Management Accounting Report for Business Decision Making

VerifiedAdded on 2023/01/19

|16

|3827

|80

Report

AI Summary

This report delves into the core concepts of management accounting, utilizing Aspall Cyder Ltd as a case study. It explores various management accounting systems, including cost accounting and inventory management, and their application in decision-making. The report examines different costing methods like marginal and absorption costing, illustrating their impact through detailed cost cards and profit statements. Furthermore, it covers planning tools and budgetary control, including sales, production, and cash budgets, along with an analysis of alternative budgeting methods and their behavioral implications. The report also addresses the adaptation of management accounting in response to financial problems and the role of financial governance. Overall, the report offers a comprehensive understanding of management accounting principles and their practical application in a business context.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management Accounting System:..........................................................................................1

P2 Management Accounting Reporting:.....................................................................................2

TASK 2............................................................................................................................................3

P3 Application of appropriate costing method:...........................................................................3

Case 1............................................................................................................................3

Case 2............................................................................................................................4

TASK 3............................................................................................................................................5

P4 Planning tools and budgetary control:....................................................................................5

Budget:..........................................................................................................................8

Alternative methods of budget:...................................................................................10

Behavioural implications of budget:...........................................................................10

TASK 4..........................................................................................................................................10

P5 Adaptation of management accounting in response to financial problems..........................10

Financial Problems:.....................................................................................................10

Financial Governance:................................................................................................11

Comparison:................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management Accounting System:..........................................................................................1

P2 Management Accounting Reporting:.....................................................................................2

TASK 2............................................................................................................................................3

P3 Application of appropriate costing method:...........................................................................3

Case 1............................................................................................................................3

Case 2............................................................................................................................4

TASK 3............................................................................................................................................5

P4 Planning tools and budgetary control:....................................................................................5

Budget:..........................................................................................................................8

Alternative methods of budget:...................................................................................10

Behavioural implications of budget:...........................................................................10

TASK 4..........................................................................................................................................10

P5 Adaptation of management accounting in response to financial problems..........................10

Financial Problems:.....................................................................................................10

Financial Governance:................................................................................................11

Comparison:................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

In a competitive environment of business, each organization have to develop a strong

emphasis on its internal management and operations so that it can survive. Management

accounting is a set of activities and tools for doing the same. It is a framework that develop and

control the internal environment and functions of the establishment.

For a better understanding of management accounting, Aspall Cyder Ltd has been chosen

which is an England based manufacturing company deals in ciders and other apple derived

drinks and purchased by Molson Coors Brewing Company in 2018. this report covers an enhance

knowledge of management accounting system and reporting, application of financial and costing

techniques, use of different planning tools and financial governance in identifying and solving

financial problems.

TASK 1

P1 Management Accounting System:

Management accounting system: Management or managerial accounting system is a

framework that collects the data and convert it into such material information and statements that

help the internal management to plan strategies and make decisions in an effective and efficient

manner (Banham and He, 2014). The management of Aspall Cyder uses various types of

managerial accounting system in order to manage the internal matters. Some of them are

mentioned below:

Cost Accounting System: This system is specially helpful for manufacturing companies

such as Aspall Cyder as this system is used to evaluate the overall manufacturing cost of the

products manufactured by the companies. Cost accounting system is used to calculate the actual

and standard costs on each level from production to sell.

Inventory management system: Inventory management system is a preliminary system

that shape, monitor and control the movement of stock or goods. This system is developed to

track the overall process of manufacturing from purchase of raw ingredients to delivery or

shipment of the finished goods. The management of the selected company follow this system to

trace the location of its products.

Price optimization system: Price optimisation system is utilized to maximize the

organizational profit along with providing optimum customer satisfaction. The management of

1

In a competitive environment of business, each organization have to develop a strong

emphasis on its internal management and operations so that it can survive. Management

accounting is a set of activities and tools for doing the same. It is a framework that develop and

control the internal environment and functions of the establishment.

For a better understanding of management accounting, Aspall Cyder Ltd has been chosen

which is an England based manufacturing company deals in ciders and other apple derived

drinks and purchased by Molson Coors Brewing Company in 2018. this report covers an enhance

knowledge of management accounting system and reporting, application of financial and costing

techniques, use of different planning tools and financial governance in identifying and solving

financial problems.

TASK 1

P1 Management Accounting System:

Management accounting system: Management or managerial accounting system is a

framework that collects the data and convert it into such material information and statements that

help the internal management to plan strategies and make decisions in an effective and efficient

manner (Banham and He, 2014). The management of Aspall Cyder uses various types of

managerial accounting system in order to manage the internal matters. Some of them are

mentioned below:

Cost Accounting System: This system is specially helpful for manufacturing companies

such as Aspall Cyder as this system is used to evaluate the overall manufacturing cost of the

products manufactured by the companies. Cost accounting system is used to calculate the actual

and standard costs on each level from production to sell.

Inventory management system: Inventory management system is a preliminary system

that shape, monitor and control the movement of stock or goods. This system is developed to

track the overall process of manufacturing from purchase of raw ingredients to delivery or

shipment of the finished goods. The management of the selected company follow this system to

trace the location of its products.

Price optimization system: Price optimisation system is utilized to maximize the

organizational profit along with providing optimum customer satisfaction. The management of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

respective establishment follows this system to evaluate the reactions of customers regarding

different price set for the various products provide by the firm and find out the best price

according to the customers and organization as well.

Job order costing system: Job costing system is mostly used by the construction

companies to calculate the cost of a specific task or project (Carlsson-Wall, Kraus and Karlsson,

2017). When a particular or customised project of manufacturing products is given to the chosen

company, the management apply job costing management system to evaluate the cost of that

particular task.

