Management Accounting Report: Financial Issue Analysis for UCK

VerifiedAdded on 2023/03/20

|11

|2616

|85

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on the UCK Group. It begins with an introduction to management accounting and its importance, followed by an examination of costing methods, including absorption and marginal costing, used to calculate net profit. The report then delves into the advantages and disadvantages of planning tools, such as forecasting and contingency tools, and their role in budgetary control. Furthermore, it evaluates expenses for specific periods and explores the purpose and components of a cash budget. The report also assesses the use of accounting systems to examine financial issues, evaluates vital measures to overcome financial challenges, and analyzes planning tools used in management accounting. The conclusion summarizes the key findings and emphasizes the significance of management accounting for the UCK Group's financial performance and decision-making.

Management Accounting

(PART 2)

(PART 2)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1: Costing methods use for calculating net profit the company......................................................3

1.2: Range of management accounting techniques............................................................................5

1.3: Interpretation of collected data from incomes statement.............................................................5

TASK 2.................................................................................................................................................6

2.1: Advantage and disadvantage of using planning tools.................................................................6

2.2: Evaluation of expenses for July and August...............................................................................7

2.3: Purpose and cash budget.............................................................................................................7

TASK 3.................................................................................................................................................8

3.1: Use of accounting system to examine financial issues................................................................8

3.2: Evaluating vital measure to overcome financial issues..............................................................9

3.3: Analysing planning tools used in management accounting.........................................................9

CONCLUSION...................................................................................................................................10

REFERENCES....................................................................................................................................11

INTRODUCTION.................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1: Costing methods use for calculating net profit the company......................................................3

1.2: Range of management accounting techniques............................................................................5

1.3: Interpretation of collected data from incomes statement.............................................................5

TASK 2.................................................................................................................................................6

2.1: Advantage and disadvantage of using planning tools.................................................................6

2.2: Evaluation of expenses for July and August...............................................................................7

2.3: Purpose and cash budget.............................................................................................................7

TASK 3.................................................................................................................................................8

3.1: Use of accounting system to examine financial issues................................................................8

3.2: Evaluating vital measure to overcome financial issues..............................................................9

3.3: Analysing planning tools used in management accounting.........................................................9

CONCLUSION...................................................................................................................................10

REFERENCES....................................................................................................................................11

INTRODUCTION

In context to current scenario, it has been seen that organisation need to make regular

search of innovative and effective systems that can help the company to gain maximum

benefit during the time. Management accounting is essential aspects which will be consider

as more reliable and accurate tool that assist in increasing profitability for UCK group of

company. By the help of this, they can easily be able to attain their long term aims and

objectives. This particular project report is providing more valuable information about

various costing method which is use for the computing net profit for the company. In

accordance to this, advantage and disadvantage of using planning tools which are helpful in

budgetary control are mentioned under this report. Analysis of financial issues those are

arises in an organisation (Amoako, 2013).

TASK 1

1.1: Costing methods use for calculating net profit the company

Cost is an essential aspect which would be considers more effective tools for the

company. They need continuous planning to manage and control their extra costs which are

increasing profitability during the time. It has been seen that costs are affecting production of

products and services of the company either directly or indirectly. Costs is said to be value of

amount which is related with manufacture process. The primary role of managers is to make

valuable decisions to manage and control excess costs for the company. With the help of this,

overall productivity of the company can also be increase at the same point of time. There are

various types of costing methods which are useful in evaluating overall profit for UCK group

ltd. Some of them are illustrated underneath:

Absorption costing: This seems to be one of the effective methods which are

applicable with production process. It uses to consider both variable and fixed costs

simultaneously, because of this it is known as full costing approaches (Absorption costing,

2018). There are various benefits of using this method but at the same time, it is having

certain limitation. This cannot be taken as more effective tools for making future decision

making.

Marginal costing: It refers as those costs which is uses by the managers in production

of one additional unit. It only considered variable costs and fixed costs are absorbed while

In context to current scenario, it has been seen that organisation need to make regular

search of innovative and effective systems that can help the company to gain maximum

benefit during the time. Management accounting is essential aspects which will be consider

as more reliable and accurate tool that assist in increasing profitability for UCK group of

company. By the help of this, they can easily be able to attain their long term aims and

objectives. This particular project report is providing more valuable information about

various costing method which is use for the computing net profit for the company. In

accordance to this, advantage and disadvantage of using planning tools which are helpful in

budgetary control are mentioned under this report. Analysis of financial issues those are

arises in an organisation (Amoako, 2013).

TASK 1

1.1: Costing methods use for calculating net profit the company

Cost is an essential aspect which would be considers more effective tools for the

company. They need continuous planning to manage and control their extra costs which are

increasing profitability during the time. It has been seen that costs are affecting production of

products and services of the company either directly or indirectly. Costs is said to be value of

amount which is related with manufacture process. The primary role of managers is to make

valuable decisions to manage and control excess costs for the company. With the help of this,

overall productivity of the company can also be increase at the same point of time. There are

various types of costing methods which are useful in evaluating overall profit for UCK group

ltd. Some of them are illustrated underneath:

Absorption costing: This seems to be one of the effective methods which are

applicable with production process. It uses to consider both variable and fixed costs

simultaneously, because of this it is known as full costing approaches (Absorption costing,

2018). There are various benefits of using this method but at the same time, it is having

certain limitation. This cannot be taken as more effective tools for making future decision

making.

