Management Accounting Report: Systems and Reporting

VerifiedAdded on 2023/01/11

|21

|5354

|81

Report

AI Summary

This report delves into the core concepts of management accounting, encompassing various systems and techniques applied to Creams Ltd, an ice cream, waffle, and doughnut business. It explores management accounting systems such as inventory management, cost accounting, price optimization, and job costing, highlighting their advantages and integration within organizational processes. The report also examines different types of management accounting reporting, including budget reports, performance reports, and accounts receivable reports, demonstrating their significance in facilitating strategic decision-making. Furthermore, it provides a detailed comparison of marginal and absorption costing methods through income statements, and it discusses the use of planning tools for budget preparation and financial forecasting. The report concludes with an evaluation of how management accounting systems are utilized to address financial problems, ultimately contributing to sustainable success. The analysis includes relevant financial reports and their interpretation for business operational activities.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1. Management accounting systems......................................................................................................3

P2. Management accounting reporting....................................................................................................5

M1. Advantages of management accounting systems..............................................................................6

D1 Evaluation of accounting systems and management accounting reporting that are integrated within

organizational processes..........................................................................................................................7

TASK 2..........................................................................................................................................................8

P3 Preparation of income statement by using marginal or absorption costing method............................8

M2.Application of wide range of management accounting techniques and production of appropriate

financial reporting documents...............................................................................................................14

D2. Financial reports which helps in interpreting business operational activities..................................14

TASK 3........................................................................................................................................................14

P4 Planning Tools..................................................................................................................................14

M3 Application to prepare and forecast budget.....................................................................................16

TASK 4........................................................................................................................................................17

P5 Use of management accounting system for responding few of financial problems..........................17

M4 Responding to financial problem, management accounting lead to sustainable success.................19

D3 Evaluation of planning tools for address financial problem.............................................................19

CONCLUSION.............................................................................................................................................19

REFERENCES..............................................................................................................................................21

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1. Management accounting systems......................................................................................................3

P2. Management accounting reporting....................................................................................................5

M1. Advantages of management accounting systems..............................................................................6

D1 Evaluation of accounting systems and management accounting reporting that are integrated within

organizational processes..........................................................................................................................7

TASK 2..........................................................................................................................................................8

P3 Preparation of income statement by using marginal or absorption costing method............................8

M2.Application of wide range of management accounting techniques and production of appropriate

financial reporting documents...............................................................................................................14

D2. Financial reports which helps in interpreting business operational activities..................................14

TASK 3........................................................................................................................................................14

P4 Planning Tools..................................................................................................................................14

M3 Application to prepare and forecast budget.....................................................................................16

TASK 4........................................................................................................................................................17

P5 Use of management accounting system for responding few of financial problems..........................17

M4 Responding to financial problem, management accounting lead to sustainable success.................19

D3 Evaluation of planning tools for address financial problem.............................................................19

CONCLUSION.............................................................................................................................................19

REFERENCES..............................................................................................................................................21

INTRODUCTION

Management accounting involves different processes related to preparing along with

presenting annual reports in this way as to facilitate internal development in planning for the

future, formulating strategies and managing company activities (Bennett and James, 2017). Such

accountability has the purpose of assisting managers when making choices to enhance the

business. Any company does not need to follow management accounting, as its criteria rely on

organizational priorities. To better understand the concept of management accounting selected

Creams Ltd, who is dealing into ice creams, waffles, doughnuts and many other products. The

study addresses management accounting frameworks with their key criteria, accounting

procedures, use of acceptable market analysis methodology to prepare financial statements

utilizing absorption charges, and also marginal costs. This also requires tools for preparation

with benefits and drawbacks, the use of accounting management solutions to react to financial

issues that contribute that sustained performance.

TASK 1

P1. Management accounting systems

Management Accounting: Management accounting is a systematic process that involves

recognizing, defining, documenting, evaluating, assessing and transmitting financial and semi-

financial details to main executives in order to make strategic choices to achieve organizational

objectives. This reporting also deals with systemic considerations, as well as helps financial

professionals in the planning and presentation of essential financial reporting. It is also used by

Creams Ltd's executives when they make quick-term and lengthy-term actions to take through

activities or events without further obstacles.

Management accounting System: The management accounting system definition is a

long run-oriented approach that incorporates numerous processes and has broad range covering

different company divisions. Many of Creams Ltd's company information systems shown are as

pursues:

Inventory Management system: Inventory represents the amount of stock of the

products used at different levels to manufacture a finished brand and make it available for sale.

Such program is concerned with both administration and monitoring of business products. A

Management accounting involves different processes related to preparing along with

presenting annual reports in this way as to facilitate internal development in planning for the

future, formulating strategies and managing company activities (Bennett and James, 2017). Such

accountability has the purpose of assisting managers when making choices to enhance the

business. Any company does not need to follow management accounting, as its criteria rely on

organizational priorities. To better understand the concept of management accounting selected

Creams Ltd, who is dealing into ice creams, waffles, doughnuts and many other products. The

study addresses management accounting frameworks with their key criteria, accounting

procedures, use of acceptable market analysis methodology to prepare financial statements

utilizing absorption charges, and also marginal costs. This also requires tools for preparation

with benefits and drawbacks, the use of accounting management solutions to react to financial

issues that contribute that sustained performance.

TASK 1

P1. Management accounting systems

Management Accounting: Management accounting is a systematic process that involves

recognizing, defining, documenting, evaluating, assessing and transmitting financial and semi-

financial details to main executives in order to make strategic choices to achieve organizational

objectives. This reporting also deals with systemic considerations, as well as helps financial

professionals in the planning and presentation of essential financial reporting. It is also used by

Creams Ltd's executives when they make quick-term and lengthy-term actions to take through

activities or events without further obstacles.

Management accounting System: The management accounting system definition is a

long run-oriented approach that incorporates numerous processes and has broad range covering

different company divisions. Many of Creams Ltd's company information systems shown are as

pursues:

Inventory Management system: Inventory represents the amount of stock of the

products used at different levels to manufacture a finished brand and make it available for sale.

