Management Accounting Report: Continental Clothing Ltd Analysis

VerifiedAdded on 2023/01/19

|19

|3611

|82

Report

AI Summary

This report delves into the application of management accounting principles within Continental Clothing Ltd. It begins by defining management accounting and its role in financial decision-making, then outlines various management accounting systems (MAS) such as stock management, cost accounting, and price optimization. The report explores different types of financial reports, including budget reports, and assesses their benefits. It then analyzes costing techniques, specifically absorption and marginal costing, using financial data from the company. The report includes profit and loss statements and reconciliation statements to compare these costing methods. Furthermore, it examines budgetary control tools like cash and master budgets and their advantages and disadvantages, with examples of sales, production, and material purchase budgets. Finally, the report calculates variances between actual and flexible budgets to assess performance.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1.................................................................................................................................................3

P2.................................................................................................................................................4

M1................................................................................................................................................4

D1.................................................................................................................................................5

TASK 2............................................................................................................................................5

P3.................................................................................................................................................5

M2................................................................................................................................................9

D2.................................................................................................................................................9

TASK 3............................................................................................................................................9

P4.................................................................................................................................................9

M3..............................................................................................................................................13

TASK 4..........................................................................................................................................13

P5...............................................................................................................................................13

M4..............................................................................................................................................15

D3. .............................................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1.................................................................................................................................................3

P2.................................................................................................................................................4

M1................................................................................................................................................4

D1.................................................................................................................................................5

TASK 2............................................................................................................................................5

P3.................................................................................................................................................5

M2................................................................................................................................................9

D2.................................................................................................................................................9

TASK 3............................................................................................................................................9

P4.................................................................................................................................................9

M3..............................................................................................................................................13

TASK 4..........................................................................................................................................13

P5...............................................................................................................................................13

M4..............................................................................................................................................15

D3. .............................................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting (MA) is defined as the particular process which includes the

certain process such as identifying, analysing, processing, measuring the financial data and

information in order to make the futuristic decision by the management of the business

organisation. It manages the financial performance of the by setting up new objects and plan in

the business. For the better understanding of this particular topic company continental clothing

Ltd. is selected that is engaged in fabrication of the clothing at the various location of UK. The

reports content the various topic such as management accounting system (MAS), reporting,

different problem established in the business, various budgeting techniques and control that used

by business as planning tools (Schaltegger, Burritt, and Petersen, 2017).

TASK 1.

P1

Management accounting includes the different kind of accounting tools that devising the

plan and object of the business in respect to providing the expertise in the financial statement and

reporting and assist the manager regarding formulation the business strategies and objectives and

implement it into business for earn more profit in future. Here, the different kind of management

accounting are mentioned as under:

Stock management system: It is also called inventory method that related with the

handle the overall cost of the product at processing unit of business. It manages the inflow and

outflow of the stock at warehouses. The company continental clothing Ltd is using this method

to ensure the stock at the warehouse.

Cost accounting system: This is the system that is defined as the overall cost that incur

at the different level of the manufacturing the goods. It consists the the total cost from stage of

raw material to finished goods. Continental clothing uses this method in the business to know the

overall cost at the time of manufacture.

Price optimisation system (POS)- In the method, business sets the price to its products

at the certain level. It is totally based on the cost of production and the review of the customers.

In respect to selected company, management are applying particular system to set the amount to

its products.

Management accounting (MA) is defined as the particular process which includes the

certain process such as identifying, analysing, processing, measuring the financial data and

information in order to make the futuristic decision by the management of the business

organisation. It manages the financial performance of the by setting up new objects and plan in

the business. For the better understanding of this particular topic company continental clothing

Ltd. is selected that is engaged in fabrication of the clothing at the various location of UK. The

reports content the various topic such as management accounting system (MAS), reporting,

different problem established in the business, various budgeting techniques and control that used

by business as planning tools (Schaltegger, Burritt, and Petersen, 2017).

TASK 1.

P1

Management accounting includes the different kind of accounting tools that devising the

plan and object of the business in respect to providing the expertise in the financial statement and

reporting and assist the manager regarding formulation the business strategies and objectives and

implement it into business for earn more profit in future. Here, the different kind of management

accounting are mentioned as under:

Stock management system: It is also called inventory method that related with the

handle the overall cost of the product at processing unit of business. It manages the inflow and

outflow of the stock at warehouses. The company continental clothing Ltd is using this method

to ensure the stock at the warehouse.

Cost accounting system: This is the system that is defined as the overall cost that incur

at the different level of the manufacturing the goods. It consists the the total cost from stage of

raw material to finished goods. Continental clothing uses this method in the business to know the

overall cost at the time of manufacture.

Price optimisation system (POS)- In the method, business sets the price to its products

at the certain level. It is totally based on the cost of production and the review of the customers.

In respect to selected company, management are applying particular system to set the amount to

its products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing system- This is the method that is defined as the transfer the cost to its

particular products and job. It measure the cost incurred from direct material, labour and

overhead. Company is using this tool to make effective decision in the business regarding

allocation of the cost to its projects and job.

P2

These reports are the basic statement of the business that represent the monetary item in

the statement to its management of the company. The main object behind it to provides all the

detail regarding the business to make the internal planning and policy. The different kind of

reports are as follows:

Budget reports: This is the reports that is defined as the statements of the future income

and expenditure at the different level of manufacturing. This report play a major role in analysing

the standard data with actual performance. Continental clothing company is using this tool of

MAR in the business to identify the cost at various level of the production (Santini, 2013).

Account receivable ageing report- In this report, it show the total amount due with the

debtors. This reports is only for those business which deal in the credit to its customers. The

management creates this reports to know the balance amount with the customers. In the company

continental clothing business uses this reports to know the credit business transaction with

customer.

