Detailed Management Accounting Report: Ever Joy Enterprise, UK (KPMG)

VerifiedAdded on 2021/01/02

|16

|4501

|492

Report

AI Summary

This report analyzes management accounting practices for Ever Joy Enterprise, a UK-based leisure and entertainment company. It begins by differentiating between management and financial accounting, then delves into cost accounting systems, including direct and standard costing. The report explores inventory and job costing systems, highlighting their benefits for Ever Joy Enterprise. It then examines different types of management accounting reports, such as budget, job cost, and inventory reports, and assesses the advantages of using these systems. Task 2 applies break-even analysis, calculating the number of tickets needed to break even and achieve a profit target. Finally, the report evaluates budgeting as a planning tool and financial governance to prevent financial losses. The conclusion summarizes the key findings, referencing relevant sources. The report aims to provide KPMG UK with insights into improving Ever Joy Enterprise's financial management and decision-making processes.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A. Difference between management and financial accounting ..................................................3

B. Cost accounting systems.........................................................................................................4

C. Inventory management system...............................................................................................5

D. Job costing system..................................................................................................................5

E. Different types of Management Accounting Report..............................................................6

F. Benefits of using management accounting systems:..............................................................6

TASK 2............................................................................................................................................7

a. The number of tickets that must be sold to break even (i.e. the point at which there is

neither profit nor loss).................................................................................................................7

b. If we want to make a profit of £30,000.00, how many tickets should be sold?......................7

c. What profit would result if 8,000 tickets were sold? ...........................................................8

TASK 3 ...........................................................................................................................................8

a. Evaluation of budgeting which can be used by Ever Joy Enterprises as a planning and

problem solving tool ..................................................................................................................8

b. Evaluation of financial governance which can help to pre-empt or prevent from financial

losses.........................................................................................................................................11

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A. Difference between management and financial accounting ..................................................3

B. Cost accounting systems.........................................................................................................4

C. Inventory management system...............................................................................................5

D. Job costing system..................................................................................................................5

E. Different types of Management Accounting Report..............................................................6

F. Benefits of using management accounting systems:..............................................................6

TASK 2............................................................................................................................................7

a. The number of tickets that must be sold to break even (i.e. the point at which there is

neither profit nor loss).................................................................................................................7

b. If we want to make a profit of £30,000.00, how many tickets should be sold?......................7

c. What profit would result if 8,000 tickets were sold? ...........................................................8

TASK 3 ...........................................................................................................................................8

a. Evaluation of budgeting which can be used by Ever Joy Enterprises as a planning and

problem solving tool ..................................................................................................................8

b. Evaluation of financial governance which can help to pre-empt or prevent from financial

losses.........................................................................................................................................11

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the analytical concept which involves determining, analysing,

interpreting and presentation of accounting information that is collected with the help of cost and

financial accounting. It helps in creating budgets, perform assets, cost management and

formulation of other financial reports (Csutora, M., 2012). This project is based on the case study

of Ever Joy Enterprise that deals in leisure and entertainment industry in UK. The company has

approached KPMG UK to prepare their draft for their management accounting department. The

report will present a deep understanding of Management Accounting System, its types and roles.

Apart from this, a detailed explanation about different management techniques will be discussed

along with various planning tools and their use with advantages/disadvantages. Further a

comparison of ways in which firm can apply management accounting in responding to its

financial issues will be discussed.

TASK 1

A. Difference between management and financial accounting

Management Accounting System

This is the process of identifying, measuring, analysing, interpreting and communicating

the information to the managers for pursuing the organisation goal. Management accounting

helps the managers to make the day to day decisions in the organisation. Basically it helps in

preparing management report and accounts that provide accurate and timely information’s

(Zainun, Tuanmat and Smith, 2011).

Financial Accounting

Financial accounting deals in preparing the financial statements of company's like

balance sheet, income statement and cash flows of the company's. It helps in disclosing the

overall business performance and financial health. Basically financial accounting is created for

its investors, creditors and industry regulators.

Difference between Management Accounting and Financial Accounting

Particular Management Accounting Financial Accounting

Objective The main objective of

management accounting is to

assist the management in

The main objective is to

provide financial information

4

Management accounting is the analytical concept which involves determining, analysing,

interpreting and presentation of accounting information that is collected with the help of cost and

financial accounting. It helps in creating budgets, perform assets, cost management and

formulation of other financial reports (Csutora, M., 2012). This project is based on the case study

of Ever Joy Enterprise that deals in leisure and entertainment industry in UK. The company has

approached KPMG UK to prepare their draft for their management accounting department. The

report will present a deep understanding of Management Accounting System, its types and roles.

Apart from this, a detailed explanation about different management techniques will be discussed

along with various planning tools and their use with advantages/disadvantages. Further a

comparison of ways in which firm can apply management accounting in responding to its

financial issues will be discussed.

