Management Accounting Report: Analysis of MAS and Financial Reports

VerifiedAdded on 2023/01/11

|22

|5488

|27

Report

AI Summary

This report delves into the core concepts of management accounting, exploring its role in recognizing, analyzing, and generating financial data for informed managerial decisions. It uses Creams Ltd as a case study to illustrate the application of various Management Accounting Systems (MAS), including inventory management, cost accounting, and pricing optimization systems. The report explains different methods used for management accounting reporting, such as inventory management reports, performance reports, and cost accounting reports. It also evaluates the advantages of management accounting and its integration with organizational processes. Furthermore, the report presents a detailed comparison between absorption and marginal costing methods, including income statement calculations. The report covers planning tools like budgetary control, and how management accounting addresses financial problems. The report concludes with a discussion on how businesses can use management accounting systems to solve financial issues.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1. Management accounting and essential requirement of these systems............................................3

P2 Explanation of various methods used for management accounting reporting...................................5

M1.Evaluation of advantages of management accounting......................................................................5

D1. Integration with the organisational process of management accounting system and reporting......6

TASK 2..........................................................................................................................................................6

P3.Calculation of income statements by using absorption and marginal costing approach:...................6

M2.Application of various range of MAS techniques for production of financial reporting documents:

...............................................................................................................................................................10

D2.Interpretation of financial reports i.e. income statements..............................................................11

TASK 3........................................................................................................................................................11

P4. Benefits and drawback of planning tools of budgetary control.......................................................11

M3. Various planning tools for preparing and forecasting the budgets................................................12

TASK 4........................................................................................................................................................12

P5. Management accounting system to solve the financial problems...................................................12

M4. Management accounting in solving the financial problems...........................................................14

D3. Planning tools in response to solve the financial issues..................................................................14

CONCLUSION.............................................................................................................................................15

REFERENCES..............................................................................................................................................16

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1. Management accounting and essential requirement of these systems............................................3

P2 Explanation of various methods used for management accounting reporting...................................5

M1.Evaluation of advantages of management accounting......................................................................5

D1. Integration with the organisational process of management accounting system and reporting......6

TASK 2..........................................................................................................................................................6

P3.Calculation of income statements by using absorption and marginal costing approach:...................6

M2.Application of various range of MAS techniques for production of financial reporting documents:

...............................................................................................................................................................10

D2.Interpretation of financial reports i.e. income statements..............................................................11

TASK 3........................................................................................................................................................11

P4. Benefits and drawback of planning tools of budgetary control.......................................................11

M3. Various planning tools for preparing and forecasting the budgets................................................12

TASK 4........................................................................................................................................................12

P5. Management accounting system to solve the financial problems...................................................12

M4. Management accounting in solving the financial problems...........................................................14

D3. Planning tools in response to solve the financial issues..................................................................14

CONCLUSION.............................................................................................................................................15

REFERENCES..............................................................................................................................................16

INTRODUCTION

Management accounting is a procedure of recognizing, analyzing, recording and

generating financial data that will be beneficial for managers to make informed decision about

the activities of the corporation. The business can use the management accounting system

(MAS) in the fields of budget preparation, decision-making, measuring efficiency etc. It will

offer the managers within an organization with monetary and also non - monetary to increase

the efficiency and effectiveness of its labor force. MAS 'main goal is to frame overarching

goals, create long term plans, and distribute wealth within an organization (Strauss, Kristandl

and Quinn, 2015).

To better understand of this report selected Creams Ltd which is dealing into ice creams,

waffles and other things. This study describes the concept management accounting and

numerous kinds of MAS together with different approaches which an organization may use for

external reporting. Different advantages that a corporation can receive by the use of MAS are

also described together with different project resources that an organization can use to manage

its expenditure using its management techniques. This report presents a comparison between

two organizations on how businesses embrace financial accounting systems to address their

money difficulties.

TASK 1

P1. Management accounting and essential requirement of these systems.

Management accounting: Management accounting is described as incorporating the

relationship into managerial decisions, departmental efficiency measurement and management

systems and offering economic monitoring and analysis resources to appropriate actions in

formulating and implementing a business vision.

Management accounting system: Accounting management systems are part of internal

management. It is used to get the administration with essential details that can be used in

routine business decision-making. A production department will use these methods to support

in the going to cost and management of their procedure. Such as, Creams Ltd use these systems

in order to analysis of different systems in appropriate manner. There are discussed various

systems in broad manner such as:

Inventory management system: This is a type of accounting method associated with

the management of production costs and also the efficient volume assessment of inventory. This

accounting scheme essentially provides the corporations with a process for assessing total

Management accounting is a procedure of recognizing, analyzing, recording and

generating financial data that will be beneficial for managers to make informed decision about

the activities of the corporation. The business can use the management accounting system

(MAS) in the fields of budget preparation, decision-making, measuring efficiency etc. It will

offer the managers within an organization with monetary and also non - monetary to increase

the efficiency and effectiveness of its labor force. MAS 'main goal is to frame overarching

goals, create long term plans, and distribute wealth within an organization (Strauss, Kristandl

and Quinn, 2015).

To better understand of this report selected Creams Ltd which is dealing into ice creams,

waffles and other things. This study describes the concept management accounting and

numerous kinds of MAS together with different approaches which an organization may use for

external reporting. Different advantages that a corporation can receive by the use of MAS are

also described together with different project resources that an organization can use to manage

its expenditure using its management techniques. This report presents a comparison between

two organizations on how businesses embrace financial accounting systems to address their

money difficulties.

TASK 1

P1. Management accounting and essential requirement of these systems.

Management accounting: Management accounting is described as incorporating the

relationship into managerial decisions, departmental efficiency measurement and management

systems and offering economic monitoring and analysis resources to appropriate actions in

formulating and implementing a business vision.

