Management Accounting Report: Financial Analysis and Reporting

VerifiedAdded on 2020/01/07

|17

|5565

|121

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its principles, types, and practical applications within the context of Apis Limited, a hospitality industry firm. The report begins by defining management accounting and differentiating it from financial accounting, emphasizing its role in internal decision-making and financial planning. It then explores various management accounting systems, including cost accounting, job costing, batch costing, inventory management, and price optimization. The report also examines different methods used for management accounting reporting, such as make-or-buy decisions, Just-in-Time (JIT) inventory management, and Activity-Based Costing (ABC). Furthermore, it delves into the advantages and disadvantages of budgetary control planning tools and compares how organizations can use management accounting to address financial challenges. The report concludes by summarizing the benefits of management accounting, including reduced expenses, increased financial returns, and improved decision-making processes, and highlights the importance of financial analysis and interpretation. The report emphasizes the importance of financial planning, cost control, and the use of financial data to improve business performance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK1.............................................................................................................................................3

P1 Explain management accounting and their different types of management accounting

systems........................................................................................................................................3

P2 Explain different methods used for management accounting reporting ...............................5

P3 Prepare an income statement using marginal and absorption costs.......................................7

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of budgetary control planning tools...................................11

P5 Comparison between how organisation could use management accounting so as to respond

to problems related to finance...................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES .............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK1.............................................................................................................................................3

P1 Explain management accounting and their different types of management accounting

systems........................................................................................................................................3

P2 Explain different methods used for management accounting reporting ...............................5

P3 Prepare an income statement using marginal and absorption costs.......................................7

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of budgetary control planning tools...................................11

P5 Comparison between how organisation could use management accounting so as to respond

to problems related to finance...................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES .............................................................................................................................17

INTRODUCTION

Management accounting is a process that is used by the management in order to identify

and present the financial information in an efficient manner. On the basis of this data, manager

can make their plans and can take decisions so that they can achieve profits. This is more useful

for the internal manager and executives as through this they can control their expenses. The top

management can use this information in order to forecast the data on the basis of the past

information (Brosel, Toll and Zimmermann, 2012). Through this, they will be able to improve

their growth and brand position in the market. The present report is based on Apis Limited which

perform their operations in hospitality industry. They are focusing on their business activities so

that their overall performance can be improved in an efficient manner. In this context, report

explains the different types of management accounting system and methods that are used in order

to manage the overall accounting system. Along with this, it explains the cost techniques that are

used to prepare to income statement. The advantages and disadvantages of the different planning

control techniques and budgetary control are explained in detail.

TASK1

P1 Explain management accounting and their different types of management accounting systems

Management accounting refers to preparing or managing accounts, that provides straight

and timely financial content to the managers. It is helpful for them to take short term and day to

day decisions. Although management accounting, also provides annual reports to the external

stakeholders. Apis Ltd. also prefer to use to managerial accounts and financial reports. These

reports are related with sales revenue, available cash in organisation, accounts receivable,

accounts payable, outstanding debts, raw material; amounts of others in hand and inventory. It

engaged with the planning of information that is helpful to the managers in planning and

controlling their business operation's. It is also accommodating for those only peoples who are

involved in decision making process (Briciu, Groza and Ganfalean, 2009). Apis Ltd. Industry

mostly uses management accounting system to meet requirements of managers regarding with

financial reports and data. It is an internal function of any business and which is responsible for

reporting and collecting any financial information.

It is a activity of presentation, analyse and interpretation of financial information in order

to assist the process of management as daily operations, policy creation and decision making.

Management accounting is a process that is used by the management in order to identify

and present the financial information in an efficient manner. On the basis of this data, manager

can make their plans and can take decisions so that they can achieve profits. This is more useful

for the internal manager and executives as through this they can control their expenses. The top

management can use this information in order to forecast the data on the basis of the past

information (Brosel, Toll and Zimmermann, 2012). Through this, they will be able to improve

their growth and brand position in the market. The present report is based on Apis Limited which

perform their operations in hospitality industry. They are focusing on their business activities so

that their overall performance can be improved in an efficient manner. In this context, report

explains the different types of management accounting system and methods that are used in order

to manage the overall accounting system. Along with this, it explains the cost techniques that are

used to prepare to income statement. The advantages and disadvantages of the different planning

control techniques and budgetary control are explained in detail.

TASK1

P1 Explain management accounting and their different types of management accounting systems

Management accounting refers to preparing or managing accounts, that provides straight

and timely financial content to the managers. It is helpful for them to take short term and day to

day decisions. Although management accounting, also provides annual reports to the external

stakeholders. Apis Ltd. also prefer to use to managerial accounts and financial reports. These

reports are related with sales revenue, available cash in organisation, accounts receivable,

accounts payable, outstanding debts, raw material; amounts of others in hand and inventory. It

engaged with the planning of information that is helpful to the managers in planning and

controlling their business operation's. It is also accommodating for those only peoples who are

involved in decision making process (Briciu, Groza and Ganfalean, 2009). Apis Ltd. Industry

mostly uses management accounting system to meet requirements of managers regarding with

financial reports and data. It is an internal function of any business and which is responsible for

reporting and collecting any financial information.

