Management Accounting Report: Techniques, Budgeting, and Analysis

VerifiedAdded on 2023/01/13

|19

|4927

|34

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on techniques such as cost allocation, cost-volume-profit analysis, and flexible budgeting. It explores different product costing methods, including absorption and marginal costing, and examines the role of costing in determining product prices. The report also delves into inventory costing, covering methods like FIFO, LIFO, and weighted average cost. Furthermore, it discusses various budgeting types, including operating, capital, and cash flow budgets, along with alternative budgeting approaches such as incremental, activity-based, value proposition, and zero-based budgeting. The report analyzes the behavioral implications of budgeting and examines different pricing strategies. The financial data of Prime Furniture is used to illustrate the application of these concepts.

Unit 5 - Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO2..................................................................................................................................................3

Techniques of Management Accounting.....................................................................................3

LO3................................................................................................................................................10

Budget and its types...................................................................................................................10

Pricing strategies........................................................................................................................11

LO 4...............................................................................................................................................14

Compare different management accounting tools.....................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

LO2..................................................................................................................................................3

Techniques of Management Accounting.....................................................................................3

LO3................................................................................................................................................10

Budget and its types...................................................................................................................10

Pricing strategies........................................................................................................................11

LO 4...............................................................................................................................................14

Compare different management accounting tools.....................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES................................................................................................................................1

INTRODUCTION

Management Accounting is that branch of accounting that deals with the evaluation of

the financial data that is associated with the company and the financial statements are interpreted

so as to evaluate and forecast the business performance. In the current report, different aspects

related to management accounting will be evaluated and distinction between management and

financial accounting will be discussed. The report will also identify the different product costing

techniques and the inventory costing techniques along with development of proper budgets that

are associated with the company. Further, financial data of Prime Furniture will be evaluated and

appropriate interpretation will be made in the report.

LO2

Techniques of Management Accounting

Microeconomics techniques

Cost is the value that is spent by the organization in producing and delivery of product.

There are different types of cost such as fixed and variable cost, direct and indirect cost etc. Cost

analysis is a measure of determining the cost incurred and how well it can be organized which

can help in increasing the productivity (Weetman, 2019). Different types of cost analysis

techniques that can be used by Prime Furniture's are stated below.

Cost Allocation: It refers to process of identifying and assigning cost to different cost objects,

products or departments. The cost is allocated because it is not possible to directly trace te cost

for the specific object.

Cost effectiveness analysis: It is the technique that is used to analyze and compare the relative

cost to the outcome (Holopainen, Niskanen and Rissanen, 2019). It considers both monetary and

non-monetary aspects for comparison.

Cost benefit analysis: It is a process that is used by the organization in analyzing decisions

regarding systems, processes. This method provides evidence based view which is not influenced

by any politics or partiality.

Cost-volume profit

This method helps in determining how variation in cost and volume can affect the

operating profit of the organization. This analysis requires company's all cost to be divided into

fixed and variable which includes manufacturing, selling and administration (Burney and

Management Accounting is that branch of accounting that deals with the evaluation of

the financial data that is associated with the company and the financial statements are interpreted

so as to evaluate and forecast the business performance. In the current report, different aspects

related to management accounting will be evaluated and distinction between management and

financial accounting will be discussed. The report will also identify the different product costing

techniques and the inventory costing techniques along with development of proper budgets that

are associated with the company. Further, financial data of Prime Furniture will be evaluated and

appropriate interpretation will be made in the report.

LO2

Techniques of Management Accounting

Microeconomics techniques

Cost is the value that is spent by the organization in producing and delivery of product.

There are different types of cost such as fixed and variable cost, direct and indirect cost etc. Cost

analysis is a measure of determining the cost incurred and how well it can be organized which

can help in increasing the productivity (Weetman, 2019). Different types of cost analysis

techniques that can be used by Prime Furniture's are stated below.

Cost Allocation: It refers to process of identifying and assigning cost to different cost objects,

products or departments. The cost is allocated because it is not possible to directly trace te cost

for the specific object.

Cost effectiveness analysis: It is the technique that is used to analyze and compare the relative

cost to the outcome (Holopainen, Niskanen and Rissanen, 2019). It considers both monetary and

non-monetary aspects for comparison.

Cost benefit analysis: It is a process that is used by the organization in analyzing decisions

regarding systems, processes. This method provides evidence based view which is not influenced

by any politics or partiality.

