Management Accounting: Systems, Methods, and Reporting for Creams Ltd

VerifiedAdded on 2023/01/11

|19

|5207

|30

Report

AI Summary

This report provides a detailed analysis of management accounting, focusing on its core principles, systems, and reporting methods. It explores essential requirements of management accounting systems, including cost accounting, inventory management, job costing, and price optimization. The report examines different costing methods and their application in generating financial reporting statements. It also delves into planning tools used for budgetary control, evaluating their advantages and disadvantages. Furthermore, the report investigates how organizations, specifically Creams Ltd, utilize management accounting systems to address and resolve financial problems, including an evaluation of appropriate planning tools and their role in achieving sustainable success. The analysis covers various reporting methods, such as job cost reports, inventory management reports, operating budget reports, and accounts receivable aging reports, highlighting their significance in decision-making processes. The report concludes with an overview of the benefits of management accounting systems and their impact on organizational performance and profitability.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

TASK 1............................................................................................................................................1

P1. Explain management accounting and essential requirement of management accounting

systems.........................................................................................................................................1

M1. Benefit of management accounting systems........................................................................3

D1. Evaluate how accounting systems linked with accounting reports.......................................4

P2. Different method used for management accounting reporting..............................................4

TASK 2............................................................................................................................................5

P3. Calculate cost by using different costing method..................................................................5

M2. Apply range of management accounting techniques and generate financial reporting

statements....................................................................................................................................8

D2.Produce financial reports that accurately apply and interpret data for a range of business

activities.......................................................................................................................................8

TASK 3............................................................................................................................................8

P4. Explain advantage or disadvantage of different planning tools used for budgetary control. 8

M3. Evaluate the use of different planning tools and preparing budgets for forecasting..........11

TASK 4..........................................................................................................................................11

P5. Explain how organizations follow management accounting systems to response their

financial problems.....................................................................................................................11

M4. Evaluate that how organizations responding to their financial problems..........................13

D3. Evaluate planning tools appropriately and how it used to solving financial problems to

lead organizations towards sustainable success.........................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

MAIN BODY..................................................................................................................................1

TASK 1............................................................................................................................................1

P1. Explain management accounting and essential requirement of management accounting

systems.........................................................................................................................................1

M1. Benefit of management accounting systems........................................................................3

D1. Evaluate how accounting systems linked with accounting reports.......................................4

P2. Different method used for management accounting reporting..............................................4

TASK 2............................................................................................................................................5

P3. Calculate cost by using different costing method..................................................................5

M2. Apply range of management accounting techniques and generate financial reporting

statements....................................................................................................................................8

D2.Produce financial reports that accurately apply and interpret data for a range of business

activities.......................................................................................................................................8

TASK 3............................................................................................................................................8

P4. Explain advantage or disadvantage of different planning tools used for budgetary control. 8

M3. Evaluate the use of different planning tools and preparing budgets for forecasting..........11

TASK 4..........................................................................................................................................11

P5. Explain how organizations follow management accounting systems to response their

financial problems.....................................................................................................................11

M4. Evaluate that how organizations responding to their financial problems..........................13

D3. Evaluate planning tools appropriately and how it used to solving financial problems to

lead organizations towards sustainable success.........................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial accounting is the methodology to classify, calculate, assess, evaluate, and

convey financial reports to management to achieve the goals of an entity. It distinguishes from

financial accounting because both have different purpose (Bottomley and Bosman, 2018).

Management accounting analyzes and outcomes are managed to keep in house for corporate

leaders that can be used to take part in decision-making process and better run the company.

Management accountants tackle countless important aspects of accounting. That includes

margin, restrictions, financial planning, trends and predictions, pricing and costing of the goods.

For the better understanding of management accounting, Creams Ltd selected which is UK based

food manufacturing company.

This assessment covers the several topics such as understanding of management accounting

systems, reporting methods, costing methods and planning tools which used to budgetary

control. In addition, it includes that how organizations resolve their financial issues by using

management accounting systems.

