Management Accounting Report: Techniques, Analysis, and Application

VerifiedAdded on 2022/12/07

|20

|5186

|177

Report

AI Summary

This report provides a critical evaluation of management accounting integration and reporting, focusing on Eastern Engineering Co. Ltd. It explores the benefits of management accounting systems, their practical applications within the business, and the underlying principles. The report covers various techniques, including financial planning, ratio analysis, standard costing, and budgetary control, with an emphasis on marginal and absorption costing methods. It further calculates income statements under both costing methods for January and February, explaining the differences. The report also addresses how management accounting systems can help overcome financial issues, and discusses the advantages and disadvantages of planning tools, such as forward-looking nature, adaptability and the ability to maintain working capital.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Critical evaluation integration of management accounting reporting................................3

Benefits of management accounting systems......................................................................4

Application of management accounting within the business.............................................5

Principles of management accounting...................................................................................6

Different techniques and methods of management accounting reporting.......................6

Task 2...............................................................................................................................................9

Task 3.............................................................................................................................................11

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Critical evaluation integration of management accounting reporting................................3

Benefits of management accounting systems......................................................................4

Application of management accounting within the business.............................................5

Principles of management accounting...................................................................................6

Different techniques and methods of management accounting reporting.......................6

Task 2...............................................................................................................................................9

Task 3.............................................................................................................................................11

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................1

INTRODUCTION

Management accounting basically uses the financial statement for preparing the

report on the basis of which they managers can easily take decision. If a company

wants to make a plan and analyse the business performance than they have to adopt

this technique also. So, in this context, this report will critically evaluate the integration

of management accounting system and reporting in the Eastern Engineering Co. ltd.

The report further will evaluate the benefits of management accounting systems and

their application in the Eastern Engineering company. The report will also include the

principles of management accounting and the importance of integration of management

accounting within the business. The report will also cover the different techniques and

method of management accounting by using it the company can make decision in less

time. The report will further calculate the income statement under the absorption costing

and marginal costing for the month of January and February. The report will also state

the reason behind the difference between the absorption costing and marginal costing.

The report also defines how the application of management accounting systems help

them in overcoming the financial issues.

MAIN BODY

Critical evaluation integration of management accounting reporting

Management accounting helps the company in maintaining coordination among

the departments by integrating the task among each other. For example, in order to

prepare the budgets each department need to coordinate with each other so that actual

data can be collected. Eastern engineering company by using the management

accounting tools and techniques such as job costing, batch costing, process costing etc.

ascertain the cost between the process, batch and job. This will further help the

company in identifying the unit and department which causes loss to the business. With

the use of activity-based costing the managers of Eastern engineering company can

allocate the cost on the basis of the activity occur to produce products. With the help of

this the unprofitable and low performance activity are easily get identified as well as the

company can also remove it. By integrating the management accounting, managers can

help the company in planning the finances with the help of which they work for the

Management accounting basically uses the financial statement for preparing the

report on the basis of which they managers can easily take decision. If a company

wants to make a plan and analyse the business performance than they have to adopt

this technique also. So, in this context, this report will critically evaluate the integration

of management accounting system and reporting in the Eastern Engineering Co. ltd.

The report further will evaluate the benefits of management accounting systems and

their application in the Eastern Engineering company. The report will also include the

principles of management accounting and the importance of integration of management

accounting within the business. The report will also cover the different techniques and

method of management accounting by using it the company can make decision in less

time. The report will further calculate the income statement under the absorption costing

and marginal costing for the month of January and February. The report will also state

the reason behind the difference between the absorption costing and marginal costing.

The report also defines how the application of management accounting systems help

them in overcoming the financial issues.

