Management Accounting Report: Capital Joinery Ltd Case Study

VerifiedAdded on 2023/01/05

|18

|5088

|43

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Capital Joinery Ltd. It begins by defining management accounting, outlining its essential requirements, and differentiating it from financial accounting. The report then explores various management accounting reporting methods, including budget reports, accounts receivable aging reports, performance reports, and inventory and manufacturing reports. It delves into the benefits and applications of different management accounting systems, such as cost-accounting, inventory management, job-costing, and price-optimizing systems. Furthermore, the report examines cost analysis techniques, including fixed, variable, and semi-variable costs, and their impact on income statement preparation using marginal and absorption costing methods. It also discusses various planning tools used for budgetary control, evaluating their advantages and disadvantages. Finally, the report addresses how entities adapt management accounting systems to respond to financial problems, emphasizing the role of management accounting in achieving sustainable success through effective financial management and strategic planning. The report provides a detailed case study of Capital Joinery Ltd, illustrating how these concepts are applied in a real-world business setting.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Defining management accounting and its essential requirements..........................................1

P2. Management accounting reporting different methods...........................................................2

M1. Describing benefits and application of management accounting system.............................3

D1. Evaluating the integration of management accounting reporting and management

accounting system........................................................................................................................4

TASK 2............................................................................................................................................4

P3. Preparation of income statement using marginal and absorption cost using cost analysis

technique......................................................................................................................................4

M2. Application of management accounting techniques for financial reporting documents......8

D2. Explanation of financial reports that apply and interpret data for business activities..........9

TASK 3............................................................................................................................................9

P4 Explanation of advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................9

M3. Different planning tools and their application for forecasting and preparing budget........10

TASK 4..........................................................................................................................................11

P5. Comparing how entities adapts management accounting systems for responding financial

problems.....................................................................................................................................11

M4. Explaining that management accounting can lead organisation to sustainable success by

responding financial problems...................................................................................................12

D3. Explanation of planning tools that solves financial problems so that firm could be

successful...................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Defining management accounting and its essential requirements..........................................1

P2. Management accounting reporting different methods...........................................................2

M1. Describing benefits and application of management accounting system.............................3

D1. Evaluating the integration of management accounting reporting and management

accounting system........................................................................................................................4

TASK 2............................................................................................................................................4

P3. Preparation of income statement using marginal and absorption cost using cost analysis

technique......................................................................................................................................4

M2. Application of management accounting techniques for financial reporting documents......8

D2. Explanation of financial reports that apply and interpret data for business activities..........9

TASK 3............................................................................................................................................9

P4 Explanation of advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................9

M3. Different planning tools and their application for forecasting and preparing budget........10

TASK 4..........................................................................................................................................11

P5. Comparing how entities adapts management accounting systems for responding financial

problems.....................................................................................................................................11

M4. Explaining that management accounting can lead organisation to sustainable success by

responding financial problems...................................................................................................12

D3. Explanation of planning tools that solves financial problems so that firm could be

successful...................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is a process of identifying the aspects that affects the working of

the business directly or indirectly and then making a report with reference to the data that is

collected. Capital Joinery Ltd is a firm that deals in various products an services and is operating

since 2008 in London. This report covers various topics such as different types of management

accounting system and techniques. Apart from this it also covers topics of planning tools, cost

analysis, and different types of costs. Also the way in which an organisation deals with the

problems that are of financial nature.

TASK 1

P1 Defining management accounting and its essential requirements

Management accounting refers to a process of critically identifying and evaluating the

information related to accounts so that it can be precisely used by the managers to take decisions

which is in accordance with the information provided so that it can help a business to grow and

prosper in its industry. It is very important for a business as it helps management to take

decisions which can either be short or long term that helps a firm to improve its financial

stability. Capital joinery Ltd is a carpenter and joinery firm which provides made to measure

doors, double gazed, stairs, sash windows, etc. though the firm has been established in 2008

only, but it has gathered a pool of customer base (Abba, 2018). It is very essential to have a

improved and sophisticated version of management accounting system so that decisions taken

could be well directed and thus helping the firm to grow and capture a larger share of market.

Management accounting originated during 1900's from financial management but it is a lot

different from it in all aspects. Role of management accounting is to collect relevant data and

then analysing it so that it can be beneficial for the company. Principles of it includes that there

should be credibility of the data that is given, as well as it should influence the working of firm

in a positive way. Management and financial accounting differentiation is done below briefly-

Management accounting Financial accounting

It is optional in nature as it involves

decision making concept and a firm has

to decide about it accordingly. Capital

It is mandatory for a firm as it involves

communicating the financial position of

the business. Capital joinery Ltd does

1

Management accounting is a process of identifying the aspects that affects the working of

the business directly or indirectly and then making a report with reference to the data that is

collected. Capital Joinery Ltd is a firm that deals in various products an services and is operating

since 2008 in London. This report covers various topics such as different types of management

accounting system and techniques. Apart from this it also covers topics of planning tools, cost

analysis, and different types of costs. Also the way in which an organisation deals with the

problems that are of financial nature.

TASK 1

P1 Defining management accounting and its essential requirements

Management accounting refers to a process of critically identifying and evaluating the

information related to accounts so that it can be precisely used by the managers to take decisions

which is in accordance with the information provided so that it can help a business to grow and

prosper in its industry. It is very important for a business as it helps management to take

decisions which can either be short or long term that helps a firm to improve its financial

stability. Capital joinery Ltd is a carpenter and joinery firm which provides made to measure

doors, double gazed, stairs, sash windows, etc. though the firm has been established in 2008

only, but it has gathered a pool of customer base (Abba, 2018). It is very essential to have a

improved and sophisticated version of management accounting system so that decisions taken

could be well directed and thus helping the firm to grow and capture a larger share of market.

