Management Accounting Report: Prime Furniture Analysis and Insights

VerifiedAdded on 2023/01/17

|12

|2808

|26

Report

AI Summary

This report on management accounting analyzes various techniques and tools used in the field, with a specific focus on their application within Prime Furniture. The report delves into microeconomic techniques, including cost analysis (fixed, variable, and semi-variable costs), cost-volume-profit analysis, flexible budgeting, absorption costing, marginal costing, and product costing. It further explores the use of planning tools, such as capital and operating budgets, zero-based budgeting, and strategic planning using the PEST framework. The report also compares how different organizations, including Prime Furniture and Triumph Company Furniture, utilize management accounting to address financial problems and improve performance, highlighting the use of benchmarking, key performance indicators, and financial governance. The analysis provides insights into the practical application of management accounting principles and their role in organizational decision-making.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

L O 2................................................................................................................................................3

Application of techniques of management accounting................................................................3

L O 3................................................................................................................................................6

Use of planning tools that are applied in management accounting.............................................6

L O 4................................................................................................................................................9

Compare ways in which organizations use management accounting..........................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

L O 2................................................................................................................................................3

Application of techniques of management accounting................................................................3

L O 3................................................................................................................................................6

Use of planning tools that are applied in management accounting.............................................6

L O 4................................................................................................................................................9

Compare ways in which organizations use management accounting..........................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is defined as the process of determining the cost of business and

operations to prepare financial records and reports that supports decision-making of management

in achieving the goals of company (Childress and et.al, 2015). The Report is based on Prime

Furniture. The Report will outline various management accounting techniques, use of various

planning tools in management accounting. Further, it will also describe ways in which different

organizations are using management accounting to respond to financial problems etc.

L O 2

Application of techniques of management accounting.

Overview of management accounting-

The term management accounting refers to the presentation of information with the aim

of developing policies that are to be adopted by the management and supports in day-to-day

activities. It uses the details related with operations of business to prepare reports that offer

consistent insight into profit margin, labour utilization of the business that acts as an input to take

routine decisions (Christian, 2018).

Microeconomic techniques :

Cost- It means the amount that has to be paid in order to get something . In business, cost refers

to monetary valuation of material, labour, time, resources etc.

Types of cost-

On the basis of nature of costs-

Fixed cost : It refers to the cost of fixed inputs that are used in the process of production. These

cost does not change with change in production volume.

Variable cost: It means the cost variable inputs that are used by business in production of goods.

It changes with the change in volume of production.

Semi variable cost: It means the cost which is partly variable and partly fixed. It does not

directly influence the production but may change with production facilities.

On the basis of expense-

Material cost:

It means the cost of purchasing raw material used in production of goods.

Labour cost:

It refers to the payment made to temporary and permanent workers for their services.

Management accounting is defined as the process of determining the cost of business and

operations to prepare financial records and reports that supports decision-making of management

in achieving the goals of company (Childress and et.al, 2015). The Report is based on Prime

Furniture. The Report will outline various management accounting techniques, use of various

planning tools in management accounting. Further, it will also describe ways in which different

organizations are using management accounting to respond to financial problems etc.

L O 2

Application of techniques of management accounting.

Overview of management accounting-

The term management accounting refers to the presentation of information with the aim

of developing policies that are to be adopted by the management and supports in day-to-day

activities. It uses the details related with operations of business to prepare reports that offer

consistent insight into profit margin, labour utilization of the business that acts as an input to take

routine decisions (Christian, 2018).

Microeconomic techniques :

Cost- It means the amount that has to be paid in order to get something . In business, cost refers

to monetary valuation of material, labour, time, resources etc.

Types of cost-

On the basis of nature of costs-

Fixed cost : It refers to the cost of fixed inputs that are used in the process of production. These

cost does not change with change in production volume.

Variable cost: It means the cost variable inputs that are used by business in production of goods.

It changes with the change in volume of production.

Semi variable cost: It means the cost which is partly variable and partly fixed. It does not

directly influence the production but may change with production facilities.

On the basis of expense-

Material cost:

It means the cost of purchasing raw material used in production of goods.

Labour cost:

It refers to the payment made to temporary and permanent workers for their services.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Overhead:

It is the cost which changes with the level of production like cost of indirect labour etc.

