Management Accounting Report: TATA Motors Financial Analysis

VerifiedAdded on 2023/03/20

|20

|5188

|82

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within TATA Motors. It begins with an introduction to management accounting, its essential requirements, and a comparison with financial accounting. The report then evaluates different types of management accounting reports, including job cost reports, inventory and manufacturing reports, and accounts receivable reports, highlighting their importance in strategic planning and operational efficiency. The report also explores various management accounting systems, such as inventory management, job costing, and price optimization. The report further delves into the application of absorption and marginal costing techniques and analyzes the use of planning tools for forecasting and budgeting. Finally, the report examines how management accounting systems can respond to financial problems, analyzing financial issues and evaluating the role of planning tools in resolving them. The report concludes by emphasizing the importance of management accounting in enhancing organizational performance and decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and its essential requirements...................................................3

P2 Evaluation of the three different types of management accounting reports......................6

M1...........................................................................................................................................7

M2: Different types of accounting techniques.......................................................................7

D1: Critically evaluation on how management accounting system and its reporting can be

integrated within organisational process................................................................................8

TASK 2............................................................................................................................................8

P3 Application of absorption and marginal costing techniques.............................................8

M3 Analyse the use of various planning tools and its application for forecasting and preparing

budgets..................................................................................................................................11

D2 Data Interpretation..........................................................................................................11

TASK 3..........................................................................................................................................11

P5 Application of management accounting system to respond financial problems.............13

M4 Analyse financial problems, management accounting lead organisations to make success

..............................................................................................................................................14

D3: How planning tools for accounting respond appropriately to resolve financial problems15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and its essential requirements...................................................3

P2 Evaluation of the three different types of management accounting reports......................6

M1...........................................................................................................................................7

M2: Different types of accounting techniques.......................................................................7

D1: Critically evaluation on how management accounting system and its reporting can be

integrated within organisational process................................................................................8

TASK 2............................................................................................................................................8

P3 Application of absorption and marginal costing techniques.............................................8

M3 Analyse the use of various planning tools and its application for forecasting and preparing

budgets..................................................................................................................................11

D2 Data Interpretation..........................................................................................................11

TASK 3..........................................................................................................................................11

P5 Application of management accounting system to respond financial problems.............13

M4 Analyse financial problems, management accounting lead organisations to make success

..............................................................................................................................................14

D3: How planning tools for accounting respond appropriately to resolve financial problems15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a tool which assists the manager of organisation about better

planning of different aspects which ensures higher control over their business operations. It is

refers as the process which involves the aspects regarding identifying, measuring, evaluating,

interpreting and communicating information which is directly or indirectly related to

organisation and contributes in accomplishment of organisational objectives. Application of the

different accounting systems provides opportunity in improvement of the understanding of the

different departments through which their support is ascertain in the completion of common

objectives of organisation. There is huge importance of these systems in the process of providing

effective response to financial issues which results in loss. This will provides the opportunity is

to make the internal structure more strength and reliable. TATA Motors is global brand which

manufactures different utility vehicles according to the needs of customers (Albelda, 2011).

In the present report explain about, application of management accounting systems to

gather different information about organisational performance along with their requirements and

various kind of management accounting reports and their importance. Also, advantages and

disadvantages different kind of budgets and contribution management accounting systems to

respond financial issues.

TASK 1

P1 Management accounting and its essential requirements

Management Accounting: It is important concept which is used by the managers of

TATA Motors is adopt the principles of accounting to improve their information before taking

important decisions in relation to the different matters of organisation. This will helps them to

perform control functions in adequate manner. It is stated by AICPA that the practices of

management accounting used mainly in three area which includes strategic, performance and risk

management.

Definitions

According to IMA, Management accounting is important profession which contributes in

decision-making, planning and management of performance in effective manner. The different

provisions also provide expertise in financial reporting and controlling functions which assist in

the formulation of effective organisational strategy.

Management accounting is a tool which assists the manager of organisation about better

planning of different aspects which ensures higher control over their business operations. It is

refers as the process which involves the aspects regarding identifying, measuring, evaluating,

interpreting and communicating information which is directly or indirectly related to

organisation and contributes in accomplishment of organisational objectives. Application of the

different accounting systems provides opportunity in improvement of the understanding of the

different departments through which their support is ascertain in the completion of common

objectives of organisation. There is huge importance of these systems in the process of providing

effective response to financial issues which results in loss. This will provides the opportunity is

to make the internal structure more strength and reliable. TATA Motors is global brand which

manufactures different utility vehicles according to the needs of customers (Albelda, 2011).

