Comprehensive Report on Management Accounting Systems and Reports

VerifiedAdded on 2023/02/01

|17

|4709

|97

Report

AI Summary

This report delves into the realm of management accounting, specifically examining its systems and their interplay with management accounting reports. The study focuses on ABC Ltd, a medium-sized manufacturing enterprise, and explores various management accounting systems such as inventory management, job costing, and cost accounting, highlighting their roles in cost analysis and decision-making. The report further analyzes different management accounting reports, including budget reports, accounts receivable aging reports, performance reports, and cost managerial accounting reports, emphasizing their significance in evaluating performance and improving efficiency. The study includes practical applications, such as preparing income statements using absorption and marginal costing methods and assessing the advantages and disadvantages of budgetary control tools like cash budgets, providing valuable insights for effective financial management and strategic planning.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

..........................................................................................................................................................2

TASK 1............................................................................................................................................5

TASK 2............................................................................................................................................8

TASK 3..........................................................................................................................................11

TASK 4..........................................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

..........................................................................................................................................................2

TASK 1............................................................................................................................................5

TASK 2............................................................................................................................................8

TASK 3..........................................................................................................................................11

TASK 4..........................................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is basically consisted of the internal system of the organisation'

which is used to measure and evaluate the process for the management of the organisation. It is

the process of analysing and evaluating the cost of running and managing the business. And

includes the preparation of reports which help, organisation in further decision making which

help in achieving organisational goal.

The present study is based on the ABC Ltd a medium sized enterprise in manufacturing

sector. The report will include the study about the management accounting system and their

relation to the management accounting reports.

Furthermore, it will explain about the different planning tools for budgetary control

which helps the organisation in achieving their gaols effectively and efficiently.

TASK 1

Management accounting is basically consisted of the internal system of the organisation'

which is used to measure and evaluating the process for the management of the organisation. It is

the process of preparing the management reports and accounts which provide accurate, reliable,

timely financial and statical information to the mangers of the company to make the useful short

term ad long term decisions (Hall, 2016). It is the process of analysing and evaluating the cost of

running and managing the business. The company's affairs are managed under the management

accounting.

There are different types of management accounting system which helps in effectively managing

the business operations some of them are:

Inventory management system-

This system is used to manage the stock of the company and inflow and outflow of the

stock of the Company (Skouloudis, Malesios and Dimitrakopoulos, 2019). This system is

required by the organisation in order to control and oversee the ordering, use and storing of the

components which business is used in the production of the goods. It also combines the

application of barcode scanners, mobile devices, barcode printers, desktop software so that they

can streamline the inventory management as like consumable goods, stock and supplies. This

system is used to control the quantities of the finished goods' for sale. The objective of the

inventory management is to accurately and appropriate management of the present inventory

Management accounting is basically consisted of the internal system of the organisation'

which is used to measure and evaluate the process for the management of the organisation. It is

the process of analysing and evaluating the cost of running and managing the business. And

includes the preparation of reports which help, organisation in further decision making which

help in achieving organisational goal.

The present study is based on the ABC Ltd a medium sized enterprise in manufacturing

sector. The report will include the study about the management accounting system and their

relation to the management accounting reports.

Furthermore, it will explain about the different planning tools for budgetary control

which helps the organisation in achieving their gaols effectively and efficiently.

TASK 1

Management accounting is basically consisted of the internal system of the organisation'

which is used to measure and evaluating the process for the management of the organisation. It is

the process of preparing the management reports and accounts which provide accurate, reliable,

timely financial and statical information to the mangers of the company to make the useful short

term ad long term decisions (Hall, 2016). It is the process of analysing and evaluating the cost of

running and managing the business. The company's affairs are managed under the management

accounting.

There are different types of management accounting system which helps in effectively managing

the business operations some of them are:

Inventory management system-

This system is used to manage the stock of the company and inflow and outflow of the

stock of the Company (Skouloudis, Malesios and Dimitrakopoulos, 2019). This system is

required by the organisation in order to control and oversee the ordering, use and storing of the

components which business is used in the production of the goods. It also combines the

application of barcode scanners, mobile devices, barcode printers, desktop software so that they

can streamline the inventory management as like consumable goods, stock and supplies. This

system is used to control the quantities of the finished goods' for sale. The objective of the

inventory management is to accurately and appropriate management of the present inventory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

levels and minimizing overstock and under stock situations of the company through effective

tracking mangers will lead to know and take the sufficient and effective inventory

decisions(Boiral, 2016).

Job costing systems-

It refers to the system which allocated the manufacturing cost to individual unit or item

of the products. This system is applied when the goods are processed are different from one

another. It basically involves the process of accumulating the data on the cost related to

production job. This information can be sued to submit the cost data to consumer under some

contracts in which costs are refunded (van Helden and Uddin, 2016). The information generated

to this system also help in determining the accuracy of estimating system of the company that in

such a way that they must be in capable of quoting the right prices with permit for a reasonable

income.