Cost volume profit analysis-

It refers to the method of cost accounting that focuses at the impact that different levels of

volume and cost have on operating profit. It is also known as break even analysis that helps to

determine break even point for various levels of cost structure and sales volume that are useful

for managers to make short term economic decisions.

Flexible budgeting-

Flexible budget is a type of budget that helps to recognize the variation in difference

between variable and fixed cost to fluctuations in turnover, output etc. It is developed to change

in the relation to the level of activity attained by firm actually (Duan and et.al, 2016). This type

of budget is also called multi-volume budget. Major advantage is that it helps Prime Furniture to

forecast its performance. Major limitation is that fixed cost is generally fixed only over a

significant output range.

Absorption costing-

It refers to the approach of accumulating cost related with the process of production and

dividing them to individual products. The indirect and direct cost like direct labour, direct

material and insurance etc. are accounted for using this method.

cost per unit (absorption costing)

Figures (in

£)

Production cost(variable) 0.65

Production cost (fixed) 0.2

Cost of production per unit 0.85

Profitability statement as per absorption costing

Quarter 1

Particulars Units

per

unit

price

(in £)

Figures

(in £)

Net

figure

(in £)

It is the cost which changes with the level of production like cost of indirect labour etc.

Cost volume profit analysis-

It refers to the method of cost accounting that focuses at the impact that different levels of

volume and cost have on operating profit. It is also known as break even analysis that helps to

determine break even point for various levels of cost structure and sales volume that are useful

for managers to make short term economic decisions.

Flexible budgeting-

Flexible budget is a type of budget that helps to recognize the variation in difference

between variable and fixed cost to fluctuations in turnover, output etc. It is developed to change

in the relation to the level of activity attained by firm actually (Duan and et.al, 2016). This type

of budget is also called multi-volume budget. Major advantage is that it helps Prime Furniture to

forecast its performance. Major limitation is that fixed cost is generally fixed only over a

significant output range.

Absorption costing-

It refers to the approach of accumulating cost related with the process of production and

dividing them to individual products. The indirect and direct cost like direct labour, direct

material and insurance etc. are accounted for using this method.

cost per unit (absorption costing)

Figures (in

£)

Production cost(variable) 0.65

Production cost (fixed) 0.2

Cost of production per unit 0.85

Profitability statement as per absorption costing

Quarter 1

Particulars Units

per

unit

price

(in £)

Figures

(in £)