TASK 1

A. Difference between management and financial accounting

Management Accounting System

This is the process of identifying, measuring, analysing, interpreting and communicating

the information to the managers for pursuing the organisation goal. Management accounting

helps the managers to make the day to day decisions in the organisation. Basically it helps in

preparing management report and accounts that provide accurate and timely information’s

(Zainun, Tuanmat and Smith, 2011).

Financial Accounting

Financial accounting deals in preparing the financial statements of company's like

balance sheet, income statement and cash flows of the company's. It helps in disclosing the

overall business performance and financial health. Basically financial accounting is created for

its investors, creditors and industry regulators.

Difference between Management Accounting and Financial Accounting

Particular Management Accounting Financial Accounting

Objective The main objective of

management accounting is to

assist the management in

The main objective is to

provide financial information

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

planning and decision making to the outsiders.

Information It provides the qualitative and

quantitative information’s.

It only provides the

quantitative information.

Time The reports are prepared as per

the organisational needs

As these reports are prepared

at the end of financial year.

Users This report provide only used

by the internal management.

These financial reports can be

used by both internal and

external parties.

Publishing and auditing These reports are neither

published by the organisation

nor audited by auditors.

It is required to be published

and audited by the statutory

auditors.

Management accounting can be helpful to 'Ever Joy Enterprises' in maximization of

profit, as in this process every possible effort are made to cut the unnecessary expenses. As

management accounting involves designing of budgets and trend charts, so managers of 'Ever

Joy Enterprise' can use this information for allocating budgets. There are various plans and

policies before the management, so management accounting can help the managers of Ever Joy

to decide the effective plan which can be more useful and helpful for the company (Dražić

Lutilsky and Dragija, 2012).

B. Cost accounting systems

Cost accounting is about determining the connection between the costs of inputs and the

outputs emanate from them. It enables a firm to be more efficient by allocating its resources to

the most profitable functions of firm. As it can be helpful for the Ever Joy enterprises also, by

using this system, managers of company can allocate the resources of firm to that functions,

which generates the most profit for the firm. There are two types of cost which are as follows -

Direct Costing

Direct costing, is directly related to the project. It can be easily connected to the specific

cost object like software, equipment and raw materials. As for the Ever Joy Enterprise, labour

can be the direct cost (Moser, 2012).

Standard costing

5

Information It provides the qualitative and

quantitative information’s.

It only provides the

quantitative information.

Time The reports are prepared as per

the organisational needs

As these reports are prepared

at the end of financial year.

Users This report provide only used

by the internal management.

These financial reports can be

used by both internal and

external parties.

Publishing and auditing These reports are neither

published by the organisation

nor audited by auditors.

It is required to be published

and audited by the statutory

auditors.

Management accounting can be helpful to 'Ever Joy Enterprises' in maximization of

profit, as in this process every possible effort are made to cut the unnecessary expenses. As

management accounting involves designing of budgets and trend charts, so managers of 'Ever

Joy Enterprise' can use this information for allocating budgets. There are various plans and

policies before the management, so management accounting can help the managers of Ever Joy

to decide the effective plan which can be more useful and helpful for the company (Dražić

Lutilsky and Dragija, 2012).

B. Cost accounting systems

Cost accounting is about determining the connection between the costs of inputs and the

outputs emanate from them. It enables a firm to be more efficient by allocating its resources to

the most profitable functions of firm. As it can be helpful for the Ever Joy enterprises also, by

using this system, managers of company can allocate the resources of firm to that functions,

which generates the most profit for the firm. There are two types of cost which are as follows -

Direct Costing

Direct costing, is directly related to the project. It can be easily connected to the specific

cost object like software, equipment and raw materials. As for the Ever Joy Enterprise, labour

can be the direct cost (Moser, 2012).

Standard costing

5

Standard costing is a costing method that is used to compare standard cost and revenues

with the actual outcomes. It is helpful to know the variances along with its causes, this inform

the management about the deviation and take corrective actions for the improvements. For an

example, Ever Joy enterprise is going to organise a musical concert in city, the standard costing

according to their manager would be 20000 pound, but actual costing they incurred is 15000

pound, so there is variance of 5000 pound in actual costing and standard costing (Granlund,

2011).

C. Inventory management system

In simplest word, to manage the inventory on daily basis in business, it is important to

have an appropriate inventory management system. Managing inventory in business is the most

difficult part, if any business manages the same efficiently then they can earn higher profits.

Because in today's time there are various types of systems to manage the inventory and that

allows the firm to earn extra income also. The Ever Joy enterprise should also use the system, for

the smooth incoming and outgoing of inventories. There are various inventory management

systems, which allows managers to track their inventory efficiently. FIFO, First in first out

method of inventory management talks about the oldest items of stocks are the ones being sold

first, regardless of which units are actually sold first. LIFO, last in first out, that allows to most

recently produced or received are the items to be recorded as sold first. JUST IN TIME, which

align raw materials orders from suppliers directly with production schedules. This helps in

minimising the warehouse cost for the company, as raw materials arrive at the time of

production, so it does not need to store the material in warehouses (Johnson, 2013).

