Management Accounting Report: Systems, Techniques, and Planning Tools

VerifiedAdded on 2023/01/12

|23

|4952

|97

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Creams Ltd. It begins with an introduction to management accounting, emphasizing its role in providing financial data for decision-making, cost reduction, and profit maximization. The report then explores essential components of management accounting systems, including cost accounting, inventory management, job costing, price optimization, and financial accounting. It highlights the differences between financial and management accounting. The report further analyzes various management accounting reporting methods, such as budget reports, accounts receivables aging reports, cost managerial accounting reports, and performance reports. Task 2 provides an income statement using marginal costing. Finally, the report evaluates management accounting systems and reporting, emphasizing their importance in strategic decision-making and achieving organizational goals. The assignment covers cost calculations, planning tools, and the use of management accounting to address financial challenges, ultimately aiming to provide a comprehensive understanding of the subject.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................4

TASK 1..........................................................................................................................................................4

D1: Critical evaluation of management accounting systems and reporting............................................9

TASK 2..........................................................................................................................................................9

P3: Calculation of costs by using appropriate techniques.......................................................................9

M2: Application of management accounting techniques......................................................................16

TASK 3........................................................................................................................................................16

Planning tools in management accounting............................................................................................16

Application of different planning tools for prepare budget and forecast..............................................18

TASK 4........................................................................................................................................................19

Use of management accounting system for responding few of financial problems..............................19

Analysing the way in which management accounting lead companies to respond financial problems.22

Application of planning tools to respond financial issue along with attainment of sustainable success

...............................................................................................................................................................22

CONCLUSION.............................................................................................................................................22

REFERENCES..............................................................................................................................................23

INTRODUCTION...........................................................................................................................................4

TASK 1..........................................................................................................................................................4

D1: Critical evaluation of management accounting systems and reporting............................................9

TASK 2..........................................................................................................................................................9

P3: Calculation of costs by using appropriate techniques.......................................................................9

M2: Application of management accounting techniques......................................................................16

TASK 3........................................................................................................................................................16

Planning tools in management accounting............................................................................................16

Application of different planning tools for prepare budget and forecast..............................................18

TASK 4........................................................................................................................................................19

Use of management accounting system for responding few of financial problems..............................19

Analysing the way in which management accounting lead companies to respond financial problems.22

Application of planning tools to respond financial issue along with attainment of sustainable success

...............................................................................................................................................................22

CONCLUSION.............................................................................................................................................22

REFERENCES..............................................................................................................................................23

INTRODUCTION

Management accounting refers to a provision of financial data and advice which a company

can use for policymaking and taking of decisions. Management has to use it so that the right

decisions can be taken which can benefit the organization in the long-run (Akkermans and Van

Oorschot, 2018). It helps the enterprises in realizing their long-term aims which includes

reducing costs and maximizing the level of profits. Problems and issues can be eradicated using

it and processes can be streamlined. It aids the management in controlling the various functions

in an organization and helps in taking the right decisions for the benefit of the organization. This

report is based on Creams Ltd. which provides a range of products such as ice-creams,

doughnuts, waffles etc. In this assignment, focus will be made on understanding of systems of

management accounting, applying a range of techniques. Additionally, the use of planning tools

and the ways in which firms can use management accounting to solve their financial problems

will be discussed as a part of this report.

TASK 1

P1 and M1: Explanation of management accounting and essential requirements of its systems

Management accounting is a part of accounting which helps the managers in taking

decisions on the basis of its various concepts and approaches. The essential requirements of its

various systems is explained in the context of Creams Ltd. as follows-

Cost accounting system-

Cost accounting refers to procedures which are used in order to find out the costs of the

company. It also states methods for reduction of cost. Creams Ltd. can use it to find out its costs

and to reduce them.

Advantages-

Cost accounting helps in elimination of wastage by identifying their source and also

provides methods for reducing it.

It reduces the inefficiencies which generally occur in the production process so that

efficiency can be brought into production (Barros and da Costa, 2019).

