Management Accounting: Systems and Reporting Analysis

VerifiedAdded on 2023/02/01

|16

|3964

|96

Report

AI Summary

This report comprehensively examines management accounting, covering various systems and their applications. It begins by defining management accounting and its significance in internal reporting, exploring different types of systems such as inventory management, cost accounting, and job costing. The report then details various management accounting reporting methods, including budget reports and cost reports, and highlights the benefits of these systems. A significant portion of the report is dedicated to a comparative analysis of marginal costing and absorption costing, including the preparation of income statements under both methods. Furthermore, the report delves into budgetary control, outlining the advantages and disadvantages of planning tools like flexible and fixed budgets, and cash budgets. Finally, it addresses how different management accounting systems can be used to resolve financial problems, providing a holistic view of the subject.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1.......................................................................................................................................................3

Management accounting and the essential requirement of different types of management accounting

systems....................................................................................................................................................3

Different method used for management accounting reporting.................................................................4

Benefits of management accounting systems..........................................................................................5

Integration of management accounting system and management accounting reporting...........................5

TASK 2.......................................................................................................................................................6

Income statement as per marginal costing and absorption costing...........................................................6

TASK 3.......................................................................................................................................................9

Explaining the advantages and disadvantages of different planning tools of budgetary.........................9

control.....................................................................................................................................................9

Analyzing the usefulness and application of different planning tools...................................................11

TASK 4.....................................................................................................................................................12

Different types of management accounting systems available for resolving the financial....................12

problems...............................................................................................................................................12

CONCLUSION.........................................................................................................................................14

REFERENCES..........................................................................................................................................15

TASK 1.......................................................................................................................................................3

Management accounting and the essential requirement of different types of management accounting

systems....................................................................................................................................................3

Different method used for management accounting reporting.................................................................4

Benefits of management accounting systems..........................................................................................5

Integration of management accounting system and management accounting reporting...........................5

TASK 2.......................................................................................................................................................6

Income statement as per marginal costing and absorption costing...........................................................6

TASK 3.......................................................................................................................................................9

Explaining the advantages and disadvantages of different planning tools of budgetary.........................9

control.....................................................................................................................................................9

Analyzing the usefulness and application of different planning tools...................................................11

TASK 4.....................................................................................................................................................12

Different types of management accounting systems available for resolving the financial....................12

problems...............................................................................................................................................12

CONCLUSION.........................................................................................................................................14

REFERENCES..........................................................................................................................................15

INTROUCTION

Management accounting is the process of analyzing the cost of business and assist in

preparing internal financial report. This assignment will provide understanding about the

different types of management accounting systems. Moreover, it consists of different methods

used for management accounting reporting. It also evaluates the benefits of management

accounting systems. It also includes the different types of planning tools used for budgetary

control. Also, it will assist in providing information regarding the management accounting

systems which helps in responding to the financial problems.

TASK 1

Management accounting and the essential requirement of different types of management

accounting systems

Management accounting assists in preparing the internal report on the basis of which the

organization is able to make the decision for improving the future performance and profitability.

It assist in allocating the cost and identifying the ways in order to reduce the cost for increasing

the profitability of organization (Kaplan and Atkinson, 2015). The management accounting is

the way the organizations able to manage the internal accounting of the firm and helps in

reducing the cost in order to achieve the goals and objectives of organization. With the help of

identifying the cost of the process the management accountant is able to provide the organization

the reports on the basis of which the firm can take decision which will be profitable for the

business in future. There are different types of management accounting systems which are as

follows :

Inventory management system: It is the management accounting system

through which the organization is able to manage the level of inventory which

will helps in reducing the wastage and also the cost of the organization will be

reduced. It helps in identifying the level of inventory which is required in the

organization and can assist in providing the firm with the benefits and cost of

maintenance of the inventory is also minimized.

Management accounting is the process of analyzing the cost of business and assist in

preparing internal financial report. This assignment will provide understanding about the

different types of management accounting systems. Moreover, it consists of different methods

used for management accounting reporting. It also evaluates the benefits of management

accounting systems. It also includes the different types of planning tools used for budgetary

control. Also, it will assist in providing information regarding the management accounting

systems which helps in responding to the financial problems.

TASK 1

Management accounting and the essential requirement of different types of management

accounting systems

Management accounting assists in preparing the internal report on the basis of which the

organization is able to make the decision for improving the future performance and profitability.

It assist in allocating the cost and identifying the ways in order to reduce the cost for increasing

the profitability of organization (Kaplan and Atkinson, 2015). The management accounting is

the way the organizations able to manage the internal accounting of the firm and helps in

reducing the cost in order to achieve the goals and objectives of organization. With the help of

identifying the cost of the process the management accountant is able to provide the organization

the reports on the basis of which the firm can take decision which will be profitable for the

business in future. There are different types of management accounting systems which are as

follows :

Inventory management system: It is the management accounting system

through which the organization is able to manage the level of inventory which

will helps in reducing the wastage and also the cost of the organization will be

reduced. It helps in identifying the level of inventory which is required in the

organization and can assist in providing the firm with the benefits and cost of

maintenance of the inventory is also minimized.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system: It is the system used in the organization in order to

estimate the cost of their product in order to determine the level of profitability an

control the cost for the future which will help in increasing the profit margin

(Quattrone, 2016). It helps in controlling the cost by allocating the cost in the

effective and efficient manner.

Job costing system: It is the process of allocating the cost to the specific job in

order to identify the profit associated with that job. It will assist in identifying the

cost of every job and the information regarding them.

Different method used for management accounting reporting

Management accounting reporting assist in identifying the performance and profitability

of the firm on the basis of which he organization is able to make decision for the future. With the

help of this report the firm is able to make forecast for the future and can determine the strategies

which are required to be formulated in the organization in order to improve the profitability and

performance in future. The following are the different reports which are being prepared by the

management accountant.