MAIN BODY

Critical evaluation integration of management accounting reporting

Management accounting helps the company in maintaining coordination among

the departments by integrating the task among each other. For example, in order to

prepare the budgets each department need to coordinate with each other so that actual

data can be collected. Eastern engineering company by using the management

accounting tools and techniques such as job costing, batch costing, process costing etc.

ascertain the cost between the process, batch and job. This will further help the

company in identifying the unit and department which causes loss to the business. With

the use of activity-based costing the managers of Eastern engineering company can

allocate the cost on the basis of the activity occur to produce products. With the help of

this the unprofitable and low performance activity are easily get identified as well as the

company can also remove it. By integrating the management accounting, managers can

help the company in planning the finances with the help of which they work for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

growth of the business. By capital budgeting company can find out best sources of

funds such as equity, debt etc. as well as with the help of investment appraisal such as

NPV, IRR etc. the company can investment the funds in high return proposals (Pelz,

2019).

By using the budgetary control method, marginal costing method and standard

costing method of the management accounting the company can analyse the variance

between the actual cost and planned cost. After that the company can also adopt best

strategy which help them in removing the gaps if any arises in the actual and planned

budgets. The another step the company can do while integration of management

accounting systems is using technologies which removes the error of human and

increase the time of the processing of work. With the help of cash flow and fund flow

analysis the Eastern Engineering company can identify the sources from where the

cash is coming and where is going from the business. Not only that MA implementation

helps the company in creating cash budgets with the help of which they can maintain

minimum opening and closing cash balance. However, such integration may also bring

conflicts among the departments if the company unable to communicate properly with

them. So, it is important for the company that before implementing MA they must

minimize the communication gap if any and keep motivated their staffs (Pedroso and

Gomes, 2020).

Benefits of management accounting systems

Management Accounting systems helps the companies in such ways which indicate

that if company really wants to increase their performance and productivity than they

must go with MA system and implement MAS in the building. The benefits it provided to

the company involve:

By using the forecasting technique, the company can analyse and visualise the

past, present and future trends and identify the answers related to important

questions such as whether company should invest in equipment’s or not? etc.

Management Accounting systems also helps the company in making the decision

regarding whether to buy same products from the supplier and sell it in the

market or to make all the products in the organization only.

funds such as equity, debt etc. as well as with the help of investment appraisal such as

NPV, IRR etc. the company can investment the funds in high return proposals (Pelz,

2019).

By using the budgetary control method, marginal costing method and standard

costing method of the management accounting the company can analyse the variance

between the actual cost and planned cost. After that the company can also adopt best

strategy which help them in removing the gaps if any arises in the actual and planned

budgets. The another step the company can do while integration of management

accounting systems is using technologies which removes the error of human and

increase the time of the processing of work. With the help of cash flow and fund flow

analysis the Eastern Engineering company can identify the sources from where the

cash is coming and where is going from the business. Not only that MA implementation

helps the company in creating cash budgets with the help of which they can maintain

minimum opening and closing cash balance. However, such integration may also bring

conflicts among the departments if the company unable to communicate properly with

them. So, it is important for the company that before implementing MA they must

minimize the communication gap if any and keep motivated their staffs (Pedroso and

Gomes, 2020).

Benefits of management accounting systems

Management Accounting systems helps the companies in such ways which indicate

that if company really wants to increase their performance and productivity than they

must go with MA system and implement MAS in the building. The benefits it provided to

the company involve:

By using the forecasting technique, the company can analyse and visualise the

past, present and future trends and identify the answers related to important

questions such as whether company should invest in equipment’s or not? etc.

Management Accounting systems also helps the company in making the decision

regarding whether to buy same products from the supplier and sell it in the

market or to make all the products in the organization only.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It also helps the company in analysing the rate of return offer by the investment

proposals by using investment appraisal technique. With this the company can

analyse all the probability and expected returns and select the project with higher

NPV.

It helps in overall decision-making process of the company and identifying the

main area led to business problems by using the variance analysis tool (Solovida

and Latan, 2017).

The management accounting structure is flexible and their company can shape

MAS as per the requirements of the company. So, for Eastern Engineering

company the MA in the business so that they can produce high quality products

and services.

Application of management accounting within the business

Application of management accounting is useful for every situation from tracking

the productivity of the product and services to understanding the sales trend. By

applying the management accounting practices the Eastern Engineering Co. ltd. can

track their software construction and management services, colour printing services etc.