In the present report explain about, application of management accounting systems to

gather different information about organisational performance along with their requirements and

various kind of management accounting reports and their importance. Also, advantages and

disadvantages different kind of budgets and contribution management accounting systems to

respond financial issues.

TASK 1

P1 Management accounting and its essential requirements

Management Accounting: It is important concept which is used by the managers of

TATA Motors is adopt the principles of accounting to improve their information before taking

important decisions in relation to the different matters of organisation. This will helps them to

perform control functions in adequate manner. It is stated by AICPA that the practices of

management accounting used mainly in three area which includes strategic, performance and risk

management.

Definitions

According to IMA, Management accounting is important profession which contributes in

decision-making, planning and management of performance in effective manner. The different

provisions also provide expertise in financial reporting and controlling functions which assist in

the formulation of effective organisational strategy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

According to CIMA, management accounting is the process of identification,

measurement, analysis, preparation, accumulation, interpretation and communication of

information which is used further by the manager of organisation regarding planning and

controlling of different aspects of organisation (Arroyo, 2012 ).

Difference between management and financial accounting

Management Accounting Financial Accounting

This concept helps in internal management It is used regarding providence of the

periodical reports about their financial

performance to owners, creditors and

government

It is related to making of future plans and

policies which assist the employees in

performance of different function in

appropriate manner

The more emphasis is provided to historical

records

These system has limited coverage as it

includes the preparation of different reports in

respect of the performance of departments

This will deals the business as a whole

It is not compulsory adopted within the

organisation in voluntary basis

It is statutory for every business

Functions of management accounting

TATA Motors is branded vehicles company which provides different style of vehicles

according to need of different segment of society. The different types of vehicles which are

provided includes SUV, MUV, hatchback etc. They customised the vehicles according to the

local conditions and perform their work with high standards of quality, safety, environment

norms etc. Implementation of management accounting systems helps to accomplish standards

which are defined about regarding their vehicles through performance of four major functions

through the support of these systems (Baldvinsdottir, Mitchell and Nørreklit, 2010). Such major

functions are defined below:

Planning: It is the process of formulating short and long term plans which assist the

employees of TATA Motors to attain particular end. It is financial planning which shows about

measurement, analysis, preparation, accumulation, interpretation and communication of

information which is used further by the manager of organisation regarding planning and

controlling of different aspects of organisation (Arroyo, 2012 ).

Difference between management and financial accounting

Management Accounting Financial Accounting

This concept helps in internal management It is used regarding providence of the

periodical reports about their financial

performance to owners, creditors and

government

It is related to making of future plans and

policies which assist the employees in

performance of different function in

appropriate manner

The more emphasis is provided to historical

records

These system has limited coverage as it

includes the preparation of different reports in

respect of the performance of departments

This will deals the business as a whole

It is not compulsory adopted within the

organisation in voluntary basis

It is statutory for every business

Functions of management accounting

TATA Motors is branded vehicles company which provides different style of vehicles

according to need of different segment of society. The different types of vehicles which are

provided includes SUV, MUV, hatchback etc. They customised the vehicles according to the

local conditions and perform their work with high standards of quality, safety, environment

norms etc. Implementation of management accounting systems helps to accomplish standards

which are defined about regarding their vehicles through performance of four major functions

through the support of these systems (Baldvinsdottir, Mitchell and Nørreklit, 2010). Such major

functions are defined below:

Planning: It is the process of formulating short and long term plans which assist the

employees of TATA Motors to attain particular end. It is financial planning which shows about

the procedure regarding acquirement of different resources and their application in different

departments over the specified period of time. Management accounting plays an important role

in accounting as it provides information for decision-making.

Organising: It is the important function which is need to perform effectively in TATA

Motors for distribution of the roles and responsibilities among the employees of organisation for

accomplishment of common goals of organisation. It contributes in establishment of effective

organisation structure.

Controlling: It is the process which includes the activities regarding monitoring,

measuring, evaluating and correcting the actual performances of employees to attain business

goals and targets.