Budget reports : This are the reports which are being prepared by the management

accountants in order to make forecast for the future on the basis of which they are able to

determine the future performance and profitability of the firm and can also take the

decision for improving the performance and profitability. It consist of case budget report,

operating budget report, sales budget reports etc.

Account receivable aging report: It is the reports which is prepared by management

accountant in order to know the customers that have taken credit for the amount payable.

It also assist company in taking the decision regarding limiting the credit limit in order to

reduce the bad debts which affect the credibility of the firm and also the firm profitability

is affected to a great extent (Otley, 2016). It helps in tracking the customers and the

balance which not payable by them. This report assist the firm in making the effective

decision for improving the credibility of the firm and receiving the payment by customers

on time in order to reduce the bad debts.

Cost report : The cost report assist in allocation of the cost to the different products

manufactured by the organization. With the help of cost report the firm is able to identify

estimate the cost of their product in order to determine the level of profitability an

control the cost for the future which will help in increasing the profit margin

(Quattrone, 2016). It helps in controlling the cost by allocating the cost in the

effective and efficient manner.

Job costing system: It is the process of allocating the cost to the specific job in

order to identify the profit associated with that job. It will assist in identifying the

cost of every job and the information regarding them.

Different method used for management accounting reporting

Management accounting reporting assist in identifying the performance and profitability

of the firm on the basis of which he organization is able to make decision for the future. With the

help of this report the firm is able to make forecast for the future and can determine the strategies

which are required to be formulated in the organization in order to improve the profitability and

performance in future. The following are the different reports which are being prepared by the

management accountant.

Budget reports : This are the reports which are being prepared by the management

accountants in order to make forecast for the future on the basis of which they are able to

determine the future performance and profitability of the firm and can also take the

decision for improving the performance and profitability. It consist of case budget report,

operating budget report, sales budget reports etc.

Account receivable aging report: It is the reports which is prepared by management

accountant in order to know the customers that have taken credit for the amount payable.

It also assist company in taking the decision regarding limiting the credit limit in order to

reduce the bad debts which affect the credibility of the firm and also the firm profitability

is affected to a great extent (Otley, 2016). It helps in tracking the customers and the

balance which not payable by them. This report assist the firm in making the effective

decision for improving the credibility of the firm and receiving the payment by customers

on time in order to reduce the bad debts.

Cost report : The cost report assist in allocation of the cost to the different products

manufactured by the organization. With the help of cost report the firm is able to identify

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the cost of different product on the basis of which they are able to minimize the expenses

and identifying the selling price of the product. The cost report helps in making the

effective decision for improving the performance and profitability of the organization.

Benefits of management accounting systems

Management accounting system assist in improving the internal system of the firm. The

firm through the use of management accounting system helps in making the effective decision

for the firm growth and success. The following are the benefits of the different management

account ting systems :

Benefits of inventory management system

It helps in managing the flow of inventory in the organization. With the help of inventory

management system the organization is able to make the inventory

It assist in reducing the cost of maintaining inventory for the disposal an also assist in

increasing sales and profit.

It is also beneficial because it helps in achieving the efficiency and productivity in

operations.

Benefits of cost accounting system

It helps in estimating and allocation of cost for the products and services offered by the

firm.

With the help of cost accounting system the organization is able to reduce the cost of the

firm which will help in increasing the profitability and performance of the firm.

It helps in improving the efficiency and measurement in the organization (Renz, 2016).

Integration of management accounting system and management accounting reporting

Management accounting systems and management accounting reporting are integrated

because f the firm follows the management accounting system than the firm is able to prepare the

reports which can be helpful in making the effective decision for improving the performance

and profitability of the firm (Maas, Schaltegger and Crutzen, 2016). Management accounting

system helps in preparing the management accounting reports which assist the firm in order to

prepare the reports n the basis of which the organization will make the effective decision for the

and identifying the selling price of the product. The cost report helps in making the

effective decision for improving the performance and profitability of the organization.

Benefits of management accounting systems

Management accounting system assist in improving the internal system of the firm. The

firm through the use of management accounting system helps in making the effective decision

for the firm growth and success. The following are the benefits of the different management

account ting systems :

Benefits of inventory management system

It helps in managing the flow of inventory in the organization. With the help of inventory

management system the organization is able to make the inventory

It assist in reducing the cost of maintaining inventory for the disposal an also assist in

increasing sales and profit.

It is also beneficial because it helps in achieving the efficiency and productivity in

operations.

Benefits of cost accounting system

It helps in estimating and allocation of cost for the products and services offered by the

firm.

With the help of cost accounting system the organization is able to reduce the cost of the

firm which will help in increasing the profitability and performance of the firm.

It helps in improving the efficiency and measurement in the organization (Renz, 2016).

Integration of management accounting system and management accounting reporting

Management accounting systems and management accounting reporting are integrated

because f the firm follows the management accounting system than the firm is able to prepare the

reports which can be helpful in making the effective decision for improving the performance

and profitability of the firm (Maas, Schaltegger and Crutzen, 2016). Management accounting

system helps in preparing the management accounting reports which assist the firm in order to

prepare the reports n the basis of which the organization will make the effective decision for the

future. The cost accounting system assist in preparing the cost accounting reports on the basis of

which the organization will be able to make the decision regarding minimizing the cost in order

to increase the profitability. Moreover, the job costing system helps in preparing the job costing

report which assist in identifying the profitability of business regarding the specific job.