P2 Management Accounting Reporting:

Management accounting reporting: Managerial accounting reporting is a process to

create impressive reports which assist the owners and managers in monitoring performance of

the organization as well as the effectiveness of the employees. These reports are prepared by the

management accountants of the Aspall Cyder Ltd for various departments, employees and

activities as well. Some of the accounting reports created by the administration are presented

below:

Budget Report: Budget reports are prepared with the help of previous year outcomes,

current year budget and actual outcomes at the end of the financial period. This report helps the

management in identifying the variances between actual results and budgeted figures and it also

defines the reasons behind these deviations (Endenich and others, 2016). Aspall Cyder's

managers utilise these reports in evaluating the measures and accurate level of income and

expenditures in upcoming budgets.

Accounts Receivable report: The companies which extend the credit to their customers

are essentially needed to prepare these reports on a regular basis so that they can manage the

cash flow of the organization. The management team of respective firm create these reports to

track the due receipts, interest on credits, details of the debtors and manage its debtor turnover

ratio.

Inventory management report: The manufacturing companies such as Aspall Cyder

creates this reports to track their physical inventory. These reports include the information

related to the material wastages, per unit overhead cost, labour hour rates, etc. The management

can use these reports to compare different processes of manufacturing and improve the

production quality along with cost reduction (Grossi and others, 2014).

2

different price set for the various products provide by the firm and find out the best price

according to the customers and organization as well.

Job order costing system: Job costing system is mostly used by the construction

companies to calculate the cost of a specific task or project (Carlsson-Wall, Kraus and Karlsson,

2017). When a particular or customised project of manufacturing products is given to the chosen

company, the management apply job costing management system to evaluate the cost of that

particular task.

P2 Management Accounting Reporting:

Management accounting reporting: Managerial accounting reporting is a process to

create impressive reports which assist the owners and managers in monitoring performance of

the organization as well as the effectiveness of the employees. These reports are prepared by the

management accountants of the Aspall Cyder Ltd for various departments, employees and

activities as well. Some of the accounting reports created by the administration are presented

below:

Budget Report: Budget reports are prepared with the help of previous year outcomes,

current year budget and actual outcomes at the end of the financial period. This report helps the

management in identifying the variances between actual results and budgeted figures and it also

defines the reasons behind these deviations (Endenich and others, 2016). Aspall Cyder's

managers utilise these reports in evaluating the measures and accurate level of income and

expenditures in upcoming budgets.

Accounts Receivable report: The companies which extend the credit to their customers

are essentially needed to prepare these reports on a regular basis so that they can manage the

cash flow of the organization. The management team of respective firm create these reports to

track the due receipts, interest on credits, details of the debtors and manage its debtor turnover

ratio.

Inventory management report: The manufacturing companies such as Aspall Cyder

creates this reports to track their physical inventory. These reports include the information

related to the material wastages, per unit overhead cost, labour hour rates, etc. The management

can use these reports to compare different processes of manufacturing and improve the

production quality along with cost reduction (Grossi and others, 2014).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

P3 Application of appropriate costing method:

Cost: Cost is the value that is incurred by the seller in order to sale its products. Overall

expenses that are paid by the Aspall Cyder in the process of purchasing raw material to deliver

the products to the customers will be consider as the cost. There are various types of the cost

which are described as under:

Direct cost: Direct costs are an overhead that can be completely assigned to the

manufacturing of particular product. The examples of direct costs are labour wages, machine

hours, manufacturing overheads, etc.

Indirect cost: These are the costs that are not directly connected with the production

process hence not accountable to a cost project such as depreciation and administrative expenses.

Fixed cost: The costs which remains unchanged or irrelevant to the production process

and output level are known as fixed costs. Insurance charges, interest, salaries, rent, etc. are the

examples of fixed costs (Halaoua, Hamdi and Mejri, 2017).

Variable cost: The costs which varies or fluctuate with the level of production or unit of

products are called variable costs. If there is no production in the factory then there will be no

variable cost.