Net

figure

(in £)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

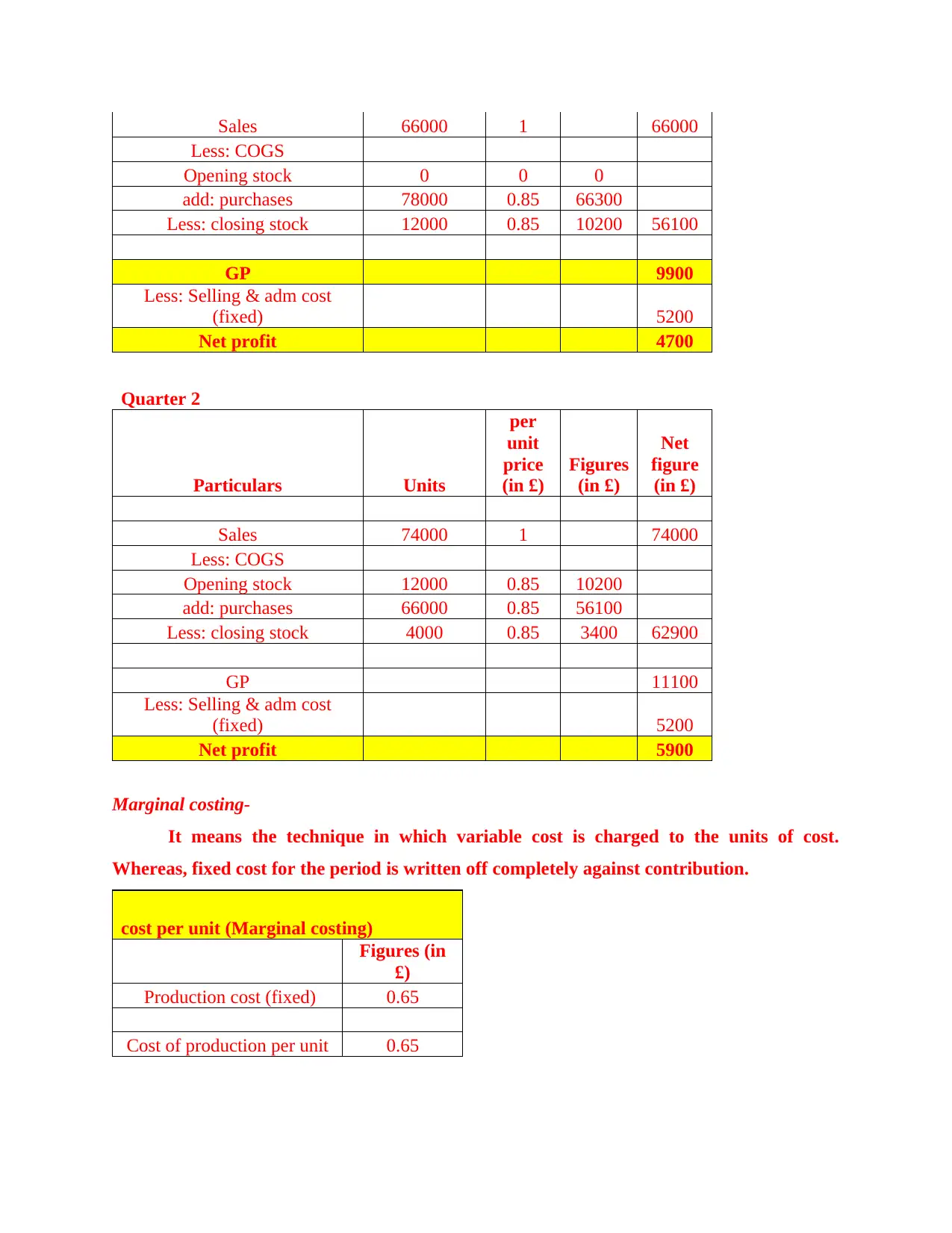

Sales 66000 1 66000

Less: COGS

Opening stock 0 0 0

add: purchases 78000 0.85 66300

Less: closing stock 12000 0.85 10200 56100

GP 9900

Less: Selling & adm cost

(fixed) 5200

Net profit 4700

Quarter 2

Particulars Units

per

unit

price

(in £)

Figures

(in £)

Net

figure

(in £)

Sales 74000 1 74000

Less: COGS

Opening stock 12000 0.85 10200

add: purchases 66000 0.85 56100

Less: closing stock 4000 0.85 3400 62900

GP 11100

Less: Selling & adm cost

(fixed) 5200

Net profit 5900

Marginal costing-

It means the technique in which variable cost is charged to the units of cost.

Whereas, fixed cost for the period is written off completely against contribution.

cost per unit (Marginal costing)

Figures (in

£)

Production cost (fixed) 0.65

Cost of production per unit 0.65

Less: COGS

Opening stock 0 0 0

add: purchases 78000 0.85 66300

Less: closing stock 12000 0.85 10200 56100

GP 9900

Less: Selling & adm cost

(fixed) 5200

Net profit 4700

Quarter 2

Particulars Units

per

unit

price

(in £)

Figures

(in £)

Net

figure

(in £)

Sales 74000 1 74000

Less: COGS

Opening stock 12000 0.85 10200

add: purchases 66000 0.85 56100

Less: closing stock 4000 0.85 3400 62900

GP 11100

Less: Selling & adm cost

(fixed) 5200

Net profit 5900

Marginal costing-

It means the technique in which variable cost is charged to the units of cost.

Whereas, fixed cost for the period is written off completely against contribution.

cost per unit (Marginal costing)

Figures (in

£)