Cost accounting systems -Cost accounting system is also called the product costing system or

costing system which is the framework used by the companies to estimate their cost of the

products and services for analysing profitability, inventory valuation and cost control, there are

generally two types of counting systems that is Jo order costing ad process costing (O'Dwyer and

Unerman, 2016)

Job order costing is the system of assigning the cost of individual unity of output whereas

process costing is method which traces and accumulate the direct and indirect cost of

manufacturing the goods. Costing system measure and record the costs and then compare the

input outcome to actual result or output so that they can assist management of the company for

measuring the financial performance of the business.

Price optimization systems

Price optimization is the system in which application of mathematical analysis is applied

on the organisation to determine that how the consumers will react to different price for the

goods and services (Kaplan and Atkinson, 2015). This system is also useful in determining that

price which is best for maximizing the satisfaction of the customers and helps in maximizing the

operating profit of the company's so that they can able to achieve the highest performance in

attracting more and more customers towards the organisation which helps them in achieving

their organisational goal.

Different Methods used for management Accounting reports

tracking mangers will lead to know and take the sufficient and effective inventory

decisions(Boiral, 2016).

Job costing systems-

It refers to the system which allocated the manufacturing cost to individual unit or item

of the products. This system is applied when the goods are processed are different from one

another. It basically involves the process of accumulating the data on the cost related to

production job. This information can be sued to submit the cost data to consumer under some

contracts in which costs are refunded (van Helden and Uddin, 2016). The information generated

to this system also help in determining the accuracy of estimating system of the company that in

such a way that they must be in capable of quoting the right prices with permit for a reasonable

income.

Cost accounting systems -Cost accounting system is also called the product costing system or

costing system which is the framework used by the companies to estimate their cost of the

products and services for analysing profitability, inventory valuation and cost control, there are

generally two types of counting systems that is Jo order costing ad process costing (O'Dwyer and

Unerman, 2016)

Job order costing is the system of assigning the cost of individual unity of output whereas

process costing is method which traces and accumulate the direct and indirect cost of

manufacturing the goods. Costing system measure and record the costs and then compare the

input outcome to actual result or output so that they can assist management of the company for

measuring the financial performance of the business.

Price optimization systems

Price optimization is the system in which application of mathematical analysis is applied

on the organisation to determine that how the consumers will react to different price for the

goods and services (Kaplan and Atkinson, 2015). This system is also useful in determining that

price which is best for maximizing the satisfaction of the customers and helps in maximizing the

operating profit of the company's so that they can able to achieve the highest performance in

attracting more and more customers towards the organisation which helps them in achieving

their organisational goal.

Different Methods used for management Accounting reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are different types of management accounting reports which are used by the

organisation to manage the transactions effectively and efficiently so that accurate, reliable and

appropriate information can be generated which can be use further for making the useful

decisions. Some essential reports made by the company are:

Budget report-These budgets report re made by the organisation department wise so that these

budgets helps the organisation in estimating their requirements of future and they will able to

arrange the resource to continue the operations of the business (Otley, 2016) The budgets which

are made by the company are completely based on the previous experiences and effective

research which will lead to preparation of the budgets. After completion of the activities the

companies compare the actual with estimated so to ascertain the difference between them and to

eliminate the deviation so that actual and estimated budget can be matched.

Accounts Receivable ageing reports- If the organisation is heavily relies in extending the credit

to the parties or customers than they need to prepare the account receivables ageing report which

specifies the balance of the client with specified tie period which is allowed to them so that

company can able to identify the defaulters as well as find issues and problems in the collection

process (Ismail, Isa and Mia, 2018). If in the case there are many defaulters than company needs

to make tighter credit policies as because cash inflow is very essential in the operation of any

business.

Performance reports -Performance reports are created by the company fort reviewing the

performance of the company as whole and as each individual to ascertain the efficiency and

effectiveness of activities performed by them. Departmental performance' reports are also

generated by the organisation in order to measure that each department is work according to the

direction of achieving goal or not (Schaltegger and Burritt, 2017). If not than corrective measures

are taken for improving the performance as by giving effective training and development

performance of the employees can be improved. The role of the performance report is vital and

essential for the company so that they can keep and accurate measure for their strategies towards

the goal and mission.

Cost managerial accounting reports -A cost report is the report which summarise the

information regarding the various costs associated with the organisation. The cost of the articles

which are manufactured and all the raw materials costs, variable costs, overhead costs, and any

organisation to manage the transactions effectively and efficiently so that accurate, reliable and

appropriate information can be generated which can be use further for making the useful

decisions. Some essential reports made by the company are:

Budget report-These budgets report re made by the organisation department wise so that these

budgets helps the organisation in estimating their requirements of future and they will able to

arrange the resource to continue the operations of the business (Otley, 2016) The budgets which

are made by the company are completely based on the previous experiences and effective

research which will lead to preparation of the budgets. After completion of the activities the

companies compare the actual with estimated so to ascertain the difference between them and to

eliminate the deviation so that actual and estimated budget can be matched.