D. Job costing system

Job costing is a system for assigning manufacturing costs to an individual products or

batches of products. Generally the job costing system is used, when there is different kinds of

products are manufactured or more than one job are performed. For an example, Ever joy

Enterprise, organise event they perform different kind of service, so by the help of job costing

system, they can assign the cost to each service. At the time of completion of event, comparison

is made with reference to estimated cost, so Ever Joy Enterprise can get benefit by applying this

costing system (Leitner, 2013).

6

with the actual outcomes. It is helpful to know the variances along with its causes, this inform

the management about the deviation and take corrective actions for the improvements. For an

example, Ever Joy enterprise is going to organise a musical concert in city, the standard costing

according to their manager would be 20000 pound, but actual costing they incurred is 15000

pound, so there is variance of 5000 pound in actual costing and standard costing (Granlund,

2011).

C. Inventory management system

In simplest word, to manage the inventory on daily basis in business, it is important to

have an appropriate inventory management system. Managing inventory in business is the most

difficult part, if any business manages the same efficiently then they can earn higher profits.

Because in today's time there are various types of systems to manage the inventory and that

allows the firm to earn extra income also. The Ever Joy enterprise should also use the system, for

the smooth incoming and outgoing of inventories. There are various inventory management

systems, which allows managers to track their inventory efficiently. FIFO, First in first out

method of inventory management talks about the oldest items of stocks are the ones being sold

first, regardless of which units are actually sold first. LIFO, last in first out, that allows to most

recently produced or received are the items to be recorded as sold first. JUST IN TIME, which

align raw materials orders from suppliers directly with production schedules. This helps in

minimising the warehouse cost for the company, as raw materials arrive at the time of

production, so it does not need to store the material in warehouses (Johnson, 2013).

D. Job costing system

Job costing is a system for assigning manufacturing costs to an individual products or

batches of products. Generally the job costing system is used, when there is different kinds of

products are manufactured or more than one job are performed. For an example, Ever joy

Enterprise, organise event they perform different kind of service, so by the help of job costing

system, they can assign the cost to each service. At the time of completion of event, comparison

is made with reference to estimated cost, so Ever Joy Enterprise can get benefit by applying this

costing system (Leitner, 2013).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

E. Different types of Management Accounting Report

Accounting reports are the important part of business, these reports show the actual

position of business. As a comprehensive report is produced at every quarter to know the

performance of business. The different types of managerial reports are as follows :

Budget Report

This is the most fundamental report for business owners to understand and control the

costs across the enterprise. As by evaluation of previous year expenses, it becomes possible to

estimates budget for the following year and find places to cut the costs. As Ever Joy Enterprise

can prepare this report by evaluation of previous years budgets, and they can cut the extra cost in

budget. This can help in increasing the profitability of firm (JOSHI and et. al., 2011).

Job Cost Report

It provides a view of the total cost accrued in single project compared to the expected

revenue earned by that project. This report helps managers to evaluate the profitability of the job

and optimise their operations by focusing on the job that are most profitable for the overall

business. As Ever Joy Enterprise can also prepare this report as they perform different type of

jobs in an event. So by the help of this report, company would come to know about their most

profitable job (Budding, Grossi and Tagesson, 2014).

Inventory and Manufacturing report

Basically these reports are useful for those who manufactures the physical products,

especially for those who manufacture this with low fault tolerance. They help centralised data on

inventory cost, labour and other overheads involved in the process of production, providing raw

data to optimise assembly.

F. Benefits of using management accounting systems:

Cost accounting system:

Using cost accounting system helps in preparing the budget for the future by analysing

the previous budgets. This reduces the chances of having wastage of cost which directly make

positive impact on the profitability of company. This helps in monitoring and controlling the

labour cost. According to the nature of business wage expenses can be taken from the

departments. It can help management to pick and choose how it determines efficiency and

productivity (Kuula, Putkiranta and Toivanen, 2012).

Inventory management system:

7

Accounting reports are the important part of business, these reports show the actual

position of business. As a comprehensive report is produced at every quarter to know the

performance of business. The different types of managerial reports are as follows :

Budget Report

This is the most fundamental report for business owners to understand and control the

costs across the enterprise. As by evaluation of previous year expenses, it becomes possible to

estimates budget for the following year and find places to cut the costs. As Ever Joy Enterprise

can prepare this report by evaluation of previous years budgets, and they can cut the extra cost in

budget. This can help in increasing the profitability of firm (JOSHI and et. al., 2011).

Job Cost Report

It provides a view of the total cost accrued in single project compared to the expected

revenue earned by that project. This report helps managers to evaluate the profitability of the job

and optimise their operations by focusing on the job that are most profitable for the overall

business. As Ever Joy Enterprise can also prepare this report as they perform different type of

jobs in an event. So by the help of this report, company would come to know about their most

profitable job (Budding, Grossi and Tagesson, 2014).