TASK 2

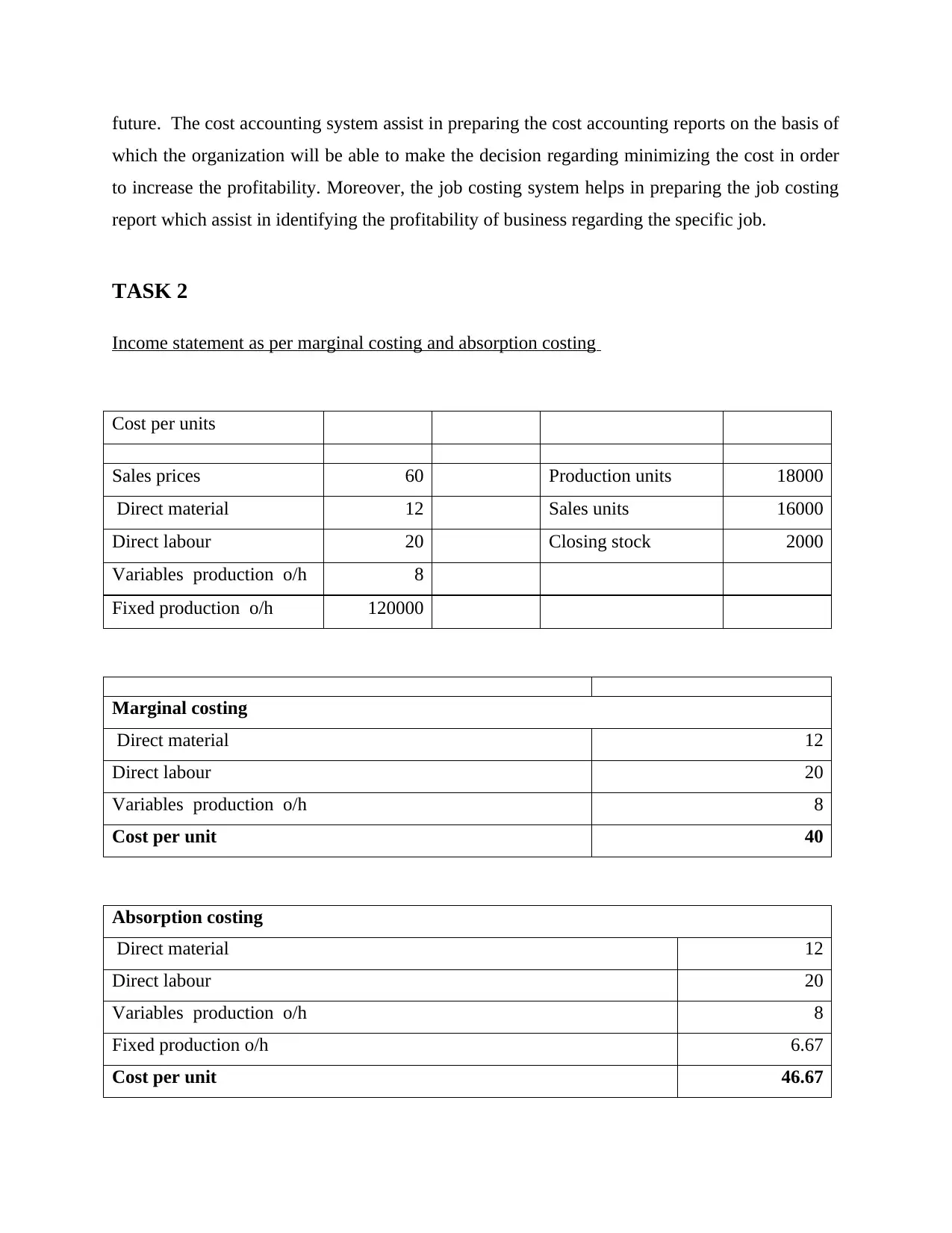

Income statement as per marginal costing and absorption costing

Cost per units

Sales prices 60 Production units 18000

Direct material 12 Sales units 16000

Direct labour 20 Closing stock 2000

Variables production o/h 8

Fixed production o/h 120000

Marginal costing

Direct material 12

Direct labour 20

Variables production o/h 8

Cost per unit 40

Absorption costing

Direct material 12

Direct labour 20

Variables production o/h 8

Fixed production o/h 6.67

Cost per unit 46.67

which the organization will be able to make the decision regarding minimizing the cost in order

to increase the profitability. Moreover, the job costing system helps in preparing the job costing

report which assist in identifying the profitability of business regarding the specific job.