Management accounting originated during 1900's from financial management but it is a lot

different from it in all aspects. Role of management accounting is to collect relevant data and

then analysing it so that it can be beneficial for the company. Principles of it includes that there

should be credibility of the data that is given, as well as it should influence the working of firm

in a positive way. Management and financial accounting differentiation is done below briefly-

Management accounting Financial accounting

It is optional in nature as it involves

decision making concept and a firm has

to decide about it accordingly. Capital

It is mandatory for a firm as it involves

communicating the financial position of

the business. Capital joinery Ltd does

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

joinery Ltd has a business of public

dealing so the firm uses it to ensure that

decisions are taken effectively and

efficiently which act as a benchmark in

increasing the profitability.

It is used internally to analyse the

position of the business mainly by

managers and employees. Capital

joinery Ltd has a expertise team of

management that helps in this process

(Alabdullah, 2019).

financial accounting so that the

performance of the firm can be

analysed. This helps in increasing the

scope for the company in the long run.

It is done for external use so mainly for

outsiders that are directly or indirectly

interested in the working of the firm

like shareholders, lenders, banks, etc.

Capital joinery Ltd does a detailed

analysis in this regard so that it could

not hamper the working of the firm.

Different types of management accounting system are explained in detail below-

Cost-accounting system- It is a system in which cost is analysed of a product so that the

profitability level could be decided on which a firm can operate effectively. Capital joinery Ltd

employs a specialised team of experts that do research and analysis so that a perfect cost of the

product can be decided which can prevail in the market without any problems.

Inventory management system- In this system entire supply chain is tracked and so that

goods are safely procured and then supplied to the desired customer. Capital joinery Ltd has a

intact supply chain that is the backbone of the firm that helps it in working efficiently and

effectively (Askarany, 2016).

Job-costing system- This is a system in which costs regarding jobs are analysed so that

unnecessary expenses can be cut down which is beneficial for the firm. Capital joinery Ltd does

an intensive research in this aspect and reduces the wastage in its process if there is any.

Price-optimising system- In this system different prices are compared that can prevail in

the market at different levels so that a perfect decision can be taken. Capital joinery Ltd is very

precise in analysing different prices and thus helps the working of the firm in long run (Bedford

and Speklé, 2018).

P2. Management accounting reporting different methods

Management accounting reporting can be defined as a report that is given to the internal

team after rigorous evaluation so that it can help in better decision making and thus benefiting

2

dealing so the firm uses it to ensure that

decisions are taken effectively and

efficiently which act as a benchmark in

increasing the profitability.

It is used internally to analyse the

position of the business mainly by

managers and employees. Capital

joinery Ltd has a expertise team of

management that helps in this process

(Alabdullah, 2019).

financial accounting so that the

performance of the firm can be

analysed. This helps in increasing the

scope for the company in the long run.

It is done for external use so mainly for

outsiders that are directly or indirectly

interested in the working of the firm

like shareholders, lenders, banks, etc.

Capital joinery Ltd does a detailed

analysis in this regard so that it could

not hamper the working of the firm.

Different types of management accounting system are explained in detail below-

Cost-accounting system- It is a system in which cost is analysed of a product so that the

profitability level could be decided on which a firm can operate effectively. Capital joinery Ltd

employs a specialised team of experts that do research and analysis so that a perfect cost of the

product can be decided which can prevail in the market without any problems.

Inventory management system- In this system entire supply chain is tracked and so that

goods are safely procured and then supplied to the desired customer. Capital joinery Ltd has a

intact supply chain that is the backbone of the firm that helps it in working efficiently and

effectively (Askarany, 2016).

Job-costing system- This is a system in which costs regarding jobs are analysed so that

unnecessary expenses can be cut down which is beneficial for the firm. Capital joinery Ltd does

an intensive research in this aspect and reduces the wastage in its process if there is any.

Price-optimising system- In this system different prices are compared that can prevail in

the market at different levels so that a perfect decision can be taken. Capital joinery Ltd is very

precise in analysing different prices and thus helps the working of the firm in long run (Bedford

and Speklé, 2018).

P2. Management accounting reporting different methods

Management accounting reporting can be defined as a report that is given to the internal

team after rigorous evaluation so that it can help in better decision making and thus benefiting

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the overall growth of the firm. Capital joinery Ltd uses different methods of reporting that are

explained in detail below-

Budget report- It is a report in which actual performance is compared with the previous

report or with any set standards of the business. It is very helpful in analysing the variance and

cause for it and after that it can be rectified by taking necessary measures. Capital joinery Ltd

does a variance analysis through this report and the firm is able to identify the loop hole sin the

business and then the information gathered is summarised and then improvements are done

accordingly.

Accounts receivable ageing report- In this report as the name suggests it helps in

identifying the information regarding accounts receivables so that if it is performing badly it can

be improved. Capital joinery Ltd does a detailed study of its receivables and by this it gets to

know about it and then it takes necessary measures that has the potential to improve its

performance (Bisogno and Vaia, 2017).

Performance report- This is a budget which shows the performance of the company so

that the stakeholders and the government can see whether the funds are correctly utilised or not.

Capital joinery Ltd shares the detail of its performance budget with all the bodies that are directly

or indirectly connected with the firm and thus improving the market value. It also encourages the

management and employees to perform to their best because the report is seen by many and any

fall in the performance can be identified quickly.

Inventory and manufacturing report- In this report there is a detailed analysis of

inventory related things which includes all its processes starting from raw material to finished

goods. It helps a firm to reduce any wastage in terms of inventory as well as efficiency level can

also be increased. Capital joinery Ltd employs a team of skilled managers to do research and

analysis of it so that scope for any errors can be reduced. It also helped the firm to increase the

level of profitability because of reduction in wastages.