Management accounting system: Accounting management systems are part of internal

management. It is used to get the administration with essential details that can be used in

routine business decision-making. A production department will use these methods to support

in the going to cost and management of their procedure. Such as, Creams Ltd use these systems

in order to analysis of different systems in appropriate manner. There are discussed various

systems in broad manner such as:

Inventory management system: This is a type of accounting method associated with

the management of production costs and also the efficient volume assessment of inventory. This

accounting scheme essentially provides the corporations with a process for assessing total

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

inventory levels of factories that can be raw materials or manufactured goods. In other words, it

is important to stay as long as possible of the costs of inventory levels within command. They

use this accounting method in the form of Creams limited company and it assists them in

managing the process of purchasing the content. In addition, to taking decisions on the requisite

raw materials and beverage manufacturing (Spraakman, O'Grady, Askarany and Akroyd, 2015).

Essential requirement: This is essential for the business, because it comes with the

coordinated management of the goods and the ethical behaviour of all operations. It also means

that all goods are handled by the producer to meet customer demands.

Cost accounting system: The particular accounting system can be described as a

type of accounting system that is connected to documenting the costs of the overall process of

switching raw materials into finished products. This accounting system is primarily tailored to

the production companies. That is why since there are a broad variety of operations in the

industrial firms, and it is critical that their executives have full cost records. It is important to

monitor operating expenses as well as other operations. As regards Creams Limited Company,

their administrator is using this approach to monitor track of the price of buying raw resources

such as sugar, fruits etc.

Essential requirement: The essential requirement of cost accounting techniques

because it helps managers to determine the real expense of all activities. Based on it, the above-

mentioned company's financial agency keeping the costs of different types of activities as much

relatively low as feasible. It is also important for the identification of costs of different kinds of

activities, namely direct costs, associated costs etc.

Price optimization system: This accounting method is concerned with the

effective establishment of the costs of goods and facilities, so that profits can improve. Together

with this accounting plays a vital role in assessing the response of consumers to various pricing

trends. The price management method is therefore important to set the cost of goods and

services that will help to market the products more effectively. Also in the chosen organization

above, they are using this accounting method innocently restricted. This provides them with

details on the reaction of consumers to different demand trends and thus fixes the demand of

their beverages.

Essential requirement: The requirement of this system to supervisors can maximize

their income by giving the necessary price for all the sale of its products. This will also help the

company to decide whether it can satisfy all of its priorities by seeking the best value on the

goods it sells.

is important to stay as long as possible of the costs of inventory levels within command. They

use this accounting method in the form of Creams limited company and it assists them in

managing the process of purchasing the content. In addition, to taking decisions on the requisite

raw materials and beverage manufacturing (Spraakman, O'Grady, Askarany and Akroyd, 2015).

Essential requirement: This is essential for the business, because it comes with the

coordinated management of the goods and the ethical behaviour of all operations. It also means

that all goods are handled by the producer to meet customer demands.

Cost accounting system: The particular accounting system can be described as a

type of accounting system that is connected to documenting the costs of the overall process of

switching raw materials into finished products. This accounting system is primarily tailored to

the production companies. That is why since there are a broad variety of operations in the

industrial firms, and it is critical that their executives have full cost records. It is important to

monitor operating expenses as well as other operations. As regards Creams Limited Company,

their administrator is using this approach to monitor track of the price of buying raw resources

such as sugar, fruits etc.

Essential requirement: The essential requirement of cost accounting techniques

because it helps managers to determine the real expense of all activities. Based on it, the above-

mentioned company's financial agency keeping the costs of different types of activities as much

relatively low as feasible. It is also important for the identification of costs of different kinds of

activities, namely direct costs, associated costs etc.

Price optimization system: This accounting method is concerned with the

effective establishment of the costs of goods and facilities, so that profits can improve. Together

with this accounting plays a vital role in assessing the response of consumers to various pricing

trends. The price management method is therefore important to set the cost of goods and

services that will help to market the products more effectively. Also in the chosen organization

above, they are using this accounting method innocently restricted. This provides them with

details on the reaction of consumers to different demand trends and thus fixes the demand of

their beverages.

Essential requirement: The requirement of this system to supervisors can maximize

their income by giving the necessary price for all the sale of its products. This will also help the

company to decide whether it can satisfy all of its priorities by seeking the best value on the

goods it sells.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: This accountability method can be described as a cost assessment process

incurred in specific live performances. Including this accounting method, there is a wide range

of information about the costs listed above, including such:

Direct labor- The structure for job costing contains estimates of the cost of hiring labor to

handle multiple tasks in the organization.

Direct Material- provides information on overall spending on the purchase of direct technology

for the synthesis of product lines and also this financial accounting (Armitage, Webb and Glynn

2016).

Overhead- This reporting method contains details about certain other expenses in addition to

these details relating labor and materials.

Essential requirement: The essential requirement of job costing system to incredibly

valuable costing mechanism for job orders because it could be used to meet the needs of

customers effectively. In reality, it will also be obtaining business objectives like better profits

and extremely satisfied consumers.

Thus this management accounting provides these all the details. It is important to provide in-

depth estimates of the cost of work in any given operations. Similar to the above-mentioned

Creams Limited Company, they use this accounting method to help them efficiently determine

how much expenses are required to spend in employment.

Therefore these are the forms of accounting management system and each reporting system has

its own value and important necessity for the businesses.

P2 Explanation of various methods used for management accounting reporting.

Managerial accounting reports can be described as there’re providing all the detailed

knowledge to the administrators. Along with, presented the company's financial and non

financial details. The aim of such documents is to remind supervisors of all of the corporation's

monetary and non - monetary transactions which have become the foundation for inner

planning and policy decisions. Creams limited, the aforementioned company, generate some

other type of reports that are useful to them and in business decisions Budding, Grossi and

Tagesson, 2014). All the reports are mentioned below:

Inventory management report: There are forms of documents which are related to the

provision of inventory data presented in factories and also overall costs that arise during the

inventory storage procedure. Industries could get an awareness regarding coherent system of

their accessible raw resources and ready products with the aid of this study. As regards all

incurred in specific live performances. Including this accounting method, there is a wide range

of information about the costs listed above, including such:

Direct labor- The structure for job costing contains estimates of the cost of hiring labor to

handle multiple tasks in the organization.

