Management Accounting Analysis for Playdough Company Report

VerifiedAdded on 2019/11/25

|9

|1533

|163

Report

AI Summary

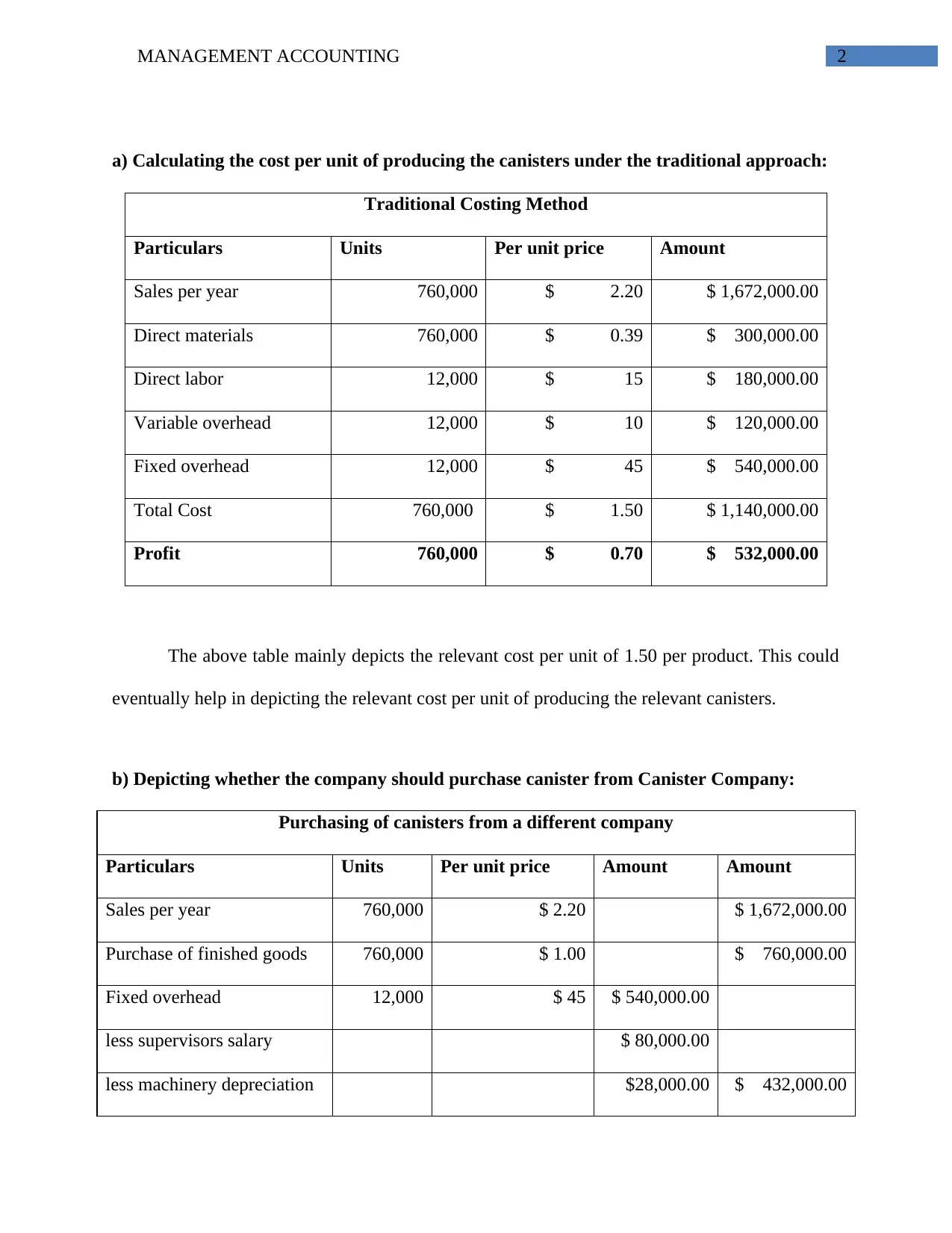

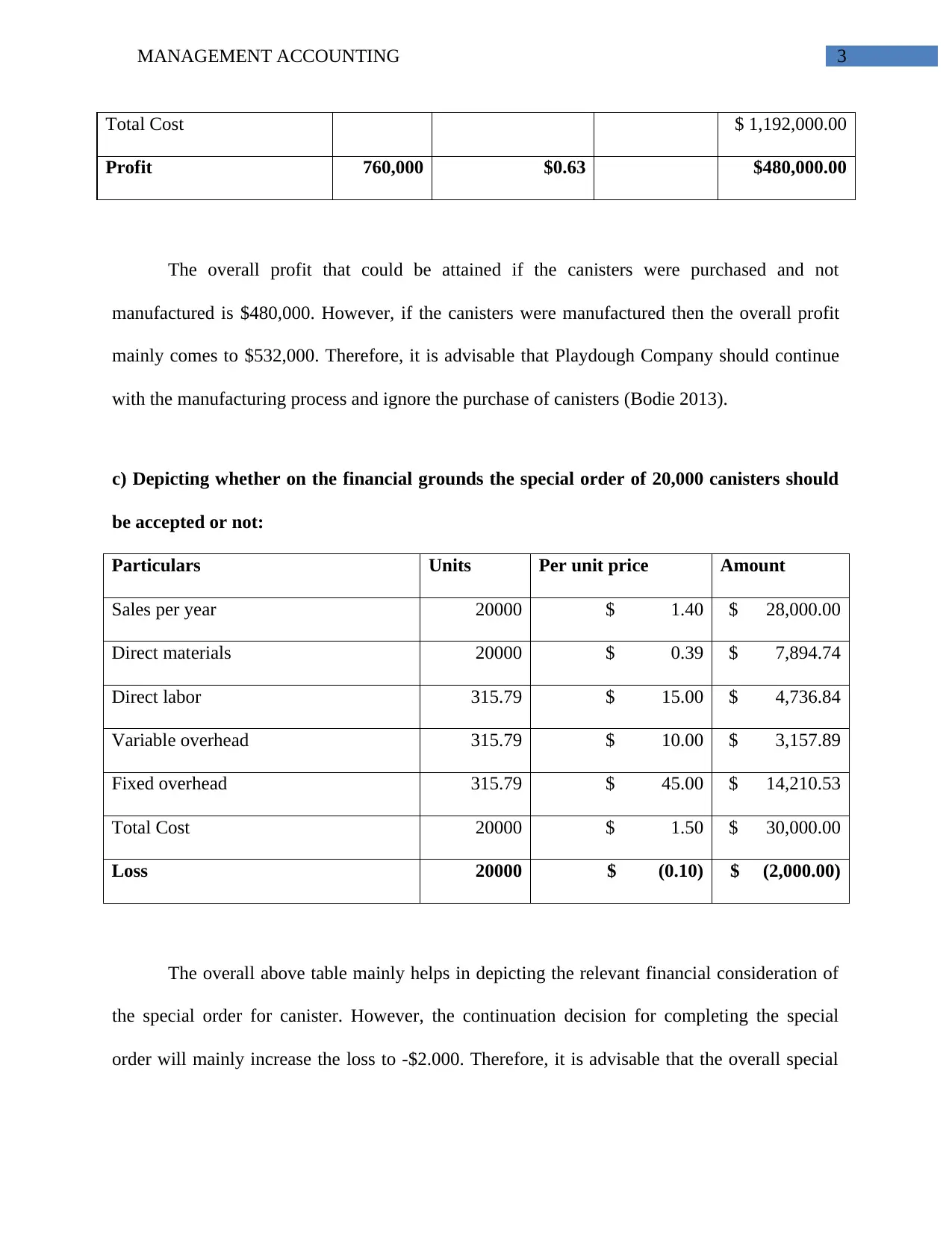

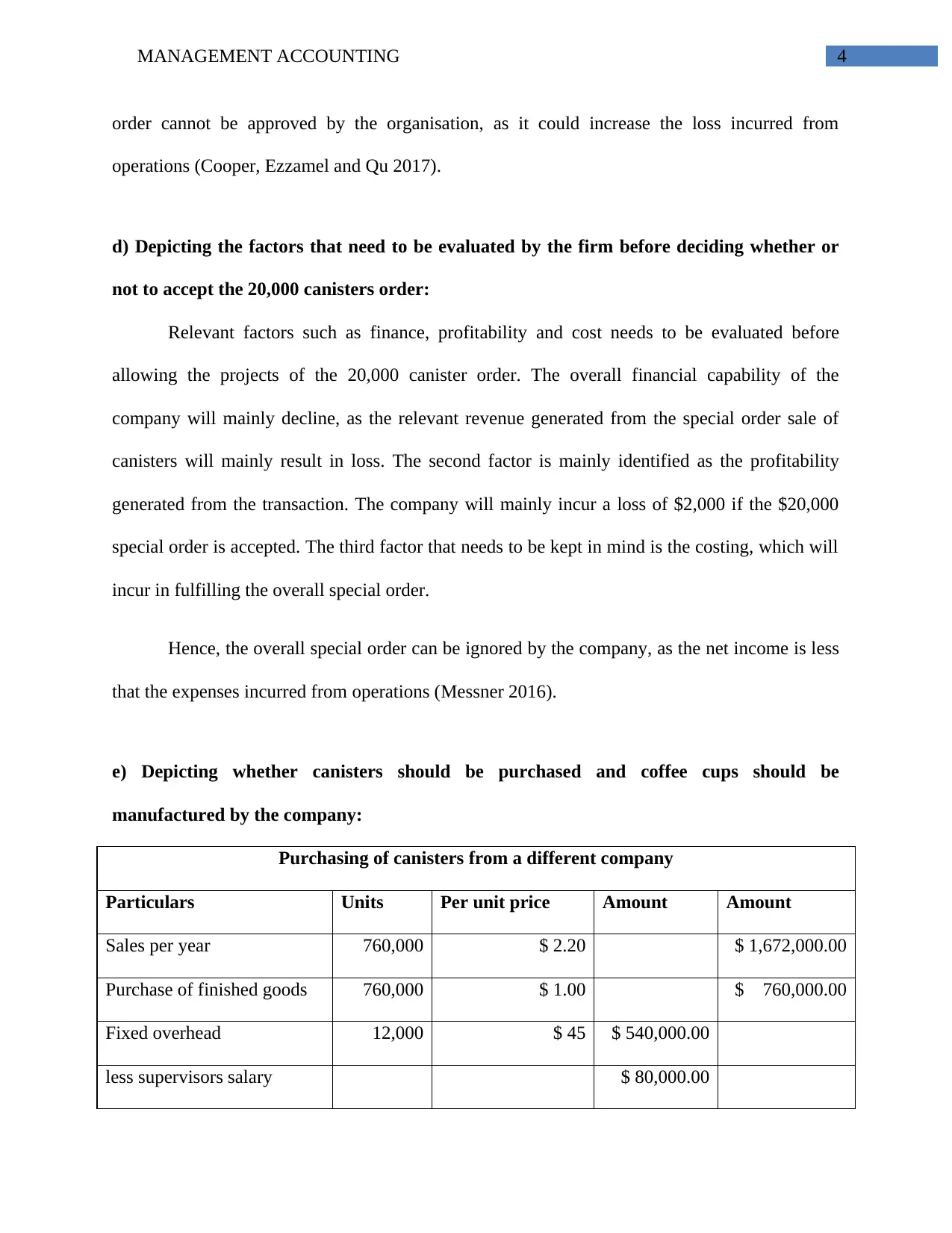

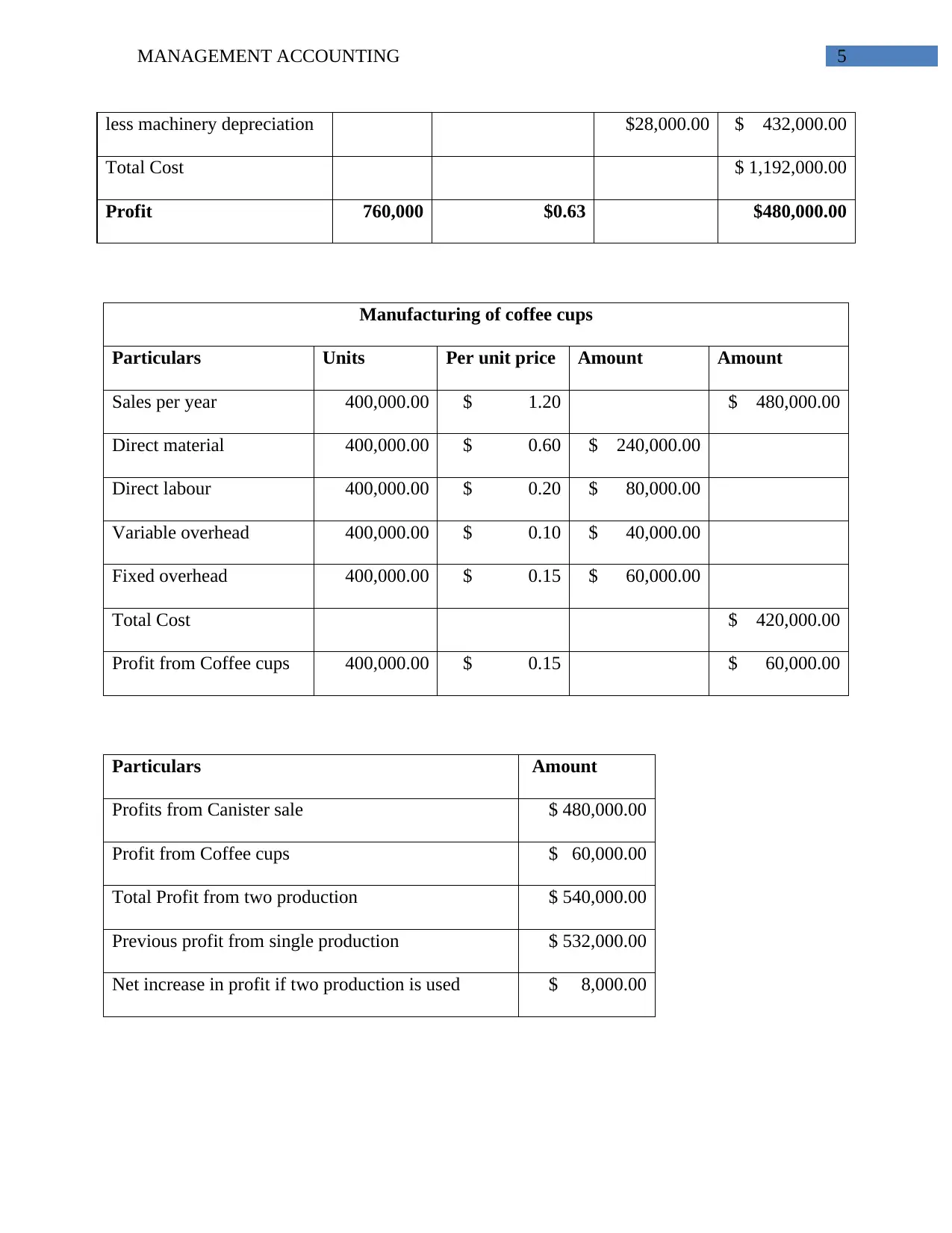

This report provides a detailed analysis of management accounting principles applied to the Playdough Company. It begins by calculating the cost per unit of producing canisters using the traditional costing method, establishing a baseline for financial analysis. The report then explores the make-or-buy decision, comparing the profitability of manufacturing canisters versus purchasing them from an external supplier, and determines that manufacturing is the more profitable option. A crucial part of the analysis evaluates a special order of 20,000 canisters, concluding that accepting this order would result in a loss. The report outlines the factors the firm should consider before accepting the special order, emphasizing financial capability, profitability, and cost. Furthermore, the report assesses the strategic implications of purchasing canisters while manufacturing coffee cups, concluding that this combination yields a higher overall profit. Finally, it discusses the key factors, including profitability, resource availability, and product quality, that the company must consider when deciding between manufacturing and purchasing canisters. The report uses financial data and calculations to support its conclusions, offering valuable insights into the financial management of the Playdough Company.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.