Cost accounting report- This is the report that is accompanying the information

regarding the overall cost of the manufacturing the goods and product. It covers the various cost

of production such as direct material, certain overhead like fix and variable cost. The company,

continental clothing Ltd is making this particular reports in the business to measure the

incurring in their operation.

Performance report- This reports is all about the measuring the specified business

activities and operation in concern with the business performance and employee contribution

towards the business organisation. Company is using this report to make analysation in the

business regards the whole performance of the business.

M1

Every management system have its own role and function in the business that play a

major role in handling the business activities. Here, some of the benefit are as under :

particular products and job. It measure the cost incurred from direct material, labour and

overhead. Company is using this tool to make effective decision in the business regarding

allocation of the cost to its projects and job.

P2

These reports are the basic statement of the business that represent the monetary item in

the statement to its management of the company. The main object behind it to provides all the

detail regarding the business to make the internal planning and policy. The different kind of

reports are as follows:

Budget reports: This is the reports that is defined as the statements of the future income

and expenditure at the different level of manufacturing. This report play a major role in analysing

the standard data with actual performance. Continental clothing company is using this tool of

MAR in the business to identify the cost at various level of the production (Santini, 2013).

Account receivable ageing report- In this report, it show the total amount due with the

debtors. This reports is only for those business which deal in the credit to its customers. The

management creates this reports to know the balance amount with the customers. In the company

continental clothing business uses this reports to know the credit business transaction with

customer.

Cost accounting report- This is the report that is accompanying the information

regarding the overall cost of the manufacturing the goods and product. It covers the various cost

of production such as direct material, certain overhead like fix and variable cost. The company,

continental clothing Ltd is making this particular reports in the business to measure the

incurring in their operation.

Performance report- This reports is all about the measuring the specified business

activities and operation in concern with the business performance and employee contribution

towards the business organisation. Company is using this report to make analysation in the

business regards the whole performance of the business.

M1

Every management system have its own role and function in the business that play a

major role in handling the business activities. Here, some of the benefit are as under :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

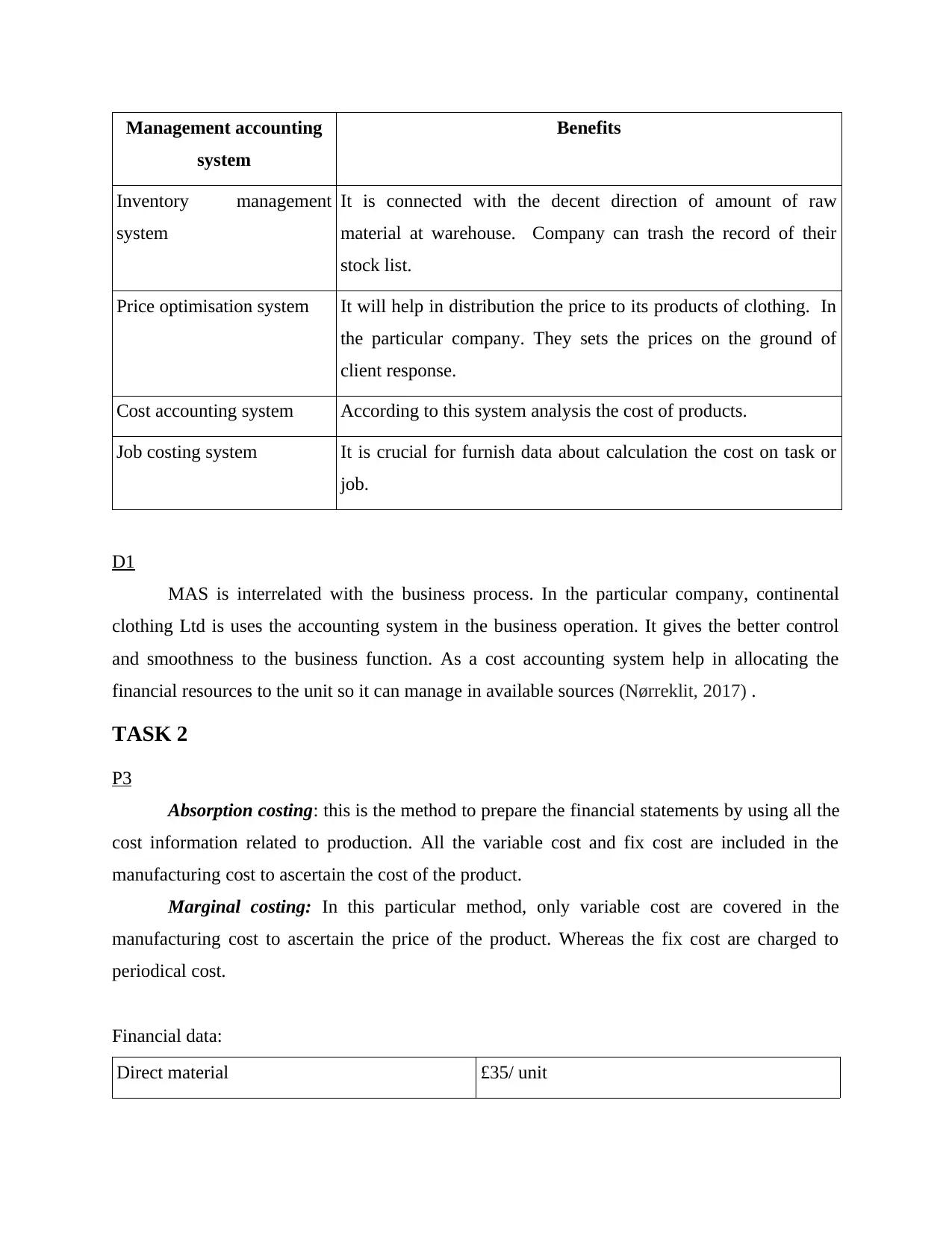

Management accounting

system

Benefits

Inventory management

system

It is connected with the decent direction of amount of raw

material at warehouse. Company can trash the record of their

stock list.