Marginal costing: It refers as those costs which is uses by the managers in production

of one additional unit. It only considered variable costs and fixed costs are absorbed while

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

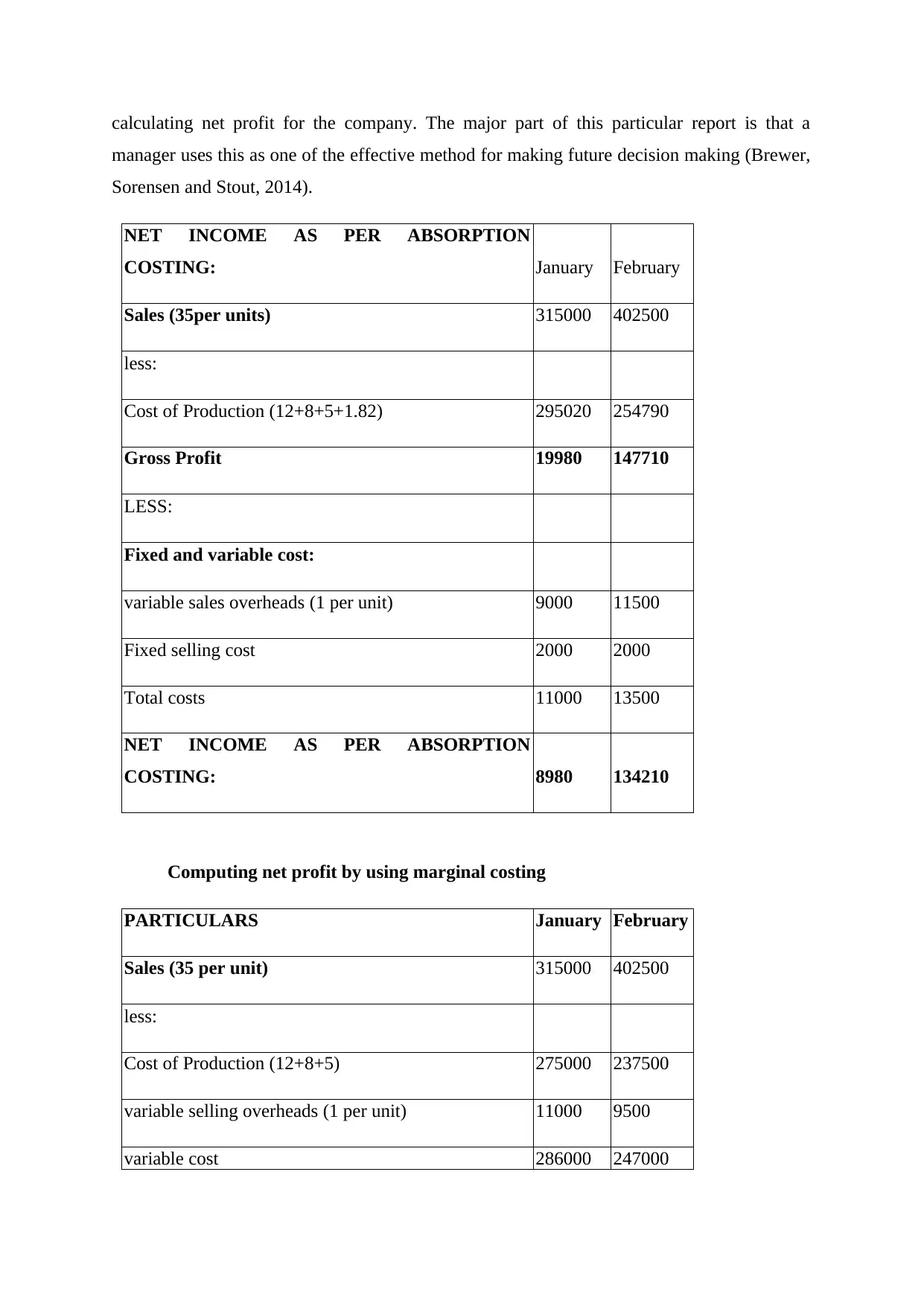

calculating net profit for the company. The major part of this particular report is that a

manager uses this as one of the effective method for making future decision making (Brewer,

Sorensen and Stout, 2014).

NET INCOME AS PER ABSORPTION

COSTING: January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION

COSTING: 8980 134210

Computing net profit by using marginal costing

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

manager uses this as one of the effective method for making future decision making (Brewer,

Sorensen and Stout, 2014).

