Management Accounting Report: UCK Furniture, Costing and Budgeting

VerifiedAdded on 2023/01/12

|24

|2763

|93

Report

AI Summary

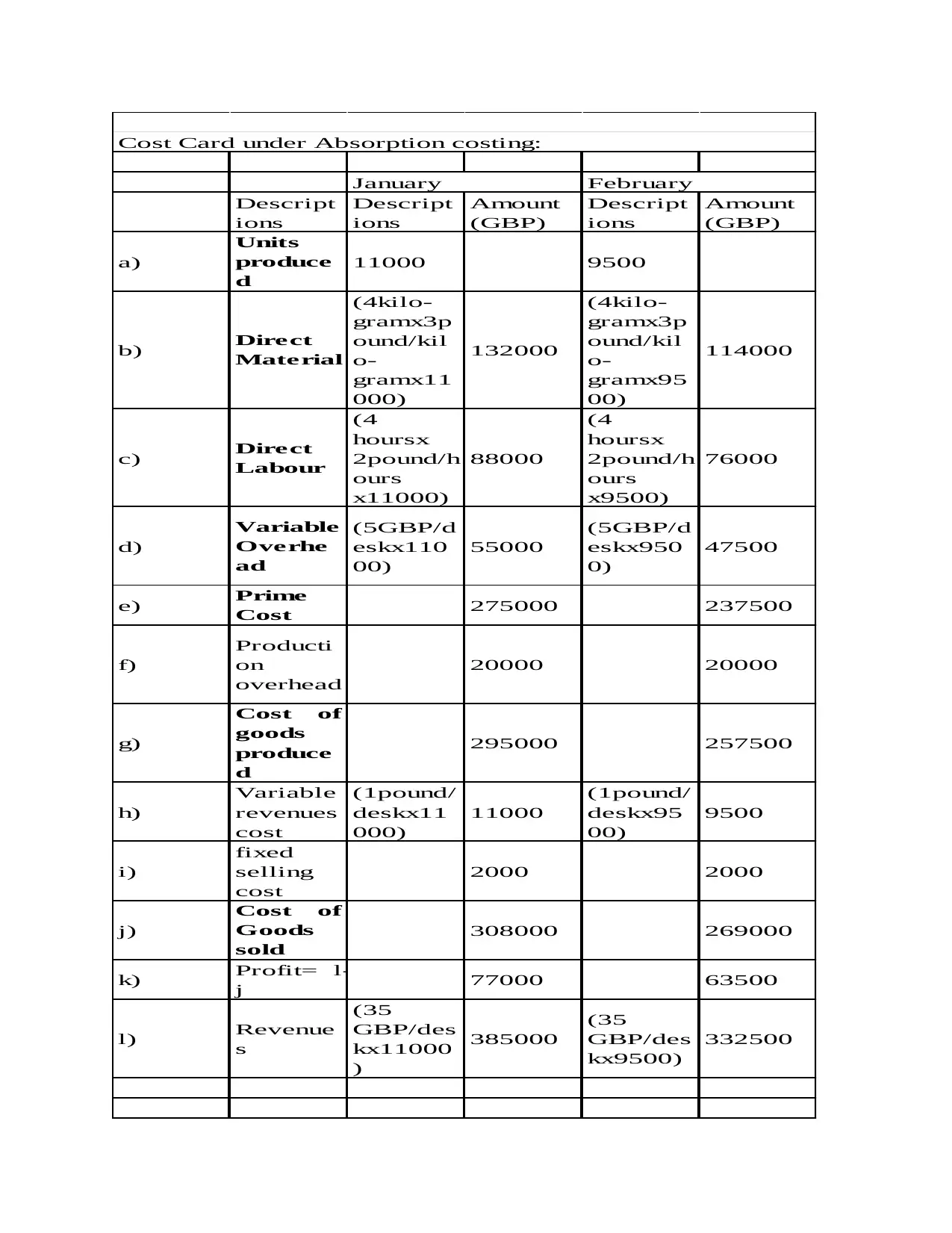

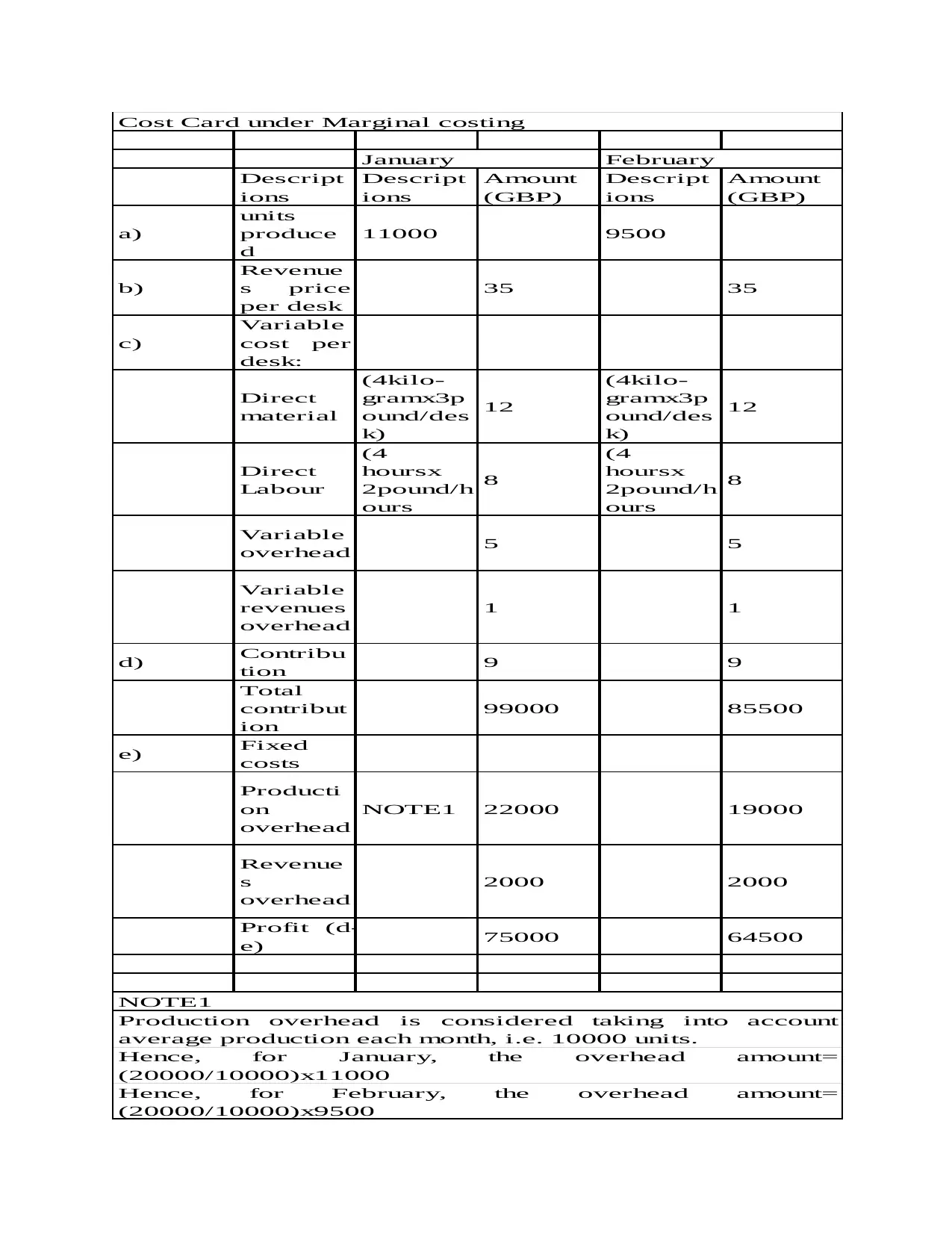

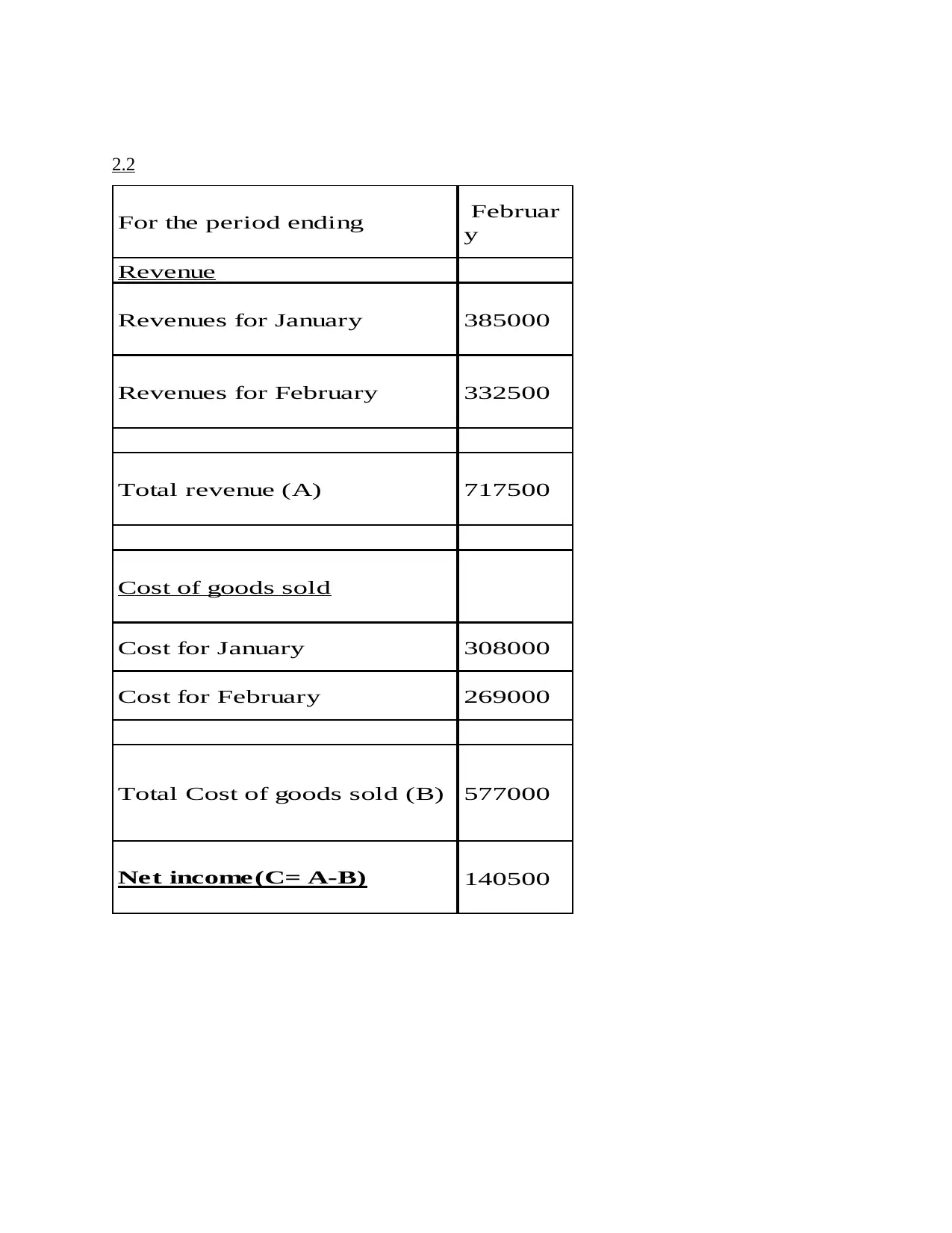

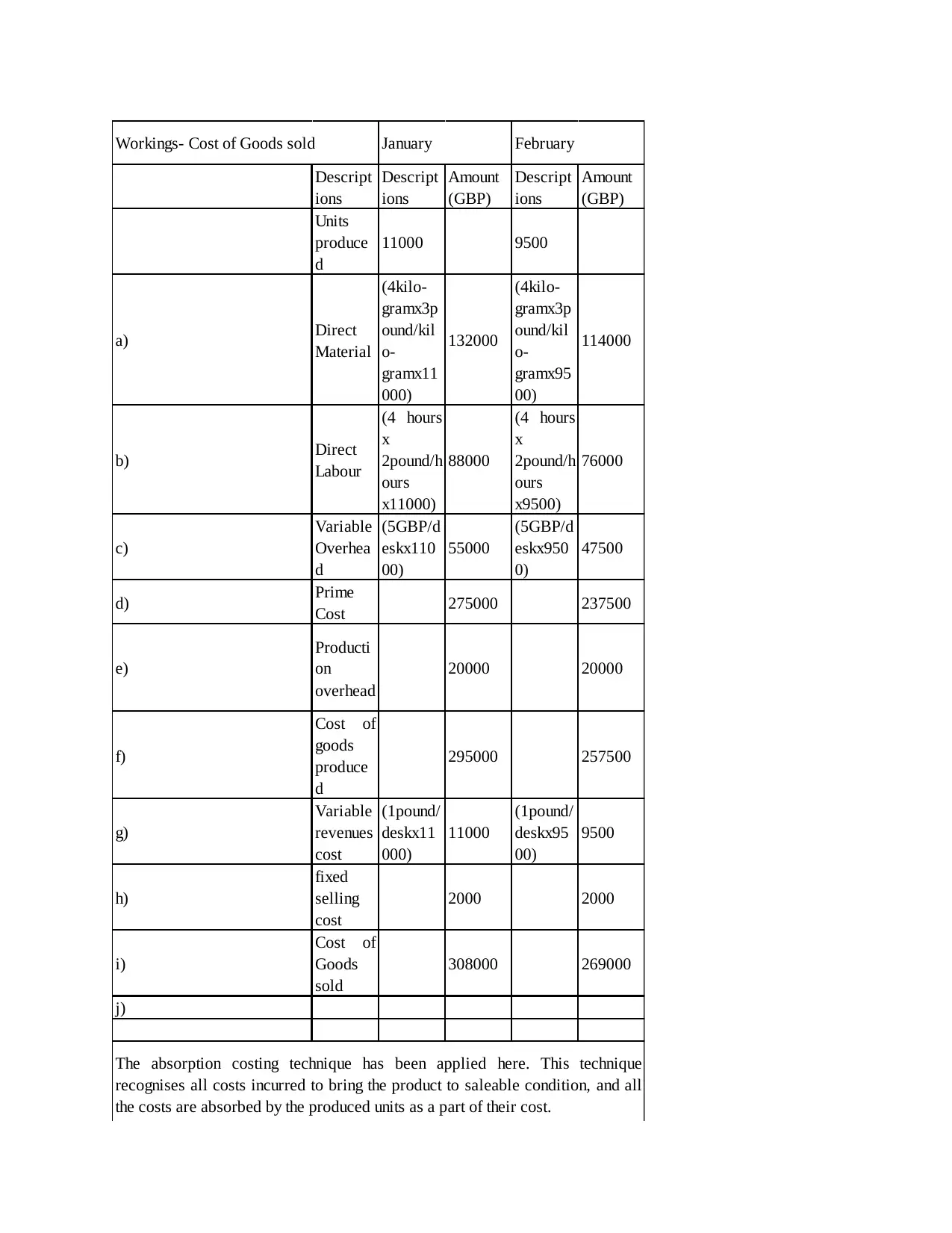

This report provides a detailed analysis of management accounting systems and their application within UCK Furniture. It begins with an introduction to management accounting, its importance, and the various systems employed, including inventory management, job costing, and price optimization. The report then delves into practical applications, such as the preparation of cost cards using both absorption and marginal costing methods, along with a comparative analysis of their merits and demerits. Furthermore, it includes an income statement analysis and interpretation. The report also covers budgeting, including cash collection and disbursement schedules, and a cash budget. It concludes with a comparison of enterprises utilizing management accounting systems to address financial issues and a ratio analysis of UCK Furniture's divisions, assessing return on capital employed, asset turnover, and operating profit margin. The report provides a comprehensive overview of financial management accounting principles.

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.