Price optimisation system It will help in distribution the price to its products of clothing. In

the particular company. They sets the prices on the ground of

client response.

Cost accounting system According to this system analysis the cost of products.

Job costing system It is crucial for furnish data about calculation the cost on task or

job.

D1

MAS is interrelated with the business process. In the particular company, continental

clothing Ltd is uses the accounting system in the business operation. It gives the better control

and smoothness to the business function. As a cost accounting system help in allocating the

financial resources to the unit so it can manage in available sources (Nørreklit, 2017) .

TASK 2

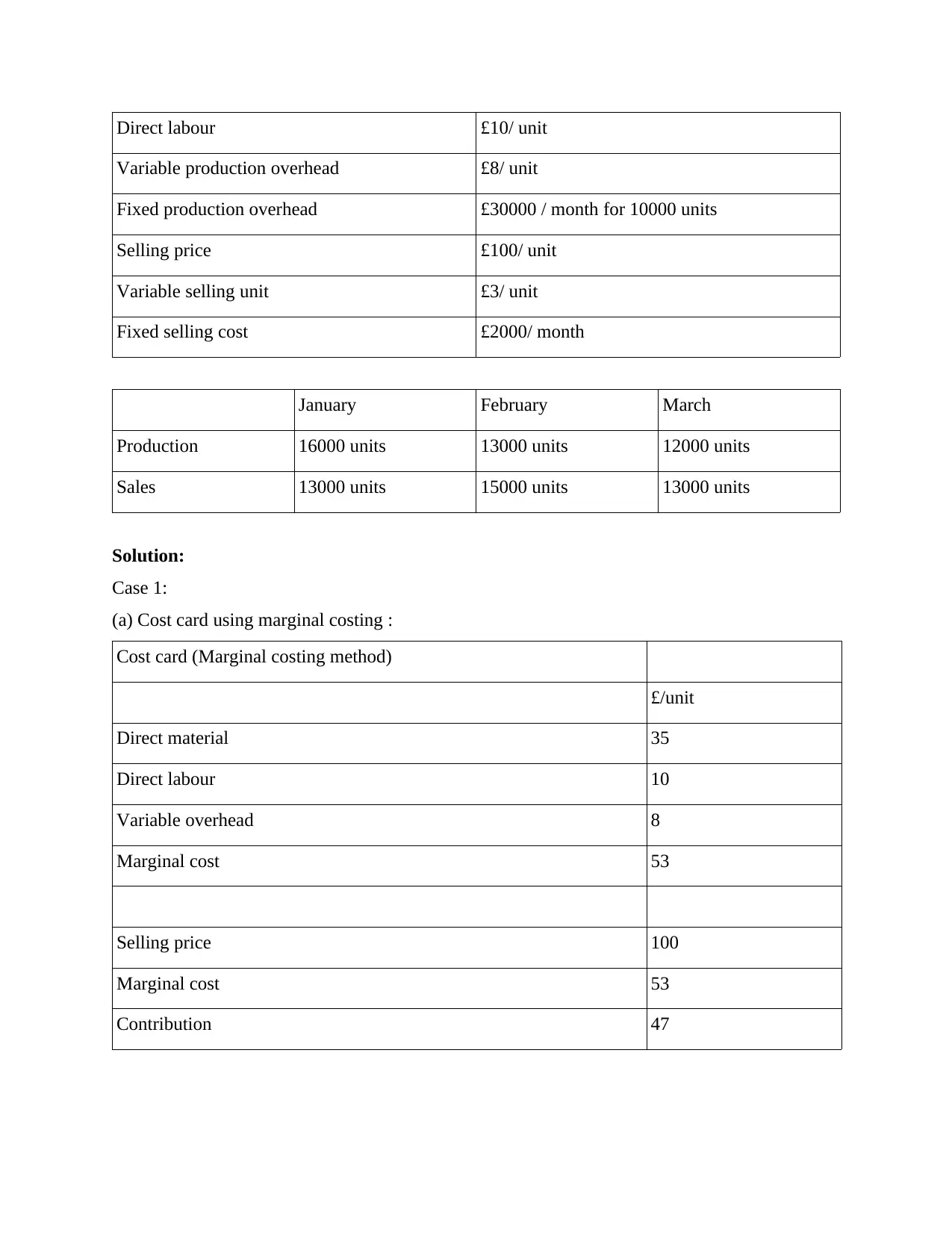

P3

Absorption costing: this is the method to prepare the financial statements by using all the

cost information related to production. All the variable cost and fix cost are included in the

manufacturing cost to ascertain the cost of the product.

Marginal costing: In this particular method, only variable cost are covered in the

manufacturing cost to ascertain the price of the product. Whereas the fix cost are charged to

periodical cost.

Financial data:

Direct material £35/ unit

system

Benefits

Inventory management

system

It is connected with the decent direction of amount of raw

material at warehouse. Company can trash the record of their

stock list.

Price optimisation system It will help in distribution the price to its products of clothing. In

the particular company. They sets the prices on the ground of

client response.

Cost accounting system According to this system analysis the cost of products.

Job costing system It is crucial for furnish data about calculation the cost on task or

job.

D1

MAS is interrelated with the business process. In the particular company, continental

clothing Ltd is uses the accounting system in the business operation. It gives the better control

and smoothness to the business function. As a cost accounting system help in allocating the

financial resources to the unit so it can manage in available sources (Nørreklit, 2017) .

TASK 2

P3

Absorption costing: this is the method to prepare the financial statements by using all the

cost information related to production. All the variable cost and fix cost are included in the

manufacturing cost to ascertain the cost of the product.