Cost-volume profit

This method helps in determining how variation in cost and volume can affect the

operating profit of the organization. This analysis requires company's all cost to be divided into

fixed and variable which includes manufacturing, selling and administration (Burney and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Malina, 2019). This method is based on several assumptions such as sales price per unit and

variable price per unit is constant, total fixed cost are constant, everything produced is sold.

Flexible budgeting

Flexible budget is a budget that adjusts with the change in volume and activity. As

flexible budget includes variable rate per unit of activity instead of total fixed amount. It uses

revenue and expenses based on current production and estimates how it will change with the

change in output (Bogt and Scapens, 2019). This helps management in comparing the figures to

know the area of improvement and areas improved.

Cost variances

It is a way of showing financial performance of a project. It is the difference between the

actual performance and the standard performance. These variances are bifurcated into different

types of cost such as direct material price variance, labor rate variance, variable overhead

spending variance, fixed overhead spending variance and purchase price variance.

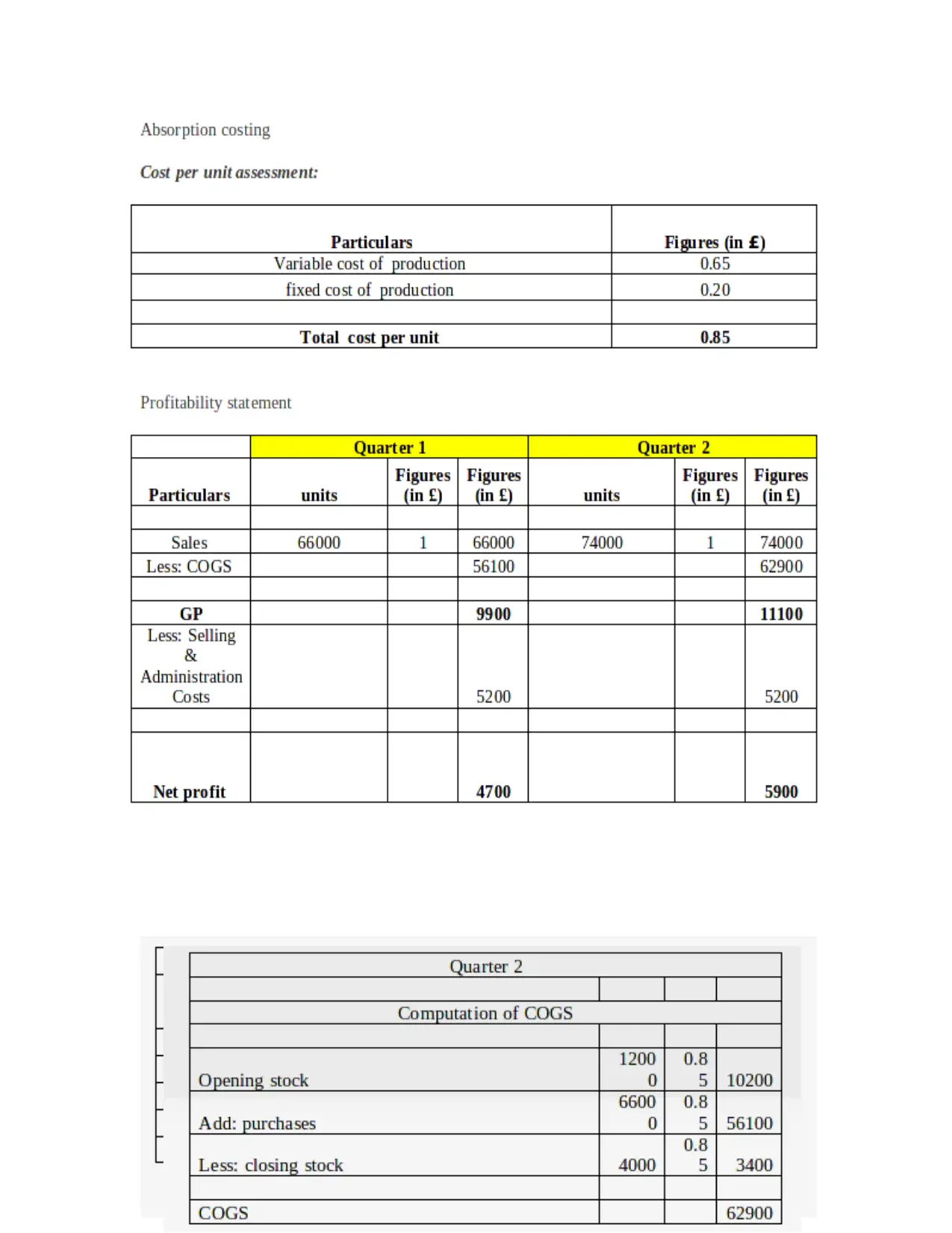

Absorption and Marginal Costing

Absorption Costing helps in ascertaining the costs that are incurred by the organization by

incorporating both direct and indirect expenses in an economy.

variable price per unit is constant, total fixed cost are constant, everything produced is sold.

Flexible budgeting

Flexible budget is a budget that adjusts with the change in volume and activity. As

flexible budget includes variable rate per unit of activity instead of total fixed amount. It uses

revenue and expenses based on current production and estimates how it will change with the

change in output (Bogt and Scapens, 2019). This helps management in comparing the figures to

know the area of improvement and areas improved.

Cost variances

It is a way of showing financial performance of a project. It is the difference between the

actual performance and the standard performance. These variances are bifurcated into different

types of cost such as direct material price variance, labor rate variance, variable overhead

spending variance, fixed overhead spending variance and purchase price variance.

Absorption and Marginal Costing

Absorption Costing helps in ascertaining the costs that are incurred by the organization by

incorporating both direct and indirect expenses in an economy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