NET INCOME AS PER ABSORPTION

COSTING: January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION

COSTING: 8980 134210

Computing net profit by using marginal costing

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

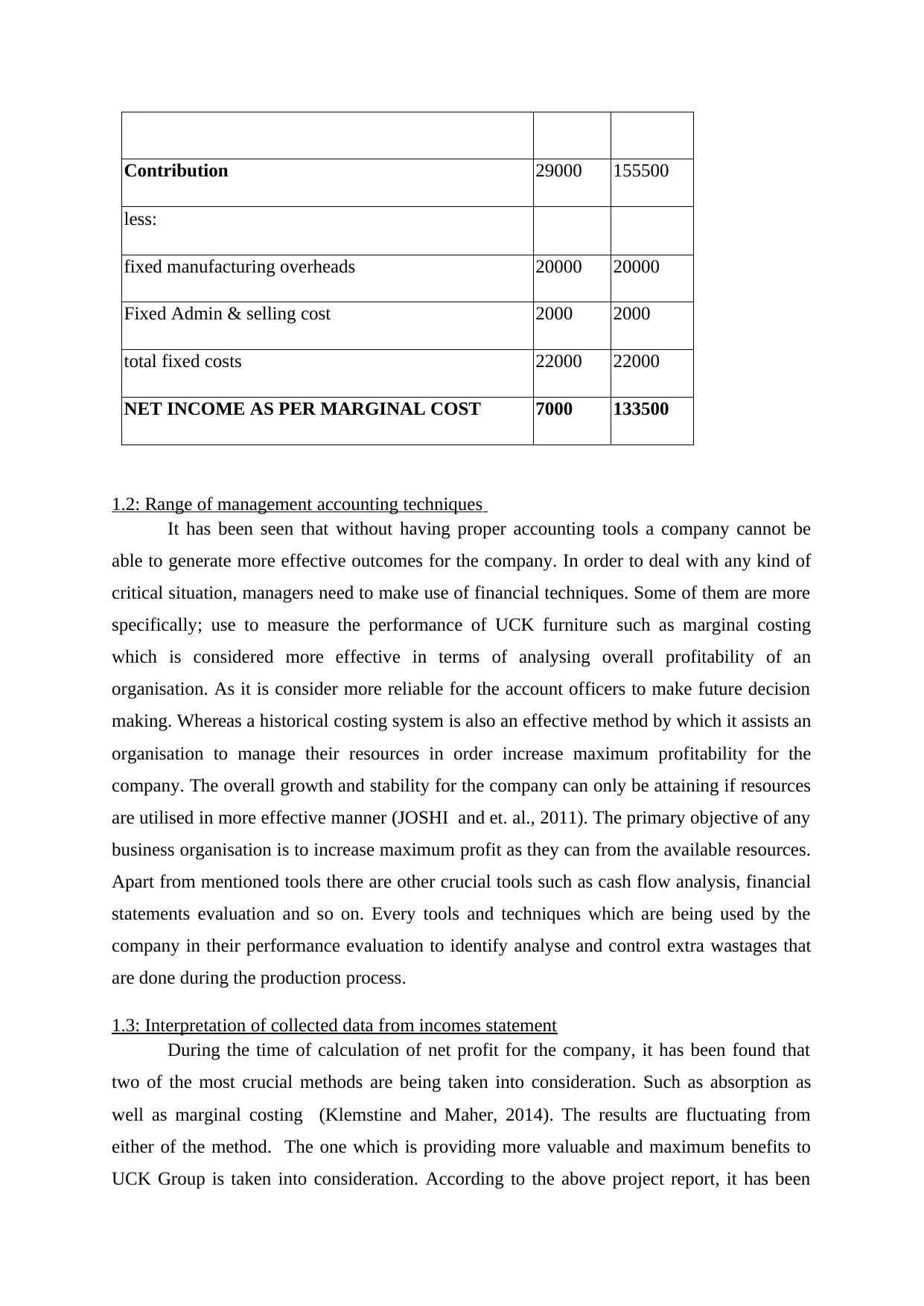

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

1.2: Range of management accounting techniques

It has been seen that without having proper accounting tools a company cannot be

able to generate more effective outcomes for the company. In order to deal with any kind of

critical situation, managers need to make use of financial techniques. Some of them are more

specifically; use to measure the performance of UCK furniture such as marginal costing

which is considered more effective in terms of analysing overall profitability of an

organisation. As it is consider more reliable for the account officers to make future decision

making. Whereas a historical costing system is also an effective method by which it assists an

organisation to manage their resources in order increase maximum profitability for the

company. The overall growth and stability for the company can only be attaining if resources

are utilised in more effective manner (JOSHI and et. al., 2011). The primary objective of any

business organisation is to increase maximum profit as they can from the available resources.

Apart from mentioned tools there are other crucial tools such as cash flow analysis, financial

statements evaluation and so on. Every tools and techniques which are being used by the

company in their performance evaluation to identify analyse and control extra wastages that

are done during the production process.

