Management Accounting Report: Techniques and Analysis for Clarasys Ltd

VerifiedAdded on 2020/11/23

|20

|6322

|492

Report

AI Summary

This report delves into the intricacies of management accounting, exploring various systems and reporting methods. It begins with an introduction to management accounting, contrasting it with financial accounting and highlighting its essential requirements. The report then examines different types of management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems. The analysis extends to different reporting methods, such as ratio analysis, budget reports, and job cost reports. The report further discusses the benefits of these systems and their applications within an organizational context, followed by an integration of management accounting systems and reporting within organizational processes. The core of the report focuses on cost analysis techniques, specifically absorption and marginal costing, preparing income statements using these methods, and applying a range of management accounting techniques to produce appropriate financial accounting documents. The report also evaluates the advantages and disadvantages of planning tools used for budgetary control, analyzing their use in budget preparation and forecasting. Finally, it examines how organizations adapt management accounting systems to respond to financial problems, using various planning tools to resolve these issues.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements od different types of management

accounting system.......................................................................................................................1

P2 Different methods used for management accounting reporting.............................................3

M1 Benefits of management accounting system and their application in organisation context. 4

D1 Management accounting system and management accounting reporting integrated within

organisational processes..............................................................................................................4

TASK 2............................................................................................................................................5

P3 Appropriate techniques of cost analysis to prepare an income statement..............................5

M2 Apply a range of management accounting techniques and produce appropriate financial

accounting documents.................................................................................................................8

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities......................................................................................................................................8

TASK 3............................................................................................................................................9

P3. Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................9

M3. Analyses the use of planning tools and applications for preparation and forecasting

budgets......................................................................................................................................13

P5. Organisations are adapting management accounting systems to respond to financial

problems....................................................................................................................................13

D3. Various planning tools to resolve financial problems........................................................16

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements od different types of management

accounting system.......................................................................................................................1

P2 Different methods used for management accounting reporting.............................................3

M1 Benefits of management accounting system and their application in organisation context. 4

D1 Management accounting system and management accounting reporting integrated within

organisational processes..............................................................................................................4

TASK 2............................................................................................................................................5

P3 Appropriate techniques of cost analysis to prepare an income statement..............................5

M2 Apply a range of management accounting techniques and produce appropriate financial

accounting documents.................................................................................................................8

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities......................................................................................................................................8

TASK 3............................................................................................................................................9

P3. Advantages and disadvantages of different types of planning tools used for budgetary

control.........................................................................................................................................9

M3. Analyses the use of planning tools and applications for preparation and forecasting

budgets......................................................................................................................................13

P5. Organisations are adapting management accounting systems to respond to financial

problems....................................................................................................................................13

D3. Various planning tools to resolve financial problems........................................................16

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is the process of producing management accounts and reports

that provide accurate and timely financial and statistical information which can require by

managers to decision making process related to day to day activities (Alyousef and Mickan,

2016). It is used as management tool which look at the events hat happen in and around a

business while considering the needs of a business. In the present report selected company,

Clarasys Ltd which is London based management consultancy with their sights set on the United

states. It is a truly democratic company and constantly making improvements to the working

environment with new desks, divider and poster. In this report consist of different management

accounting system and different methods of management accounting reports. Apart from

calculate cost by using appropriate costing techniques and analysis cost to prepare income

statement. In addition identify different advantages and disadvantage of different types of

planning tools in budgetary control and selected company compare with other organisation to

respond financial problems.

TASK 1

P1 Management accounting and essential requirements od different types of management

accounting system

Introduction to Management Accounting

Management accounting is the process of identifying, measuring, analysing, interpreting

and communicating information to managers for the pursuit of an organization's goals. It is also

known as cost accounting and managerial accounting which is different from financial

accounting.

Difference between management and financial accounting

Basis Management Accounting Financial Accounting

Purpose It is prepared by accountant for

internal used.

It is used foe external reporting

primarily although the management

also reviews it.

Regulation It is not based on particular

regulation and law

It is presented by company as per

accounting concepts and standards.

1

Management accounting is the process of producing management accounts and reports

that provide accurate and timely financial and statistical information which can require by

managers to decision making process related to day to day activities (Alyousef and Mickan,

2016). It is used as management tool which look at the events hat happen in and around a

business while considering the needs of a business. In the present report selected company,

Clarasys Ltd which is London based management consultancy with their sights set on the United

states. It is a truly democratic company and constantly making improvements to the working

environment with new desks, divider and poster. In this report consist of different management

accounting system and different methods of management accounting reports. Apart from

calculate cost by using appropriate costing techniques and analysis cost to prepare income

statement. In addition identify different advantages and disadvantage of different types of

planning tools in budgetary control and selected company compare with other organisation to

respond financial problems.

