Management Accounting Report: IKEA Financial Performance Analysis

VerifiedAdded on 2022/12/26

|16

|4191

|83

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its principles, techniques, and practical applications within an organizational context. The report begins by defining management accounting and its importance in strategic decision-making, emphasizing its role in resource allocation and performance improvement. It then explores different types of accounting systems, including cost accounting, inventory management, and job order costing, highlighting their features, advantages, and disadvantages. The report delves into the principles of management accounting, such as influence, relevance, value, and credibility, and explains how these principles guide the application of various techniques. Furthermore, the report analyzes management accounting reporting and implementation, covering budget reporting, accounts receivables reporting, job costing reporting, and performance reporting. It also includes a detailed comparison of marginal and absorption costing methods, using financial data from Marwa Limited to illustrate their impact on profit calculation. The report concludes by discussing how organizations adapt management accounting systems to address financial problems, making it a valuable resource for students and professionals seeking to understand and apply management accounting principles.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1. Management accounting and requirements of different types of accounting systems.........3

a. Features and Principles............................................................................................................3

P2. Management accounting reporting and implementation.......................................................6

P3. Techniques of cost analysis and interpretation.....................................................................7

P4. Planning tools in management accounting.........................................................................10

P5. Ways the organisation are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1. Management accounting and requirements of different types of accounting systems.........3

a. Features and Principles............................................................................................................3

P2. Management accounting reporting and implementation.......................................................6

P3. Techniques of cost analysis and interpretation.....................................................................7

P4. Planning tools in management accounting.........................................................................10

P5. Ways the organisation are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is an important element that helps in the managers to take

strategic decisions. The methods and techniques that forms management accounting and the

usage and implementation of it is popular among the management of the organisations. The use

of financial instruments of the management accounting helps in the improvement of the

organisation's performance. It aims for the efficient use and allocation of the resources within the

process by keeping the cost drivers low (Nørreklit, H. ed., 2017). The report highlights the

analysis of the financial information of the company IKEA a producer of children’s scooters

which started operations on 1st January 2019. The marginal costing approach and absorption

costing approach is being introduced to find out the valuation of the stocks. Further in this report

the advantages and disadvantages of the various planning and budgetary tools are highlighted. At

the end of the report the use of management accounting in solving financial problems is outlined.

MAIN BODY

P1. Management accounting and requirements of different types of accounting systems

Management accounting is the execution of strategic planning and resource allocation in

such a way that it provide maximum productivity (Collis and Hussey, 2017).

Management accounting provides important information of costs of the various functions of the

business to helps in cost control and the preparation of budgets to track the performance and

proper allocation of the resources (Drury, 2018). The effective implementation of the methods

and systems by the managers of the IKEA helps in the improvement of the output and hence

increase the performance of the organisation.

a. Features and Principles

The management accounting systems provides information related to finance to the managers of

the company. It shows the analysis of costs that affects the operation and revenue of the

organisation. Use of different tools like marginal costing, absorption costing, ratio analysis, etc.

that uses accounting data. Management accounting helps in forecasting and setting of standards

that helps in improving efficiency of the organisation.

There are 4 basic principles that adopted in management accounting that are as follows:

Influence

Management accounting is an important element that helps in the managers to take

strategic decisions. The methods and techniques that forms management accounting and the

usage and implementation of it is popular among the management of the organisations. The use

of financial instruments of the management accounting helps in the improvement of the

organisation's performance. It aims for the efficient use and allocation of the resources within the

process by keeping the cost drivers low (Nørreklit, H. ed., 2017). The report highlights the

analysis of the financial information of the company IKEA a producer of children’s scooters

which started operations on 1st January 2019. The marginal costing approach and absorption

costing approach is being introduced to find out the valuation of the stocks. Further in this report

the advantages and disadvantages of the various planning and budgetary tools are highlighted. At

the end of the report the use of management accounting in solving financial problems is outlined.

MAIN BODY

P1. Management accounting and requirements of different types of accounting systems

Management accounting is the execution of strategic planning and resource allocation in

such a way that it provide maximum productivity (Collis and Hussey, 2017).

Management accounting provides important information of costs of the various functions of the

business to helps in cost control and the preparation of budgets to track the performance and

proper allocation of the resources (Drury, 2018). The effective implementation of the methods

and systems by the managers of the IKEA helps in the improvement of the output and hence

increase the performance of the organisation.

a. Features and Principles

The management accounting systems provides information related to finance to the managers of

the company. It shows the analysis of costs that affects the operation and revenue of the

organisation. Use of different tools like marginal costing, absorption costing, ratio analysis, etc.

that uses accounting data. Management accounting helps in forecasting and setting of standards

that helps in improving efficiency of the organisation.

There are 4 basic principles that adopted in management accounting that are as follows:

Influence

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting helps in to find out the impact of various activities of the organisation

on each other. By analysis of different types of costs managers will be able to influence the

overall costs.

Relevance

Management accounting use past and present data for the analysis of the effect of costs and

results in future estimations.

Value

Management accounting helps in identification of the unnecessary activities in the production

process and through budgeting managers are able to establish reasonable pricing of the products

and services.

Credibility

Management accounting helps in the taking informed decision based on critical analysis and

ethical practices. It generates credibility for the stakeholders of the organisation.