Marginal costing: In this particular method, only variable cost are covered in the

manufacturing cost to ascertain the price of the product. Whereas the fix cost are charged to

periodical cost.

Financial data:

Direct material £35/ unit

Direct labour £10/ unit

Variable production overhead £8/ unit

Fixed production overhead £30000 / month for 10000 units

Selling price £100/ unit

Variable selling unit £3/ unit

Fixed selling cost £2000/ month

January February March

Production 16000 units 13000 units 12000 units

Sales 13000 units 15000 units 13000 units

Solution:

Case 1:

(a) Cost card using marginal costing :

Cost card (Marginal costing method)

£/unit

Direct material 35

Direct labour 10

Variable overhead 8

Marginal cost 53

Selling price 100

Marginal cost 53

Contribution 47

Variable production overhead £8/ unit

Fixed production overhead £30000 / month for 10000 units

Selling price £100/ unit

Variable selling unit £3/ unit

Fixed selling cost £2000/ month

January February March

Production 16000 units 13000 units 12000 units

Sales 13000 units 15000 units 13000 units

Solution:

Case 1:

(a) Cost card using marginal costing :

Cost card (Marginal costing method)

£/unit

Direct material 35

Direct labour 10

Variable overhead 8

Marginal cost 53

Selling price 100

Marginal cost 53

Contribution 47

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

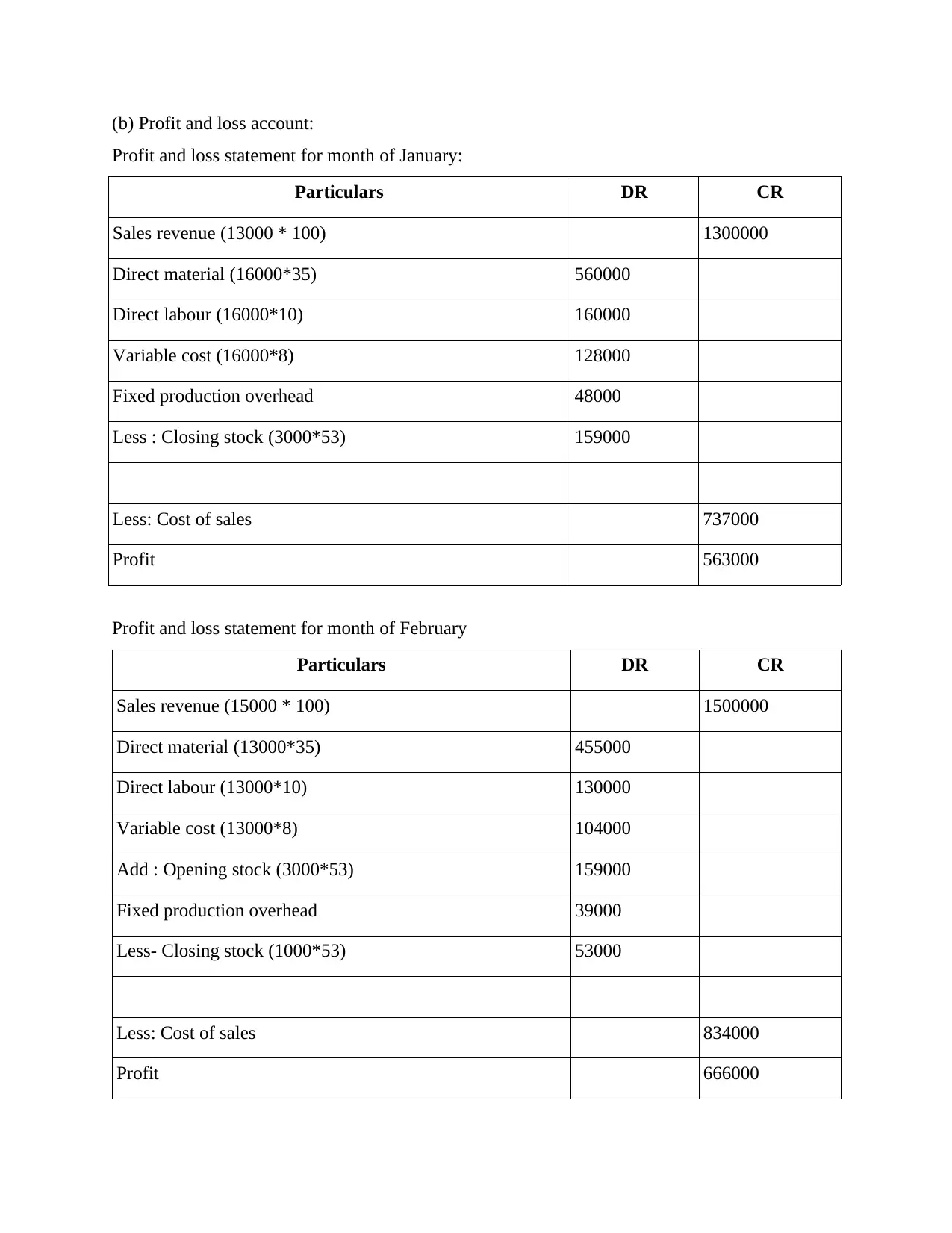

(b) Profit and loss account:

Profit and loss statement for month of January:

Particulars DR CR

Sales revenue (13000 * 100) 1300000

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Variable cost (16000*8) 128000

Fixed production overhead 48000

Less : Closing stock (3000*53) 159000

Less: Cost of sales 737000

Profit 563000

Profit and loss statement for month of February

Particulars DR CR

Sales revenue (15000 * 100) 1500000

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Variable cost (13000*8) 104000

Add : Opening stock (3000*53) 159000

Fixed production overhead 39000

Less- Closing stock (1000*53) 53000

Less: Cost of sales 834000

Profit 666000

Profit and loss statement for month of January:

Particulars DR CR

Sales revenue (13000 * 100) 1300000

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Variable cost (16000*8) 128000

Fixed production overhead 48000

Less : Closing stock (3000*53) 159000

Less: Cost of sales 737000

Profit 563000

Profit and loss statement for month of February

Particulars DR CR

Sales revenue (15000 * 100) 1500000

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Variable cost (13000*8) 104000

Add : Opening stock (3000*53) 159000

Fixed production overhead 39000

Less- Closing stock (1000*53) 53000

Less: Cost of sales 834000

Profit 666000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

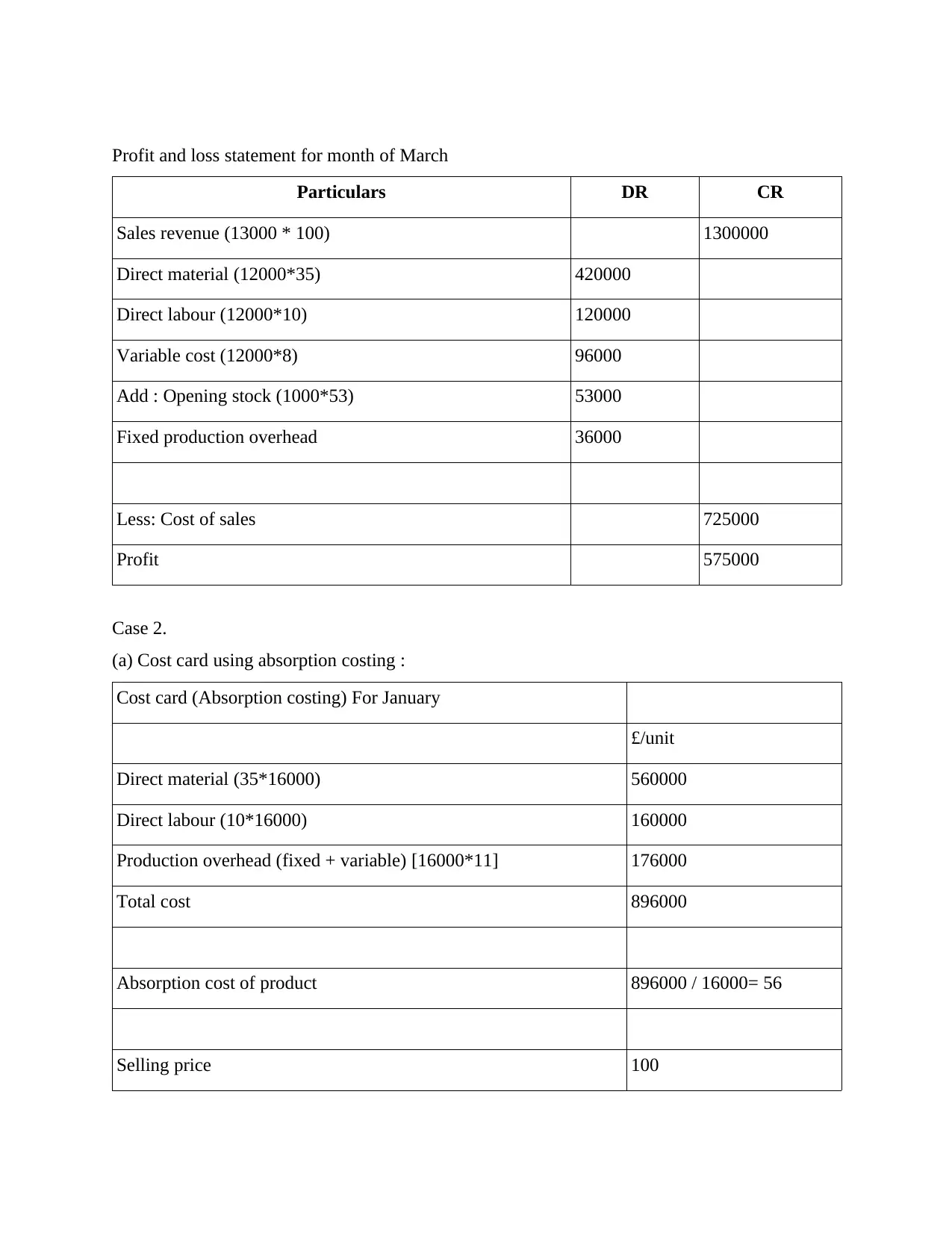

Profit and loss statement for month of March

Particulars DR CR

Sales revenue (13000 * 100) 1300000

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Variable cost (12000*8) 96000

Add : Opening stock (1000*53) 53000

Fixed production overhead 36000

Less: Cost of sales 725000

Profit 575000

Case 2.

(a) Cost card using absorption costing :

Cost card (Absorption costing) For January

£/unit

Direct material (35*16000) 560000

Direct labour (10*16000) 160000

Production overhead (fixed + variable) [16000*11] 176000

Total cost 896000

Absorption cost of product 896000 / 16000= 56

Selling price 100

Particulars DR CR

Sales revenue (13000 * 100) 1300000

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Variable cost (12000*8) 96000

Add : Opening stock (1000*53) 53000

Fixed production overhead 36000

Less: Cost of sales 725000

Profit 575000

Case 2.

