Management Accounting Report for London Clothing Works - BTEC HND

VerifiedAdded on 2023/01/17

|17

|3539

|83

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the case study of London Clothing Works, a manufacturing firm specializing in raincoats and outerwear. The report addresses key management accounting requirements, including various reporting methods, cost calculations, and income statement development. It delves into cost techniques like marginal and absorption costing, presenting profit and loss statements under each method for three months and a reconciliation statement. Furthermore, the report explores budgetary control, examining cash and sales budgets, and discusses their advantages and disadvantages. The report also covers performance, accounts receivable ageing, and inventory reports. The document concludes by analyzing the application of management accounting in decision-making processes and financial planning within the organization.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is defined as the provision of monetary as well as non monetary

information of decision making to managers. It is also known as managerial accounting and is

method of examining operations and cost of business for preparing internal reports that aids

manager to attain organisational objectives (Busco, Caglio and Scapens, 2015). As per the

scenario, the undertaken organisation for this report is London Clothing Works which is a

manufacturing firm that specialises in raincoats, outerwear and unstructured garments. Its

headquarters is in North London, UK. This report crucial many MAS requirements, various

management accounting reporting methods. calculation as well as income statement

development, tools of budgetary planning along with their advantage and disadvantage are

explained. Moreover, comparison of adopting management accounting system to responds

financial issues are also discussed in this report.

TASK1

P1

Management accounting is regarded as the profession which includes partnering

administrative decision making, devising planing as well as performance of management system,

facilitating expertise into financial report and control to aids management into development as

well as execution of a firm's strategy (Meaning and Definition of Management Accounting,

2019). In London Clothing Works its manager follow this to assure that it will improve their

enterprises in future with aids of current plan of action which are develop by them. The vital

intent of this is to gather detailed information to produce internal report that help undertaken

entities to make efficacious decision within many situation. Also, it plays crucial role in London

Clothing Works. Few are as follows: Assists in efficacious controlling: Management accounting is beneficial for business

concern to make appropriate control over many practices (Cooper, Ezzamel and Qu,

2017). As by utilising key information from internal report manager may focused on that

activities that outcomes in lower profit or higher cost. In relation to London Clothing

Works, their manager may control many prospects efficaciously by aids of management

accounting.

1

Management accounting is defined as the provision of monetary as well as non monetary

information of decision making to managers. It is also known as managerial accounting and is

method of examining operations and cost of business for preparing internal reports that aids

manager to attain organisational objectives (Busco, Caglio and Scapens, 2015). As per the

scenario, the undertaken organisation for this report is London Clothing Works which is a

manufacturing firm that specialises in raincoats, outerwear and unstructured garments. Its

headquarters is in North London, UK. This report crucial many MAS requirements, various

management accounting reporting methods. calculation as well as income statement

development, tools of budgetary planning along with their advantage and disadvantage are

explained. Moreover, comparison of adopting management accounting system to responds

financial issues are also discussed in this report.

TASK1

P1

Management accounting is regarded as the profession which includes partnering

administrative decision making, devising planing as well as performance of management system,

facilitating expertise into financial report and control to aids management into development as

well as execution of a firm's strategy (Meaning and Definition of Management Accounting,

2019). In London Clothing Works its manager follow this to assure that it will improve their

enterprises in future with aids of current plan of action which are develop by them. The vital

intent of this is to gather detailed information to produce internal report that help undertaken

entities to make efficacious decision within many situation. Also, it plays crucial role in London

Clothing Works. Few are as follows: Assists in efficacious controlling: Management accounting is beneficial for business

concern to make appropriate control over many practices (Cooper, Ezzamel and Qu,

2017). As by utilising key information from internal report manager may focused on that

activities that outcomes in lower profit or higher cost. In relation to London Clothing

Works, their manager may control many prospects efficaciously by aids of management

accounting.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assists in decision making: Management accounting plays vita role as it aids entities to

formulate gainful decision. Such as the manager of London Clothing Works may take

appropriate actions and decision with help of respective accounting.

Management accounting system is regarded as intrinsic system which is applied by

several entities to observe and assess whole direct as well as indirect enterprises procedures.

London Clothing Works applied some management accounting system are discussed underneath:

Inventory management accounting: It is regarded as accounting system whcih is

alloted into task to keep records of whole kinds of stock which is purchased or sold

through entities. The main aim of inventory system is to assure that approrpiate usages of

stored raw materials is being performed through organsaition (Gibassier and Schaltegger,

2015). Such as London Clothing Works manufacturing department used this system for

efficacious management of raw material likes clothes, thread and others so that while

production there will be not any issues occurs realted to unavailability of resources

effectively.

Price optimisation system: It is regadred as teh system that is related into systematice

methods of operating entities to utilised appropriate pricing strategies. As per this, entities

obatin knowledge about what type of changes is needed within its pricing methods. Such

as London Clothing Works sales department applied respective system to revise the price

of their cloths as this assists them to enahnce sales units.

Cost accounting system: It is regarded as set of framework which are focused by small

as well as large entities for the aim of analysing exact cost which is related with

organisation's practices. In London Clothing Works manager utilsied this to determine

the cost of operation practices which generates more profit by assessing its costs.

Job order costing system: It is regadred as management accounting system that directs

administration to delegate costs to overall operations according to their features. As

London Clothing Works manfacture raincoats, outerwear and others so this system aids

their manufacturing department to assesss teh each job unit cost of producing cloths.

