Application of Management Accounting in Business Context Report

VerifiedAdded on 2023/01/12

|10

|2203

|95

Report

AI Summary

This report delves into the core principles and practical applications of management accounting within a business context, using Nisa retail as a case study. It begins with an introduction to management accounting, emphasizing its role in managerial decision-making, and explores different management accounting systems such as cost accounting, job costing, inventory management, and price optimization systems. The report then examines various management accounting reports, including budget reports, accounts receivable aging reports, job cost reports, performance reports, and inventory and manufacturing reports, highlighting their significance in organizational performance evaluation and control. Furthermore, it critically evaluates the integration of management accounting and reporting systems. The report also analyzes different management accounting techniques, specifically marginal costing and absorption costing, providing detailed calculations and comparisons. The conclusion emphasizes the importance of management accounting for effective business decision-making and provides references to support the analysis.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

ACTIVITY 1....................................................................................................................................3

Management accounting system and different types of management accounting system...........3

Different methods of management accounting reports................................................................4

Critical evaluation of integrating management accounting system and reporting in an

organization..................................................................................................................................5

Activity-2.........................................................................................................................................6

Different types of management accounting techniques...............................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

ACTIVITY 1....................................................................................................................................3

Management accounting system and different types of management accounting system...........3

Different methods of management accounting reports................................................................4

Critical evaluation of integrating management accounting system and reporting in an

organization..................................................................................................................................5

Activity-2.........................................................................................................................................6

Different types of management accounting techniques...............................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting is the financial process of providing relevant information to the

manager of the organization which helps in decision making. It mainly utilized by the internal

management team and is not disclosed to outsiders. The core objective of this is to take better

and accurate decision. In this report, Nisa retail is taken is an organization which is retail grocery

store in UK. This report presents about introduction to management accounting and the different

types of management accounting system. It also includes different types of reports prepared by

the organization.

ACTIVITY 1

Management accounting system and different types of management accounting system

Management accounting is defined as the process through which all the accounting

information is being analysed in order to take the decision for the betterment of the company

(Alaeddin and Thabet, 2018). Them management accounting is very important for the success of

the company as this help the company in analysing the need to take relevant decisions in order to

make the working of company effective and efficient. There are many different types of

management accounting system which can be used by Nisa which are as follows-

Cost accounting system- this is a system which is used by the company in order to

manage the allocation of the cost to all the activities involved in the manufacturing of product

and services. This is mainly used in order to calculate the cost levied and the profit earned

against the cost incurred. The major requirement of cost accounting system are like calculating

cost like direct cost, indirect cost, overheads and many others. Thus, it is very necessary for Nisa

to manage the cost because if the cost will be high then this will not be profitable for company,

and they may face loss.

Job costing system- this is another major system of management accounting and this

system is related with the process of accumulation of all the information relating to different jobs

involved in whole manufacturing process. This management system involves separately

calculating the cost for each and every task which is undertaken to complete the activities of the

whole process of manufacturing. The major requirement of job costing system are like labour

cost, overhead cost, cost of material and many other different types of cost.

Inventory management system- this is another system which is undertaken by Nisa is the

inventory management system. This is an important system because of the fact that the inventory

Management accounting is the financial process of providing relevant information to the

manager of the organization which helps in decision making. It mainly utilized by the internal

management team and is not disclosed to outsiders. The core objective of this is to take better

and accurate decision. In this report, Nisa retail is taken is an organization which is retail grocery

store in UK. This report presents about introduction to management accounting and the different

types of management accounting system. It also includes different types of reports prepared by

the organization.

ACTIVITY 1

Management accounting system and different types of management accounting system

Management accounting is defined as the process through which all the accounting

information is being analysed in order to take the decision for the betterment of the company

(Alaeddin and Thabet, 2018). Them management accounting is very important for the success of

the company as this help the company in analysing the need to take relevant decisions in order to

make the working of company effective and efficient. There are many different types of

management accounting system which can be used by Nisa which are as follows-

Cost accounting system- this is a system which is used by the company in order to

manage the allocation of the cost to all the activities involved in the manufacturing of product

and services. This is mainly used in order to calculate the cost levied and the profit earned

against the cost incurred. The major requirement of cost accounting system are like calculating

cost like direct cost, indirect cost, overheads and many others. Thus, it is very necessary for Nisa

to manage the cost because if the cost will be high then this will not be profitable for company,

and they may face loss.