(a) Cost card using absorption costing :

Cost card (Absorption costing) For January

£/unit

Direct material (35*16000) 560000

Direct labour (10*16000) 160000

Production overhead (fixed + variable) [16000*11] 176000

Total cost 896000

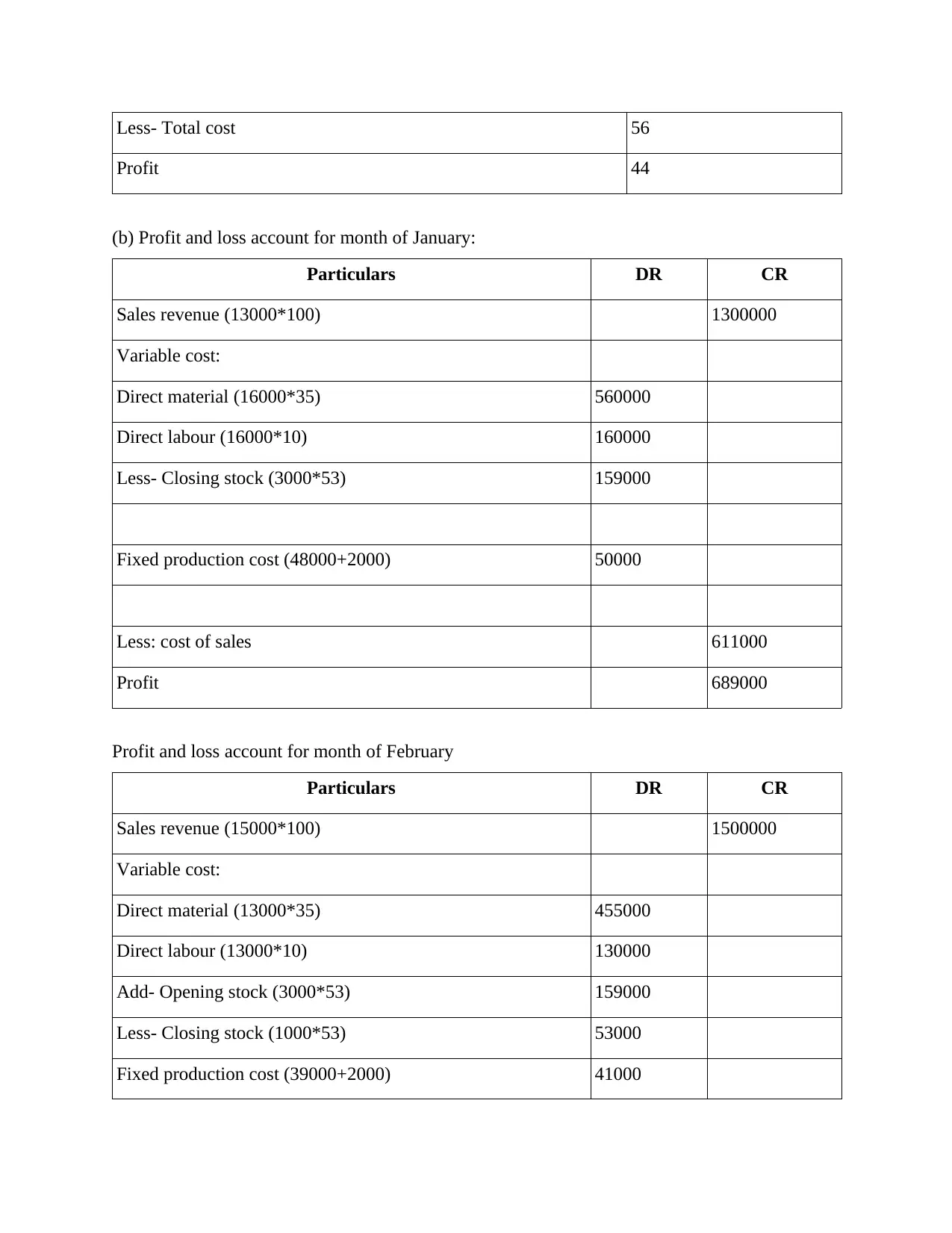

Absorption cost of product 896000 / 16000= 56

Selling price 100

Less- Total cost 56

Profit 44

(b) Profit and loss account for month of January:

Particulars DR CR

Sales revenue (13000*100) 1300000

Variable cost:

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Less- Closing stock (3000*53) 159000

Fixed production cost (48000+2000) 50000

Less: cost of sales 611000

Profit 689000

Profit and loss account for month of February

Particulars DR CR

Sales revenue (15000*100) 1500000

Variable cost:

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Add- Opening stock (3000*53) 159000

Less- Closing stock (1000*53) 53000

Fixed production cost (39000+2000) 41000

Profit 44

(b) Profit and loss account for month of January:

Particulars DR CR

Sales revenue (13000*100) 1300000

Variable cost:

Direct material (16000*35) 560000

Direct labour (16000*10) 160000

Less- Closing stock (3000*53) 159000

Fixed production cost (48000+2000) 50000

Less: cost of sales 611000

Profit 689000

Profit and loss account for month of February

Particulars DR CR

Sales revenue (15000*100) 1500000

Variable cost:

Direct material (13000*35) 455000

Direct labour (13000*10) 130000

Add- Opening stock (3000*53) 159000

Less- Closing stock (1000*53) 53000

Fixed production cost (39000+2000) 41000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