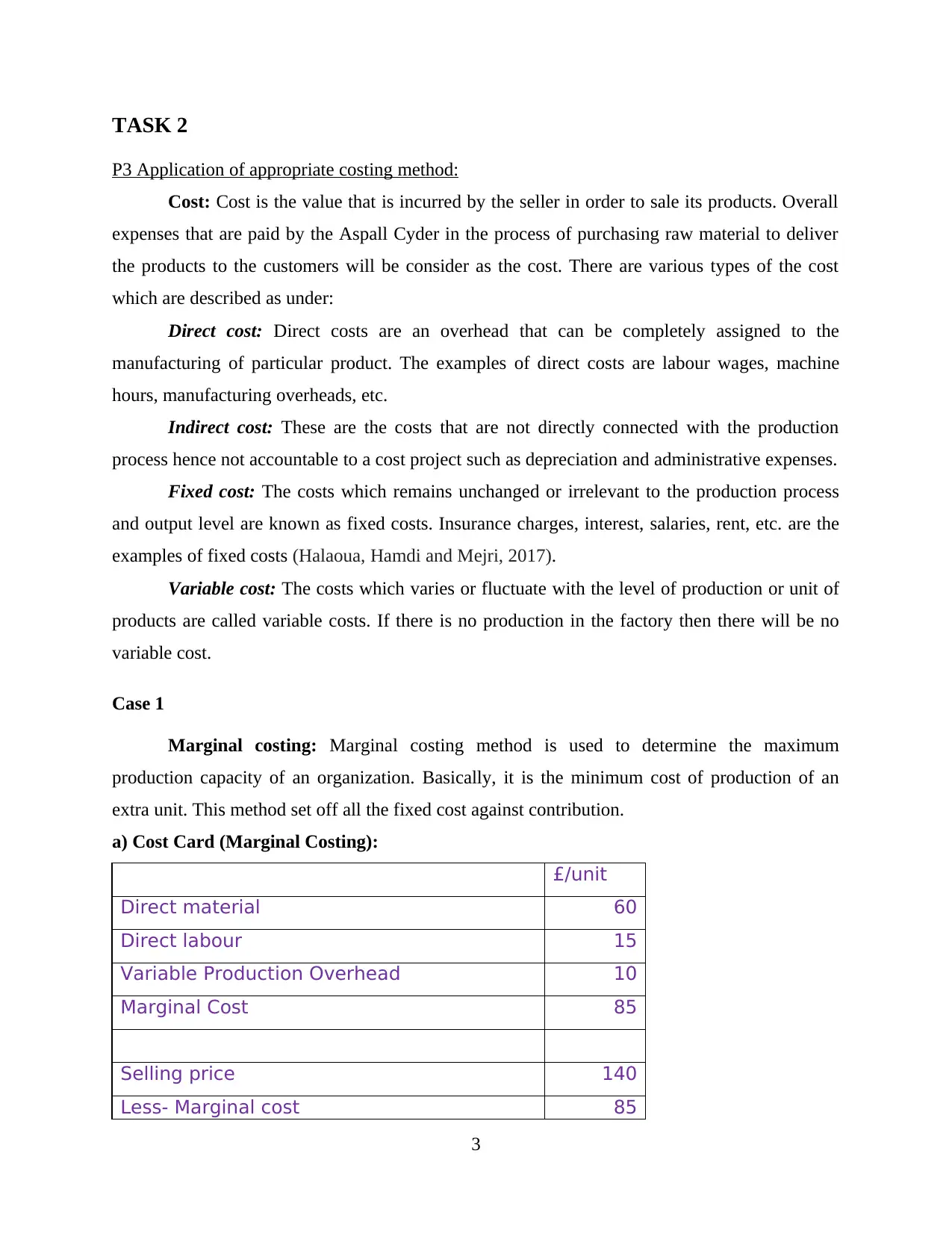

Case 1

Marginal costing: Marginal costing method is used to determine the maximum

production capacity of an organization. Basically, it is the minimum cost of production of an

extra unit. This method set off all the fixed cost against contribution.

a) Cost Card (Marginal Costing):

£/unit

Direct material 60

Direct labour 15

Variable Production Overhead 10

Marginal Cost 85

Selling price 140

Less- Marginal cost 85

3

P3 Application of appropriate costing method:

Cost: Cost is the value that is incurred by the seller in order to sale its products. Overall

expenses that are paid by the Aspall Cyder in the process of purchasing raw material to deliver

the products to the customers will be consider as the cost. There are various types of the cost

which are described as under:

Direct cost: Direct costs are an overhead that can be completely assigned to the

manufacturing of particular product. The examples of direct costs are labour wages, machine

hours, manufacturing overheads, etc.

Indirect cost: These are the costs that are not directly connected with the production

process hence not accountable to a cost project such as depreciation and administrative expenses.

Fixed cost: The costs which remains unchanged or irrelevant to the production process

and output level are known as fixed costs. Insurance charges, interest, salaries, rent, etc. are the

examples of fixed costs (Halaoua, Hamdi and Mejri, 2017).

Variable cost: The costs which varies or fluctuate with the level of production or unit of

products are called variable costs. If there is no production in the factory then there will be no

variable cost.

Case 1

Marginal costing: Marginal costing method is used to determine the maximum

production capacity of an organization. Basically, it is the minimum cost of production of an

extra unit. This method set off all the fixed cost against contribution.

a) Cost Card (Marginal Costing):