Accounts Receivable ageing reports- If the organisation is heavily relies in extending the credit

to the parties or customers than they need to prepare the account receivables ageing report which

specifies the balance of the client with specified tie period which is allowed to them so that

company can able to identify the defaulters as well as find issues and problems in the collection

process (Ismail, Isa and Mia, 2018). If in the case there are many defaulters than company needs

to make tighter credit policies as because cash inflow is very essential in the operation of any

business.

Performance reports -Performance reports are created by the company fort reviewing the

performance of the company as whole and as each individual to ascertain the efficiency and

effectiveness of activities performed by them. Departmental performance' reports are also

generated by the organisation in order to measure that each department is work according to the

direction of achieving goal or not (Schaltegger and Burritt, 2017). If not than corrective measures

are taken for improving the performance as by giving effective training and development

performance of the employees can be improved. The role of the performance report is vital and

essential for the company so that they can keep and accurate measure for their strategies towards

the goal and mission.

Cost managerial accounting reports -A cost report is the report which summarise the

information regarding the various costs associated with the organisation. The cost of the articles

which are manufactured and all the raw materials costs, variable costs, overhead costs, and any

other added cots are taken into consideration and the totals are divided by the total amount of the

products produced. This reports help the mangers to estimate the cost price of items with their

selling price so to ascertain the actual profit earned (Quattrone, 2016().

There are several benefits of the management accounting which help the company in

improving their overall efficiency and lead the organisation in achieving their goals and

missions.

Management accounting helps in measuring the actual performance with the estimated

budgets to eliminate the deviations.

By effective budgeting and planning function of the management accounting businesses

activities are managed better and effectively.

It helps to increase the overall efficiency of the business.

It helps to improve the relation between the management ad the employees and other

members of the organisation (Bennett and James, 2017).

This help management for making future plans based on the past results and experiences.

Through the management accounting effective communication can be take place between

the top and lower level of the organisation

Management accounting system and management accounting report is integrated with

organisation process in way that with the help of systems management accounting reports can be

made say with job costing system, job costing report can be made. And these reports help the

management in taking the corrective and effective decisions which help further in directing their

activities towards the direction of achieving the organisation goal.

Similarly, with cost accounting systems it is possible for the management to made cost

accounting reports which guide the business to decide the sales price and profit margin according

to the actual cost of their units products (Nuhu, Baird and Bala Appuhamilage, 2017). These

systems help in making the reports which ultimately contributed towards the effective and

efficient performance of the complete operational process of the organisation.