It is a activity of presentation, analyse and interpretation of financial information in order

to assist the process of management as daily operations, policy creation and decision making.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The objective of management accounting is allocation of resource and analyse the risk in order to

exploit the risk. It is also helpful in measuring performance of employees and measurement of

efficiency of employees. Management accounts also lean in providing content about execution

that is more often than financial accounts (Michalski, 2012). So management accounting is

based on cost and financial accounting. Management accounting is system of financial

statements through ration analysis. The main of management accounting is financial planning of

each and every activity that is related with economic resources of the business. There are

different types of management accounting; - Cost accounting system: A cost accounting system is tool which is used to assess the cost

of the product in order to make the profits in a most optimum manner. However, there is

no such tool which can be used to ascertain the appropriate cost, but by applying the cost

accounting system, company could attain the idea to reduce the cost of a product. Now,

there is a strong need to know about the product cost in order to make the product

profitable. Job costing system: Under this costing technique, there is need to know the

manufacturing costs individually for each job. This technique is useful for the firms

which are engaged in the manufacturing process. Batch costing system: this is the technique which is used like job costing technique. It is

a kind of specific order costing technique. Under Each batch, there are so many units are

covered. So, there is need to assess the total cost of the batch. Inventory management system: This system is used to know the inventory levels, orders

and deliveries. This is the system which is used to assess the stock and manage

accordingly.

Price optimisation system: This is the system which is used to identify about the

consumer’s reaction at different at the various prices of the products or services.

P2 Explain different methods used for management accounting reporting:

These methods are regulating by Apis ltd. In management accounting process. They are

such as follow: -

exploit the risk. It is also helpful in measuring performance of employees and measurement of

efficiency of employees. Management accounts also lean in providing content about execution

that is more often than financial accounts (Michalski, 2012). So management accounting is

based on cost and financial accounting. Management accounting is system of financial

statements through ration analysis. The main of management accounting is financial planning of

each and every activity that is related with economic resources of the business. There are

different types of management accounting; - Cost accounting system: A cost accounting system is tool which is used to assess the cost

of the product in order to make the profits in a most optimum manner. However, there is

no such tool which can be used to ascertain the appropriate cost, but by applying the cost

accounting system, company could attain the idea to reduce the cost of a product. Now,

there is a strong need to know about the product cost in order to make the product

profitable. Job costing system: Under this costing technique, there is need to know the

manufacturing costs individually for each job. This technique is useful for the firms

which are engaged in the manufacturing process. Batch costing system: this is the technique which is used like job costing technique. It is

a kind of specific order costing technique. Under Each batch, there are so many units are

covered. So, there is need to assess the total cost of the batch. Inventory management system: This system is used to know the inventory levels, orders

and deliveries. This is the system which is used to assess the stock and manage

accordingly.

Price optimisation system: This is the system which is used to identify about the

consumer’s reaction at different at the various prices of the products or services.

P2 Explain different methods used for management accounting reporting:

These methods are regulating by Apis ltd. In management accounting process. They are

such as follow: -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Make or buy decision- the make or buy decision concerns with choosing among

manufacturing a product in industry and purchase it from another supplier. The most important

factors in make or buy decisions, that they are regarding with the part of numerical analysis. In

that products are associated with production costs and whether business have the ability to

produce at require levels. Basically every item which is presently buying from an external seller

is a person for internal production and every part which is currently factory-made in house is a

latent candidate for acquisition. Make and buy decision are basically take in the basis of prices.

But is is only single criteria which is to be measured in strategical decisions.

JIT:- It is also known as Toyota production system. Just in time method is a

merchandise strategy of industries. Apis Ltd. Prefer such kind of strategics. In that increasing

employee’s effectiveness and his efficiency and decreasing wasting by establishing good

production methods. It is helpful in reducing inventory costs and provides producers to

forecasting of demand accurately. A good example if JITN is a car manufacture that functions

with very low product levels and relying on its supply chan. It makes ease up the production, by

this procedure can move one product to another very easily (Dechow, Myers and Shakespeare,

2010). Just in time method also reduces cost by destroying wastage keeping needs. It is a

management philosophy, that is used by managers to reduces wastage in production system by

using new techniques and strategies. There are several types of reducing wastage. Such as

inventory wastages, waste of motion, processing wastage, transportation wastage, wastage of

waiting time and waste from overproduction. Apis Ltd. Must have to make plan and strategics

to stopped these wastages that can ease up the production cost and production process also.

Activity based costing- ABC analysis is the managerial accounting methods that

accommodating in identifying the activities on which a firm is performed and it assigns

production's cost. It recognizes the relationship between product, cost and activities and through

this, ABC also assigns indirect costs of products makes less randomly than conventional

methods. In Apis Ltd. ABC found its place in today's manufacturing sector. Mostly hospitality

industries prefer to usage ABC analysis, because it extends the dependability of cost data. Th

method is used in profitability analysis, product line, target costing, service pricing and product

costing (Cohen and Zarowin, 2010.). If cost of product is better grasped, so organisations can

make convergent strategics. Under this system, any activity can be considered as an event or a

transaction. These activities are consumed as considers cost objects and elevated resources.

manufacturing a product in industry and purchase it from another supplier. The most important

factors in make or buy decisions, that they are regarding with the part of numerical analysis. In

that products are associated with production costs and whether business have the ability to

produce at require levels. Basically every item which is presently buying from an external seller

is a person for internal production and every part which is currently factory-made in house is a

latent candidate for acquisition. Make and buy decision are basically take in the basis of prices.