Direct Material- provides information on overall spending on the purchase of direct technology

for the synthesis of product lines and also this financial accounting (Armitage, Webb and Glynn

2016).

Overhead- This reporting method contains details about certain other expenses in addition to

these details relating labor and materials.

Essential requirement: The essential requirement of job costing system to incredibly

valuable costing mechanism for job orders because it could be used to meet the needs of

customers effectively. In reality, it will also be obtaining business objectives like better profits

and extremely satisfied consumers.

Thus this management accounting provides these all the details. It is important to provide in-

depth estimates of the cost of work in any given operations. Similar to the above-mentioned

Creams Limited Company, they use this accounting method to help them efficiently determine

how much expenses are required to spend in employment.

Therefore these are the forms of accounting management system and each reporting system has

its own value and important necessity for the businesses.

P2 Explanation of various methods used for management accounting reporting.

Managerial accounting reports can be described as there’re providing all the detailed

knowledge to the administrators. Along with, presented the company's financial and non

financial details. The aim of such documents is to remind supervisors of all of the corporation's

monetary and non - monetary transactions which have become the foundation for inner

planning and policy decisions. Creams limited, the aforementioned company, generate some

other type of reports that are useful to them and in business decisions Budding, Grossi and

Tagesson, 2014). All the reports are mentioned below:

Inventory management report: There are forms of documents which are related to the

provision of inventory data presented in factories and also overall costs that arise during the

inventory storage procedure. Industries could get an awareness regarding coherent system of

their accessible raw resources and ready products with the aid of this study. As regards all

above Creams limited company, they are preparing this report which provides data on the

number of raw resources obtainable in their distribution centre, including such berries, fruit

juice etc. In addition to this, it is often useful for them to gain details about how many packaged

drinks are accessible as well as on the strength of which they determine for potential

manufacturing.

Performance report: Even as title accompanies, these could be described as any type of

reporting related to offering feedback on the effectiveness of different things and persons. They

generate this document, like in the previous section-mentioned organisation, that also helps

them evaluate the quality among all their business transactions and workers specializing in

multiple actions. This document mainly helps in monitoring and tracking organization system

effectiveness (Edwards, 2013).

Cost accounting report: It may be identified as a sort of study associated with the

provision of accounting data for different types of options. Through the aid of these studies,

businesses will be informed of just how much expense their activities have to incur. Together

with this study analyze the cost-effectiveness of all operations. For example, they generate this

document in and then Creams limited company with the intention of having accurate data about

the amount of their activities. As well as costs for the procurement of raw resources, payments

for supplies, leases, salaries for workers, etc.

M1.Evaluation of advantages of management accounting

Growing management accounting systems has its own position in the works of different

processes and tasks. Many of the benefits of financial management as continue to follow:

Management accounting

system

Benefits

Inventory management

system

This method is related to the effective supervision of the

manufactured goods volume and completed goods. As in the

office documents above, Creams Ltd have restricted their

monitoring of their inventory records.

Price optimisation system This accounting system basically implementation is focused on

allocating the price of their goods and services. This accounting

system supports to assess the costs based on customer response in

the Creams limited business.

Cost accounting system This accounting method is useful in calculating the range of

different operations that are carried out on a regular basis. The

number of raw resources obtainable in their distribution centre, including such berries, fruit

juice etc. In addition to this, it is often useful for them to gain details about how many packaged

drinks are accessible as well as on the strength of which they determine for potential

manufacturing.

Performance report: Even as title accompanies, these could be described as any type of

reporting related to offering feedback on the effectiveness of different things and persons. They

generate this document, like in the previous section-mentioned organisation, that also helps

them evaluate the quality among all their business transactions and workers specializing in

multiple actions. This document mainly helps in monitoring and tracking organization system

effectiveness (Edwards, 2013).

Cost accounting report: It may be identified as a sort of study associated with the

provision of accounting data for different types of options. Through the aid of these studies,

businesses will be informed of just how much expense their activities have to incur. Together

with this study analyze the cost-effectiveness of all operations. For example, they generate this

document in and then Creams limited company with the intention of having accurate data about

the amount of their activities. As well as costs for the procurement of raw resources, payments

for supplies, leases, salaries for workers, etc.

M1.Evaluation of advantages of management accounting

Growing management accounting systems has its own position in the works of different

processes and tasks. Many of the benefits of financial management as continue to follow:

Management accounting

system

Benefits

Inventory management

system

This method is related to the effective supervision of the

manufactured goods volume and completed goods. As in the

office documents above, Creams Ltd have restricted their

monitoring of their inventory records.

Price optimisation system This accounting system basically implementation is focused on

allocating the price of their goods and services. This accounting

system supports to assess the costs based on customer response in

the Creams limited business.

Cost accounting system This accounting method is useful in calculating the range of

different operations that are carried out on a regular basis. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost accounting system assists them in presenting cost information

as regards the Creams limited company part. Including a way of

efficiently allocating the budget so that expenses can be cut.

D1. Integration with the organisational process of management accounting system and reporting

It is accurate says that the accounts management system is connected to the organizational

cycle. Like in the above-mentioned business, innocent drinks are restricted they have different

aspects of financial systems and every one of them is connected to their operating method. For

instance, the cost accounting framework is relevant to financial capital being best distributed.

Like other accounting systems, the organizational method is similar. Although these documents

are also consistent with the framework from the above management team in the management

accounting performance element. Like the article on inventory management, it is connected

with the efficient management of their existing resources.