Decision-making: Application of the provisions of management accounting systems to

gather information which contributes in selection of best possible choice from large number of

alternatives. It helps to operate their day to day operations effectively (Christ and Burritt, 2013).

Different management accounting systems

TATA is manufacturing organisation which produces different utility vehicles as per the

requirements of customers. To attain the trust and loyalty of customers, it is important to

understand the preferences of customer and bring changes in their functions. It helps to build the

organisational structure more profound. Functions of different systems are defined below:

Inventory management system: This system is used within the organisation for

effective management of stock and non capitalised assets. It helps the manager of TATA Motors

is to track their different stock to ascertain the information about the availability of stock.

Integration of the different provisions of this system with organisational process contributes in

effective flow of inventory within different departments. Th two mail tools which are used in this

regard in TATA Motors includes Just in Time and ABC.

Job costing system: This method is important for TATA Motors to implement because it

manufactures different types of vehicles. This method is used by the manager of TATA Motors

to assign the cost to individuals product and keep effective track on their expenses. This method

provides the opportunity to control unnecessary costs and improve profit margins.

Price optimisation system: It is important to implement this system within TATA

Motors because it helps to attain control over the prices of their different resources. As

competition is high in auto mobile industry, need to adopt effective prices through use of this

departments over the specified period of time. Management accounting plays an important role

in accounting as it provides information for decision-making.

Organising: It is the important function which is need to perform effectively in TATA

Motors for distribution of the roles and responsibilities among the employees of organisation for

accomplishment of common goals of organisation. It contributes in establishment of effective

organisation structure.

Controlling: It is the process which includes the activities regarding monitoring,

measuring, evaluating and correcting the actual performances of employees to attain business

goals and targets.

Decision-making: Application of the provisions of management accounting systems to

gather information which contributes in selection of best possible choice from large number of

alternatives. It helps to operate their day to day operations effectively (Christ and Burritt, 2013).

Different management accounting systems

TATA is manufacturing organisation which produces different utility vehicles as per the

requirements of customers. To attain the trust and loyalty of customers, it is important to

understand the preferences of customer and bring changes in their functions. It helps to build the

organisational structure more profound. Functions of different systems are defined below:

Inventory management system: This system is used within the organisation for

effective management of stock and non capitalised assets. It helps the manager of TATA Motors

is to track their different stock to ascertain the information about the availability of stock.

Integration of the different provisions of this system with organisational process contributes in

effective flow of inventory within different departments. Th two mail tools which are used in this

regard in TATA Motors includes Just in Time and ABC.

Job costing system: This method is important for TATA Motors to implement because it

manufactures different types of vehicles. This method is used by the manager of TATA Motors

to assign the cost to individuals product and keep effective track on their expenses. This method

provides the opportunity to control unnecessary costs and improve profit margins.

Price optimisation system: It is important to implement this system within TATA

Motors because it helps to attain control over the prices of their different resources. As

competition is high in auto mobile industry, need to adopt effective prices through use of this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

system. It helps the manager of organisation is to assess the variation in demand at different

pricing levels.

P2 Evaluation of the three different types of management accounting reports

There are many kind of reports which are formed by the management of TATA Motors

through the information which is gathered from the application of provisions of different

systems. There is huge importance of these kind of reports within TATA Motors regarding

development of the effective strategies and plans for the guidance of employees. It provides the

opportunity regarding building of standards which are required to adhere by the employees in

performance of their different tasks. It enhance the quality of the vehicles which are produced by

TATA Motors through which they attain competitiveness in their operations. There are different

benefits which are associated with the formulation of reports which is attained by TATA Motors

in market includes high market share, high customer base, build good position in market, good

brand image etc. The different kind of reports which are formulated by the manager of TATA

Motors are defined below:

Job cost report: It is one of the important report which refers the activities regarding

identification of cost, expense and profitability of each vehicle which is produced by TATA

Motors. Such kins of evaluation helps the management of organisation is to identify the most

earning segment of vehicle where they need to provide more efforts to make them more better

and satisfy the current trends of market ( DRURY, 2013). These reports has huge contribution in

the process of controlling cost and expenses through removal of such activities which are

unusual.

Inventory and manufacturing reports: These kind of reports are prepared in the big

organisation is to make their inventory and manufacturing process more effective and efficient.