Production cost (fixed) 0.65

Cost of production per unit 0.65

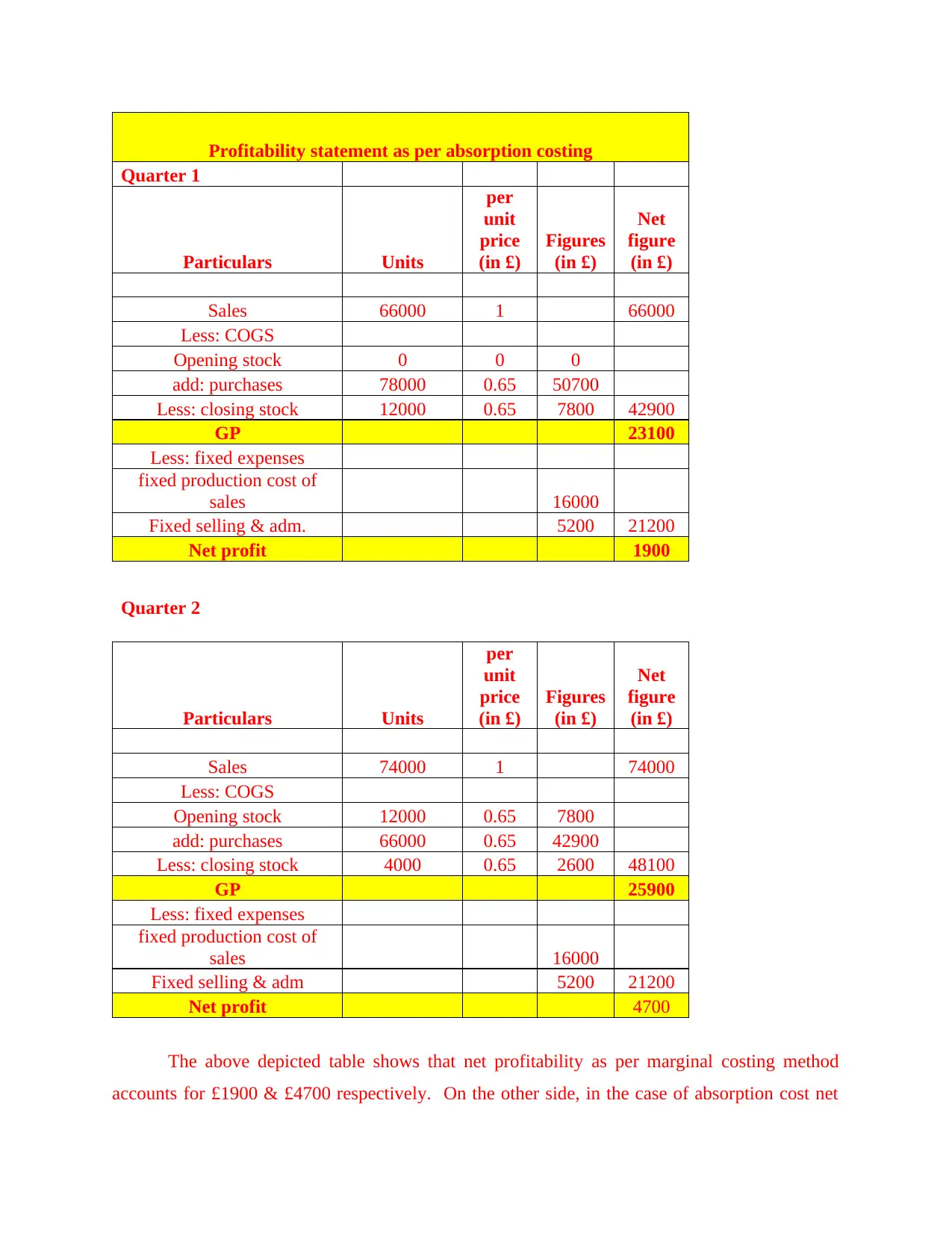

Profitability statement as per absorption costing

Quarter 1

Particulars Units

per

unit

price

(in £)

Figures

(in £)

Net

figure

(in £)

Sales 66000 1 66000

Less: COGS

Opening stock 0 0 0

add: purchases 78000 0.65 50700

Less: closing stock 12000 0.65 7800 42900

GP 23100

Less: fixed expenses

fixed production cost of

sales 16000

Fixed selling & adm. 5200 21200

Net profit 1900

Quarter 2

Particulars Units

per

unit

price

(in £)

Figures

(in £)

Net

figure

(in £)

Sales 74000 1 74000

Less: COGS

Opening stock 12000 0.65 7800

add: purchases 66000 0.65 42900

Less: closing stock 4000 0.65 2600 48100

GP 25900

Less: fixed expenses

fixed production cost of

sales 16000

Fixed selling & adm 5200 21200

Net profit 4700

The above depicted table shows that net profitability as per marginal costing method

accounts for £1900 & £4700 respectively. On the other side, in the case of absorption cost net