Types of management accounting systems

Cost Accounting

In this method of accounting Several costs are calculated viz. variable costs, fixed cost

and Semi-variable costs. These costs arises in the production process and the estimation of these

cost required helps to ascertain the profit and per unit contribution (Wang and et.al, 2020). The

methods and techniques helps IKEA to find out how much cost is incurred in the production

process and helps the managers to device strategies that reduce the cost of production. Example:

Cost accounting calculate both specific and overall cost. That will help to reduce costs

Advantages of cost accounting

The cost accounting method will be adopted easily and helps the IKEA's management to

find the total cost of the production and the overheads that can be controlled to maximize the

revenue of the company.

Disadvantages of cost accounting

For the adoption of the cost accounting, managers have the knowledge of the system.

What are the constraints used and understanding of the accounting methods.

Inventory Management

Management of the inventory also incur costs. Effective management of the stocks of the

company IKEA is done with the help of different methods of inventory systems viz. First In First

on each other. By analysis of different types of costs managers will be able to influence the

overall costs.

Relevance

Management accounting use past and present data for the analysis of the effect of costs and

results in future estimations.

Value

Management accounting helps in identification of the unnecessary activities in the production

process and through budgeting managers are able to establish reasonable pricing of the products

and services.

Credibility

Management accounting helps in the taking informed decision based on critical analysis and

ethical practices. It generates credibility for the stakeholders of the organisation.

Types of management accounting systems

Cost Accounting

In this method of accounting Several costs are calculated viz. variable costs, fixed cost

and Semi-variable costs. These costs arises in the production process and the estimation of these

cost required helps to ascertain the profit and per unit contribution (Wang and et.al, 2020). The

methods and techniques helps IKEA to find out how much cost is incurred in the production

process and helps the managers to device strategies that reduce the cost of production. Example:

Cost accounting calculate both specific and overall cost. That will help to reduce costs

Advantages of cost accounting

The cost accounting method will be adopted easily and helps the IKEA's management to

find the total cost of the production and the overheads that can be controlled to maximize the

revenue of the company.

Disadvantages of cost accounting

For the adoption of the cost accounting, managers have the knowledge of the system.

What are the constraints used and understanding of the accounting methods.

Inventory Management

Management of the inventory also incur costs. Effective management of the stocks of the

company IKEA is done with the help of different methods of inventory systems viz. First In First

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Out, Last In First Out, Average inventory method, etc. Presently, soft-wares are use to review

and checks the inventories in the vicinity which reduce the resources, time and funds (Wild, T.,

2017). Example: Use of FIFO method helps in balancing the effect of inflation by dispatching

costly inventory in last.

Advantages of inventory management

The system reduces the complexities of the managing stocks of the company. The IKEA

with the introduction of inventory management system saves much time and resources and can

promptly complete the order processing of the clients.

Disadvantages of inventory management

The implementation of the inventory system is complex and expensive. The IKEA

managers should analyse the impact on cost before introducing the system.

Job order costing

This system consider every job and the cost of each job of specific process of production.

The job order costing accumulate three different costs namely direct materials, direct labour and

overheads. Example: Organisation calculate and assign each cost to specific job that helps in

calculation of overall cost and accordingly strategies can be made.

Advantages of job order costing

As the costs for each job ascertained separately the profits arises from the jobs are

calculated separately. The company IKEA with the comparison of the actual costs from the

predetermined cost will check the performance of the production.

Disadvantages of job order costing

The system has no standard process of costing and is a time consuming and expensive.

The precise cost of the production is not easily calculated as sizeable number of jobs are

evaluated at the time of job costing.

Price optimisation

This system helps to calculate demand of the products at various price levels. There are 4

pricing strategies namely premium, skimming, value and penetration (Nakhe, P., 2017). The

information gathered from the analysis of the demand then combined with inventories and costs

to find out the level where the profits are maximised. Example: Organisation at different period

of time use distinct pricing strategies to optimise its revenue.

Advantages of price optimisation

and checks the inventories in the vicinity which reduce the resources, time and funds (Wild, T.,

2017). Example: Use of FIFO method helps in balancing the effect of inflation by dispatching

costly inventory in last.

Advantages of inventory management

The system reduces the complexities of the managing stocks of the company. The IKEA

with the introduction of inventory management system saves much time and resources and can

promptly complete the order processing of the clients.

Disadvantages of inventory management

The implementation of the inventory system is complex and expensive. The IKEA

managers should analyse the impact on cost before introducing the system.

Job order costing

This system consider every job and the cost of each job of specific process of production.

The job order costing accumulate three different costs namely direct materials, direct labour and

overheads. Example: Organisation calculate and assign each cost to specific job that helps in

calculation of overall cost and accordingly strategies can be made.

Advantages of job order costing

As the costs for each job ascertained separately the profits arises from the jobs are

calculated separately. The company IKEA with the comparison of the actual costs from the

predetermined cost will check the performance of the production.

Disadvantages of job order costing

The system has no standard process of costing and is a time consuming and expensive.

The precise cost of the production is not easily calculated as sizeable number of jobs are

evaluated at the time of job costing.

Price optimisation

This system helps to calculate demand of the products at various price levels. There are 4

pricing strategies namely premium, skimming, value and penetration (Nakhe, P., 2017). The

information gathered from the analysis of the demand then combined with inventories and costs

to find out the level where the profits are maximised. Example: Organisation at different period

of time use distinct pricing strategies to optimise its revenue.

Advantages of price optimisation

The system helps in generating profits from increase in sales by offering discounted

prices. It helps IKEA to find out best price levels.