The different information which is contained by this report includes labour cost, per unit

overhead cost, wastages which are happened related to inventory etc. It enhance the decision

making power of the manager of organisation to further use this information regarding its

comparison in different assembly lines which helps in determination of the areas of improvement

which are exploited by the different departs through their bad performance.

Accounts receivable report: It is also one of the kind of report which necessary to

maintain by the manager of TATA Motors for maintaining the liquidity within the organisation

to perform their different functions effectively. Here, debtors of organisation are apportioned on

pricing levels.

P2 Evaluation of the three different types of management accounting reports

There are many kind of reports which are formed by the management of TATA Motors

through the information which is gathered from the application of provisions of different

systems. There is huge importance of these kind of reports within TATA Motors regarding

development of the effective strategies and plans for the guidance of employees. It provides the

opportunity regarding building of standards which are required to adhere by the employees in

performance of their different tasks. It enhance the quality of the vehicles which are produced by

TATA Motors through which they attain competitiveness in their operations. There are different

benefits which are associated with the formulation of reports which is attained by TATA Motors

in market includes high market share, high customer base, build good position in market, good

brand image etc. The different kind of reports which are formulated by the manager of TATA

Motors are defined below:

Job cost report: It is one of the important report which refers the activities regarding

identification of cost, expense and profitability of each vehicle which is produced by TATA

Motors. Such kins of evaluation helps the management of organisation is to identify the most

earning segment of vehicle where they need to provide more efforts to make them more better

and satisfy the current trends of market ( DRURY, 2013). These reports has huge contribution in

the process of controlling cost and expenses through removal of such activities which are

unusual.

Inventory and manufacturing reports: These kind of reports are prepared in the big

organisation is to make their inventory and manufacturing process more effective and efficient.

The different information which is contained by this report includes labour cost, per unit

overhead cost, wastages which are happened related to inventory etc. It enhance the decision

making power of the manager of organisation to further use this information regarding its

comparison in different assembly lines which helps in determination of the areas of improvement

which are exploited by the different departs through their bad performance.

Accounts receivable report: It is also one of the kind of report which necessary to

maintain by the manager of TATA Motors for maintaining the liquidity within the organisation

to perform their different functions effectively. Here, debtors of organisation are apportioned on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the basis of the time period from their their amount is due to pay organisation. It provides the

opportunity regarding bring changes in their credit policies to collect the outstanding amount

within stipulated period of time.

M1

Management accounting system is a part of strategic planning of the company, further it

aids in formulating effective balance sheet and controls purchasing actions. The finance

department of Tata Motors has acquired the concept of management accounting thus to look in

the matter of enhancing performance level of the company. Management accounting plays a

crucial role in decision making process of business organisations by excelling profit margins as

well as raising possibilities to make competitive place over the world. There are various

applications of management accounting, such as - Job cost report, Inventory and manufacturing

reports and accounts receivable report. in which, Job costing is contributes to remove unsual

expenses and controlling costs whereas Inventory and manufacturing reports are beneficial in

recognising the availability of raw materials in order to produce effective products and services.

At last, accounts receivable report helps to understand changes in cash inflows and outflows of

the company. By considering them, management of TATA Motors will take effective financial

decisions.

M2: Different types of accounting techniques

It has been analysed that accounting technique consists of large number of methods that

can be incorporated by companies so as to determine net operating income which can further

influence business operations and profitability as well.

Standard costing: This is determine as an accounting and management tool that assist

company in identifying difference between standard and actual cost of commodities.

Therefore, standard costing is recorded periodically so that variations can be identified

and evaluated.

Marginal costing: This is used for analysing computing net profitability of company that

consist of variable costs which will be required for production. Thus, through this, firm

improves net profit of organisation.

opportunity regarding bring changes in their credit policies to collect the outstanding amount

within stipulated period of time.

M1

Management accounting system is a part of strategic planning of the company, further it

aids in formulating effective balance sheet and controls purchasing actions. The finance

department of Tata Motors has acquired the concept of management accounting thus to look in

the matter of enhancing performance level of the company. Management accounting plays a

crucial role in decision making process of business organisations by excelling profit margins as

well as raising possibilities to make competitive place over the world. There are various

applications of management accounting, such as - Job cost report, Inventory and manufacturing

reports and accounts receivable report. in which, Job costing is contributes to remove unsual

expenses and controlling costs whereas Inventory and manufacturing reports are beneficial in

recognising the availability of raw materials in order to produce effective products and services.