£/unit

Direct material 60

Direct labour 15

Variable Production Overhead 10

Marginal Cost 85

Selling price 140

Less- Marginal cost 85

3

Contribution / Profit margin 55

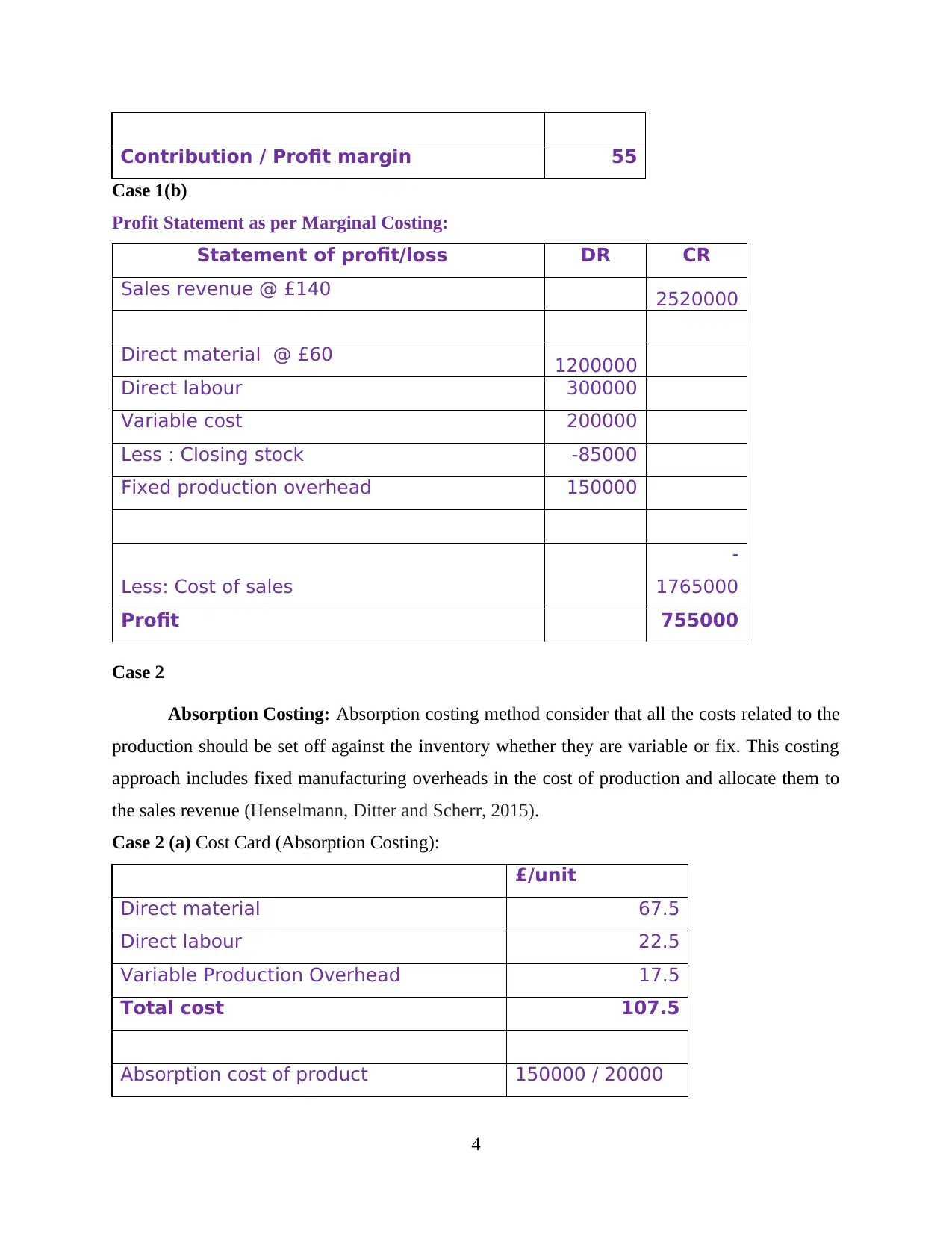

Case 1(b)

Profit Statement as per Marginal Costing:

Statement of profit/loss DR CR

Sales revenue @ £140 2520000

Direct material @ £60 1200000

Direct labour 300000

Variable cost 200000

Less : Closing stock -85000

Fixed production overhead 150000

Less: Cost of sales

-

1765000

Profit 755000

Case 2

Absorption Costing: Absorption costing method consider that all the costs related to the

production should be set off against the inventory whether they are variable or fix. This costing

approach includes fixed manufacturing overheads in the cost of production and allocate them to

the sales revenue (Henselmann, Ditter and Scherr, 2015).

Case 2 (a) Cost Card (Absorption Costing):

£/unit

Direct material 67.5

Direct labour 22.5

Variable Production Overhead 17.5

Total cost 107.5

Absorption cost of product 150000 / 20000

4

Case 1(b)

Profit Statement as per Marginal Costing:

Statement of profit/loss DR CR

Sales revenue @ £140 2520000

Direct material @ £60 1200000

Direct labour 300000

Variable cost 200000

Less : Closing stock -85000

Fixed production overhead 150000

Less: Cost of sales

-

1765000

Profit 755000

Case 2

Absorption Costing: Absorption costing method consider that all the costs related to the

production should be set off against the inventory whether they are variable or fix. This costing

approach includes fixed manufacturing overheads in the cost of production and allocate them to

the sales revenue (Henselmann, Ditter and Scherr, 2015).

Case 2 (a) Cost Card (Absorption Costing):

£/unit

Direct material 67.5

Direct labour 22.5

Variable Production Overhead 17.5

Total cost 107.5

Absorption cost of product 150000 / 20000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 7.5

Selling price 140

Less- Total cost 107.5

Gross Profit 32.5

Profit Statement as per Absorption Costing:

Particulars DR CR

Sales revenue

252000

0

Variable cost

Direct material 1350000

Direct labour 450000

Lees: Closing inventory -107500

1692500

Fixed production overheads 150000

Less: Cost of sales

-

184250

0

Profit 677500

Reconciliation Statement:

Between marginal costing and absorption costing £

Profit as per marginal costing 755000

Increase in stock level

Marginal cost/unit

Absorption cost/unit

Difference -77500

Profit as per absorption costing 677500

5

Selling price 140

Less- Total cost 107.5

Gross Profit 32.5

Profit Statement as per Absorption Costing:

Particulars DR CR

Sales revenue

252000

0

Variable cost

Direct material 1350000

Direct labour 450000

Lees: Closing inventory -107500

1692500

Fixed production overheads 150000

Less: Cost of sales

-

184250

0

Profit 677500

Reconciliation Statement:

Between marginal costing and absorption costing £

Profit as per marginal costing 755000

Increase in stock level

Marginal cost/unit

Absorption cost/unit

Difference -77500

Profit as per absorption costing 677500

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

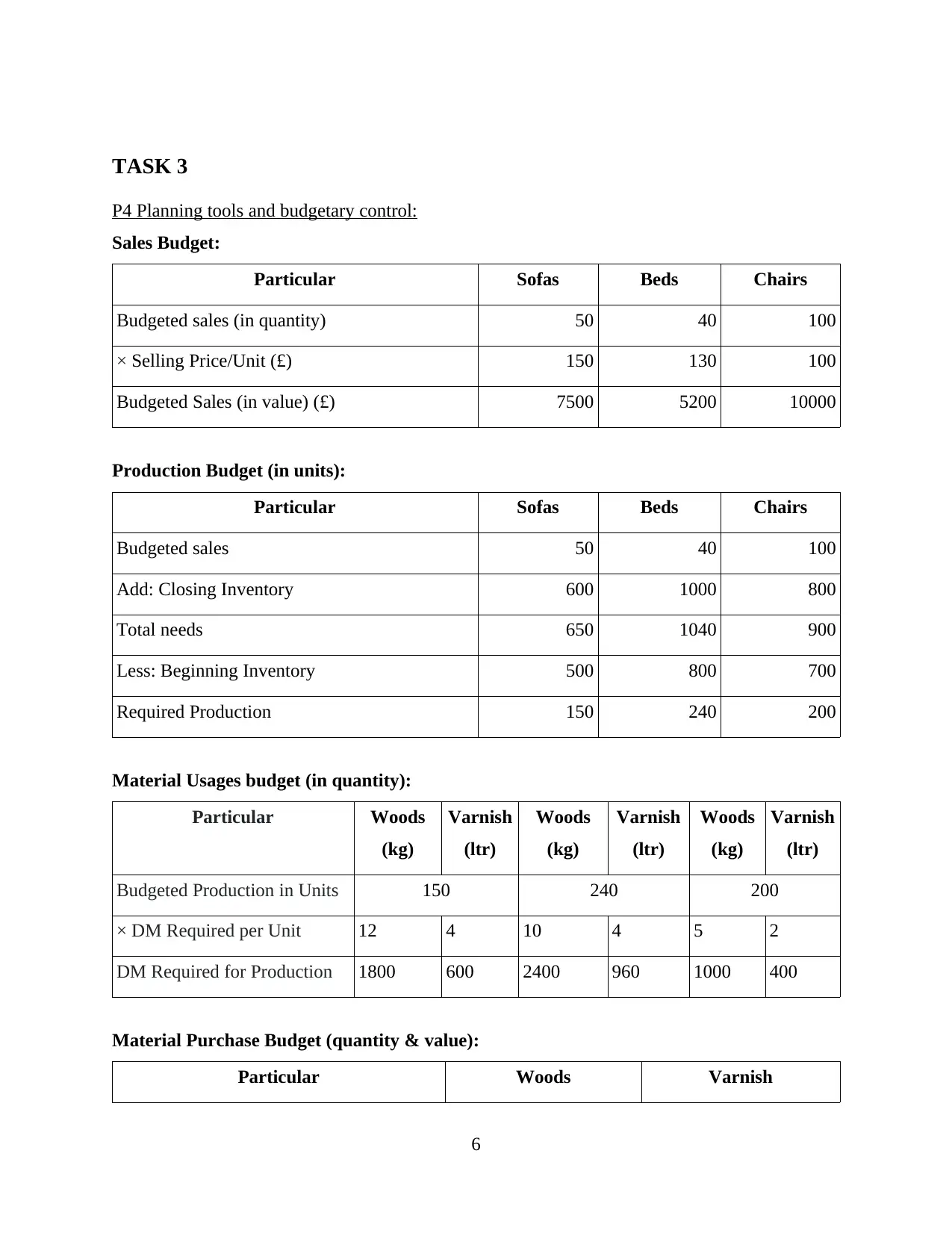

P4 Planning tools and budgetary control:

Sales Budget:

Particular Sofas Beds Chairs

Budgeted sales (in quantity) 50 40 100

× Selling Price/Unit (£) 150 130 100

Budgeted Sales (in value) (£) 7500 5200 10000

Production Budget (in units):