TASK 2

Preparing income statement using absorption and marginal costing method

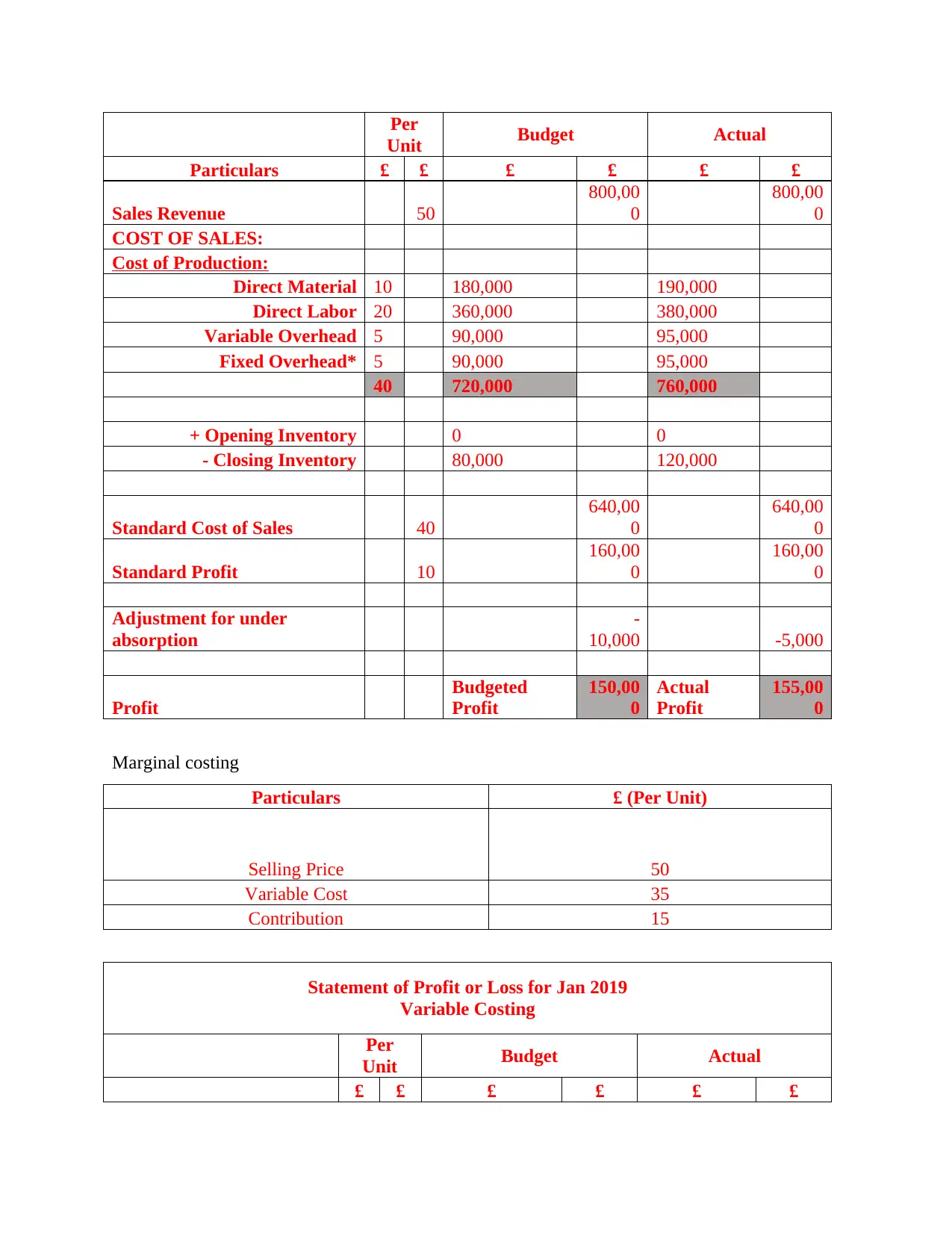

Statement of Profit or Loss for Jan 2019

Absorption Costing

products produced. This reports help the mangers to estimate the cost price of items with their

selling price so to ascertain the actual profit earned (Quattrone, 2016().

There are several benefits of the management accounting which help the company in

improving their overall efficiency and lead the organisation in achieving their goals and

missions.

Management accounting helps in measuring the actual performance with the estimated

budgets to eliminate the deviations.

By effective budgeting and planning function of the management accounting businesses

activities are managed better and effectively.

It helps to increase the overall efficiency of the business.

It helps to improve the relation between the management ad the employees and other

members of the organisation (Bennett and James, 2017).

This help management for making future plans based on the past results and experiences.

Through the management accounting effective communication can be take place between

the top and lower level of the organisation

Management accounting system and management accounting report is integrated with

organisation process in way that with the help of systems management accounting reports can be

made say with job costing system, job costing report can be made. And these reports help the

management in taking the corrective and effective decisions which help further in directing their

activities towards the direction of achieving the organisation goal.

Similarly, with cost accounting systems it is possible for the management to made cost

accounting reports which guide the business to decide the sales price and profit margin according

to the actual cost of their units products (Nuhu, Baird and Bala Appuhamilage, 2017). These

systems help in making the reports which ultimately contributed towards the effective and

efficient performance of the complete operational process of the organisation.

TASK 2

Preparing income statement using absorption and marginal costing method

Statement of Profit or Loss for Jan 2019

Absorption Costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Per

Unit Budget Actual

Particulars £ £ £ £ £ £

Sales Revenue 50

800,00

0

800,00

0

COST OF SALES:

Cost of Production:

Direct Material 10 180,000 190,000

Direct Labor 20 360,000 380,000

Variable Overhead 5 90,000 95,000

Fixed Overhead* 5 90,000 95,000

40 720,000 760,000

+ Opening Inventory 0 0

- Closing Inventory 80,000 120,000

Standard Cost of Sales 40

640,00

0

640,00

0

Standard Profit 10

160,00

0

160,00

0

Adjustment for under

absorption

-

10,000 -5,000

Profit

Budgeted

Profit

150,00

0

Actual

Profit

155,00

0

Marginal costing

Particulars £ (Per Unit)