TASK 1

P1 Management accounting and essential requirements od different types of management

accounting system

Introduction to Management Accounting

Management accounting is the process of identifying, measuring, analysing, interpreting

and communicating information to managers for the pursuit of an organization's goals. It is also

known as cost accounting and managerial accounting which is different from financial

accounting.

Difference between management and financial accounting

Basis Management Accounting Financial Accounting

Purpose It is prepared by accountant for

internal used.

It is used foe external reporting

primarily although the management

also reviews it.

Regulation It is not based on particular

regulation and law

It is presented by company as per

accounting concepts and standards.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Users The users of this accounting is

internal management

Its users are shareholders, regulators

and investors.

Origin, role, principles of management accounting

Management accounting first emerged as a significant activity during the early industry

revolution, in the leading industries and enterprises of the day. As such, management accounting

arose after financial accounting, which can trace its origins to its stewardship role in European

merchant trading ventures. Double entry book keeping had been used for more than 300 years by

the time management accounting first emerged as a recognizable field (Armitage, Webb and

Glynn, 2016).

The management accounting play different role in an organisation as a internal part like

planing, organising, motivating, coordinating, control, communicate and interpret financial

information.

Principles of management accounting are mentioned which are – Influence

(communication provides insight that is influential), Relevance (Providing information is

relevant), value (This principle can show impact on value is analysed) and trust (stewardship

builds trust).

Different types of management accounting system

Management accounting system is the internal system of an organization which is used to

measure and determine it processes for the management of the organization.

Cost accounting system

A cost accounting system is a framework which is used by an organisation to determine

the cost of their products regarding to profitability analysis, inventory valuation and cost control.

This system mainly used by manufactures to record production activities using a perceptual

inventory system. This accounting system mainly designed for producers to track the the flow of

inventory continually through the several level of production. In Clarasys Ltd is used by the

managers to keep track record of cost which is faced by them while attend meetings with clients

(Bedford and Speklé, 2018).

Inventory management system

The system is used for identifying inventory item that can make products in efficient

manner. In Clarasys Ltd followed by this system in order to keep track record of all activities

related to inventory at each level. The company has applied three different types of inventory

2

internal management

Its users are shareholders, regulators

and investors.

Origin, role, principles of management accounting

Management accounting first emerged as a significant activity during the early industry

revolution, in the leading industries and enterprises of the day. As such, management accounting

arose after financial accounting, which can trace its origins to its stewardship role in European

merchant trading ventures. Double entry book keeping had been used for more than 300 years by

the time management accounting first emerged as a recognizable field (Armitage, Webb and

Glynn, 2016).

The management accounting play different role in an organisation as a internal part like

planing, organising, motivating, coordinating, control, communicate and interpret financial

information.

Principles of management accounting are mentioned which are – Influence

(communication provides insight that is influential), Relevance (Providing information is

relevant), value (This principle can show impact on value is analysed) and trust (stewardship

builds trust).

Different types of management accounting system

Management accounting system is the internal system of an organization which is used to

measure and determine it processes for the management of the organization.

Cost accounting system

A cost accounting system is a framework which is used by an organisation to determine

the cost of their products regarding to profitability analysis, inventory valuation and cost control.

This system mainly used by manufactures to record production activities using a perceptual

inventory system. This accounting system mainly designed for producers to track the the flow of

inventory continually through the several level of production. In Clarasys Ltd is used by the

managers to keep track record of cost which is faced by them while attend meetings with clients

(Bedford and Speklé, 2018).

Inventory management system

The system is used for identifying inventory item that can make products in efficient

manner. In Clarasys Ltd followed by this system in order to keep track record of all activities

related to inventory at each level. The company has applied three different types of inventory

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management system which can apply according to their requirement such as LIFO, FIFO and

AVCO. The manager of the company provide bes financial services and keep all details

regarding to their problems.

Job costing system

In this system business entities can record the jobs according to performance of customer.

In the context of company it is mainly used by managers to analyse the cost which is involved in

service providing of the company. This system very important for the business in order to

manage and analyse cost of each job to perform under particular time period.

Price Optimising system

This system used by company to know different perception of different customer

regarding to financial services. Management of Clarasys Ltd used this system and know about

best prices of their services. It can help to attract more customers and they are taking interest to

know financial advise. It is very beneficial for a company and help to survive long time (Christ

and Burritt, 2013).

P2 Different methods used for management accounting reporting

Information should be relevant

When the company prepare financial report of the company so it will be prepared

according to requirement and it will present in front of management for decision making process

and know financial performance of the company. These information should be presented

according to user perspective, reliable, accurate and up to date.

Different types of managerial accounting reports

Ratio Analysis – It is calculated to know financial performance of the business and

perform how well the business has performed in the different operational activities. For example

net profit ratio will inform the management on how much profit earn as a percentage of the sales

value. Clarasys Ltd can analysis ratio to compare performance from last year and provide all

reliable and under-stable information.