TASK 2

Income statement as per marginal costing and absorption costing

Cost per units

Sales prices 60 Production units 18000

Direct material 12 Sales units 16000

Direct labour 20 Closing stock 2000

Variables production o/h 8

Fixed production o/h 120000

Marginal costing

Direct material 12

Direct labour 20

Variables production o/h 8

Cost per unit 40

Absorption costing

Direct material 12

Direct labour 20

Variables production o/h 8

Fixed production o/h 6.67

Cost per unit 46.67

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

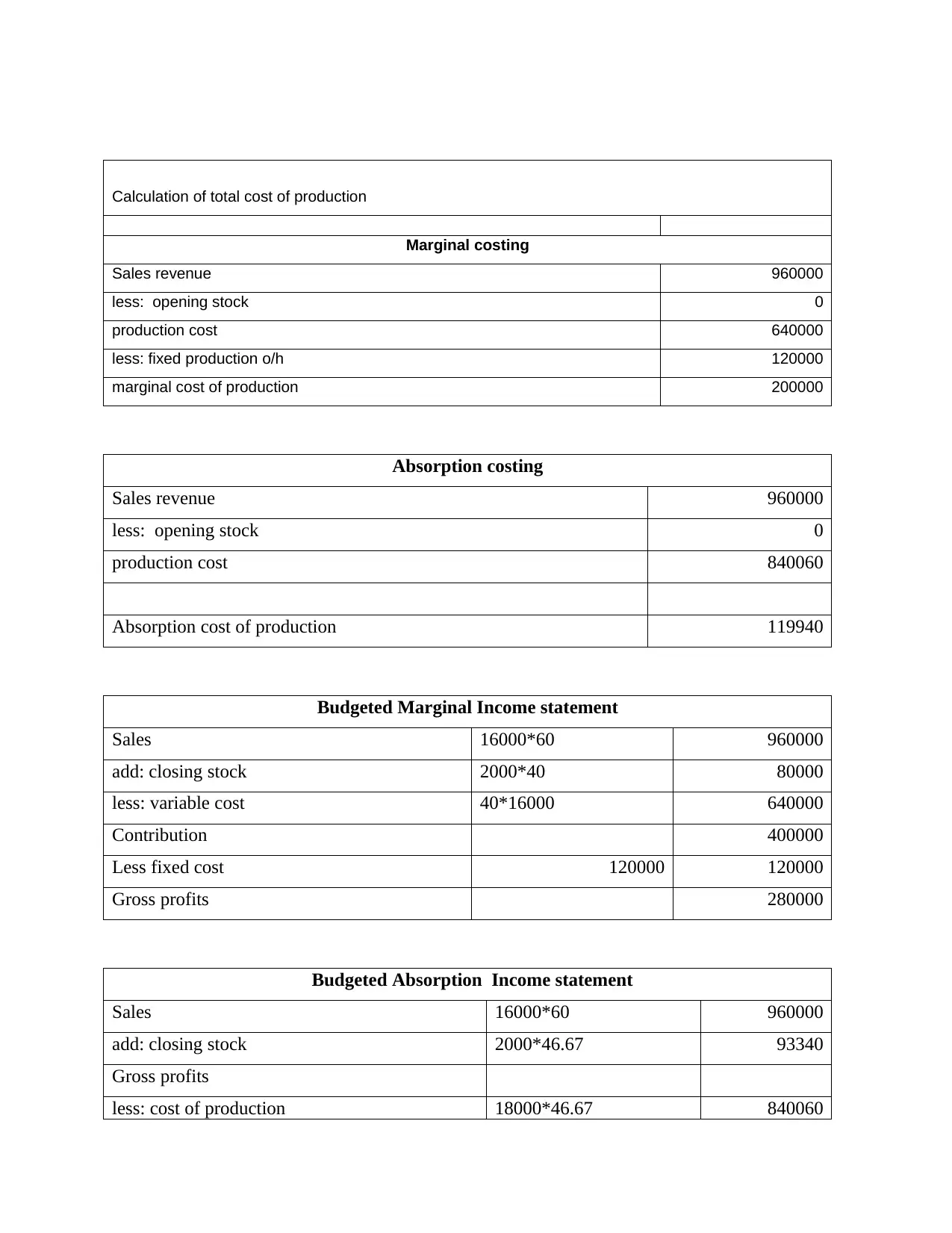

Calculation of total cost of production

Marginal costing

Sales revenue 960000

less: opening stock 0

production cost 640000

less: fixed production o/h 120000

marginal cost of production 200000

Absorption costing

Sales revenue 960000

less: opening stock 0

production cost 840060

Absorption cost of production 119940

Budgeted Marginal Income statement

Sales 16000*60 960000

add: closing stock 2000*40 80000

less: variable cost 40*16000 640000

Contribution 400000

Less fixed cost 120000 120000

Gross profits 280000

Budgeted Absorption Income statement

Sales 16000*60 960000

add: closing stock 2000*46.67 93340

Gross profits

less: cost of production 18000*46.67 840060

Marginal costing

Sales revenue 960000

less: opening stock 0

production cost 640000

less: fixed production o/h 120000

marginal cost of production 200000

Absorption costing

Sales revenue 960000

less: opening stock 0

production cost 840060

Absorption cost of production 119940

Budgeted Marginal Income statement

Sales 16000*60 960000

add: closing stock 2000*40 80000

less: variable cost 40*16000 640000

Contribution 400000

Less fixed cost 120000 120000

Gross profits 280000

Budgeted Absorption Income statement

Sales 16000*60 960000

add: closing stock 2000*46.67 93340

Gross profits

less: cost of production 18000*46.67 840060

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

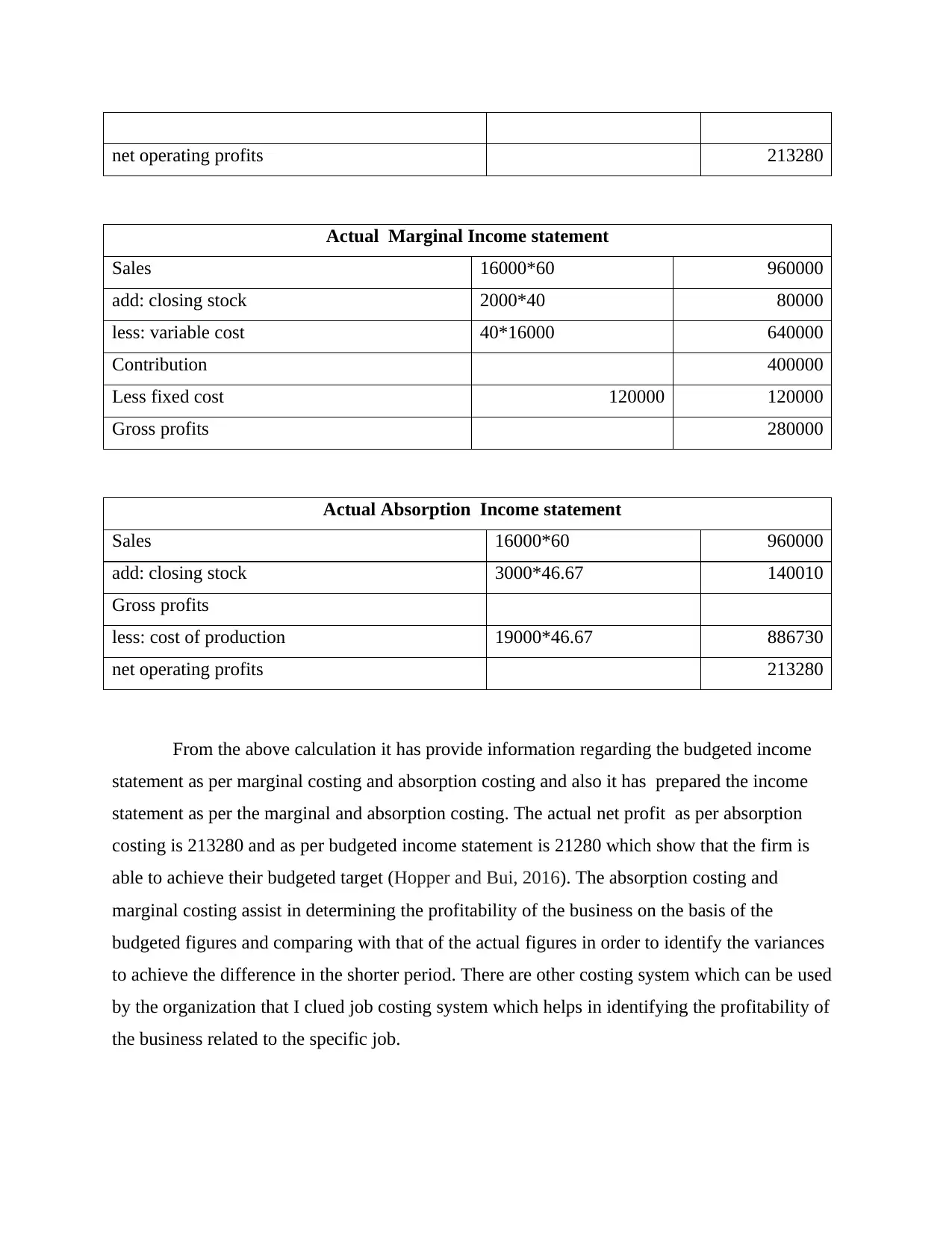

net operating profits 213280

Actual Marginal Income statement

Sales 16000*60 960000

add: closing stock 2000*40 80000

less: variable cost 40*16000 640000

Contribution 400000

Less fixed cost 120000 120000

Gross profits 280000

Actual Absorption Income statement

Sales 16000*60 960000