Selling Price 50

Variable Cost 35

Contribution 15

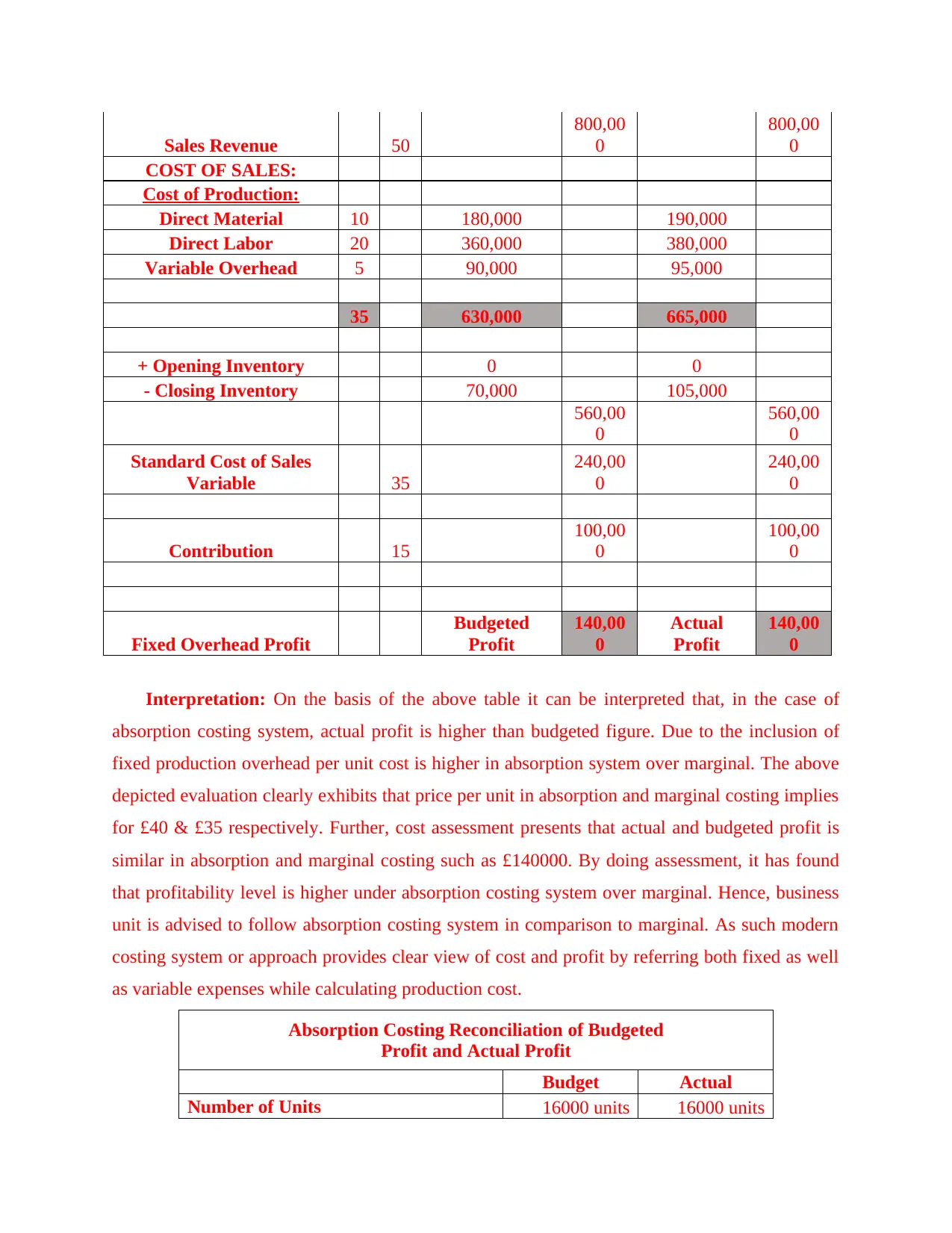

Statement of Profit or Loss for Jan 2019

Variable Costing

Per

Unit Budget Actual

£ £ £ £ £ £

Unit Budget Actual

Particulars £ £ £ £ £ £

Sales Revenue 50

800,00

0

800,00

0

COST OF SALES:

Cost of Production:

Direct Material 10 180,000 190,000

Direct Labor 20 360,000 380,000

Variable Overhead 5 90,000 95,000

Fixed Overhead* 5 90,000 95,000

40 720,000 760,000

+ Opening Inventory 0 0

- Closing Inventory 80,000 120,000

Standard Cost of Sales 40

640,00

0

640,00

0

Standard Profit 10

160,00

0

160,00

0

Adjustment for under

absorption

-

10,000 -5,000

Profit

Budgeted

Profit

150,00

0

Actual

Profit

155,00

0

Marginal costing

Particulars £ (Per Unit)

Selling Price 50

Variable Cost 35

Contribution 15

Statement of Profit or Loss for Jan 2019

Variable Costing

Per

Unit Budget Actual

£ £ £ £ £ £

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales Revenue 50

800,00

0

800,00

0

COST OF SALES:

Cost of Production:

Direct Material 10 180,000 190,000

Direct Labor 20 360,000 380,000

Variable Overhead 5 90,000 95,000

35 630,000 665,000

+ Opening Inventory 0 0

- Closing Inventory 70,000 105,000

560,00

0

560,00

0

Standard Cost of Sales

Variable 35

240,00

0

240,00

0

Contribution 15

100,00

0

100,00

0

Fixed Overhead Profit

Budgeted

Profit

140,00

0

Actual

Profit

140,00

0

Interpretation: On the basis of the above table it can be interpreted that, in the case of

absorption costing system, actual profit is higher than budgeted figure. Due to the inclusion of

fixed production overhead per unit cost is higher in absorption system over marginal. The above

depicted evaluation clearly exhibits that price per unit in absorption and marginal costing implies

for £40 & £35 respectively. Further, cost assessment presents that actual and budgeted profit is

similar in absorption and marginal costing such as £140000. By doing assessment, it has found

that profitability level is higher under absorption costing system over marginal. Hence, business

unit is advised to follow absorption costing system in comparison to marginal. As such modern

costing system or approach provides clear view of cost and profit by referring both fixed as well

as variable expenses while calculating production cost.