M1. Describing benefits and application of management accounting system

Benefits of management accounting system with reference to firm is given below in

detail-

Cost-accounting system- This system helps in identifying the activities so that the

profitable one can be chosen and measures can be introduces so that the unprofitable activities

can be reduced as much as possible. Capital joinery Ltd has used many measures to identify and

3

explained in detail below-

Budget report- It is a report in which actual performance is compared with the previous

report or with any set standards of the business. It is very helpful in analysing the variance and

cause for it and after that it can be rectified by taking necessary measures. Capital joinery Ltd

does a variance analysis through this report and the firm is able to identify the loop hole sin the

business and then the information gathered is summarised and then improvements are done

accordingly.

Accounts receivable ageing report- In this report as the name suggests it helps in

identifying the information regarding accounts receivables so that if it is performing badly it can

be improved. Capital joinery Ltd does a detailed study of its receivables and by this it gets to

know about it and then it takes necessary measures that has the potential to improve its

performance (Bisogno and Vaia, 2017).

Performance report- This is a budget which shows the performance of the company so

that the stakeholders and the government can see whether the funds are correctly utilised or not.

Capital joinery Ltd shares the detail of its performance budget with all the bodies that are directly

or indirectly connected with the firm and thus improving the market value. It also encourages the

management and employees to perform to their best because the report is seen by many and any

fall in the performance can be identified quickly.

Inventory and manufacturing report- In this report there is a detailed analysis of

inventory related things which includes all its processes starting from raw material to finished

goods. It helps a firm to reduce any wastage in terms of inventory as well as efficiency level can

also be increased. Capital joinery Ltd employs a team of skilled managers to do research and

analysis of it so that scope for any errors can be reduced. It also helped the firm to increase the

level of profitability because of reduction in wastages.

M1. Describing benefits and application of management accounting system

Benefits of management accounting system with reference to firm is given below in

detail-

Cost-accounting system- This system helps in identifying the activities so that the

profitable one can be chosen and measures can be introduces so that the unprofitable activities

can be reduced as much as possible. Capital joinery Ltd has used many measures to identify and

3

prevent wastage and this system is taken the firm to a new heights making it a valuable company

within a short period of time (Gnawali, 2017).

Inventory management system- This system simplifies the inventory management

process which helps a business to grow. This system has helped Capital joinery Ltd to simplify

tits complex process.

Job-costing system- It measures and monitors the cost and employee performance which

is very important for a business. Capital joinery Ltd is performing best in its operations and

profitability just because of this system.

Price-optimising system- It is very helpful in making better and quick decisions and thus

reducing the time and effort in it. Capital joinery Ltd has reduces the time it consumes in

decision making and also improves the accuracy of it.

D1. Evaluating the integration of management accounting reporting and management accounting

system

Management accounting systems and reporting is integrated and helps in company's

processes. It has been discussed below-

Budget report- It helps in company's processes as it identify variances and the reasons

for it and it is very beneficial for a firm in long run. Capital joinery Ltd has been in one of the

most profitable firm in a very short time and budget report helped it a lot (Kashora and 2016).

Cost-accounting system- It contributes a lot in improving company's processes as it

helps in cutting down cost which is of no use. Capital joinery Ltd when started is not doing very

well due to additional costs that it incurs but when it used this system it has changed it a lot and

the firm has become much more profitable than earlier by reducing unnecessary costs.

TASK 2

P3. Preparation of income statement using marginal and absorption cost using cost analysis

technique

Cost can be defined as the price that is paid for using a particular service or for

purchasing a product. There are different types of cost that are explained briefly below-

Fixed cost- These type of costs are those which remain constant during the course of

business. It plays a very important part in the working of a business because this cost will incur

whether business is operational or not so each firm wants to cover its fixed cost first. Capital

4

within a short period of time (Gnawali, 2017).

Inventory management system- This system simplifies the inventory management

process which helps a business to grow. This system has helped Capital joinery Ltd to simplify

tits complex process.

Job-costing system- It measures and monitors the cost and employee performance which

is very important for a business. Capital joinery Ltd is performing best in its operations and

profitability just because of this system.

Price-optimising system- It is very helpful in making better and quick decisions and thus

reducing the time and effort in it. Capital joinery Ltd has reduces the time it consumes in

decision making and also improves the accuracy of it.

D1. Evaluating the integration of management accounting reporting and management accounting

system

Management accounting systems and reporting is integrated and helps in company's

processes. It has been discussed below-

Budget report- It helps in company's processes as it identify variances and the reasons

for it and it is very beneficial for a firm in long run. Capital joinery Ltd has been in one of the

most profitable firm in a very short time and budget report helped it a lot (Kashora and 2016).

Cost-accounting system- It contributes a lot in improving company's processes as it

helps in cutting down cost which is of no use. Capital joinery Ltd when started is not doing very

well due to additional costs that it incurs but when it used this system it has changed it a lot and

the firm has become much more profitable than earlier by reducing unnecessary costs.

TASK 2

P3. Preparation of income statement using marginal and absorption cost using cost analysis

technique

Cost can be defined as the price that is paid for using a particular service or for

purchasing a product. There are different types of cost that are explained briefly below-

Fixed cost- These type of costs are those which remain constant during the course of

business. It plays a very important part in the working of a business because this cost will incur

whether business is operational or not so each firm wants to cover its fixed cost first. Capital

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

joinery Ltd operates with a little fixed cost so it covers it easily which is helpful in its overall

profitability.

Variable cost- It is a cost which changes with the change in output. If there is a increase

in output variable cost also increases and if there is decrease in output variable cost also

decreases. Capital joinery Ltd decide its level of output very carefully so that variable cost would

not become a burden for the company and this helped the firm in maintaining a good level of

profit (Lay and Jusoh, 2017).