The application of management also helps the company in managing the performance

of the employees by collecting and evaluating data about the employees. With this the

company can identify the which services are more profitable to the company and which

of their product is causing loses to the business which need to be discontinue by the

company. As it always uses the data provided by the financial statement than it can be

say that it covers actual data and trends and with the help of which the business will

improve. With the application of management accounting systems, the work of the

company will decrease because it might remove human work which generally take more

time. It also helps in removing the human error which is obvious. But as this require lots

of research which might be wrong if the data is not as per the standard which need to

be consider by the company before its application. It also increases the cost of the

company which also need to consider by the Eastern company and need to make

arrangement of funds for the same (OTLEY, 2019).

proposals by using investment appraisal technique. With this the company can

analyse all the probability and expected returns and select the project with higher

NPV.

It helps in overall decision-making process of the company and identifying the

main area led to business problems by using the variance analysis tool (Solovida

and Latan, 2017).

The management accounting structure is flexible and their company can shape

MAS as per the requirements of the company. So, for Eastern Engineering

company the MA in the business so that they can produce high quality products

and services.

Application of management accounting within the business

Application of management accounting is useful for every situation from tracking

the productivity of the product and services to understanding the sales trend. By

applying the management accounting practices the Eastern Engineering Co. ltd. can

track their software construction and management services, colour printing services etc.

The application of management also helps the company in managing the performance

of the employees by collecting and evaluating data about the employees. With this the

company can identify the which services are more profitable to the company and which

of their product is causing loses to the business which need to be discontinue by the

company. As it always uses the data provided by the financial statement than it can be

say that it covers actual data and trends and with the help of which the business will

improve. With the application of management accounting systems, the work of the

company will decrease because it might remove human work which generally take more

time. It also helps in removing the human error which is obvious. But as this require lots

of research which might be wrong if the data is not as per the standard which need to

be consider by the company before its application. It also increases the cost of the

company which also need to consider by the Eastern company and need to make

arrangement of funds for the same (OTLEY, 2019).

Principles of management accounting

With the help of effective management accounting principles company can easily

improve their overall decision-making process. It helps the Eastern Engineering Co ltd.

in taking the long-term decisions and also help in analysing their financial statement.

The principles include:

Influence: Sound communication is one of the principles of MA which helps the

company in identifying the critical information regarding the business process

and it encourages integrated thought process.

Relevance: It is significant for the company that they must prepare budgets and

reports on the basis of relevant information and resources. And thus, MA

provides best and materialistic information to company for making decisions. It

includes past, present, future dependent, internal, external, financial and non-

financial information.

Value: MA help the company in linking the business process to its core business

model with the help of which they can adopt new opportunities, concentrate on

risk factors and minimize their expenses. For this the company can involve

situational analysis to review organization decision (Yoder and et.al., 2017).

Credibility: This provides the responsibility and scrutiny of looking out the whole

task to the authorized personnel. Management accounting experts with their

knowledge and commitments help the company in decision-making and growing

business to the next level.

Different techniques and methods of management accounting reporting

The management accounting reporting provide variety of techniques with the help of

which a company can make decision in short span of time. This includes:

Financial Planning: This is a technique which help in deciding the financial

activities of the company in advance. The company can determine their both

short-term and long-term objectives as well as they can also form the financial

policies. This is also helpful for developing the financial procedure of the

company.

With the help of effective management accounting principles company can easily

improve their overall decision-making process. It helps the Eastern Engineering Co ltd.

in taking the long-term decisions and also help in analysing their financial statement.

The principles include:

Influence: Sound communication is one of the principles of MA which helps the

company in identifying the critical information regarding the business process

and it encourages integrated thought process.

Relevance: It is significant for the company that they must prepare budgets and

reports on the basis of relevant information and resources. And thus, MA

provides best and materialistic information to company for making decisions. It

includes past, present, future dependent, internal, external, financial and non-

financial information.