MAIN BODY

TASK 1

P1. Explain management accounting and essential requirement of management accounting

systems

Management accounting involves evaluating and reporting corporate operations that can

be used by internal users to maximize performance and profitability. It is the analysis of

accounting material to establish the company's policies to be accepted and to support its daily

basis activities (Fleischman and McLean, 2020). In other words, it enables administrators

to fulfil all of their tasks including arranging, scheduling, hiring, overseeing and governing.

Importance of management accounting:

Management accountants deliver crucial viewpoints which allow the executive team of a

company to make much of its decisions. By offering a variety of monetary and numerical

knowledge, frequently supported by powerful accounting tools, they even facilitate decision

making process within the organization. Management accountancy should send everyone all the

monetary and business-critical data that help managers to determine precisely what goods are

competitive, which weren't, and how to fix that. It can help to discover important metrics to

1

Managerial accounting is the methodology to classify, calculate, assess, evaluate, and

convey financial reports to management to achieve the goals of an entity. It distinguishes from

financial accounting because both have different purpose (Bottomley and Bosman, 2018).

Management accounting analyzes and outcomes are managed to keep in house for corporate

leaders that can be used to take part in decision-making process and better run the company.

Management accountants tackle countless important aspects of accounting. That includes

margin, restrictions, financial planning, trends and predictions, pricing and costing of the goods.

For the better understanding of management accounting, Creams Ltd selected which is UK based

food manufacturing company.

This assessment covers the several topics such as understanding of management accounting

systems, reporting methods, costing methods and planning tools which used to budgetary

control. In addition, it includes that how organizations resolve their financial issues by using

management accounting systems.

MAIN BODY

TASK 1

P1. Explain management accounting and essential requirement of management accounting

systems

Management accounting involves evaluating and reporting corporate operations that can

be used by internal users to maximize performance and profitability. It is the analysis of

accounting material to establish the company's policies to be accepted and to support its daily

basis activities (Fleischman and McLean, 2020). In other words, it enables administrators

to fulfil all of their tasks including arranging, scheduling, hiring, overseeing and governing.

Importance of management accounting:

Management accountants deliver crucial viewpoints which allow the executive team of a

company to make much of its decisions. By offering a variety of monetary and numerical

knowledge, frequently supported by powerful accounting tools, they even facilitate decision

making process within the organization. Management accountancy should send everyone all the

monetary and business-critical data that help managers to determine precisely what goods are

competitive, which weren't, and how to fix that. It can help to discover important metrics to

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

know how choices make have impacted the productivity of an individual product or performance

of individual.

Management accounting systems include the several approaches which help the

organization to operate their business performance effectively or maximise the profit. It includes

several systems such as cost accounting, inventory management, price optimization etc. these are

discussed below:

Cost accounting system: It is the accounting system which is used by incorporates for a

range of operations and monetary considerations. It is important for companies to estimate costs

and try to control for the entire period of production (Feldman and Paul, 2019). In the sense of

Creams Ltd, this accounting system is used to hold the operating expenses below the expected

costs. This system's primary purpose is to focus as much as possible on keeping down the costs

of different activities. This system essentially desired by Creams Ltd to calculate the cost of their

good or service and ensure that the manufacturing costs will not surpass it. Otherwise it

minimizes the gross margin that is not beneficial for the companies to run its manufacturing for

far too long.

Inventory management system: A tool for increased supply protection across the firm's

delivery chain is called inventory management system. In Creams Ltd, the the whole sales

process is monitored by this method from placing orders to suppliers and made the entire path

from business to the customer. The inventory management software involves important

methodologies likes LIFO, FIFO and Average Cost. It is critical that companies take corrective

measures to manage stored inventories. Cream Ltd follows FIFO method to avoid

unnecessary wastage or physical damage of raw material. Because of that, the corporation

essentially required this system and keep monitor of its inventory position that helps in

making further purchasing decisions appropriately.

Job costing system: The job order costing system monitors the costs of every task inside

the organization. Management must track the expenses of each job carefully and determine if the

actual costs generated are fairly similar and the expected costs are higher. Significant cost

deficiencies will allow managers to identify and implement constructive steps to mitigate the

cause of increased costs (Hicks and et.al., 2019). This approach collects and consumes costs

relating to particular jobs, tasks or work commands. The cost of each task is calculated

accurately, and each work is decided independently. Using this method, Cream Ltd's managers

2

of individual.