At last, accounts receivable report helps to understand changes in cash inflows and outflows of

the company. By considering them, management of TATA Motors will take effective financial

decisions.

M2: Different types of accounting techniques

It has been analysed that accounting technique consists of large number of methods that

can be incorporated by companies so as to determine net operating income which can further

influence business operations and profitability as well.

Standard costing: This is determine as an accounting and management tool that assist

company in identifying difference between standard and actual cost of commodities.

Therefore, standard costing is recorded periodically so that variations can be identified

and evaluated.

Marginal costing: This is used for analysing computing net profitability of company that

consist of variable costs which will be required for production. Thus, through this, firm

improves net profit of organisation.

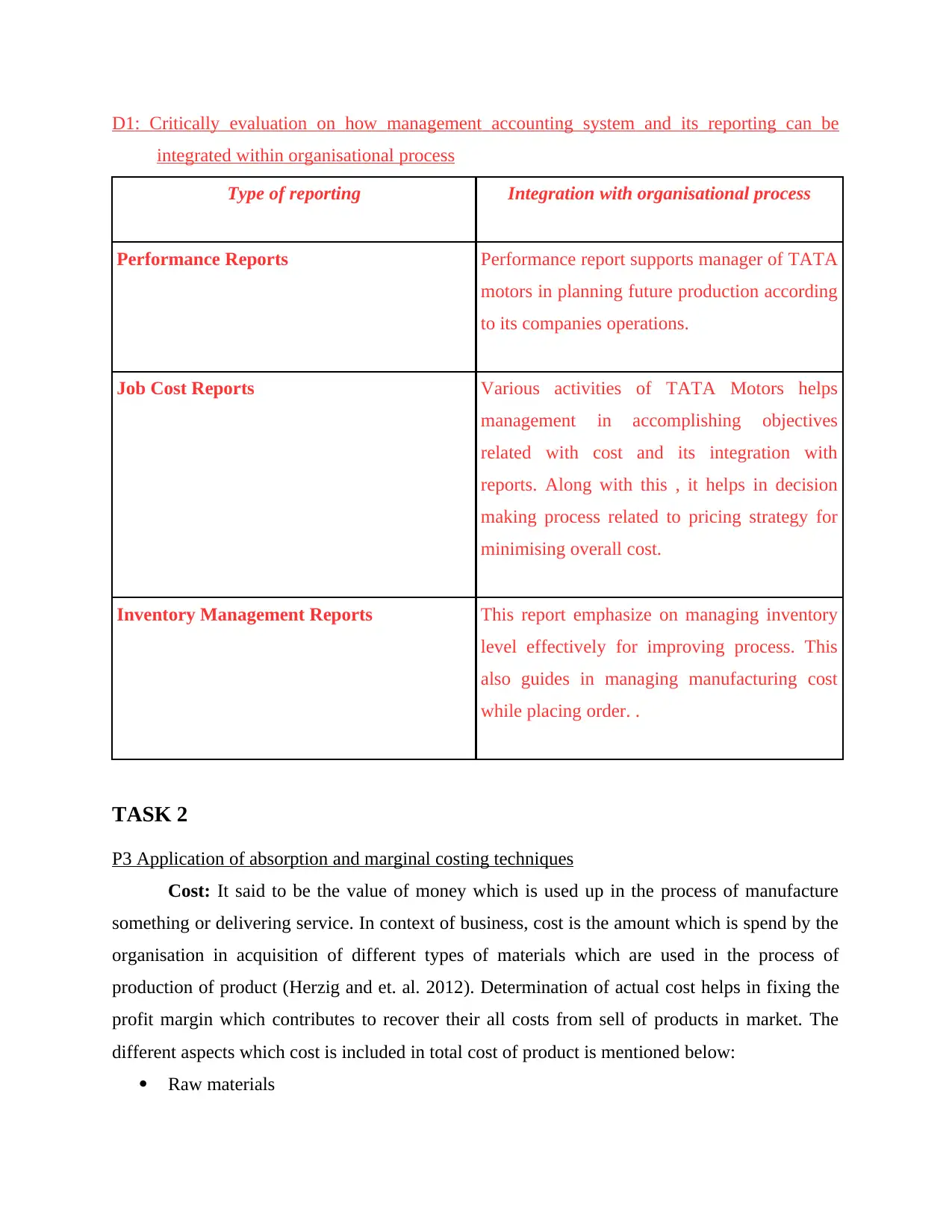

D1: Critically evaluation on how management accounting system and its reporting can be

integrated within organisational process

Type of reporting Integration with organisational process

Performance Reports Performance report supports manager of TATA

motors in planning future production according

to its companies operations.