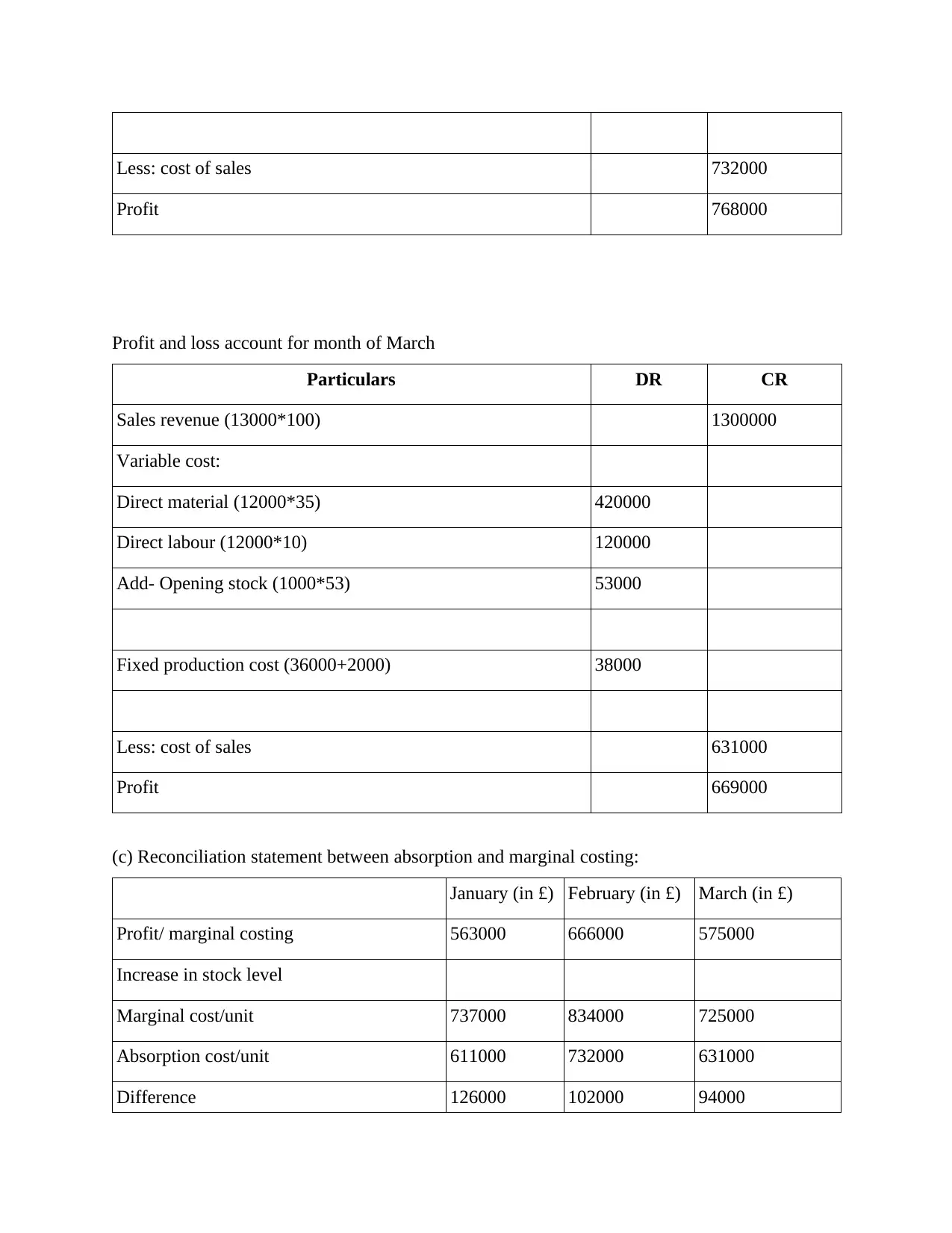

Less: cost of sales 732000

Profit 768000

Profit and loss account for month of March

Particulars DR CR

Sales revenue (13000*100) 1300000

Variable cost:

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Add- Opening stock (1000*53) 53000

Fixed production cost (36000+2000) 38000

Less: cost of sales 631000

Profit 669000

(c) Reconciliation statement between absorption and marginal costing:

January (in £) February (in £) March (in £)

Profit/ marginal costing 563000 666000 575000

Increase in stock level

Marginal cost/unit 737000 834000 725000

Absorption cost/unit 611000 732000 631000

Difference 126000 102000 94000

Profit 768000

Profit and loss account for month of March

Particulars DR CR

Sales revenue (13000*100) 1300000

Variable cost:

Direct material (12000*35) 420000

Direct labour (12000*10) 120000

Add- Opening stock (1000*53) 53000

Fixed production cost (36000+2000) 38000

Less: cost of sales 631000

Profit 669000

(c) Reconciliation statement between absorption and marginal costing:

January (in £) February (in £) March (in £)

Profit/ marginal costing 563000 666000 575000

Increase in stock level

Marginal cost/unit 737000 834000 725000

Absorption cost/unit 611000 732000 631000

Difference 126000 102000 94000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit/Absorption costing 689000 768000 669000

M2.

To conduct several management techniques it is required to apply costing techniques in

the context of MAS -

Historical technique – These techniques apply by the company to conduct business

activities in positive manner.

Modern techniques – These types of techniques apply when company have not any

option to sort out the problem.

D2

From the above table it is analysed that in order to prepare the income statement as per

the marginal costing the profit is around 800000 in respective month. And the absorption costing,

the profit are around 1100000 in the particular month. So it is recommanded to adopt absorption

method of costing.

TASK 3.

P4.

There are different type of planning tools that used in the business. The various type of

budgetary control like cash budget, production budget., sales budget, fix budget, flexible budget

helping in determine the estimated income and expenditure. Here some budget are explained as

under:

Cash budget- cash budget is the statements that shows the inflow and outflow of the

cash for the particular time of period. This budget is prepared to know the cash balances is

enough to operate the business activities. In the company, continental clothing the management

are prepared this report to maintain the minimum balance to operate the organisational function

(Abdelmoneim Mohamed and Jones, 2014).

M2.

To conduct several management techniques it is required to apply costing techniques in

the context of MAS -

Historical technique – These techniques apply by the company to conduct business

activities in positive manner.

Modern techniques – These types of techniques apply when company have not any

option to sort out the problem.

D2

From the above table it is analysed that in order to prepare the income statement as per

the marginal costing the profit is around 800000 in respective month. And the absorption costing,

the profit are around 1100000 in the particular month. So it is recommanded to adopt absorption

method of costing.

TASK 3.

P4.