Such program is concerned with both administration and monitoring of business products. A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

detailed database is kept to use such a method, which involves the date and time of the amount of

product brought into the company, and its storage, including the removal of larger quantities for

sale, it is simple to measure and assess the existing properties accessible and the inventory

needed for more activities(Christ, 2014). Within Creams Ltd's framework, administration utilizes

this method to monitor stock at various organizational places in order to obtain reliable

information connected to current storage volume that tends to make choices about additional

stock needed. The main benefit of the inventory management program is to maintain a

comprehensive stock level database in order to avoid overstock-related or stock-related issues at

different processing points. The essential requirement of maintain stock level in appropriate

manner and supply on time.

Cost accounting system: The system that succeeds in estimating the value of different

organizational goods and evaluating factors linked to productivity, assessment of stock and

regulation of costs. Estimating reliable expenses related with goods is very critical for

manufacturing leaders, as successful evaluation contributes to efficient processes. Creams Ltd

executives need such a method to measure the stock cost of the closure stock, the stock of

manufactured goods and the function in the stock of processes. The benefit of this method,

administrators establish appropriate accounting sheets are tracking the expense of raw resources

used when processing final fruit drink items such as sugar amount, berries, sugar, water content,

colors, etc. In order to measure the cost of various sales volumes of organizational goods as to

make finished reports, the cost accounting method is effectively necessary at workspace. The

essential requirement of this system to analysis the cost of every product that manufacturing by

an organisation.

Price optimization system: A statistical model in which production fluctuations are

measured at various price rates is called the method of market optimizations. Administrative

executives use it to monitor crucial-resource costs (Fullerton, Kennedy and Widener, 2014).

Creams Ltd's administrators decide user reply to various price points of ice creams, waffles, and

soft drinks would use such a model. To determining retail prices, it allows supervisors to assess

different flavors in this kind of way that maximizes the profitability. It is essential require to

efficiently distribute commodity prices resulting in the fulfillment of both functional and

corporate priorities.

product brought into the company, and its storage, including the removal of larger quantities for

sale, it is simple to measure and assess the existing properties accessible and the inventory

needed for more activities(Christ, 2014). Within Creams Ltd's framework, administration utilizes

this method to monitor stock at various organizational places in order to obtain reliable

information connected to current storage volume that tends to make choices about additional

stock needed. The main benefit of the inventory management program is to maintain a

comprehensive stock level database in order to avoid overstock-related or stock-related issues at

different processing points. The essential requirement of maintain stock level in appropriate

manner and supply on time.

Cost accounting system: The system that succeeds in estimating the value of different

organizational goods and evaluating factors linked to productivity, assessment of stock and

regulation of costs. Estimating reliable expenses related with goods is very critical for

manufacturing leaders, as successful evaluation contributes to efficient processes. Creams Ltd

executives need such a method to measure the stock cost of the closure stock, the stock of

manufactured goods and the function in the stock of processes. The benefit of this method,

administrators establish appropriate accounting sheets are tracking the expense of raw resources

used when processing final fruit drink items such as sugar amount, berries, sugar, water content,

colors, etc. In order to measure the cost of various sales volumes of organizational goods as to

make finished reports, the cost accounting method is effectively necessary at workspace. The

essential requirement of this system to analysis the cost of every product that manufacturing by

an organisation.

Price optimization system: A statistical model in which production fluctuations are

measured at various price rates is called the method of market optimizations. Administrative

executives use it to monitor crucial-resource costs (Fullerton, Kennedy and Widener, 2014).

Creams Ltd's administrators decide user reply to various price points of ice creams, waffles, and

soft drinks would use such a model. To determining retail prices, it allows supervisors to assess

different flavors in this kind of way that maximizes the profitability. It is essential require to

efficiently distribute commodity prices resulting in the fulfillment of both functional and

corporate priorities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: The aggregation of inventory, payroll and wage costs for a specific

product or job is referred to as a method of labor costs. Such a program is implemented in the

workforce as multiple items are manufactured which are distinct from one another and require

considerable costs in each object. Moreover, it discusses production costs through sub-parts

including direct content, specific manpower, depreciation and therefore with the intention of

calculating real product costs. With respect to Creams Ltd, it is built a different section that is

responsible for controlling expenses including major product expenditures. The benefit of this

system to analysis job cost and essential requirement of this system that to analysis sub

production cost in authentic manner.

Thus, the successful use of any of the above-mentioned accounting systems allows Creams Ltd's

administration to regularly maintain perfect accounts of the events or procedures that occurred at

the workplace. All of this helps to boost the operating performance to growing the firm's

profitability.

P2. Management accounting reporting.

Management Accounting Reporting: Different types of reporting documents are

compiled in a company, all of which have important relevance when supplying details to top

management agencies. Financial reporting documents are written with the aim to assist in

preparation, success assessment and successful policy taking. Both administrators on the

employee compile these documents, since they provide consistent and reliable statistical or

financial records (Hall, 2016). Creams Ltd heads of departments arrange the preceding

accounting reports:

Budget Report: The critical report which aims to measure overall financial results over

the accountability term. They are organized by the executives at organizational and

administrative stage, which allows formulating the company's overall plan. Creams Ltd's

executives evaluate all previous fiscal assets output, and devise potential strategies to achieve

realistic results

Performance Report: As whole and performance documents are designed for the

intention of monitoring and assessing staff and organization results. Such a study offers a

comparison of results in each venture within overall results and dependent boarded output. The

product or job is referred to as a method of labor costs. Such a program is implemented in the

workforce as multiple items are manufactured which are distinct from one another and require

considerable costs in each object. Moreover, it discusses production costs through sub-parts

including direct content, specific manpower, depreciation and therefore with the intention of

calculating real product costs. With respect to Creams Ltd, it is built a different section that is

responsible for controlling expenses including major product expenditures. The benefit of this

system to analysis job cost and essential requirement of this system that to analysis sub

production cost in authentic manner.

Thus, the successful use of any of the above-mentioned accounting systems allows Creams Ltd's

administration to regularly maintain perfect accounts of the events or procedures that occurred at

the workplace. All of this helps to boost the operating performance to growing the firm's

profitability.