Particular Sofas Beds Chairs

Budgeted sales 50 40 100

Add: Closing Inventory 600 1000 800

Total needs 650 1040 900

Less: Beginning Inventory 500 800 700

Required Production 150 240 200

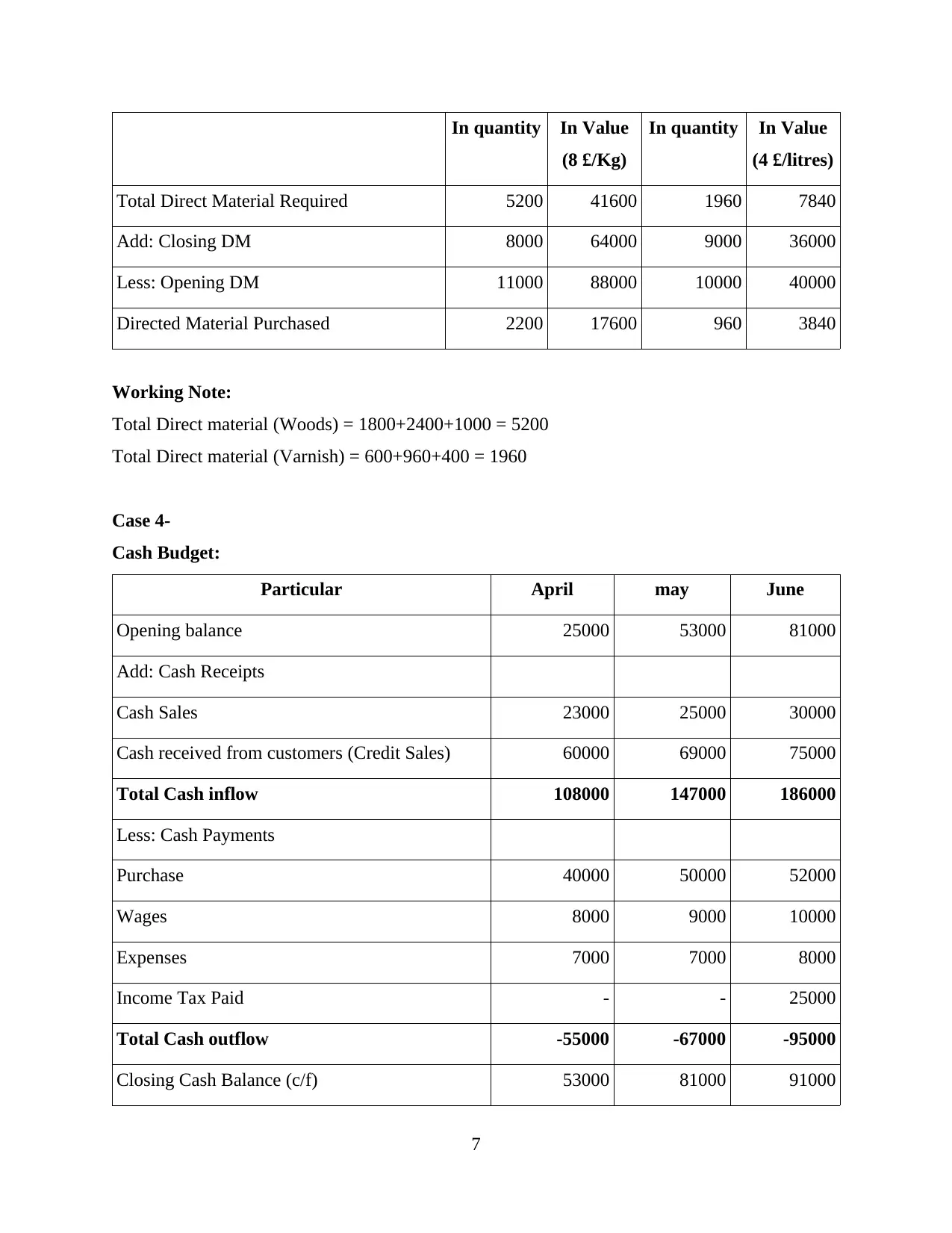

Material Usages budget (in quantity):

Particular Woods

(kg)

Varnish

(ltr)

Woods

(kg)

Varnish

(ltr)

Woods

(kg)

Varnish

(ltr)

Budgeted Production in Units 150 240 200

× DM Required per Unit 12 4 10 4 5 2

DM Required for Production 1800 600 2400 960 1000 400

Material Purchase Budget (quantity & value):

Particular Woods Varnish

6

P4 Planning tools and budgetary control:

Sales Budget:

Particular Sofas Beds Chairs

Budgeted sales (in quantity) 50 40 100

× Selling Price/Unit (£) 150 130 100

Budgeted Sales (in value) (£) 7500 5200 10000

Production Budget (in units):

Particular Sofas Beds Chairs

Budgeted sales 50 40 100

Add: Closing Inventory 600 1000 800

Total needs 650 1040 900

Less: Beginning Inventory 500 800 700

Required Production 150 240 200

Material Usages budget (in quantity):

Particular Woods

(kg)

Varnish

(ltr)

Woods

(kg)

Varnish

(ltr)

Woods

(kg)

Varnish

(ltr)

Budgeted Production in Units 150 240 200

× DM Required per Unit 12 4 10 4 5 2

DM Required for Production 1800 600 2400 960 1000 400

Material Purchase Budget (quantity & value):

Particular Woods Varnish

6

In quantity In Value

(8 £/Kg)

In quantity In Value

(4 £/litres)

Total Direct Material Required 5200 41600 1960 7840

Add: Closing DM 8000 64000 9000 36000

Less: Opening DM 11000 88000 10000 40000

Directed Material Purchased 2200 17600 960 3840

Working Note:

Total Direct material (Woods) = 1800+2400+1000 = 5200

Total Direct material (Varnish) = 600+960+400 = 1960

Case 4-

Cash Budget:

Particular April may June

Opening balance 25000 53000 81000

Add: Cash Receipts

Cash Sales 23000 25000 30000

Cash received from customers (Credit Sales) 60000 69000 75000

Total Cash inflow 108000 147000 186000

Less: Cash Payments

Purchase 40000 50000 52000

Wages 8000 9000 10000

Expenses 7000 7000 8000

Income Tax Paid - - 25000

Total Cash outflow -55000 -67000 -95000

Closing Cash Balance (c/f) 53000 81000 91000

7

(8 £/Kg)

In quantity In Value

(4 £/litres)

Total Direct Material Required 5200 41600 1960 7840

Add: Closing DM 8000 64000 9000 36000

Less: Opening DM 11000 88000 10000 40000

Directed Material Purchased 2200 17600 960 3840

Working Note:

Total Direct material (Woods) = 1800+2400+1000 = 5200

Total Direct material (Varnish) = 600+960+400 = 1960

Case 4-

Cash Budget:

Particular April may June

Opening balance 25000 53000 81000

Add: Cash Receipts

Cash Sales 23000 25000 30000

Cash received from customers (Credit Sales) 60000 69000 75000

Total Cash inflow 108000 147000 186000

Less: Cash Payments

Purchase 40000 50000 52000

Wages 8000 9000 10000

Expenses 7000 7000 8000

Income Tax Paid - - 25000

Total Cash outflow -55000 -67000 -95000

Closing Cash Balance (c/f) 53000 81000 91000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