Semi-variable cost- As the name suggests it is a cost which includes both fixed cost and

variable cost. Part of fixed cost will be fixed but variable cost increases and decreases in

reference to output. Capital joinery Ltd has a low semi-variable cost due to its research and

analysis which helped in decreasing these costs which proved beneficial for the firm in long run.

Cost analysis- It may be defined as the analysis of different types of cost so that a

comparison can be done within different types. It is very beneficial for a business as it helps in

reducing the extra costs that are not benefiting the firm in any way. Capital joinery Ltd has a

specialised team of experts in the research and development wing which do a detailed analysis of

all the costs separately so that it can add to the value of the firm.

Cost-volume profit- It is a method which analysis the impact of cost and volume at

different levels of operating profits. It is very important for a firm as both cost and volume are an

integral part of the business and it analysis this aspect of the company (Ng and 2017).

Flexible budget- It is a budget which is flexible in nature which means it changes

according to the activity, volume, or both. It shows the variations that a firm possess in relation

to the different cost it operates in.

Cost variances- It can be defined as the variance between the actual and budgeted. It is

preferable at lower side because lower variance means there is a least deviation which is very

beneficial for the firm in short as well as in long run.

Absorption costing- It can be defined as summation of all the different types of costs

such as land, labour, capital, entrepreneur. The cost are rent for land, wages for labour, etc. all

are included in this type of costing.

Marginal costing- It can be defined as cost of producing a extra unit of output it can

either increased or decreased depending upon the variable. It can be further simplified as change

in total cost of a product due to change in output.

5

profitability.

Variable cost- It is a cost which changes with the change in output. If there is a increase

in output variable cost also increases and if there is decrease in output variable cost also

decreases. Capital joinery Ltd decide its level of output very carefully so that variable cost would

not become a burden for the company and this helped the firm in maintaining a good level of

profit (Lay and Jusoh, 2017).

Semi-variable cost- As the name suggests it is a cost which includes both fixed cost and

variable cost. Part of fixed cost will be fixed but variable cost increases and decreases in

reference to output. Capital joinery Ltd has a low semi-variable cost due to its research and

analysis which helped in decreasing these costs which proved beneficial for the firm in long run.

Cost analysis- It may be defined as the analysis of different types of cost so that a

comparison can be done within different types. It is very beneficial for a business as it helps in

reducing the extra costs that are not benefiting the firm in any way. Capital joinery Ltd has a

specialised team of experts in the research and development wing which do a detailed analysis of

all the costs separately so that it can add to the value of the firm.

Cost-volume profit- It is a method which analysis the impact of cost and volume at

different levels of operating profits. It is very important for a firm as both cost and volume are an

integral part of the business and it analysis this aspect of the company (Ng and 2017).

Flexible budget- It is a budget which is flexible in nature which means it changes

according to the activity, volume, or both. It shows the variations that a firm possess in relation

to the different cost it operates in.

Cost variances- It can be defined as the variance between the actual and budgeted. It is

preferable at lower side because lower variance means there is a least deviation which is very

beneficial for the firm in short as well as in long run.

Absorption costing- It can be defined as summation of all the different types of costs

such as land, labour, capital, entrepreneur. The cost are rent for land, wages for labour, etc. all

are included in this type of costing.

Marginal costing- It can be defined as cost of producing a extra unit of output it can

either increased or decreased depending upon the variable. It can be further simplified as change

in total cost of a product due to change in output.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