Absorption Costing Reconciliation of Budgeted

Profit and Actual Profit

Budget Actual

Number of Units 16000 units 16000 units

800,00

0

800,00

0

COST OF SALES:

Cost of Production:

Direct Material 10 180,000 190,000

Direct Labor 20 360,000 380,000

Variable Overhead 5 90,000 95,000

35 630,000 665,000

+ Opening Inventory 0 0

- Closing Inventory 70,000 105,000

560,00

0

560,00

0

Standard Cost of Sales

Variable 35

240,00

0

240,00

0

Contribution 15

100,00

0

100,00

0

Fixed Overhead Profit

Budgeted

Profit

140,00

0

Actual

Profit

140,00

0

Interpretation: On the basis of the above table it can be interpreted that, in the case of

absorption costing system, actual profit is higher than budgeted figure. Due to the inclusion of

fixed production overhead per unit cost is higher in absorption system over marginal. The above

depicted evaluation clearly exhibits that price per unit in absorption and marginal costing implies

for £40 & £35 respectively. Further, cost assessment presents that actual and budgeted profit is

similar in absorption and marginal costing such as £140000. By doing assessment, it has found

that profitability level is higher under absorption costing system over marginal. Hence, business

unit is advised to follow absorption costing system in comparison to marginal. As such modern

costing system or approach provides clear view of cost and profit by referring both fixed as well

as variable expenses while calculating production cost.

Absorption Costing Reconciliation of Budgeted

Profit and Actual Profit

Budget Actual

Number of Units 16000 units 16000 units

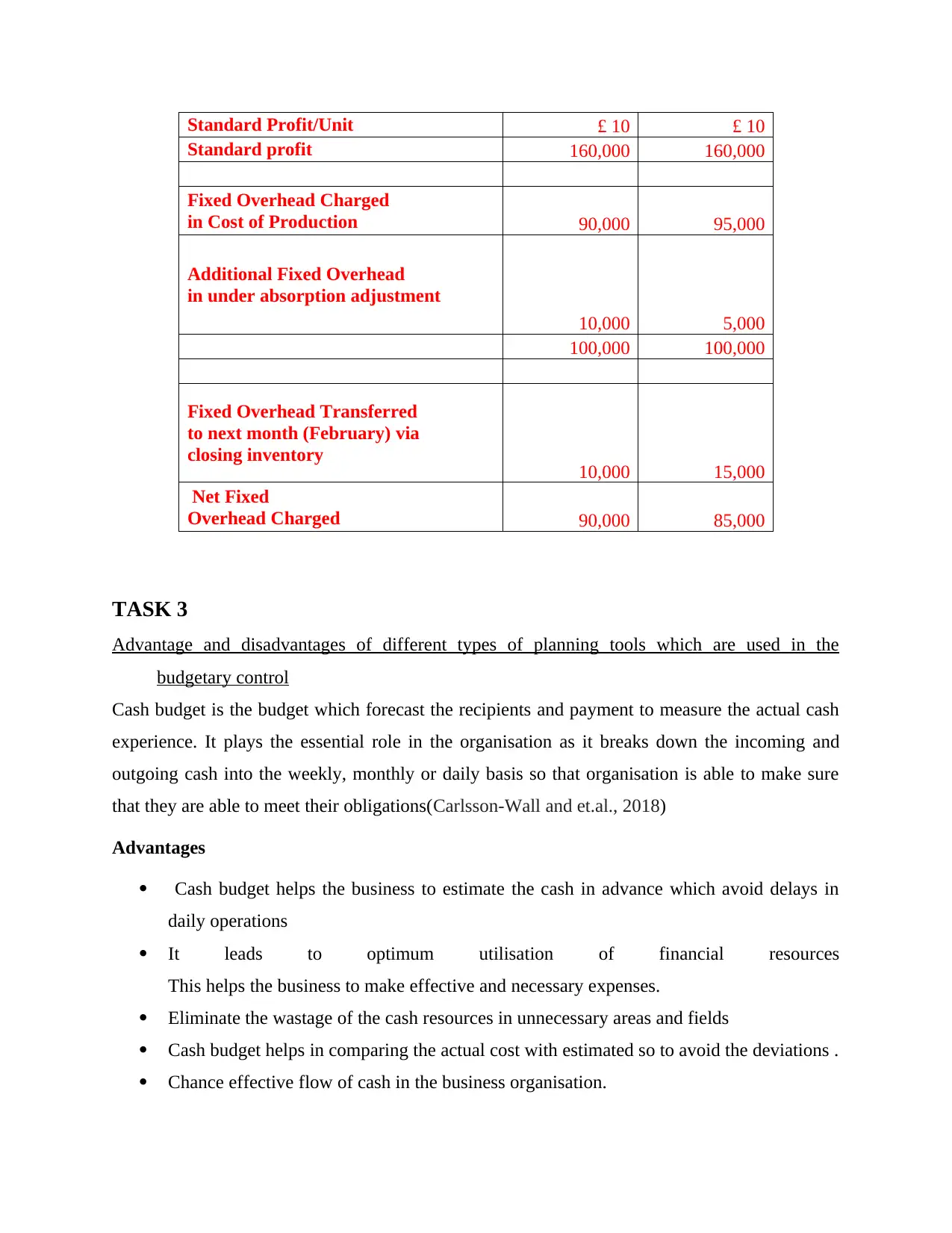

Standard Profit/Unit £ 10 £ 10

Standard profit 160,000 160,000

Fixed Overhead Charged

in Cost of Production 90,000 95,000

Additional Fixed Overhead

in under absorption adjustment

10,000 5,000

100,000 100,000

Fixed Overhead Transferred

to next month (February) via

closing inventory 10,000 15,000

Net Fixed

Overhead Charged 90,000 85,000

TASK 3

Advantage and disadvantages of different types of planning tools which are used in the