Inventory and Manufacturing report

Basically these reports are useful for those who manufactures the physical products,

especially for those who manufacture this with low fault tolerance. They help centralised data on

inventory cost, labour and other overheads involved in the process of production, providing raw

data to optimise assembly.

F. Benefits of using management accounting systems:

Cost accounting system:

Using cost accounting system helps in preparing the budget for the future by analysing

the previous budgets. This reduces the chances of having wastage of cost which directly make

positive impact on the profitability of company. This helps in monitoring and controlling the

labour cost. According to the nature of business wage expenses can be taken from the

departments. It can help management to pick and choose how it determines efficiency and

productivity (Kuula, Putkiranta and Toivanen, 2012).

Inventory management system:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system assist company to maintain the adequate level of

inventory at the time it needed. It also increases the productivity and efficiency as it helps in

avoiding excess stock and stock outs.

Job costing system:

Job costing system assist the company on the total cost incurred on individual job. It

helps the company to identify the costs and when costs are identified by job it allows managers

to understand the complete cost of a job. This information helps mangers to estimate cost of

upcoming projects (Schaltegger and Burritt, 2017).

Price Optimising System:

Price optimisation is an analysis by a company to determine how customers will respond

to different prices of its product and service through different channels. It use data analysis to

predict the attitude of potential buyers to different prices of a product or services. As the Ever

Joy can also use this, company should optimise the prices in a way, that satisfy customer and

company also earns good profits also (Kuula, Putkiranta and Toivanen,2012).

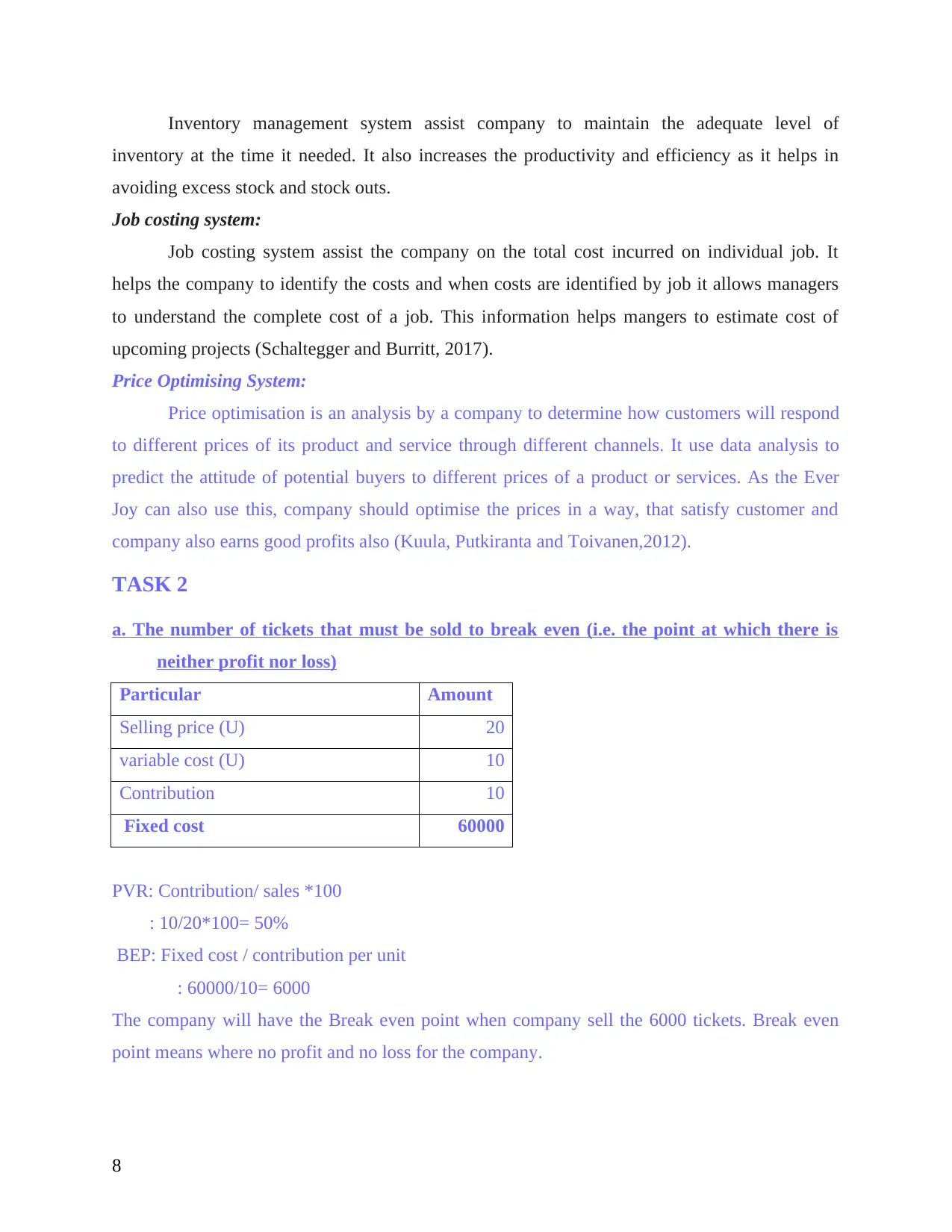

TASK 2

a. The number of tickets that must be sold to break even (i.e. the point at which there is

neither profit nor loss)