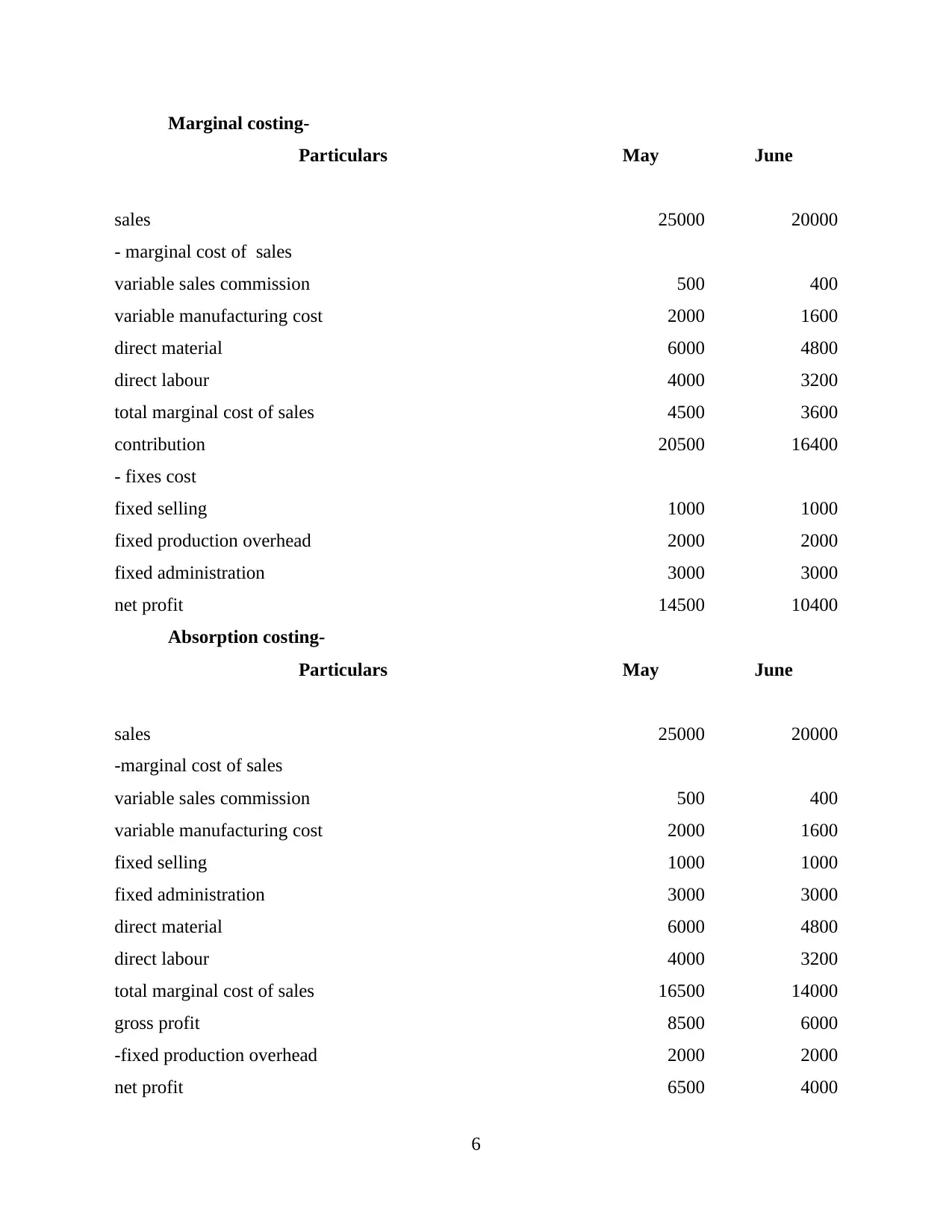

Marginal costing-

Particulars May June

sales 25000 20000

- marginal cost of sales

variable sales commission 500 400

variable manufacturing cost 2000 1600

direct material 6000 4800

direct labour 4000 3200

total marginal cost of sales 4500 3600

contribution 20500 16400

- fixes cost

fixed selling 1000 1000

fixed production overhead 2000 2000

fixed administration 3000 3000

net profit 14500 10400

Absorption costing-

Particulars May June

sales 25000 20000

-marginal cost of sales

variable sales commission 500 400

variable manufacturing cost 2000 1600

fixed selling 1000 1000

fixed administration 3000 3000

direct material 6000 4800

direct labour 4000 3200

total marginal cost of sales 16500 14000

gross profit 8500 6000

-fixed production overhead 2000 2000

net profit 6500 4000

6

Particulars May June

sales 25000 20000

- marginal cost of sales

variable sales commission 500 400

variable manufacturing cost 2000 1600

direct material 6000 4800

direct labour 4000 3200

total marginal cost of sales 4500 3600

contribution 20500 16400

- fixes cost

fixed selling 1000 1000

fixed production overhead 2000 2000

fixed administration 3000 3000

net profit 14500 10400

Absorption costing-

Particulars May June

sales 25000 20000

-marginal cost of sales

variable sales commission 500 400

variable manufacturing cost 2000 1600

fixed selling 1000 1000

fixed administration 3000 3000

direct material 6000 4800