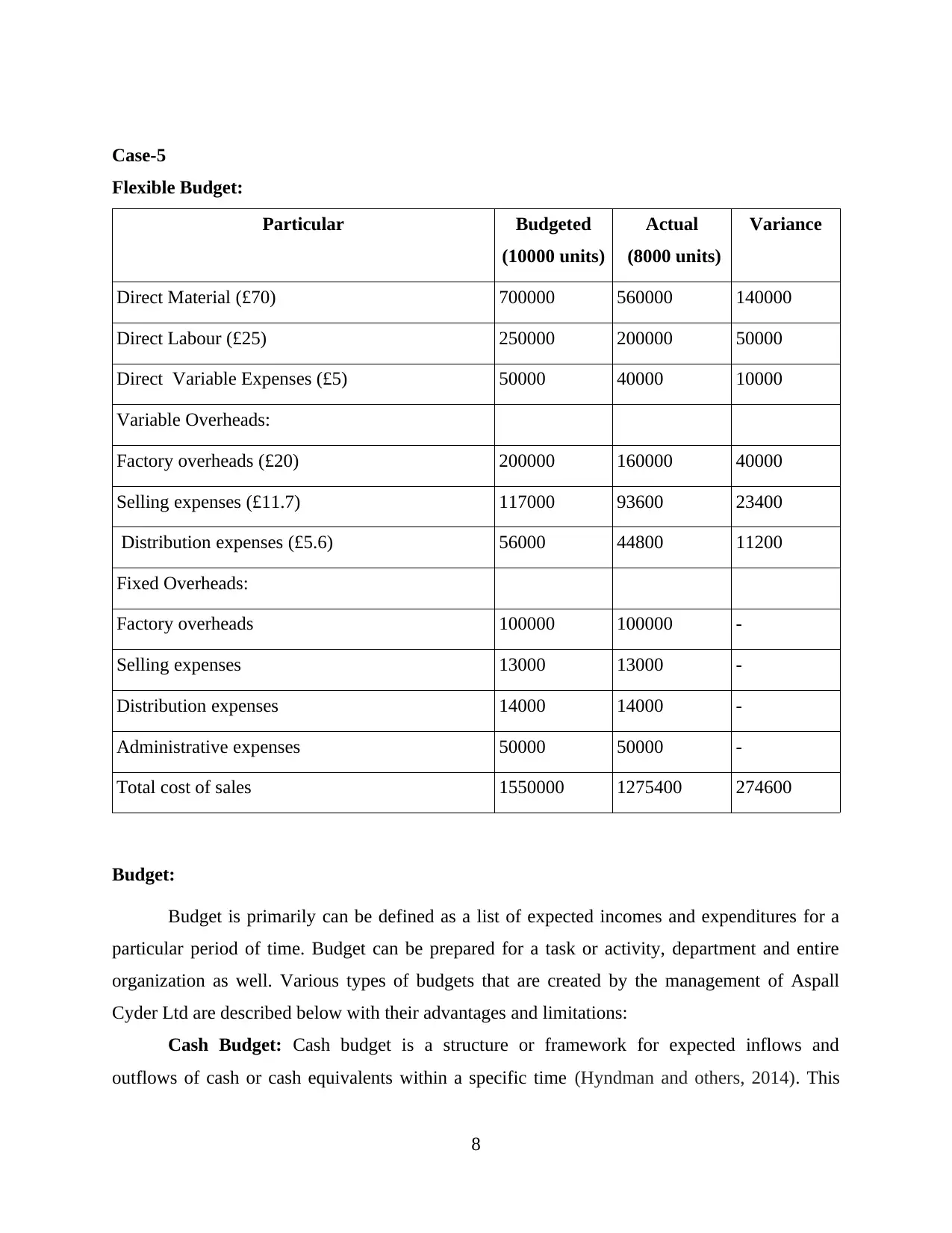

Case-5

Flexible Budget:

Particular Budgeted

(10000 units)

Actual

(8000 units)

Variance

Direct Material (£70) 700000 560000 140000

Direct Labour (£25) 250000 200000 50000

Direct Variable Expenses (£5) 50000 40000 10000

Variable Overheads:

Factory overheads (£20) 200000 160000 40000

Selling expenses (£11.7) 117000 93600 23400

Distribution expenses (£5.6) 56000 44800 11200

Fixed Overheads:

Factory overheads 100000 100000 -

Selling expenses 13000 13000 -

Distribution expenses 14000 14000 -

Administrative expenses 50000 50000 -

Total cost of sales 1550000 1275400 274600

Budget:

Budget is primarily can be defined as a list of expected incomes and expenditures for a

particular period of time. Budget can be prepared for a task or activity, department and entire

organization as well. Various types of budgets that are created by the management of Aspall

Cyder Ltd are described below with their advantages and limitations:

Cash Budget: Cash budget is a structure or framework for expected inflows and

outflows of cash or cash equivalents within a specific time (Hyndman and others, 2014). This

8

Flexible Budget:

Particular Budgeted

(10000 units)

Actual

(8000 units)

Variance

Direct Material (£70) 700000 560000 140000

Direct Labour (£25) 250000 200000 50000

Direct Variable Expenses (£5) 50000 40000 10000

Variable Overheads:

Factory overheads (£20) 200000 160000 40000

Selling expenses (£11.7) 117000 93600 23400

Distribution expenses (£5.6) 56000 44800 11200

Fixed Overheads:

Factory overheads 100000 100000 -

Selling expenses 13000 13000 -

Distribution expenses 14000 14000 -

Administrative expenses 50000 50000 -

Total cost of sales 1550000 1275400 274600

Budget:

Budget is primarily can be defined as a list of expected incomes and expenditures for a

particular period of time. Budget can be prepared for a task or activity, department and entire

organization as well. Various types of budgets that are created by the management of Aspall

Cyder Ltd are described below with their advantages and limitations:

Cash Budget: Cash budget is a structure or framework for expected inflows and

outflows of cash or cash equivalents within a specific time (Hyndman and others, 2014). This

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budget helps the management of respective firm in managing and planning for availability of

funds regarding daily transactions.