But is is only single criteria which is to be measured in strategical decisions.

JIT:- It is also known as Toyota production system. Just in time method is a

merchandise strategy of industries. Apis Ltd. Prefer such kind of strategics. In that increasing

employee’s effectiveness and his efficiency and decreasing wasting by establishing good

production methods. It is helpful in reducing inventory costs and provides producers to

forecasting of demand accurately. A good example if JITN is a car manufacture that functions

with very low product levels and relying on its supply chan. It makes ease up the production, by

this procedure can move one product to another very easily (Dechow, Myers and Shakespeare,

2010). Just in time method also reduces cost by destroying wastage keeping needs. It is a

management philosophy, that is used by managers to reduces wastage in production system by

using new techniques and strategies. There are several types of reducing wastage. Such as

inventory wastages, waste of motion, processing wastage, transportation wastage, wastage of

waiting time and waste from overproduction. Apis Ltd. Must have to make plan and strategics

to stopped these wastages that can ease up the production cost and production process also.

Activity based costing- ABC analysis is the managerial accounting methods that

accommodating in identifying the activities on which a firm is performed and it assigns

production's cost. It recognizes the relationship between product, cost and activities and through

this, ABC also assigns indirect costs of products makes less randomly than conventional

methods. In Apis Ltd. ABC found its place in today's manufacturing sector. Mostly hospitality

industries prefer to usage ABC analysis, because it extends the dependability of cost data. Th

method is used in profitability analysis, product line, target costing, service pricing and product

costing (Cohen and Zarowin, 2010.). If cost of product is better grasped, so organisations can

make convergent strategics. Under this system, any activity can be considered as an event or a

transaction. These activities are consumed as considers cost objects and elevated resources.

Inventory Management: - Inventory means an idle stock of goods and services that

would be transform in an item. For Apis Ltd. It is very essential thing manages its inventory and

stocks. The main of this method it is to reduces wastages in production. It determines the impact

of financial activities on balance sheets and health of supply chain management. Every

organisation continuously to maintain inventory by applying various methods of productions.

The main impact of inventory management is on financial figures of the business. (Hillier,

Grinblatt and Titman, 2011.) Because inventory is flexible and dynamic Inventory management

defines the evaluation of internal and external factors, constantly and carefully and controlling

through preparation and reviewing.

Many organisation prefers a separate department for inventory managers, who are

constantly planning and managing inventory and interact with procurement, financial and

production departments.

There are some different methods which can be used by an enterprise in order to make a

management accounting report. Some of these are as follows:

Sales report: It is a kind of report which includes data of products and services sold in

the market at particular time frame. This can be prepared for monthly and quarterly so that data

can be managed in an appropriate form.

Account receivable report: This can be prepared by companies in order to manage their

cash flow. This report is based on the balances that are credited to the customers. Along with

this, most of these are prepared on the basis of aging that in what duration the consumer

repayment the amount.

Performance report: These are prepared monthly or quarterly as per the need of

companies. The accountant prepare budget in order to compare their actual expenditure with the

total revenues that are generated by them after performing some operations. so, in this manner

Apis Ltd will be able to evaluate their current performance as compare to their past data.

Inventory management reports: The business organization can use these reports in order

to maintain their inventory level. This includes some factors such as labour cost, inventory waste

and overhead cost. By preparing this, manager can make the improvements at the workplace so

that their performance can be improved.

would be transform in an item. For Apis Ltd. It is very essential thing manages its inventory and

stocks. The main of this method it is to reduces wastages in production. It determines the impact

of financial activities on balance sheets and health of supply chain management. Every

organisation continuously to maintain inventory by applying various methods of productions.

The main impact of inventory management is on financial figures of the business. (Hillier,

Grinblatt and Titman, 2011.) Because inventory is flexible and dynamic Inventory management

defines the evaluation of internal and external factors, constantly and carefully and controlling

through preparation and reviewing.

Many organisation prefers a separate department for inventory managers, who are

constantly planning and managing inventory and interact with procurement, financial and

production departments.

There are some different methods which can be used by an enterprise in order to make a

management accounting report. Some of these are as follows:

Sales report: It is a kind of report which includes data of products and services sold in

the market at particular time frame. This can be prepared for monthly and quarterly so that data

can be managed in an appropriate form.

Account receivable report: This can be prepared by companies in order to manage their

cash flow. This report is based on the balances that are credited to the customers. Along with

this, most of these are prepared on the basis of aging that in what duration the consumer

repayment the amount.

Performance report: These are prepared monthly or quarterly as per the need of

companies. The accountant prepare budget in order to compare their actual expenditure with the

total revenues that are generated by them after performing some operations. so, in this manner

Apis Ltd will be able to evaluate their current performance as compare to their past data.

Inventory management reports: The business organization can use these reports in order

to maintain their inventory level. This includes some factors such as labour cost, inventory waste

and overhead cost. By preparing this, manager can make the improvements at the workplace so

that their performance can be improved.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job cost reports: This report shows the expenses which are related to particular project.