Job costing system- this is another major system of management accounting and this

system is related with the process of accumulation of all the information relating to different jobs

involved in whole manufacturing process. This management system involves separately

calculating the cost for each and every task which is undertaken to complete the activities of the

whole process of manufacturing. The major requirement of job costing system are like labour

cost, overhead cost, cost of material and many other different types of cost.

Inventory management system- this is another system which is undertaken by Nisa is the

inventory management system. This is an important system because of the fact that the inventory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is very important because without inventory the manufacturing process cannot be undertaken in

successful manner (Ratnatunga, Balachandran and Tse, 2017). Thus, for Nisa it is very necessary

for the company that they manage the inventory in effective manner so that the production and

manufacturing goes smoothly. The major requirements of the inventory management system is to

collect and analyse the data in effective manner so that the availability of the inventory is

assessed and it is very necessary for the company to manage the inventory on time.

Price optimization system- this is another model which works in accordance with some

mathematical programs in order to calculate the fact that how the demand of the goods and

services varies at different price levels within the economy. This help Nisa in identifying the

sales at different prices levels of the prevailing within the economy. Thus, this will help Nisa in

assessing the level of profit which the company can earn at different level of prices within the

working of the economy (Shields and Shelleman, 2016). The major requirement of price

optimization systme is the market forces that is the demand of the goods and the supply of goods

and the related prices prevailing within the economy.

Different methods of management accounting reports

There are different types of management accounting reports prepared by the

organizations as per the requirement. Some most important reports are stated below.

Budget report

This report is very essential in measuring the performance of the organization and is

useful for both small and large organizations. The budget is prepared based on the previous

year's data and performance. But it caters to the need of considering the unforeseen events or

circumstances that might arise (Singhvi and BODHANWALA, 2018). This budget helps

businesses in analysing the performance department wise and cost controls. For example, in the

previous year, the business was gone little over budget and the organization was unable to find

ways to trim the cost and in the next year, the budget will be increased to a certain required level.

This budget can be used to provide incentives to the employees for meeting the specific goals.

Accounts receivable aging report

This tool is effective for managing the cash flow if the huge credit is provided to the

customers or the business depends upon providing heavy credit. This such case, it is important to

prepare account receivable aging report. It provides a complete breakdown of the each customers

remaining balance which helps in identifying the defaulters and also any issue persisting in the

successful manner (Ratnatunga, Balachandran and Tse, 2017). Thus, for Nisa it is very necessary

for the company that they manage the inventory in effective manner so that the production and

manufacturing goes smoothly. The major requirements of the inventory management system is to

collect and analyse the data in effective manner so that the availability of the inventory is

assessed and it is very necessary for the company to manage the inventory on time.

Price optimization system- this is another model which works in accordance with some

mathematical programs in order to calculate the fact that how the demand of the goods and

services varies at different price levels within the economy. This help Nisa in identifying the

sales at different prices levels of the prevailing within the economy. Thus, this will help Nisa in

assessing the level of profit which the company can earn at different level of prices within the

working of the economy (Shields and Shelleman, 2016). The major requirement of price

optimization systme is the market forces that is the demand of the goods and the supply of goods

and the related prices prevailing within the economy.

Different methods of management accounting reports

There are different types of management accounting reports prepared by the

organizations as per the requirement. Some most important reports are stated below.

Budget report

This report is very essential in measuring the performance of the organization and is

useful for both small and large organizations. The budget is prepared based on the previous

year's data and performance. But it caters to the need of considering the unforeseen events or

circumstances that might arise (Singhvi and BODHANWALA, 2018). This budget helps

businesses in analysing the performance department wise and cost controls. For example, in the

previous year, the business was gone little over budget and the organization was unable to find

ways to trim the cost and in the next year, the budget will be increased to a certain required level.