Value: MA help the company in linking the business process to its core business

model with the help of which they can adopt new opportunities, concentrate on

risk factors and minimize their expenses. For this the company can involve

situational analysis to review organization decision (Yoder and et.al., 2017).

Credibility: This provides the responsibility and scrutiny of looking out the whole

task to the authorized personnel. Management accounting experts with their

knowledge and commitments help the company in decision-making and growing

business to the next level.

Different techniques and methods of management accounting reporting

The management accounting reporting provide variety of techniques with the help of

which a company can make decision in short span of time. This includes:

Financial Planning: This is a technique which help in deciding the financial

activities of the company in advance. The company can determine their both

short-term and long-term objectives as well as they can also form the financial

policies. This is also helpful for developing the financial procedure of the

company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of financial statement: Management accounting is also useful for

analysing the financial information by using the ratio analysis tools. Ratio

analysis helps the company in determining and analysing the financial and

operational performance. This is also used for forecasting which is generally

made by the company for determining future ability and earnings (Rachmawati

and et.al., 2019).

Standard costing: This technique of management accounting is used by the

company in order to know the difference between the actual and expected

expenses. Every company prepare budgets in which they can estimate the

expected income and expenses along with profits. And if the company actually

incur the expenses and earn the income then with the help of variance analysis,

they can identify the gaps if any. In case, if the analysis is favourable than

company have to further improve it and in case of unfavourable gap than

company have to adopt strategy with the help of which the gaps get easily

minimized.

Budgetary control: The company can use budgetary control tool for planning

and controlling the various activities of the company. Budget is always crucial for

the business because it works as a base for the next year actual. In order to

move the business in a desired direction the company have to use this

technique. It also helps the company in achieving the satisfied return on the

investment (Ammar, 2017).

Marginal costing: This is a technique of management accounting in which the

company can use break-even analysis tool and identify the margin of safety level

of the business production. Break-even analysis is helpful for identification of no

profit no loss sales unit of the business because here the contribution of the

business is equal to the fixed cost that the company incur. In order to reach at

margin of safety level the company need to do two thing first is they need to

reduce expenses and second, they have to increase their sales.

Fund flow statement: It is a technique used for the purpose of identifying the

changes between the financial position of the company between two dates. It

basically tells the business about the sources from where the funds are

analysing the financial information by using the ratio analysis tools. Ratio

analysis helps the company in determining and analysing the financial and

operational performance. This is also used for forecasting which is generally

made by the company for determining future ability and earnings (Rachmawati

and et.al., 2019).

Standard costing: This technique of management accounting is used by the

company in order to know the difference between the actual and expected

expenses. Every company prepare budgets in which they can estimate the

expected income and expenses along with profits. And if the company actually

incur the expenses and earn the income then with the help of variance analysis,

they can identify the gaps if any. In case, if the analysis is favourable than

company have to further improve it and in case of unfavourable gap than

company have to adopt strategy with the help of which the gaps get easily

minimized.

Budgetary control: The company can use budgetary control tool for planning

and controlling the various activities of the company. Budget is always crucial for

the business because it works as a base for the next year actual. In order to

move the business in a desired direction the company have to use this

technique. It also helps the company in achieving the satisfied return on the

investment (Ammar, 2017).

Marginal costing: This is a technique of management accounting in which the

company can use break-even analysis tool and identify the margin of safety level

of the business production. Break-even analysis is helpful for identification of no

profit no loss sales unit of the business because here the contribution of the

business is equal to the fixed cost that the company incur. In order to reach at

margin of safety level the company need to do two thing first is they need to

reduce expenses and second, they have to increase their sales.

Fund flow statement: It is a technique used for the purpose of identifying the

changes between the financial position of the company between two dates. It

basically tells the business about the sources from where the funds are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

generating and actually where it is used by the company in order to generate

higher returns. For financial analysis and control it is very helpful for the company

(Kasasbeh, 2018).