Advantages:

This budget helps in avoiding access holding of cash and investing it into other

productive activities.

Cash budget allows the management to forecast its annual expenses and costs along with

revenues and profitability.

Disadvantages:

The profit or net income disclosed by this budget does not provide true image of the

organizational profit.

This budget only consider cash transactions only and omit non-financial activities which

may be materialistic for the management.

Capital Budget: Capital budget is prepared to determine and measure potential

investments or expenses that may be huge in nature. It considers the purchase of fixed assets,

income from sale of old assets, payment of loans and debentures, etc.

Advantages:

It helps in making decision regarding huge investments whether they are profitable or

not.

This budget is also helpful in influencing the creditors, capitalists, bankers and other

external stakeholders.

Disadvantages:

Estimation of accurate and true value of the asset is difficult and time consuming and also

needs expertise.

Decision based on capital budget are for long-term and irreversible which may be wrong

because of inappropriate estimations.

Operating Budget: Operating budget is prepared to estimate the income and

expenditures related to the day-to-day transactions for a particular period which is normally one

year. Sales budget is the most important for preparing operating budget (Libby and Salterio,

2017).

Advantages:

9

funds regarding daily transactions.

Advantages:

This budget helps in avoiding access holding of cash and investing it into other

productive activities.

Cash budget allows the management to forecast its annual expenses and costs along with

revenues and profitability.

Disadvantages:

The profit or net income disclosed by this budget does not provide true image of the

organizational profit.

This budget only consider cash transactions only and omit non-financial activities which

may be materialistic for the management.

Capital Budget: Capital budget is prepared to determine and measure potential

investments or expenses that may be huge in nature. It considers the purchase of fixed assets,

income from sale of old assets, payment of loans and debentures, etc.

Advantages:

It helps in making decision regarding huge investments whether they are profitable or

not.

This budget is also helpful in influencing the creditors, capitalists, bankers and other

external stakeholders.

Disadvantages:

Estimation of accurate and true value of the asset is difficult and time consuming and also

needs expertise.

Decision based on capital budget are for long-term and irreversible which may be wrong

because of inappropriate estimations.

Operating Budget: Operating budget is prepared to estimate the income and

expenditures related to the day-to-day transactions for a particular period which is normally one

year. Sales budget is the most important for preparing operating budget (Libby and Salterio,

2017).

Advantages:

9

Short term operations and goals can easily be maintained with the help of operating

budget.

Operating budget id helpful in maintaining the flexibility and addressing the variables

within the organizations.

Disadvantages:

This budget is time consuming as it includes all size of transactions and operations and

also provide detailed description.

The changes of being more inaccurate in estimations are more in this budget as changes

take place rapidly.

Alternative methods of budget:

Zero-based Budget: This method of budgeting is an approach to prepare without

scratching previous budgets which means it is prepared with the zero value for each cost centre

and defined every increment in the cost. This budget method helps in avoiding irrelevant costs

and justify each expanse (Nwogugu, 2015).

Activity-based budget: This method of budgeting examines the strength and efficiency

of individuals' activities and their contributions to organization and then provide and assign

budget according to their given ranks or priorities.

Behavioural implications of budget:

Budgetary Slack: Budgetary slack can be defined as padding or cushioning activities

with the budget. When there is a continuous underestimation of revenues or overestimation of

expenses take place in the budget then the managers start to window dressing on the budget. This

practise take place when upper management do not pay attention towards deliberate mismatching

of the budget.

Participative budgeting: It has been seen that when managers and other key employees

are taken into consideration in the process of budget making, it increases their moral and

budgetary targets can be achieved with more efficiency and effectively. Participative budgeting

impacts positively on the performance of overall organization.

10

budget.

Operating budget id helpful in maintaining the flexibility and addressing the variables

within the organizations.

Disadvantages:

This budget is time consuming as it includes all size of transactions and operations and

also provide detailed description.

The changes of being more inaccurate in estimations are more in this budget as changes

take place rapidly.

Alternative methods of budget:

Zero-based Budget: This method of budgeting is an approach to prepare without

scratching previous budgets which means it is prepared with the zero value for each cost centre

and defined every increment in the cost. This budget method helps in avoiding irrelevant costs

and justify each expanse (Nwogugu, 2015).

Activity-based budget: This method of budgeting examines the strength and efficiency

of individuals' activities and their contributions to organization and then provide and assign

budget according to their given ranks or priorities.

Behavioural implications of budget:

Budgetary Slack: Budgetary slack can be defined as padding or cushioning activities

with the budget. When there is a continuous underestimation of revenues or overestimation of

expenses take place in the budget then the managers start to window dressing on the budget. This

practise take place when upper management do not pay attention towards deliberate mismatching

of the budget.

Participative budgeting: It has been seen that when managers and other key employees

are taken into consideration in the process of budget making, it increases their moral and

budgetary targets can be achieved with more efficiency and effectively. Participative budgeting

impacts positively on the performance of overall organization.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.