Budget Report – It very important for company to prepare budget report of each section

to predict future income and expenses in order to reduce risk. These budgets will assist the

management in controlling the resources in the most efficiency way possible. The budgets are

therefore used in planning decision making process as well as planning by the management of

Clarasys Ltd (Collis and Hussey, 2017).

3

AVCO. The manager of the company provide bes financial services and keep all details

regarding to their problems.

Job costing system

In this system business entities can record the jobs according to performance of customer.

In the context of company it is mainly used by managers to analyse the cost which is involved in

service providing of the company. This system very important for the business in order to

manage and analyse cost of each job to perform under particular time period.

Price Optimising system

This system used by company to know different perception of different customer

regarding to financial services. Management of Clarasys Ltd used this system and know about

best prices of their services. It can help to attract more customers and they are taking interest to

know financial advise. It is very beneficial for a company and help to survive long time (Christ

and Burritt, 2013).

P2 Different methods used for management accounting reporting

Information should be relevant

When the company prepare financial report of the company so it will be prepared

according to requirement and it will present in front of management for decision making process

and know financial performance of the company. These information should be presented

according to user perspective, reliable, accurate and up to date.

Different types of managerial accounting reports

Ratio Analysis – It is calculated to know financial performance of the business and

perform how well the business has performed in the different operational activities. For example

net profit ratio will inform the management on how much profit earn as a percentage of the sales

value. Clarasys Ltd can analysis ratio to compare performance from last year and provide all

reliable and under-stable information.

Budget Report – It very important for company to prepare budget report of each section

to predict future income and expenses in order to reduce risk. These budgets will assist the

management in controlling the resources in the most efficiency way possible. The budgets are

therefore used in planning decision making process as well as planning by the management of

Clarasys Ltd (Collis and Hussey, 2017).

3

Credit control Report – This report will evaluate credit limit granted to the customers in

particular time period. In this report highlighted those people who pay late and sometime can not

pay and take financial services from business. So this report prepare by Clarasys Ltd to control

credit and reducing amount of bad debt and facilitating the customers in order to maximise the

sales.

Job Cost Report – It is prepared to show actual amounts which can spent on completion

of the job. This can be compared with the expected amounts to find variances. This report will

assist the management to making sure about to control cost and the profit margins from the jobs.

It will help to Clarasys Ltd to meet the overall profitability targets of the business.

Inventory and manufacturing Report – With the help of this report focus on the stock

which is mainly used by manufacturing department to produce the budgeted production units.

This report help to highlight on wastage production and help to management of Clarasys Ltd to

understand work breakdown of the unit costs. So it will help to cost savings can be planned and

important pricing decision can be made (DRURY, 2013).

M1 Benefits of management accounting system and their application in organisation context

Management accounting system related to internal function of a company and it can

adopt by company to manage all business activities. Cost accounting system help to know

functional budget cost of each section and arrange according to product wise and department

wise for planning all resources. Price optimization system apply by organisation to know

different reaction of different customer and it can help to set best prices according to their

services. In inventory management system create bills of materials, work order and other

production document which is related to inventory data. In job costing system involve process to

accumulated information about regarding to costs with a specific production or service job.

D1 Management accounting system and management accounting reporting integrated within

organisational processes

every organisation required management accounting system or accounting report to to

perform well in the business to achieve their goals & objectives. with the help of cost accounting

system manager identify the each product cost where further decision taken by according to it.

Along with this, performance report help the manager to identify employees performance which

the help of this report offer incentives which motivate people regarding their work. so basically

these system or management accounting report helps in organisational process.

4

particular time period. In this report highlighted those people who pay late and sometime can not

pay and take financial services from business. So this report prepare by Clarasys Ltd to control

credit and reducing amount of bad debt and facilitating the customers in order to maximise the

sales.

Job Cost Report – It is prepared to show actual amounts which can spent on completion

of the job. This can be compared with the expected amounts to find variances. This report will

assist the management to making sure about to control cost and the profit margins from the jobs.

It will help to Clarasys Ltd to meet the overall profitability targets of the business.

Inventory and manufacturing Report – With the help of this report focus on the stock

which is mainly used by manufacturing department to produce the budgeted production units.

This report help to highlight on wastage production and help to management of Clarasys Ltd to

understand work breakdown of the unit costs. So it will help to cost savings can be planned and

important pricing decision can be made (DRURY, 2013).

M1 Benefits of management accounting system and their application in organisation context

Management accounting system related to internal function of a company and it can

adopt by company to manage all business activities. Cost accounting system help to know

functional budget cost of each section and arrange according to product wise and department

wise for planning all resources. Price optimization system apply by organisation to know

different reaction of different customer and it can help to set best prices according to their

services. In inventory management system create bills of materials, work order and other

production document which is related to inventory data. In job costing system involve process to

accumulated information about regarding to costs with a specific production or service job.