This budget can be used to provide incentives to the employees for meeting the specific goals.

Accounts receivable aging report

This tool is effective for managing the cash flow if the huge credit is provided to the

customers or the business depends upon providing heavy credit. This such case, it is important to

prepare account receivable aging report. It provides a complete breakdown of the each customers

remaining balance which helps in identifying the defaulters and also any issue persisting in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

collection system (Butterfield, 2016). This report, presents for how long debt is owed and most

of the time a separate column for invoices is made such as 30/60/90 days late and more. Based

on this report, Nisa can transform its credit policies in order to maintain required level of cash for

the business operation. It also helps in identifying the bad debts which are required to be written

off and also creates provision for the same.

Job cost report

This report shows the complete detail about the cost incurred in the specific project. This

report is matched with the revenue estimated which can help in proper evaluation of the job

profitability (Bromwich and Scapens, 2016). This report helps businesses in determining the high

earning areas so that essential steps can be taken to make additional efforts instead of wasting

time and money on low earning areas. This report will help Nisa in analysing the expenses even

when the project is in progress so that timely action can be taken in order to exercise control

cost.

Performance report

This report is prepared to review the organization's performance in terms of each and

every employee and the organization as a whole. In large organizations, reports are also prepared

departmental wise which assists manager in making strategic decision with respect to achieving

the organizational objectives (Weetman, 2019). Based on this, employees are also rewarded

based on their performance and their commitment towards work. It provides a deep analysis into

the working of the organization. This report will help Nisa in identifying the flaws in the setup.

The core importance of this report is to measure its strategy towards the organization's objective.

Inventory and manufacturing report

This report is very valuable to the manufacturing concerns as it makes the process more

efficient. This report includes the item such as inventory waste, labour cost and overhead

expenses. Also, a comparison can be drawn between various assembly lines which helps in

highlighting the areas of improvement and also provides bonuses to the best departments. This

report will help Nisa in optimum utilization of resources.

Critical evaluation of integrating management accounting system and reporting in an

organization

The integration of management accounting and reporting in an organization results into

integrated system. This will help organization in efficiently analysing the performance of the

of the time a separate column for invoices is made such as 30/60/90 days late and more. Based

on this report, Nisa can transform its credit policies in order to maintain required level of cash for

the business operation. It also helps in identifying the bad debts which are required to be written

off and also creates provision for the same.

Job cost report

This report shows the complete detail about the cost incurred in the specific project. This

report is matched with the revenue estimated which can help in proper evaluation of the job

profitability (Bromwich and Scapens, 2016). This report helps businesses in determining the high

earning areas so that essential steps can be taken to make additional efforts instead of wasting

time and money on low earning areas. This report will help Nisa in analysing the expenses even

when the project is in progress so that timely action can be taken in order to exercise control

cost.

Performance report

This report is prepared to review the organization's performance in terms of each and

every employee and the organization as a whole. In large organizations, reports are also prepared

departmental wise which assists manager in making strategic decision with respect to achieving

the organizational objectives (Weetman, 2019). Based on this, employees are also rewarded

based on their performance and their commitment towards work. It provides a deep analysis into

the working of the organization. This report will help Nisa in identifying the flaws in the setup.

The core importance of this report is to measure its strategy towards the organization's objective.

Inventory and manufacturing report

This report is very valuable to the manufacturing concerns as it makes the process more

efficient. This report includes the item such as inventory waste, labour cost and overhead

expenses. Also, a comparison can be drawn between various assembly lines which helps in

highlighting the areas of improvement and also provides bonuses to the best departments. This

report will help Nisa in optimum utilization of resources.

Critical evaluation of integrating management accounting system and reporting in an

organization

The integration of management accounting and reporting in an organization results into

integrated system. This will help organization in efficiently analysing the performance of the

business which will help in proper decision making and the managerial reports provides direction

to the managers in order to make effective strategy. These reports can provide assistance in terms

of managing, directing and controlling the business strategy.

