Management Accounting: Cost Analysis, Budgeting, and Reporting

VerifiedAdded on 2023/06/18

|17

|4362

|286

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on cost analysis techniques and budgetary control methods. It defines management accounting and its essential requirements, highlighting its role in decision-making within organizations like Prime Furniture. The report explores various methods of management accounting reporting, including budget reports and accounts receivable reports. It delves into cost analysis, explaining marginal and absorption costing, job costing, process costing, and ABC costing, with practical applications demonstrated through income statements. Furthermore, it discusses the advantages and disadvantages of different planning tools used for budgetary control, such as operating budgets and master budgets. The report concludes with a comparison of organizations in terms of adapting management accounting systems to address financial challenges.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of systems..........................................1

P2. Different methods of management accounting reporting......................................................2

TASK 2............................................................................................................................................3

P3: Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................3

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................8

TASK 4..........................................................................................................................................10

P5: Comparison of organizations...............................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of systems..........................................1

P2. Different methods of management accounting reporting......................................................2

TASK 2............................................................................................................................................3

P3: Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................3

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................8

TASK 4..........................................................................................................................................10

P5: Comparison of organizations...............................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting refers to the use of a wide range of methods and techniques

through which the organizations are able to ensure that they can attain their goals and objectives

by properly managing the financial data, facts and information in the right manner (Golyagina

and Valuckas, 2020). It is quite important that the use of Management Accounting is made by the

organizations for the particular purpose of taking of important decisions which can be quite

useful in managing the different types of needs and requirements in a proper way. Management

accounting is related to presenting information to forecast inconsistencies within finances in

order to make rational decisions to maximise profits together with minimise losses. For the

presentation, Prime Furniture is selected company which is a growing London Based

organisation. It is making plan for starting training courses for new internes.

The report covers definition of management accounting and essential requirements of

each management accounting system. It also highlights methods which are used by businesses in

management accounting reporting. The report highlights key management accounting techniques

for preparing income statement. It also explains usage of multiple planning tools in budgetary

control. At last, comparison among organisations in aspect of adapting management accounting

systems for the purpose of responding to problems related with funds are discussed.

TASK 1

P1. Management accounting and essential requirements of systems

Management accounting is defined as practice for recognising, measuring, evaluating,

interpreting and exchanging information about financial aspects to top management with pursuit

to goals of entity. In Prime Furniture, purpose which management accounting serve is to guide

users internal to business in well informed and rational decision making. Role of management

accounting in Prime Furniture is to conduct relevant cost analysis with the hope of determining

current expenses along with giving suggestions about future practices. It also plays role of

creating financial plans for any type of organisational undertaking related to financial department

(Johnstone, 2020).

Management accounting system could be described to internal systems of entity which

provides critical information to top managers for operational decision making. Prime Furniture is

a type of manufacturing entity that opts management accounting systems for costing addition to

1

Management Accounting refers to the use of a wide range of methods and techniques

through which the organizations are able to ensure that they can attain their goals and objectives

by properly managing the financial data, facts and information in the right manner (Golyagina

and Valuckas, 2020). It is quite important that the use of Management Accounting is made by the

organizations for the particular purpose of taking of important decisions which can be quite

useful in managing the different types of needs and requirements in a proper way. Management

accounting is related to presenting information to forecast inconsistencies within finances in

order to make rational decisions to maximise profits together with minimise losses. For the

presentation, Prime Furniture is selected company which is a growing London Based

organisation. It is making plan for starting training courses for new internes.

The report covers definition of management accounting and essential requirements of

each management accounting system. It also highlights methods which are used by businesses in

management accounting reporting. The report highlights key management accounting techniques

for preparing income statement. It also explains usage of multiple planning tools in budgetary

control. At last, comparison among organisations in aspect of adapting management accounting

systems for the purpose of responding to problems related with funds are discussed.

TASK 1

P1. Management accounting and essential requirements of systems

Management accounting is defined as practice for recognising, measuring, evaluating,

interpreting and exchanging information about financial aspects to top management with pursuit

to goals of entity. In Prime Furniture, purpose which management accounting serve is to guide

users internal to business in well informed and rational decision making. Role of management

accounting in Prime Furniture is to conduct relevant cost analysis with the hope of determining

current expenses along with giving suggestions about future practices. It also plays role of

creating financial plans for any type of organisational undertaking related to financial department

(Johnstone, 2020).