Particular Amount

Selling price (U) 20

variable cost (U) 10

Contribution 10

Fixed cost 60000

PVR: Contribution/ sales *100

: 10/20*100= 50%

BEP: Fixed cost / contribution per unit

: 60000/10= 6000

The company will have the Break even point when company sell the 6000 tickets. Break even

point means where no profit and no loss for the company.

8

inventory at the time it needed. It also increases the productivity and efficiency as it helps in

avoiding excess stock and stock outs.

Job costing system:

Job costing system assist the company on the total cost incurred on individual job. It

helps the company to identify the costs and when costs are identified by job it allows managers

to understand the complete cost of a job. This information helps mangers to estimate cost of

upcoming projects (Schaltegger and Burritt, 2017).

Price Optimising System:

Price optimisation is an analysis by a company to determine how customers will respond

to different prices of its product and service through different channels. It use data analysis to

predict the attitude of potential buyers to different prices of a product or services. As the Ever

Joy can also use this, company should optimise the prices in a way, that satisfy customer and

company also earns good profits also (Kuula, Putkiranta and Toivanen,2012).

TASK 2

a. The number of tickets that must be sold to break even (i.e. the point at which there is

neither profit nor loss)

Particular Amount

Selling price (U) 20

variable cost (U) 10

Contribution 10

Fixed cost 60000

PVR: Contribution/ sales *100

: 10/20*100= 50%

BEP: Fixed cost / contribution per unit

: 60000/10= 6000

The company will have the Break even point when company sell the 6000 tickets. Break even

point means where no profit and no loss for the company.

8

Break even units is the volume of finished goods that must be sold by an organisation to

attain situation of no profit and n profit. When fixed cost for the products is 60000 and

contribution is 10 per nit, then BEP is ascertained as 6000 units. If the organisation is able to sold

6000 units then they can be said to out of danger or loss position.