Activity-2

Different types of management accounting techniques

There are different types of techniques used in management accounting in cost analysis.

The two widely used techniques are stated below.

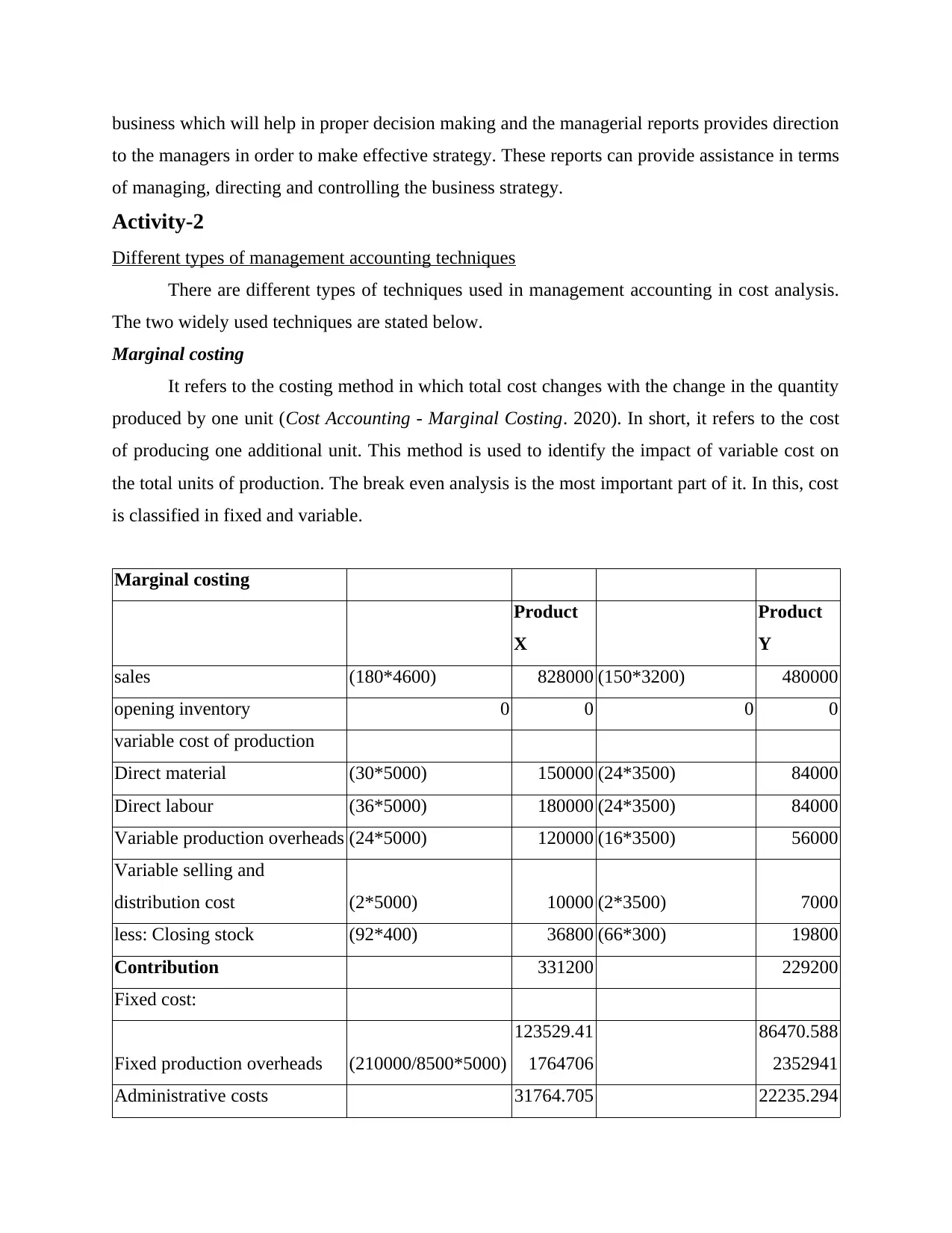

Marginal costing

It refers to the costing method in which total cost changes with the change in the quantity

produced by one unit (Cost Accounting - Marginal Costing. 2020). In short, it refers to the cost

of producing one additional unit. This method is used to identify the impact of variable cost on

the total units of production. The break even analysis is the most important part of it. In this, cost

is classified in fixed and variable.