P2

For all entities, it is vital for them to keep appropriate information of whole intrinsic as

well as extrinsic activities to examine the deficits cause and formulate plan of action for

futuristic period (Gunarathne and Lee, 2015). For this aim, a certain methods is applied to

2

formulate gainful decision. Such as the manager of London Clothing Works may take

appropriate actions and decision with help of respective accounting.

Management accounting system is regarded as intrinsic system which is applied by

several entities to observe and assess whole direct as well as indirect enterprises procedures.

London Clothing Works applied some management accounting system are discussed underneath:

Inventory management accounting: It is regarded as accounting system whcih is

alloted into task to keep records of whole kinds of stock which is purchased or sold

through entities. The main aim of inventory system is to assure that approrpiate usages of

stored raw materials is being performed through organsaition (Gibassier and Schaltegger,

2015). Such as London Clothing Works manufacturing department used this system for

efficacious management of raw material likes clothes, thread and others so that while

production there will be not any issues occurs realted to unavailability of resources

effectively.

Price optimisation system: It is regadred as teh system that is related into systematice

methods of operating entities to utilised appropriate pricing strategies. As per this, entities

obatin knowledge about what type of changes is needed within its pricing methods. Such

as London Clothing Works sales department applied respective system to revise the price

of their cloths as this assists them to enahnce sales units.

Cost accounting system: It is regarded as set of framework which are focused by small

as well as large entities for the aim of analysing exact cost which is related with

organisation's practices. In London Clothing Works manager utilsied this to determine

the cost of operation practices which generates more profit by assessing its costs.

Job order costing system: It is regadred as management accounting system that directs

administration to delegate costs to overall operations according to their features. As

London Clothing Works manfacture raincoats, outerwear and others so this system aids

their manufacturing department to assesss teh each job unit cost of producing cloths.

P2

For all entities, it is vital for them to keep appropriate information of whole intrinsic as

well as extrinsic activities to examine the deficits cause and formulate plan of action for

futuristic period (Gunarathne and Lee, 2015). For this aim, a certain methods is applied to

2

prepare many report of management accounting. Also, this assist them to take effective actions

for handling the available resources. Thus, London Clothing Work manager prepared various

reports to record appropriate data. Few of them are described underneath:

Performance report: This is regarded as the type of management accounting report that

involves information in context of estimated and appropriate outcomes of many

operations. Based on this, the entities manager take effectual action associated to improve

overall performance. In relation to employees performance, information are provide by

respective reports (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015). As this

assists manager in assessing performance of each employees so that their growth may be

assured. In respect to London Clothing Work, their workers may be promoted based on

its performance which is gather with aids of performance report.

Accounts receivable ageing report: It is regarded as the kinds of management

accounting report that consists information related to overall debtors whose payment is

due. In addition to this, respective reports keep systematized records in respect with dates

like all debts amount, interest rate, transaction and so on. With the assistance of this

management accounting report, manager may able to approach information which is

related to debt amount and that is essential to be collected. Such as, finance department

of London Clothing Work can able to collect the debt amount form their users in less

time and money. Moreover, due to this their receivable turnover ratio will be enhanced.

Budget report: It is regarded as the management accounting report that involves

information related to estimated expense and spending. Due to this, various practices

variances is computed that aids in considering efficacious action for future time. In

relation to London Clothing Work, their accountant make this report with the purpose of

managing their financial outcomes. Also, for appropriate utilisation of available resources

associated to financial and non financial.

Inventory report: It is regarded as report that involves information associated with

overall inventory quantity such as raw materials, work in progress and others. Into

inventory report, information is included based on their effectual valuation of stock with

the assistance of LIFO, FIFO and so on (Nitzl, 2016). It is beneficial entities to control

overall cost of stock. For example: In London Clothing Work, their production

3

for handling the available resources. Thus, London Clothing Work manager prepared various

reports to record appropriate data. Few of them are described underneath:

Performance report: This is regarded as the type of management accounting report that

involves information in context of estimated and appropriate outcomes of many

operations. Based on this, the entities manager take effectual action associated to improve

overall performance. In relation to employees performance, information are provide by

respective reports (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015). As this

assists manager in assessing performance of each employees so that their growth may be

assured. In respect to London Clothing Work, their workers may be promoted based on

its performance which is gather with aids of performance report.

Accounts receivable ageing report: It is regarded as the kinds of management

accounting report that consists information related to overall debtors whose payment is

due. In addition to this, respective reports keep systematized records in respect with dates

like all debts amount, interest rate, transaction and so on. With the assistance of this

management accounting report, manager may able to approach information which is

related to debt amount and that is essential to be collected. Such as, finance department

of London Clothing Work can able to collect the debt amount form their users in less

time and money. Moreover, due to this their receivable turnover ratio will be enhanced.

Budget report: It is regarded as the management accounting report that involves

information related to estimated expense and spending. Due to this, various practices

variances is computed that aids in considering efficacious action for future time. In

relation to London Clothing Work, their accountant make this report with the purpose of

managing their financial outcomes. Also, for appropriate utilisation of available resources

associated to financial and non financial.