1.3: Interpretation of collected data from incomes statement

During the time of calculation of net profit for the company, it has been found that

two of the most crucial methods are being taken into consideration. Such as absorption as

well as marginal costing (Klemstine and Maher, 2014). The results are fluctuating from

either of the method. The one which is providing more valuable and maximum benefits to

UCK Group is taken into consideration. According to the above project report, it has been

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

1.2: Range of management accounting techniques

It has been seen that without having proper accounting tools a company cannot be

able to generate more effective outcomes for the company. In order to deal with any kind of

critical situation, managers need to make use of financial techniques. Some of them are more

specifically; use to measure the performance of UCK furniture such as marginal costing

which is considered more effective in terms of analysing overall profitability of an

organisation. As it is consider more reliable for the account officers to make future decision

making. Whereas a historical costing system is also an effective method by which it assists an

organisation to manage their resources in order increase maximum profitability for the

company. The overall growth and stability for the company can only be attaining if resources

are utilised in more effective manner (JOSHI and et. al., 2011). The primary objective of any

business organisation is to increase maximum profit as they can from the available resources.

Apart from mentioned tools there are other crucial tools such as cash flow analysis, financial

statements evaluation and so on. Every tools and techniques which are being used by the

company in their performance evaluation to identify analyse and control extra wastages that

are done during the production process.

1.3: Interpretation of collected data from incomes statement

During the time of calculation of net profit for the company, it has been found that

two of the most crucial methods are being taken into consideration. Such as absorption as

well as marginal costing (Klemstine and Maher, 2014). The results are fluctuating from

either of the method. The one which is providing more valuable and maximum benefits to

UCK Group is taken into consideration. According to the above project report, it has been

seen that company wants to increase their productivity by using best techniques for

calculating net profit during the time. With the use of these methods chances of getting

maximum results can be taken from using marginal costing because they are considering only

variable costs.

TASK 2

2.1: Advantage and disadvantage of using planning tools

It has been observed that company can control their additional costs and expenses so

that to increase maximum growth and stability of UCK Group Ltd. The primary purpose of

doing so is to generate more valuable and reliable outcomes for the company. In accordance

with this, managers need to make use of budgets prior making any crucial decision making. It

is required to recalculate on continuous basis to make effective standard to enhance overall

growth for the employees (Lim, 2011). It is effectively associated with internal techniques

that are useful in order to control overall risk factors those are present in an organisation.

Budgets are said to be an estimation of future costs and expenditure that are incur by the

company. In order to control the budgets company is using certain kind of planning tools.

Some of them are discuss underneath:

Forecasting tools: According to these particular tools, one can easily be able to

determine future activities on continuous basis. It can be done by using past and present data

more the purpose of analysing performance of the company.

Advantages: One of the primary benefits of using these particular tools is to examine

early estimation of costs and expense that are going to be done by the UCK Group Ltd

during the time. It is consider more accurate for decision making (Tessier and Otley,

2012).

Disadvantage: It has been seen that sometime, it is very difficult to predict future in

more accurate manner because of qualitative aspects.

Contingency tools: This seems to be an effective planning which is done by the company

to control overall risk that is present in an organisation. These are more devising through

domestic government as well as large business organisation in case of any urgency.

calculating net profit during the time. With the use of these methods chances of getting

maximum results can be taken from using marginal costing because they are considering only

variable costs.

TASK 2

2.1: Advantage and disadvantage of using planning tools

It has been observed that company can control their additional costs and expenses so

that to increase maximum growth and stability of UCK Group Ltd. The primary purpose of

doing so is to generate more valuable and reliable outcomes for the company. In accordance

with this, managers need to make use of budgets prior making any crucial decision making. It

is required to recalculate on continuous basis to make effective standard to enhance overall

growth for the employees (Lim, 2011). It is effectively associated with internal techniques

that are useful in order to control overall risk factors those are present in an organisation.

Budgets are said to be an estimation of future costs and expenditure that are incur by the

company. In order to control the budgets company is using certain kind of planning tools.

Some of them are discuss underneath:

Forecasting tools: According to these particular tools, one can easily be able to

determine future activities on continuous basis. It can be done by using past and present data

more the purpose of analysing performance of the company.

Advantages: One of the primary benefits of using these particular tools is to examine

early estimation of costs and expense that are going to be done by the UCK Group Ltd

during the time. It is consider more accurate for decision making (Tessier and Otley,

2012).

Disadvantage: It has been seen that sometime, it is very difficult to predict future in

more accurate manner because of qualitative aspects.

Contingency tools: This seems to be an effective planning which is done by the company

to control overall risk that is present in an organisation. These are more devising through

domestic government as well as large business organisation in case of any urgency.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