Cash flow statement: Along with the fund flow statement the cash flow

statement is also helpful for the business in identifying the cash inflow and cash

outflow. It is helpful for controlling and maintain the minimum cash balance in the

business. Cash flow statement show different position of the company as

compared as compared to the financial statement. It is because non-cash items

are not included in the cash flow statement. Cash inflow and outflow from

operating activity, financing activity and investing activity help the business is

making fast decision regarding sources of the cash generation and also cash

disbursement (Bisogno and Vaia, 2017).

The Benefits and Drawbacks of Planning tools

Advantages include:

1.) The planning tools used in general are forward-looking and progressive in nature,

focusing on future planning.

2.) Accounting reports are prepared for internal use by managers and do not need to

adhere to specific guidelines.

3.) Financial planning aids in determining the appropriate rate of return on projects

as well as the maintenance of working capital and cash flow balance (Hiebl and

Richter, 2018).

4.) The tools are adaptable, allowing managers to create reports when needed,

rather than only periodically or annually.

5.) The costing methods employed are effective in calculating overall costs from the

start of the process and providing a summary of all expenditures incurred in the

production of the product, which aids in the determination of sale prices.

higher returns. For financial analysis and control it is very helpful for the company

(Kasasbeh, 2018).

Cash flow statement: Along with the fund flow statement the cash flow

statement is also helpful for the business in identifying the cash inflow and cash

outflow. It is helpful for controlling and maintain the minimum cash balance in the

business. Cash flow statement show different position of the company as

compared as compared to the financial statement. It is because non-cash items

are not included in the cash flow statement. Cash inflow and outflow from

operating activity, financing activity and investing activity help the business is

making fast decision regarding sources of the cash generation and also cash

disbursement (Bisogno and Vaia, 2017).

The Benefits and Drawbacks of Planning tools

Advantages include:

1.) The planning tools used in general are forward-looking and progressive in nature,

focusing on future planning.

2.) Accounting reports are prepared for internal use by managers and do not need to

adhere to specific guidelines.

3.) Financial planning aids in determining the appropriate rate of return on projects

as well as the maintenance of working capital and cash flow balance (Hiebl and

Richter, 2018).

4.) The tools are adaptable, allowing managers to create reports when needed,

rather than only periodically or annually.

5.) The costing methods employed are effective in calculating overall costs from the

start of the process and providing a summary of all expenditures incurred in the

production of the product, which aids in the determination of sale prices.