D1 Management accounting system and management accounting reporting integrated within

organisational processes

every organisation required management accounting system or accounting report to to

perform well in the business to achieve their goals & objectives. with the help of cost accounting

system manager identify the each product cost where further decision taken by according to it.

Along with this, performance report help the manager to identify employees performance which

the help of this report offer incentives which motivate people regarding their work. so basically

these system or management accounting report helps in organisational process.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

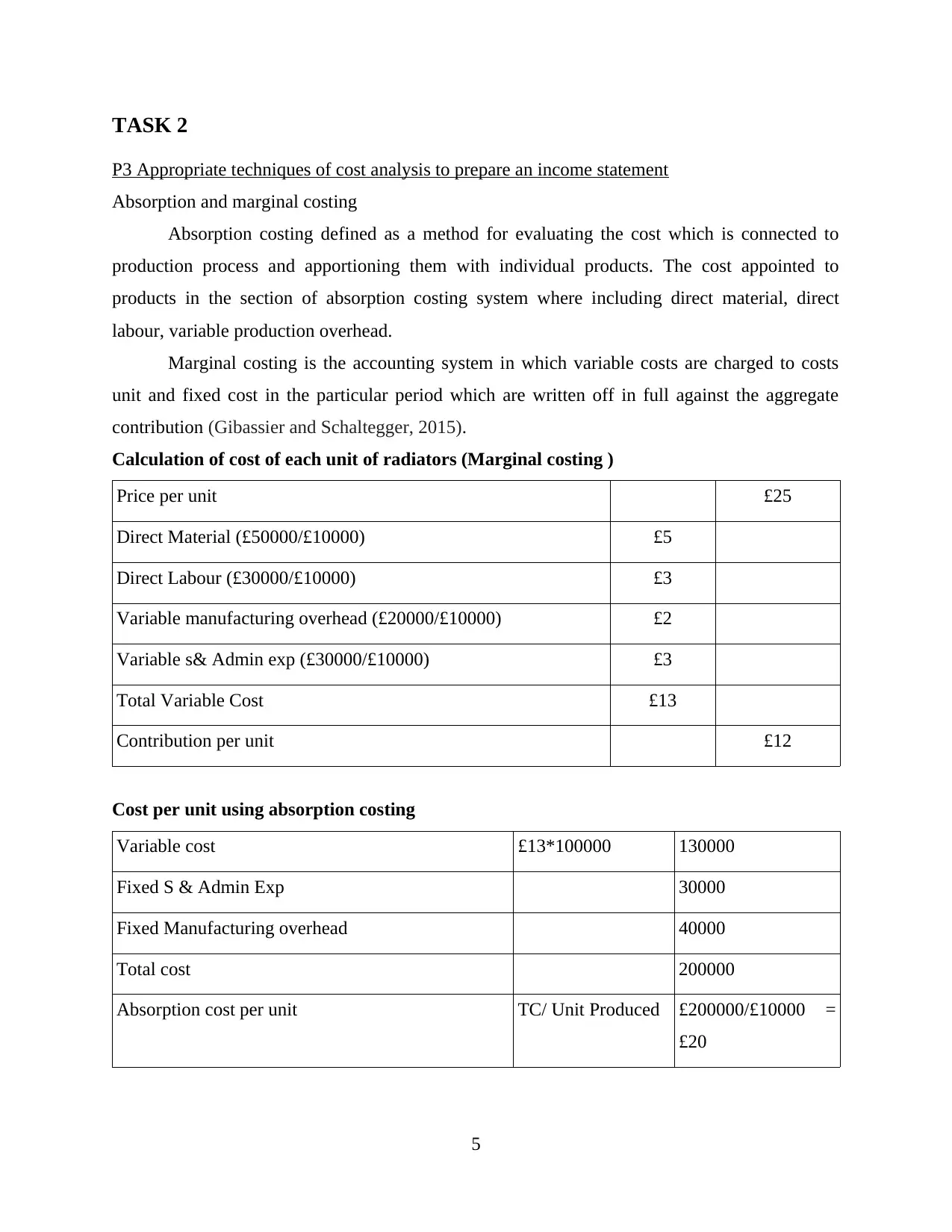

P3 Appropriate techniques of cost analysis to prepare an income statement

Absorption and marginal costing

Absorption costing defined as a method for evaluating the cost which is connected to

production process and apportioning them with individual products. The cost appointed to

products in the section of absorption costing system where including direct material, direct

labour, variable production overhead.

Marginal costing is the accounting system in which variable costs are charged to costs

unit and fixed cost in the particular period which are written off in full against the aggregate

contribution (Gibassier and Schaltegger, 2015).