The total expenses are estimated on the basis of revenues so that profitability can be achieved.

Through this, time can be saved and cost can be reduced.

M1

These are benefits of management accounting. Such as: -

Reduces Expenses: - If Apis Ltd. Industry manages their expenditures and also managing

reports of financial data, it would be lower their expenses in their operations. It also

improves the cash inflow of the organisation by creating m,aster budget for whole

expenses(Burritt and Schaltegger, 2010). It allows managers to find out how much

money and its cost on production.

Increases financial returns: - Managers can increases their return son investments by

forecasting consumers demand and prices changes & its effects on economy. In

management accounting, Managers, makes budget annually and taxation for each and

every task of the organisation to analyse the computation of variants.

Ease up the Decision making process: - It is simplifying the decisions making process, by

using past data (Badertscher, 2011). Financials reports and statements are able to take

appropriate decisions for the betterment of the business.

Financial Analysis and interpretation: - Management accounting is a study of financial

statements and reports and it is essential is strategic decision making process. Many

managerial executives do not have good technical knowledge. So management

accounting provides them to different policies and information in terms of financial

decisions.

D1

There is some reason, that are helpful in evaluating the management accounting system.

Such are as follows: -

Helps in preparation of plan- Management accounting describes the analytical evaluation

of financial data and reports for an organisation. It is conducting a plan or set aims &

goals on the basis of forecasting.

Better services to customers: - If managers have proper knowledge of market, they also

know customer's taste and choice. So they trying to produces according to same. And

The total expenses are estimated on the basis of revenues so that profitability can be achieved.

Through this, time can be saved and cost can be reduced.

M1

These are benefits of management accounting. Such as: -

Reduces Expenses: - If Apis Ltd. Industry manages their expenditures and also managing

reports of financial data, it would be lower their expenses in their operations. It also

improves the cash inflow of the organisation by creating m,aster budget for whole

expenses(Burritt and Schaltegger, 2010). It allows managers to find out how much

money and its cost on production.

Increases financial returns: - Managers can increases their return son investments by

forecasting consumers demand and prices changes & its effects on economy. In

management accounting, Managers, makes budget annually and taxation for each and

every task of the organisation to analyse the computation of variants.

Ease up the Decision making process: - It is simplifying the decisions making process, by

using past data (Badertscher, 2011). Financials reports and statements are able to take

appropriate decisions for the betterment of the business.

Financial Analysis and interpretation: - Management accounting is a study of financial

statements and reports and it is essential is strategic decision making process. Many

managerial executives do not have good technical knowledge. So management

accounting provides them to different policies and information in terms of financial

decisions.

D1

There is some reason, that are helpful in evaluating the management accounting system.

Such are as follows: -

Helps in preparation of plan- Management accounting describes the analytical evaluation

of financial data and reports for an organisation. It is conducting a plan or set aims &

goals on the basis of forecasting.

Better services to customers: - If managers have proper knowledge of market, they also

know customer's taste and choice. So they trying to produces according to same. And

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

then customers can easily meet with their needs and wants by consuming quality products

and services.

Measurement of performance: - The techniques to budgetary controls, in standard costing

able to measure the performance of employees. It is also helpful in analysing the

efficiency of the employees.