P2. Management accounting reporting.

Management Accounting Reporting: Different types of reporting documents are

compiled in a company, all of which have important relevance when supplying details to top

management agencies. Financial reporting documents are written with the aim to assist in

preparation, success assessment and successful policy taking. Both administrators on the

employee compile these documents, since they provide consistent and reliable statistical or

financial records (Hall, 2016). Creams Ltd heads of departments arrange the preceding

accounting reports:

Budget Report: The critical report which aims to measure overall financial results over

the accountability term. They are organized by the executives at organizational and

administrative stage, which allows formulating the company's overall plan. Creams Ltd's

executives evaluate all previous fiscal assets output, and devise potential strategies to achieve

realistic results

Performance Report: As whole and performance documents are designed for the

intention of monitoring and assessing staff and organization results. Such a study offers a

comparison of results in each venture within overall results and dependent boarded output. The

variations determined by analyzing actual outcomes and regular output are evaluated specifically

and are described in these studies. Using all these reports, Creams Ltd's administrators evaluate

efficiencies as well as job performance failures and other operations, and assess real behavior in

order to make choices about the enhancements.

Account receivable report: These are perfectly portioned by companies that rely on

increasing balances and also helping to assess the repayment of questionable reports. It

categorizes the organizations' accounts receivable by the time remaining period associated with

an invoice. In addition, and use such a document, the administration of Creams Ltd determines

the financial situation of clients and produces a document by creating separate categories for the

money received and the money not collected from buyers, that allows to identify the identity of

borrowers by brief glance.

Inventory and manufacturing report: Organizations included in production operations

are planning this form of reporting document to document all operations centered on stock use

and product production so that the specific practices are accurate and successful. It includes

specific details including depreciation cost per unit, consumption of inventories and labor costs.

Creams Ltd's executives equate their current records with previous year as well the study to

assess the need for changes. By reviewing these report administrators may implement ideas for

making stock and service management efficient (Lavia López and Hiebl, 2014).

Therefore, all of the above financial documents are used by administrators of Creams Ltd

to track different costs as well as make changes in the fields they are missing inside which will

contribute in more effective performance of business units.

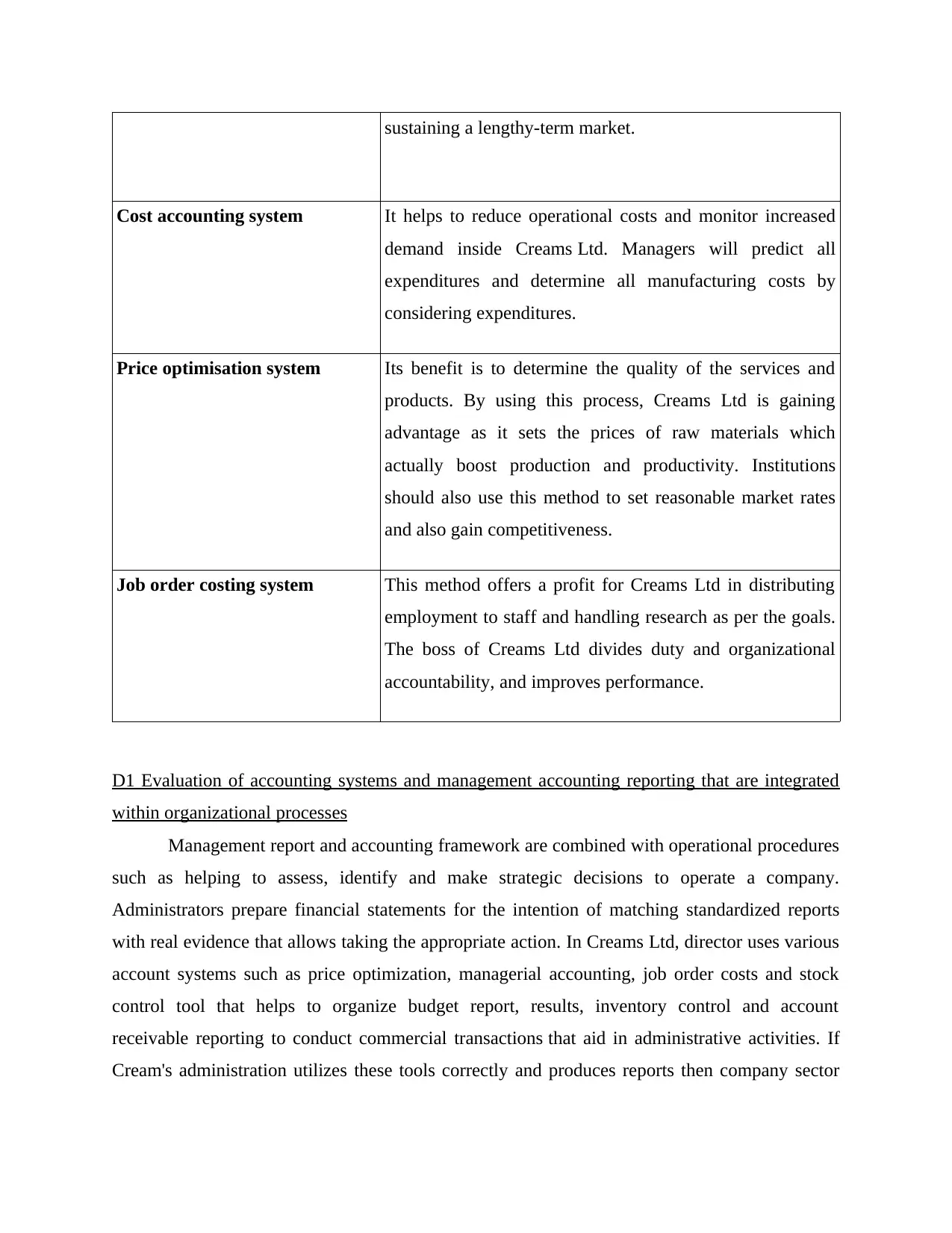

M1. Advantages of management accounting systems

Accounting system Advantages

Inventory management system This system is useful for maintaining stock information and

handling them correctly. With the aid of this device

Creams Ltd will help the environment and increase output.