Disadvantages of price optimisation

Various pricing strategies are implemented to find out the best strategy which is complex

and expensive.

P2. Management accounting reporting and implementation

Budget reporting

It is a process of preparation of the report that represents the production level over a

period of time. Comparison between actual and estimated figures are made to track the

performance of the company. It helps IKEA to measure each department's productivity and to

make strategic decisions to improve the performance.

Accounts receivables reporting

A report is prepared highlighting the due accounts receivables over the financial period.

Customer are identified and a analysis is made to calculate bad debts. IKEA from the analysis of

the reporting make strategies targeting specific debtors to recover the bad debts (Weygandt and

et.al, 2018).

Job costing reporting

The preparation of the report is based on the cost related to each job in an activity

process. The managers identifies the useful jobs and assign priorities accordingly. It helps IKEA

to track overheads of the production and take necessary steps to control the cost.

Performance Reporting

In this process a report is prepared that highlights the achievements of the company over

the financial year. The actual output is compared with the standardised estimates to watch over

the performance and relevant strategies are made to further correct or improve the performance

information of IKEA's sales of the previous financial year is compared to the sales information

of the current financial year to check the performance.

Inventory and manufacturing reporting

The reporting highlights the inventory position. The costs of ordering, carrying and

opportunity is calculated. It shows the management the flow of inventory and storage levels

(Wild, T., 2017). The lead time and re-order level helps IKEA to point out demand of the

product in the market.

prices. It helps IKEA to find out best price levels.

Disadvantages of price optimisation

Various pricing strategies are implemented to find out the best strategy which is complex

and expensive.

P2. Management accounting reporting and implementation

Budget reporting

It is a process of preparation of the report that represents the production level over a

period of time. Comparison between actual and estimated figures are made to track the

performance of the company. It helps IKEA to measure each department's productivity and to

make strategic decisions to improve the performance.

Accounts receivables reporting

A report is prepared highlighting the due accounts receivables over the financial period.

Customer are identified and a analysis is made to calculate bad debts. IKEA from the analysis of

the reporting make strategies targeting specific debtors to recover the bad debts (Weygandt and

et.al, 2018).

Job costing reporting

The preparation of the report is based on the cost related to each job in an activity

process. The managers identifies the useful jobs and assign priorities accordingly. It helps IKEA

to track overheads of the production and take necessary steps to control the cost.

Performance Reporting

In this process a report is prepared that highlights the achievements of the company over

the financial year. The actual output is compared with the standardised estimates to watch over

the performance and relevant strategies are made to further correct or improve the performance

information of IKEA's sales of the previous financial year is compared to the sales information

of the current financial year to check the performance.

Inventory and manufacturing reporting

The reporting highlights the inventory position. The costs of ordering, carrying and

opportunity is calculated. It shows the management the flow of inventory and storage levels

(Wild, T., 2017). The lead time and re-order level helps IKEA to point out demand of the

product in the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Order information reporting

The reporting signify the supply of the inventory. The orders made by the customers at a

particular time period are tracked and recorded. It helps IKEA to find out real-time ordering

status.

Business situation or opportunity reporting

The reporting highlights the comprehensive report of the different market conditions and

the list of opportunities arises. Variables are reviewed and specific strategies are prepared from

the analysis of the variables to take effective measures and procurement of the required resources

when the right opportunity arises and market is in favourable condition (Miller, G., 2018).