Management accounting system could be described to internal systems of entity which

provides critical information to top managers for operational decision making. Prime Furniture is

a type of manufacturing entity that opts management accounting systems for costing addition to

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

managing processes. Management accounting system tracks efficiency associated to internal

operations along with associated tasks to determine effectiveness of establishment in competitive

environment. It minimises errors, improves stock management, provides real time information

and data, enhance stages of decision making, gives high flexibility as well as enhances financial

visibility.

Kinds of management accounting systems that are used by Junior Accountant Manager of

Prime Furniture are as follows:

Cost accounting system: It refers to a system that is opted for estimation of cost of

offerings with the hope of profitability analysis and controlling unnecessary costs (Mahmoudian

and et.al., 2021). In Prime Furniture, essential requirement of cost accounting system is to keep

detailed and proper record of production activities, determine actual costs of manufacturing a

product and control redundant costs. It is flexible and specific system for subdividing costs and

value inventory.

Inventory management system: It is a system through which managers track goods

throughout supply chain that starts from purchase of raw material to end sales. Within Prime

Furniture, essential requirement of the system is to make process and practices to manage stock

or inventory easier and reduce risk of understock or overstock. It streamlines whole process and

eliminates inventory costs related to errors from human side.

P2. Different methods of management accounting reporting

Management accounting reporting is termed to a mechanism for planning, regulating,

measuring, making decisions and analysing performances through various reports (Zyznarska-

Dworczak, 2018). Within Prime Furniture, there are various methods opted for generating

management accounting reporting as per requirements. With these reporting methods, Junior

Accountant Manager of the entity highlight certain patterns additions to transmit them towards

useful information for the business.

Some methods that are used by managers of Prime Furniture related to management accounting

reporting are as follows:

Budget report: A method of management accounting reporting which lists past forecasted

budget projections over particular period and assist in devising budget for upcoming accounting

period for company is budget report (Pirilä, 2021). In Prime Furniture, budget report is opted for

2

operations along with associated tasks to determine effectiveness of establishment in competitive

environment. It minimises errors, improves stock management, provides real time information

and data, enhance stages of decision making, gives high flexibility as well as enhances financial

visibility.

Kinds of management accounting systems that are used by Junior Accountant Manager of

Prime Furniture are as follows:

Cost accounting system: It refers to a system that is opted for estimation of cost of

offerings with the hope of profitability analysis and controlling unnecessary costs (Mahmoudian

and et.al., 2021). In Prime Furniture, essential requirement of cost accounting system is to keep

detailed and proper record of production activities, determine actual costs of manufacturing a

product and control redundant costs. It is flexible and specific system for subdividing costs and

value inventory.

Inventory management system: It is a system through which managers track goods

throughout supply chain that starts from purchase of raw material to end sales. Within Prime

Furniture, essential requirement of the system is to make process and practices to manage stock

or inventory easier and reduce risk of understock or overstock. It streamlines whole process and

eliminates inventory costs related to errors from human side.

P2. Different methods of management accounting reporting

Management accounting reporting is termed to a mechanism for planning, regulating,

measuring, making decisions and analysing performances through various reports (Zyznarska-

Dworczak, 2018). Within Prime Furniture, there are various methods opted for generating

management accounting reporting as per requirements. With these reporting methods, Junior

Accountant Manager of the entity highlight certain patterns additions to transmit them towards

useful information for the business.

Some methods that are used by managers of Prime Furniture related to management accounting

reporting are as follows:

Budget report: A method of management accounting reporting which lists past forecasted

budget projections over particular period and assist in devising budget for upcoming accounting

period for company is budget report (Pirilä, 2021). In Prime Furniture, budget report is opted for

2

making comparison among estimates of budget and actual outcomes during designated

accounting period.

Account receivable report: Another method of management accounting reporting which

shows balances of unpaid voices with time period that have been outstanding is nature is named

to account receivable report. In Prime Furniture, accounting receivable report assist to determine

invoices which are open addition to allow keeping slow paying clients on top list.

TASK 2

P3: Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Cost – This means a monetary value that arises in business activities while buying any

products and services. To run a business and managing functions cost can be occurring that

needs to be pay out of income and profits. Within Prime Furniture, cost is considered as amount

of monetary resources that are spent on producing products. It restricts inclusion of mark-up for

profit. Different costs in manufacturing a product includes fixed cost, variable cost, operating

cost, indirect cost and many more.

Marginal costing – This can be explained as costing technique of presenting sales and

cost data where management are responsible to make short term decision like make or buy,

acceptance of special order, and sales mix selection. This involves variable cost of products and

services which are used to develop business. With usage of marginal costing, junior accountant

of Prime Furniture controls cost effectively, treats overheads in simplified manner, plan

production properly and attain better results.