Calculation of cost of each unit of radiators (Marginal costing )

Price per unit £25

Direct Material (£50000/£10000) £5

Direct Labour (£30000/£10000) £3

Variable manufacturing overhead (£20000/£10000) £2

Variable s& Admin exp (£30000/£10000) £3

Total Variable Cost £13

Contribution per unit £12

Cost per unit using absorption costing

Variable cost £13*100000 130000

Fixed S & Admin Exp 30000

Fixed Manufacturing overhead 40000

Total cost 200000

Absorption cost per unit TC/ Unit Produced £200000/£10000 =

£20

5

P3 Appropriate techniques of cost analysis to prepare an income statement

Absorption and marginal costing

Absorption costing defined as a method for evaluating the cost which is connected to

production process and apportioning them with individual products. The cost appointed to

products in the section of absorption costing system where including direct material, direct

labour, variable production overhead.

Marginal costing is the accounting system in which variable costs are charged to costs

unit and fixed cost in the particular period which are written off in full against the aggregate

contribution (Gibassier and Schaltegger, 2015).

Calculation of cost of each unit of radiators (Marginal costing )

Price per unit £25

Direct Material (£50000/£10000) £5

Direct Labour (£30000/£10000) £3

Variable manufacturing overhead (£20000/£10000) £2

Variable s& Admin exp (£30000/£10000) £3

Total Variable Cost £13

Contribution per unit £12

Cost per unit using absorption costing

Variable cost £13*100000 130000

Fixed S & Admin Exp 30000

Fixed Manufacturing overhead 40000

Total cost 200000

Absorption cost per unit TC/ Unit Produced £200000/£10000 =

£20

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Flexible Budget

£ (5000 units) £ (10000 units)