direct labour 4000 3200

total marginal cost of sales 16500 14000

gross profit 8500 6000

-fixed production overhead 2000 2000

net profit 6500 4000

6

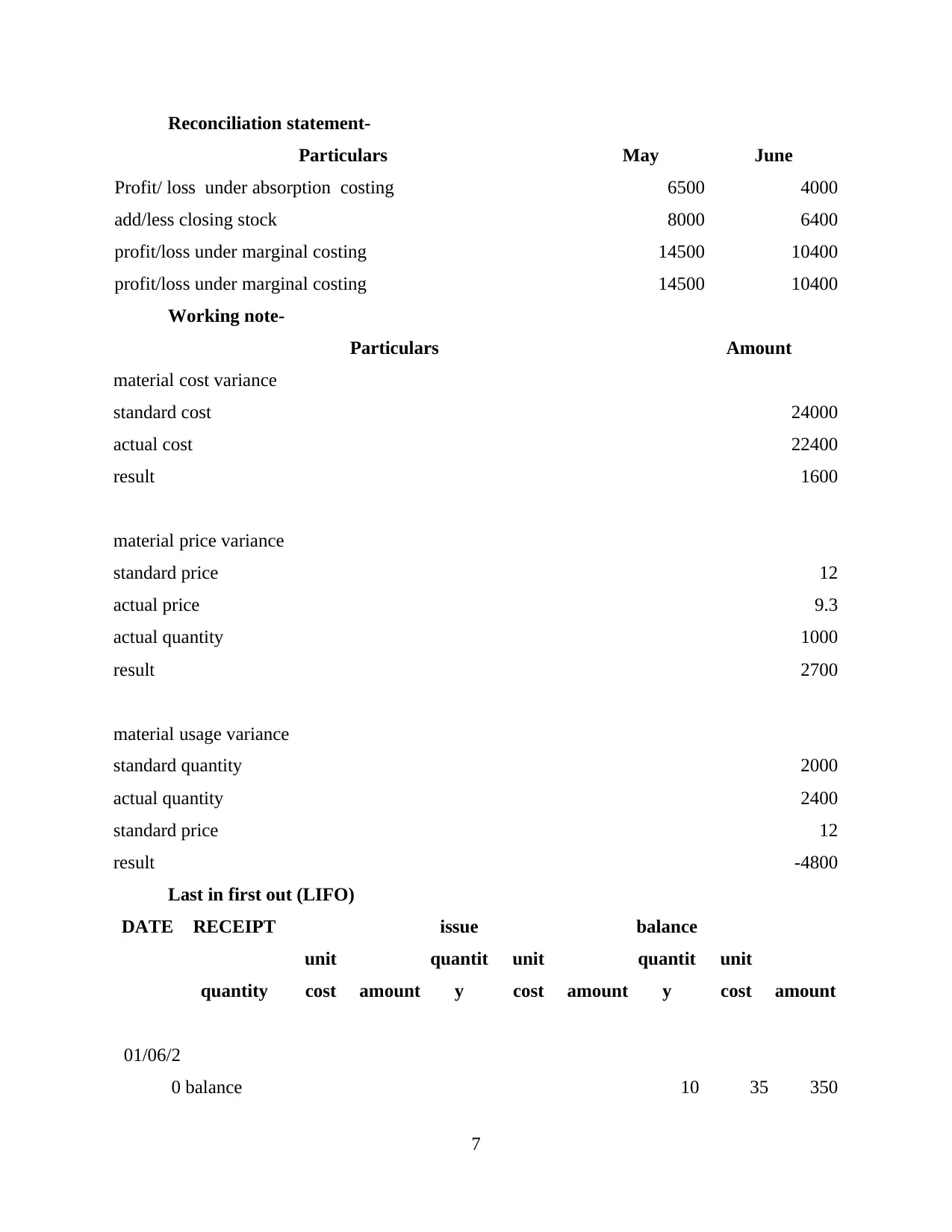

Reconciliation statement-

Particulars May June

Profit/ loss under absorption costing 6500 4000

add/less closing stock 8000 6400

profit/loss under marginal costing 14500 10400

profit/loss under marginal costing 14500 10400

Working note-

Particulars Amount

material cost variance

standard cost 24000

actual cost 22400

result 1600

material price variance

standard price 12

actual price 9.3

actual quantity 1000

result 2700

material usage variance

standard quantity 2000

actual quantity 2400

standard price 12

result -4800

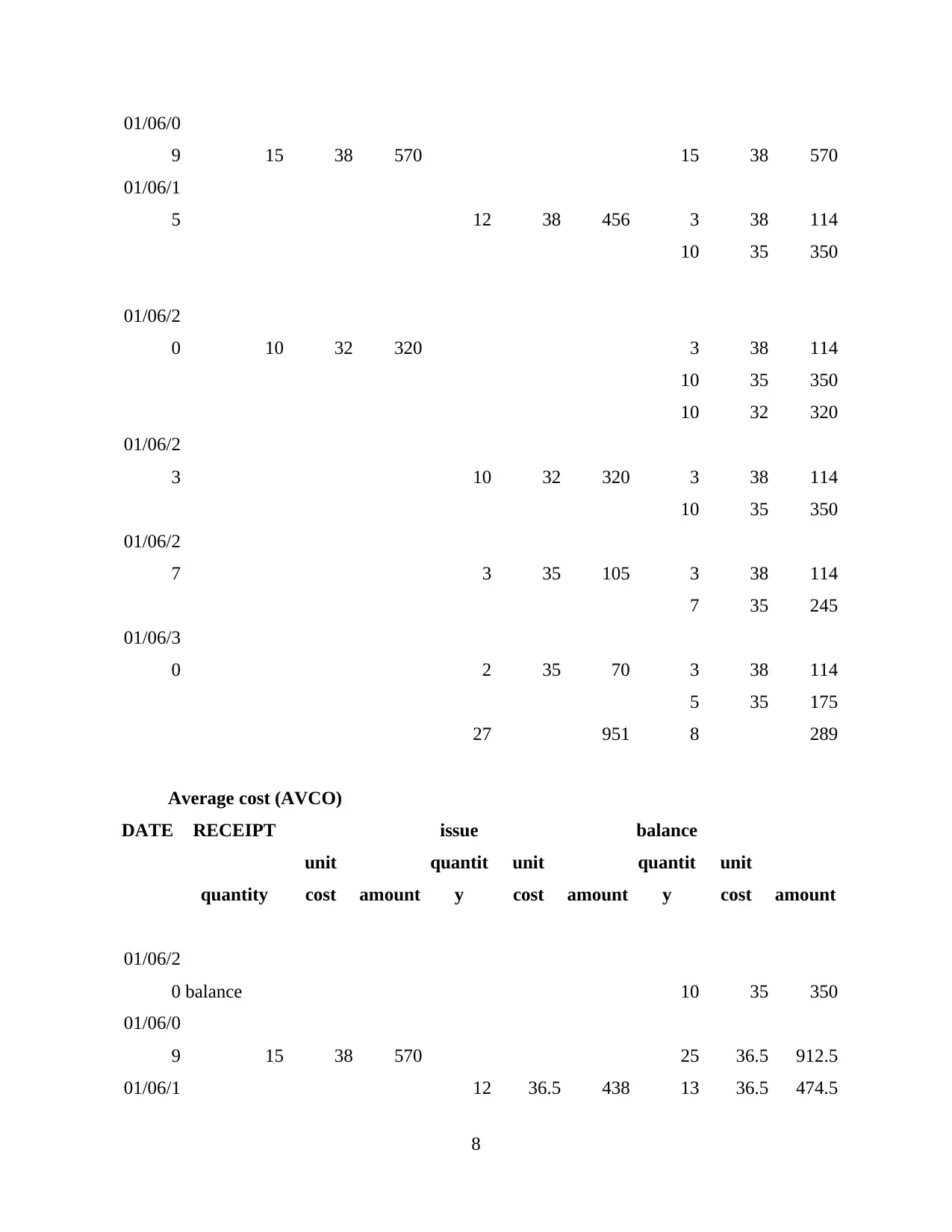

Last in first out (LIFO)

DATE RECEIPT issue balance

quantity

unit

cost amount

quantit

y

unit

cost amount

quantit

y

unit

cost amount

01/06/2

0 balance 10 35 350

7

Particulars May June

Profit/ loss under absorption costing 6500 4000

add/less closing stock 8000 6400

profit/loss under marginal costing 14500 10400

profit/loss under marginal costing 14500 10400

Working note-

Particulars Amount

material cost variance

standard cost 24000

actual cost 22400

result 1600

material price variance

standard price 12

actual price 9.3

actual quantity 1000

result 2700

material usage variance

standard quantity 2000

actual quantity 2400

standard price 12

result -4800

Last in first out (LIFO)