P3. Techniques of cost analysis and interpretation

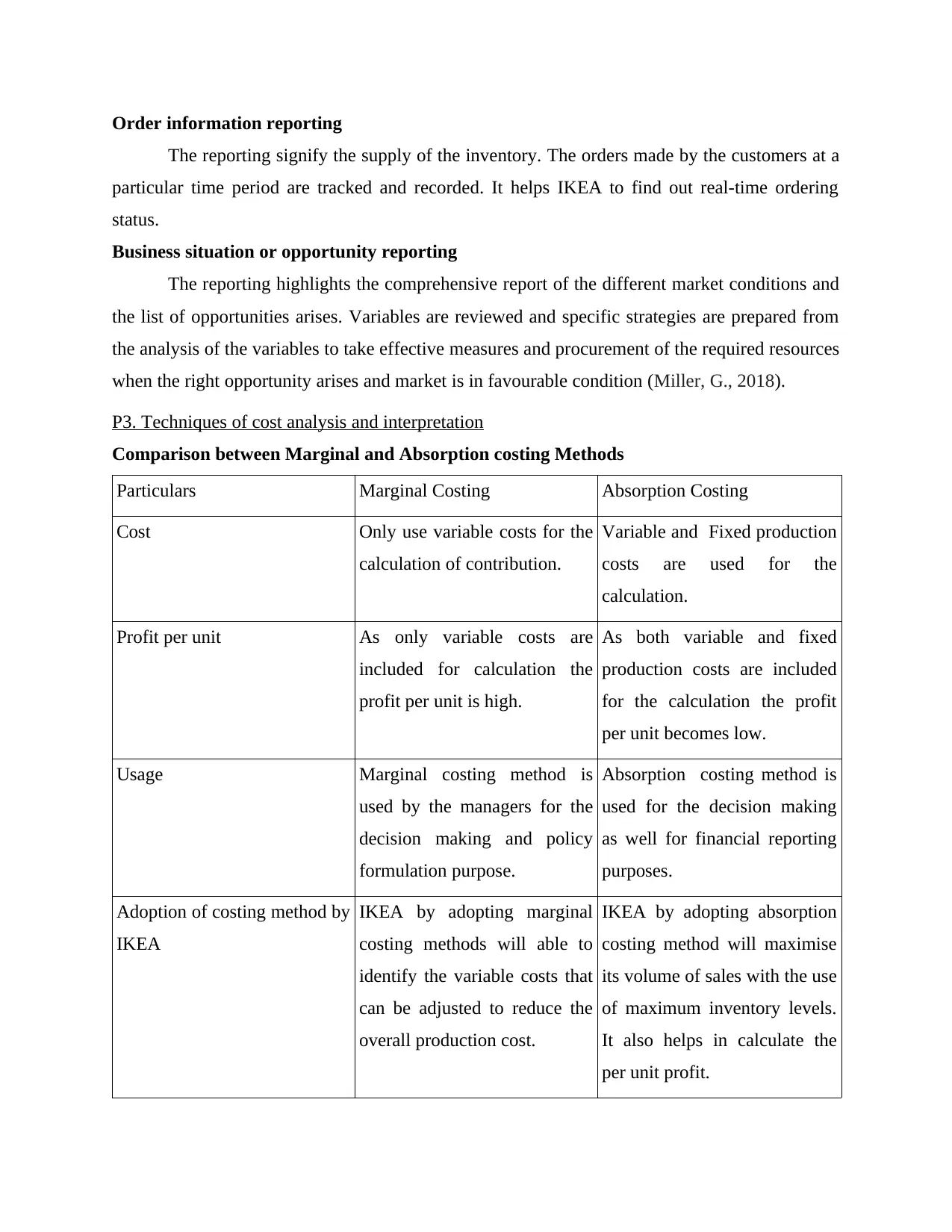

Comparison between Marginal and Absorption costing Methods

Particulars Marginal Costing Absorption Costing

Cost Only use variable costs for the

calculation of contribution.

Variable and Fixed production

costs are used for the

calculation.

Profit per unit As only variable costs are

included for calculation the

profit per unit is high.

As both variable and fixed

production costs are included

for the calculation the profit

per unit becomes low.

Usage Marginal costing method is

used by the managers for the

decision making and policy

formulation purpose.

Absorption costing method is

used for the decision making

as well for financial reporting

purposes.

Adoption of costing method by

IKEA

IKEA by adopting marginal

costing methods will able to

identify the variable costs that

can be adjusted to reduce the

overall production cost.

IKEA by adopting absorption

costing method will maximise

its volume of sales with the use

of maximum inventory levels.

It also helps in calculate the

per unit profit.

The reporting signify the supply of the inventory. The orders made by the customers at a

particular time period are tracked and recorded. It helps IKEA to find out real-time ordering

status.

Business situation or opportunity reporting

The reporting highlights the comprehensive report of the different market conditions and

the list of opportunities arises. Variables are reviewed and specific strategies are prepared from

the analysis of the variables to take effective measures and procurement of the required resources

when the right opportunity arises and market is in favourable condition (Miller, G., 2018).

P3. Techniques of cost analysis and interpretation

Comparison between Marginal and Absorption costing Methods

Particulars Marginal Costing Absorption Costing

Cost Only use variable costs for the

calculation of contribution.

Variable and Fixed production

costs are used for the

calculation.

Profit per unit As only variable costs are

included for calculation the

profit per unit is high.

As both variable and fixed

production costs are included

for the calculation the profit

per unit becomes low.

Usage Marginal costing method is

used by the managers for the

decision making and policy

formulation purpose.

Absorption costing method is

used for the decision making

as well for financial reporting

purposes.

Adoption of costing method by

IKEA

IKEA by adopting marginal

costing methods will able to

identify the variable costs that

can be adjusted to reduce the

overall production cost.

IKEA by adopting absorption

costing method will maximise

its volume of sales with the use

of maximum inventory levels.

