has been formulated which help in defining gross profit as

well as profit and after adjustment of all the essential transaction this is also useful for providing

accurate and reliable business decision and calculate cost within a given time period.

Absorption costing:

Total cost of production:

Direct materials 60

Direct labor 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labor 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

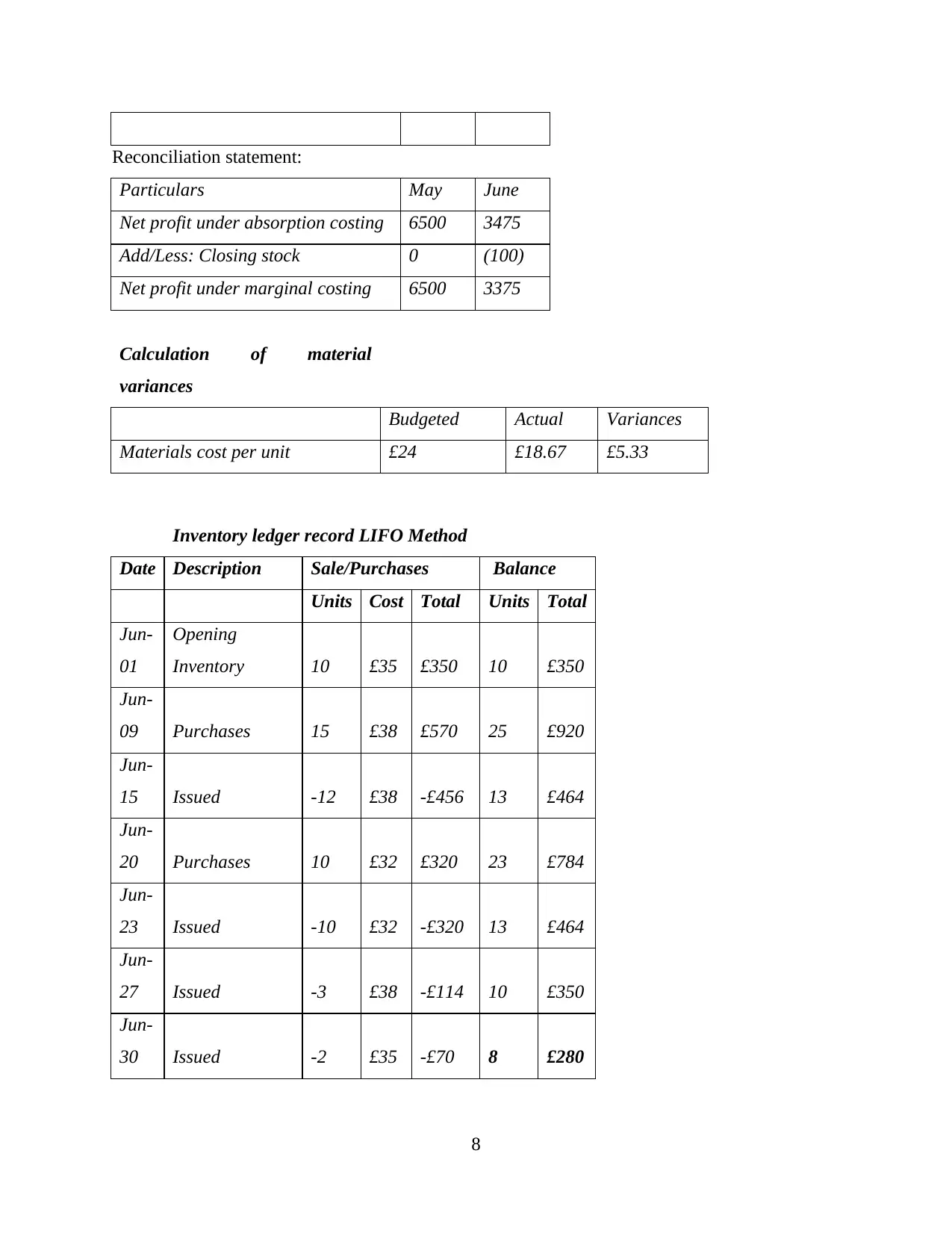

Reconciliation statement:

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Date Description Sale/Purchases Balance

Units Cost Total Units Total

Jun-

01

Opening

Inventory 10 £35 £350 10 £350

Jun-

09 Purchases 15 £38 £570 25 £920

Jun-

15 Issued -12 £38 -£456 13 £464

Jun-

20 Purchases 10 £32 £320 23 £784

Jun-

23 Issued -10 £32 -£320 13 £464

Jun-

27 Issued -3 £38 -£114 10 £350

Jun-

30 Issued -2 £35 -£70 8 £280

8

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Date Description Sale/Purchases Balance