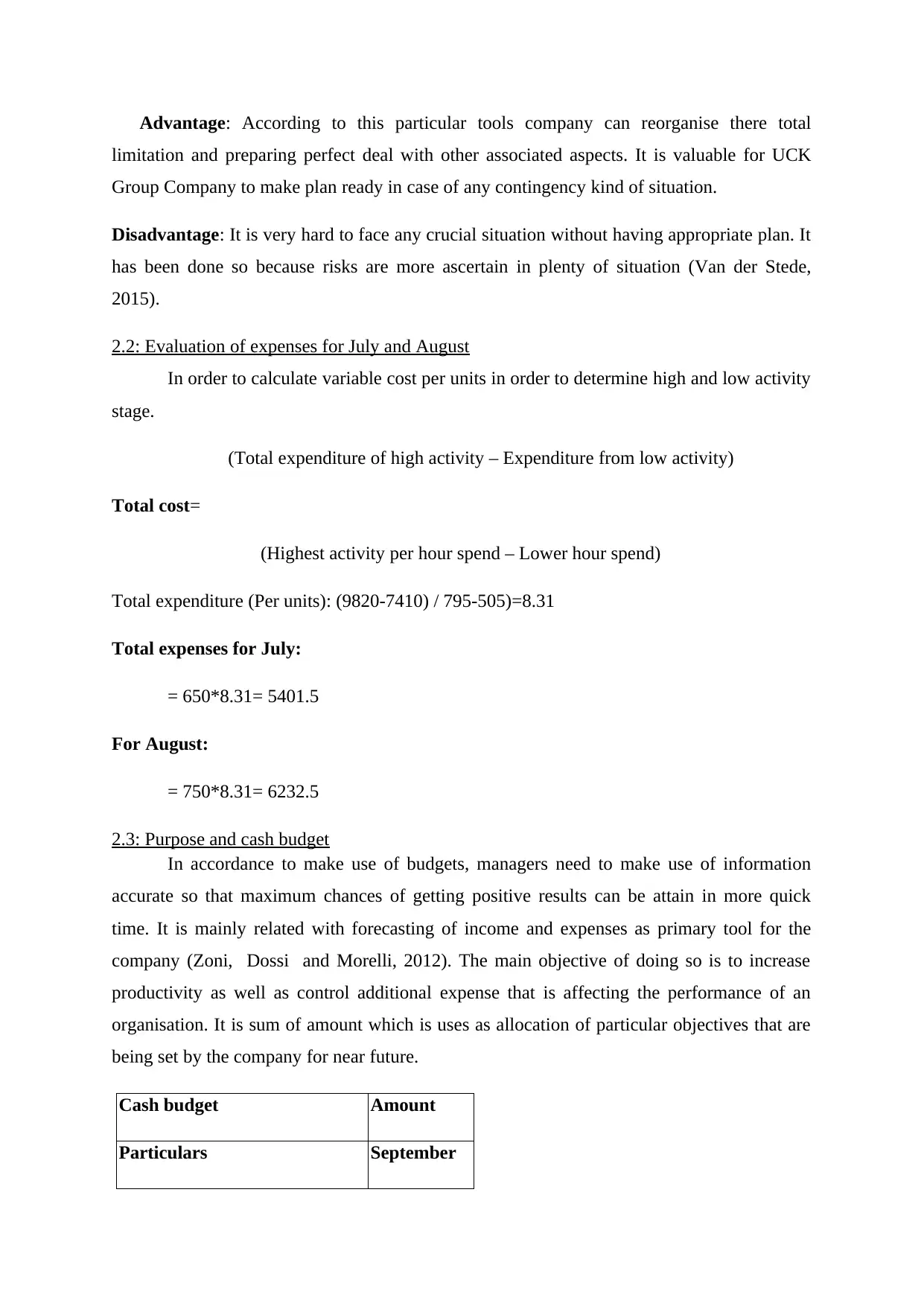

Advantage: According to this particular tools company can reorganise there total

limitation and preparing perfect deal with other associated aspects. It is valuable for UCK

Group Company to make plan ready in case of any contingency kind of situation.

Disadvantage: It is very hard to face any crucial situation without having appropriate plan. It

has been done so because risks are more ascertain in plenty of situation (Van der Stede,

2015).

2.2: Evaluation of expenses for July and August

In order to calculate variable cost per units in order to determine high and low activity

stage.

(Total expenditure of high activity – Expenditure from low activity)

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total expenditure (Per units): (9820-7410) / 795-505)=8.31

Total expenses for July:

= 650*8.31= 5401.5

For August:

= 750*8.31= 6232.5

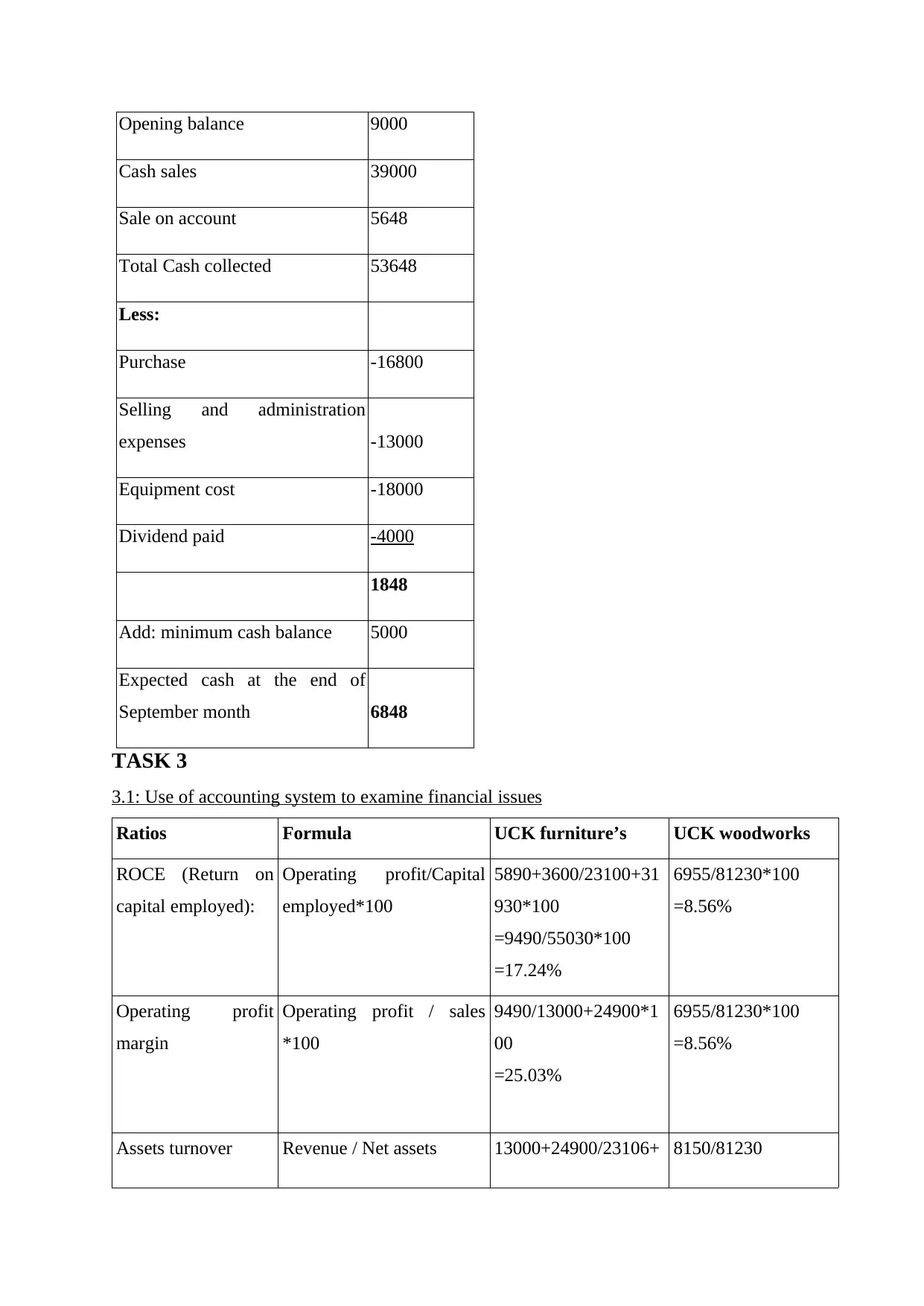

2.3: Purpose and cash budget

In accordance to make use of budgets, managers need to make use of information

accurate so that maximum chances of getting positive results can be attain in more quick

time. It is mainly related with forecasting of income and expenses as primary tool for the

company (Zoni, Dossi and Morelli, 2012). The main objective of doing so is to increase

productivity as well as control additional expense that is affecting the performance of an

organisation. It is sum of amount which is uses as allocation of particular objectives that are

being set by the company for near future.

Cash budget Amount

Particulars September

limitation and preparing perfect deal with other associated aspects. It is valuable for UCK

Group Company to make plan ready in case of any contingency kind of situation.

Disadvantage: It is very hard to face any crucial situation without having appropriate plan. It

has been done so because risks are more ascertain in plenty of situation (Van der Stede,

2015).

2.2: Evaluation of expenses for July and August

In order to calculate variable cost per units in order to determine high and low activity

stage.

(Total expenditure of high activity – Expenditure from low activity)

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total expenditure (Per units): (9820-7410) / 795-505)=8.31

Total expenses for July:

= 650*8.31= 5401.5

For August:

= 750*8.31= 6232.5

2.3: Purpose and cash budget

In accordance to make use of budgets, managers need to make use of information

accurate so that maximum chances of getting positive results can be attain in more quick

time. It is mainly related with forecasting of income and expenses as primary tool for the

company (Zoni, Dossi and Morelli, 2012). The main objective of doing so is to increase

productivity as well as control additional expense that is affecting the performance of an

organisation. It is sum of amount which is uses as allocation of particular objectives that are

being set by the company for near future.

Cash budget Amount

Particulars September

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Less:

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash at the end of

September month 6848

TASK 3

3.1: Use of accounting system to examine financial issues

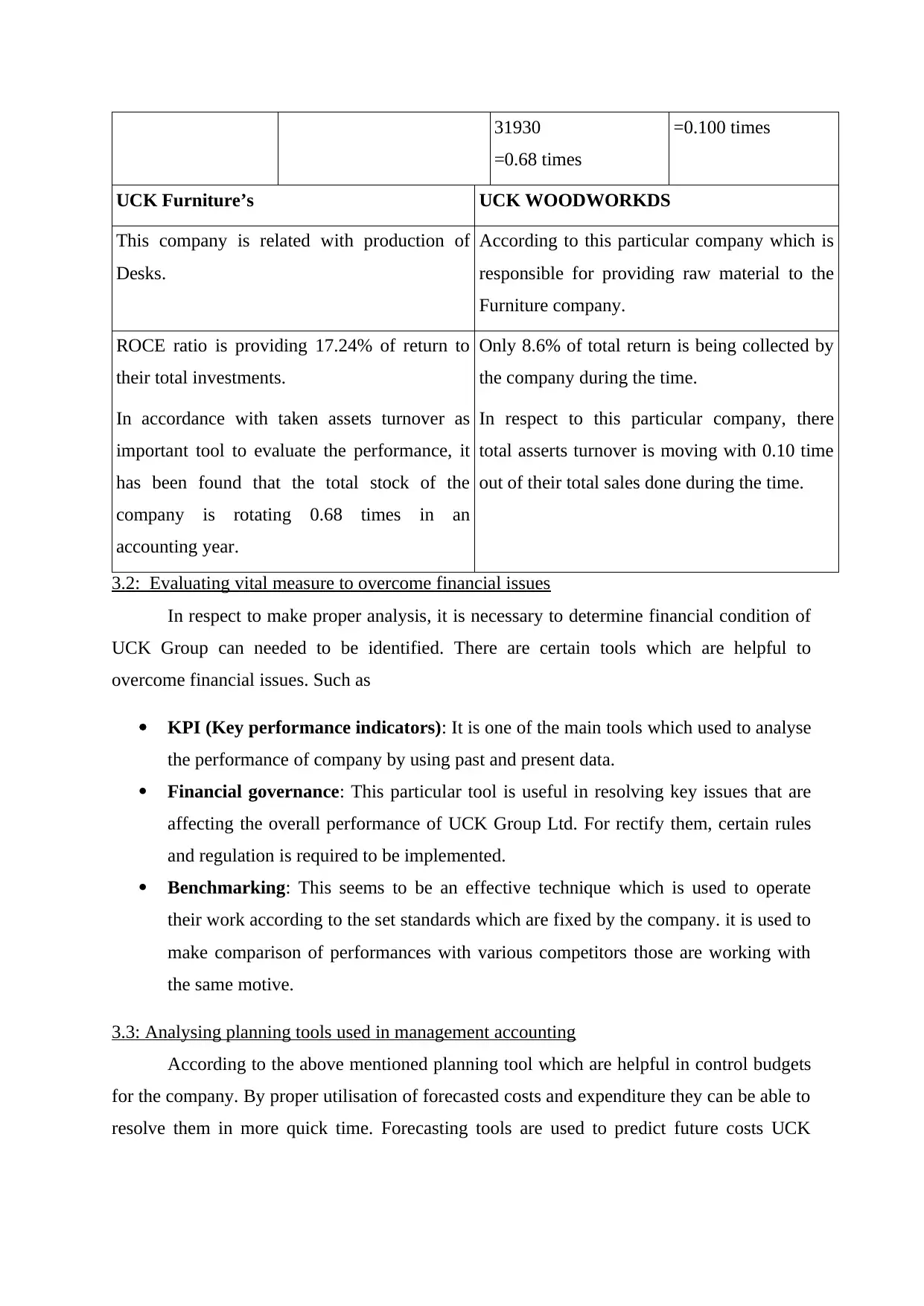

Ratios Formula UCK furniture’s UCK woodworks

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+31

930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/13000+24900*1

00

=25.03%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/23106+ 8150/81230

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Less:

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash at the end of

September month 6848

TASK 3

3.1: Use of accounting system to examine financial issues

Ratios Formula UCK furniture’s UCK woodworks

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+31

930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/13000+24900*1

00

=25.03%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/23106+ 8150/81230

31930

=0.68 times

=0.100 times

UCK Furniture’s UCK WOODWORKDS

This company is related with production of

Desks.

According to this particular company which is

responsible for providing raw material to the

Furniture company.

ROCE ratio is providing 17.24% of return to

their total investments.

Only 8.6% of total return is being collected by

the company during the time.

In accordance with taken assets turnover as

important tool to evaluate the performance, it

has been found that the total stock of the

company is rotating 0.68 times in an

accounting year.

In respect to this particular company, there

total asserts turnover is moving with 0.10 time

out of their total sales done during the time.

3.2: Evaluating vital measure to overcome financial issues

In respect to make proper analysis, it is necessary to determine financial condition of

UCK Group can needed to be identified. There are certain tools which are helpful to

overcome financial issues. Such as

KPI (Key performance indicators): It is one of the main tools which used to analyse

the performance of company by using past and present data.

Financial governance: This particular tool is useful in resolving key issues that are

affecting the overall performance of UCK Group Ltd. For rectify them, certain rules

and regulation is required to be implemented.

Benchmarking: This seems to be an effective technique which is used to operate

their work according to the set standards which are fixed by the company. it is used to

make comparison of performances with various competitors those are working with

the same motive.

3.3: Analysing planning tools used in management accounting

According to the above mentioned planning tool which are helpful in control budgets

for the company. By proper utilisation of forecasted costs and expenditure they can be able to

resolve them in more quick time. Forecasting tools are used to predict future costs UCK

=0.68 times

=0.100 times

UCK Furniture’s UCK WOODWORKDS

This company is related with production of

Desks.

According to this particular company which is

responsible for providing raw material to the

Furniture company.