Management accounting systems include the several approaches which help the

organization to operate their business performance effectively or maximise the profit. It includes

several systems such as cost accounting, inventory management, price optimization etc. these are

discussed below:

Cost accounting system: It is the accounting system which is used by incorporates for a

range of operations and monetary considerations. It is important for companies to estimate costs

and try to control for the entire period of production (Feldman and Paul, 2019). In the sense of

Creams Ltd, this accounting system is used to hold the operating expenses below the expected

costs. This system's primary purpose is to focus as much as possible on keeping down the costs

of different activities. This system essentially desired by Creams Ltd to calculate the cost of their

good or service and ensure that the manufacturing costs will not surpass it. Otherwise it

minimizes the gross margin that is not beneficial for the companies to run its manufacturing for

far too long.

Inventory management system: A tool for increased supply protection across the firm's

delivery chain is called inventory management system. In Creams Ltd, the the whole sales

process is monitored by this method from placing orders to suppliers and made the entire path

from business to the customer. The inventory management software involves important

methodologies likes LIFO, FIFO and Average Cost. It is critical that companies take corrective

measures to manage stored inventories. Cream Ltd follows FIFO method to avoid

unnecessary wastage or physical damage of raw material. Because of that, the corporation

essentially required this system and keep monitor of its inventory position that helps in

making further purchasing decisions appropriately.

Job costing system: The job order costing system monitors the costs of every task inside

the organization. Management must track the expenses of each job carefully and determine if the

actual costs generated are fairly similar and the expected costs are higher. Significant cost

deficiencies will allow managers to identify and implement constructive steps to mitigate the

cause of increased costs (Hicks and et.al., 2019). This approach collects and consumes costs

relating to particular jobs, tasks or work commands. The cost of each task is calculated

accurately, and each work is decided independently. Using this method, Cream Ltd's managers

2

will implement successful techniques that are effectively essential to assess each expense of the

order and take corrective action.

Price optimization system: This is a form of controlling system that provides a

comprehensive pricing structure and criteria for customer satisfaction. This accounting approach

helps businesses to get useful industry patterns and consumer demand knowledge. It is

essentially important for enterprises to modify the level of goods and services throughout the

market. In the case of chosen company, management team changes pricing methods according to

the customer's wishes. With the help of price optimization system, managers are able to fix

product or service price which satisfies both buyers as well as business goals. This

system essentially allowed setting appropriate prices that increase the ability of consumers to buy

products and services.

Essential requirement of management accounting systems:

Management accounting systems (MAS) are basically necessary by the company to make

sure the available records will be credible, correct, presentable, revised and in understandable

form. So people can understand and further managers of Cream Ltd may use this knowledge in

decision making process.

Accurate: All details should be accurate in MAS as executives take business decisions

which are based on it.

Reliable: Accounting records should be reliable and an important aspect of management

accounting. It assists in determining real financial status of the Cream Ltd in terms of

revenue.

Presentable: All the accounting information should be represented in common format

layout and organizations widely use the common standard for reporting.

Updated and on time: In the financial report, data reported on monthly or annual basis

as management of Cream Ltd take decisions based of it and it is an ultimately necessary

for decision taking mechanism to have additional updated information.

Reasonable and relevant: Information should be reported in understandable way, so

users of Cream Ltd can comprehend or execute their role appropriately.

M1. Benefit of management accounting systems

Accounting systems Benefits

Price optimization system Price optimisation offers opportunities to concentrate on a

3

order and take corrective action.

Price optimization system: This is a form of controlling system that provides a

comprehensive pricing structure and criteria for customer satisfaction. This accounting approach

helps businesses to get useful industry patterns and consumer demand knowledge. It is

essentially important for enterprises to modify the level of goods and services throughout the

market. In the case of chosen company, management team changes pricing methods according to

the customer's wishes. With the help of price optimization system, managers are able to fix

product or service price which satisfies both buyers as well as business goals. This

system essentially allowed setting appropriate prices that increase the ability of consumers to buy

products and services.