Marginal costing

Product

X

Product

Y

sales (180*4600) 828000 (150*3200) 480000

opening inventory 0 0 0 0

variable cost of production

Direct material (30*5000) 150000 (24*3500) 84000

Direct labour (36*5000) 180000 (24*3500) 84000

Variable production overheads (24*5000) 120000 (16*3500) 56000

Variable selling and

distribution cost (2*5000) 10000 (2*3500) 7000

less: Closing stock (92*400) 36800 (66*300) 19800

Contribution 331200 229200

Fixed cost:

Fixed production overheads (210000/8500*5000)

123529.41

1764706

86470.588

2352941

Administrative costs 31764.705 22235.294

to the managers in order to make effective strategy. These reports can provide assistance in terms

of managing, directing and controlling the business strategy.

Activity-2

Different types of management accounting techniques

There are different types of techniques used in management accounting in cost analysis.

The two widely used techniques are stated below.

Marginal costing

It refers to the costing method in which total cost changes with the change in the quantity

produced by one unit (Cost Accounting - Marginal Costing. 2020). In short, it refers to the cost

of producing one additional unit. This method is used to identify the impact of variable cost on

the total units of production. The break even analysis is the most important part of it. In this, cost

is classified in fixed and variable.

Marginal costing

Product

X

Product

Y

sales (180*4600) 828000 (150*3200) 480000

opening inventory 0 0 0 0

variable cost of production

Direct material (30*5000) 150000 (24*3500) 84000

Direct labour (36*5000) 180000 (24*3500) 84000

Variable production overheads (24*5000) 120000 (16*3500) 56000

Variable selling and

distribution cost (2*5000) 10000 (2*3500) 7000

less: Closing stock (92*400) 36800 (66*300) 19800

Contribution 331200 229200

Fixed cost:

Fixed production overheads (210000/8500*5000)