Absorption costing – This is cost calculating technique that takes in to account indirect

expenses and direct costs. This involves manufacturing cost of products and services by

considering fixed and variable (Kozachenko, Panadiy, and Сhudak, 2019). Though absorption

costing, junior accountant of Prime Furniture is able recognise all costs that are involved in

manufacturing and accurately tracks profits within definite accounting period.

Job costing: It is a costing method which is used to determine the cost associated to

specific jobs or occupation that are performed as per customer’s specifications (Wells, 2020).

Junior accountant of Prime Furniture uses the method to analyse separate projects or contract

jobs.

3

accounting period.

Account receivable report: Another method of management accounting reporting which

shows balances of unpaid voices with time period that have been outstanding is nature is named

to account receivable report. In Prime Furniture, accounting receivable report assist to determine

invoices which are open addition to allow keeping slow paying clients on top list.

TASK 2

P3: Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs

Cost – This means a monetary value that arises in business activities while buying any

products and services. To run a business and managing functions cost can be occurring that

needs to be pay out of income and profits. Within Prime Furniture, cost is considered as amount

of monetary resources that are spent on producing products. It restricts inclusion of mark-up for

profit. Different costs in manufacturing a product includes fixed cost, variable cost, operating

cost, indirect cost and many more.

Marginal costing – This can be explained as costing technique of presenting sales and

cost data where management are responsible to make short term decision like make or buy,

acceptance of special order, and sales mix selection. This involves variable cost of products and

services which are used to develop business. With usage of marginal costing, junior accountant

of Prime Furniture controls cost effectively, treats overheads in simplified manner, plan

production properly and attain better results.

Absorption costing – This is cost calculating technique that takes in to account indirect

expenses and direct costs. This involves manufacturing cost of products and services by

considering fixed and variable (Kozachenko, Panadiy, and Сhudak, 2019). Though absorption

costing, junior accountant of Prime Furniture is able recognise all costs that are involved in

manufacturing and accurately tracks profits within definite accounting period.

Job costing: It is a costing method which is used to determine the cost associated to

specific jobs or occupation that are performed as per customer’s specifications (Wells, 2020).

Junior accountant of Prime Furniture uses the method to analyse separate projects or contract