Quarter 1

Particulars Units

per

unit

price

(in £)

Figures

(in £)

Net

figure

(in £)

Sales 66000 1 66000

Less: COGS

Opening stock 0 0 0

add: purchases 78000 0.65 50700

Less: closing stock 12000 0.65 7800 42900

GP 23100

Less: fixed expenses

fixed production cost of

sales 16000

Fixed selling & adm. 5200 21200

Net profit 1900

Quarter 2

Particulars Units

per

unit

price

(in £)

Figures

(in £)

Net

figure

(in £)

Sales 74000 1 74000

Less: COGS

Opening stock 12000 0.65 7800

add: purchases 66000 0.65 42900

Less: closing stock 4000 0.65 2600 48100

GP 25900

Less: fixed expenses

fixed production cost of

sales 16000

Fixed selling & adm 5200 21200

Net profit 4700

The above depicted table shows that net profitability as per marginal costing method

accounts for £1900 & £4700 respectively. On the other side, in the case of absorption cost net

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profit, with respect to quarter 1 & 2 implies for £4700 and £5900 significantly. Hence, business

unit is advised to employ absorption costing method over marginal. The reason behind this at the

time of assessing production cost both fixed and variable expenses are considered. This in turn

presents clear view of cost as well as profitability aspect.

Product costing : It is the method of determining all the expenses related with developing

the products of company. It involves worker wages, raw material purchases etc. Fixed cost does

not vary with decrease or increase in the amount of products or services. Whereas, variable cost

are expenses that change in direct proportion to the units of output (Fisher, Gallino and Li,

2017).

Activity based costing- It refers to the system of costing that focuses on the tasks performed to

develop the products. Under this, firstly Prime Furniture will trace the activities and then to

products. Cost are assigned to output on basis of individual product's use of every task.

Cost of inventory :

Inventory cost- It means the cost related with purchasing, management and storage of raw

material.

Types-

Ordering cost: It is the cost of inbound logistics and procurement that forms a part of ordering

cost.

Carrying cost: It includes the cost of capital and inventory storage cost.

Methods-

Specific identification method:

Under this, cost of inventory attaches the actual expenses to an identifiable unit of output.

FIFO: It assumes that cost of goods purchased first are charged to cost of goods sold at the time

when firm actually sold goods.

LIFO: It assumes that expenses related with recent purchases are charged first to cost of goods

sold when actually firm sell output.

Weighted average: It is a means of costing the closing inventory using weighted avergae unit

cost.

unit is advised to employ absorption costing method over marginal. The reason behind this at the

time of assessing production cost both fixed and variable expenses are considered. This in turn

presents clear view of cost as well as profitability aspect.

Product costing : It is the method of determining all the expenses related with developing

the products of company. It involves worker wages, raw material purchases etc. Fixed cost does

not vary with decrease or increase in the amount of products or services. Whereas, variable cost

are expenses that change in direct proportion to the units of output (Fisher, Gallino and Li,

2017).

Activity based costing- It refers to the system of costing that focuses on the tasks performed to

develop the products. Under this, firstly Prime Furniture will trace the activities and then to

products. Cost are assigned to output on basis of individual product's use of every task.

Cost of inventory :

Inventory cost- It means the cost related with purchasing, management and storage of raw

material.

Types-

Ordering cost: It is the cost of inbound logistics and procurement that forms a part of ordering

cost.

Carrying cost: It includes the cost of capital and inventory storage cost.

Methods-

Specific identification method:

Under this, cost of inventory attaches the actual expenses to an identifiable unit of output.

FIFO: It assumes that cost of goods purchased first are charged to cost of goods sold at the time

when firm actually sold goods.

LIFO: It assumes that expenses related with recent purchases are charged first to cost of goods

sold when actually firm sell output.

Weighted average: It is a means of costing the closing inventory using weighted avergae unit

cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

L O 3

Use of planning tools that are applied in management accounting.

Using budgets for planning and control:

The term budget refers to the formal statement of estimated expenses and income that is

based on future objectives and plans. Prime Furniture may use various types of budgets such as-

Capital budget -

The term capital budget means thee procedure of evaluating huge expenses and

investments in order to get the best return on investment. It will help Prime Furniture to select

profitable project across various projects.