add: closing stock 3000*46.67 140010

Gross profits

less: cost of production 19000*46.67 886730

net operating profits 213280

From the above calculation it has provide information regarding the budgeted income

statement as per marginal costing and absorption costing and also it has prepared the income

statement as per the marginal and absorption costing. The actual net profit as per absorption

costing is 213280 and as per budgeted income statement is 21280 which show that the firm is

able to achieve their budgeted target (Hopper and Bui, 2016). The absorption costing and

marginal costing assist in determining the profitability of the business on the basis of the

budgeted figures and comparing with that of the actual figures in order to identify the variances

to achieve the difference in the shorter period. There are other costing system which can be used

by the organization that I clued job costing system which helps in identifying the profitability of

the business related to the specific job.

Actual Marginal Income statement

Sales 16000*60 960000

add: closing stock 2000*40 80000

less: variable cost 40*16000 640000

Contribution 400000

Less fixed cost 120000 120000

Gross profits 280000

Actual Absorption Income statement

Sales 16000*60 960000

add: closing stock 3000*46.67 140010

Gross profits

less: cost of production 19000*46.67 886730

net operating profits 213280

From the above calculation it has provide information regarding the budgeted income

statement as per marginal costing and absorption costing and also it has prepared the income

statement as per the marginal and absorption costing. The actual net profit as per absorption

costing is 213280 and as per budgeted income statement is 21280 which show that the firm is

able to achieve their budgeted target (Hopper and Bui, 2016). The absorption costing and

marginal costing assist in determining the profitability of the business on the basis of the

budgeted figures and comparing with that of the actual figures in order to identify the variances

to achieve the difference in the shorter period. There are other costing system which can be used

by the organization that I clued job costing system which helps in identifying the profitability of

the business related to the specific job.