Management accounting refers to a provision of financial data and advice which a company

can use for policymaking and taking of decisions. Management has to use it so that the right

decisions can be taken which can benefit the organization in the long-run (Akkermans and Van

Oorschot, 2018). It helps the enterprises in realizing their long-term aims which includes

reducing costs and maximizing the level of profits. Problems and issues can be eradicated using

it and processes can be streamlined. It aids the management in controlling the various functions

in an organization and helps in taking the right decisions for the benefit of the organization. This

report is based on Creams Ltd. which provides a range of products such as ice-creams,

doughnuts, waffles etc. In this assignment, focus will be made on understanding of systems of

management accounting, applying a range of techniques. Additionally, the use of planning tools

and the ways in which firms can use management accounting to solve their financial problems

will be discussed as a part of this report.

TASK 1

P1 and M1: Explanation of management accounting and essential requirements of its systems

Management accounting is a part of accounting which helps the managers in taking

decisions on the basis of its various concepts and approaches. The essential requirements of its

various systems is explained in the context of Creams Ltd. as follows-

Cost accounting system-

Cost accounting refers to procedures which are used in order to find out the costs of the

company. It also states methods for reduction of cost. Creams Ltd. can use it to find out its costs

and to reduce them.

Advantages-

Cost accounting helps in elimination of wastage by identifying their source and also

provides methods for reducing it.

It reduces the inefficiencies which generally occur in the production process so that

efficiency can be brought into production (Barros and da Costa, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantages-

Cost accounting system is quite complex and can involve complicated calculations and

thus is not easy to use.

Cost accounting system is quite expensive especially for small-scale organizations.

Essential requirements-

A good cost accounting system should be simple as well as practical to use. It should be

able to benefit the organization in the long-run. It should benefit a company by reducing

its cost effectively and efficiently so that it would be able to maximize its level of profits

in the future time period. Thus the managers of Creams Ltd. must ensure that their cost

accounting system is simple as well as easy to use.

It must display accuracy so that it can benefit the company. It should be accurate enough

to find out the costs of the business. An accurate cost accounting system can benefit the

organization a lot because accuracy will lead to correct determination of profits in the

future. Therefore the managers of Creams Ltd. need to ensure the accuracy of cost

accounting system.

Inventory management system-

Inventory management systems refer to a system in which guidelines and procedures are

set in order to keep a proper track of the inventory level. Creams Ltd. can use it so that its stock

can be tracked properly (Bedford and Speklé, 2018).

Advantages-

This system results in saving of time which in turn benefits a lot to the organization.

This system results in saving of cost for the enterprise.

Disadvantages-

Setting up of this system is quite expensive.

This system involves various complexities.

Essential requirements-

A good inventory management system should enable tracking of inventory. It must be

able to track and locate stock items whenever required. Inventory management system

Cost accounting system is quite complex and can involve complicated calculations and

thus is not easy to use.

Cost accounting system is quite expensive especially for small-scale organizations.

Essential requirements-

A good cost accounting system should be simple as well as practical to use. It should be

able to benefit the organization in the long-run. It should benefit a company by reducing

its cost effectively and efficiently so that it would be able to maximize its level of profits

in the future time period. Thus the managers of Creams Ltd. must ensure that their cost

accounting system is simple as well as easy to use.

It must display accuracy so that it can benefit the company. It should be accurate enough

to find out the costs of the business. An accurate cost accounting system can benefit the

organization a lot because accuracy will lead to correct determination of profits in the

future. Therefore the managers of Creams Ltd. need to ensure the accuracy of cost

accounting system.

Inventory management system-

Inventory management systems refer to a system in which guidelines and procedures are

set in order to keep a proper track of the inventory level. Creams Ltd. can use it so that its stock

can be tracked properly (Bedford and Speklé, 2018).

Advantages-

This system results in saving of time which in turn benefits a lot to the organization.

This system results in saving of cost for the enterprise.

Disadvantages-

Setting up of this system is quite expensive.

This system involves various complexities.

Essential requirements-

A good inventory management system should enable tracking of inventory. It must be

able to track and locate stock items whenever required. Inventory management system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

should be such so that it is able to track the inventory items which are misplaced or lost

and therefore the managers of Creams Ltd. should ensure that.

A good inventory management system should allow for reporting and analysis of

information. It must be able to find out the problems with the system of enterprise if any

to remove them as soon as possible for maximizing the profits. Managers of Creams Ltd.

have to ensure that reporting and analysis of information is done in the inventory

management system.