Sales 125000 250000

Cost of Sales 50000 100000

Prod. Contri. Margin 75000 150000

Variable selling/Admin costs 15000 30000

Net Contribution Margin 60000 120000

Less – Total Fixed Costs

Fixed Manufacturing Overhead 40000 40000

Fixed Selling & Admin 30000 30000

Net Profit (10000) 50000

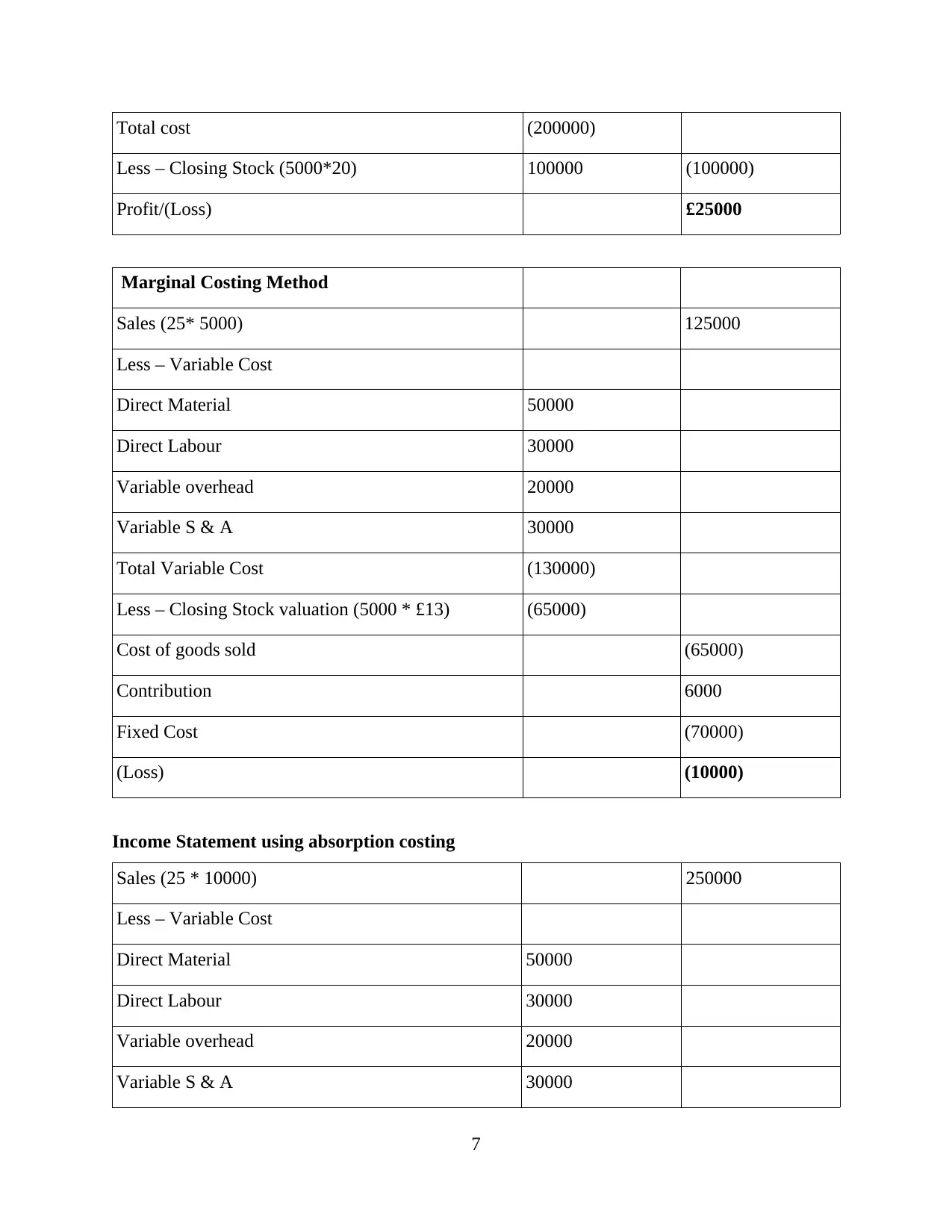

Income statement when 5000 units sold:

Absorption Costing Method

Sales (25*5000) 125000

Less – Variable Cost

Direct Material 50000

Direct Labour 30000

Variable overhead 20000

Variable S & A 30000

Total Variable cost (130000)

Fixed Cost

Fixed Manufacturing overhead 40000

Fixed S&A expenses 30000

6

£ (5000 units) £ (10000 units)

Sales 125000 250000

Cost of Sales 50000 100000

Prod. Contri. Margin 75000 150000

Variable selling/Admin costs 15000 30000

Net Contribution Margin 60000 120000

Less – Total Fixed Costs

Fixed Manufacturing Overhead 40000 40000

Fixed Selling & Admin 30000 30000

Net Profit (10000) 50000

Income statement when 5000 units sold:

Absorption Costing Method

Sales (25*5000) 125000

Less – Variable Cost

Direct Material 50000

Direct Labour 30000

Variable overhead 20000

Variable S & A 30000

Total Variable cost (130000)

Fixed Cost

Fixed Manufacturing overhead 40000

Fixed S&A expenses 30000

6

Total cost (200000)

Less – Closing Stock (5000*20) 100000 (100000)

Profit/(Loss) £25000

Marginal Costing Method

Sales (25* 5000) 125000

Less – Variable Cost

Direct Material 50000

Direct Labour 30000

Variable overhead 20000

Variable S & A 30000

Total Variable Cost (130000)

Less – Closing Stock valuation (5000 * £13) (65000)

Cost of goods sold (65000)

Contribution 6000

Fixed Cost (70000)

(Loss) (10000)

Income Statement using absorption costing

Sales (25 * 10000) 250000

Less – Variable Cost

Direct Material 50000

Direct Labour 30000

Variable overhead 20000

Variable S & A 30000

7

Less – Closing Stock (5000*20) 100000 (100000)

Profit/(Loss) £25000

Marginal Costing Method

Sales (25* 5000) 125000

Less – Variable Cost

Direct Material 50000

Direct Labour 30000

Variable overhead 20000

Variable S & A 30000

Total Variable Cost (130000)

Less – Closing Stock valuation (5000 * £13) (65000)

Cost of goods sold (65000)

Contribution 6000

Fixed Cost (70000)

(Loss) (10000)