In addition, using that same program organization can

position last ordering to raw resources that allows

and are described in these studies. Using all these reports, Creams Ltd's administrators evaluate

efficiencies as well as job performance failures and other operations, and assess real behavior in

order to make choices about the enhancements.

Account receivable report: These are perfectly portioned by companies that rely on

increasing balances and also helping to assess the repayment of questionable reports. It

categorizes the organizations' accounts receivable by the time remaining period associated with

an invoice. In addition, and use such a document, the administration of Creams Ltd determines

the financial situation of clients and produces a document by creating separate categories for the

money received and the money not collected from buyers, that allows to identify the identity of

borrowers by brief glance.

Inventory and manufacturing report: Organizations included in production operations

are planning this form of reporting document to document all operations centered on stock use

and product production so that the specific practices are accurate and successful. It includes

specific details including depreciation cost per unit, consumption of inventories and labor costs.

Creams Ltd's executives equate their current records with previous year as well the study to

assess the need for changes. By reviewing these report administrators may implement ideas for

making stock and service management efficient (Lavia López and Hiebl, 2014).

Therefore, all of the above financial documents are used by administrators of Creams Ltd

to track different costs as well as make changes in the fields they are missing inside which will

contribute in more effective performance of business units.

M1. Advantages of management accounting systems

Accounting system Advantages

Inventory management system This system is useful for maintaining stock information and

handling them correctly. With the aid of this device

Creams Ltd will help the environment and increase output.

In addition, using that same program organization can

position last ordering to raw resources that allows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sustaining a lengthy-term market.

Cost accounting system It helps to reduce operational costs and monitor increased

demand inside Creams Ltd. Managers will predict all

expenditures and determine all manufacturing costs by

considering expenditures.

Price optimisation system Its benefit is to determine the quality of the services and

products. By using this process, Creams Ltd is gaining

advantage as it sets the prices of raw materials which

actually boost production and productivity. Institutions

should also use this method to set reasonable market rates

and also gain competitiveness.

Job order costing system This method offers a profit for Creams Ltd in distributing

employment to staff and handling research as per the goals.

The boss of Creams Ltd divides duty and organizational

accountability, and improves performance.

D1 Evaluation of accounting systems and management accounting reporting that are integrated

within organizational processes

Management report and accounting framework are combined with operational procedures

such as helping to assess, identify and make strategic decisions to operate a company.

Administrators prepare financial statements for the intention of matching standardized reports

with real evidence that allows taking the appropriate action. In Creams Ltd, director uses various

account systems such as price optimization, managerial accounting, job order costs and stock

control tool that helps to organize budget report, results, inventory control and account

receivable reporting to conduct commercial transactions that aid in administrative activities. If

Cream's administration utilizes these tools correctly and produces reports then company sector

Cost accounting system It helps to reduce operational costs and monitor increased

demand inside Creams Ltd. Managers will predict all

expenditures and determine all manufacturing costs by

considering expenditures.

Price optimisation system Its benefit is to determine the quality of the services and

products. By using this process, Creams Ltd is gaining

advantage as it sets the prices of raw materials which

actually boost production and productivity. Institutions

should also use this method to set reasonable market rates

and also gain competitiveness.

Job order costing system This method offers a profit for Creams Ltd in distributing

employment to staff and handling research as per the goals.

The boss of Creams Ltd divides duty and organizational

accountability, and improves performance.

D1 Evaluation of accounting systems and management accounting reporting that are integrated

within organizational processes

Management report and accounting framework are combined with operational procedures

such as helping to assess, identify and make strategic decisions to operate a company.

Administrators prepare financial statements for the intention of matching standardized reports

with real evidence that allows taking the appropriate action. In Creams Ltd, director uses various

account systems such as price optimization, managerial accounting, job order costs and stock

control tool that helps to organize budget report, results, inventory control and account

receivable reporting to conduct commercial transactions that aid in administrative activities. If

Cream's administration utilizes these tools correctly and produces reports then company sector

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

priorities and targets can be achieved. As a consequence, high efficiency and competitiveness are

considered systems of organization (Maas, Schaltegger and Crutzen, 2016).