Job Cost Reports Various activities of TATA Motors helps

management in accomplishing objectives

related with cost and its integration with

reports. Along with this , it helps in decision

making process related to pricing strategy for

minimising overall cost.

Inventory Management Reports This report emphasize on managing inventory

level effectively for improving process. This

also guides in managing manufacturing cost

while placing order. .

TASK 2

P3 Application of absorption and marginal costing techniques

Cost: It said to be the value of money which is used up in the process of manufacture

something or delivering service. In context of business, cost is the amount which is spend by the

organisation in acquisition of different types of materials which are used in the process of

production of product (Herzig and et. al. 2012). Determination of actual cost helps in fixing the

profit margin which contributes to recover their all costs from sell of products in market. The

different aspects which cost is included in total cost of product is mentioned below:

Raw materials

integrated within organisational process

Type of reporting Integration with organisational process

Performance Reports Performance report supports manager of TATA

motors in planning future production according

to its companies operations.

Job Cost Reports Various activities of TATA Motors helps

management in accomplishing objectives

related with cost and its integration with

reports. Along with this , it helps in decision

making process related to pricing strategy for

minimising overall cost.

Inventory Management Reports This report emphasize on managing inventory

level effectively for improving process. This

also guides in managing manufacturing cost

while placing order. .

TASK 2

P3 Application of absorption and marginal costing techniques

Cost: It said to be the value of money which is used up in the process of manufacture

something or delivering service. In context of business, cost is the amount which is spend by the

organisation in acquisition of different types of materials which are used in the process of

production of product (Herzig and et. al. 2012). Determination of actual cost helps in fixing the

profit margin which contributes to recover their all costs from sell of products in market. The

different aspects which cost is included in total cost of product is mentioned below:

Raw materials

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Time

Labour

Risk

Opportunity cost

The costs are further classified into fixed and variable. Fixed costs are such which remain

constant over the period of time and not change with the change in the production level. The

different costs which are considered under this includes rent, depreciation etc. On the other hand

variable cost is such which varies with the change in production level.

Absorption costing: As per this method, all off the manufacturing cost are apportioned

to the units which are produced within the organisation. This will provides the cost of finished

product includes the amount which is spent upon direct materials, labour and variable and fixed

overhead. It is full costing method where all the costs are included whether fixed or variable in

nature in the total cost of product. This method of costing is more significant for external

reporting and income tax reporting. It assists the management of TATA Motors in improvement

of the long term decision making of management (Kotas, 2014).

Marginal costing: It is variable costing method which consider only variable cost in the

process of calculation of cost of product. According the provisions of this method only variable

cost is distributed to the units and fixed cost is write-off against contribution. This will improves

short term decision making power of manager of TATA Motors regarding determination of the

change in cost if one extra unit of good is produced.

Difference between marginal and absorption costing

Marginal costing Absorption costing

Apportionment of only direct cost into the cost

of product

Charging of all manufacturing cost to cost of

production whether in fixed or variable

The amount of cost which is ascertained from

the use of this method is lower in comparison

to absorption method

The cost of product is higher in this method

because involvement of fixed cost

The value of closing stock which is ascertained

from this method is lower then absorption

costing

The value of closing stock is higher

Labour

Risk

Opportunity cost

The costs are further classified into fixed and variable. Fixed costs are such which remain

constant over the period of time and not change with the change in the production level. The

different costs which are considered under this includes rent, depreciation etc. On the other hand

variable cost is such which varies with the change in production level.

Absorption costing: As per this method, all off the manufacturing cost are apportioned

to the units which are produced within the organisation. This will provides the cost of finished

product includes the amount which is spent upon direct materials, labour and variable and fixed

overhead. It is full costing method where all the costs are included whether fixed or variable in

nature in the total cost of product. This method of costing is more significant for external

reporting and income tax reporting. It assists the management of TATA Motors in improvement

of the long term decision making of management (Kotas, 2014).