Income Statement using absorption costing

Sales (25 * 10000) 250000

Less – Variable Cost

Direct Material 50000

Direct Labour 30000

Variable overhead 20000

Variable S & A 30000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

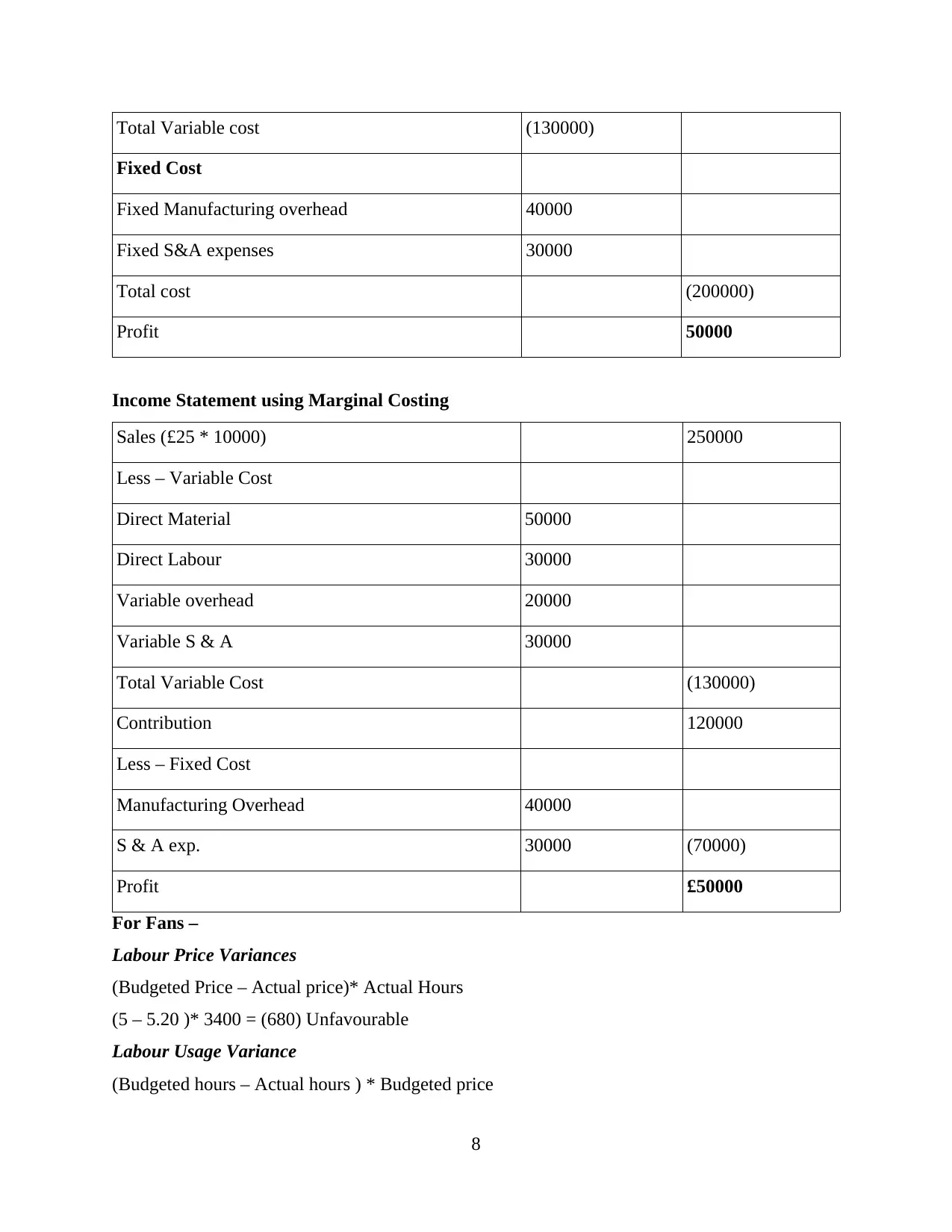

Total Variable cost (130000)

Fixed Cost

Fixed Manufacturing overhead 40000

Fixed S&A expenses 30000

Total cost (200000)

Profit 50000

Income Statement using Marginal Costing

Sales (£25 * 10000) 250000

Less – Variable Cost

Direct Material 50000

Direct Labour 30000

Variable overhead 20000

Variable S & A 30000

Total Variable Cost (130000)

Contribution 120000

Less – Fixed Cost

Manufacturing Overhead 40000

S & A exp. 30000 (70000)

Profit £50000

For Fans –

Labour Price Variances

(Budgeted Price – Actual price)* Actual Hours

(5 – 5.20 )* 3400 = (680) Unfavourable

Labour Usage Variance

(Budgeted hours – Actual hours ) * Budgeted price

8

Fixed Cost

Fixed Manufacturing overhead 40000

Fixed S&A expenses 30000

Total cost (200000)

Profit 50000

Income Statement using Marginal Costing

Sales (£25 * 10000) 250000

Less – Variable Cost

Direct Material 50000

Direct Labour 30000

Variable overhead 20000

Variable S & A 30000

Total Variable Cost (130000)

Contribution 120000

Less – Fixed Cost

Manufacturing Overhead 40000

S & A exp. 30000 (70000)

Profit £50000

For Fans –

Labour Price Variances

(Budgeted Price – Actual price)* Actual Hours

(5 – 5.20 )* 3400 = (680) Unfavourable

Labour Usage Variance

(Budgeted hours – Actual hours ) * Budgeted price

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(3000 – 3400) * 5 = (2000) Unfavourable

For packaging Boxes

Material Price Variances

(Budgeted Price – Actual price ) * Actual Usage

(10 – 9.5) *2200 = 1100 (Favourable)

Material Usage Variance

(Budgeted use – Actual use) * budgeted price

(2000 – 2200) *10 = (2000) unfavourable

M2 Apply a range of management accounting techniques and produce appropriate financial

accounting documents

Cost

It is the amount of money that spends by company on production of goods and services.

There are not including the mark up for profit.

Direct & Indirect cost – It can be defined as costs which can accurately traced to a cost

object with little effort. Indirect cost are also called overhead cost. It is divided according to

different sections after than calculate the overhead costs.

Cost allocation is used for financial reporting purpose and it is spread to cost among

departments or inventory items. It is used in the calculation of profitability at the section or

subsidiary level which is turn may be used on the basis of bonuses and funding (Gibassier,

2017).

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities

Fixed and variable cost and semi variable cost

A cost that does not change in total with the change in activity is known as fixed cost and

it is remain same in all year. It is changing according to production units and when company feel

that there are need to change fixed cost.

A cost that change in total with the change in the level of activity is called variable cost

and it is related to direct material cost.