Job costing system-

Job costing system involves procurement of information regarding execution of a particular

task or job. Creams Ltd. can use it so that it can easily track its different orders and can fulfill

them on time (Berry, Broadbent and Otley, 2019).

Advantages-

The cost of performing a specific job can be easily ascertained by using this system.

There is no under recovery of overheads in this system.

Disadvantages-

There is no standardization of work in this system.

It is a very expensive method.

Essential requirements-

A good job costing system should ensure accounting of direct materials. This is important

for Creams Ltd. because it deals in manufacturing process and therefore this system can

help a lot in accounting work related with direct materials.

A good job costing system should account for the overheads being incurred in an

enterprise. It is necessary for the managers of Creams Ltd. because overheads have to be

reduced in order to raise the level of profits.

Price optimization system-

Price optimization system uses mathematical models to identify the variation of price at

different levels of demand of a product. Creams Ltd. can make use of it so that it can set a

right price for its products.

Advantages-

and therefore the managers of Creams Ltd. should ensure that.

A good inventory management system should allow for reporting and analysis of

information. It must be able to find out the problems with the system of enterprise if any

to remove them as soon as possible for maximizing the profits. Managers of Creams Ltd.

have to ensure that reporting and analysis of information is done in the inventory

management system.

Job costing system-

Job costing system involves procurement of information regarding execution of a particular

task or job. Creams Ltd. can use it so that it can easily track its different orders and can fulfill

them on time (Berry, Broadbent and Otley, 2019).

Advantages-

The cost of performing a specific job can be easily ascertained by using this system.

There is no under recovery of overheads in this system.

Disadvantages-

There is no standardization of work in this system.

It is a very expensive method.

Essential requirements-

A good job costing system should ensure accounting of direct materials. This is important

for Creams Ltd. because it deals in manufacturing process and therefore this system can

help a lot in accounting work related with direct materials.

A good job costing system should account for the overheads being incurred in an

enterprise. It is necessary for the managers of Creams Ltd. because overheads have to be

reduced in order to raise the level of profits.

Price optimization system-

Price optimization system uses mathematical models to identify the variation of price at

different levels of demand of a product. Creams Ltd. can make use of it so that it can set a

right price for its products.

Advantages-

Firm can earn high profits by choosing an appropriate price.

It helps in setting the right price for the product.

Disadvantages-

If the right price is not set it can impact the customer base of the company.

It can result in losses if right price is not set by the company.

Essential requirements-

It requires analytics and management of performance. Managers of Creams Ltd. need to

ensure that performance is analyzed effectively by them so that right price can be set in

the organization.

It also requires price segmentation (Boddy, McCalman and Buchanan, 2018). This

ensures that the firm is able to raise its level of profits in the long-run. Therefore the

management of Creams Ltd. can use the technique of price segmentation effectively.

Financial accounting- Financial accounting refers to a specialized branch of accounting

which is used to track the accounts and financial information of a company. The

managers of Creams Ltd. make use of it in order to analyze the accounts and financial

information of their company.

Management accounting- Management accounting refers to the provision of financial

data and advice for a company for using in organization and development of the business.

The management of Creams Ltd. can make use of it to analyze and interpret the financial

information of their company.

Difference between Financial accounting and Management accounting-

Basis Financial accounting Management accounting

Aggregation Financial accounting is

used to report the results of

the entire business.

Management accounting is

used to report at a more

detailed and specific level.

Efficiency It reports the profitability of

a business.

Management accounting

focuses on problems and

their solutions.

Proven information In it, records are kept with

precision.

It deals with estimates

rather than proven facts.

P2: Various methods used for management accounting reporting

Management accounting reporting emphasizes on information received through financial

accounting. The information is used for analysis and thereby for planning, regulating,

It helps in setting the right price for the product.

Disadvantages-

If the right price is not set it can impact the customer base of the company.

It can result in losses if right price is not set by the company.

Essential requirements-

It requires analytics and management of performance. Managers of Creams Ltd. need to

ensure that performance is analyzed effectively by them so that right price can be set in

the organization.

It also requires price segmentation (Boddy, McCalman and Buchanan, 2018). This

ensures that the firm is able to raise its level of profits in the long-run. Therefore the

management of Creams Ltd. can use the technique of price segmentation effectively.

Financial accounting- Financial accounting refers to a specialized branch of accounting

which is used to track the accounts and financial information of a company. The

managers of Creams Ltd. make use of it in order to analyze the accounts and financial

information of their company.