ROCE ratio is providing 17.24% of return to

their total investments.

Only 8.6% of total return is being collected by

the company during the time.

In accordance with taken assets turnover as

important tool to evaluate the performance, it

has been found that the total stock of the

company is rotating 0.68 times in an

accounting year.

In respect to this particular company, there

total asserts turnover is moving with 0.10 time

out of their total sales done during the time.

3.2: Evaluating vital measure to overcome financial issues

In respect to make proper analysis, it is necessary to determine financial condition of

UCK Group can needed to be identified. There are certain tools which are helpful to

overcome financial issues. Such as

KPI (Key performance indicators): It is one of the main tools which used to analyse

the performance of company by using past and present data.

Financial governance: This particular tool is useful in resolving key issues that are

affecting the overall performance of UCK Group Ltd. For rectify them, certain rules

and regulation is required to be implemented.

Benchmarking: This seems to be an effective technique which is used to operate

their work according to the set standards which are fixed by the company. it is used to

make comparison of performances with various competitors those are working with

the same motive.

3.3: Analysing planning tools used in management accounting

According to the above mentioned planning tool which are helpful in control budgets

for the company. By proper utilisation of forecasted costs and expenditure they can be able to

resolve them in more quick time. Forecasting tools are used to predict future costs UCK

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

group is going to be beard. While contingencies is responsible for evaluating total risk factors

that are associated with the company.

CONCLUSION

From the above project report, it has been concluded that management accounting is

utmost crucial aspects for UCK Group Company to control their day to day business

operations. This can assist managers to make use of valuable costing methods to calculate

total profit generated by the company during the time. Further, this report is entirely based on

analysing overall performance of UCK Furniture by using various planning tools to control

their budgets that are prepared by the company. Financial data is use to analyse current

performance of company by calculating ratios. All those financial issues which are present in

an organisation are determined and valuable measures are provided to the company. This can

be done to increase better sustainability in near future.

that are associated with the company.

CONCLUSION

From the above project report, it has been concluded that management accounting is

utmost crucial aspects for UCK Group Company to control their day to day business

operations. This can assist managers to make use of valuable costing methods to calculate

total profit generated by the company during the time. Further, this report is entirely based on

analysing overall performance of UCK Furniture by using various planning tools to control

their budgets that are prepared by the company. Financial data is use to analyse current

performance of company by calculating ratios. All those financial issues which are present in

an organisation are determined and valuable measures are provided to the company. This can

be done to increase better sustainability in near future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Amoako, G.K., 2013. Accounting practices of SMEs: A case study of Kumasi Metropolis in

Ghana. International Journal of Business and Management. 8(24). p.73.

Brewer, P. C., Sorensen, J. E. and Stout, D. E., 2014. The future of accounting education:

Addressing the competency crisis. Strategic Finance. 96(2). pp.29-38.

JOSHI, P.L. and et. al., 2011. Diffusion of management accounting practices in gulf

cooperation council countries. Accounting Perspectives. 10(1). pp.23-53.

Klemstine, C. F. and Maher, M., 2014. Management Accounting Research (RLE

Accounting): A Review and Annotated Bibliography. Routledge.

Lim, M., 2011. Full cost accounting in solid waste management: the gap in the literature on

newly industrialised countries. Journal of Applied Management Accounting

Research. 9(1). p.21.

Tessier, S. and Otley, D., 2012. A conceptual development of Simons’ Levers of Control

framework. Management Accounting Research. 23(3). pp.171-185.

Van der Stede, W. A., 2015. Management accounting: Where from, where now, where to?.

Journal of Management Accounting Research. 27(1). pp.171-176.

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change:

field evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Online

Absorption costing. 2018.[Online]. Available through:

<http://www.businessdictionary.com/definition/absorption-costing.html>.

Books and Journals:

Amoako, G.K., 2013. Accounting practices of SMEs: A case study of Kumasi Metropolis in

Ghana. International Journal of Business and Management. 8(24). p.73.

Brewer, P. C., Sorensen, J. E. and Stout, D. E., 2014. The future of accounting education:

Addressing the competency crisis. Strategic Finance. 96(2). pp.29-38.

JOSHI, P.L. and et. al., 2011. Diffusion of management accounting practices in gulf

cooperation council countries. Accounting Perspectives. 10(1). pp.23-53.

Klemstine, C. F. and Maher, M., 2014. Management Accounting Research (RLE

Accounting): A Review and Annotated Bibliography. Routledge.

Lim, M., 2011. Full cost accounting in solid waste management: the gap in the literature on

newly industrialised countries. Journal of Applied Management Accounting

Research. 9(1). p.21.

Tessier, S. and Otley, D., 2012. A conceptual development of Simons’ Levers of Control

framework. Management Accounting Research. 23(3). pp.171-185.

Van der Stede, W. A., 2015. Management accounting: Where from, where now, where to?.

Journal of Management Accounting Research. 27(1). pp.171-176.

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change:

field evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Online

Absorption costing. 2018.[Online]. Available through:

<http://www.businessdictionary.com/definition/absorption-costing.html>.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.