TASK 2

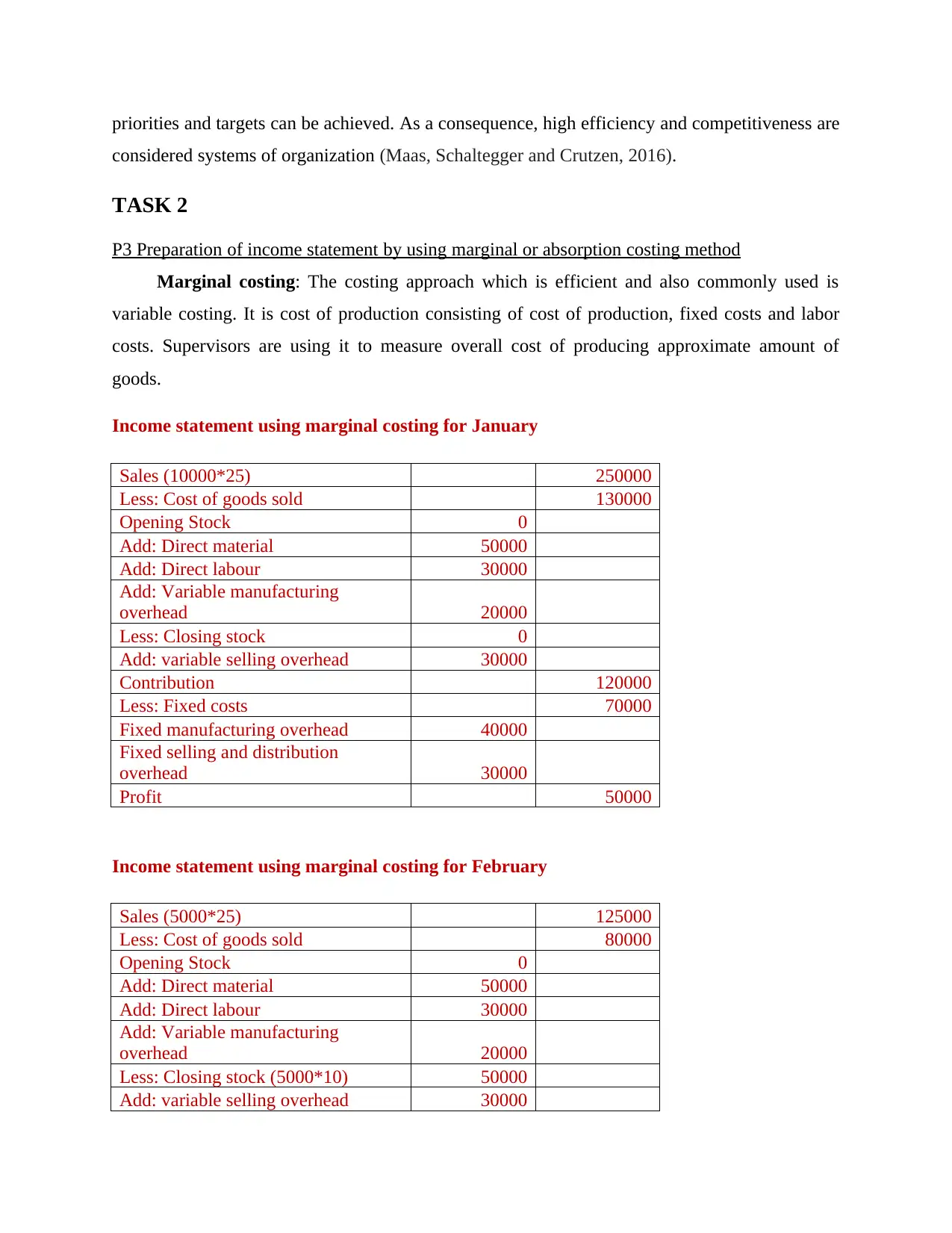

P3 Preparation of income statement by using marginal or absorption costing method

Marginal costing: The costing approach which is efficient and also commonly used is

variable costing. It is cost of production consisting of cost of production, fixed costs and labor

costs. Supervisors are using it to measure overall cost of producing approximate amount of

goods.

Income statement using marginal costing for January

Sales (10000*25) 250000

Less: Cost of goods sold 130000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing

overhead 20000

Less: Closing stock 0

Add: variable selling overhead 30000

Contribution 120000

Less: Fixed costs 70000

Fixed manufacturing overhead 40000

Fixed selling and distribution

overhead 30000

Profit 50000

Income statement using marginal costing for February

Sales (5000*25) 125000

Less: Cost of goods sold 80000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing

overhead 20000

Less: Closing stock (5000*10) 50000

Add: variable selling overhead 30000

considered systems of organization (Maas, Schaltegger and Crutzen, 2016).

TASK 2

P3 Preparation of income statement by using marginal or absorption costing method

Marginal costing: The costing approach which is efficient and also commonly used is

variable costing. It is cost of production consisting of cost of production, fixed costs and labor

costs. Supervisors are using it to measure overall cost of producing approximate amount of

goods.

Income statement using marginal costing for January

Sales (10000*25) 250000

Less: Cost of goods sold 130000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing

overhead 20000

Less: Closing stock 0

Add: variable selling overhead 30000

Contribution 120000

Less: Fixed costs 70000

Fixed manufacturing overhead 40000

Fixed selling and distribution

overhead 30000

Profit 50000

Income statement using marginal costing for February

Sales (5000*25) 125000

Less: Cost of goods sold 80000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing

overhead 20000

Less: Closing stock (5000*10) 50000

Add: variable selling overhead 30000

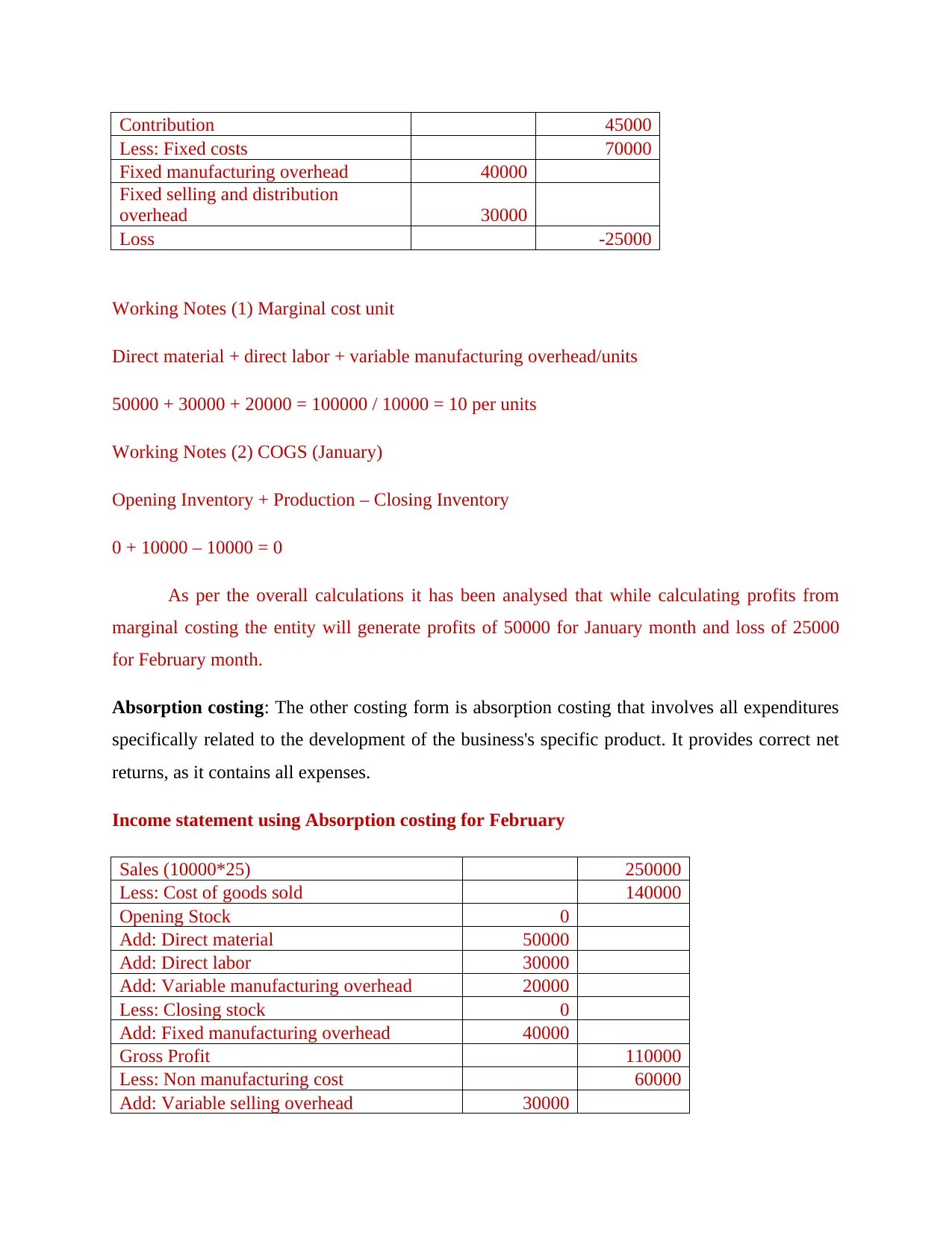

Contribution 45000

Less: Fixed costs 70000

Fixed manufacturing overhead 40000

Fixed selling and distribution

overhead 30000

Loss -25000

Working Notes (1) Marginal cost unit

Direct material + direct labor + variable manufacturing overhead/units

50000 + 30000 + 20000 = 100000 / 10000 = 10 per units

Working Notes (2) COGS (January)

Opening Inventory + Production – Closing Inventory

0 + 10000 – 10000 = 0

As per the overall calculations it has been analysed that while calculating profits from

marginal costing the entity will generate profits of 50000 for January month and loss of 25000

for February month.

Absorption costing: The other costing form is absorption costing that involves all expenditures

specifically related to the development of the business's specific product. It provides correct net

returns, as it contains all expenses.

Income statement using Absorption costing for February

Sales (10000*25) 250000

Less: Cost of goods sold 140000

Opening Stock 0

Add: Direct material 50000

Add: Direct labor 30000

Add: Variable manufacturing overhead 20000

Less: Closing stock 0

Add: Fixed manufacturing overhead 40000

Gross Profit 110000

Less: Non manufacturing cost 60000

Add: Variable selling overhead 30000

Less: Fixed costs 70000

Fixed manufacturing overhead 40000

Fixed selling and distribution

overhead 30000

Loss -25000

Working Notes (1) Marginal cost unit

Direct material + direct labor + variable manufacturing overhead/units

50000 + 30000 + 20000 = 100000 / 10000 = 10 per units

Working Notes (2) COGS (January)

Opening Inventory + Production – Closing Inventory

0 + 10000 – 10000 = 0

As per the overall calculations it has been analysed that while calculating profits from

marginal costing the entity will generate profits of 50000 for January month and loss of 25000

for February month.

Absorption costing: The other costing form is absorption costing that involves all expenditures

specifically related to the development of the business's specific product. It provides correct net

returns, as it contains all expenses.

Income statement using Absorption costing for February

Sales (10000*25) 250000

Less: Cost of goods sold 140000

Opening Stock 0

Add: Direct material 50000

Add: Direct labor 30000

Add: Variable manufacturing overhead 20000

Less: Closing stock 0

Add: Fixed manufacturing overhead 40000

Gross Profit 110000

Less: Non manufacturing cost 60000

Add: Variable selling overhead 30000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