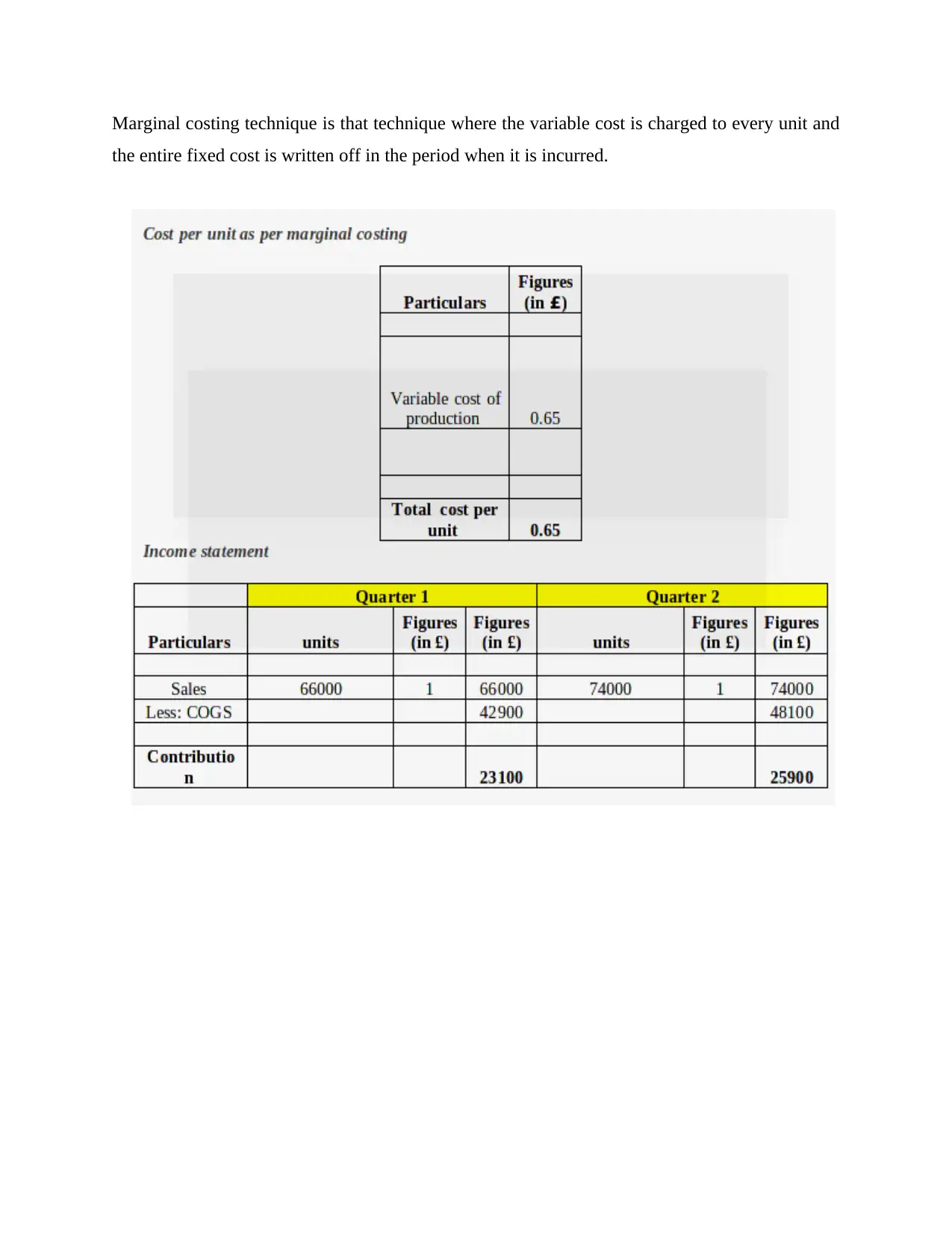

Marginal costing technique is that technique where the variable cost is charged to every unit and

the entire fixed cost is written off in the period when it is incurred.

the entire fixed cost is written off in the period when it is incurred.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