Essential requirement of management accounting systems:

Management accounting systems (MAS) are basically necessary by the company to make

sure the available records will be credible, correct, presentable, revised and in understandable

form. So people can understand and further managers of Cream Ltd may use this knowledge in

decision making process.

Accurate: All details should be accurate in MAS as executives take business decisions

which are based on it.

Reliable: Accounting records should be reliable and an important aspect of management

accounting. It assists in determining real financial status of the Cream Ltd in terms of

revenue.

Presentable: All the accounting information should be represented in common format

layout and organizations widely use the common standard for reporting.

Updated and on time: In the financial report, data reported on monthly or annual basis

as management of Cream Ltd take decisions based of it and it is an ultimately necessary

for decision taking mechanism to have additional updated information.

Reasonable and relevant: Information should be reported in understandable way, so

users of Cream Ltd can comprehend or execute their role appropriately.

M1. Benefit of management accounting systems

Accounting systems Benefits

Price optimization system Price optimisation offers opportunities to concentrate on a

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

multitude of goals such as sales margin and amount of

transformations. Also beneficial for the managers of

Creams Ltd to set product price to maximise their earning

and suitable for consumers as well which helps in meeting

their price expectations.

Job order costing system It helps the managers of Creams Ltd to make accurate

calculations of the numerical costs of resources, manpower

and overhead that would be expended when doing a work.

Managers of Cream Ltd follow this system to estimate each

product cost.

Inventory management system By using this accounting system, Creams ltd minimise the

risk of raw material wastages, reduce carrying or ordering

cost of material. It helps the managers to track stock level

and further decisions accordingly.

Cost accounting system It helps in highlighting valuable or non valuable activities

which generate cost. These help managers of Creams Ltd

to eliminate non profitable activities to minimise cost

(Maggard and Barlow, 2018).

Summary: From the above discussion, it is observed that management accounting systems

are very valuable for organisations to carry out their operations and to ensure that the

productivity and profitability are maximized. These systems help the Creams Ltd's managers

to develop efficient plans to optimize their manufacturing, productivity, and output and reduce

total manufacturing costs to achieve their company targets and objectives.

D1. Evaluate how accounting systems linked with accounting reports

The business optimisation system is incorporated into the marketing department as a

means to increase profits from purchases. Financial records, within the financial processes, are

also associated with the revenue process. Inventory analysis applies to production unit. For

example, in the above organisation, their managers use conflicting reports for corrective action in

the industry. In order to properly operate business operations, Creams Ltd managers need to

4

transformations. Also beneficial for the managers of

Creams Ltd to set product price to maximise their earning

and suitable for consumers as well which helps in meeting

their price expectations.

Job order costing system It helps the managers of Creams Ltd to make accurate

calculations of the numerical costs of resources, manpower

and overhead that would be expended when doing a work.

Managers of Cream Ltd follow this system to estimate each

product cost.

Inventory management system By using this accounting system, Creams ltd minimise the

risk of raw material wastages, reduce carrying or ordering

cost of material. It helps the managers to track stock level

and further decisions accordingly.

Cost accounting system It helps in highlighting valuable or non valuable activities

which generate cost. These help managers of Creams Ltd

to eliminate non profitable activities to minimise cost

(Maggard and Barlow, 2018).

Summary: From the above discussion, it is observed that management accounting systems

are very valuable for organisations to carry out their operations and to ensure that the

productivity and profitability are maximized. These systems help the Creams Ltd's managers

to develop efficient plans to optimize their manufacturing, productivity, and output and reduce

total manufacturing costs to achieve their company targets and objectives.

D1. Evaluate how accounting systems linked with accounting reports

The business optimisation system is incorporated into the marketing department as a

means to increase profits from purchases. Financial records, within the financial processes, are

also associated with the revenue process. Inventory analysis applies to production unit. For

example, in the above organisation, their managers use conflicting reports for corrective action in

the industry. In order to properly operate business operations, Creams Ltd managers need to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

introduce various programs such as stock control to keep track with their stock level and instead

compile inventory report for analysis level or policy taking appropriately.