Inventory report: It is regarded as report that involves information associated with

overall inventory quantity such as raw materials, work in progress and others. Into

inventory report, information is included based on their effectual valuation of stock with

the assistance of LIFO, FIFO and so on (Nitzl, 2016). It is beneficial entities to control

overall cost of stock. For example: In London Clothing Work, their production

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

department use key information related to raw materials and finished goods by assistance

of respective reports.

TASK 2

P3

Cost technique is regarded as the procedures that is applied to ascertain cost for cost

control and decision making. This can be used to formulate decisions, negotiation, price

appraisal and assess purchasing performance. Thus, London Clothing Works, applied some cost

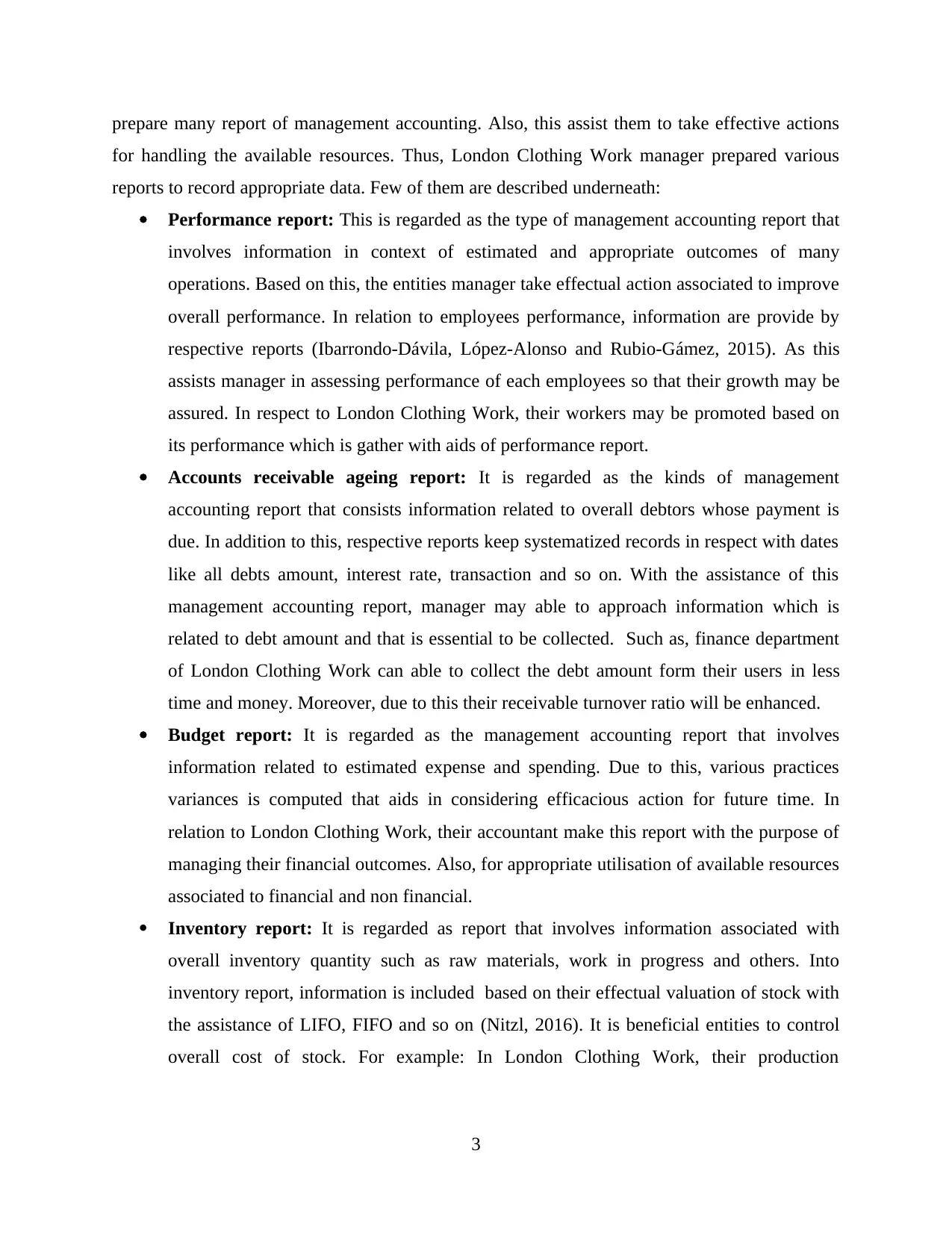

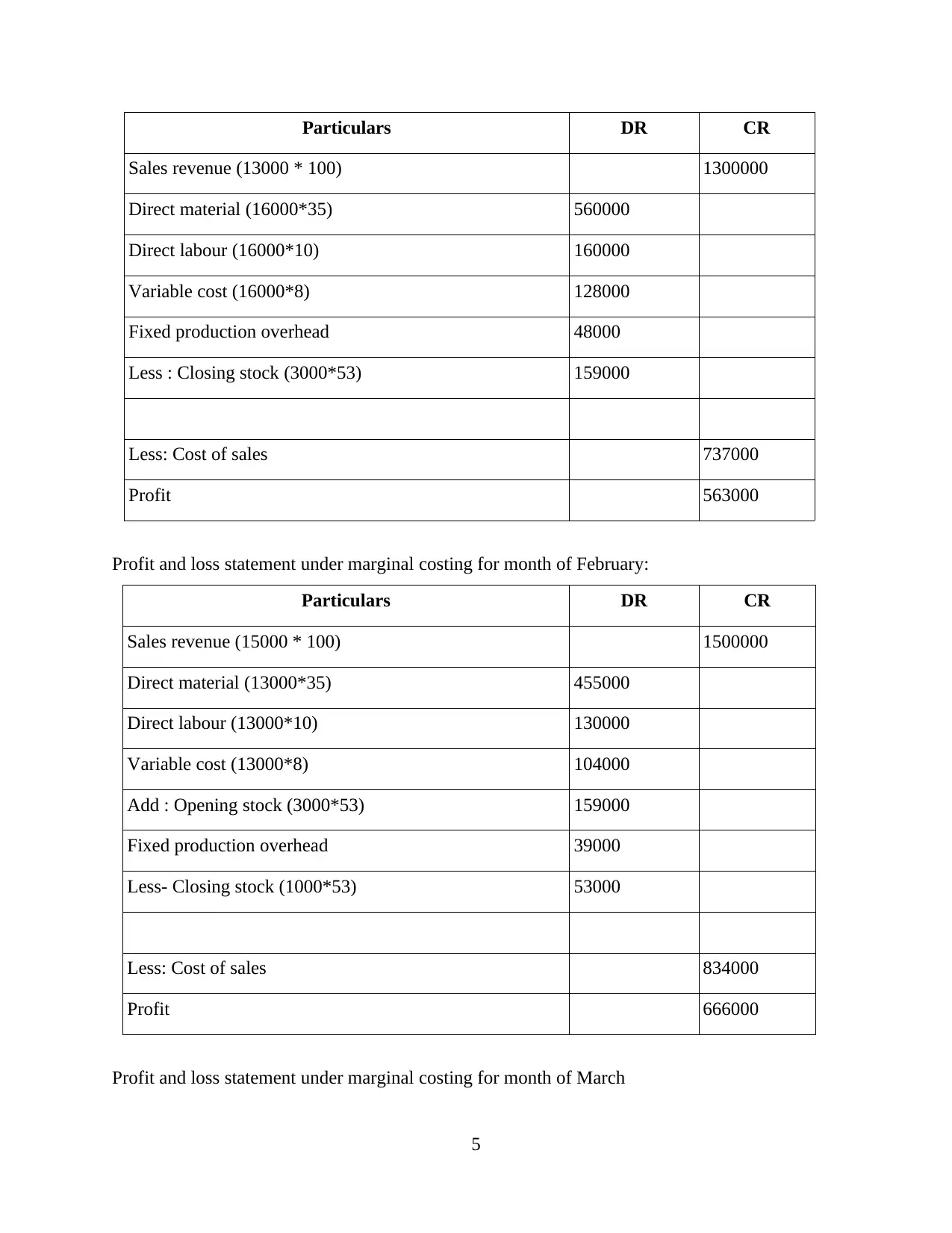

techniques that are discussed underneath: Marginal costing: This is regarded as techniques of cost where variable costs are charged

to unit of cost as well as fixed cost of particular period are written off in against the

aggregative contribution (Otley, 2016). This aids London Clothing Works, to compute

three months income statement.

Absorption costing: It is regarded as techniques which is overall cost of manufacturing is

allotted to the number of units manufactured. This assists London Clothing Works to

prepare income statement by concerning both fixed as well as non fixed costs.

Profit and loss account:

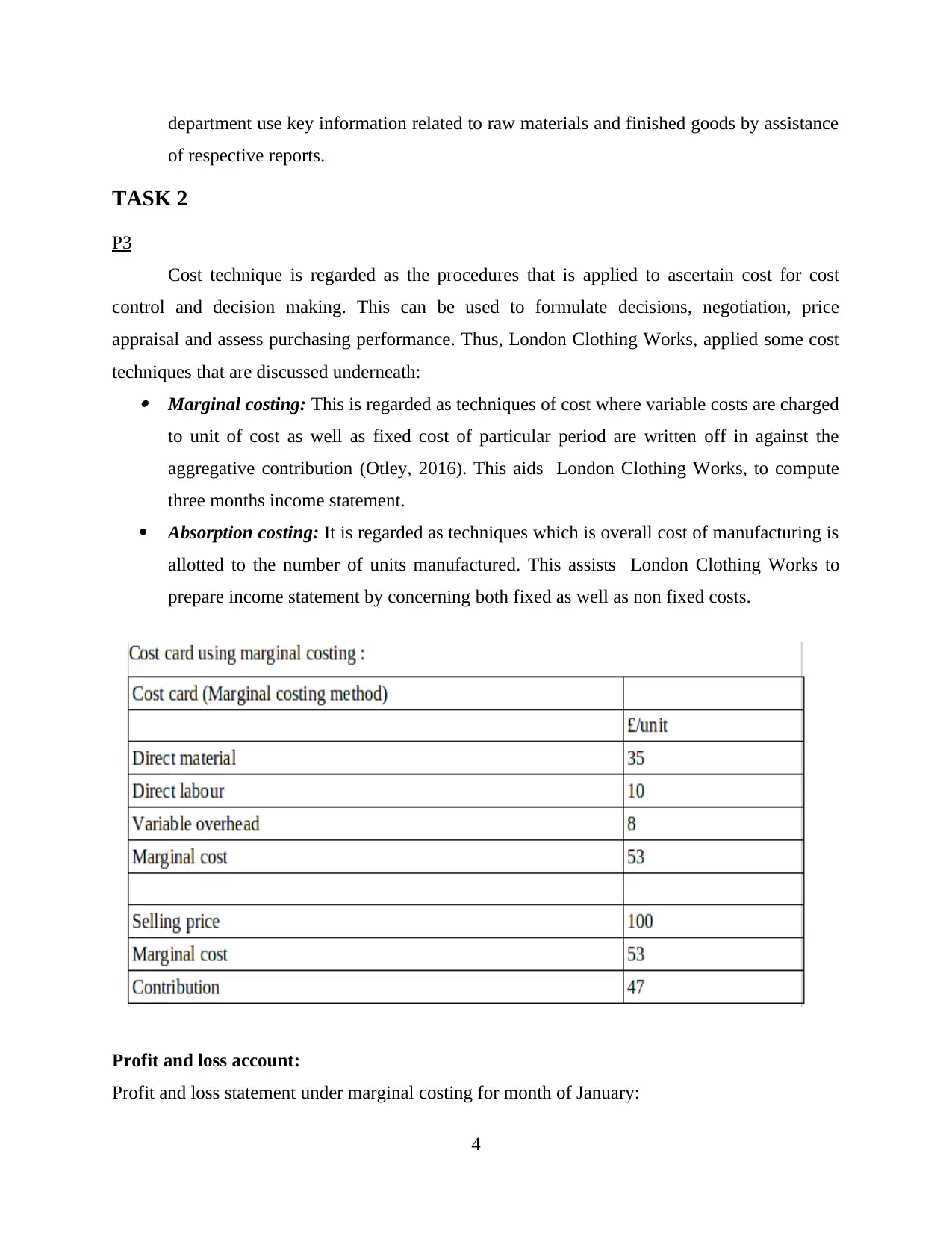

Profit and loss statement under marginal costing for month of January:

4

of respective reports.

TASK 2

P3

Cost technique is regarded as the procedures that is applied to ascertain cost for cost

control and decision making. This can be used to formulate decisions, negotiation, price

appraisal and assess purchasing performance. Thus, London Clothing Works, applied some cost

techniques that are discussed underneath: Marginal costing: This is regarded as techniques of cost where variable costs are charged

to unit of cost as well as fixed cost of particular period are written off in against the

aggregative contribution (Otley, 2016). This aids London Clothing Works, to compute

three months income statement.

Absorption costing: It is regarded as techniques which is overall cost of manufacturing is

allotted to the number of units manufactured. This assists London Clothing Works to

prepare income statement by concerning both fixed as well as non fixed costs.

Profit and loss account:

Profit and loss statement under marginal costing for month of January:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars DR CR

Sales revenue (13000 * 100) 1300000

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Variable cost (16000*8) 128000

Fixed production overhead 48000

Less : Closing stock (3000*53) 159000

Less: Cost of sales 737000

Profit 563000

Profit and loss statement under marginal costing for month of February:

Particulars DR CR

Sales revenue (15000 * 100) 1500000

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Variable cost (13000*8) 104000

Add : Opening stock (3000*53) 159000

Fixed production overhead 39000

Less- Closing stock (1000*53) 53000

Less: Cost of sales 834000

Profit 666000

Profit and loss statement under marginal costing for month of March

5

Sales revenue (13000 * 100) 1300000

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Variable cost (16000*8) 128000

Fixed production overhead 48000

Less : Closing stock (3000*53) 159000

Less: Cost of sales 737000

Profit 563000

Profit and loss statement under marginal costing for month of February:

Particulars DR CR

Sales revenue (15000 * 100) 1500000

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Variable cost (13000*8) 104000

Add : Opening stock (3000*53) 159000

Fixed production overhead 39000

Less- Closing stock (1000*53) 53000

Less: Cost of sales 834000

Profit 666000

Profit and loss statement under marginal costing for month of March

5

Particulars DR CR

Sales revenue (13000 * 100) 1300000

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Variable cost (12000*8) 96000