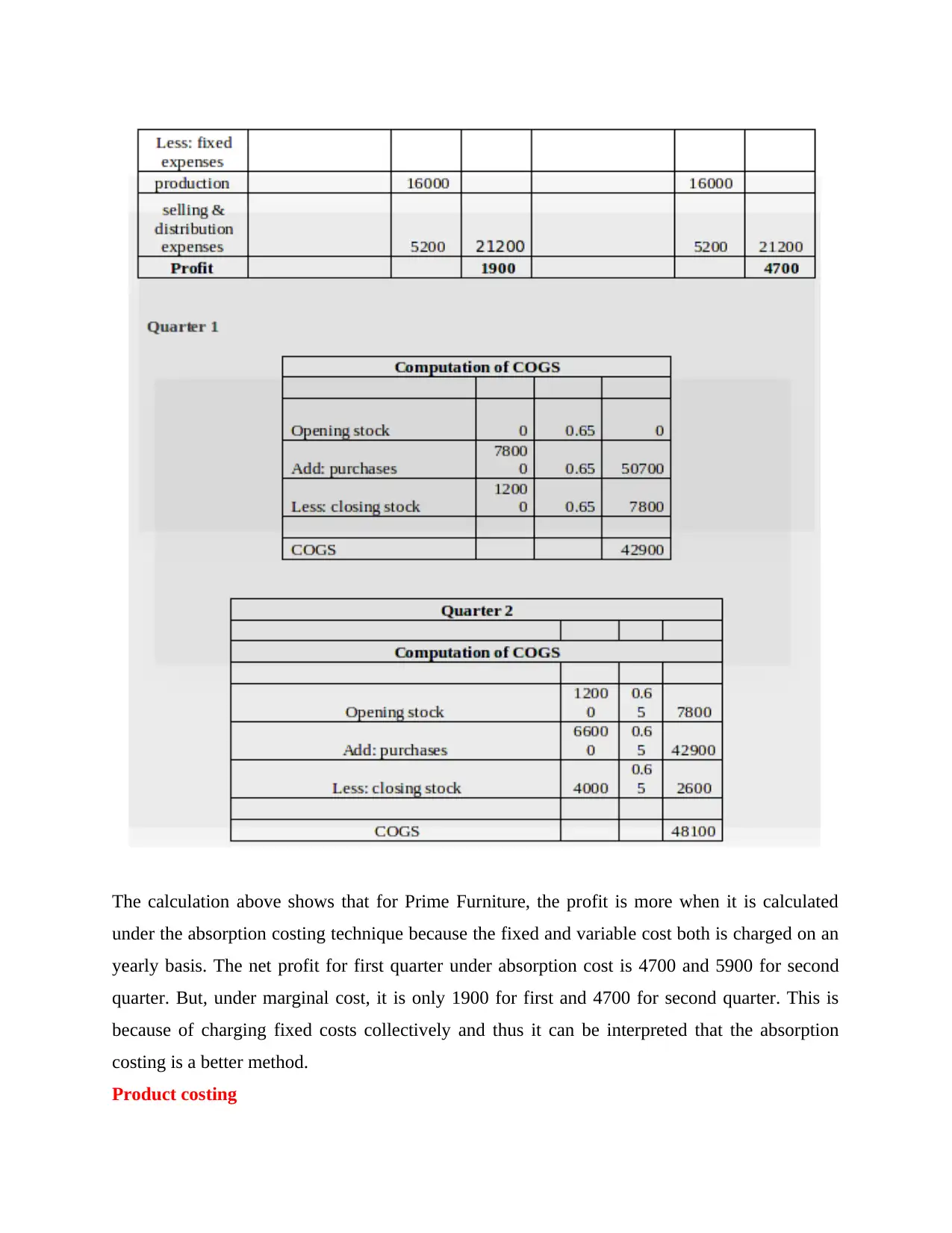

The calculation above shows that for Prime Furniture, the profit is more when it is calculated

under the absorption costing technique because the fixed and variable cost both is charged on an

yearly basis. The net profit for first quarter under absorption cost is 4700 and 5900 for second

quarter. But, under marginal cost, it is only 1900 for first and 4700 for second quarter. This is

because of charging fixed costs collectively and thus it can be interpreted that the absorption

costing is a better method.

Product costing

under the absorption costing technique because the fixed and variable cost both is charged on an

yearly basis. The net profit for first quarter under absorption cost is 4700 and 5900 for second

quarter. But, under marginal cost, it is only 1900 for first and 4700 for second quarter. This is

because of charging fixed costs collectively and thus it can be interpreted that the absorption

costing is a better method.

Product costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different types of costs

There are different types of cost which are classified based on the relationship with level

of output (Hopper and Bui, 2016). Following are cost in relation to how they change with respect

to the change in the level of output.

Fixed cost: It refers to the cost that do not vary with the change in the level of output.

This change is fixed with respect to short term changes and but in long term it may change. For

example, Office rent, insurance expenses, depreciation etc.

Variable cost: This cost changes with the change in the level of production. Variable cost

increases with the increase in production volume and decreases with the decrease in production

volume ((Otley, 2016)). For example, direct material, labor cost, packaging cost etc. It has direct

relation with the level of output.

Semi-variable cost: It is the mixture of both variable and fixed cost. These cost vary with

output but not in direct proportion. In such cases, cost is fixed for certain level of activity and

becomes variable after that activity. It is also known as mixed cost. It includes administrative

cost, maintenance cost etc.

Normal costing

It is the method used in determining the cost of a product. The components included in

this method are actual cost of material, labor and overhead rates that are mostly used for