TASK 2

P3.Calculation of income statements by using absorption and marginal costing approach:

Different strategies exist for planning an organization's financial statements including

such gross expense, absorption costing, and so on. The description of these two methods is

mentioned in detail as continues to follow:

Absorption costing: It is a form of management accounting for the planning of the statements

of profits, where all the expenditures associated with manufacturing is allocated to the quantity

manufactured. In many other terms, besides all variable cost of production, the fixed cost of

production is often used throughout measuring cost of the product.

Marginal Costing: In this process, the business shall accept only adjustable production costs in

the manufacture of a particular item, and then all manufactured costs associated with fixed costs

are paid as the cost of the era.

Cost of unit under marginal and absorption costing - January

Cost of unit under marginal costing

Units of Waffles produced 10000 units

Cost Per Unit (£)

Direct materials (50,000/10,000) 5

Direct labour (30,000/10,000) 3

Variable manufacturing overhead (20,000/10,000) 2

as regards the Creams limited company part. Including a way of

efficiently allocating the budget so that expenses can be cut.

D1. Integration with the organisational process of management accounting system and reporting

It is accurate says that the accounts management system is connected to the organizational

cycle. Like in the above-mentioned business, innocent drinks are restricted they have different

aspects of financial systems and every one of them is connected to their operating method. For

instance, the cost accounting framework is relevant to financial capital being best distributed.

Like other accounting systems, the organizational method is similar. Although these documents

are also consistent with the framework from the above management team in the management

accounting performance element. Like the article on inventory management, it is connected

with the efficient management of their existing resources.

TASK 2

P3.Calculation of income statements by using absorption and marginal costing approach:

Different strategies exist for planning an organization's financial statements including

such gross expense, absorption costing, and so on. The description of these two methods is

mentioned in detail as continues to follow:

Absorption costing: It is a form of management accounting for the planning of the statements

of profits, where all the expenditures associated with manufacturing is allocated to the quantity

manufactured. In many other terms, besides all variable cost of production, the fixed cost of

production is often used throughout measuring cost of the product.

Marginal Costing: In this process, the business shall accept only adjustable production costs in

the manufacture of a particular item, and then all manufactured costs associated with fixed costs

are paid as the cost of the era.

Cost of unit under marginal and absorption costing - January

Cost of unit under marginal costing

Units of Waffles produced 10000 units

Cost Per Unit (£)

Direct materials (50,000/10,000) 5

Direct labour (30,000/10,000) 3

Variable manufacturing overhead (20,000/10,000) 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

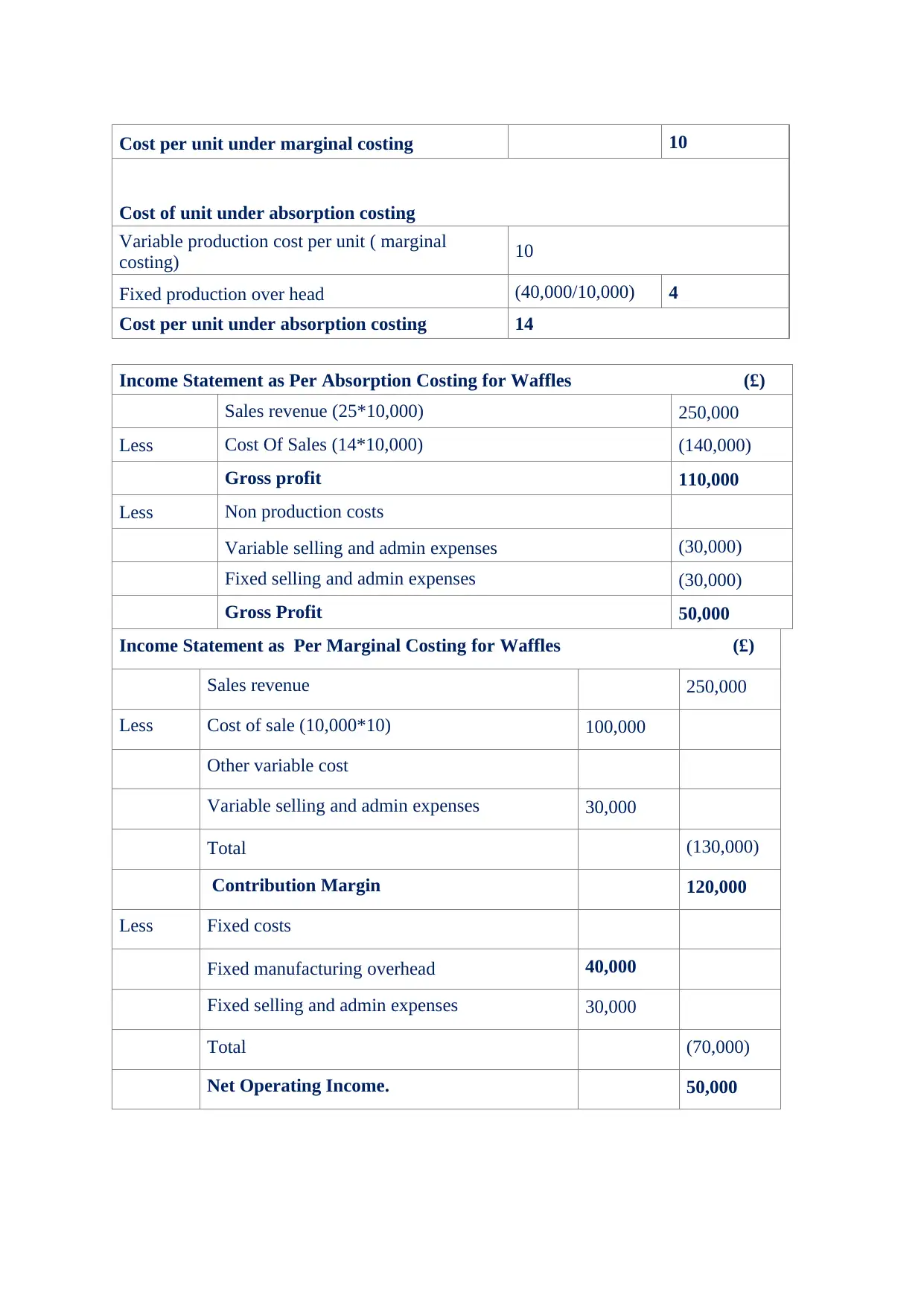

Cost per unit under marginal costing 10

Cost of unit under absorption costing

Variable production cost per unit ( marginal

costing) 10

Fixed production over head (40,000/10,000) 4

Cost per unit under absorption costing 14

Income Statement as Per Absorption Costing for Waffles (£)