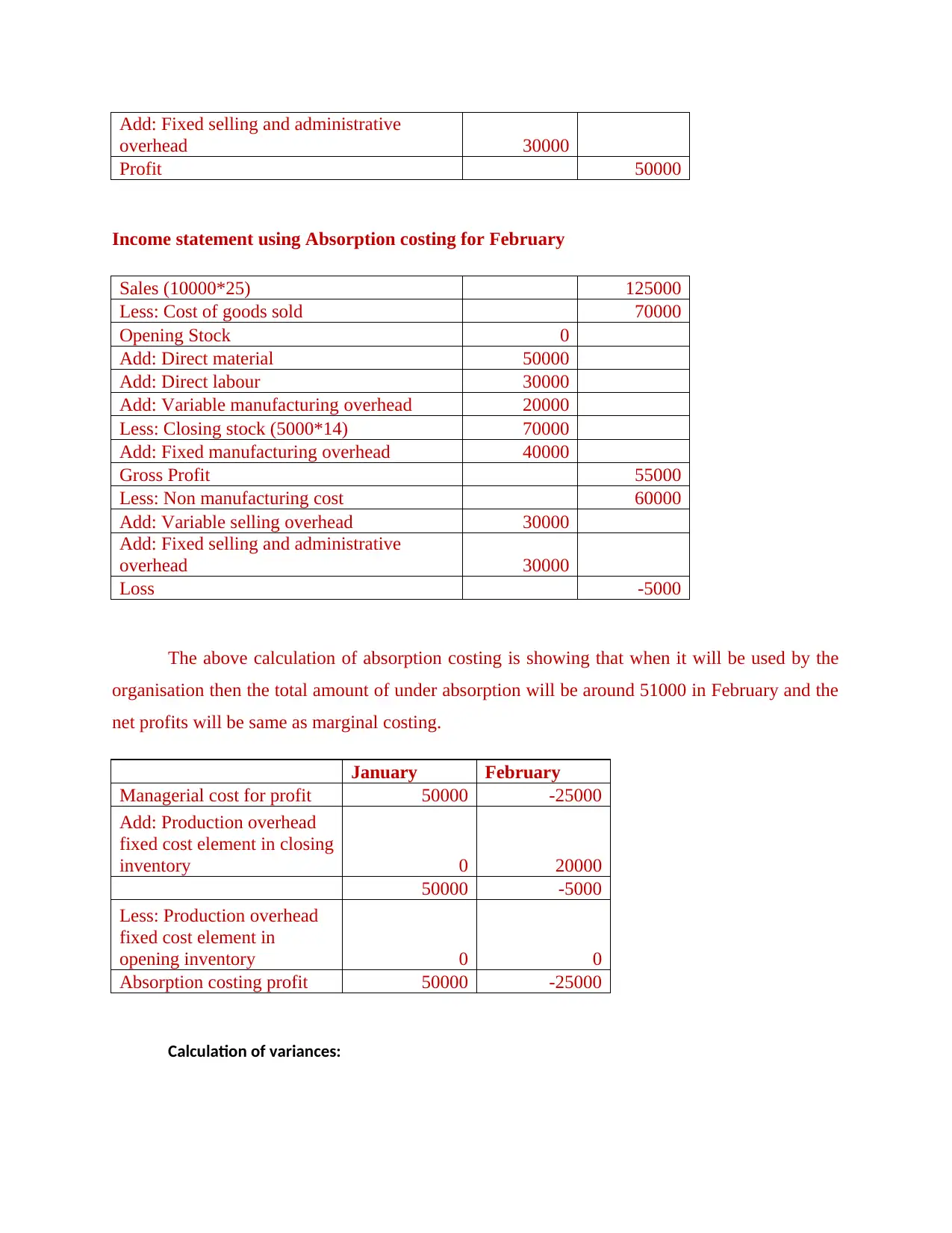

Add: Fixed selling and administrative

overhead 30000

Profit 50000

Income statement using Absorption costing for February

Sales (10000*25) 125000

Less: Cost of goods sold 70000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing overhead 20000

Less: Closing stock (5000*14) 70000

Add: Fixed manufacturing overhead 40000

Gross Profit 55000

Less: Non manufacturing cost 60000

Add: Variable selling overhead 30000

Add: Fixed selling and administrative

overhead 30000

Loss -5000

The above calculation of absorption costing is showing that when it will be used by the

organisation then the total amount of under absorption will be around 51000 in February and the

net profits will be same as marginal costing.

January February

Managerial cost for profit 50000 -25000

Add: Production overhead

fixed cost element in closing

inventory 0 20000

50000 -5000

Less: Production overhead

fixed cost element in

opening inventory 0 0

Absorption costing profit 50000 -25000

Calculation of variances:

overhead 30000

Profit 50000

Income statement using Absorption costing for February

Sales (10000*25) 125000

Less: Cost of goods sold 70000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing overhead 20000

Less: Closing stock (5000*14) 70000

Add: Fixed manufacturing overhead 40000

Gross Profit 55000

Less: Non manufacturing cost 60000

Add: Variable selling overhead 30000

Add: Fixed selling and administrative

overhead 30000

Loss -5000

The above calculation of absorption costing is showing that when it will be used by the

organisation then the total amount of under absorption will be around 51000 in February and the

net profits will be same as marginal costing.