jobs.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

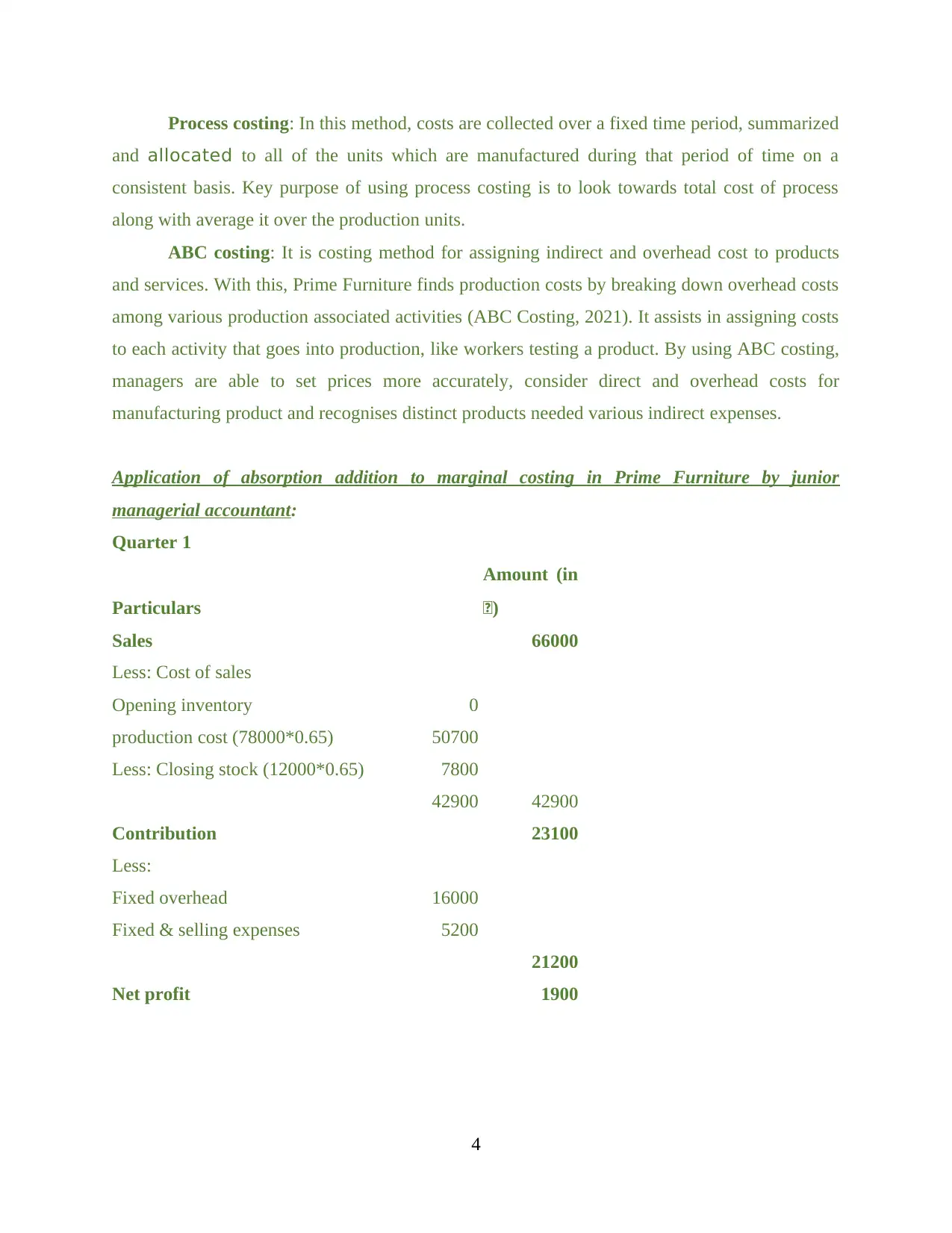

Process costing: In this method, costs are collected over a fixed time period, summarized

and allocated to all of the units which are manufactured during that period of time on a

consistent basis. Key purpose of using process costing is to look towards total cost of process

along with average it over the production units.

ABC costing: It is costing method for assigning indirect and overhead cost to products

and services. With this, Prime Furniture finds production costs by breaking down overhead costs

among various production associated activities (ABC Costing, 2021). It assists in assigning costs

to each activity that goes into production, like workers testing a product. By using ABC costing,

managers are able to set prices more accurately, consider direct and overhead costs for

manufacturing product and recognises distinct products needed various indirect expenses.

Application of absorption addition to marginal costing in Prime Furniture by junior

managerial accountant:

Quarter 1

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

4

and allocated to all of the units which are manufactured during that period of time on a

consistent basis. Key purpose of using process costing is to look towards total cost of process

along with average it over the production units.

ABC costing: It is costing method for assigning indirect and overhead cost to products

and services. With this, Prime Furniture finds production costs by breaking down overhead costs

among various production associated activities (ABC Costing, 2021). It assists in assigning costs

to each activity that goes into production, like workers testing a product. By using ABC costing,

managers are able to set prices more accurately, consider direct and overhead costs for

manufacturing product and recognises distinct products needed various indirect expenses.

Application of absorption addition to marginal costing in Prime Furniture by junior

managerial accountant:

Quarter 1

Particulars

Amount (in

£)