TASK 3

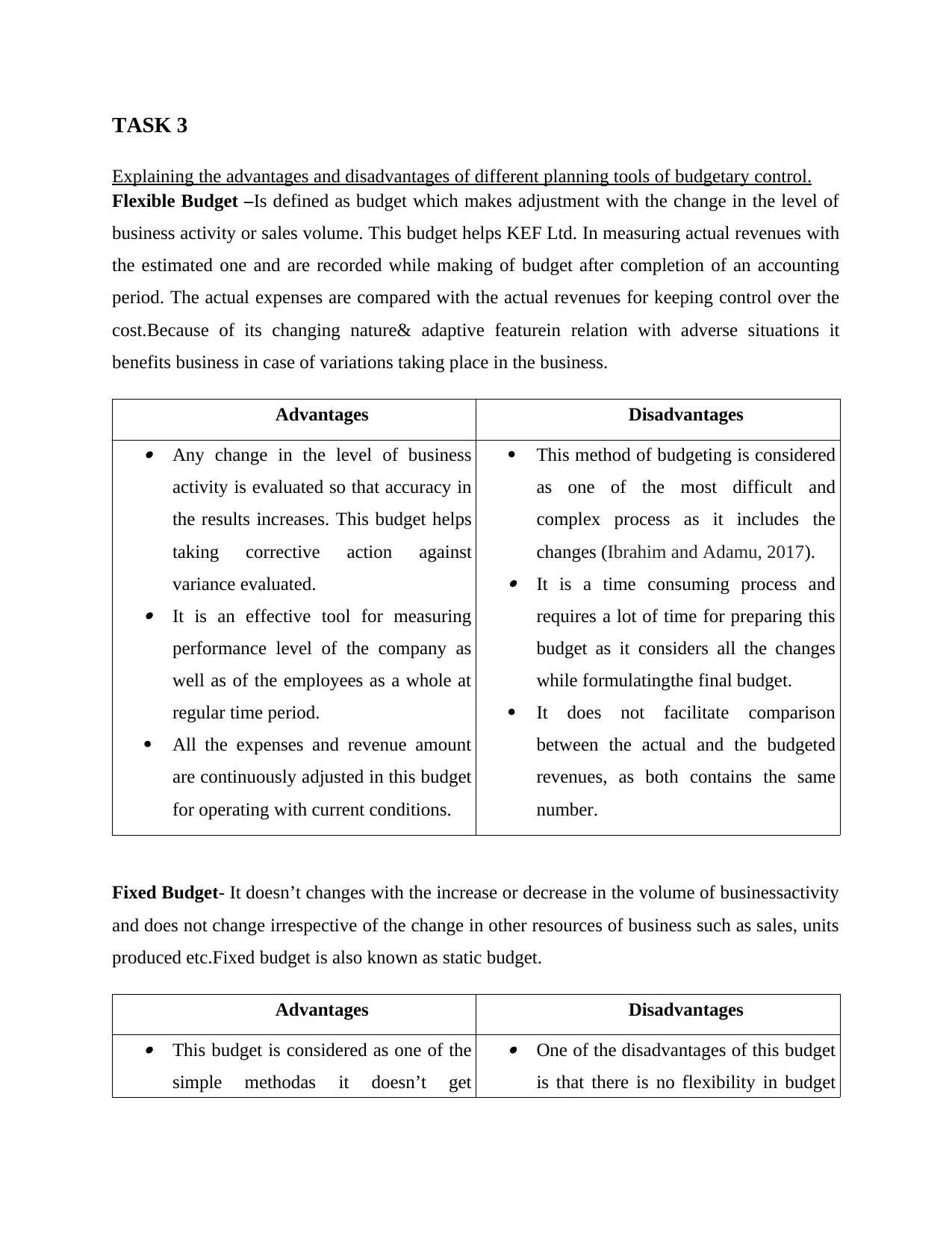

Explaining the advantages and disadvantages of different planning tools of budgetary control.

Flexible Budget –Is defined as budget which makes adjustment with the change in the level of

business activity or sales volume. This budget helps KEF Ltd. In measuring actual revenues with

the estimated one and are recorded while making of budget after completion of an accounting

period. The actual expenses are compared with the actual revenues for keeping control over the

cost.Because of its changing nature& adaptive featurein relation with adverse situations it

benefits business in case of variations taking place in the business.

Advantages Disadvantages Any change in the level of business

activity is evaluated so that accuracy in

the results increases. This budget helps

taking corrective action against

variance evaluated. It is an effective tool for measuring

performance level of the company as

well as of the employees as a whole at

regular time period.

All the expenses and revenue amount

are continuously adjusted in this budget

for operating with current conditions.

This method of budgeting is considered

as one of the most difficult and

complex process as it includes the

changes (Ibrahim and Adamu, 2017).

It is a time consuming process and

requires a lot of time for preparing this

budget as it considers all the changes

while formulatingthe final budget.

It does not facilitate comparison

between the actual and the budgeted

revenues, as both contains the same

number.