allocation purpose. This method is used in determining the cost of the product where there is no

sudden change in the costs, mainly increase in cost.

Standard costing

It is the system used by manufacturers to identify the variances between the actual

performance and the standard performance in terms of cost, that is, actual coat incurred and cost

that should have incurred to produce the actual products. The standard cost includes direct

material, direct labor and other manufacturing overhead costs. It involves creation of estimated

cost for the activities.

Activity-based costing

It is a costing method that is used in assigning the indirect and overhead cost to the

products and services. This method is mostly used in manufacturing concerns and it is

considered to be the most logical manner for allocating costs. The cost is first assigned to the

There are different types of cost which are classified based on the relationship with level

of output (Hopper and Bui, 2016). Following are cost in relation to how they change with respect

to the change in the level of output.

Fixed cost: It refers to the cost that do not vary with the change in the level of output.

This change is fixed with respect to short term changes and but in long term it may change. For

example, Office rent, insurance expenses, depreciation etc.

Variable cost: This cost changes with the change in the level of production. Variable cost

increases with the increase in production volume and decreases with the decrease in production

volume ((Otley, 2016)). For example, direct material, labor cost, packaging cost etc. It has direct

relation with the level of output.

Semi-variable cost: It is the mixture of both variable and fixed cost. These cost vary with

output but not in direct proportion. In such cases, cost is fixed for certain level of activity and

becomes variable after that activity. It is also known as mixed cost. It includes administrative

cost, maintenance cost etc.

Normal costing

It is the method used in determining the cost of a product. The components included in

this method are actual cost of material, labor and overhead rates that are mostly used for

allocation purpose. This method is used in determining the cost of the product where there is no

sudden change in the costs, mainly increase in cost.