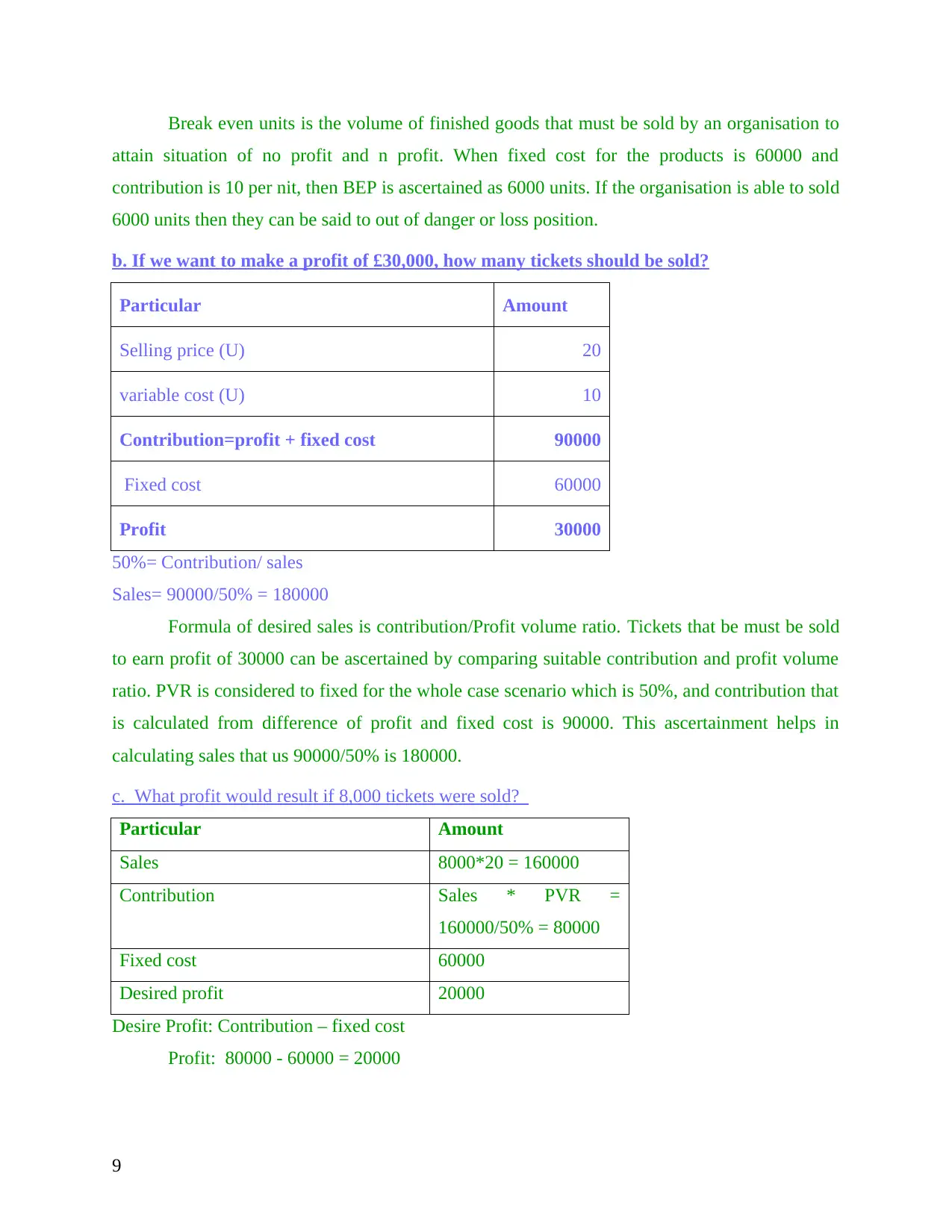

b. If we want to make a profit of £30,000, how many tickets should be sold?

Particular Amount

Selling price (U) 20

variable cost (U) 10

Contribution=profit + fixed cost 90000

Fixed cost 60000

Profit 30000

50%= Contribution/ sales

Sales= 90000/50% = 180000

Formula of desired sales is contribution/Profit volume ratio. Tickets that be must be sold

to earn profit of 30000 can be ascertained by comparing suitable contribution and profit volume

ratio. PVR is considered to fixed for the whole case scenario which is 50%, and contribution that

is calculated from difference of profit and fixed cost is 90000. This ascertainment helps in

calculating sales that us 90000/50% is 180000.

c. What profit would result if 8,000 tickets were sold?

Particular Amount

Sales 8000*20 = 160000

Contribution Sales * PVR =

160000/50% = 80000

Fixed cost 60000

Desired profit 20000

Desire Profit: Contribution – fixed cost

Profit: 80000 - 60000 = 20000

9

attain situation of no profit and n profit. When fixed cost for the products is 60000 and

contribution is 10 per nit, then BEP is ascertained as 6000 units. If the organisation is able to sold

6000 units then they can be said to out of danger or loss position.

b. If we want to make a profit of £30,000, how many tickets should be sold?

Particular Amount

Selling price (U) 20

variable cost (U) 10

Contribution=profit + fixed cost 90000

Fixed cost 60000

Profit 30000

50%= Contribution/ sales

Sales= 90000/50% = 180000

Formula of desired sales is contribution/Profit volume ratio. Tickets that be must be sold

to earn profit of 30000 can be ascertained by comparing suitable contribution and profit volume

ratio. PVR is considered to fixed for the whole case scenario which is 50%, and contribution that

is calculated from difference of profit and fixed cost is 90000. This ascertainment helps in

calculating sales that us 90000/50% is 180000.

c. What profit would result if 8,000 tickets were sold?

Particular Amount

Sales 8000*20 = 160000

Contribution Sales * PVR =

160000/50% = 80000

Fixed cost 60000

Desired profit 20000

Desire Profit: Contribution – fixed cost

Profit: 80000 - 60000 = 20000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In order to ascertain desired profit of an organisation, new contribution is determined by

the combination of PVR and sold units. By ascertaining contribution of 80000, desired profit is

calculated by comparing this contribution and fixed cost.

TASK 3

a. Evaluation of budgeting which can be used by Ever Joy Enterprises as a planning and problem

solving tool

Budget:

Budget is an estimation of revenue and expenses over a specified future period of time

with the intention of proper utilising the resources. This helps in allocating the cost to the

different business activities after evaluation of previous cost. It can help the Ever Joy Enterprise

also, as they can set the budget for their future events, by evaluating previous cost and they can

use the resources in effective manner (Quinn, 2011).

Run business without cash problem:

It is very important to have adequate cash in business for smooth functioning of business

activities. As if business maintain accurate cash flow, than it can help to maximise their profits.

So preparing an adequate budget, that is, comparison of actual expenditure with standard

expenditure, can help Ever Joy Enterprise to maintain the sufficient cash (Maheshwari, 2015).

Controlling future activities and cost:

The controlling cost is important activity for business as lower cost helps business to

generate more revenues. With the help of a standard budget, cost controlling becomes easy. It

will help Ever Joy Enterprise to evaluate previous budgets and according to that prepare budget

for future. So company can cut the cost where needed and enhance its revenues.

It sets targets to archive for the management:

Budget is a very important tool for the management to evaluate cost and according to that

set quantifies target for business. The employees and manager of company comes together to

achieve the sets target of business.

