AYB225 Management Accounting Report: Costing Methods and Analysis

VerifiedAdded on 2022/11/28

|9

|1235

|55

Report

AI Summary

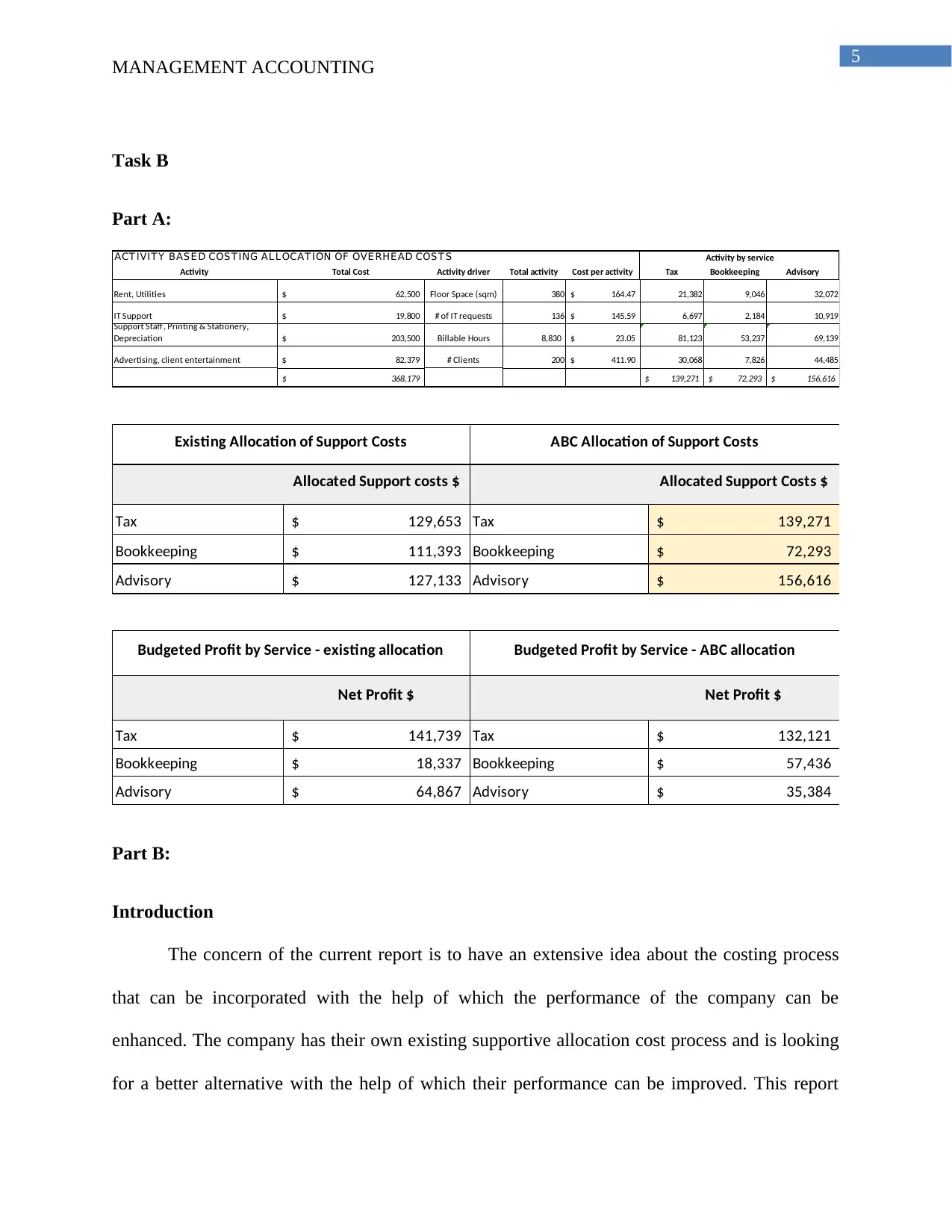

This report analyzes the financial performance of T&K Accounting Services, evaluating the impact of an advisory department on profitability. Task A presents an email notification to stakeholders, detailing budget comparisons and profit margins before and after the addition of the advisory department, advocating for its inclusion based on increased profitability and cost segregation. Task B focuses on the costing processes, comparing the current costing method with the ABC costing system. The analysis reveals that ABC costing improves the company's performance by distributing costs and profits more equitably across departments. The report recommends the adoption of ABC costing to enhance overall performance and provides detailed calculations to support its conclusions. The report concludes that ABC costing is a superior method for the company, and proper supervision should be maintained to achieve better profits. This report provides detailed financial analysis and budget comparisons to support its recommendations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.