Units Cost Total Units Total

Jun-

01

Opening

Inventory 10 £35 £350 10 £350

Jun-

09 Purchases 15 £38 £570 25 £920

Jun-

15 Issued -12 £38 -£456 13 £464

Jun-

20 Purchases 10 £32 £320 23 £784

Jun-

23 Issued -10 £32 -£320 13 £464

Jun-

27 Issued -3 £38 -£114 10 £350

Jun-

30 Issued -2 £35 -£70 8 £280

8

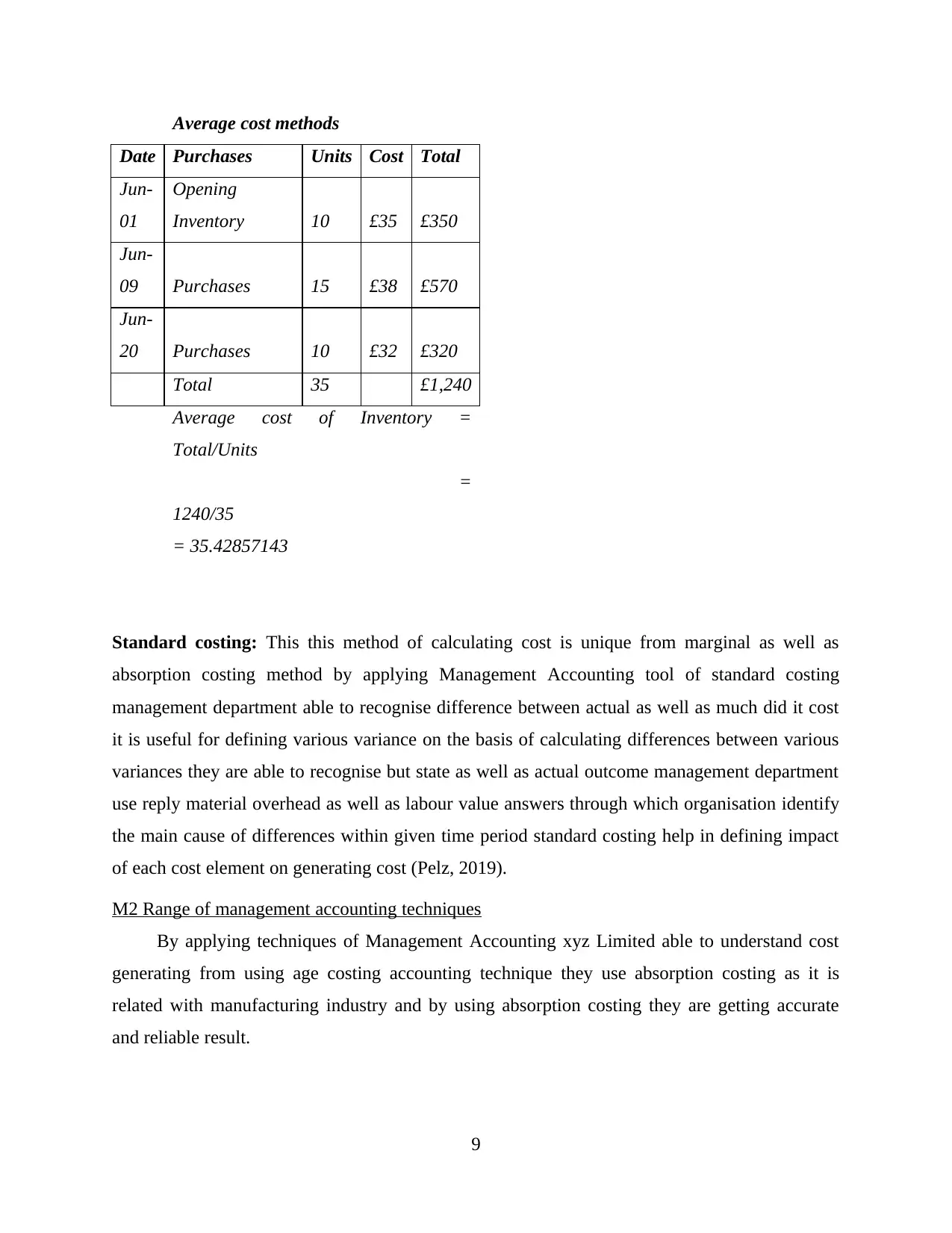

Average cost methods

Date Purchases Units Cost Total

Jun-

01

Opening

Inventory 10 £35 £350

Jun-

09 Purchases 15 £38 £570

Jun-

20 Purchases 10 £32 £320

Total 35 £1,240

Average cost of Inventory =

Total/Units

=

1240/35

= 35.42857143

Standard costing: This this method of calculating cost is unique from marginal as well as

absorption costing method by applying Management Accounting tool of standard costing

management department able to recognise difference between actual as well as much did it cost

it is useful for defining various variance on the basis of calculating differences between various

variances they are able to recognise but state as well as actual outcome management department

use reply material overhead as well as labour value answers through which organisation identify

the main cause of differences within given time period standard costing help in defining impact

of each cost element on generating cost (Pelz, 2019).

M2 Range of management accounting techniques

By applying techniques of Management Accounting xyz Limited able to understand cost

generating from using age costing accounting technique they use absorption costing as it is

related with manufacturing industry and by using absorption costing they are getting accurate

and reliable result.

9

Date Purchases Units Cost Total

Jun-

01

Opening

Inventory 10 £35 £350

Jun-

09 Purchases 15 £38 £570

Jun-

20 Purchases 10 £32 £320

Total 35 £1,240

Average cost of Inventory =

Total/Units

=

1240/35

= 35.42857143

Standard costing: This this method of calculating cost is unique from marginal as well as

absorption costing method by applying Management Accounting tool of standard costing

management department able to recognise difference between actual as well as much did it cost

it is useful for defining various variance on the basis of calculating differences between various

variances they are able to recognise but state as well as actual outcome management department

use reply material overhead as well as labour value answers through which organisation identify

the main cause of differences within given time period standard costing help in defining impact

of each cost element on generating cost (Pelz, 2019).

M2 Range of management accounting techniques

By applying techniques of Management Accounting xyz Limited able to understand cost

generating from using age costing accounting technique they use absorption costing as it is

related with manufacturing industry and by using absorption costing they are getting accurate

and reliable result.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.