Standard costing

It is the system used by manufacturers to identify the variances between the actual

performance and the standard performance in terms of cost, that is, actual coat incurred and cost

that should have incurred to produce the actual products. The standard cost includes direct

material, direct labor and other manufacturing overhead costs. It involves creation of estimated

cost for the activities.

Activity-based costing

It is a costing method that is used in assigning the indirect and overhead cost to the

products and services. This method is mostly used in manufacturing concerns and it is

considered to be the most logical manner for allocating costs. The cost is first assigned to the

related activities and then assigns cost related to those activities to the respective products.

Sometimes it become difficult to assign indirect costs such as management cost, staff salaries etc.

Role of costing in deciding price of the product

Costs do not determine price but plays a crucial role in formulating pricing strategy. It is

related to the sales level which involves cost of production, selling and administration. The price

is decided based on what buyer is willing to pay, after which quantity required is determined.

Cost affects the prices that is charged (Kaplan, and Atkinson, 2015). A low cost producer can

price low and sell more because it will attract more price sensitive customers but it is not the

same in high cost producer's, as they cannot afford to lower its cost, so it must target premium

customers. Change in cost will force producers to change its price, for example, increase in price

of fuel, material, labor etc. Thus decisions are taken to quantities to sell and the target market to

serve plays an important part in forming pricing strategy. So, Prime Furniture's should consider

these points in setting price.

Cost of inventory

Inventory cost and its types

Inventory cost is the cost related to the procurement, storage and management of

inventory. There are three types of inventory cost which are stated below.

Ordering cost: It refers to the cost incurred for procuring inventory. It includes both cost of

procurement and inbound logistics.

Carrying cost: It involves storage and management of inventory. This cost varies and depends

upon management decision to manage inventory in -house, or outsourcing it to third party.

Shortage and stock out costs and cost of replenishment: These are the cost associated with

unusual circumstances. This situation arises when business becomes out of stock and business

have to incur cost such as paying salary to idle workers and other factory overheads even if

production is stopped.

Benefits of reducing inventory cost

The benefits that an organization can enjoy by reducing its inventory cost are stated

below.

It will result in less money stuck in inventory management

Saved cost can be utilized in other activity.

Reduces the loss due to spoilage or expired products.

Sometimes it become difficult to assign indirect costs such as management cost, staff salaries etc.

Role of costing in deciding price of the product

Costs do not determine price but plays a crucial role in formulating pricing strategy. It is

related to the sales level which involves cost of production, selling and administration. The price

is decided based on what buyer is willing to pay, after which quantity required is determined.

Cost affects the prices that is charged (Kaplan, and Atkinson, 2015). A low cost producer can

price low and sell more because it will attract more price sensitive customers but it is not the

same in high cost producer's, as they cannot afford to lower its cost, so it must target premium

customers. Change in cost will force producers to change its price, for example, increase in price

of fuel, material, labor etc. Thus decisions are taken to quantities to sell and the target market to

serve plays an important part in forming pricing strategy. So, Prime Furniture's should consider

these points in setting price.

Cost of inventory

Inventory cost and its types

Inventory cost is the cost related to the procurement, storage and management of

inventory. There are three types of inventory cost which are stated below.

Ordering cost: It refers to the cost incurred for procuring inventory. It includes both cost of

procurement and inbound logistics.

Carrying cost: It involves storage and management of inventory. This cost varies and depends

upon management decision to manage inventory in -house, or outsourcing it to third party.

Shortage and stock out costs and cost of replenishment: These are the cost associated with

unusual circumstances. This situation arises when business becomes out of stock and business

have to incur cost such as paying salary to idle workers and other factory overheads even if

production is stopped.

Benefits of reducing inventory cost

The benefits that an organization can enjoy by reducing its inventory cost are stated

below.

It will result in less money stuck in inventory management

Saved cost can be utilized in other activity.

Reduces the loss due to spoilage or expired products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lowers the risk of loss and lower insurance cost.

Inventory Valuation methods

There are mainly three inventory valuation methods that are used in an organization

which are discussed below.

FIFO Method: In this method, inventory is sold in the order of its purchase or production that is,

first in , first out. This method is typically used as companies sells products in the order of

purchase.

LIFO Method: It is the opposite of FIFO method. In this, the most recent purchased item is sold

first. When prices increases, the cost of goods sold under this method is relatively high.

