Comprehensive Report on Management Accounting: Systems and Integration

VerifiedAdded on 2023/01/12

|16

|935

|96

Report

AI Summary

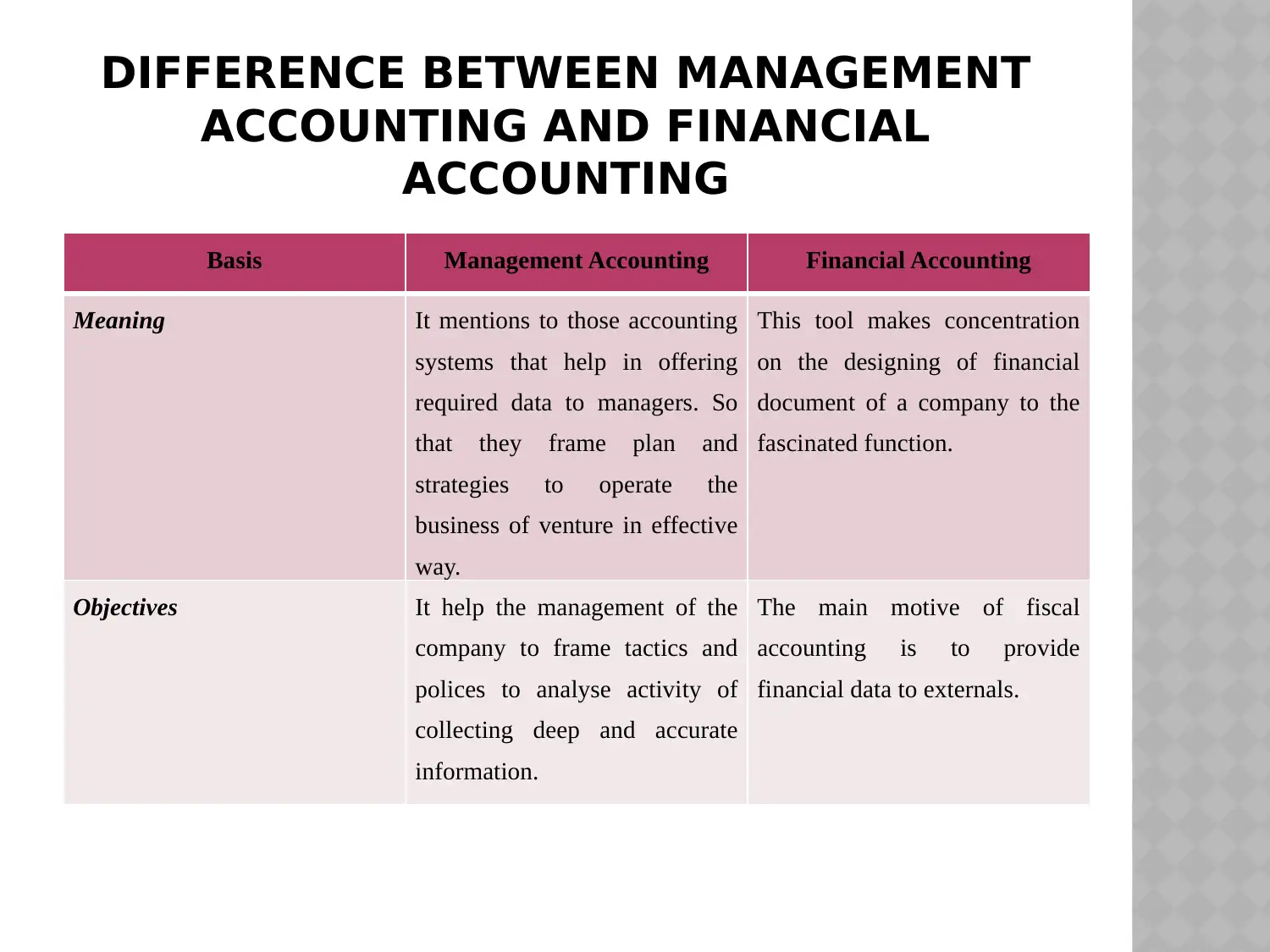

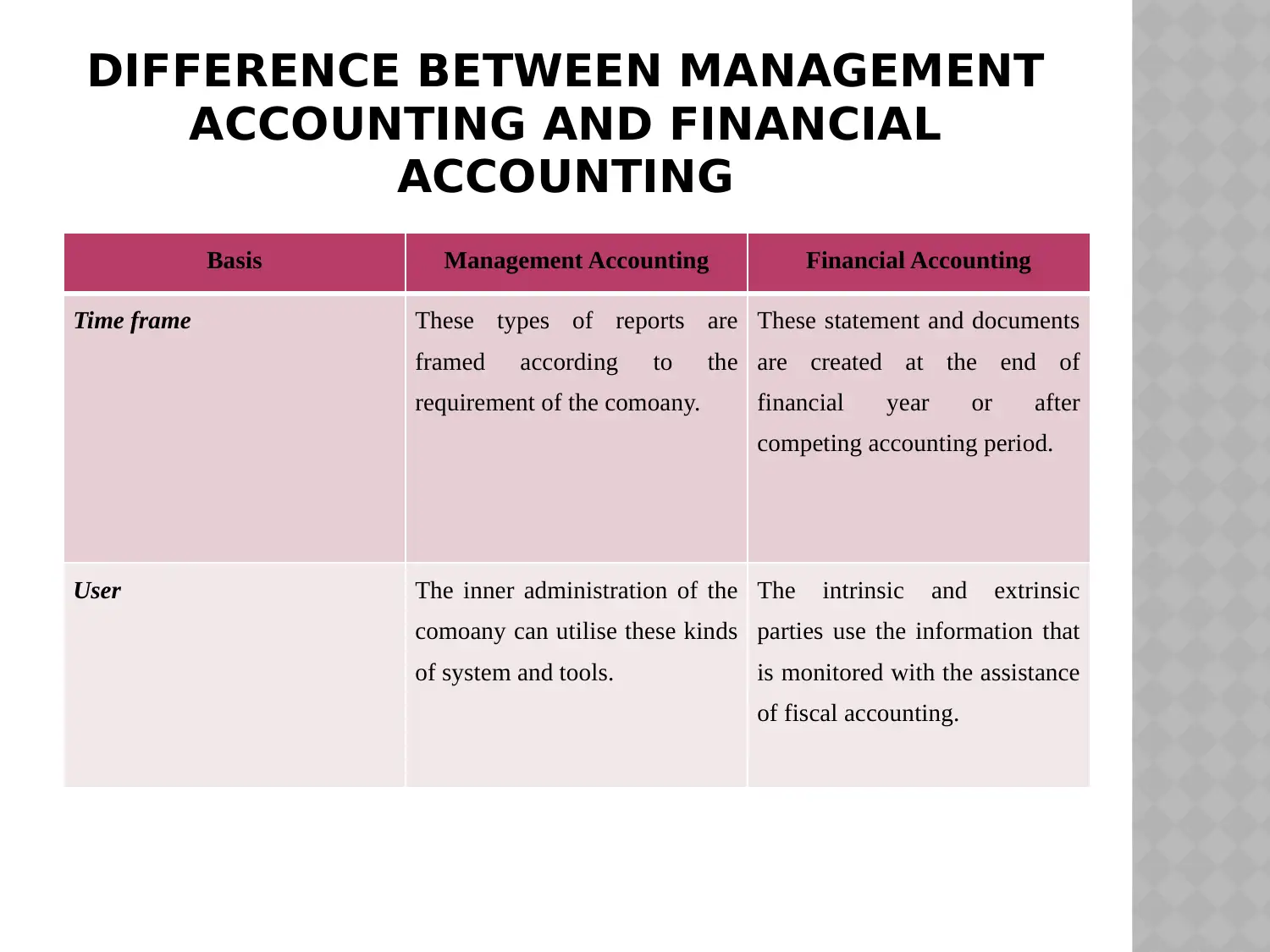

This report provides a comprehensive overview of management accounting, differentiating it from financial accounting and detailing its core components. It explores various management accounting systems, including cost accounting, price optimization, job costing, and inventory management, outlining their functions and benefits. The report further examines management accounting reporting methods such as cost accounting reporting, performance reporting, inventory management reporting, and budget reporting. It also discusses the benefits of management accounting systems and emphasizes the integration between management accounting and organizational structures. The conclusion highlights the importance of management accounting in providing vital information for effective decision-making, supported by relevant references. This report offers valuable insights into the practical applications and significance of management accounting within organizations.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.