Sales 66000

Less: Cost of sales

Opening inventory 0

production cost (78000*0.65) 50700

Less: Closing stock (12000*0.65) 7800

42900 42900

Contribution 23100

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 1900

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

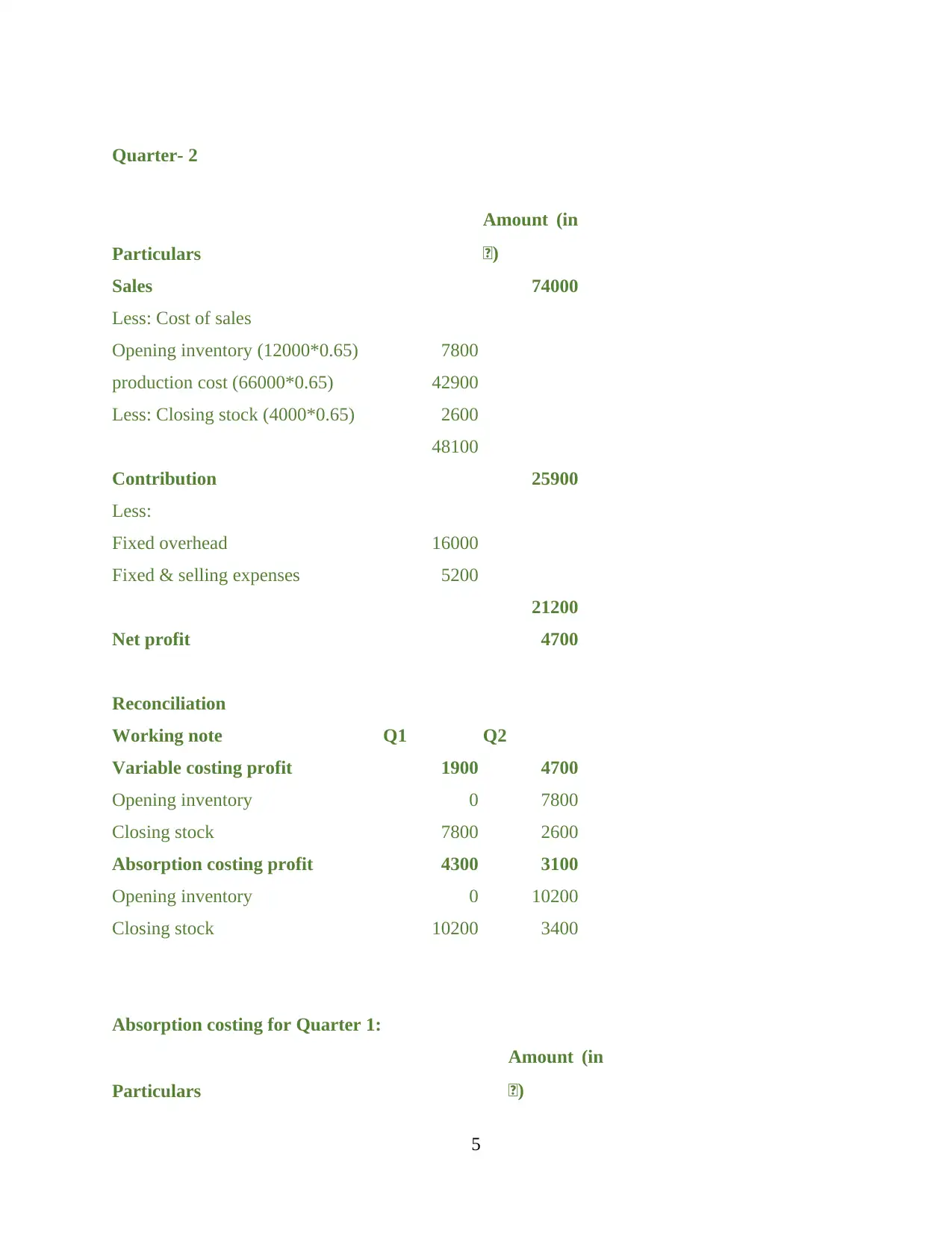

Quarter- 2

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

5

Particulars

Amount (in

£)

Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed & selling expenses 5200

21200

Net profit 4700

Reconciliation

Working note Q1 Q2

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Absorption costing for Quarter 1:

Particulars

Amount (in

£)