DATE RECEIPT issue balance

quantity

unit

cost amount

quantit

y

unit

cost amount

quantit

y

unit

cost amount

01/06/2

0 balance 10 35 350

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

01/06/0

9 15 38 570 15 38 570

01/06/1

5 12 38 456 3 38 114

10 35 350

01/06/2

0 10 32 320 3 38 114

10 35 350

10 32 320

01/06/2

3 10 32 320 3 38 114

10 35 350

01/06/2

7 3 35 105 3 38 114

7 35 245

01/06/3

0 2 35 70 3 38 114

5 35 175

27 951 8 289

Average cost (AVCO)

DATE RECEIPT issue balance

quantity

unit

cost amount

quantit

y

unit

cost amount

quantit

y

unit

cost amount

01/06/2

0 balance 10 35 350

01/06/0

9 15 38 570 25 36.5 912.5

01/06/1 12 36.5 438 13 36.5 474.5

8

9 15 38 570 15 38 570

01/06/1

5 12 38 456 3 38 114

10 35 350

01/06/2

0 10 32 320 3 38 114

10 35 350

10 32 320

01/06/2

3 10 32 320 3 38 114

10 35 350

01/06/2

7 3 35 105 3 38 114

7 35 245

01/06/3

0 2 35 70 3 38 114

5 35 175

27 951 8 289

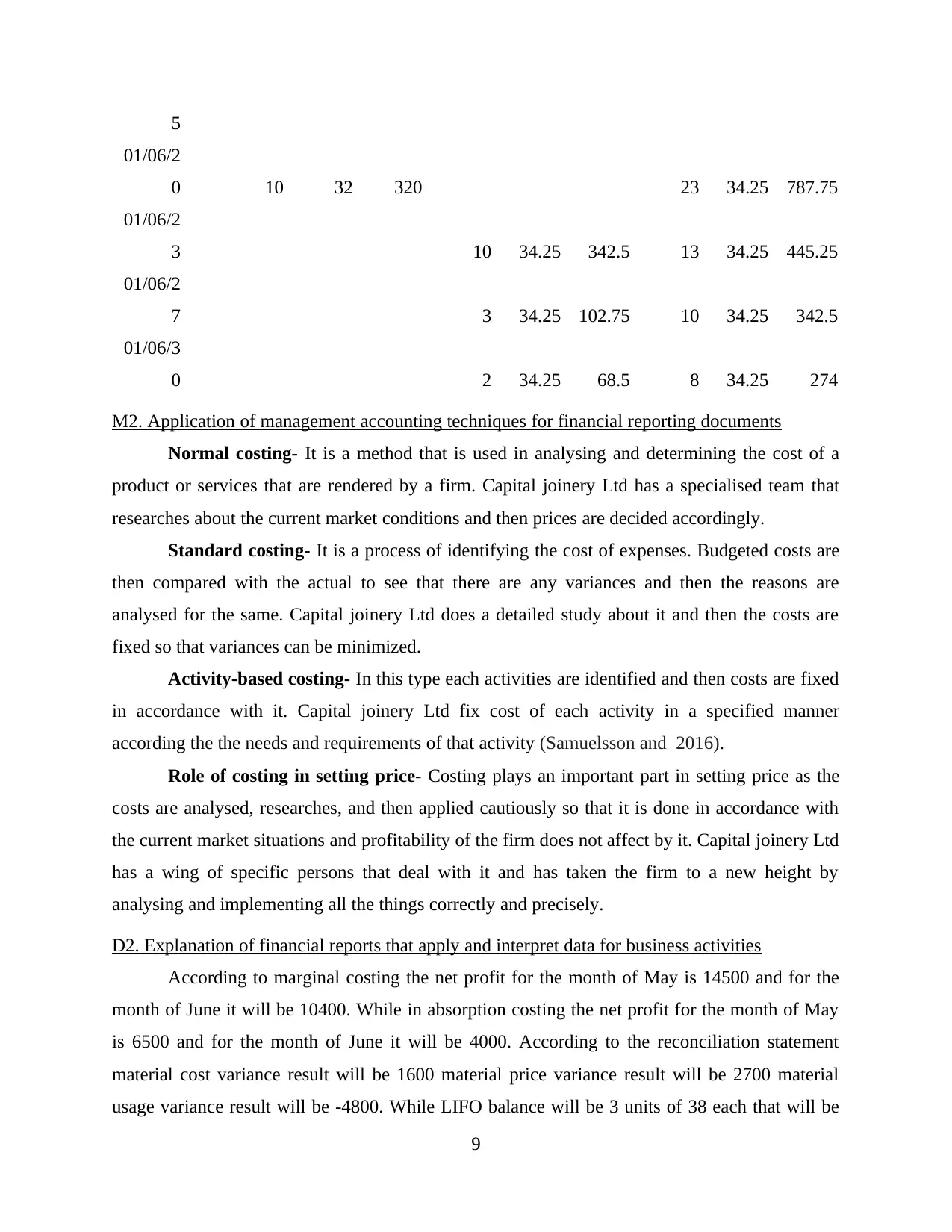

Average cost (AVCO)

DATE RECEIPT issue balance

quantity

unit

cost amount

quantit

y

unit

cost amount

quantit

y

unit

cost amount

01/06/2

0 balance 10 35 350

01/06/0

9 15 38 570 25 36.5 912.5

01/06/1 12 36.5 438 13 36.5 474.5

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

01/06/2

0 10 32 320 23 34.25 787.75

01/06/2

3 10 34.25 342.5 13 34.25 445.25

01/06/2

7 3 34.25 102.75 10 34.25 342.5

01/06/3

0 2 34.25 68.5 8 34.25 274

M2. Application of management accounting techniques for financial reporting documents

Normal costing- It is a method that is used in analysing and determining the cost of a

product or services that are rendered by a firm. Capital joinery Ltd has a specialised team that

researches about the current market conditions and then prices are decided accordingly.