Marginal costing: It is variable costing method which consider only variable cost in the

process of calculation of cost of product. According the provisions of this method only variable

cost is distributed to the units and fixed cost is write-off against contribution. This will improves

short term decision making power of manager of TATA Motors regarding determination of the

change in cost if one extra unit of good is produced.

Difference between marginal and absorption costing

Marginal costing Absorption costing

Apportionment of only direct cost into the cost

of product

Charging of all manufacturing cost to cost of

production whether in fixed or variable

The amount of cost which is ascertained from

the use of this method is lower in comparison

to absorption method

The cost of product is higher in this method

because involvement of fixed cost

The value of closing stock which is ascertained

from this method is lower then absorption

costing

The value of closing stock is higher

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

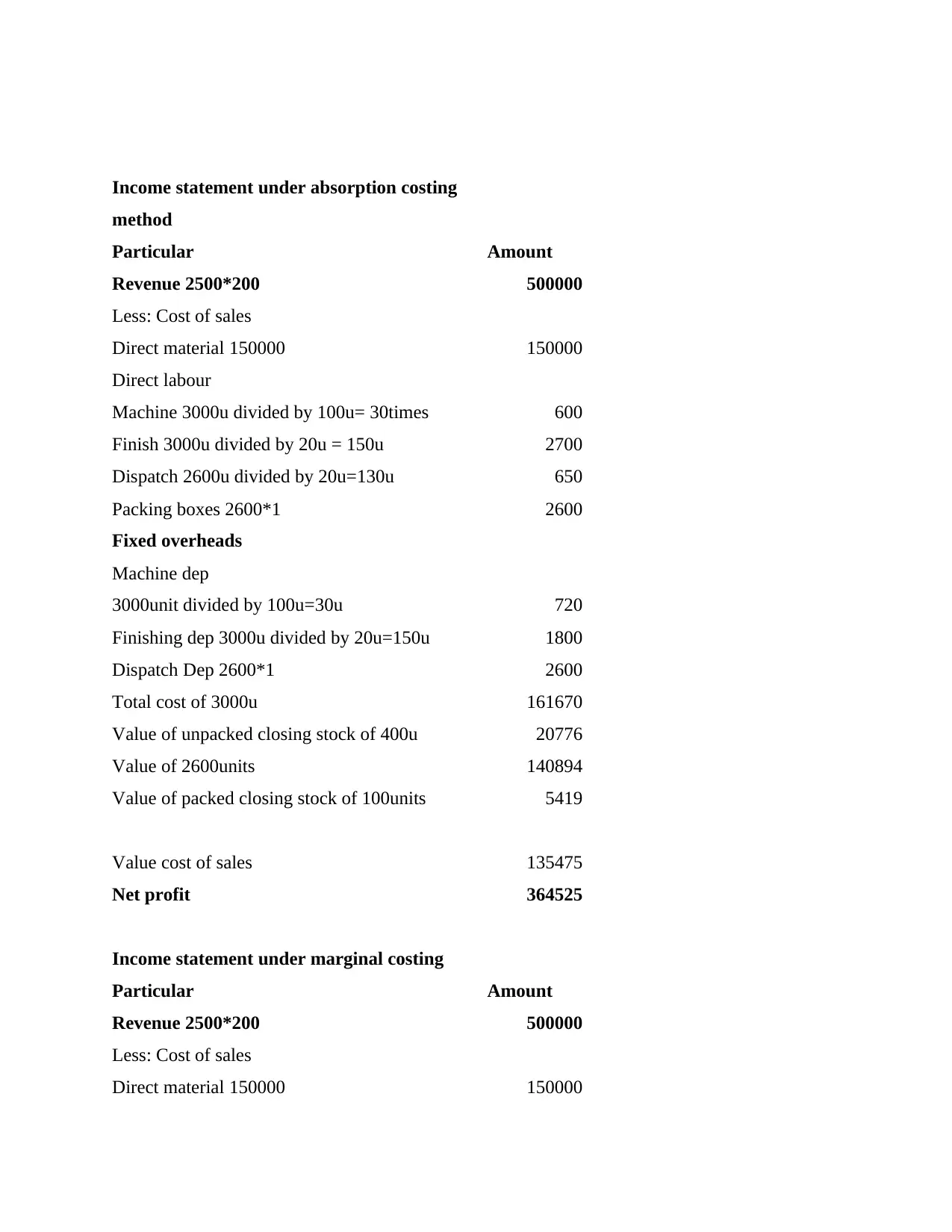

Income statement under absorption costing

method

Particular Amount

Revenue 2500*200 500000

Less: Cost of sales

Direct material 150000 150000

Direct labour

Machine 3000u divided by 100u= 30times 600

Finish 3000u divided by 20u = 150u 2700

Dispatch 2600u divided by 20u=130u 650

Packing boxes 2600*1 2600

Fixed overheads

Machine dep

3000unit divided by 100u=30u 720

Finishing dep 3000u divided by 20u=150u 1800

Dispatch Dep 2600*1 2600

Total cost of 3000u 161670

Value of unpacked closing stock of 400u 20776

Value of 2600units 140894

Value of packed closing stock of 100units 5419

Value cost of sales 135475

Net profit 364525

Income statement under marginal costing

Particular Amount

Revenue 2500*200 500000

Less: Cost of sales

Direct material 150000 150000

method

Particular Amount

Revenue 2500*200 500000

Less: Cost of sales

Direct material 150000 150000

Direct labour

Machine 3000u divided by 100u= 30times 600

Finish 3000u divided by 20u = 150u 2700

Dispatch 2600u divided by 20u=130u 650

Packing boxes 2600*1 2600

Fixed overheads

Machine dep

3000unit divided by 100u=30u 720

Finishing dep 3000u divided by 20u=150u 1800

Dispatch Dep 2600*1 2600

Total cost of 3000u 161670

Value of unpacked closing stock of 400u 20776

Value of 2600units 140894

Value of packed closing stock of 100units 5419

Value cost of sales 135475

Net profit 364525

Income statement under marginal costing

Particular Amount

Revenue 2500*200 500000

Less: Cost of sales

Direct material 150000 150000

Direct labour

Machine dep 3000u*100=30 600

Finishing dep 3000u*20u=150times 2700

Dispatch 2600u*1 2600

Fixed overheads

Machine dep 720

Finish dep 1800

Dispatch 2600u divided by 20u=130u 5120