It also helps in calculate the

per unit profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

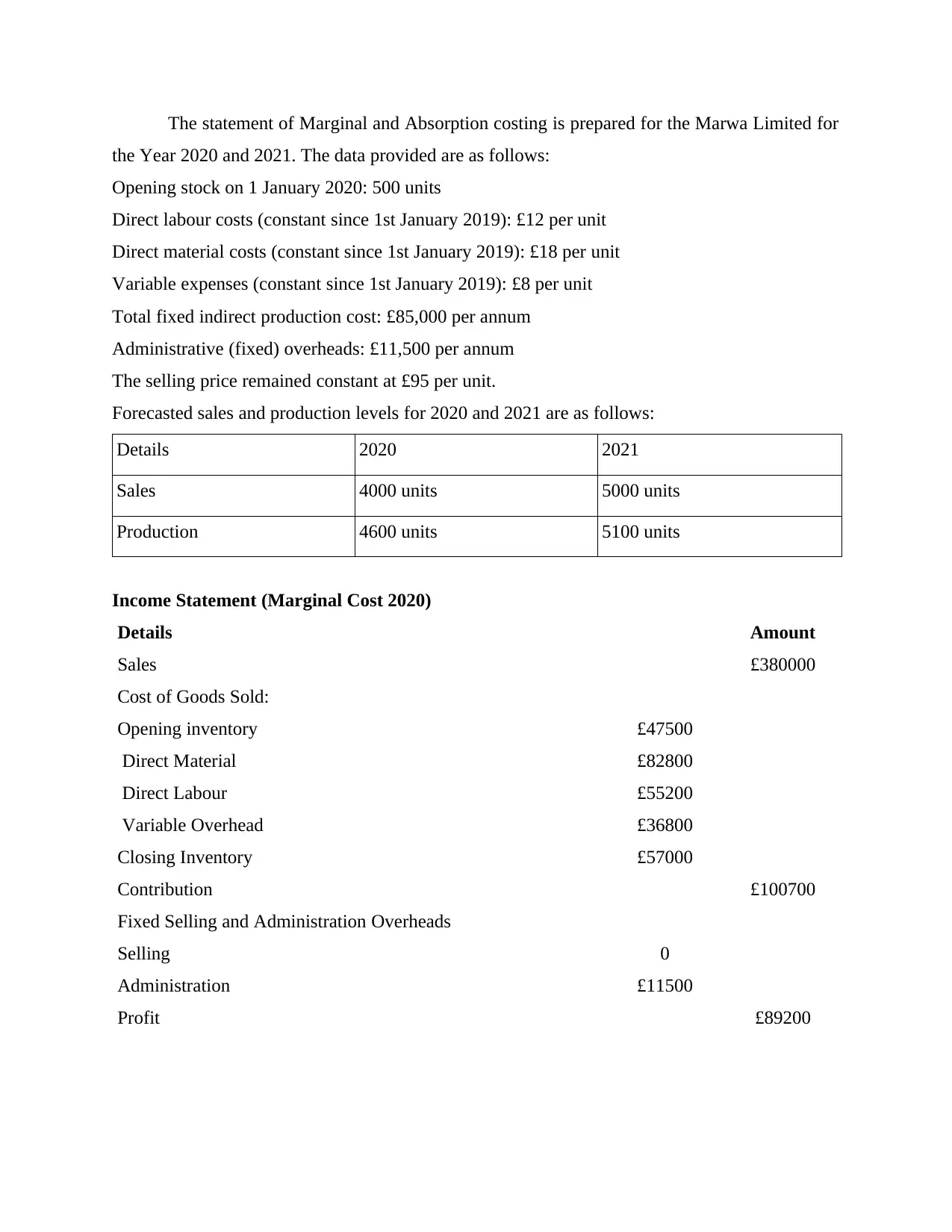

The statement of Marginal and Absorption costing is prepared for the Marwa Limited for

the Year 2020 and 2021. The data provided are as follows:

Opening stock on 1 January 2020: 500 units

Direct labour costs (constant since 1st January 2019): £12 per unit

Direct material costs (constant since 1st January 2019): £18 per unit

Variable expenses (constant since 1st January 2019): £8 per unit

Total fixed indirect production cost: £85,000 per annum

Administrative (fixed) overheads: £11,500 per annum

The selling price remained constant at £95 per unit.

Forecasted sales and production levels for 2020 and 2021 are as follows:

Details 2020 2021

Sales 4000 units 5000 units

Production 4600 units 5100 units

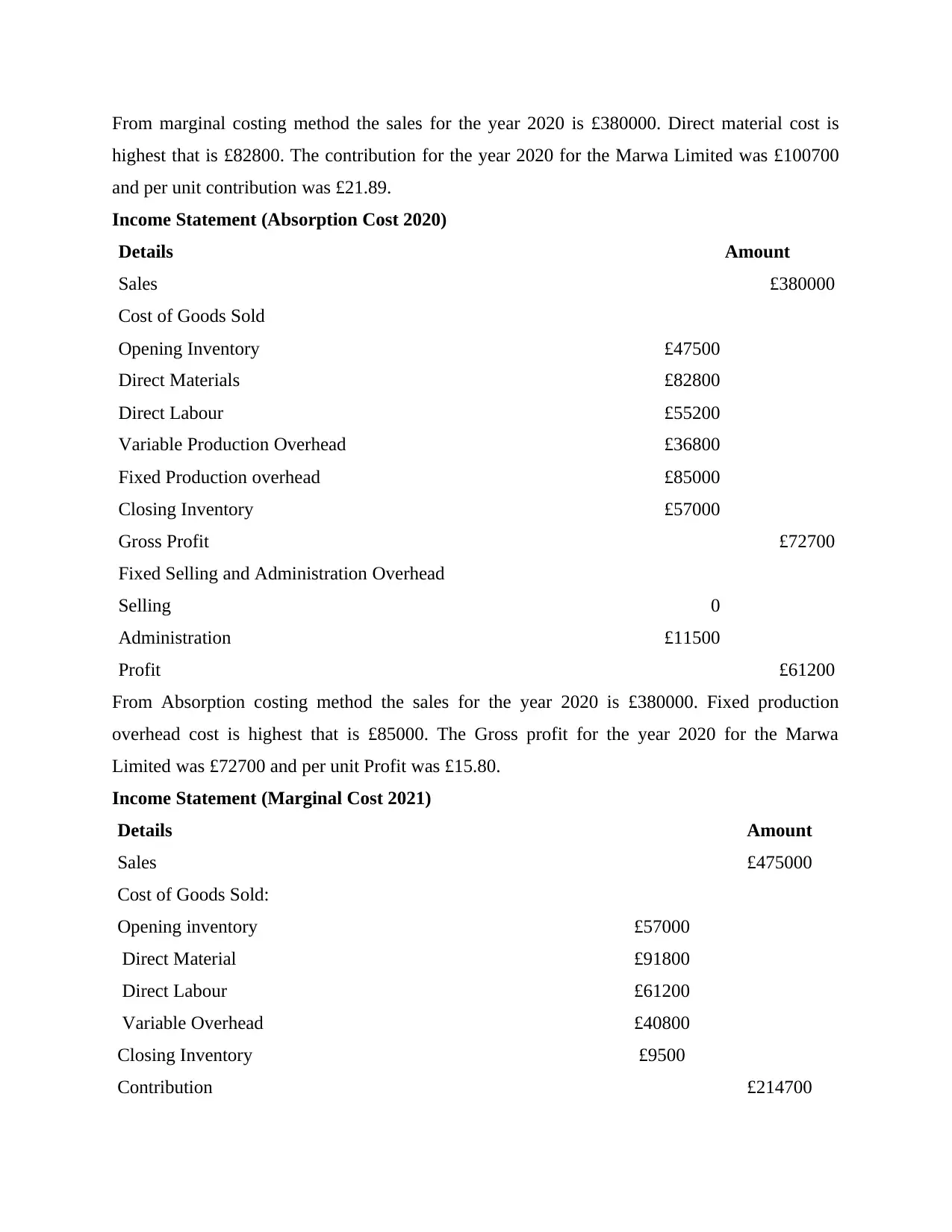

Income Statement (Marginal Cost 2020)

Details Amount

Sales £380000

Cost of Goods Sold:

Opening inventory £47500

Direct Material £82800

Direct Labour £55200

Variable Overhead £36800

Closing Inventory £57000

Contribution £100700

Fixed Selling and Administration Overheads

Selling 0

Administration £11500

Profit £89200

the Year 2020 and 2021. The data provided are as follows:

Opening stock on 1 January 2020: 500 units

Direct labour costs (constant since 1st January 2019): £12 per unit

Direct material costs (constant since 1st January 2019): £18 per unit

Variable expenses (constant since 1st January 2019): £8 per unit

Total fixed indirect production cost: £85,000 per annum

Administrative (fixed) overheads: £11,500 per annum

The selling price remained constant at £95 per unit.

Forecasted sales and production levels for 2020 and 2021 are as follows:

Details 2020 2021

Sales 4000 units 5000 units

Production 4600 units 5100 units

Income Statement (Marginal Cost 2020)

Details Amount

Sales £380000

Cost of Goods Sold:

Opening inventory £47500

Direct Material £82800

Direct Labour £55200

Variable Overhead £36800

Closing Inventory £57000

Contribution £100700

Fixed Selling and Administration Overheads

Selling 0

Administration £11500

Profit £89200

From marginal costing method the sales for the year 2020 is £380000. Direct material cost is

highest that is £82800. The contribution for the year 2020 for the Marwa Limited was £100700

and per unit contribution was £21.89.

Income Statement (Absorption Cost 2020)

Details Amount

Sales £380000

Cost of Goods Sold

Opening Inventory £47500

Direct Materials £82800

Direct Labour £55200

Variable Production Overhead £36800

Fixed Production overhead £85000

Closing Inventory £57000

Gross Profit £72700

Fixed Selling and Administration Overhead

Selling 0

Administration £11500

Profit £61200

From Absorption costing method the sales for the year 2020 is £380000. Fixed production

overhead cost is highest that is £85000. The Gross profit for the year 2020 for the Marwa

Limited was £72700 and per unit Profit was £15.80.

Income Statement (Marginal Cost 2021)

Details Amount

Sales £475000

Cost of Goods Sold:

Opening inventory £57000

Direct Material £91800

Direct Labour £61200

Variable Overhead £40800

Closing Inventory £9500

Contribution £214700

highest that is £82800. The contribution for the year 2020 for the Marwa Limited was £100700

and per unit contribution was £21.89.

Income Statement (Absorption Cost 2020)

Details Amount

Sales £380000

Cost of Goods Sold

Opening Inventory £47500

Direct Materials £82800

Direct Labour £55200

Variable Production Overhead £36800

Fixed Production overhead £85000

Closing Inventory £57000

Gross Profit £72700

Fixed Selling and Administration Overhead

Selling 0

Administration £11500

Profit £61200

From Absorption costing method the sales for the year 2020 is £380000. Fixed production

overhead cost is highest that is £85000. The Gross profit for the year 2020 for the Marwa

Limited was £72700 and per unit Profit was £15.80.

Income Statement (Marginal Cost 2021)

Details Amount

Sales £475000

Cost of Goods Sold:

Opening inventory £57000

Direct Material £91800

Direct Labour £61200

Variable Overhead £40800

Closing Inventory £9500

Contribution £214700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

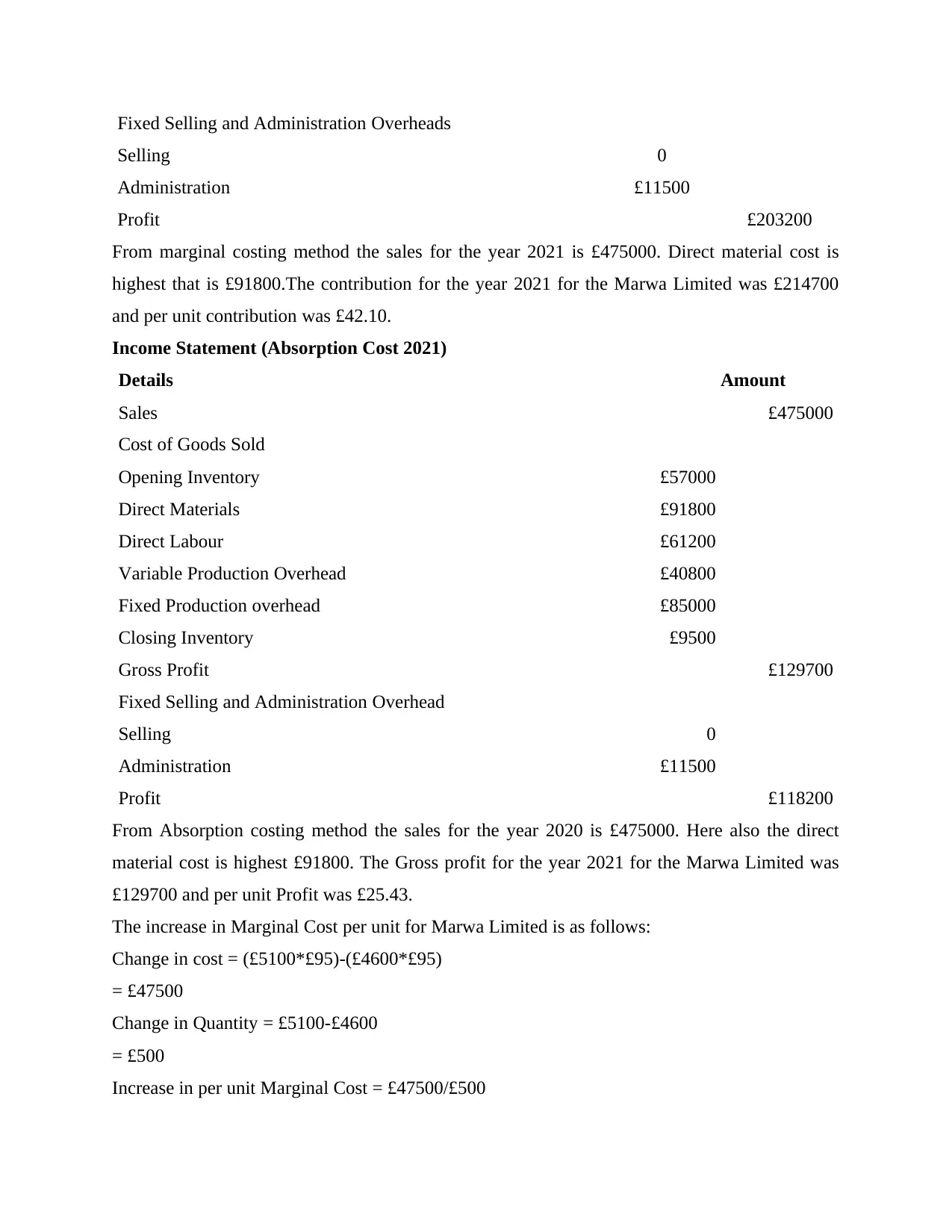

Fixed Selling and Administration Overheads

Selling 0

Administration £11500

Profit £203200

From marginal costing method the sales for the year 2021 is £475000. Direct material cost is

highest that is £91800.The contribution for the year 2021 for the Marwa Limited was £214700

and per unit contribution was £42.10.

Income Statement (Absorption Cost 2021)

Details Amount

Sales £475000

Cost of Goods Sold

Opening Inventory £57000

Direct Materials £91800

Direct Labour £61200

Variable Production Overhead £40800

Fixed Production overhead £85000

Closing Inventory £9500

Gross Profit £129700

Fixed Selling and Administration Overhead

Selling 0

Administration £11500

Profit £118200

From Absorption costing method the sales for the year 2020 is £475000. Here also the direct

material cost is highest £91800. The Gross profit for the year 2021 for the Marwa Limited was

£129700 and per unit Profit was £25.43.

The increase in Marginal Cost per unit for Marwa Limited is as follows:

Change in cost = (£5100*£95)-(£4600*£95)

= £47500

Change in Quantity = £5100-£4600

= £500

Increase in per unit Marginal Cost = £47500/£500

Selling 0

Administration £11500

Profit £203200

From marginal costing method the sales for the year 2021 is £475000. Direct material cost is

highest that is £91800.The contribution for the year 2021 for the Marwa Limited was £214700

and per unit contribution was £42.10.

Income Statement (Absorption Cost 2021)

Details Amount

Sales £475000

Cost of Goods Sold

Opening Inventory £57000

Direct Materials £91800

Direct Labour £61200

Variable Production Overhead £40800

Fixed Production overhead £85000

Closing Inventory £9500

Gross Profit £129700

Fixed Selling and Administration Overhead

Selling 0

Administration £11500

Profit £118200

From Absorption costing method the sales for the year 2020 is £475000. Here also the direct

material cost is highest £91800. The Gross profit for the year 2021 for the Marwa Limited was

£129700 and per unit Profit was £25.43.

The increase in Marginal Cost per unit for Marwa Limited is as follows:

Change in cost = (£5100*£95)-(£4600*£95)

= £47500

Change in Quantity = £5100-£4600

= £500

Increase in per unit Marginal Cost = £47500/£500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= £95

Interpretation

The marginal costing uses the variable costs to calculate the margin per product for the

period and per unit margin. While the absorption costing uses fixed cost along with the variable

cost that increase the cost and decrease the revenue. As from the above analysis, it has been seen

that the profit in marginal costing in the year 2021 is £203200 while in absorption costing

because of the addition of the fixed production overhead the profit for the year 2021 is decreases

to £118200. As sales for the period 2021 is increases from the period 2020l. So, the amount of

profit also increases from 2020 to 2021 in both marginal and absorption costing.