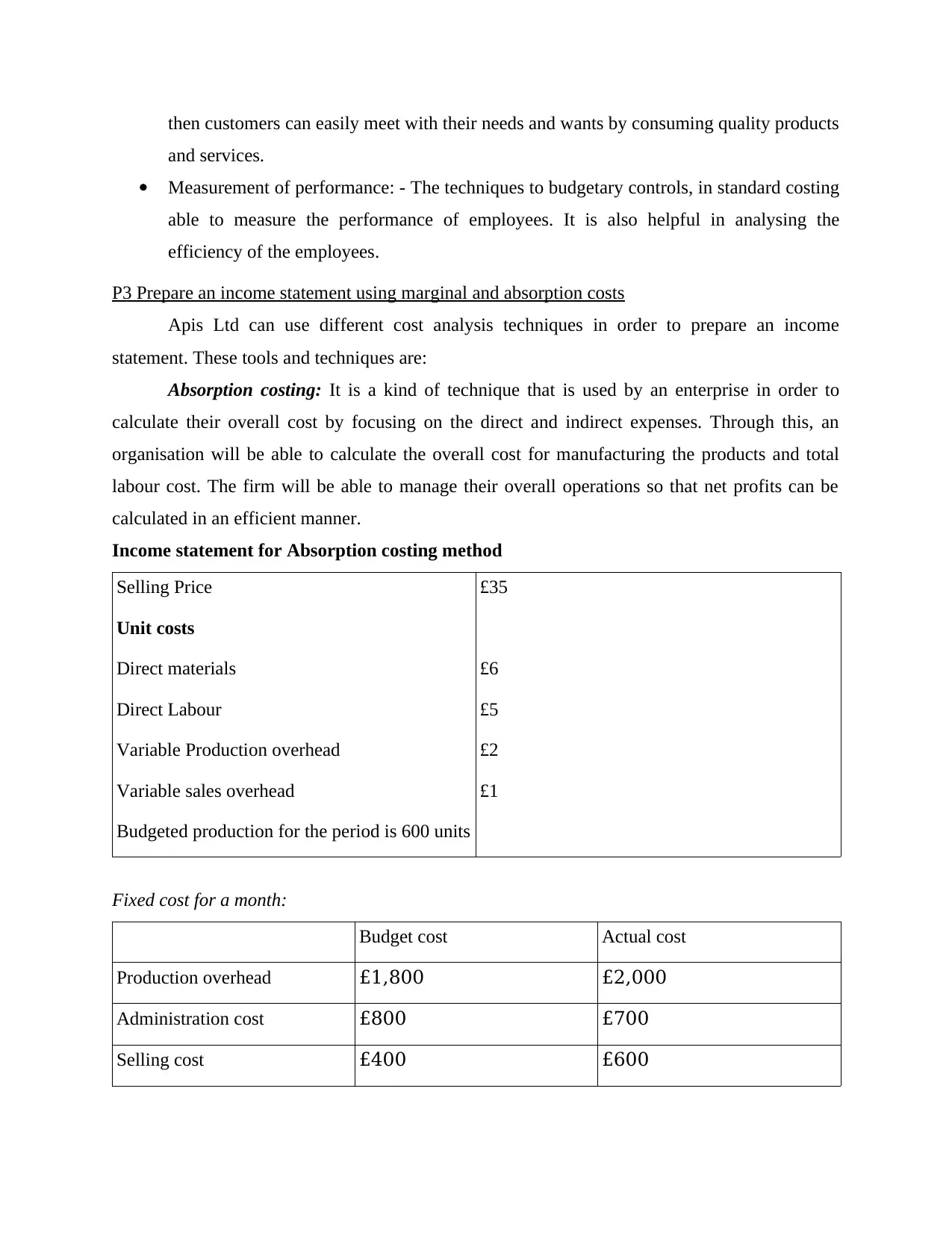

P3 Prepare an income statement using marginal and absorption costs

Apis Ltd can use different cost analysis techniques in order to prepare an income

statement. These tools and techniques are:

Absorption costing: It is a kind of technique that is used by an enterprise in order to

calculate their overall cost by focusing on the direct and indirect expenses. Through this, an

organisation will be able to calculate the overall cost for manufacturing the products and total

labour cost. The firm will be able to manage their overall operations so that net profits can be

calculated in an efficient manner.

Income statement for Absorption costing method

Selling Price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed cost for a month:

Budget cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

and services.

Measurement of performance: - The techniques to budgetary controls, in standard costing

able to measure the performance of employees. It is also helpful in analysing the

efficiency of the employees.

P3 Prepare an income statement using marginal and absorption costs

Apis Ltd can use different cost analysis techniques in order to prepare an income

statement. These tools and techniques are:

Absorption costing: It is a kind of technique that is used by an enterprise in order to

calculate their overall cost by focusing on the direct and indirect expenses. Through this, an

organisation will be able to calculate the overall cost for manufacturing the products and total

labour cost. The firm will be able to manage their overall operations so that net profits can be

calculated in an efficient manner.

Income statement for Absorption costing method

Selling Price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed cost for a month:

Budget cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

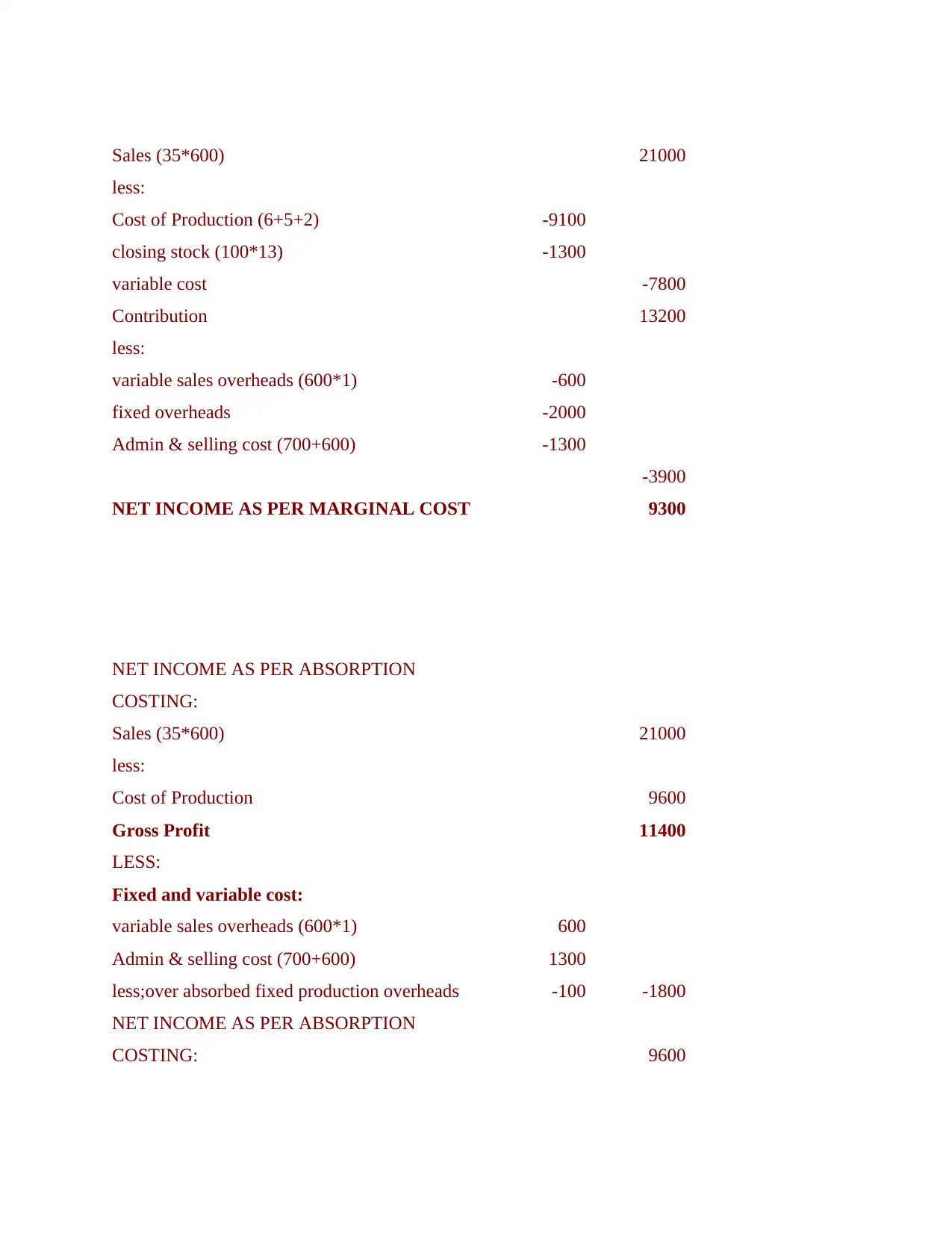

Sales (35*600) 21000

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable cost -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed overheads -2000

Admin & selling cost (700+600) -1300

-3900

NET INCOME AS PER MARGINAL COST 9300

NET INCOME AS PER ABSORPTION

COSTING:

Sales (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

less;over absorbed fixed production overheads -100 -1800

NET INCOME AS PER ABSORPTION

COSTING: 9600

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable cost -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed overheads -2000

Admin & selling cost (700+600) -1300

-3900

NET INCOME AS PER MARGINAL COST 9300

NET INCOME AS PER ABSORPTION

COSTING:

Sales (35*600) 21000

less:

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

less;over absorbed fixed production overheads -100 -1800

NET INCOME AS PER ABSORPTION

COSTING: 9600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal costing: Marginal cost is the alteration in the opportunity cost that increases

when the increment of one unit in the quantity produced is examined. Simply it is the price of

constructing one more unit of goods. The variable costing includes costs of labour and the

material, plus an estimated part of stable costs like management elevations and selling charges

(Renz, 2016).

In some corporations where average costs are really persistent their marginal cost is simply

equating the average cost. This idea of marginal cost is quite important in resource assignment.

Marginal cost is the alteration in the opportunity cost that increases when the increment

of one unit in the quantity produced is examined. Simply it is the price of constructing one more

unit of goods. The variable costing includes costs of labour and the material, plus an estimated

part of stable costs like management elevations and selling charges.

In some corporations where average costs are really persistent their marginal cost is

simply equating the average cost. This idea of marginal cost is quite important in resource

assignment.

M2

Apis Ltd can use management accounting techniques in order to improve their financial

growth in the market. The hospitality industry has approx 50 employees and their turnover is

£500, 000. So, in order to increase their turnover, they can use some of the functions in order to

enhance their overall performance. Some of these techniques are:

Absorption technique: This is a kind of technique that is used by an organisation so that

they can they can calculate their overall expenses. Through this, they will be able to prepare their

income statements so that overall account can be managed (Chandra, 2011.). Apis Ltd has total

fixed production is £200 and they have total gross profits is £9800. On the basis of this they will

be able to assess their financial growth so that they will be able to achieve success in the market.

Cost volume profit technique: On the basis of this approach, Apis ltd can determine

their overall cost so that they can identify their profitability level. This will be beneficial for the

hospitality industry as through this they will be able to enhance their performance.

D2

Organisations are performing their operations in the business environment so that their

growth can be improved. Here, Apis Ltd can use some methods and techniques in order to

calculate their financial data. Through this, the overall expenses can be identified so that they can

when the increment of one unit in the quantity produced is examined. Simply it is the price of

constructing one more unit of goods. The variable costing includes costs of labour and the

material, plus an estimated part of stable costs like management elevations and selling charges

(Renz, 2016).

In some corporations where average costs are really persistent their marginal cost is simply

equating the average cost. This idea of marginal cost is quite important in resource assignment.

Marginal cost is the alteration in the opportunity cost that increases when the increment

of one unit in the quantity produced is examined. Simply it is the price of constructing one more

unit of goods. The variable costing includes costs of labour and the material, plus an estimated

part of stable costs like management elevations and selling charges.

In some corporations where average costs are really persistent their marginal cost is

simply equating the average cost. This idea of marginal cost is quite important in resource

assignment.