budgetary control

Cash budget is the budget which forecast the recipients and payment to measure the actual cash

experience. It plays the essential role in the organisation as it breaks down the incoming and

outgoing cash into the weekly, monthly or daily basis so that organisation is able to make sure

that they are able to meet their obligations(Carlsson-Wall and et.al., 2018)

Advantages

Cash budget helps the business to estimate the cash in advance which avoid delays in

daily operations

It leads to optimum utilisation of financial resources

This helps the business to make effective and necessary expenses.

Eliminate the wastage of the cash resources in unnecessary areas and fields

Cash budget helps in comparing the actual cost with estimated so to avoid the deviations .

Chance effective flow of cash in the business organisation.

Standard profit 160,000 160,000

Fixed Overhead Charged

in Cost of Production 90,000 95,000

Additional Fixed Overhead

in under absorption adjustment

10,000 5,000

100,000 100,000

Fixed Overhead Transferred

to next month (February) via

closing inventory 10,000 15,000

Net Fixed

Overhead Charged 90,000 85,000

TASK 3

Advantage and disadvantages of different types of planning tools which are used in the

budgetary control

Cash budget is the budget which forecast the recipients and payment to measure the actual cash

experience. It plays the essential role in the organisation as it breaks down the incoming and

outgoing cash into the weekly, monthly or daily basis so that organisation is able to make sure

that they are able to meet their obligations(Carlsson-Wall and et.al., 2018)

Advantages

Cash budget helps the business to estimate the cash in advance which avoid delays in

daily operations

It leads to optimum utilisation of financial resources

This helps the business to make effective and necessary expenses.

Eliminate the wastage of the cash resources in unnecessary areas and fields

Cash budget helps in comparing the actual cost with estimated so to avoid the deviations .

Chance effective flow of cash in the business organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantage

it requires specialised knowledge to maintain the cash budgets

budgets needs to monitor and observe regularly

Time consuming process(van Helden and Uddin, 2016)

Cash budgets are the most important budget and need specialised knowledge to maintain

this budget

It involves cost for maintaining and preparing the budget.

Operating budget is the budget which helps the business to plan their day to day operations so

that operational activities can run smoothly without any disruption. Operational budget helps in

tracking the actual expenses, estimating the future expenses so that business make sufficient

availability of the funds before the actual expense incurred.

Advantages

This budget helps in tracking the income and expenses related to the operation of the

business

It helps in allocating the money

It builds the budget flexibility that means changes can be made accordingly.

The budget keeps the information accurate by effective comparison.

Disadvantage

expensive and costly to prepare and install

It is time consuming

It limits the manger to the budget which might lead to avoidance of great opportunity

available.

Operational budgets contains the strategic rigidity

Zero base budget-

it requires specialised knowledge to maintain the cash budgets

budgets needs to monitor and observe regularly

Time consuming process(van Helden and Uddin, 2016)

Cash budgets are the most important budget and need specialised knowledge to maintain

this budget

It involves cost for maintaining and preparing the budget.

Operating budget is the budget which helps the business to plan their day to day operations so

that operational activities can run smoothly without any disruption. Operational budget helps in

tracking the actual expenses, estimating the future expenses so that business make sufficient

availability of the funds before the actual expense incurred.

Advantages

This budget helps in tracking the income and expenses related to the operation of the

business

It helps in allocating the money

It builds the budget flexibility that means changes can be made accordingly.

The budget keeps the information accurate by effective comparison.

Disadvantage

expensive and costly to prepare and install

It is time consuming

It limits the manger to the budget which might lead to avoidance of great opportunity

available.

Operational budgets contains the strategic rigidity

Zero base budget-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is the method of budgeting in which all the expense are justified for each new period. The

process of zero base budget starts from the zero base and every function in the organisation is

analysed for their needs and costs(Kaplan and Atkinson, 2015). This is the budget which is step

by step process with zero base and this have nothing to do with the past data or experiences. The

preparation of the budget is doe by scratching the zero base by examining each and every

expense and cost which is essential for the company to ascertain the accurate results.

Advantages

zero base budget provides the organisation a systematic way of evaluating the operations

of the company

It allows the management to allocate the resources on basis of the priority of

programmes.

It ensures with efficient examination of every function.

Through this budget the long range goals and plans can be linked with the annual budget,

The departmental head cannot justify the expense on the basis of past expenses or records

which prevents organisation in ascertaining the accurate budget(Quattrone, 2016).