Weighted average cost: In this method, inventory and cost of goods sold are based on the

average cost of all items purchased. This method is used when cost of units are same.

Overhead costs

It refers to the all the indirect cost or expenses which includes advertising fees, legal fees,

rent, repairs etc. it is important for budgeting and as well as helps business in determining the

price of the product or service to make profit.

LO3

Budget and its types

Budget is an estimation of revenue and expenses for a specific period. It helps in tracking

and managing resources. The different types of budgets that can be used by Prime Furniture's are

stated below. Operating budget: It is a forecast of projected income and expenses for a specific period.

It is prepared weekly, monthly or yearly (Otley, 2016). It includes factors such as

material and labor cost, administrative expenses etc. Capital budget: This budget helps in determining which long term investment should be

accepted or declined. It includes purchasing or replacing new machinery, R&D projects

etc.

Cash flow budget: It helps in projecting cash flows of the business and how well

company is managing its cash. It is representing cash flow from different activities.

Alternative methods of budgeting

There are four other methods of budgeting which are discussed below.

Inventory Valuation methods

There are mainly three inventory valuation methods that are used in an organization

which are discussed below.

FIFO Method: In this method, inventory is sold in the order of its purchase or production that is,

first in , first out. This method is typically used as companies sells products in the order of

purchase.

LIFO Method: It is the opposite of FIFO method. In this, the most recent purchased item is sold

first. When prices increases, the cost of goods sold under this method is relatively high.

Weighted average cost: In this method, inventory and cost of goods sold are based on the

average cost of all items purchased. This method is used when cost of units are same.

Overhead costs

It refers to the all the indirect cost or expenses which includes advertising fees, legal fees,

rent, repairs etc. it is important for budgeting and as well as helps business in determining the

price of the product or service to make profit.

LO3

Budget and its types

Budget is an estimation of revenue and expenses for a specific period. It helps in tracking

and managing resources. The different types of budgets that can be used by Prime Furniture's are

stated below. Operating budget: It is a forecast of projected income and expenses for a specific period.

It is prepared weekly, monthly or yearly (Otley, 2016). It includes factors such as

material and labor cost, administrative expenses etc. Capital budget: This budget helps in determining which long term investment should be

accepted or declined. It includes purchasing or replacing new machinery, R&D projects

etc.

Cash flow budget: It helps in projecting cash flows of the business and how well

company is managing its cash. It is representing cash flow from different activities.

Alternative methods of budgeting

There are four other methods of budgeting which are discussed below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Incremental budgeting: It uses previous year’s budget and add and subtract a percentage

to create current year's budget. It is used when cost drivers do not change year to year. It is easy

to use.

Activity based budgeting: This approach determines the amount of input required to

achieve the target output. Company determines the activities and then cost associated with it.

Value proposition budgeting: This budget aims to avoid any unnecessary expenditure. It

refers to the value that company promises to deliver to the customers so that customers buy their

products.

Zero based budgeting: It is based on the assumption that all department budgets are zero

and managers need to justify each expenses. It aims to avoid all unnecessary expenditure for

company's success.

Behavioral implication of budgeting

Following are the behavioral implication of budgeting. Dysfunctional behavior: Budget can bring both positive and negative behavior among

employees. The improper implementation of budget results in the negative behavior of

the employees which impacts the organizational goals (Lavia López, and Hiebl, 2015).

This negativity is known as dysfunctional behavior. It is in conflict with organizational

goals. Participative budgeting: It is a bottom up approach which involves the people who are

being affected by the budget, which includes lower level employees also. This helps in

increasing motivation among employees and also reduces organizational conflicts.

Budgetary slack: It takes place when management intentionally underestimated revenue

and overestimates costs so that organization can request more funds. It is the difference

between the resources required and actual allocated resources.

Pricing

Pricing strategies

Pricing strategy is the model used in establishing the price of the product. There are

different strategies that can be used which are discussed below.

Competition based pricing: This strategy focuses on the prevailing market rate for the product

and services. It usually takes competitor's price as the benchmark. Mostly company's prices their

product below the competitor's prices.

to create current year's budget. It is used when cost drivers do not change year to year. It is easy

to use.

Activity based budgeting: This approach determines the amount of input required to

achieve the target output. Company determines the activities and then cost associated with it.

Value proposition budgeting: This budget aims to avoid any unnecessary expenditure. It

refers to the value that company promises to deliver to the customers so that customers buy their

products.