P2. Different method used for management accounting reporting

Management accounting reporting includes several types of reporting which helps in

collecting information for further decision making process. It contains enough information which

required to measure business performance. Further discussions are as follow:

Job cost report: This is accounting tool used to measure the efficiency of a project or

development against a defined or expected level (Renz, 2016). Mapping online workflow

systems is essential to insure that accounts payable invoices, procurement orders, and general

contractor contracts are entered into as rapidly as practicable and allocated to the appropriate

distribution of employment. The purpose of job costing reports is to determine inconsistencies or

beneficial outcomes, usually in financial values. They can be used to record reports both

financially and numerically. Because of that, managers of Creams Ltd use this report to record

all the essential information.

Inventory management report: A report of inventory management is essential to

understand that how much product they have on order in the warehouse. Such reports help

Creams Ltd to manage inventory levels and make sure to monitor them properly. There have

been a variety of approaches for obtaining a study on inventory control. purpose of inventory

management is just to maintain a clear track of any new or returning product entering or exiting a

store or retail outlet. This report effectively controls inventory stock to ensure the Creams Ltd's

valuable capital is utilized in the best manner. Inventories are classified into three different

aspects such as raw material, work in progress goods and finished goods. Managers of Cream ltd

should maintain proper report for each level requirement and then formulate strategies

accordingly

Operating budget report: It demonstrates the approximate revenue and associated costs of

the firm for the current year. It is also shown in the format of an income statement

which provides better understanding of each item. An administrator normally goes through the

budget which prepare on the basis of last year performance (Schaltegger and Burritt, 2017). A

report on an operating budget can consists of a high-level outline schedule, supplemented by

budget details to corroborate each line item. Creams Ltd's executives monitor this analysis and

5

compile inventory report for analysis level or policy taking appropriately.

P2. Different method used for management accounting reporting

Management accounting reporting includes several types of reporting which helps in

collecting information for further decision making process. It contains enough information which

required to measure business performance. Further discussions are as follow:

Job cost report: This is accounting tool used to measure the efficiency of a project or

development against a defined or expected level (Renz, 2016). Mapping online workflow

systems is essential to insure that accounts payable invoices, procurement orders, and general

contractor contracts are entered into as rapidly as practicable and allocated to the appropriate

distribution of employment. The purpose of job costing reports is to determine inconsistencies or

beneficial outcomes, usually in financial values. They can be used to record reports both

financially and numerically. Because of that, managers of Creams Ltd use this report to record

all the essential information.

Inventory management report: A report of inventory management is essential to

understand that how much product they have on order in the warehouse. Such reports help

Creams Ltd to manage inventory levels and make sure to monitor them properly. There have

been a variety of approaches for obtaining a study on inventory control. purpose of inventory

management is just to maintain a clear track of any new or returning product entering or exiting a

store or retail outlet. This report effectively controls inventory stock to ensure the Creams Ltd's

valuable capital is utilized in the best manner. Inventories are classified into three different

aspects such as raw material, work in progress goods and finished goods. Managers of Cream ltd

should maintain proper report for each level requirement and then formulate strategies

accordingly

Operating budget report: It demonstrates the approximate revenue and associated costs of

the firm for the current year. It is also shown in the format of an income statement

which provides better understanding of each item. An administrator normally goes through the

budget which prepare on the basis of last year performance (Schaltegger and Burritt, 2017). A

report on an operating budget can consists of a high-level outline schedule, supplemented by

budget details to corroborate each line item. Creams Ltd's executives monitor this analysis and

5

plan all of it, including projected sales or output expense, which also assists in taking strategic

decisions or developing strategies.

Account receivable aging report: This report is indicating the outstanding amount of the

invoice along with the period in which it was unpaid. Organizations locate open invoices and

encourage them to stay on track of late paying consumers. Main purpose of this report is to

locate the defaulters or build strategies to collect from them. Managers of Creams Ltd prepare

this report to identify number of outstanding payment or build strict policy to recover for them. It

is essentially important for the organization to make list of defaulters to make further managerial

decisions.