Major advantage is that it helps business to understand different risks involved in

investment opportunity. Limitation is that wrong decision may affect long term durability of

business.

Operating budget -

It reflects the expenses, estimated income, estimated cost by considering annual or

quarterly performance. It should consider historical sales etc. Major benefit is that it will help

Prime Furniture to work towards the aim of building financial reserves. Limitation is that if the

budget is not changes each time to reflect new figures that it will provide inaccurate results

(Maas, Schaltegger and Crutzen, 2016).

Alternative methods of budgeting-

Zero based budgeting-

It includes developing budget from scratch with zero base. It includes re-evaluating every

part of cash flow and justifying expenditure that is incurred by business.

It helps Prime Furniture to make efficient allocation of resources. It also assists organization to

identify various ways of doing things.

Major limitation is that it is very time-consuming method. It requires large number of employees.

Behavioural implications of budgets-

Dysfunctional behaviour:

Budgets may bring positive behaviour among individuals when objectives of managers

are found in consistent with goals of business.

Participative budgeting:

Use of planning tools that are applied in management accounting.

Using budgets for planning and control:

The term budget refers to the formal statement of estimated expenses and income that is

based on future objectives and plans. Prime Furniture may use various types of budgets such as-

Capital budget -

The term capital budget means thee procedure of evaluating huge expenses and

investments in order to get the best return on investment. It will help Prime Furniture to select

profitable project across various projects.

Major advantage is that it helps business to understand different risks involved in

investment opportunity. Limitation is that wrong decision may affect long term durability of

business.

Operating budget -

It reflects the expenses, estimated income, estimated cost by considering annual or

quarterly performance. It should consider historical sales etc. Major benefit is that it will help

Prime Furniture to work towards the aim of building financial reserves. Limitation is that if the

budget is not changes each time to reflect new figures that it will provide inaccurate results

(Maas, Schaltegger and Crutzen, 2016).

Alternative methods of budgeting-

Zero based budgeting-

It includes developing budget from scratch with zero base. It includes re-evaluating every

part of cash flow and justifying expenditure that is incurred by business.

It helps Prime Furniture to make efficient allocation of resources. It also assists organization to

identify various ways of doing things.

Major limitation is that it is very time-consuming method. It requires large number of employees.

Behavioural implications of budgets-

Dysfunctional behaviour:

Budgets may bring positive behaviour among individuals when objectives of managers

are found in consistent with goals of business.

Participative budgeting:

The process of budgeting is either bottom up or top down. In top down process, top

management develops budgets for organization. In bottom up approach all the people are

involved in preparing budgets (Moloney, 2016).

Pricing: It is a method used by business to set the best price for goods or services.

Pricing strategies.

Competition based pricing strategy:

Under this, company focuses on current market rate for a specific product or service. It

does not consider consumer demand.

Skimming pricing strategy:

In this, firms charge the highest possible price for new items and reduces the price over

time when product become less popular.

Common costing systems:

Actual costing-

This type of costing system only uses actual expenses that are allocated and incurred and

it does not includes budgeted or standard amount. It requires no pre planning of standard cost.

Normal costing-

It is the method that assigns cost of products on the basis of overheads, labour and

material that are used to produce them.

Standard costing system-

It is a tool for controlling, managing costs, planning budgets and evaluating cost

management performance. It also includes estimating required expenses of a production process.

Job costing-

Under this, business ascertain the cost separately for different jobs as each work order is

different from clients to clients. Cost is compiled for particular quantity of goods or services that

moves through production process (Olatunji, Oladipupo and Joshua, 2017).

Process costing-

It is the method used by firm to assign and collect manufacturing costs to the output

produced. It is used when company produces identical units.

Strategic planning:

PEST- It is a tool that helps Prime Furniture to identify the impact of external factors on

business.

management develops budgets for organization. In bottom up approach all the people are

involved in preparing budgets (Moloney, 2016).

Pricing: It is a method used by business to set the best price for goods or services.

Pricing strategies.

Competition based pricing strategy:

Under this, company focuses on current market rate for a specific product or service. It

does not consider consumer demand.

Skimming pricing strategy:

In this, firms charge the highest possible price for new items and reduces the price over

time when product become less popular.

Common costing systems:

Actual costing-

This type of costing system only uses actual expenses that are allocated and incurred and

it does not includes budgeted or standard amount. It requires no pre planning of standard cost.