Zero based budgeting: It is based on the assumption that all department budgets are zero

and managers need to justify each expenses. It aims to avoid all unnecessary expenditure for

company's success.

Behavioral implication of budgeting

Following are the behavioral implication of budgeting. Dysfunctional behavior: Budget can bring both positive and negative behavior among

employees. The improper implementation of budget results in the negative behavior of

the employees which impacts the organizational goals (Lavia López, and Hiebl, 2015).

This negativity is known as dysfunctional behavior. It is in conflict with organizational

goals. Participative budgeting: It is a bottom up approach which involves the people who are

being affected by the budget, which includes lower level employees also. This helps in

increasing motivation among employees and also reduces organizational conflicts.

Budgetary slack: It takes place when management intentionally underestimated revenue

and overestimates costs so that organization can request more funds. It is the difference

between the resources required and actual allocated resources.

Pricing

Pricing strategies

Pricing strategy is the model used in establishing the price of the product. There are

different strategies that can be used which are discussed below.

Competition based pricing: This strategy focuses on the prevailing market rate for the product

and services. It usually takes competitor's price as the benchmark. Mostly company's prices their

product below the competitor's prices.

Price skimming strategy: In this, company's set the price of the product higher initially and then

lowers it as product becomes less popular. This method is good for new businesses, looking to

enter the market.

Premium pricing strategy: This strategy is used when company's put the prices of the product

high to make it a luxury or premium product. It is helpful in creating brand awareness.

Effect of supply and demand on price

Supply and demand is used in determining the price and it based on some laws. If

demand increases, price of the product will also increase and vise-versa. If supply of the product

increases, then price decreases. So, the price is decided at the point where quantity demanded

and supplied are equal. It is known as the point of equilibrium.

Common costing system

Actual costing

It is the method that uses actual cost for recording the cost of the product. It includes the

actual cost of material, labor, overheads incurred in the production. It is used to determine the

cost to specific products.

Different costing system

Job costing: It refers to the method of recording and tracking costs by job. It maintains

the data which can be used in future for similar job. These costs are examined carefully

so that costs can be reduced next time.

Process costing: This method is used in mass production of similar products. In this, the

cost of one unit is assumed to be same as that of others.

Batch costing: In this method, products are manufactured in batches. The number of

units in a batch may vary from batch to batch. In this, batch cost is used to determine the

cost per unit.

Contract costing: It is a specific order costing method. It tracks cost with specific

contract of the customers. It is mainly used in construction and engineering projects.

Strategic planning:

Strategic planning is most effective and important for company to increase their sales by

attracting customer towards company (Messner, 2016). This is process of defining strategy or

direction for making decision for allocating resources to pursue strategy. This may extend to

control mechanisms for guiding implementation of strategy. This creates my effectiveness for

lowers it as product becomes less popular. This method is good for new businesses, looking to

enter the market.

Premium pricing strategy: This strategy is used when company's put the prices of the product

high to make it a luxury or premium product. It is helpful in creating brand awareness.

Effect of supply and demand on price

Supply and demand is used in determining the price and it based on some laws. If

demand increases, price of the product will also increase and vise-versa. If supply of the product

increases, then price decreases. So, the price is decided at the point where quantity demanded

and supplied are equal. It is known as the point of equilibrium.

Common costing system

Actual costing

It is the method that uses actual cost for recording the cost of the product. It includes the

actual cost of material, labor, overheads incurred in the production. It is used to determine the

cost to specific products.

Different costing system

Job costing: It refers to the method of recording and tracking costs by job. It maintains

the data which can be used in future for similar job. These costs are examined carefully

so that costs can be reduced next time.

Process costing: This method is used in mass production of similar products. In this, the

cost of one unit is assumed to be same as that of others.

Batch costing: In this method, products are manufactured in batches. The number of

units in a batch may vary from batch to batch. In this, batch cost is used to determine the

cost per unit.

Contract costing: It is a specific order costing method. It tracks cost with specific

contract of the customers. It is mainly used in construction and engineering projects.

Strategic planning:

Strategic planning is most effective and important for company to increase their sales by

attracting customer towards company (Messner, 2016). This is process of defining strategy or

direction for making decision for allocating resources to pursue strategy. This may extend to

control mechanisms for guiding implementation of strategy. This creates my effectiveness for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.