Add : Opening stock (1000*53) 53000

Fixed production overhead 36000

Less: Cost of sales 725000

Profit 575000

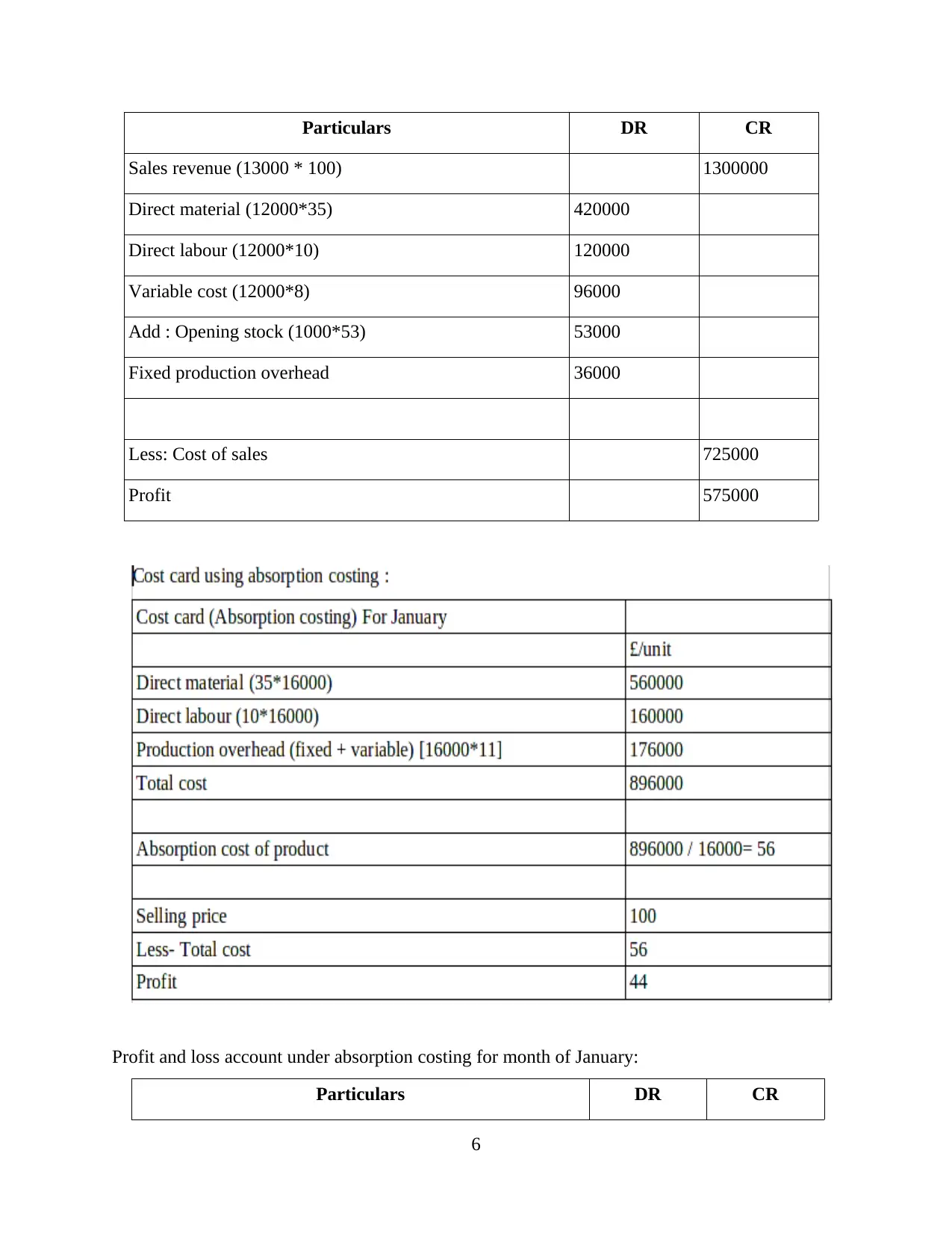

Profit and loss account under absorption costing for month of January:

Particulars DR CR

6

Sales revenue (13000 * 100) 1300000

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Variable cost (12000*8) 96000

Add : Opening stock (1000*53) 53000

Fixed production overhead 36000

Less: Cost of sales 725000

Profit 575000

Profit and loss account under absorption costing for month of January:

Particulars DR CR

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales revenue (13000*100) 1300000

Variable cost:

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Less- Closing stock (3000*53) 159000