M2

Apis Ltd can use management accounting techniques in order to improve their financial

growth in the market. The hospitality industry has approx 50 employees and their turnover is

£500, 000. So, in order to increase their turnover, they can use some of the functions in order to

enhance their overall performance. Some of these techniques are:

Absorption technique: This is a kind of technique that is used by an organisation so that

they can they can calculate their overall expenses. Through this, they will be able to prepare their

income statements so that overall account can be managed (Chandra, 2011.). Apis Ltd has total

fixed production is £200 and they have total gross profits is £9800. On the basis of this they will

be able to assess their financial growth so that they will be able to achieve success in the market.

Cost volume profit technique: On the basis of this approach, Apis ltd can determine

their overall cost so that they can identify their profitability level. This will be beneficial for the

hospitality industry as through this they will be able to enhance their performance.

D2

Organisations are performing their operations in the business environment so that their

growth can be improved. Here, Apis Ltd can use some methods and techniques in order to

calculate their financial data. Through this, the overall expenses can be identified so that they can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

achieve success in the market (Schaltegger and Burritt, 2010). As per the marginal costing

technique the net profit is 7500. so, through this, they will be able to make an effective strategy.

TASK 3

P4. Advantages and disadvantages of budgetary control planning tools:

Budgetary control can be defined as how well superiors or managers can make utilisation of

budget so as to monitor or control operations and cost in the specific accounting time (Renz,

2016). In Apis Ltd., it is the process for managers to fix performance and financial goals with

budgets and then compare the actual results with desired results and adjust performance

accordingly as needed. Budget is the formal statements of the financial resources that is used to

carry out specific activities in a specific time. Budgetary control is the technique where actual

results are compared with budget.

Budget is essential for the planning of financial resources in the company. There are various

planning tools for the budgetary control: Operational Budget: It is concerned with expenses and revenues of operating activities.

Profit from sells is revenue and the expenses which are there in process are expenses on

operating. Master Budget: It is the comprehensive projection that explains in which way company

wants to carry out its operations in period of budget. Income statement, cash budget give

supports to master budget (Lukka, 2010) Financial Budget: It provides a detailed view on how to manage funds and from where

the funds will be collected. It provides revenue information and return from capital

expenditure. Static Budget: Budget of static contains those elements which are not modified according

to sales. Overhead cost shows a static budget type. These kinds of budgets are used by the

non-profit organisations and SME's .

Cash flow Budget: It is prepared to manage flow of cash during the business operations.

Cash flow budget is being prepared by accounting officers to get useful information

regarding shortfall in expenses and sales. With the help of it the movement of cash can be

monitored by the entity and can be used in useful projects (Zadek, Evans and Pruzan,

2013)

technique the net profit is 7500. so, through this, they will be able to make an effective strategy.

TASK 3

P4. Advantages and disadvantages of budgetary control planning tools:

Budgetary control can be defined as how well superiors or managers can make utilisation of

budget so as to monitor or control operations and cost in the specific accounting time (Renz,

2016). In Apis Ltd., it is the process for managers to fix performance and financial goals with

budgets and then compare the actual results with desired results and adjust performance

accordingly as needed. Budget is the formal statements of the financial resources that is used to

carry out specific activities in a specific time. Budgetary control is the technique where actual

results are compared with budget.

Budget is essential for the planning of financial resources in the company. There are various

planning tools for the budgetary control: Operational Budget: It is concerned with expenses and revenues of operating activities.

Profit from sells is revenue and the expenses which are there in process are expenses on

operating. Master Budget: It is the comprehensive projection that explains in which way company

wants to carry out its operations in period of budget. Income statement, cash budget give

supports to master budget (Lukka, 2010) Financial Budget: It provides a detailed view on how to manage funds and from where

the funds will be collected. It provides revenue information and return from capital

expenditure. Static Budget: Budget of static contains those elements which are not modified according

to sales. Overhead cost shows a static budget type. These kinds of budgets are used by the

non-profit organisations and SME's .

Cash flow Budget: It is prepared to manage flow of cash during the business operations.

Cash flow budget is being prepared by accounting officers to get useful information

regarding shortfall in expenses and sales. With the help of it the movement of cash can be

monitored by the entity and can be used in useful projects (Zadek, Evans and Pruzan,

2013)