Sales revenue (25*10,000) 250,000

Less Cost Of Sales (14*10,000) (140,000)

Gross profit 110,000

Less Non production costs

Variable selling and admin expenses (30,000)

Fixed selling and admin expenses (30,000)

Gross Profit 50,000

Income Statement as Per Marginal Costing for Waffles (£)

Sales revenue 250,000

Less Cost of sale (10,000*10) 100,000

Other variable cost

Variable selling and admin expenses 30,000

Total (130,000)

Contribution Margin 120,000

Less Fixed costs

Fixed manufacturing overhead 40,000

Fixed selling and admin expenses 30,000

Total (70,000)

Net Operating Income. 50,000

Cost of unit under absorption costing

Variable production cost per unit ( marginal

costing) 10

Fixed production over head (40,000/10,000) 4

Cost per unit under absorption costing 14

Income Statement as Per Absorption Costing for Waffles (£)

Sales revenue (25*10,000) 250,000

Less Cost Of Sales (14*10,000) (140,000)

Gross profit 110,000

Less Non production costs

Variable selling and admin expenses (30,000)

Fixed selling and admin expenses (30,000)

Gross Profit 50,000

Income Statement as Per Marginal Costing for Waffles (£)

Sales revenue 250,000

Less Cost of sale (10,000*10) 100,000

Other variable cost

Variable selling and admin expenses 30,000

Total (130,000)

Contribution Margin 120,000

Less Fixed costs

Fixed manufacturing overhead 40,000

Fixed selling and admin expenses 30,000

Total (70,000)

Net Operating Income. 50,000

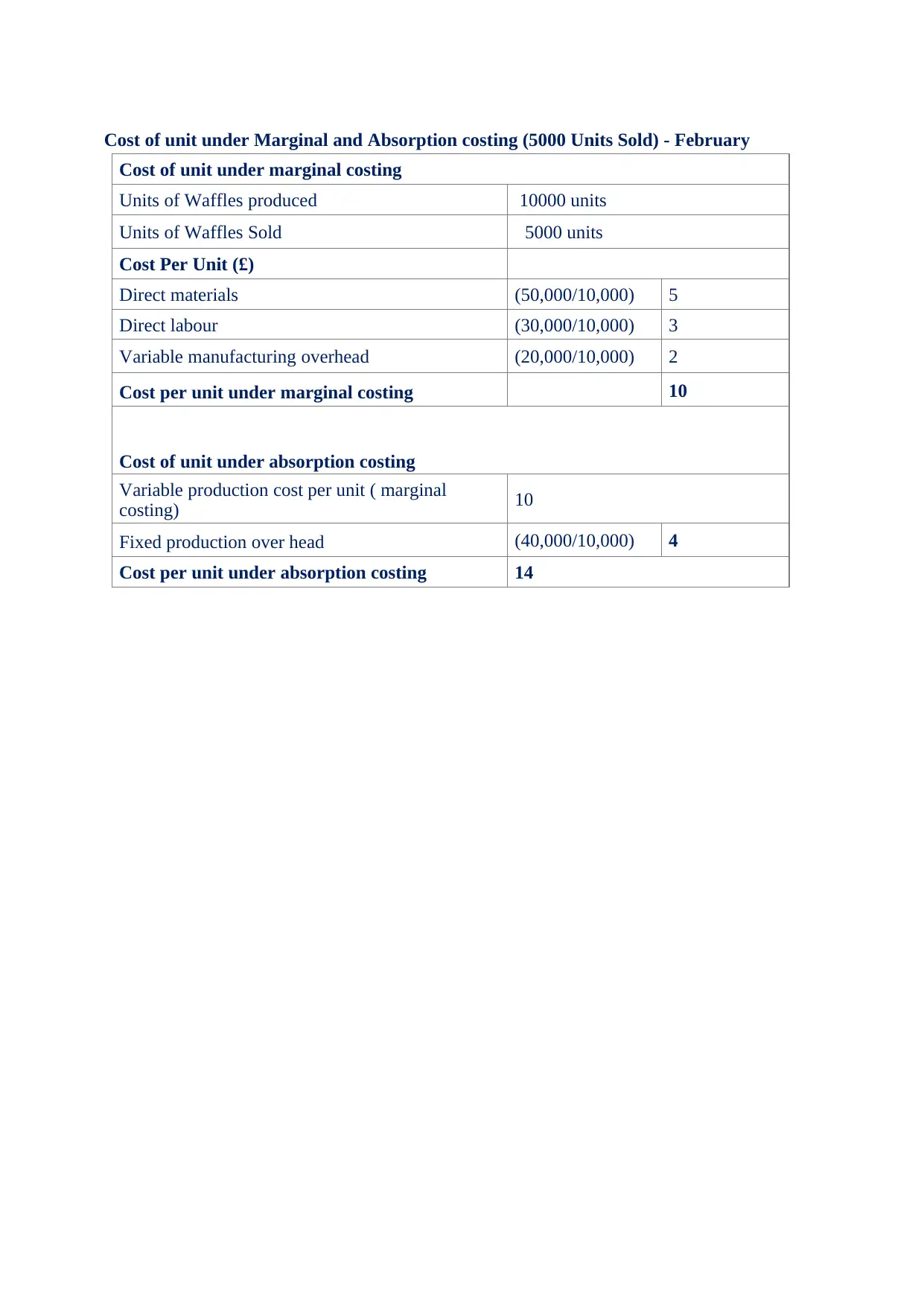

Cost of unit under Marginal and Absorption costing (5000 Units Sold) - February

Cost of unit under marginal costing

Units of Waffles produced 10000 units

Units of Waffles Sold 5000 units

Cost Per Unit (£)