Total cost for 3000u*400 20440

Value of 2600units 136110

Closing stock for 100untis packed 5235

Variable value cost of sales 2500units 130875

Total net profit 364005

M3 Analyse the use of various planning tools and its application for forecasting and preparing

budgets

In Tata Motors, planning tools are adopted by organisation in order to have knowledge about

buyers needs. Along with this, management need to make system as per crisis which have

changes of occur in future. It will help top authority in budgetary control from future and past

trends. In this, it separate funds limit which is set by every activity in order to run proper

activities of enterprise. Along with this, risk and uncertainties have possibility in future are

acknowledged which gave advantage to administration in order to take decisions. Hence,

management can make effective use of resources as well as organise operations as per market

situations.

D2 Data Interpretation

With the help of income statement, it has been interpreted that under absorption costing

method the net profit was calculated in the amount of £364525 by TATA Motors. On the other

hand, based on marginal costing it has been calculated that net profit that was made by this

organisation was in amount of £364005.

Machine dep 3000u*100=30 600

Finishing dep 3000u*20u=150times 2700

Dispatch 2600u*1 2600

Fixed overheads

Machine dep 720

Finish dep 1800

Dispatch 2600u divided by 20u=130u 5120

Total cost for 3000u*400 20440

Value of 2600units 136110

Closing stock for 100untis packed 5235

Variable value cost of sales 2500units 130875

Total net profit 364005

M3 Analyse the use of various planning tools and its application for forecasting and preparing

budgets

In Tata Motors, planning tools are adopted by organisation in order to have knowledge about

buyers needs. Along with this, management need to make system as per crisis which have

changes of occur in future. It will help top authority in budgetary control from future and past

trends. In this, it separate funds limit which is set by every activity in order to run proper

activities of enterprise. Along with this, risk and uncertainties have possibility in future are

acknowledged which gave advantage to administration in order to take decisions. Hence,

management can make effective use of resources as well as organise operations as per market

situations.

D2 Data Interpretation

With the help of income statement, it has been interpreted that under absorption costing

method the net profit was calculated in the amount of £364525 by TATA Motors. On the other

hand, based on marginal costing it has been calculated that net profit that was made by this

organisation was in amount of £364005.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.