5

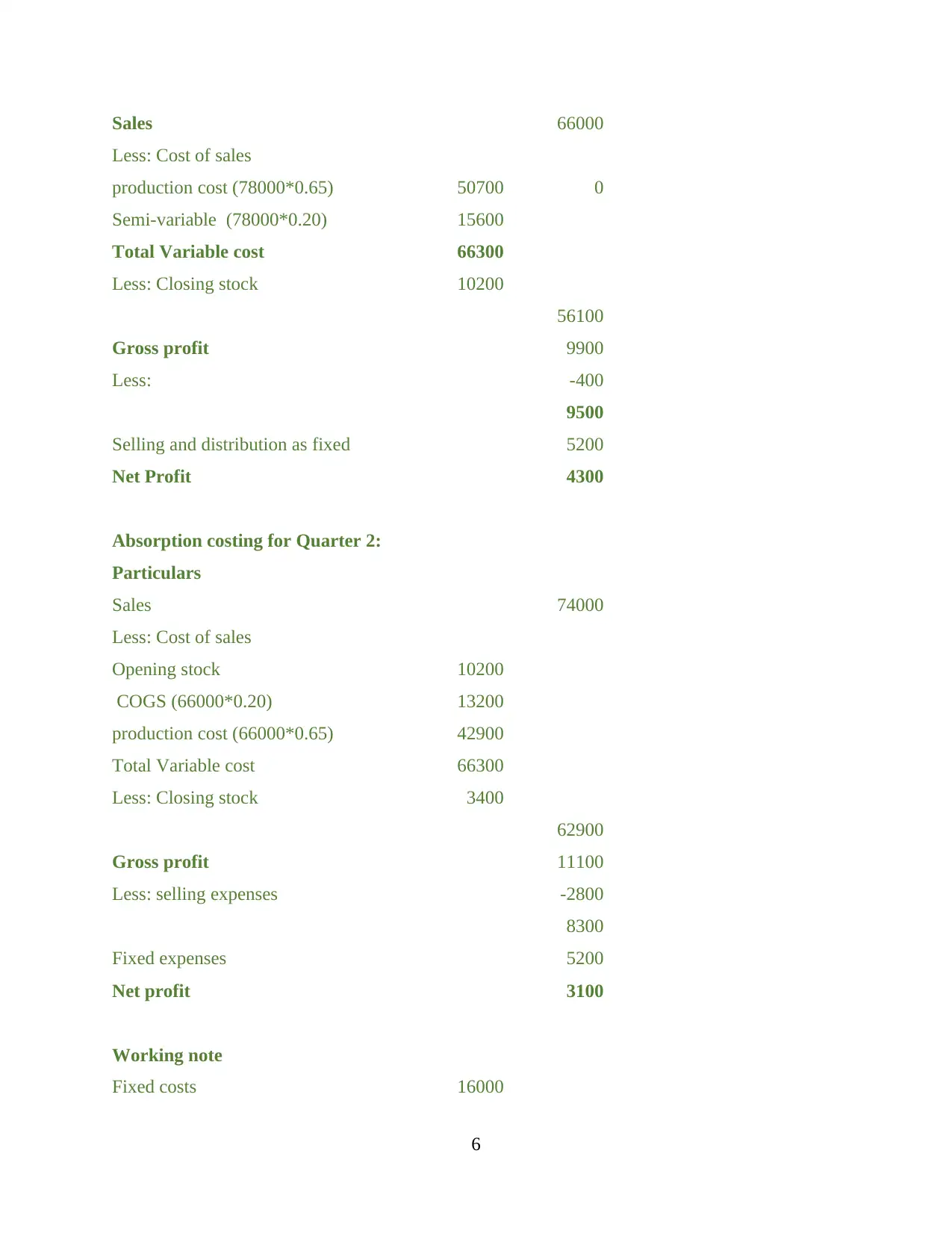

Sales 66000

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

6

Less: Cost of sales

production cost (78000*0.65) 50700 0

Semi-variable (78000*0.20) 15600

Total Variable cost 66300

Less: Closing stock 10200

56100

Gross profit 9900

Less: -400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Absorption costing for Quarter 2:

Particulars

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*0.20) 13200

production cost (66000*0.65) 42900

Total Variable cost 66300

Less: Closing stock 3400

62900

Gross profit 11100

Less: selling expenses -2800

8300

Fixed expenses 5200

Net profit 3100

Working note

Fixed costs 16000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

Product costing:

Fixed along with variable cost, allocation of cost: The term fixed cost is said to cost

which lacks changes with modifications in volume of activities. In contrary, variable cost is

defined to costs associated to activity volumes. Within Prime Furniture, cost allocation is an

aspect to classify, accumulate along with assigning of costs to objects.

Normal and standard, activity based costing addition to role of costing in

establishing prices: In context to normal costing, actual data is preferred for deriving product

cost with exception of producing overhead rate. However, within standard costing, costs that are

used are predetermined that is based on budgeted costs. In Prime Furniture, role of costing is

setting price is to look towards all business activities and adding them to reach final cost prior

establishing product prices. It also helps in controlling unnecessary costs along with improving

price efficiency.

Analysing variation in profits:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

Reconciliation Statements:

Particular Q1 Q2

Profit from absorption 4700 5900

7

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

Product costing:

Fixed along with variable cost, allocation of cost: The term fixed cost is said to cost

which lacks changes with modifications in volume of activities. In contrary, variable cost is

defined to costs associated to activity volumes. Within Prime Furniture, cost allocation is an

aspect to classify, accumulate along with assigning of costs to objects.

Normal and standard, activity based costing addition to role of costing in

establishing prices: In context to normal costing, actual data is preferred for deriving product

cost with exception of producing overhead rate. However, within standard costing, costs that are

used are predetermined that is based on budgeted costs. In Prime Furniture, role of costing is

setting price is to look towards all business activities and adding them to reach final cost prior

establishing product prices. It also helps in controlling unnecessary costs along with improving

price efficiency.