Standard costing- It is a process of identifying the cost of expenses. Budgeted costs are

then compared with the actual to see that there are any variances and then the reasons are

analysed for the same. Capital joinery Ltd does a detailed study about it and then the costs are

fixed so that variances can be minimized.

Activity-based costing- In this type each activities are identified and then costs are fixed

in accordance with it. Capital joinery Ltd fix cost of each activity in a specified manner

according the the needs and requirements of that activity (Samuelsson and 2016).

Role of costing in setting price- Costing plays an important part in setting price as the

costs are analysed, researches, and then applied cautiously so that it is done in accordance with

the current market situations and profitability of the firm does not affect by it. Capital joinery Ltd

has a wing of specific persons that deal with it and has taken the firm to a new height by

analysing and implementing all the things correctly and precisely.

D2. Explanation of financial reports that apply and interpret data for business activities

According to marginal costing the net profit for the month of May is 14500 and for the

month of June it will be 10400. While in absorption costing the net profit for the month of May

is 6500 and for the month of June it will be 4000. According to the reconciliation statement

material cost variance result will be 1600 material price variance result will be 2700 material

usage variance result will be -4800. While LIFO balance will be 3 units of 38 each that will be

9

01/06/2

0 10 32 320 23 34.25 787.75

01/06/2

3 10 34.25 342.5 13 34.25 445.25

01/06/2

7 3 34.25 102.75 10 34.25 342.5

01/06/3

0 2 34.25 68.5 8 34.25 274

M2. Application of management accounting techniques for financial reporting documents

Normal costing- It is a method that is used in analysing and determining the cost of a

product or services that are rendered by a firm. Capital joinery Ltd has a specialised team that

researches about the current market conditions and then prices are decided accordingly.

Standard costing- It is a process of identifying the cost of expenses. Budgeted costs are

then compared with the actual to see that there are any variances and then the reasons are

analysed for the same. Capital joinery Ltd does a detailed study about it and then the costs are

fixed so that variances can be minimized.

Activity-based costing- In this type each activities are identified and then costs are fixed

in accordance with it. Capital joinery Ltd fix cost of each activity in a specified manner

according the the needs and requirements of that activity (Samuelsson and 2016).

Role of costing in setting price- Costing plays an important part in setting price as the

costs are analysed, researches, and then applied cautiously so that it is done in accordance with

the current market situations and profitability of the firm does not affect by it. Capital joinery Ltd

has a wing of specific persons that deal with it and has taken the firm to a new height by

analysing and implementing all the things correctly and precisely.

D2. Explanation of financial reports that apply and interpret data for business activities

According to marginal costing the net profit for the month of May is 14500 and for the

month of June it will be 10400. While in absorption costing the net profit for the month of May

is 6500 and for the month of June it will be 4000. According to the reconciliation statement

material cost variance result will be 1600 material price variance result will be 2700 material

usage variance result will be -4800. While LIFO balance will be 3 units of 38 each that will be

9

114 and 5 units of 35 each that will be 175 whereas AVCO balance will be 8 units of 34.25 each

that will amount to 274.

TASK 3

P4 Explanation of advantages and disadvantages of different types of planning tools used for

budgetary control.

Budget is the estimation of incomes and expenses for a specific future period of time

which is usually compiled and re-evaluated on periodical basis by Capital Joinery Ltd. It is made

by a person, group of people, government or anybody who makes and spends money. Budgetary

control Budgeting methods many depend upon the type of business company is operating. The

following are some types of budgeting techniques used in Capital Joinery Ltd:

Capital Budgeting- This budgeting method revolves around capital expenditures which involves

large inflow and outflow of money in financial investments of Capital Joinery Ltd. With this

process company decides whether it should invest in project or not (okolov and Elsukova 2016).

Advantages

It helps in understanding the risks and its effects of the business of company.

The main focus is over decision making for the decisions related to and investment

opportunities.

Disadvantages

The decisions through such budgeting technique takes long time, which is irreversible in

nature.

The availability of skilled professionals is not too easy for such long term based

decisions.

Operating Budgeting- It is financial plan which is designed to help Capital Joinery Ltd meet

the debt obligations and sustain growth over time period. By creating operational budgeting plan

company can find out ways to spend its money and areas of business needs money the most

(Tan, 2016).

Advantages

It keeps the track of entire business activities which indicates both money that would be

spent by company and money well come in.

10

that will amount to 274.

TASK 3

P4 Explanation of advantages and disadvantages of different types of planning tools used for

budgetary control.

Budget is the estimation of incomes and expenses for a specific future period of time

which is usually compiled and re-evaluated on periodical basis by Capital Joinery Ltd. It is made

by a person, group of people, government or anybody who makes and spends money. Budgetary

control Budgeting methods many depend upon the type of business company is operating. The

following are some types of budgeting techniques used in Capital Joinery Ltd:

Capital Budgeting- This budgeting method revolves around capital expenditures which involves

large inflow and outflow of money in financial investments of Capital Joinery Ltd. With this

process company decides whether it should invest in project or not (okolov and Elsukova 2016).

Advantages

It helps in understanding the risks and its effects of the business of company.

The main focus is over decision making for the decisions related to and investment

opportunities.

Disadvantages

The decisions through such budgeting technique takes long time, which is irreversible in

nature.

The availability of skilled professionals is not too easy for such long term based

decisions.

Operating Budgeting- It is financial plan which is designed to help Capital Joinery Ltd meet

the debt obligations and sustain growth over time period. By creating operational budgeting plan

company can find out ways to spend its money and areas of business needs money the most

(Tan, 2016).

Advantages

It keeps the track of entire business activities which indicates both money that would be

spent by company and money well come in.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.