Management accounting- Management accounting refers to the provision of financial

data and advice for a company for using in organization and development of the business.

The management of Creams Ltd. can make use of it to analyze and interpret the financial

information of their company.

Difference between Financial accounting and Management accounting-

Basis Financial accounting Management accounting

Aggregation Financial accounting is

used to report the results of

the entire business.

Management accounting is

used to report at a more

detailed and specific level.

Efficiency It reports the profitability of

a business.

Management accounting

focuses on problems and

their solutions.

Proven information In it, records are kept with

precision.

It deals with estimates

rather than proven facts.

P2: Various methods used for management accounting reporting

Management accounting reporting emphasizes on information received through financial

accounting. The information is used for analysis and thereby for planning, regulating,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision-making and measurement of performance of the organization. The methods of

management accounting reporting which Creams Ltd. can use are as follows-

Budget reports- Budget reports are used for measurement of performance of different

departments and the whole company. These reports can be used by managers of Creams Ltd. to

effectively and efficiently ensure that the expenses being incurred are in check and are not more

than the budgeted ones. It also helps a lot in comparison purposes. It includes summary of all

types of budgets such as cash budget, operating budget, master budget etc. Overall, they also tell

whether the company’s budget is in deficit. Also guidance is provided to managers to facilitate

better decision-making in the future. It facilitates improvement of performance in different

departments of the company (Booth, 2018).

Accounts receivables aging reports- Accounts receivables aging reports are used in

order to find out those debtors who have not paid their dues since a long time. Creams Ltd.’s

management can use them to identify these defaulters so that collection can be done from

them to prevent bad debts. It is quite helpful for the managers to avoid bad debts and collect

the dues from debtors on time. Thus, it actually prevents mismanagement in an organization.

Also if there are many defaulters identified in this report then it signals that it is time for the

company to tighten its credit policy.

Cost managerial accounting reports- It accounts for all raw material, overhead, labor

any other costs. It provides summary of all the costs being incurred in the organization.

Creams Ltd.’s managers can make use of it to identify the departments where the cost is

increasing so that measures can be taken to prevent it so that profits can be maximized in the

future. Also it brings out efficiency and effectiveness in the organization by facilitating

improvement of performance in every area of the enterprise. Managers can use these reports

for comparison purpose with the standard costs being set up by the industry or with the costs

incurred by the company in the previous years. Thus these reports are extremely helpful in

the context of an organization.

Performance reports- Performance reports are used for reviewing the overall

performance of the company. Also it measures the working of every employee at the end of the

term. Creams Ltd’s managers can use these reports to measure performance as well to take

management accounting reporting which Creams Ltd. can use are as follows-

Budget reports- Budget reports are used for measurement of performance of different

departments and the whole company. These reports can be used by managers of Creams Ltd. to

effectively and efficiently ensure that the expenses being incurred are in check and are not more

than the budgeted ones. It also helps a lot in comparison purposes. It includes summary of all

types of budgets such as cash budget, operating budget, master budget etc. Overall, they also tell

whether the company’s budget is in deficit. Also guidance is provided to managers to facilitate

better decision-making in the future. It facilitates improvement of performance in different

departments of the company (Booth, 2018).

Accounts receivables aging reports- Accounts receivables aging reports are used in

order to find out those debtors who have not paid their dues since a long time. Creams Ltd.’s

management can use them to identify these defaulters so that collection can be done from

them to prevent bad debts. It is quite helpful for the managers to avoid bad debts and collect

the dues from debtors on time. Thus, it actually prevents mismanagement in an organization.

Also if there are many defaulters identified in this report then it signals that it is time for the

company to tighten its credit policy.

Cost managerial accounting reports- It accounts for all raw material, overhead, labor

any other costs. It provides summary of all the costs being incurred in the organization.

Creams Ltd.’s managers can make use of it to identify the departments where the cost is

increasing so that measures can be taken to prevent it so that profits can be maximized in the

future. Also it brings out efficiency and effectiveness in the organization by facilitating

improvement of performance in every area of the enterprise. Managers can use these reports

for comparison purpose with the standard costs being set up by the industry or with the costs

incurred by the company in the previous years. Thus these reports are extremely helpful in

the context of an organization.