In context of organization, managers have to prepare different reports which contain

variety of information and it helps in building strategies or makes decisions in context of

maximising operational efficiency as well as performance.

TASK 2

P3. Calculate cost by using different costing method

6

decisions or developing strategies.

Account receivable aging report: This report is indicating the outstanding amount of the

invoice along with the period in which it was unpaid. Organizations locate open invoices and

encourage them to stay on track of late paying consumers. Main purpose of this report is to

locate the defaulters or build strategies to collect from them. Managers of Creams Ltd prepare

this report to identify number of outstanding payment or build strict policy to recover for them. It

is essentially important for the organization to make list of defaulters to make further managerial

decisions.

In context of organization, managers have to prepare different reports which contain

variety of information and it helps in building strategies or makes decisions in context of

maximising operational efficiency as well as performance.

TASK 2

P3. Calculate cost by using different costing method

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

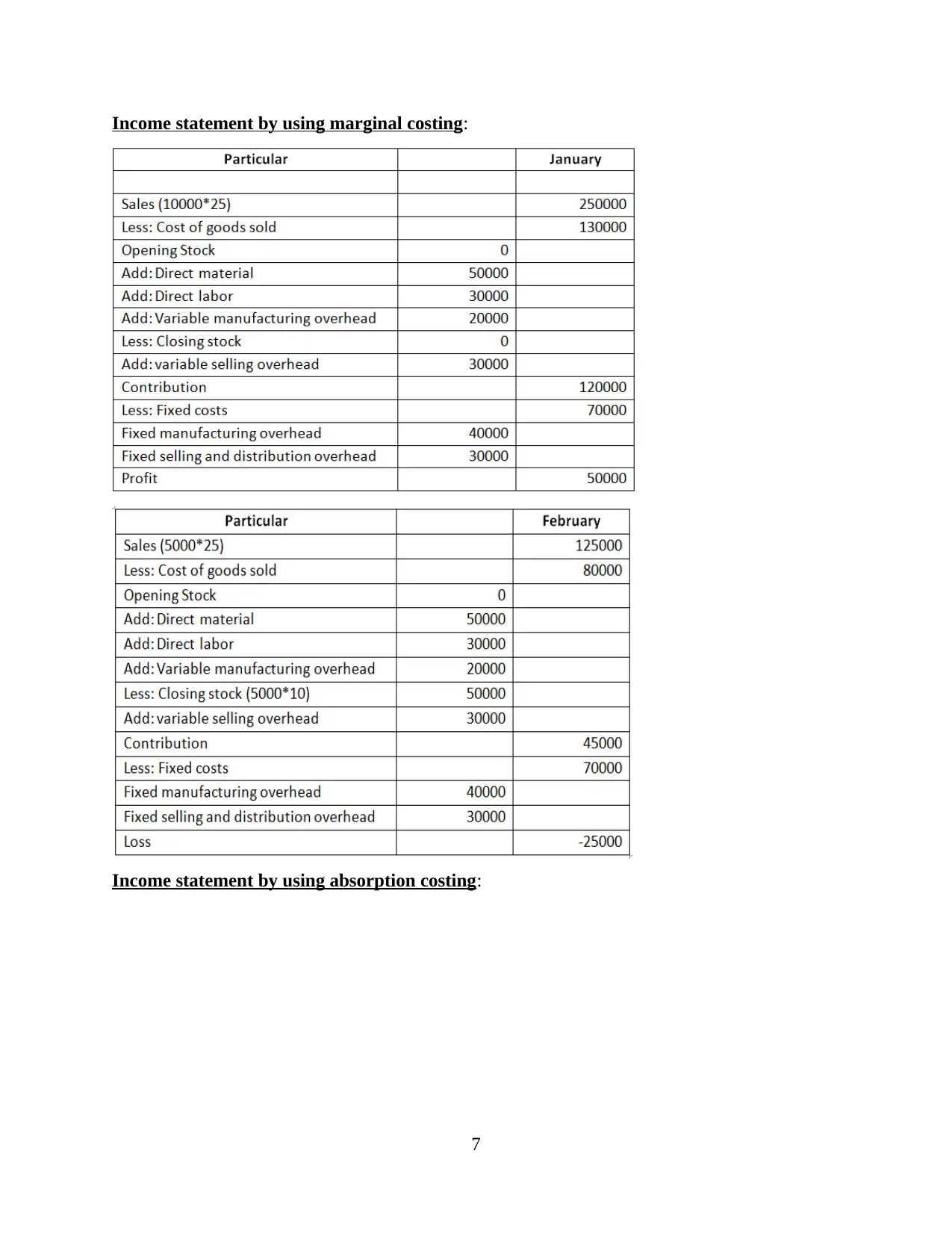

Income statement by using marginal costing:

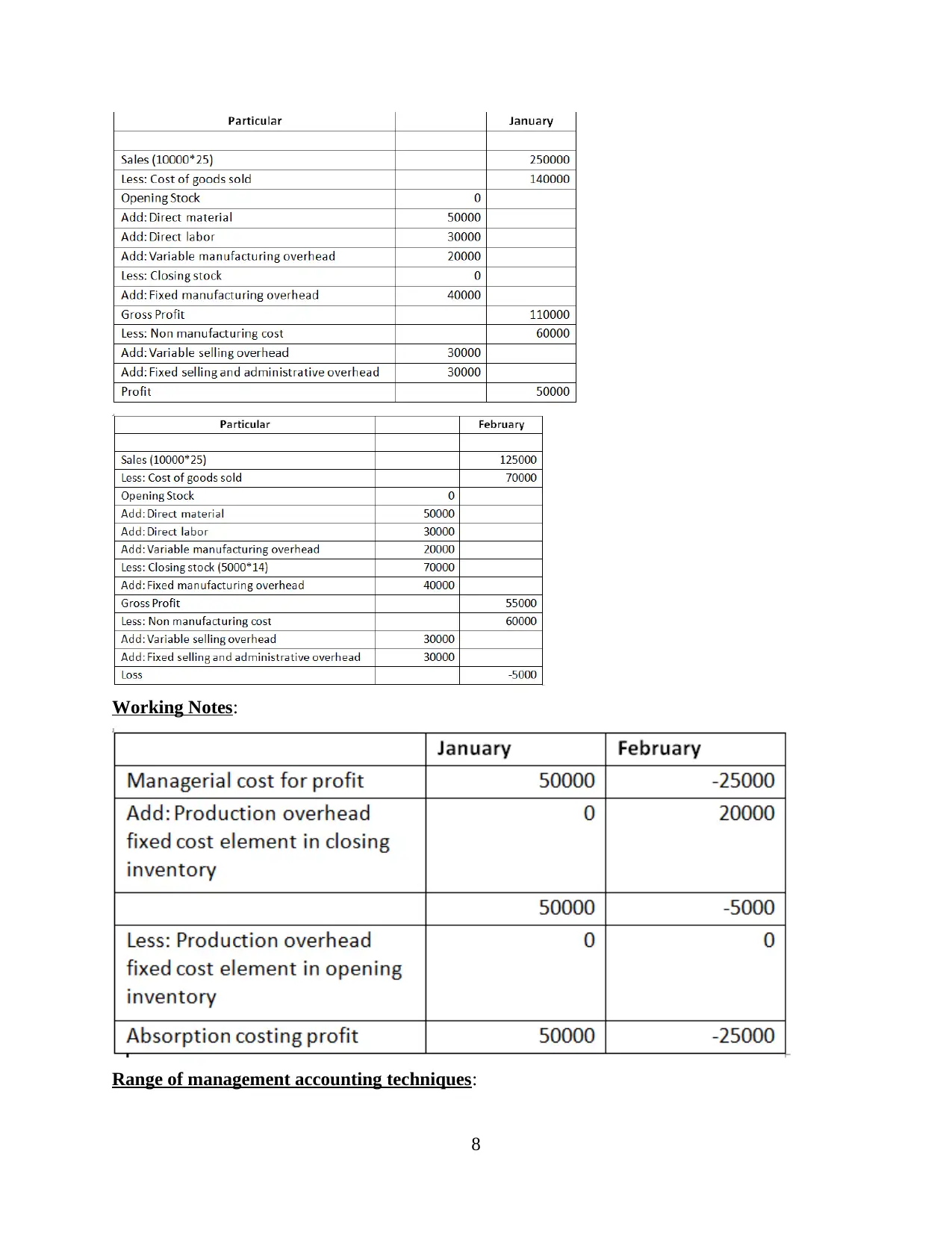

Income statement by using absorption costing:

7

Income statement by using absorption costing:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working Notes:

Range of management accounting techniques:

8

Range of management accounting techniques:

8

Variance analysis: It is an important to assist with handling expenditures by tracking

budgeted vs real costs. Variances between expected and real costs may contribute to changing

business priorities, objectives or strategies. Managers of Creams Ltd use this analysis to

formulate business strategies.

Marginal costing: It is the strategy in which fixed cost are removed but only variable

cost are performed because of it, this approach is also recognized as variable cost method. This

approach is being used by Creams ltd to calculate overall profit of the company.

Absorption costing: In this costing approach both fixed and variable cost are used from

which this is useful tool for major company such as Creams Ltd. Likewise this process is used by

Creams ltd in order to evaluate overall profitability of the business.

M2. Apply range of management accounting techniques and generate financial reporting

statements

In corporate terms, there are so many accounting approaches that are used to measure net

profit or loss for the fiscal quarter by using various accounting methods, administrators produce

financial results with the assistance of available financial evidence, they provide the financial

position of the organizations (Singh and Verma, 2018). Using this expertise, managers will

devise potential investment choices and strategies needed for company activities to be carried

out. Additionally it is desirable to achieve recognition and significant growth in the industry. By

using marginal or absorption costing approach, Creams Ltd managers plan income statement that

indicates the benefit or loss for January or February time.

D2.Produce financial reports that accurately apply and interpret data for a range of business

activities

It has already been objectively determined that financial reporting is important to plan,

because management analyze the success of the company and possible plans appropriately with

the assistance of it. Creams Ltd's net profit for the period of January and February was 50,000

and (25,000), using marginal approaches. While on the other hand, net profit was 50000 for the

month of January using absorption method and 5000 for the month of February and it was loss.

The Company's net efficiency decreases and is calculated using income statement. They should

do something to boost their business efficiency else it would harm the credibility of the

organization or the decision making process of the stakeholders.

9

budgeted vs real costs. Variances between expected and real costs may contribute to changing

business priorities, objectives or strategies. Managers of Creams Ltd use this analysis to

formulate business strategies.

Marginal costing: It is the strategy in which fixed cost are removed but only variable

cost are performed because of it, this approach is also recognized as variable cost method. This

approach is being used by Creams ltd to calculate overall profit of the company.

Absorption costing: In this costing approach both fixed and variable cost are used from

which this is useful tool for major company such as Creams Ltd. Likewise this process is used by

Creams ltd in order to evaluate overall profitability of the business.

M2. Apply range of management accounting techniques and generate financial reporting

statements

In corporate terms, there are so many accounting approaches that are used to measure net

profit or loss for the fiscal quarter by using various accounting methods, administrators produce

financial results with the assistance of available financial evidence, they provide the financial

position of the organizations (Singh and Verma, 2018). Using this expertise, managers will

devise potential investment choices and strategies needed for company activities to be carried

out. Additionally it is desirable to achieve recognition and significant growth in the industry. By

using marginal or absorption costing approach, Creams Ltd managers plan income statement that

indicates the benefit or loss for January or February time.

D2.Produce financial reports that accurately apply and interpret data for a range of business

activities

It has already been objectively determined that financial reporting is important to plan,

because management analyze the success of the company and possible plans appropriately with

the assistance of it. Creams Ltd's net profit for the period of January and February was 50,000

and (25,000), using marginal approaches. While on the other hand, net profit was 50000 for the

month of January using absorption method and 5000 for the month of February and it was loss.

The Company's net efficiency decreases and is calculated using income statement. They should

do something to boost their business efficiency else it would harm the credibility of the

organization or the decision making process of the stakeholders.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.