Fixed production cost (48000+2000) 50000

Less: cost of sales 611000

Profit 689000

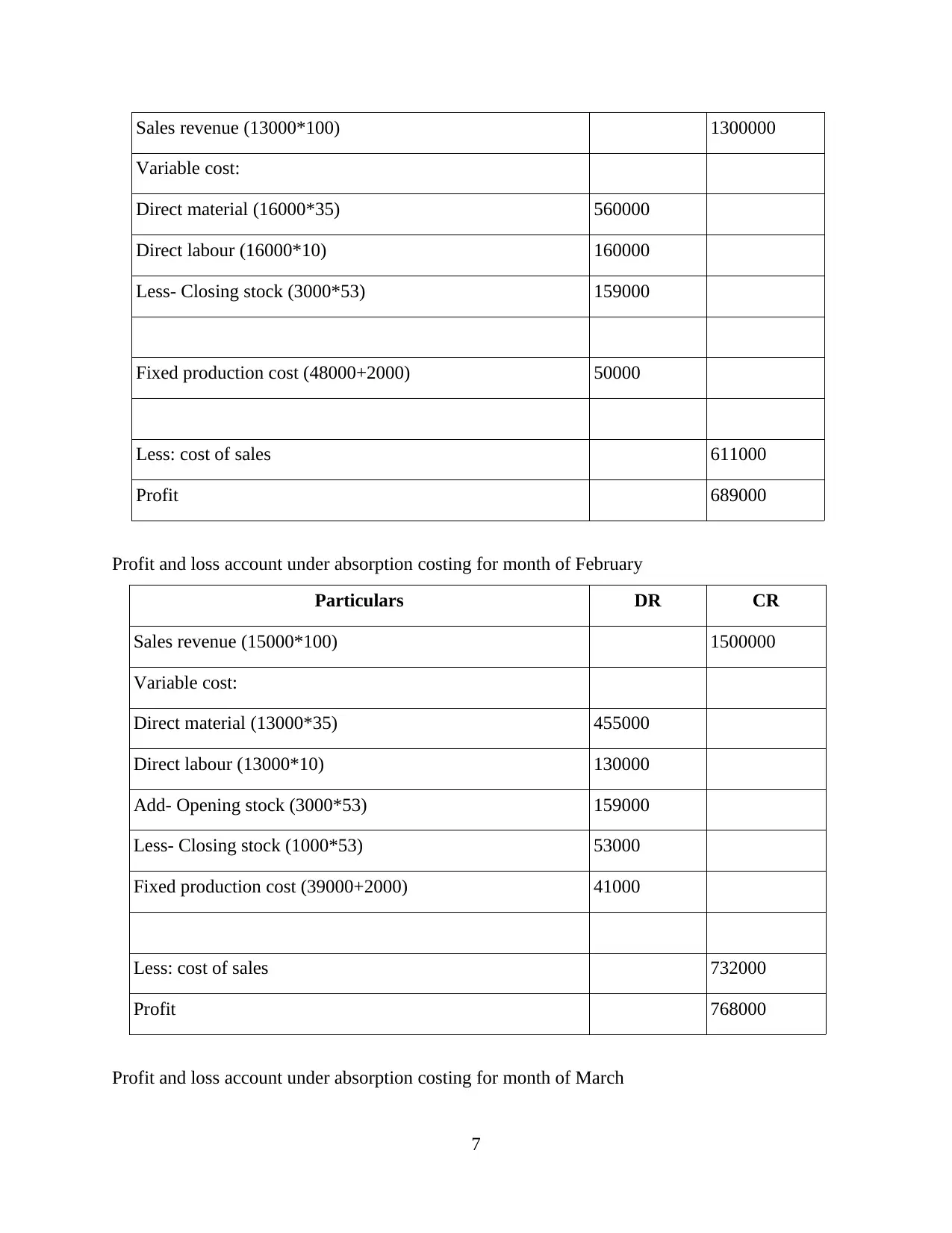

Profit and loss account under absorption costing for month of February

Particulars DR CR

Sales revenue (15000*100) 1500000

Variable cost:

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Add- Opening stock (3000*53) 159000

Less- Closing stock (1000*53) 53000

Fixed production cost (39000+2000) 41000

Less: cost of sales 732000

Profit 768000

Profit and loss account under absorption costing for month of March

7

Variable cost:

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Less- Closing stock (3000*53) 159000

Fixed production cost (48000+2000) 50000

Less: cost of sales 611000

Profit 689000

Profit and loss account under absorption costing for month of February

Particulars DR CR

Sales revenue (15000*100) 1500000

Variable cost:

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Add- Opening stock (3000*53) 159000