Can be used for corrective actions:

The basic feature of budget is to evaluate the actual cost and standard cost and know

variance. So it will be beneficial for Ever Joy Enterprise as they can take corrective action to

remove the variance (Johnson, 2013).

10

the combination of PVR and sold units. By ascertaining contribution of 80000, desired profit is

calculated by comparing this contribution and fixed cost.

TASK 3

a. Evaluation of budgeting which can be used by Ever Joy Enterprises as a planning and problem

solving tool

Budget:

Budget is an estimation of revenue and expenses over a specified future period of time

with the intention of proper utilising the resources. This helps in allocating the cost to the

different business activities after evaluation of previous cost. It can help the Ever Joy Enterprise

also, as they can set the budget for their future events, by evaluating previous cost and they can

use the resources in effective manner (Quinn, 2011).

Run business without cash problem:

It is very important to have adequate cash in business for smooth functioning of business

activities. As if business maintain accurate cash flow, than it can help to maximise their profits.

So preparing an adequate budget, that is, comparison of actual expenditure with standard

expenditure, can help Ever Joy Enterprise to maintain the sufficient cash (Maheshwari, 2015).

Controlling future activities and cost:

The controlling cost is important activity for business as lower cost helps business to

generate more revenues. With the help of a standard budget, cost controlling becomes easy. It

will help Ever Joy Enterprise to evaluate previous budgets and according to that prepare budget

for future. So company can cut the cost where needed and enhance its revenues.

It sets targets to archive for the management:

Budget is a very important tool for the management to evaluate cost and according to that

set quantifies target for business. The employees and manager of company comes together to

achieve the sets target of business.

Can be used for corrective actions:

The basic feature of budget is to evaluate the actual cost and standard cost and know

variance. So it will be beneficial for Ever Joy Enterprise as they can take corrective action to

remove the variance (Johnson, 2013).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Goal congruence:

Goal Congruence is a situation where multiple levels of people in organisation share

same goal. This assist organisation being able to work together to accomplish a strategy. The

Ever Joy Enterprise organise the events so it is important to have synergy among the workers for

successfully completion of an event (Takeda, Boyns, 2014).

Creates coordination and communication among the departments:

There are various kinds of department who works in an organisation like HR, Finance

and marketing. And for a successful organisation it is important to have coordination among

departments. The Ever Joy organises an Event for that budget is prepared by Finance department

for performing marketing activities according to budget. And employees who perform activities

are recruited by HR department. So this is necessary to have better synergy for achieving the

goals.