Normal costing-

It is the method that assigns cost of products on the basis of overheads, labour and

material that are used to produce them.

Standard costing system-

It is a tool for controlling, managing costs, planning budgets and evaluating cost

management performance. It also includes estimating required expenses of a production process.

Job costing-

Under this, business ascertain the cost separately for different jobs as each work order is

different from clients to clients. Cost is compiled for particular quantity of goods or services that

moves through production process (Olatunji, Oladipupo and Joshua, 2017).

Process costing-

It is the method used by firm to assign and collect manufacturing costs to the output

produced. It is used when company produces identical units.

Strategic planning:

PEST- It is a tool that helps Prime Furniture to identify the impact of external factors on

business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Political: It involves factors like political stability in the country, rules and regulations of the

Government etc. Political conditions of the country will affect operations of Prime Furniture.

Economical: It includes factors like purchasing power of customers, rate of inflation etc. If

purchasing power of people is high they will spend money on purchasing furniture.

Social: It involves attitude, beliefs of people towards the company and products. Firm should

develop products as per the customer requirements (Said, 2016).

Technological: It includes change in technology of producing and distributing items to clients.

Prime Furniture should use innovative tools to make furniture items.

L O 4

Compare ways in which organizations use management accounting.

Basis Prime Furniture Triumph Furniture

Company

Financial problems Currently, firm is facing the

problem of inconsistency in

sales volume.

At present, company is facing

the issue of high expenses as

compared with operating

income.

Benchmarking It is the process of obtaining

measure. Firm uses

benchmarking to make inquiry

to facilities an processes used

by competitors (Shigaev,

2015).

Company uses benchmarks to

determine the methods adopted

by other firms operating in

furniture industry to improve

their performance. It develops

set of metrics to monitor the

expenses.

Key Performance Indicators It is the measurable value that

demonstrates how effectively

firm is attaining business

objectives. To improve the

consistency in sales Prime

Furniture uses financial

indicators like operating cash

To reduce the cost of

operations the organization

uses financial KPI's like

current ratio etc. Further, it

also uses non financial KPI's

like operations quality etc.

Government etc. Political conditions of the country will affect operations of Prime Furniture.

Economical: It includes factors like purchasing power of customers, rate of inflation etc. If

purchasing power of people is high they will spend money on purchasing furniture.

Social: It involves attitude, beliefs of people towards the company and products. Firm should

develop products as per the customer requirements (Said, 2016).

Technological: It includes change in technology of producing and distributing items to clients.

Prime Furniture should use innovative tools to make furniture items.

L O 4

Compare ways in which organizations use management accounting.

Basis Prime Furniture Triumph Furniture

Company

Financial problems Currently, firm is facing the

problem of inconsistency in

sales volume.

At present, company is facing

the issue of high expenses as

compared with operating

income.

Benchmarking It is the process of obtaining

measure. Firm uses

benchmarking to make inquiry

to facilities an processes used

by competitors (Shigaev,

2015).

Company uses benchmarks to

determine the methods adopted

by other firms operating in

furniture industry to improve

their performance. It develops

set of metrics to monitor the

expenses.

Key Performance Indicators It is the measurable value that

demonstrates how effectively

firm is attaining business

objectives. To improve the

consistency in sales Prime

Furniture uses financial

indicators like operating cash

To reduce the cost of

operations the organization

uses financial KPI's like

current ratio etc. Further, it

also uses non financial KPI's

like operations quality etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

flow etc.

Financial governance -

It is defined as the way an organization manages, collects, controls and monitor financial

nature information. It involves the way firm track financial transactions etc. It is important

because it provides accurate information and records that executives uses to dictate the direction

based on business financial reality.

Management accounting skill-

Characteristics of effective management accountant:

Effective management accountant possess features like a strong sense of ethics, sense of

accountability, ability to work in a team etc.

These skills help management accountant of Prime Furniture to deal with complex

business situations. It also helps to coordinate accounting operations, maintaining budgets etc

(Said, 2016).

Effective strategies and systems-

Inefficient management processes that provides wrong information generally causes more

harm than good. Strong management reporting is required to produce reliable, timely

information. It helps to make better quality business decisions regarding the future of the

business. Insight collected from reporting helps to make deeper analysis to understand problems

and to offer right comparison against competitors.