P4. Planning tools in management accounting

Budgetary Control

It is a management accounting technique used for management control. In this system a

estimated budget is prepared and forecasting of resources and funds needed for the production

process in the financial year is done. It helps IKEA to resolve the issues related to allocation of

resources and expenses during the period (Schiavo-Campo, S., 2017). For the preparation of

budget, past records of the company is gathered and analysed. The actual production than

compared to forecasted production to track performance for the period.

Tools for the Budgetary Control

Incremental Budget

It is simple and traditional budget preparation method. Organisations prepare new budget

by addition or reduction in the values to the past budget. The company IKEA will be able to

prepare an entirely new budget just by changing the values of the past years budget.

Advantages

This type of budget is comparatively simple and easy to implement.

The resource allocation for various departments of the company can be done without any issue.

Incremental Budget have fewer complexities of calculations for preparation of new budget.

Disadvantages

In this type of budget there are fewer changes as only marginal increments/decrements in the

past data is done.

If there is a need for the major restructuring this type of budgeting becomes irrelevant.

It did not take into consideration any new change in production process.

Interpretation

The marginal costing uses the variable costs to calculate the margin per product for the

period and per unit margin. While the absorption costing uses fixed cost along with the variable

cost that increase the cost and decrease the revenue. As from the above analysis, it has been seen

that the profit in marginal costing in the year 2021 is £203200 while in absorption costing

because of the addition of the fixed production overhead the profit for the year 2021 is decreases

to £118200. As sales for the period 2021 is increases from the period 2020l. So, the amount of

profit also increases from 2020 to 2021 in both marginal and absorption costing.

P4. Planning tools in management accounting

Budgetary Control

It is a management accounting technique used for management control. In this system a

estimated budget is prepared and forecasting of resources and funds needed for the production

process in the financial year is done. It helps IKEA to resolve the issues related to allocation of

resources and expenses during the period (Schiavo-Campo, S., 2017). For the preparation of

budget, past records of the company is gathered and analysed. The actual production than

compared to forecasted production to track performance for the period.

Tools for the Budgetary Control

Incremental Budget

It is simple and traditional budget preparation method. Organisations prepare new budget

by addition or reduction in the values to the past budget. The company IKEA will be able to

prepare an entirely new budget just by changing the values of the past years budget.

Advantages

This type of budget is comparatively simple and easy to implement.

The resource allocation for various departments of the company can be done without any issue.

Incremental Budget have fewer complexities of calculations for preparation of new budget.

Disadvantages

In this type of budget there are fewer changes as only marginal increments/decrements in the

past data is done.

If there is a need for the major restructuring this type of budgeting becomes irrelevant.

It did not take into consideration any new change in production process.

Activity-Based Budgeting

For the preparation of the budget and analysis is made and those activities are identified

which are costly. Each process of the activity is monitored and cost is identified. Steps are taken

to reduce the overall cost and achieve efficiency.

Advantages

For the preparation of this type of budget each activity of the operational process is evaluated.

By breaking down of the costs IKEA can identified which costs are influencing the production

process.

Each activity can be identified individually.

Disadvantages

The preparation of this type of budget is much more costly.

It is a time-consuming process.

Further a detailed understanding of the business process is required by the management.

Value Proposition Budgeting

A budget is prepared on the basis of the conviction on how the company generate value

so the potential customers are persuaded to buy IKEA products and services (Barnes and et.al,

2017).

Advantages

The budget report is prepared considering value which helps IKEA to avoid time and resources

by disposing that activities which are not relevant.

Helps in identification of jobs that possess not much value.

Quality production can be achieved.

Disadvantages

It increases the overall production cost.

The budgeting takes into consideration those activities that provides value to the customers other

activities are neglected.

The cost analysis of the relevant activities must be done by IKEA whether the preparation of the

budget by this method is feasible or not which is time-consuming.

Zero Based Budgeting

This budgeting method prepares on the approach that the values generated by production

process is zero. All the activities are evaluated from the nil. The activities added in the budget

For the preparation of the budget and analysis is made and those activities are identified

which are costly. Each process of the activity is monitored and cost is identified. Steps are taken

to reduce the overall cost and achieve efficiency.

Advantages

For the preparation of this type of budget each activity of the operational process is evaluated.

By breaking down of the costs IKEA can identified which costs are influencing the production

process.

Each activity can be identified individually.

Disadvantages

The preparation of this type of budget is much more costly.

It is a time-consuming process.

Further a detailed understanding of the business process is required by the management.

Value Proposition Budgeting

A budget is prepared on the basis of the conviction on how the company generate value

so the potential customers are persuaded to buy IKEA products and services (Barnes and et.al,

2017).

Advantages

The budget report is prepared considering value which helps IKEA to avoid time and resources

by disposing that activities which are not relevant.

Helps in identification of jobs that possess not much value.

Quality production can be achieved.

Disadvantages

It increases the overall production cost.

The budgeting takes into consideration those activities that provides value to the customers other

activities are neglected.

The cost analysis of the relevant activities must be done by IKEA whether the preparation of the

budget by this method is feasible or not which is time-consuming.

Zero Based Budgeting

This budgeting method prepares on the approach that the values generated by production

process is zero. All the activities are evaluated from the nil. The activities added in the budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.