Analysing variation in profits:

For the first quarter:

Overhead absorbed= (66000*0.20)= 13,200

Fixed overhead costs= 16,000

Under absorption: (2,800)

For Second quarter:

Total absorbed expenses: (74000*0.20)= 14,800

Fixed costs= 16,000

Under absorption= (1200)

Reconciliation Statements:

Particular Q1 Q2

Profit from absorption 4700 5900

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

-2800 -1200

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control

Budget is described to a financial plan that outlines expenses and revenues for defined

accounting period. In Prime Furniture, preparing a budget is essential to manage money

effectively, improve decision making, identify financial problems prior to occurrence, allocate

funds appropriately to projects and monitor financial performances. Budget enables junior

accountant manager of establishment to take benefit of purchasing along with investing

opportunities, plan ways to lower debts and allocate funds in all business departments. Planning

tool are mechanisms to plan future of company. In accounting, planning tools are budgets that

guides management and team to make revenue with appropriate spending. Different kinds of

budget that are used as planning tool in Prime Furniture are as explained:

Operating Budget – This is a type of planning tool which is used by management to

contain the all income and expenditures that are generated from daily business function. In

relation to Prime Furniture, management uses the operating budget for the purpose of keeping

record of all day to day transaction and develop business activities. This can help to develop the

business activities and performance in competitive environment by keeping records of all

transactions (Aitken-Davies, 2020).

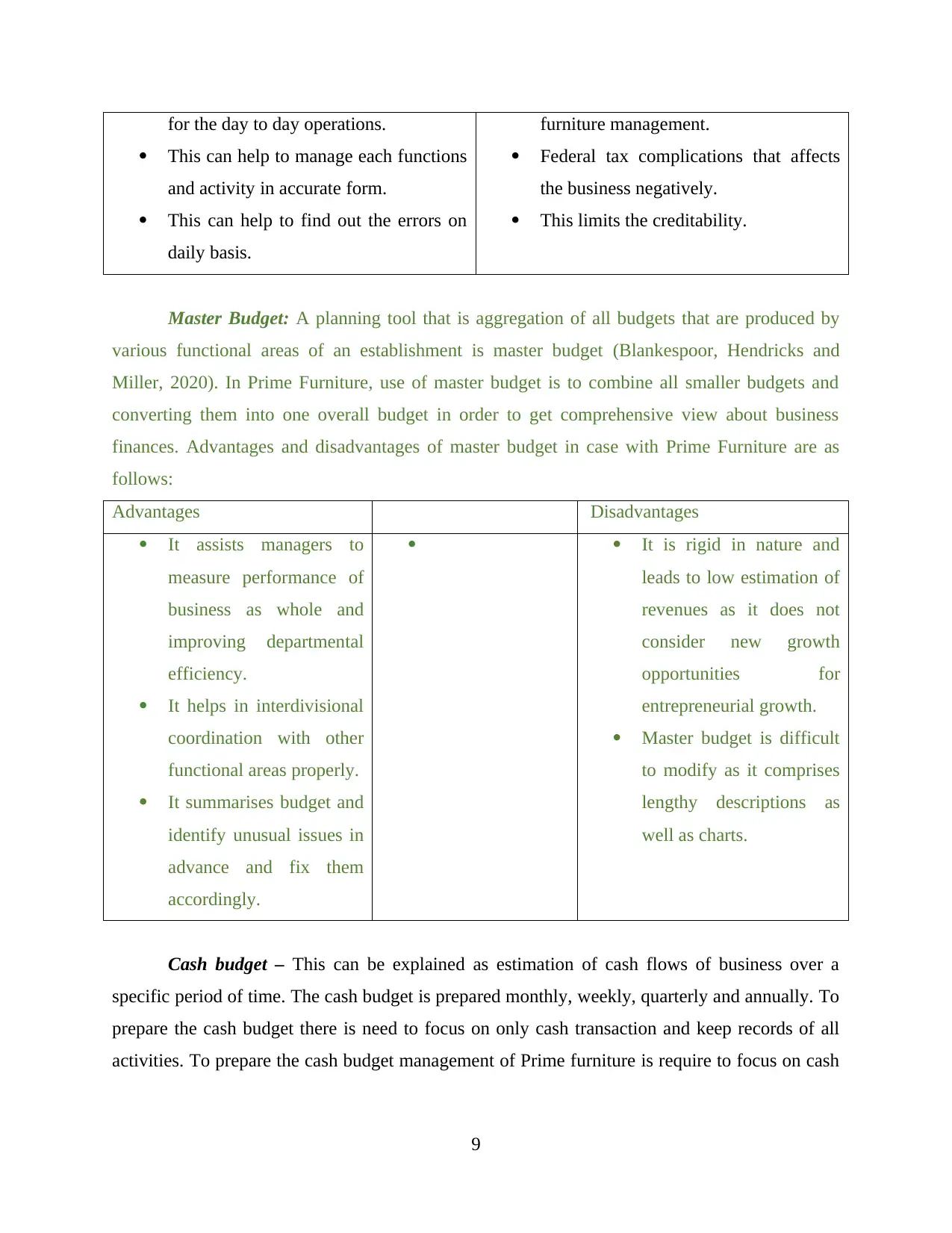

Advantages Disadvantages

This helps management to make plan This is time taken planning tool that can

be create the challenge for Prime

8

Profits as from marginal 1900 4700

Working notes:

Fixed charges= 16,000

=66000*0.20= 13,200

Under absorption=(2800)

= 74000*0.20= 14,800

Fixed expenditure: 16000

Under absorption= (1200)

P4: Explain the advantages and disadvantages of different types of planning tools used for

budgetary control

Budget is described to a financial plan that outlines expenses and revenues for defined

accounting period. In Prime Furniture, preparing a budget is essential to manage money

effectively, improve decision making, identify financial problems prior to occurrence, allocate

funds appropriately to projects and monitor financial performances. Budget enables junior

accountant manager of establishment to take benefit of purchasing along with investing

opportunities, plan ways to lower debts and allocate funds in all business departments. Planning

tool are mechanisms to plan future of company. In accounting, planning tools are budgets that

guides management and team to make revenue with appropriate spending. Different kinds of

budget that are used as planning tool in Prime Furniture are as explained:

Operating Budget – This is a type of planning tool which is used by management to

contain the all income and expenditures that are generated from daily business function. In

relation to Prime Furniture, management uses the operating budget for the purpose of keeping

record of all day to day transaction and develop business activities. This can help to develop the

business activities and performance in competitive environment by keeping records of all

transactions (Aitken-Davies, 2020).

Advantages Disadvantages

This helps management to make plan This is time taken planning tool that can

be create the challenge for Prime

8

for the day to day operations.

This can help to manage each functions

and activity in accurate form.

This can help to find out the errors on

daily basis.

furniture management.

Federal tax complications that affects

the business negatively.

This limits the creditability.

Master Budget: A planning tool that is aggregation of all budgets that are produced by

various functional areas of an establishment is master budget (Blankespoor, Hendricks and

Miller, 2020). In Prime Furniture, use of master budget is to combine all smaller budgets and

converting them into one overall budget in order to get comprehensive view about business

finances. Advantages and disadvantages of master budget in case with Prime Furniture are as

follows:

Advantages Disadvantages

It assists managers to

measure performance of

business as whole and

improving departmental

efficiency.

It helps in interdivisional

coordination with other

functional areas properly.

It summarises budget and

identify unusual issues in

advance and fix them

accordingly.

It is rigid in nature and

leads to low estimation of

revenues as it does not

consider new growth

opportunities for

entrepreneurial growth.

Master budget is difficult

to modify as it comprises

lengthy descriptions as

well as charts.

Cash budget – This can be explained as estimation of cash flows of business over a

specific period of time. The cash budget is prepared monthly, weekly, quarterly and annually. To

prepare the cash budget there is need to focus on only cash transaction and keep records of all

activities. To prepare the cash budget management of Prime furniture is require to focus on cash

9

This can help to manage each functions

and activity in accurate form.

This can help to find out the errors on

daily basis.

furniture management.

Federal tax complications that affects

the business negatively.

This limits the creditability.

Master Budget: A planning tool that is aggregation of all budgets that are produced by

various functional areas of an establishment is master budget (Blankespoor, Hendricks and

Miller, 2020). In Prime Furniture, use of master budget is to combine all smaller budgets and

converting them into one overall budget in order to get comprehensive view about business

finances. Advantages and disadvantages of master budget in case with Prime Furniture are as

follows:

Advantages Disadvantages

It assists managers to

measure performance of

business as whole and

improving departmental

efficiency.

It helps in interdivisional

coordination with other

functional areas properly.

It summarises budget and

identify unusual issues in

advance and fix them

accordingly.

It is rigid in nature and

leads to low estimation of

revenues as it does not

consider new growth

opportunities for

entrepreneurial growth.

Master budget is difficult

to modify as it comprises

lengthy descriptions as

well as charts.

Cash budget – This can be explained as estimation of cash flows of business over a

specific period of time. The cash budget is prepared monthly, weekly, quarterly and annually. To

prepare the cash budget there is need to focus on only cash transaction and keep records of all

activities. To prepare the cash budget management of Prime furniture is require to focus on cash

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.