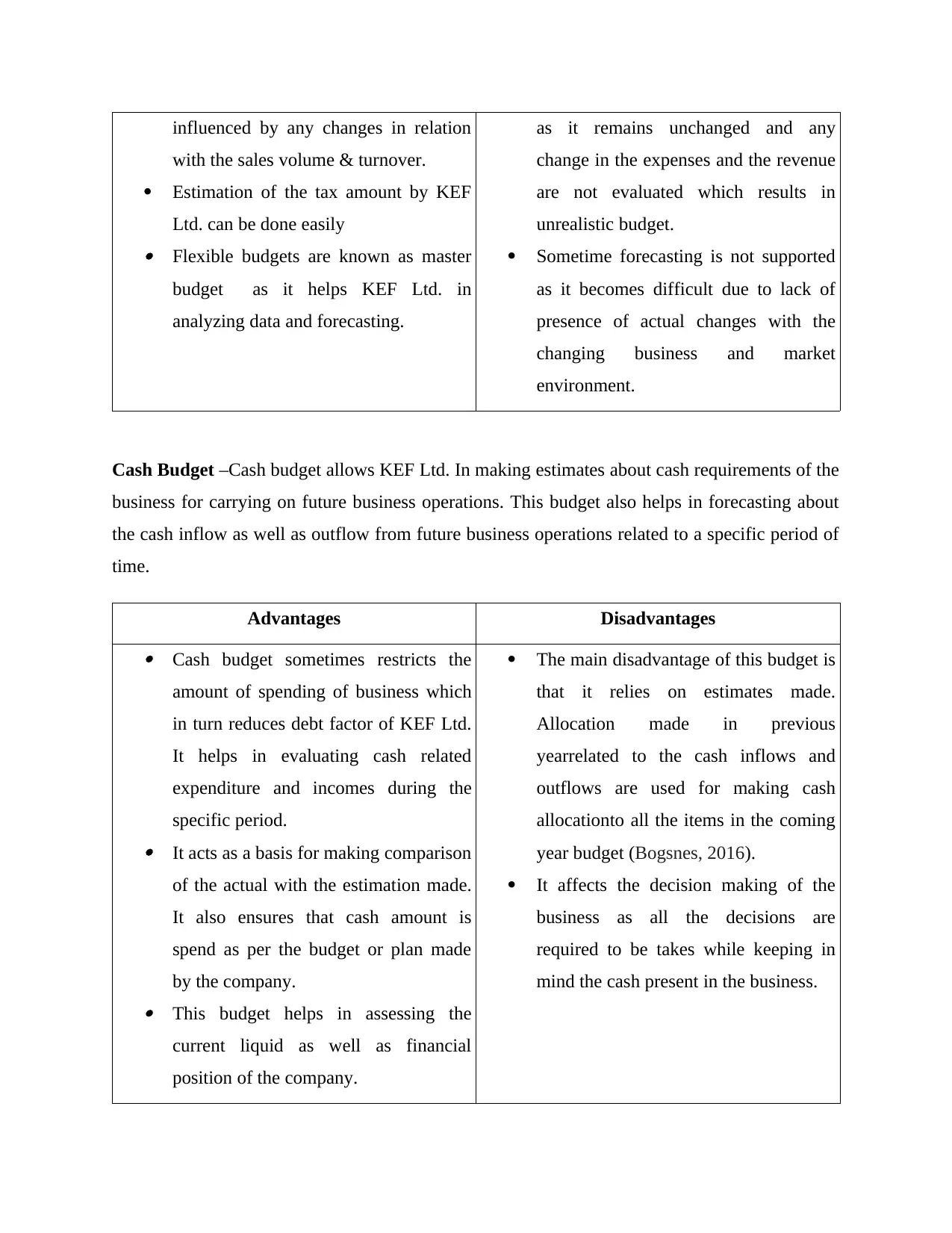

Fixed Budget- It doesn’t changes with the increase or decrease in the volume of businessactivity

and does not change irrespective of the change in other resources of business such as sales, units

produced etc.Fixed budget is also known as static budget.

Advantages Disadvantages This budget is considered as one of the

simple methodas it doesn’t get

One of the disadvantages of this budget

is that there is no flexibility in budget

Explaining the advantages and disadvantages of different planning tools of budgetary control.

Flexible Budget –Is defined as budget which makes adjustment with the change in the level of

business activity or sales volume. This budget helps KEF Ltd. In measuring actual revenues with

the estimated one and are recorded while making of budget after completion of an accounting

period. The actual expenses are compared with the actual revenues for keeping control over the

cost.Because of its changing nature& adaptive featurein relation with adverse situations it

benefits business in case of variations taking place in the business.

Advantages Disadvantages Any change in the level of business

activity is evaluated so that accuracy in

the results increases. This budget helps

taking corrective action against

variance evaluated. It is an effective tool for measuring

performance level of the company as

well as of the employees as a whole at

regular time period.

All the expenses and revenue amount

are continuously adjusted in this budget

for operating with current conditions.

This method of budgeting is considered

as one of the most difficult and

complex process as it includes the

changes (Ibrahim and Adamu, 2017).

It is a time consuming process and

requires a lot of time for preparing this

budget as it considers all the changes

while formulatingthe final budget.

It does not facilitate comparison

between the actual and the budgeted

revenues, as both contains the same

number.

Fixed Budget- It doesn’t changes with the increase or decrease in the volume of businessactivity

and does not change irrespective of the change in other resources of business such as sales, units

produced etc.Fixed budget is also known as static budget.

Advantages Disadvantages This budget is considered as one of the

simple methodas it doesn’t get

One of the disadvantages of this budget

is that there is no flexibility in budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

influenced by any changes in relation

with the sales volume & turnover.

Estimation of the tax amount by KEF

Ltd. can be done easily Flexible budgets are known as master

budget as it helps KEF Ltd. in

analyzing data and forecasting.

as it remains unchanged and any

change in the expenses and the revenue

are not evaluated which results in

unrealistic budget.

Sometime forecasting is not supported

as it becomes difficult due to lack of

presence of actual changes with the

changing business and market

environment.

Cash Budget –Cash budget allows KEF Ltd. In making estimates about cash requirements of the

business for carrying on future business operations. This budget also helps in forecasting about

the cash inflow as well as outflow from future business operations related to a specific period of

time.

Advantages Disadvantages Cash budget sometimes restricts the

amount of spending of business which

in turn reduces debt factor of KEF Ltd.

It helps in evaluating cash related

expenditure and incomes during the

specific period. It acts as a basis for making comparison

of the actual with the estimation made.

It also ensures that cash amount is

spend as per the budget or plan made

by the company. This budget helps in assessing the

current liquid as well as financial

position of the company.

The main disadvantage of this budget is

that it relies on estimates made.

Allocation made in previous

yearrelated to the cash inflows and

outflows are used for making cash

allocationto all the items in the coming

year budget (Bogsnes, 2016).

It affects the decision making of the

business as all the decisions are

required to be takes while keeping in

mind the cash present in the business.

with the sales volume & turnover.

Estimation of the tax amount by KEF

Ltd. can be done easily Flexible budgets are known as master

budget as it helps KEF Ltd. in

analyzing data and forecasting.

as it remains unchanged and any

change in the expenses and the revenue

are not evaluated which results in

unrealistic budget.

Sometime forecasting is not supported

as it becomes difficult due to lack of

presence of actual changes with the

changing business and market

environment.

Cash Budget –Cash budget allows KEF Ltd. In making estimates about cash requirements of the

business for carrying on future business operations. This budget also helps in forecasting about

the cash inflow as well as outflow from future business operations related to a specific period of

time.