Direct materials (50,000/10,000) 5

Direct labour (30,000/10,000) 3

Variable manufacturing overhead (20,000/10,000) 2

Cost per unit under marginal costing 10

Cost of unit under absorption costing

Variable production cost per unit ( marginal

costing) 10

Fixed production over head (40,000/10,000) 4

Cost per unit under absorption costing 14

Cost of unit under marginal costing

Units of Waffles produced 10000 units

Units of Waffles Sold 5000 units

Cost Per Unit (£)

Direct materials (50,000/10,000) 5

Direct labour (30,000/10,000) 3

Variable manufacturing overhead (20,000/10,000) 2

Cost per unit under marginal costing 10

Cost of unit under absorption costing

Variable production cost per unit ( marginal

costing) 10

Fixed production over head (40,000/10,000) 4

Cost per unit under absorption costing 14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

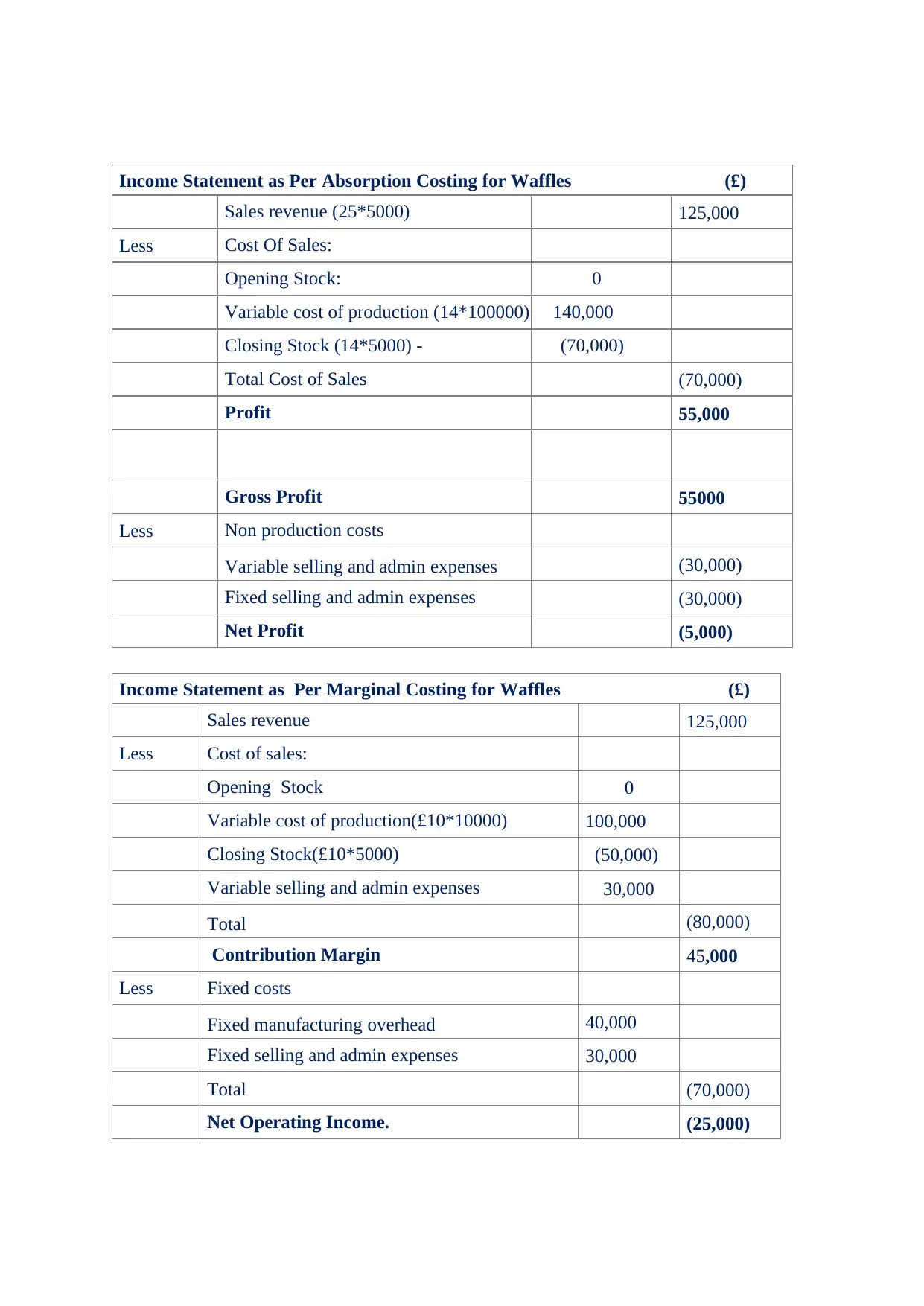

Income Statement as Per Absorption Costing for Waffles (£)

Sales revenue (25*5000) 125,000

Less Cost Of Sales:

Opening Stock: 0

Variable cost of production (14*100000) 140,000

Closing Stock (14*5000) - (70,000)

Total Cost of Sales (70,000)

Profit 55,000

Gross Profit 55000

Less Non production costs

Variable selling and admin expenses (30,000)

Fixed selling and admin expenses (30,000)

Net Profit (5,000)

Income Statement as Per Marginal Costing for Waffles (£)

Sales revenue 125,000

Less Cost of sales:

Opening Stock 0

Variable cost of production(£10*10000) 100,000

Closing Stock(£10*5000) (50,000)

Variable selling and admin expenses 30,000

Total (80,000)

Contribution Margin 45,000

Less Fixed costs

Fixed manufacturing overhead 40,000

Fixed selling and admin expenses 30,000

Total (70,000)

Net Operating Income. (25,000)

Sales revenue (25*5000) 125,000

Less Cost Of Sales:

Opening Stock: 0

Variable cost of production (14*100000) 140,000

Closing Stock (14*5000) - (70,000)

Total Cost of Sales (70,000)

Profit 55,000

Gross Profit 55000

Less Non production costs

Variable selling and admin expenses (30,000)

Fixed selling and admin expenses (30,000)

Net Profit (5,000)

Income Statement as Per Marginal Costing for Waffles (£)

Sales revenue 125,000

Less Cost of sales:

Opening Stock 0

Variable cost of production(£10*10000) 100,000

Closing Stock(£10*5000) (50,000)

Variable selling and admin expenses 30,000

Total (80,000)

Contribution Margin 45,000

Less Fixed costs

Fixed manufacturing overhead 40,000

Fixed selling and admin expenses 30,000

Total (70,000)

Net Operating Income. (25,000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

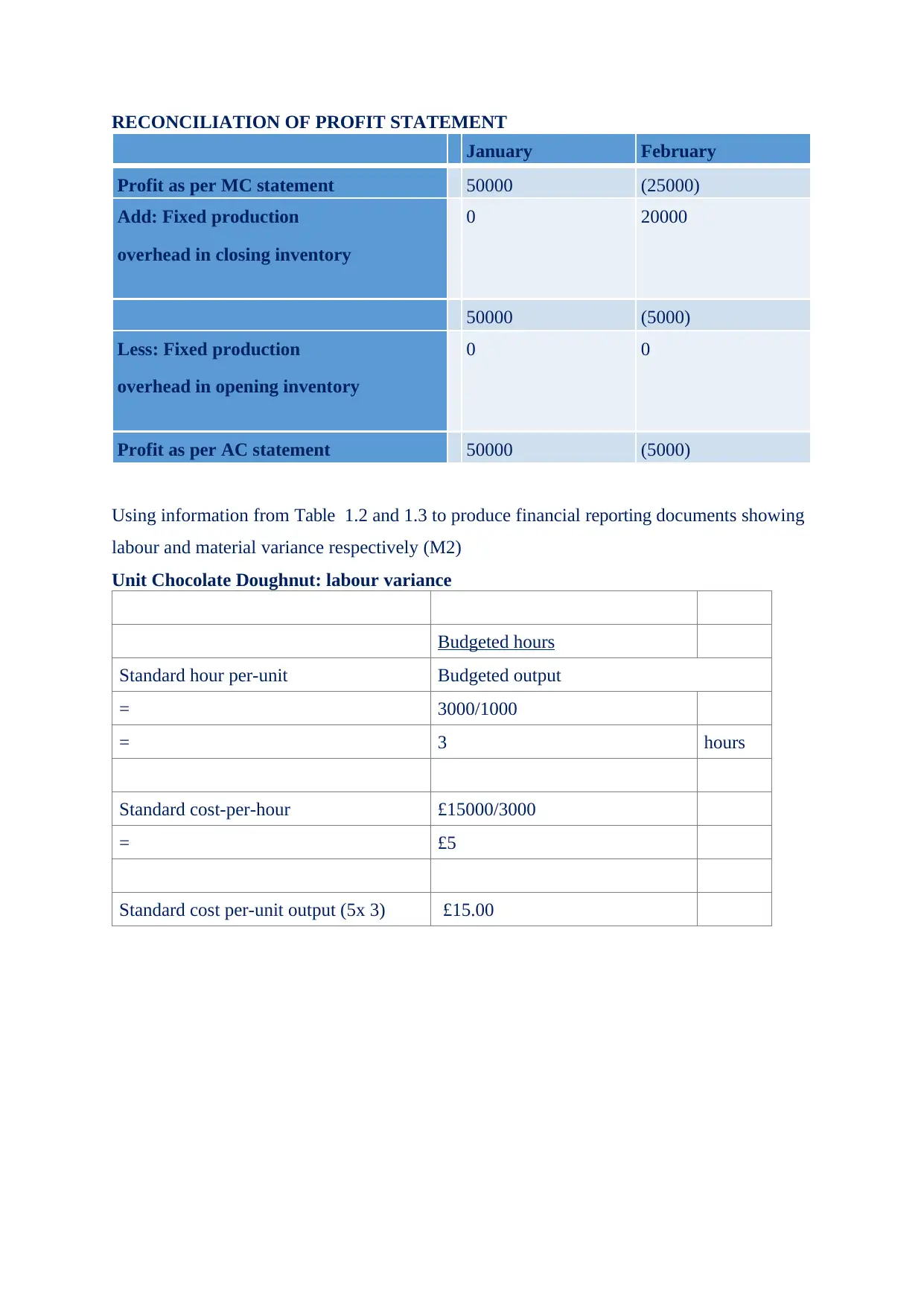

RECONCILIATION OF PROFIT STATEMENT

January February

Profit as per MC statement 50000 (25000)

Add: Fixed production

overhead in closing inventory

0 20000

50000 (5000)

Less: Fixed production

overhead in opening inventory

0 0

Profit as per AC statement 50000 (5000)

Using information from Table 1.2 and 1.3 to produce financial reporting documents showing

labour and material variance respectively (M2)

Unit Chocolate Doughnut: labour variance

Budgeted hours

Standard hour per-unit Budgeted output

= 3000/1000

= 3 hours

Standard cost-per-hour £15000/3000

= £5

Standard cost per-unit output (5x 3) £15.00

January February

Profit as per MC statement 50000 (25000)