CONCLUSION

The above Report has outlined that there are various types of cost such as fixed cost,

variable cost, semi-variable cost etc. Cost volume profit analysis is the method of cost

accounting that focuses at the effect that different levels of volume and cost have on operating

profit Further, it has been concluded that fixed cost does not changes with decrease or increase in

the amount of products or services. The two major types of inventory cost are ordering and

carrying cost.

REFERENCES

Books and Journals -

Childress, S., and et.al, 2015. Using an activity-based model to explore the potential impacts of

automated vehicles. Transportation Research Record. 2493(1). pp.99-106.

Financial governance -

It is defined as the way an organization manages, collects, controls and monitor financial

nature information. It involves the way firm track financial transactions etc. It is important

because it provides accurate information and records that executives uses to dictate the direction

based on business financial reality.

Management accounting skill-

Characteristics of effective management accountant:

Effective management accountant possess features like a strong sense of ethics, sense of

accountability, ability to work in a team etc.

These skills help management accountant of Prime Furniture to deal with complex

business situations. It also helps to coordinate accounting operations, maintaining budgets etc

(Said, 2016).

Effective strategies and systems-

Inefficient management processes that provides wrong information generally causes more

harm than good. Strong management reporting is required to produce reliable, timely

information. It helps to make better quality business decisions regarding the future of the

business. Insight collected from reporting helps to make deeper analysis to understand problems

and to offer right comparison against competitors.

CONCLUSION

The above Report has outlined that there are various types of cost such as fixed cost,

variable cost, semi-variable cost etc. Cost volume profit analysis is the method of cost

accounting that focuses at the effect that different levels of volume and cost have on operating

profit Further, it has been concluded that fixed cost does not changes with decrease or increase in

the amount of products or services. The two major types of inventory cost are ordering and

carrying cost.

REFERENCES

Books and Journals -

Childress, S., and et.al, 2015. Using an activity-based model to explore the potential impacts of

automated vehicles. Transportation Research Record. 2493(1). pp.99-106.

Christian, D., 2018. Building Cost Management: Case Study Using Costing Methods. IJAME.

Duan, Y., and et.al, 2016, June. Benchmarking deep reinforcement learning for continuous

control. In International Conference on Machine Learning (pp. 1329-1338).

Fisher, M., Gallino, S. and Li, J., 2017. Competition-based dynamic pricing in online retailing: A

methodology validated with field experiments. Management Science. 64(6). pp.2496-2514.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136. pp.237-

248.

Moloney, N., 2016. International financial governance, the EU, and Brexit: the ‘agencification’of

EU financial governance and the implications. European Business Organization Law Review.

17(4). pp.451-480.

Olatunji, O.C., Oladipupo, O.F. and Joshua, A.A., 2017. Impact of Capital Budget

Implementation on Economic Growth in Nigeria. Global Journal of Management And

Business Research.

Said, H.A., 2016. Using Different Probability Distributions for Managerial Accounting

Technique: The Cost-Volume-Profit Analysis. Journal of Business and Accounting. 9(1). p.3.

Shigaev, A., 2015. Accounting entries for activity-based costing system: The case of a

distribution company. Procedia Economics and Finance. 24. pp.625-633.

Duan, Y., and et.al, 2016, June. Benchmarking deep reinforcement learning for continuous

control. In International Conference on Machine Learning (pp. 1329-1338).

Fisher, M., Gallino, S. and Li, J., 2017. Competition-based dynamic pricing in online retailing: A

methodology validated with field experiments. Management Science. 64(6). pp.2496-2514.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136. pp.237-

248.

Moloney, N., 2016. International financial governance, the EU, and Brexit: the ‘agencification’of

EU financial governance and the implications. European Business Organization Law Review.

17(4). pp.451-480.

Olatunji, O.C., Oladipupo, O.F. and Joshua, A.A., 2017. Impact of Capital Budget

Implementation on Economic Growth in Nigeria. Global Journal of Management And

Business Research.

Said, H.A., 2016. Using Different Probability Distributions for Managerial Accounting

Technique: The Cost-Volume-Profit Analysis. Journal of Business and Accounting. 9(1). p.3.

Shigaev, A., 2015. Accounting entries for activity-based costing system: The case of a

distribution company. Procedia Economics and Finance. 24. pp.625-633.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.