A cost that the characteristics of both fixed cost is called mixed and semi variable cost.

Normal and standard costing

9

For packaging Boxes

Material Price Variances

(Budgeted Price – Actual price ) * Actual Usage

(10 – 9.5) *2200 = 1100 (Favourable)

Material Usage Variance

(Budgeted use – Actual use) * budgeted price

(2000 – 2200) *10 = (2000) unfavourable

M2 Apply a range of management accounting techniques and produce appropriate financial

accounting documents

Cost

It is the amount of money that spends by company on production of goods and services.

There are not including the mark up for profit.

Direct & Indirect cost – It can be defined as costs which can accurately traced to a cost

object with little effort. Indirect cost are also called overhead cost. It is divided according to

different sections after than calculate the overhead costs.

Cost allocation is used for financial reporting purpose and it is spread to cost among

departments or inventory items. It is used in the calculation of profitability at the section or

subsidiary level which is turn may be used on the basis of bonuses and funding (Gibassier,

2017).

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities

Fixed and variable cost and semi variable cost

A cost that does not change in total with the change in activity is known as fixed cost and

it is remain same in all year. It is changing according to production units and when company feel

that there are need to change fixed cost.

A cost that change in total with the change in the level of activity is called variable cost

and it is related to direct material cost.

A cost that the characteristics of both fixed cost is called mixed and semi variable cost.

Normal and standard costing

9

Normal costing is used to value manufactured products with the actual material cost, the

actual direct labour cost and manufacturing overhead based on a predetermination manufacturing

overhead rate.

Standard costing values its manufactured products with a predetermined material cost, a

planned direct labour cost and planned manufacturing overhead cost.

Inventory cost- This cost is associated with expenses of holding and storing stocks for

the purpose of sale. There are three types of inventory costs:-

Inventory purchase cost- It is related to buying raw materials or other components for

the purpose of resale or producing new product.

Inventory processing costs- These are related to doing some work on already existing

inventory and further selling it. For example assembling parts of product.

Inventory distribution cost- It is concerned with expenses of shipping and storing

inventory at distribution centre or warehouse before sales (Hilton and Platt, 2013).

TASK 3

P3. Advantages and disadvantages of different types of planning tools used for budgetary control

Budgetary control: It is a technique which helps in utilization of budgets by the

managers for evaluation, monitoring as well as controlling various costs associated with the

operations in a financial year. It provides a framework to the managers for setting financial along

with performance objectives with budgets for the purpose of comparing the actual results with

the forecasted budgets.

Budgetary planning: It is a tool which helps in preparing the budgets as well as utilizing

them for controlling the business operations. These are helpful in planning for future based on

past experiences.

Preparing a budget: Different organisations follow different procedures for preparing its

budgets. Clarasys Ltd prepares its budgets by listing its sources of incomes and tally them with

the past budgets. Then fixed costs are recorded of the current year along with expenses. Later all

the items are carefully analysed and recorded by the accountants in their budgetary statements.

All the steps are carefully monitored at all processes (Hirsch, Nitzl and Schauß, 2015).

Different types of budgets: The selected consultancy firm uses different types of budgets. These

are explained as:

10

actual direct labour cost and manufacturing overhead based on a predetermination manufacturing

overhead rate.

Standard costing values its manufactured products with a predetermined material cost, a

planned direct labour cost and planned manufacturing overhead cost.

Inventory cost- This cost is associated with expenses of holding and storing stocks for

the purpose of sale. There are three types of inventory costs:-

Inventory purchase cost- It is related to buying raw materials or other components for

the purpose of resale or producing new product.

Inventory processing costs- These are related to doing some work on already existing

inventory and further selling it. For example assembling parts of product.

Inventory distribution cost- It is concerned with expenses of shipping and storing

inventory at distribution centre or warehouse before sales (Hilton and Platt, 2013).

TASK 3

P3. Advantages and disadvantages of different types of planning tools used for budgetary control

Budgetary control: It is a technique which helps in utilization of budgets by the

managers for evaluation, monitoring as well as controlling various costs associated with the

operations in a financial year. It provides a framework to the managers for setting financial along

with performance objectives with budgets for the purpose of comparing the actual results with

the forecasted budgets.

Budgetary planning: It is a tool which helps in preparing the budgets as well as utilizing

them for controlling the business operations. These are helpful in planning for future based on

past experiences.

Preparing a budget: Different organisations follow different procedures for preparing its

budgets. Clarasys Ltd prepares its budgets by listing its sources of incomes and tally them with

the past budgets. Then fixed costs are recorded of the current year along with expenses. Later all

the items are carefully analysed and recorded by the accountants in their budgetary statements.

All the steps are carefully monitored at all processes (Hirsch, Nitzl and Schauß, 2015).

Different types of budgets: The selected consultancy firm uses different types of budgets. These

are explained as:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.