Performance reports- Performance reports are used for reviewing the overall

performance of the company. Also it measures the working of every employee at the end of the

term. Creams Ltd’s managers can use these reports to measure performance as well to take

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

strategic decisions for the benefit of the company. They offer deep insights into the working

pattern of the organization which can be quite helpful for analysis purposes. Also performance

can be easily compared using these reports with the competitors to find out where the firm is

lacking and the areas it can improve. Their role is vital for a company to keep an accurate

measure of their strategy towards their mission (Dewi, and et. al., 2018).

D1: Critical evaluation of management accounting systems and reporting

Management accounting systems and reporting are helpful for an organization to frame

its policy. Creams Ltd.’s management can use them effectively and efficiently to optimize the

performance of the entire company. This will result in strategic decision-making which can put

the company ahead of its competitors and can facilitate maximization of profits and help in

achievement of short-term, medium-term and long-term goals and objectives which are set up in

the organization.

TASK 2

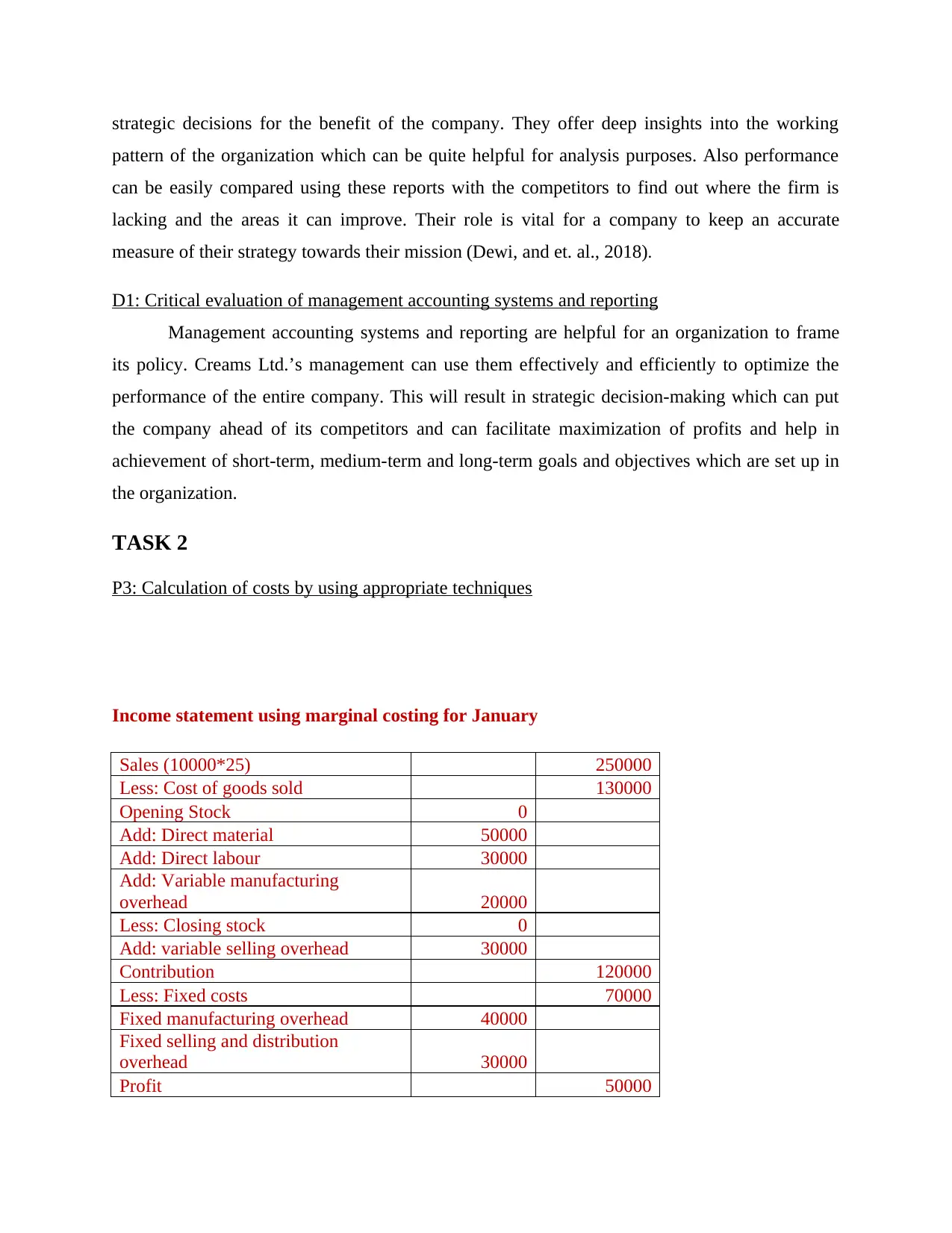

P3: Calculation of costs by using appropriate techniques

Income statement using marginal costing for January

Sales (10000*25) 250000

Less: Cost of goods sold 130000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing

overhead 20000

Less: Closing stock 0

Add: variable selling overhead 30000

Contribution 120000

Less: Fixed costs 70000

Fixed manufacturing overhead 40000

Fixed selling and distribution

overhead 30000

Profit 50000

pattern of the organization which can be quite helpful for analysis purposes. Also performance

can be easily compared using these reports with the competitors to find out where the firm is

lacking and the areas it can improve. Their role is vital for a company to keep an accurate

measure of their strategy towards their mission (Dewi, and et. al., 2018).

D1: Critical evaluation of management accounting systems and reporting

Management accounting systems and reporting are helpful for an organization to frame

its policy. Creams Ltd.’s management can use them effectively and efficiently to optimize the

performance of the entire company. This will result in strategic decision-making which can put

the company ahead of its competitors and can facilitate maximization of profits and help in

achievement of short-term, medium-term and long-term goals and objectives which are set up in

the organization.

TASK 2

P3: Calculation of costs by using appropriate techniques

Income statement using marginal costing for January

Sales (10000*25) 250000

Less: Cost of goods sold 130000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing

overhead 20000

Less: Closing stock 0

Add: variable selling overhead 30000

Contribution 120000

Less: Fixed costs 70000

Fixed manufacturing overhead 40000

Fixed selling and distribution

overhead 30000

Profit 50000

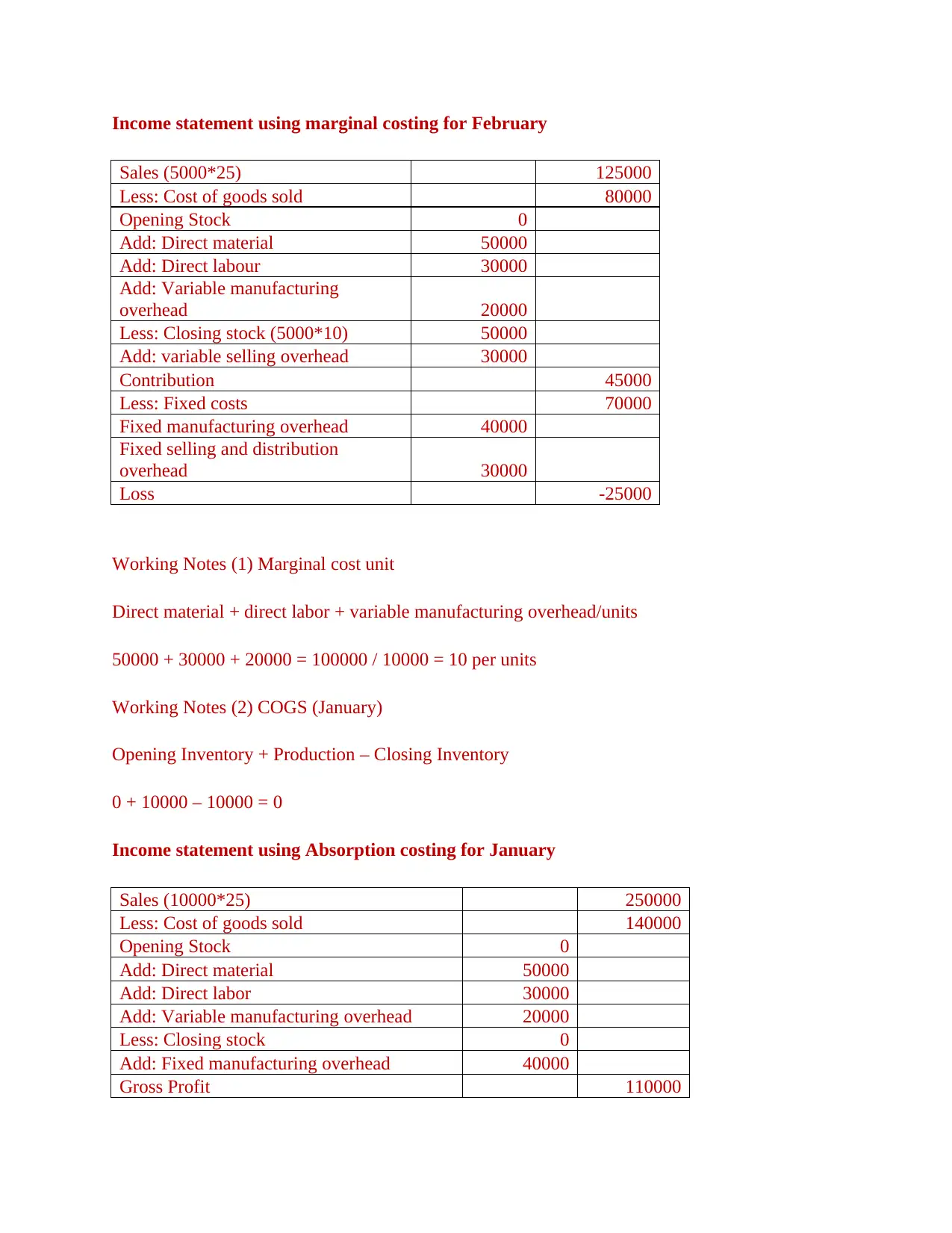

Income statement using marginal costing for February

Sales (5000*25) 125000

Less: Cost of goods sold 80000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing

overhead 20000

Less: Closing stock (5000*10) 50000

Add: variable selling overhead 30000

Contribution 45000

Less: Fixed costs 70000

Fixed manufacturing overhead 40000

Fixed selling and distribution

overhead 30000

Loss -25000

Working Notes (1) Marginal cost unit

Direct material + direct labor + variable manufacturing overhead/units

50000 + 30000 + 20000 = 100000 / 10000 = 10 per units

Working Notes (2) COGS (January)

Opening Inventory + Production – Closing Inventory

0 + 10000 – 10000 = 0

Income statement using Absorption costing for January

Sales (10000*25) 250000

Less: Cost of goods sold 140000

Opening Stock 0

Add: Direct material 50000

Add: Direct labor 30000

Add: Variable manufacturing overhead 20000

Less: Closing stock 0

Add: Fixed manufacturing overhead 40000

Gross Profit 110000

Sales (5000*25) 125000

Less: Cost of goods sold 80000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing

overhead 20000

Less: Closing stock (5000*10) 50000

Add: variable selling overhead 30000

Contribution 45000

Less: Fixed costs 70000

Fixed manufacturing overhead 40000

Fixed selling and distribution

overhead 30000

Loss -25000

Working Notes (1) Marginal cost unit

Direct material + direct labor + variable manufacturing overhead/units

50000 + 30000 + 20000 = 100000 / 10000 = 10 per units

Working Notes (2) COGS (January)