Disadvantage

It is very time consuming process as organ' needs to start with zero base and they do not

have any base.

It is tedious to justify all the expenses and non justification may leads to rejection of the

business.

It has Lack of acceptance

Use of the different planning tools and their applications for preparing and forecasting the

budgets

Planning tools are some tools of budgetary control which focuses on controlling the budget by

comparing the actual budget with estimated budget so that deviations can be found out and

corrective measures can be taken to solve the deviations(Skouloudis, Malesios and

Dimitrakopoulos, 2019). Planning tools are the tools which convert the raw data into some useful

information which helps the organisation in ascertaining the best and effective information so tat

process of zero base budget starts from the zero base and every function in the organisation is

analysed for their needs and costs(Kaplan and Atkinson, 2015). This is the budget which is step

by step process with zero base and this have nothing to do with the past data or experiences. The

preparation of the budget is doe by scratching the zero base by examining each and every

expense and cost which is essential for the company to ascertain the accurate results.

Advantages

zero base budget provides the organisation a systematic way of evaluating the operations

of the company

It allows the management to allocate the resources on basis of the priority of

programmes.

It ensures with efficient examination of every function.

Through this budget the long range goals and plans can be linked with the annual budget,

The departmental head cannot justify the expense on the basis of past expenses or records

which prevents organisation in ascertaining the accurate budget(Quattrone, 2016).

Disadvantage

It is very time consuming process as organ' needs to start with zero base and they do not

have any base.

It is tedious to justify all the expenses and non justification may leads to rejection of the

business.

It has Lack of acceptance

Use of the different planning tools and their applications for preparing and forecasting the

budgets

Planning tools are some tools of budgetary control which focuses on controlling the budget by

comparing the actual budget with estimated budget so that deviations can be found out and

corrective measures can be taken to solve the deviations(Skouloudis, Malesios and

Dimitrakopoulos, 2019). Planning tools are the tools which convert the raw data into some useful

information which helps the organisation in ascertaining the best and effective information so tat

they can make decisions accordingly. The different types of planing tools used by the ABC Ltd

are ;

Zero base budgeting: it is also known as the ZBB. It is the process in which organisation needs

to evaluate every expenses' individuality and have to prepare the budget with zero base that is

they do not have nay base of past expense or budget. This is the technique which examine the

every expense ad costs which is essential for the company. Zero base budgeting is method in

which company needs to start with no base and all the expense are need to justified. This method

is used to control the costs of the organisation. In this method current year budget is prepared

from the scratch that is taking the base as zero.

Operating budgets are the budgets which records the planned operation of the business so that

actual operations can done in the direction of those budget to avoid any issue or problem which

may faced by the organisation while performing their operational activities(Boiral, 2016)

There are different types of operating budget which are classified as under the following:

Sale or revenue budget this budget focuses on the revenue that company is expecting to receive

in the future which helps them in ascertaining their financial performance(Hall, 2016 ).

Expense budget it anticipates the expenses of the organisation during a specified time period

and it also includes the upcoming expense so that sufficient availability of fund can arranges to

avoid the delay in operational activities of the business.

Project budget- It anticipates the difference between the sales or revenue and if the profit

percentage is small than company needs to take necessary steps to eliminate or control the

expense of the organisation.

Fixed and flexible budgets

Fixed budgets are those in which changes cannot be made according to the changes and

requirements of the organisation and situation(Drake, Roulstone and Thornock, 2016). The

budget need to be followed rigidity without making nay changes in it. These kinds of budget are

easier to follow but impracticable to accept. Whereas flexible budgets are those budgets which

are ;

Zero base budgeting: it is also known as the ZBB. It is the process in which organisation needs

to evaluate every expenses' individuality and have to prepare the budget with zero base that is

they do not have nay base of past expense or budget. This is the technique which examine the

every expense ad costs which is essential for the company. Zero base budgeting is method in

which company needs to start with no base and all the expense are need to justified. This method

is used to control the costs of the organisation. In this method current year budget is prepared

from the scratch that is taking the base as zero.

Operating budgets are the budgets which records the planned operation of the business so that

actual operations can done in the direction of those budget to avoid any issue or problem which

may faced by the organisation while performing their operational activities(Boiral, 2016)

There are different types of operating budget which are classified as under the following:

Sale or revenue budget this budget focuses on the revenue that company is expecting to receive

in the future which helps them in ascertaining their financial performance(Hall, 2016 ).

Expense budget it anticipates the expenses of the organisation during a specified time period

and it also includes the upcoming expense so that sufficient availability of fund can arranges to

avoid the delay in operational activities of the business.

Project budget- It anticipates the difference between the sales or revenue and if the profit

percentage is small than company needs to take necessary steps to eliminate or control the

expense of the organisation.

Fixed and flexible budgets

Fixed budgets are those in which changes cannot be made according to the changes and

requirements of the organisation and situation(Drake, Roulstone and Thornock, 2016). The

budget need to be followed rigidity without making nay changes in it. These kinds of budget are

easier to follow but impracticable to accept. Whereas flexible budgets are those budgets which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.