123529.41

1764706

86470.588

2352941

Administrative costs 31764.705 22235.294

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8823529 1176471

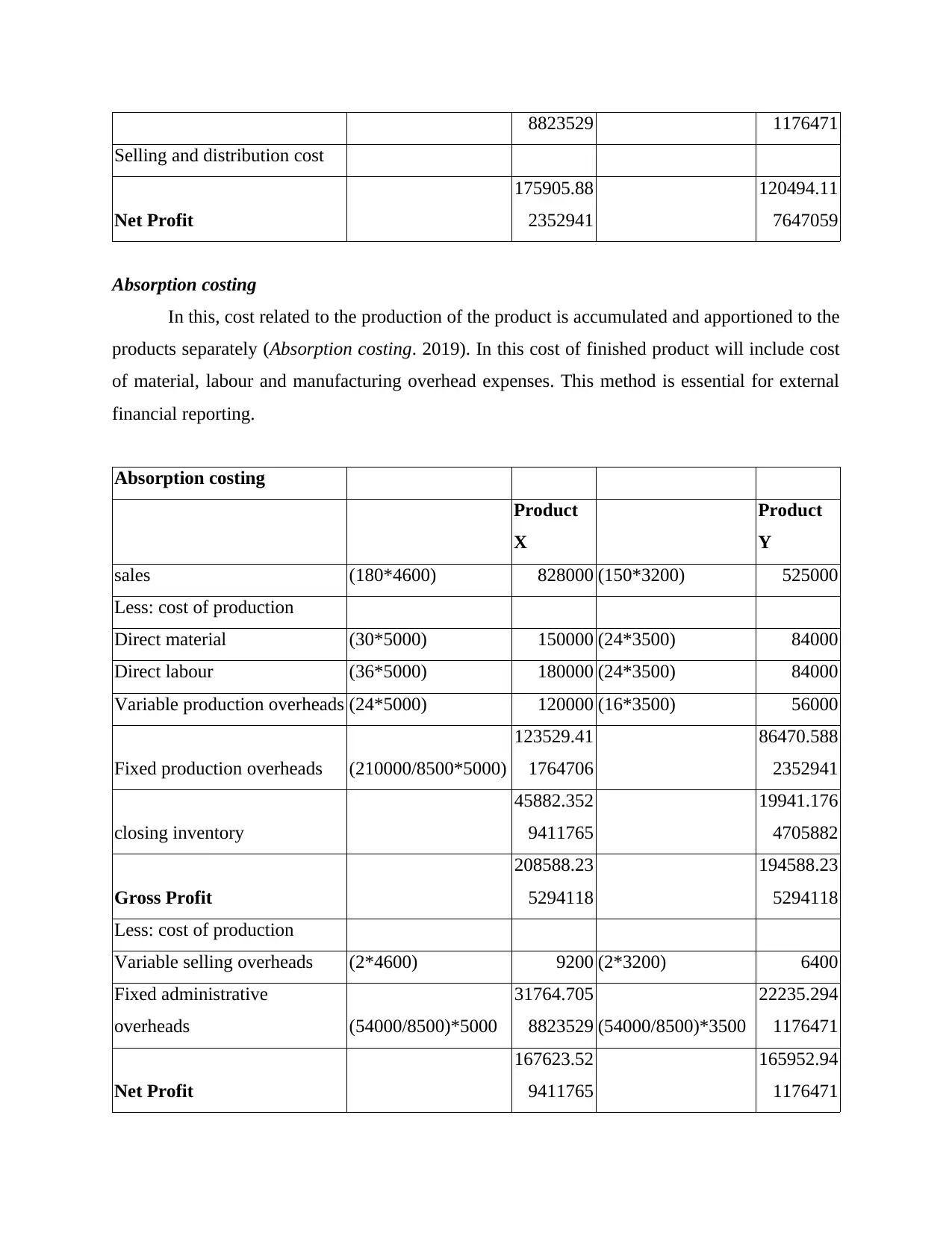

Selling and distribution cost

Net Profit

175905.88

2352941

120494.11

7647059

Absorption costing

In this, cost related to the production of the product is accumulated and apportioned to the

products separately (Absorption costing. 2019). In this cost of finished product will include cost

of material, labour and manufacturing overhead expenses. This method is essential for external

financial reporting.

Absorption costing

Product

X

Product

Y

sales (180*4600) 828000 (150*3200) 525000

Less: cost of production

Direct material (30*5000) 150000 (24*3500) 84000

Direct labour (36*5000) 180000 (24*3500) 84000

Variable production overheads (24*5000) 120000 (16*3500) 56000

Fixed production overheads (210000/8500*5000)

123529.41

1764706

86470.588

2352941

closing inventory

45882.352

9411765

19941.176

4705882

Gross Profit

208588.23

5294118

194588.23

5294118

Less: cost of production

Variable selling overheads (2*4600) 9200 (2*3200) 6400

Fixed administrative

overheads (54000/8500)*5000

31764.705

8823529 (54000/8500)*3500

22235.294

1176471

Net Profit

167623.52

9411765

165952.94

1176471

Selling and distribution cost

Net Profit

175905.88

2352941

120494.11

7647059

Absorption costing

In this, cost related to the production of the product is accumulated and apportioned to the

products separately (Absorption costing. 2019). In this cost of finished product will include cost

of material, labour and manufacturing overhead expenses. This method is essential for external

financial reporting.