Opening Inventory + Production – Closing Inventory

0 + 10000 – 10000 = 0

Income statement using Absorption costing for January

Sales (10000*25) 250000

Less: Cost of goods sold 140000

Opening Stock 0

Add: Direct material 50000

Add: Direct labor 30000

Add: Variable manufacturing overhead 20000

Less: Closing stock 0

Add: Fixed manufacturing overhead 40000

Gross Profit 110000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

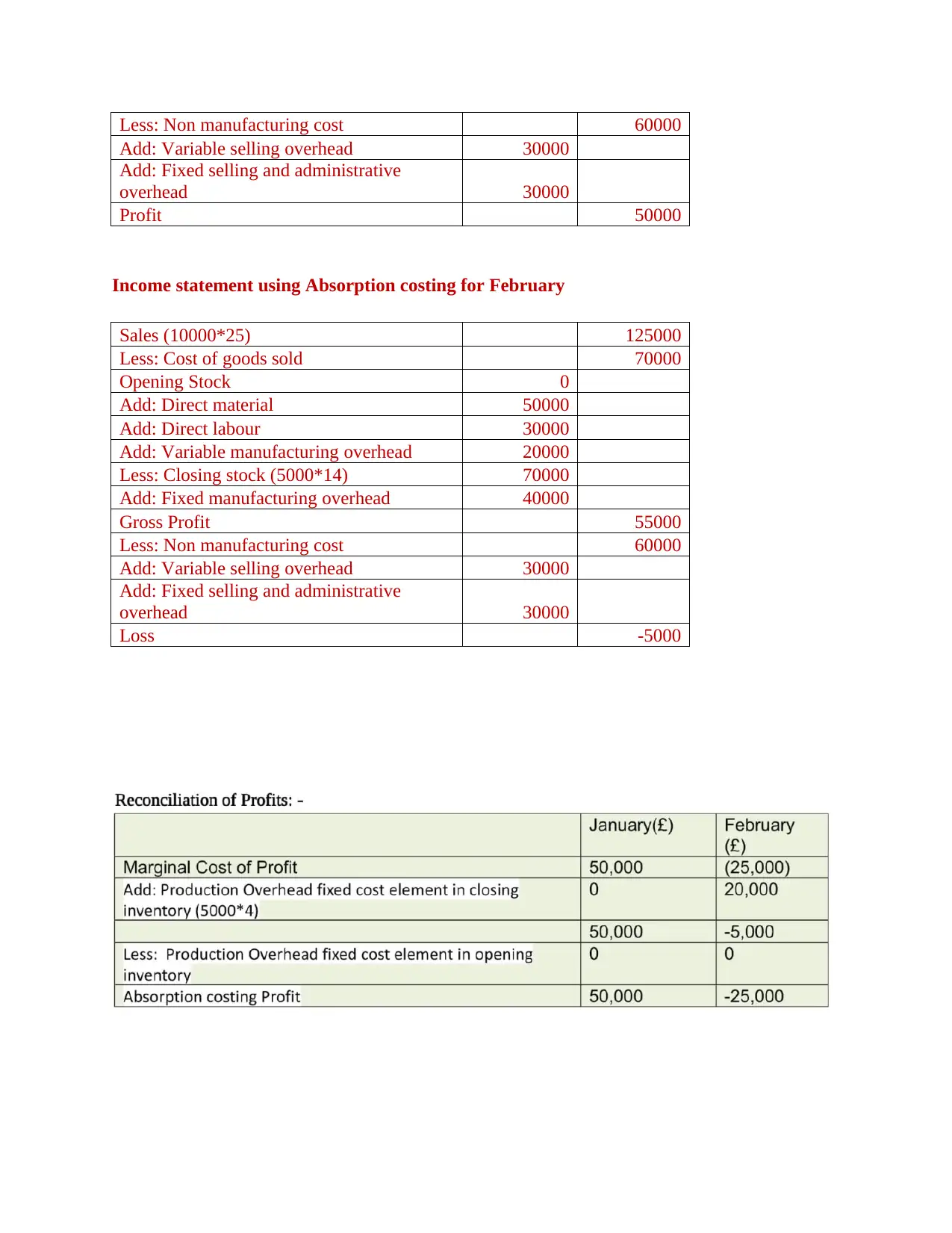

Less: Non manufacturing cost 60000

Add: Variable selling overhead 30000

Add: Fixed selling and administrative

overhead 30000

Profit 50000

Income statement using Absorption costing for February

Sales (10000*25) 125000

Less: Cost of goods sold 70000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing overhead 20000

Less: Closing stock (5000*14) 70000

Add: Fixed manufacturing overhead 40000

Gross Profit 55000

Less: Non manufacturing cost 60000

Add: Variable selling overhead 30000

Add: Fixed selling and administrative

overhead 30000

Loss -5000

Add: Variable selling overhead 30000

Add: Fixed selling and administrative

overhead 30000

Profit 50000

Income statement using Absorption costing for February

Sales (10000*25) 125000

Less: Cost of goods sold 70000

Opening Stock 0

Add: Direct material 50000

Add: Direct labour 30000

Add: Variable manufacturing overhead 20000

Less: Closing stock (5000*14) 70000

Add: Fixed manufacturing overhead 40000

Gross Profit 55000

Less: Non manufacturing cost 60000

Add: Variable selling overhead 30000

Add: Fixed selling and administrative

overhead 30000

Loss -5000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.