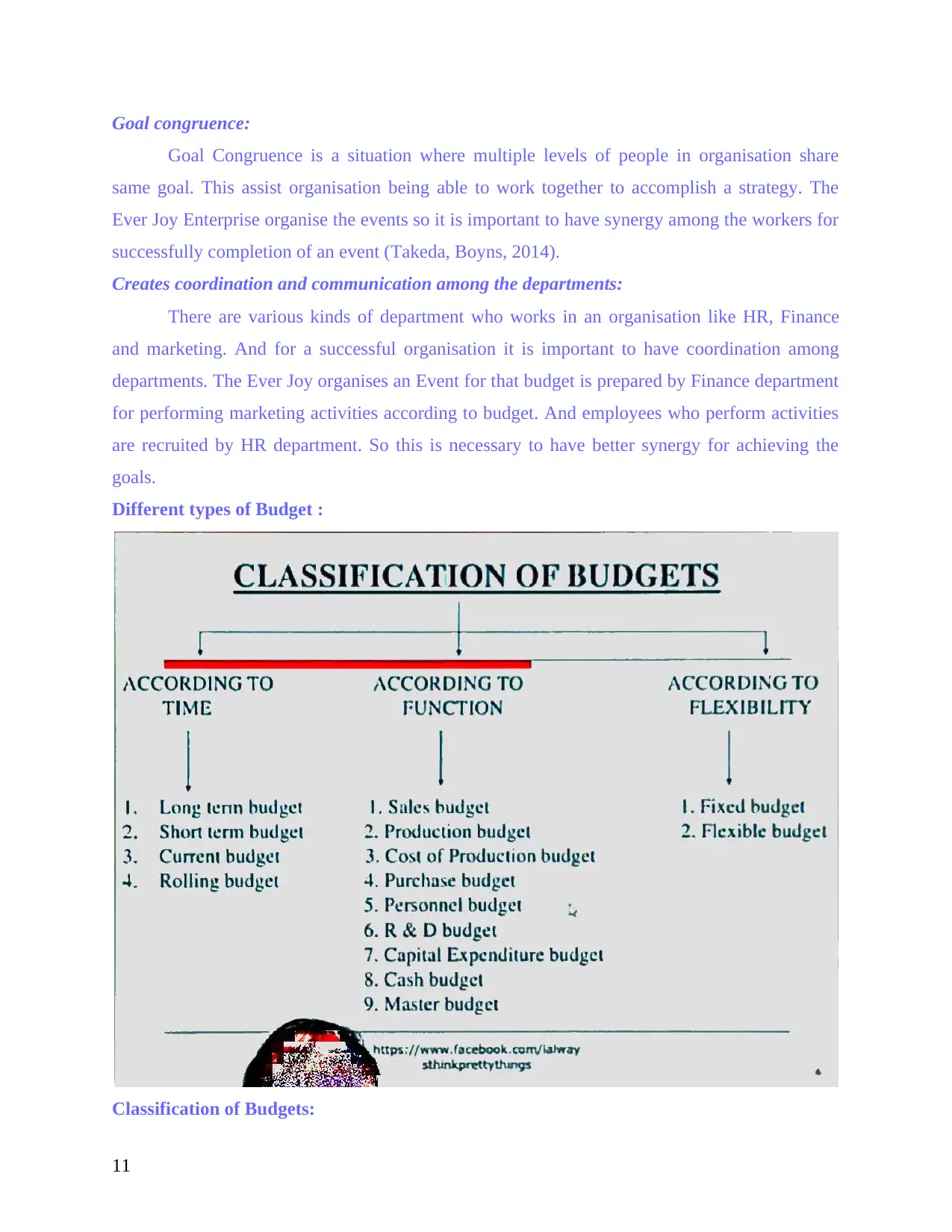

Different types of Budget :

Classification of Budgets:

11

Goal Congruence is a situation where multiple levels of people in organisation share

same goal. This assist organisation being able to work together to accomplish a strategy. The

Ever Joy Enterprise organise the events so it is important to have synergy among the workers for

successfully completion of an event (Takeda, Boyns, 2014).

Creates coordination and communication among the departments:

There are various kinds of department who works in an organisation like HR, Finance

and marketing. And for a successful organisation it is important to have coordination among

departments. The Ever Joy organises an Event for that budget is prepared by Finance department

for performing marketing activities according to budget. And employees who perform activities

are recruited by HR department. So this is necessary to have better synergy for achieving the

goals.

Different types of Budget :

Classification of Budgets:

11

The company Ever Joy enterprise can prepare different kinds of budget according to the

nature, for smooth functioning of business. These are as follows:

Short Term Budget:

The short term budget is a time based budget, which is prepared for short span of time.

The Ever Joy Enterprise organise events frequently so they can prepare this budget for a

particular event to know the standard income and expenditure from event.

Long term Budget:

It is a time based budget and prepared with a long term vision. They are concerned with

planning the operations of a firm over a perspective of five to ten years.

Current Budget:

This budget is similar to short term budget. As it gets adjusted according to

circumstances.

Rolling Budget:

It involve the incremental extension of the existing budget model. A rolling established at

the beginning of an accounting period and changes according to circumstances. As Everjoy can

use this budget to get an estimated cost for its upcoming events. And then company can make

changes according to situations.

Flexible Budget:

Flexible budget is financial plan of estimated revenues and expenses based on current

actual amount of output. In other words, it shows how changes in output made changes in

revenues and expenses of business, it is also called variable budget. The Ever Joy enterprise can

use this budget to know the variance between actual and standard budget.

Fixed Budget:

Fixed budget does not depended on any business activity. It does not change when sales

or some other activity of business increases or decreases.

Purchase Budget:

Purchase budget is considered as functional budget for business. The company purchase

various kinds of material to perform an event successfully. So for that company can prepare

purchase budget, according to that they can buy require material for an event and control their

cost(Schermann, Wiesche and Krcmar, 2012).

Sales Budget:

12

nature, for smooth functioning of business. These are as follows:

Short Term Budget:

The short term budget is a time based budget, which is prepared for short span of time.

The Ever Joy Enterprise organise events frequently so they can prepare this budget for a

particular event to know the standard income and expenditure from event.

Long term Budget:

It is a time based budget and prepared with a long term vision. They are concerned with

planning the operations of a firm over a perspective of five to ten years.

Current Budget:

This budget is similar to short term budget. As it gets adjusted according to

circumstances.

Rolling Budget:

It involve the incremental extension of the existing budget model. A rolling established at

the beginning of an accounting period and changes according to circumstances. As Everjoy can

use this budget to get an estimated cost for its upcoming events. And then company can make

changes according to situations.

Flexible Budget:

Flexible budget is financial plan of estimated revenues and expenses based on current

actual amount of output. In other words, it shows how changes in output made changes in

revenues and expenses of business, it is also called variable budget. The Ever Joy enterprise can

use this budget to know the variance between actual and standard budget.

Fixed Budget:

Fixed budget does not depended on any business activity. It does not change when sales

or some other activity of business increases or decreases.

Purchase Budget:

Purchase budget is considered as functional budget for business. The company purchase

various kinds of material to perform an event successfully. So for that company can prepare

purchase budget, according to that they can buy require material for an event and control their

cost(Schermann, Wiesche and Krcmar, 2012).

Sales Budget:

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.