Absorption costing

Product

X

Product

Y

sales (180*4600) 828000 (150*3200) 525000

Less: cost of production

Direct material (30*5000) 150000 (24*3500) 84000

Direct labour (36*5000) 180000 (24*3500) 84000

Variable production overheads (24*5000) 120000 (16*3500) 56000

Fixed production overheads (210000/8500*5000)

123529.41

1764706

86470.588

2352941

closing inventory

45882.352

9411765

19941.176

4705882

Gross Profit

208588.23

5294118

194588.23

5294118

Less: cost of production

Variable selling overheads (2*4600) 9200 (2*3200) 6400

Fixed administrative

overheads (54000/8500)*5000

31764.705

8823529 (54000/8500)*3500

22235.294

1176471

Net Profit

167623.52

9411765

165952.94

1176471

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing method is better than marginal costing because it takes into

consideration both fixed and variable cost in the cost of production of the product. Also, it

includes fixed cost in the valuation of closing inventory which is justifiable.

consideration both fixed and variable cost in the cost of production of the product. Also, it

includes fixed cost in the valuation of closing inventory which is justifiable.

CONCLUSION

It can be concluded from the above that management accounting is very essential in

managing the business. The different type of management accounting system that can be used by

the organization based on the needs and the industry and the key benefits associated with it.

Also, the various reports that can be prepared for further evaluating the performance of the

business. This, management accounting is important for business in taking effective business

decisions.

It can be concluded from the above that management accounting is very essential in

managing the business. The different type of management accounting system that can be used by

the organization based on the needs and the industry and the key benefits associated with it.

Also, the various reports that can be prepared for further evaluating the performance of the

business. This, management accounting is important for business in taking effective business

decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Alaeddin, O. and Thabet, A., 2018. Management Accounting System and Credit Risk

Management Policies and Practices towards Organizational Performance in Palestinian

Commercial Banks.

Bromwich, M. and Scapens, R. W., 2016. Management accounting research: 25 years

on. Management Accounting Research. 31. pp.1-9.

Butterfield, E., 2016. Managerial Decision-making and Management Accounting Information.

Ratnatunga, J., Balachandran, K. and Tse, M., 2017. Development of management accounting in

Sri Lanka. In The Routledge Handbook of Accounting in Asia (pp. 125-135). Routledge.

Shields, J. and Shelleman, J.M., 2016. Management accounting systems in micro-SMEs. Journal

of Applied Management and Entrepreneurship. 21(1). p.19.

Singhvi, N. M. and BODHANWALA, J. R., 2018. Management Accounting: Text and Cases.

PHI Learning Pvt. Ltd..

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Online

Absorption costing. 2019. [Online]. Available

Through:<https://www.accountingtools.com/articles/2017/5/4/absorption-costing>.

Cost Accounting - Marginal Costing. 2020. [Online]. Available

Through:<https://www.tutorialspoint.com/accounting_basics/cost_accounting_marginal

_costing.htm>.

1

Books and journals

Alaeddin, O. and Thabet, A., 2018. Management Accounting System and Credit Risk

Management Policies and Practices towards Organizational Performance in Palestinian

Commercial Banks.

Bromwich, M. and Scapens, R. W., 2016. Management accounting research: 25 years

on. Management Accounting Research. 31. pp.1-9.

Butterfield, E., 2016. Managerial Decision-making and Management Accounting Information.

Ratnatunga, J., Balachandran, K. and Tse, M., 2017. Development of management accounting in

Sri Lanka. In The Routledge Handbook of Accounting in Asia (pp. 125-135). Routledge.

Shields, J. and Shelleman, J.M., 2016. Management accounting systems in micro-SMEs. Journal

of Applied Management and Entrepreneurship. 21(1). p.19.

Singhvi, N. M. and BODHANWALA, J. R., 2018. Management Accounting: Text and Cases.

PHI Learning Pvt. Ltd..

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Online

Absorption costing. 2019. [Online]. Available

Through:<https://www.accountingtools.com/articles/2017/5/4/absorption-costing>.

Cost Accounting - Marginal Costing. 2020. [Online]. Available

Through:<https://www.tutorialspoint.com/accounting_basics/cost_accounting_marginal

_costing.htm>.

1

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.