Add: Fixed production

overhead in closing inventory

0 20000

50000 (5000)

Less: Fixed production

overhead in opening inventory

0 0

Profit as per AC statement 50000 (5000)

Using information from Table 1.2 and 1.3 to produce financial reporting documents showing

labour and material variance respectively (M2)

Unit Chocolate Doughnut: labour variance

Budgeted hours

Standard hour per-unit Budgeted output

= 3000/1000

= 3 hours

Standard cost-per-hour £15000/3000

= £5

Standard cost per-unit output (5x 3) £15.00

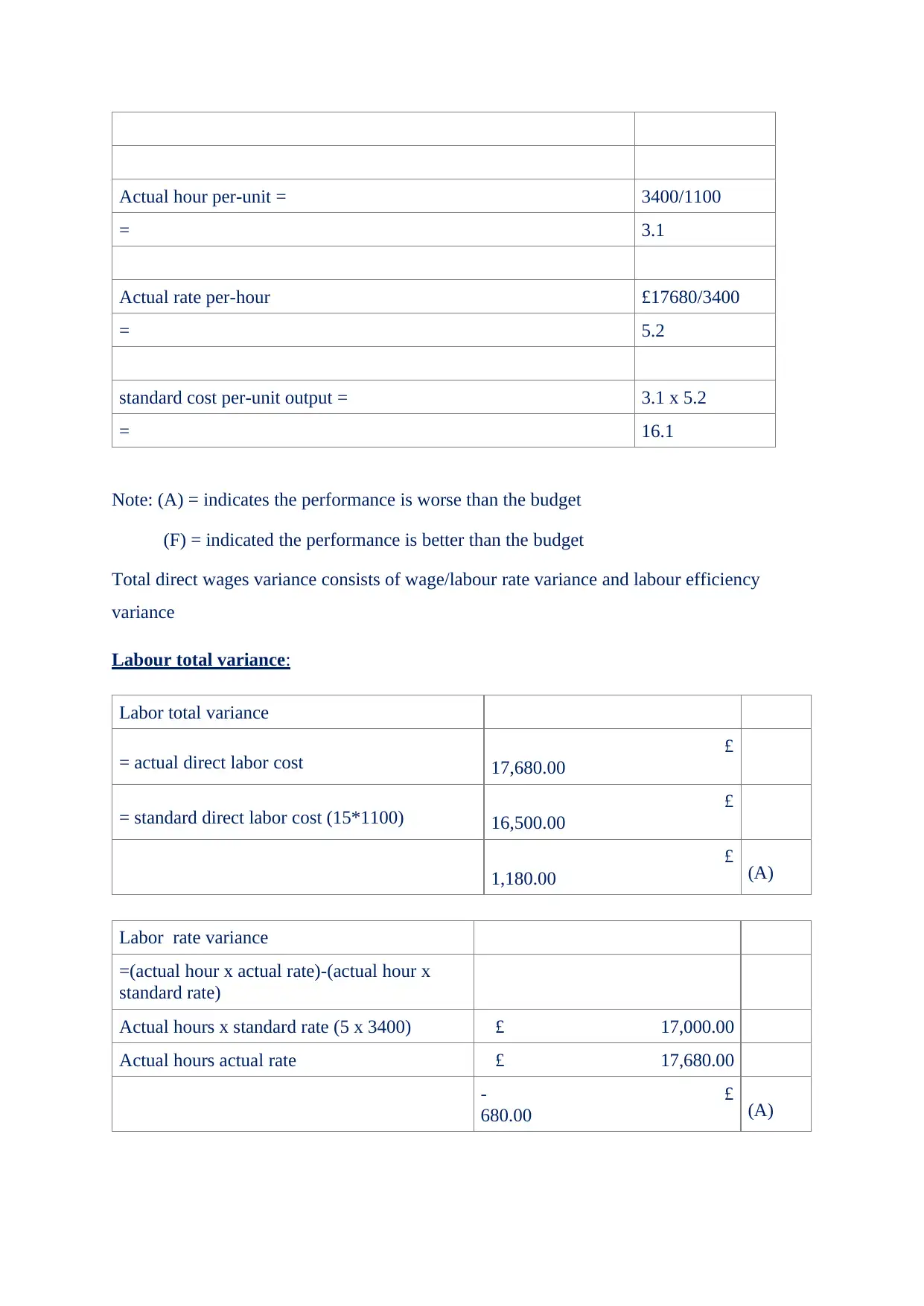

Actual hour per-unit = 3400/1100

= 3.1

Actual rate per-hour £17680/3400

= 5.2

standard cost per-unit output = 3.1 x 5.2

= 16.1

Note: (A) = indicates the performance is worse than the budget

(F) = indicated the performance is better than the budget

Total direct wages variance consists of wage/labour rate variance and labour efficiency

variance

Labour total variance:

Labor total variance

= actual direct labor cost £

17,680.00

= standard direct labor cost (15*1100) £

16,500.00

£

1,180.00 (A)

Labor rate variance

=(actual hour x actual rate)-(actual hour x

standard rate)

Actual hours x standard rate (5 x 3400) £ 17,000.00

Actual hours actual rate £ 17,680.00

- £

680.00 (A)

= 3.1

Actual rate per-hour £17680/3400

= 5.2

standard cost per-unit output = 3.1 x 5.2

= 16.1

Note: (A) = indicates the performance is worse than the budget

(F) = indicated the performance is better than the budget

Total direct wages variance consists of wage/labour rate variance and labour efficiency

variance

Labour total variance:

Labor total variance

= actual direct labor cost £

17,680.00

= standard direct labor cost (15*1100) £

16,500.00

£

1,180.00 (A)

Labor rate variance

=(actual hour x actual rate)-(actual hour x

standard rate)

Actual hours x standard rate (5 x 3400) £ 17,000.00

Actual hours actual rate £ 17,680.00

- £

680.00 (A)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.