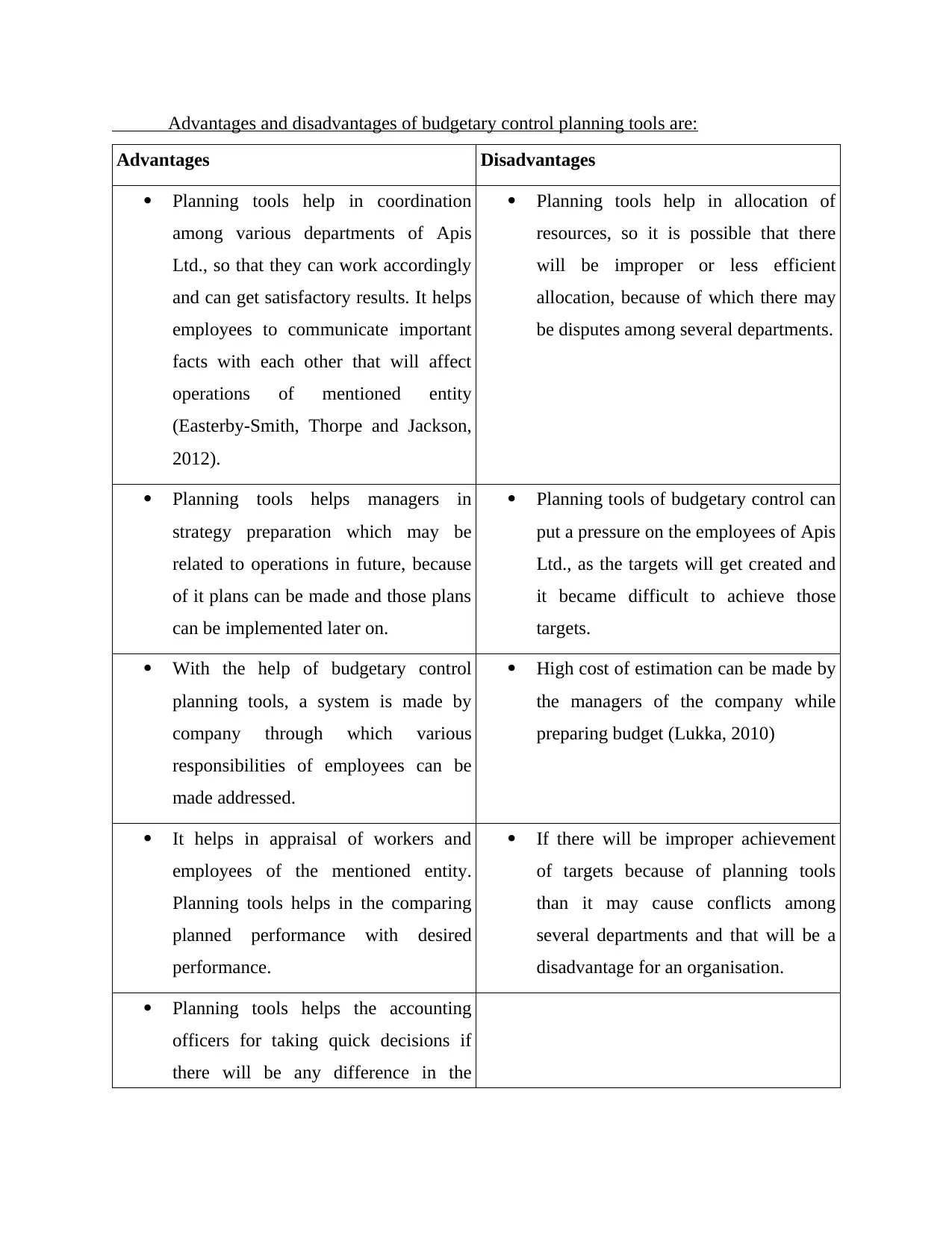

Advantages and disadvantages of budgetary control planning tools are:

Advantages Disadvantages

Planning tools help in coordination

among various departments of Apis

Ltd., so that they can work accordingly

and can get satisfactory results. It helps

employees to communicate important

facts with each other that will affect

operations of mentioned entity

(Easterby-Smith, Thorpe and Jackson,

2012).

Planning tools help in allocation of

resources, so it is possible that there

will be improper or less efficient

allocation, because of which there may

be disputes among several departments.

Planning tools helps managers in

strategy preparation which may be

related to operations in future, because

of it plans can be made and those plans

can be implemented later on.

Planning tools of budgetary control can

put a pressure on the employees of Apis

Ltd., as the targets will get created and

it became difficult to achieve those

targets.

With the help of budgetary control

planning tools, a system is made by

company through which various

responsibilities of employees can be

made addressed.

High cost of estimation can be made by

the managers of the company while

preparing budget (Lukka, 2010)

It helps in appraisal of workers and

employees of the mentioned entity.

Planning tools helps in the comparing

planned performance with desired

performance.

If there will be improper achievement

of targets because of planning tools

than it may cause conflicts among

several departments and that will be a

disadvantage for an organisation.

Planning tools helps the accounting

officers for taking quick decisions if

there will be any difference in the

Advantages Disadvantages

Planning tools help in coordination

among various departments of Apis

Ltd., so that they can work accordingly

and can get satisfactory results. It helps

employees to communicate important

facts with each other that will affect

operations of mentioned entity

(Easterby-Smith, Thorpe and Jackson,

2012).

Planning tools help in allocation of

resources, so it is possible that there

will be improper or less efficient

allocation, because of which there may

be disputes among several departments.

Planning tools helps managers in

strategy preparation which may be

related to operations in future, because

of it plans can be made and those plans

can be implemented later on.

Planning tools of budgetary control can

put a pressure on the employees of Apis

Ltd., as the targets will get created and

it became difficult to achieve those

targets.

With the help of budgetary control

planning tools, a system is made by

company through which various

responsibilities of employees can be

made addressed.

High cost of estimation can be made by

the managers of the company while

preparing budget (Lukka, 2010)

It helps in appraisal of workers and

employees of the mentioned entity.

Planning tools helps in the comparing

planned performance with desired

performance.

If there will be improper achievement

of targets because of planning tools

than it may cause conflicts among

several departments and that will be a

disadvantage for an organisation.

Planning tools helps the accounting

officers for taking quick decisions if

there will be any difference in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.