Less- Closing stock (1000*53) 53000

Fixed production cost (39000+2000) 41000

Less: cost of sales 732000

Profit 768000

Profit and loss account under absorption costing for month of March

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

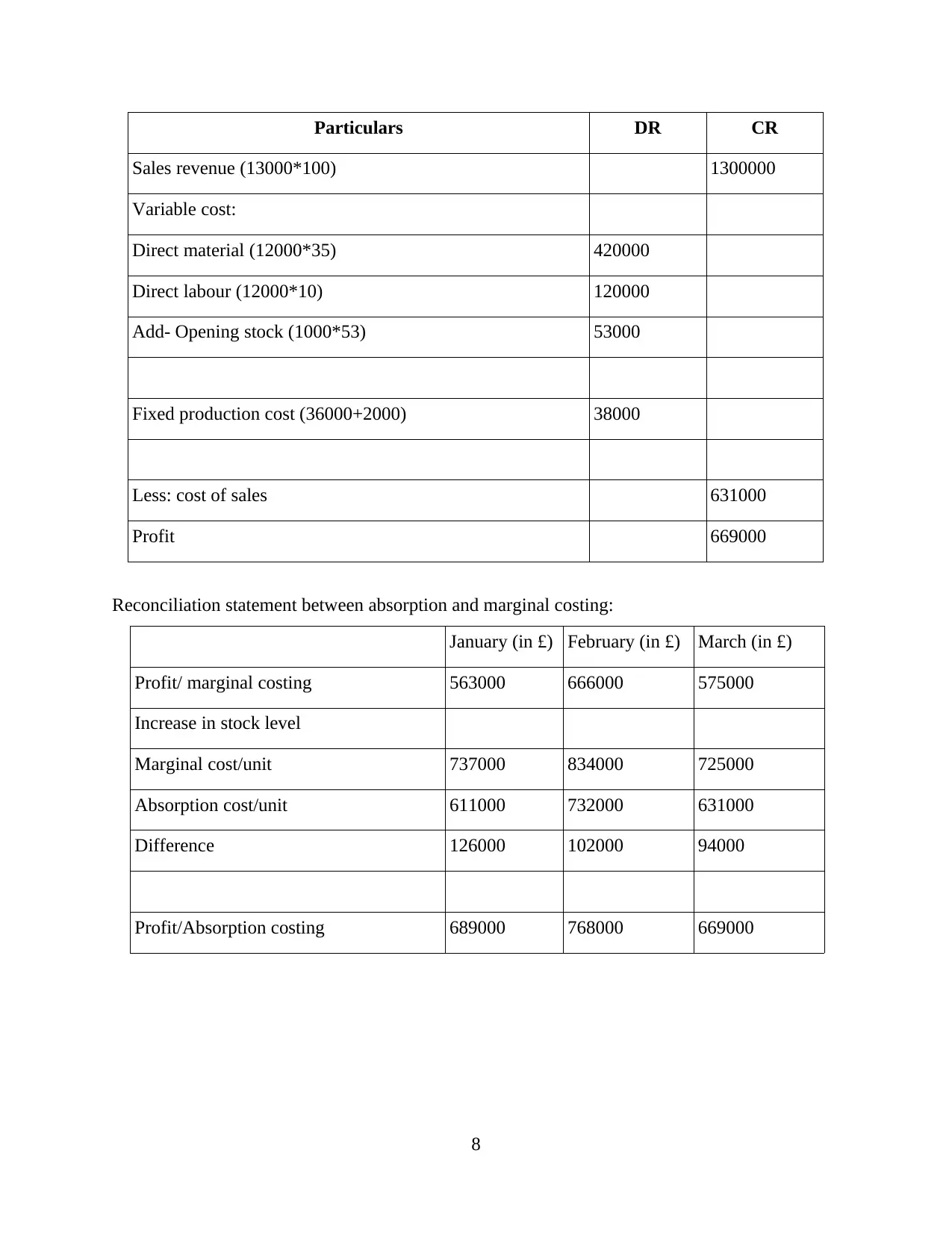

Particulars DR CR

Sales revenue (13000*100) 1300000

Variable cost:

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Add- Opening stock (1000*53) 53000

Fixed production cost (36000+2000) 38000

Less: cost of sales 631000

Profit 669000

Reconciliation statement between absorption and marginal costing:

January (in £) February (in £) March (in £)

Profit/ marginal costing 563000 666000 575000

Increase in stock level

Marginal cost/unit 737000 834000 725000

Absorption cost/unit 611000 732000 631000

Difference 126000 102000 94000

Profit/Absorption costing 689000 768000 669000

8

Sales revenue (13000*100) 1300000

Variable cost:

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Add- Opening stock (1000*53) 53000

Fixed production cost (36000+2000) 38000

Less: cost of sales 631000

Profit 669000

Reconciliation statement between absorption and marginal costing:

January (in £) February (in £) March (in £)

Profit/ marginal costing 563000 666000 575000

Increase in stock level

Marginal cost/unit 737000 834000 725000

Absorption cost/unit 611000 732000 631000

Difference 126000 102000 94000

Profit/Absorption costing 689000 768000 669000

8

TASK 3

P4

Budgetary control is regarded as the methods which is utilised for assuring firm's actual

revenues as well as expenses correspond closely to their financial plan. It includes various

planning tools and few of them are utilised by London Clothing Works are discussed underneath:

Cash budget: This is regarded as planning tools in which cash outflows as well as

inflows of entities details are specified during the budget period like annually, quarterly or

monthly. The main aim of this is to facilitate the status of entities cash position (Pavlatos and

Kostakis, 2015). Therefore, this aids finance department of London Clothing Works to get

knowledge about its organisation's cash position and also make effectual strategies related to

cash. Advantage: This assists London Clothing Works to find potential deficits in quick time

period.

Disadvantage: The main drawbacks is that it is totally based on estimation as this may be

lost in simple way.

Sales budget: It is regarded as the types of budget that consists information related to

expected units of sales and revenue as well as possible expenses that may incurs in selling

methods. Based on this information, entity's manager may formulate their pan of action to

accomplish the targeted sales (Quattrone, 2016). So, London Clothing Works accountant make

this budget as it assists their manufacturing department to take corrective action. Advantage: The sales budget is beneficial for London Clothing Works in order to

delegate resources to many products, services and so on with an aim to realize hoped-for

sales.

Disadvantage: The main drawback of sales budget is, it is prepared based on last data and

in some situation this may leads towards huge financial loses.

Production budget: This is regarded as the forms of budget that consists information

related to expected units of production and possible expenses that may occurs within

manufacturing process. Based on this information, the manger of entities set their plan of action

to accomplish targeted production units. The London Clothing Work accountant prepare this

budget that assists production division to take corrective actions.

9

P4

Budgetary control is regarded as the methods which is utilised for assuring firm's actual

revenues as well as expenses correspond closely to their financial plan. It includes various

planning tools and few of them are utilised by London Clothing Works are discussed underneath:

Cash budget: This is regarded as planning tools in which cash outflows as well as

inflows of entities details are specified during the budget period like annually, quarterly or

monthly. The main aim of this is to facilitate the status of entities cash position (Pavlatos and

Kostakis, 2015). Therefore, this aids finance department of London Clothing Works to get

knowledge about its organisation's cash position and also make effectual strategies related to

cash. Advantage: This assists London Clothing Works to find potential deficits in quick time

period.

Disadvantage: The main drawbacks is that it is totally based on estimation as this may be

lost in simple way.

Sales budget: It is regarded as the types of budget that consists information related to

expected units of sales and revenue as well as possible expenses that may incurs in selling

methods. Based on this information, entity's manager may formulate their pan of action to

accomplish the targeted sales (Quattrone, 2016). So, London Clothing Works accountant make

this budget as it assists their manufacturing department to take corrective action. Advantage: The sales budget is beneficial for London Clothing Works in order to

delegate resources to many products, services and so on with an aim to realize hoped-for

sales.

Disadvantage: The main drawback of sales budget is, it is prepared based on last data and

in some situation this may leads towards huge financial loses.

Production budget: This is regarded as the forms of budget that consists information

related to expected units of production and possible expenses that may occurs within

manufacturing process. Based on this information, the manger of entities set their plan of action

to accomplish targeted production units. The London Clothing Work accountant prepare this

budget that assists production division to take corrective actions.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.