January February

Managerial cost for profit 50000 -25000

Add: Production overhead

fixed cost element in closing

inventory 0 20000

50000 -5000

Less: Production overhead

fixed cost element in

opening inventory 0 0

Absorption costing profit 50000 -25000

Calculation of variances:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

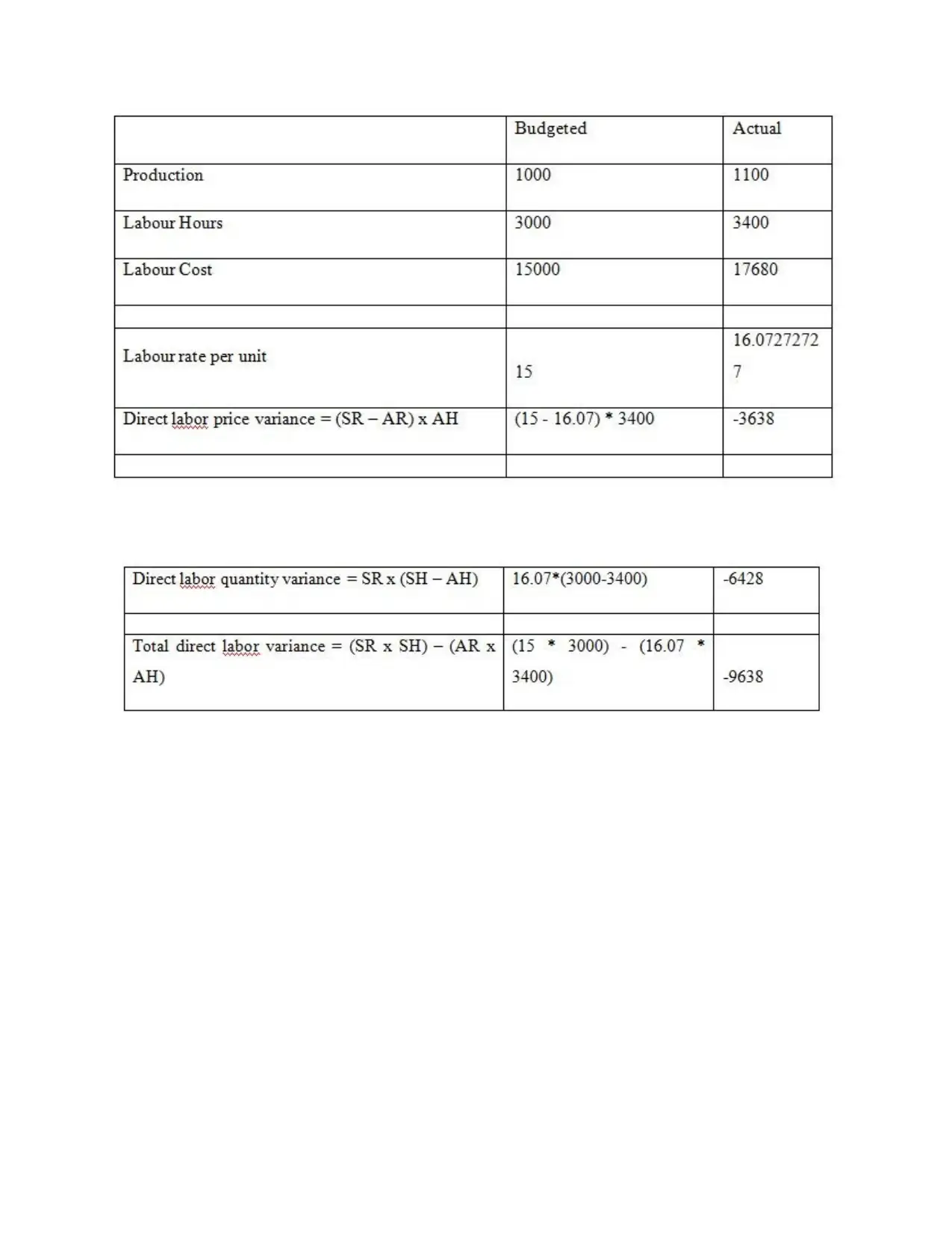

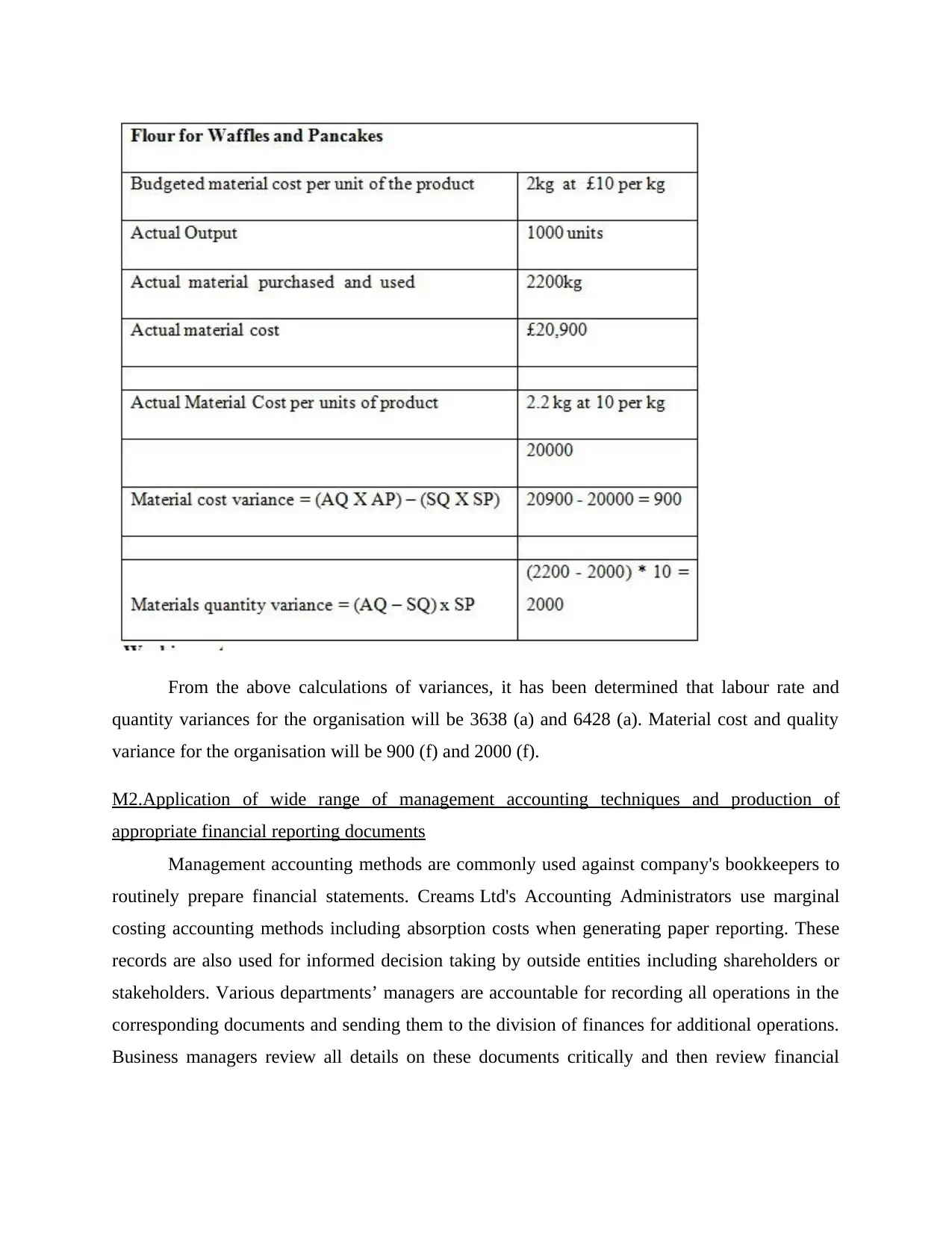

From the above calculations of variances, it has been determined that labour rate and

quantity variances for the organisation will be 3638 (a) and 6428 (a). Material cost and quality

variance for the organisation will be 900 (f) and 2000 (f).

M2.Application of wide range of management accounting techniques and production of

appropriate financial reporting documents

Management accounting methods are commonly used against company's bookkeepers to

routinely prepare financial statements. Creams Ltd's Accounting Administrators use marginal

costing accounting methods including absorption costs when generating paper reporting. These

records are also used for informed decision taking by outside entities including shareholders or

stakeholders. Various departments’ managers are accountable for recording all operations in the

corresponding documents and sending them to the division of finances for additional operations.

Business managers review all details on these documents critically and then review financial

quantity variances for the organisation will be 3638 (a) and 6428 (a). Material cost and quality

variance for the organisation will be 900 (f) and 2000 (f).

M2.Application of wide range of management accounting techniques and production of

appropriate financial reporting documents

Management accounting methods are commonly used against company's bookkeepers to

routinely prepare financial statements. Creams Ltd's Accounting Administrators use marginal

costing accounting methods including absorption costs when generating paper reporting. These

records are also used for informed decision taking by outside entities including shareholders or

stakeholders. Various departments’ managers are accountable for recording all operations in the

corresponding documents and sending them to the division of finances for additional operations.

Business managers review all details on these documents critically and then review financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.