Advantages Disadvantages Cash budget sometimes restricts the

amount of spending of business which

in turn reduces debt factor of KEF Ltd.

It helps in evaluating cash related

expenditure and incomes during the

specific period. It acts as a basis for making comparison

of the actual with the estimation made.

It also ensures that cash amount is

spend as per the budget or plan made

by the company. This budget helps in assessing the

current liquid as well as financial

position of the company.

The main disadvantage of this budget is

that it relies on estimates made.

Allocation made in previous

yearrelated to the cash inflows and

outflows are used for making cash

allocationto all the items in the coming

year budget (Bogsnes, 2016).

It affects the decision making of the

business as all the decisions are

required to be takes while keeping in

mind the cash present in the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analyzing the usefulness and application of different planning tools.

Planning tools Uses Application

Flexible Budget This budget is used for making

estimates related to amount of

income and expense associated

with business operation and

profit planning. It also helps in

controlling cost and provides a

balanced approach for making

comparison. It is also used for

deciding its product and

service price and for setting

the future business quotations

(Mirgorodskayaand et.al.,

2017).

This type of budget is best

suited in organizations where

the business activity level

varies or changes at a regular

interval. For making future

estimates this planning tool is

very useful as it helps in

forecasting demand of the new

product and service.

Fixed Budget This budgetary planning tool

helps KEF Ltd. in measuring

performance level of both the

company and its employees for

making of final budget. It

provides better plan by

allocating a fixed amount in

relation with the business

operations like overhead cost.

This budget can be applied in

those business organizations in

which business activities are of

stable nature and operates in a

consistent environment at the

workplace. The main

application of this budget is by

Small business firms as there

level of business activities do

not fluctuatefrom period to

period.

Cash Budget It is considered as one of the

most useful planning tool for

every business organization as

This budget is prepared and

applied to overcome the

position of the firm where it

Planning tools Uses Application

Flexible Budget This budget is used for making

estimates related to amount of

income and expense associated

with business operation and

profit planning. It also helps in

controlling cost and provides a

balanced approach for making

comparison. It is also used for

deciding its product and

service price and for setting

the future business quotations

(Mirgorodskayaand et.al.,

2017).

This type of budget is best

suited in organizations where

the business activity level

varies or changes at a regular

interval. For making future

estimates this planning tool is

very useful as it helps in

forecasting demand of the new

product and service.

Fixed Budget This budgetary planning tool

helps KEF Ltd. in measuring

performance level of both the

company and its employees for

making of final budget. It

provides better plan by

allocating a fixed amount in

relation with the business

operations like overhead cost.

This budget can be applied in

those business organizations in

which business activities are of

stable nature and operates in a

consistent environment at the

workplace. The main

application of this budget is by

Small business firms as there

level of business activities do

not fluctuatefrom period to

period.

Cash Budget It is considered as one of the

most useful planning tool for

every business organization as

This budget is prepared and

applied to overcome the

position of the firm where it

it provides detailed plan

related to cash allocation. It

can also be used to itemize the

budgeted sources and cash

uses in a future time period. It

helps in ascertaining the

liquidity and the cash position

of the company as well.

holds excess of nonproductive

cash balances. With the help of

this budget, KEF Ltd. can

make proper use of available

cash amount for making more

profits and to improve

business performance.

TASK 4

Different types of management accounting systems available for resolving the financial

problems.

For overcoming financial problems of the business, KEF Ltd. Can use various performance

indicators along with various management accounting tools which are as follows-

Benchmarking - It is the method in which actual performance is compared with the standard

performance as set as the benchmark by the company. It helps KEF Ltd. At the time offraming of

budget and financial performance goals (Li and et.al., 2019). Companies often compare their

own performance with other companies in the same industry to see and evaluate their

performance and focus on goals for improving their overall business performance.With the help

of benchmarking KEF Ltd. Can evaluate how their business department are performing on

individual basis and thus company as a whole. It helps company in setting performance targets,

improvement in business operations etc.

Balanced scorecard - Balanced scorecard is another tool which is used by the company to

achieve goals by making comparison of performance of the four main attributes present in the

business viz. growth, process of business, customers and finance. With the help of balanced

scorecard, KEF Ltd. can easily assess the factor which is hampering business performance of the

company and can makes changes accordingly. It also assists in framing of different business

plans and strategies for attaining business objectives successfully. The learning and growth

related to cash allocation. It

can also be used to itemize the

budgeted sources and cash

uses in a future time period. It

helps in ascertaining the

liquidity and the cash position

of the company as well.

holds excess of nonproductive

cash balances. With the help of

this budget, KEF Ltd. can

make proper use of available

cash amount for making more

profits and to improve

business performance.

TASK 4

Different types of management accounting systems available for resolving the financial

problems.

For overcoming financial problems of the business, KEF Ltd. Can use various performance

indicators along with various management accounting tools which are as follows-

Benchmarking - It is the method in which actual performance is compared with the standard

performance as set as the benchmark by the company. It helps KEF Ltd. At the time offraming of

budget and financial performance goals (Li and et.al., 2019). Companies often compare their

own performance with other companies in the same industry to see and evaluate their

performance and focus on goals for improving their overall business performance.With the help

of benchmarking KEF Ltd. Can evaluate how their business department are performing on

individual basis and thus company as a whole. It helps company in setting performance targets,

improvement in business operations etc.

Balanced scorecard - Balanced scorecard is another tool which is used by the company to

achieve goals by making comparison of performance of the four main attributes present in the

business viz. growth, process of business, customers and finance. With the help of balanced

scorecard, KEF Ltd. can easily assess the factor which is hampering business performance of the

company and can makes changes accordingly. It also assists in framing of different business

plans and strategies for attaining business objectives successfully. The learning and growth

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.