There are different type of planning tools that used in the business. The various type of

budgetary control like cash budget, production budget., sales budget, fix budget, flexible budget

helping in determine the estimated income and expenditure. Here some budget are explained as

under:

Cash budget- cash budget is the statements that shows the inflow and outflow of the

cash for the particular time of period. This budget is prepared to know the cash balances is

enough to operate the business activities. In the company, continental clothing the management

are prepared this report to maintain the minimum balance to operate the organisational function

(Abdelmoneim Mohamed and Jones, 2014).

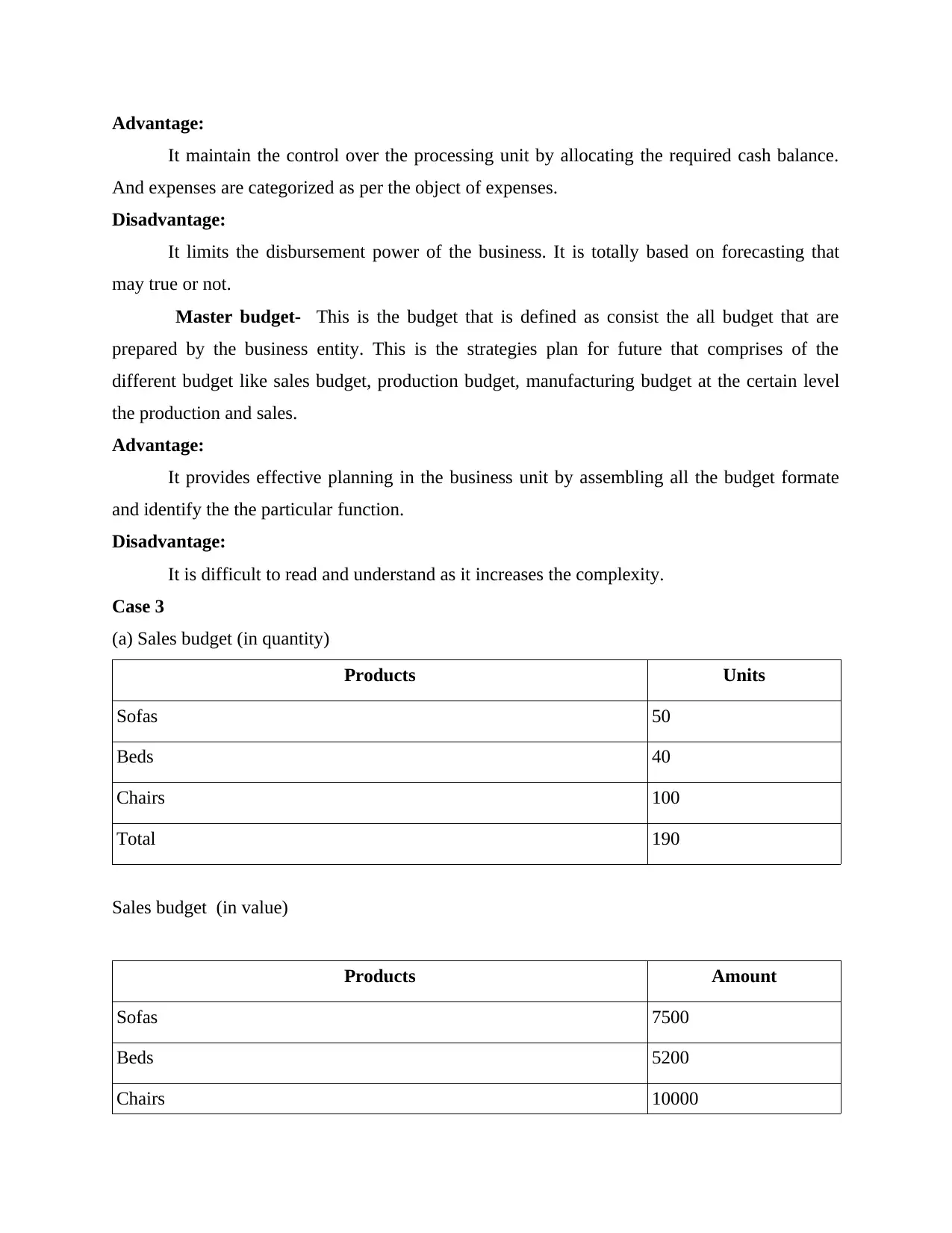

Advantage:

It maintain the control over the processing unit by allocating the required cash balance.

And expenses are categorized as per the object of expenses.

Disadvantage:

It limits the disbursement power of the business. It is totally based on forecasting that

may true or not.

Master budget- This is the budget that is defined as consist the all budget that are

prepared by the business entity. This is the strategies plan for future that comprises of the

different budget like sales budget, production budget, manufacturing budget at the certain level

the production and sales.

Advantage:

It provides effective planning in the business unit by assembling all the budget formate

and identify the the particular function.

Disadvantage:

It is difficult to read and understand as it increases the complexity.

Case 3

(a) Sales budget (in quantity)

Products Units

Sofas 50

Beds 40

Chairs 100

Total 190

Sales budget (in value)

Products Amount

Sofas 7500

Beds 5200

Chairs 10000

It maintain the control over the processing unit by allocating the required cash balance.

And expenses are categorized as per the object of expenses.

Disadvantage:

It limits the disbursement power of the business. It is totally based on forecasting that

may true or not.

Master budget- This is the budget that is defined as consist the all budget that are

prepared by the business entity. This is the strategies plan for future that comprises of the

different budget like sales budget, production budget, manufacturing budget at the certain level

the production and sales.

Advantage:

It provides effective planning in the business unit by assembling all the budget formate

and identify the the particular function.

Disadvantage:

It is difficult to read and understand as it increases the complexity.

Case 3

(a) Sales budget (in quantity)

Products Units

Sofas 50

Beds 40

Chairs 100

Total 190

Sales budget (in value)

Products Amount

Sofas 7500

Beds 5200

Chairs 10000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.