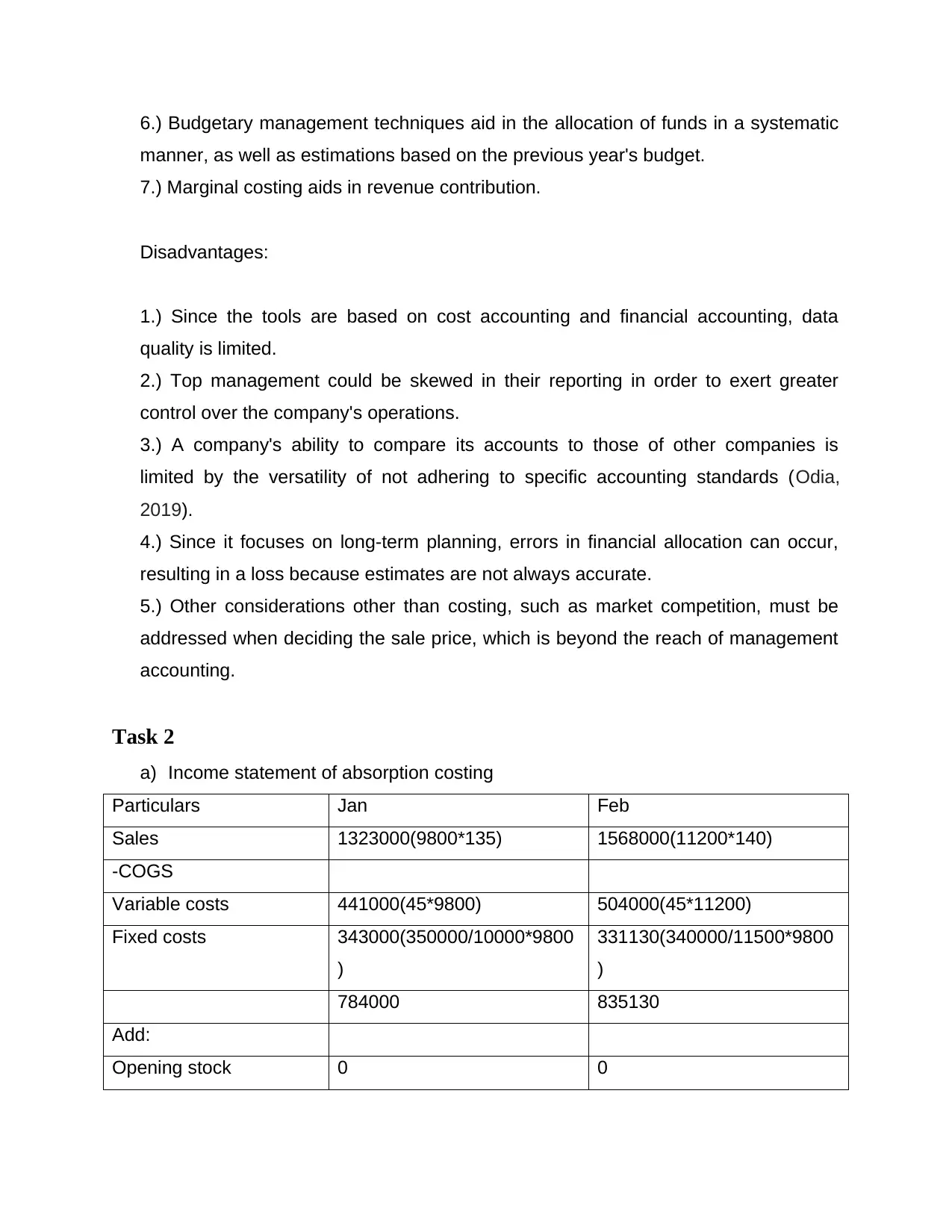

6.) Budgetary management techniques aid in the allocation of funds in a systematic

manner, as well as estimations based on the previous year's budget.

7.) Marginal costing aids in revenue contribution.

Disadvantages:

1.) Since the tools are based on cost accounting and financial accounting, data

quality is limited.

2.) Top management could be skewed in their reporting in order to exert greater

control over the company's operations.

3.) A company's ability to compare its accounts to those of other companies is

limited by the versatility of not adhering to specific accounting standards (Odia,

2019).

4.) Since it focuses on long-term planning, errors in financial allocation can occur,

resulting in a loss because estimates are not always accurate.

5.) Other considerations other than costing, such as market competition, must be

addressed when deciding the sale price, which is beyond the reach of management

accounting.

Task 2

a) Income statement of absorption costing

Particulars Jan Feb

Sales 1323000(9800*135) 1568000(11200*140)

-COGS

Variable costs 441000(45*9800) 504000(45*11200)

Fixed costs 343000(350000/10000*9800

)

331130(340000/11500*9800

)

784000 835130

Add:

Opening stock 0 0

manner, as well as estimations based on the previous year's budget.

7.) Marginal costing aids in revenue contribution.

Disadvantages:

1.) Since the tools are based on cost accounting and financial accounting, data

quality is limited.

2.) Top management could be skewed in their reporting in order to exert greater

control over the company's operations.

3.) A company's ability to compare its accounts to those of other companies is

limited by the versatility of not adhering to specific accounting standards (Odia,

2019).

4.) Since it focuses on long-term planning, errors in financial allocation can occur,

resulting in a loss because estimates are not always accurate.

5.) Other considerations other than costing, such as market competition, must be

addressed when deciding the sale price, which is beyond the reach of management

accounting.

Task 2

a) Income statement of absorption costing

Particulars Jan Feb

Sales 1323000(9800*135) 1568000(11200*140)

-COGS

Variable costs 441000(45*9800) 504000(45*11200)

Fixed costs 343000(350000/10000*9800

)

331130(340000/11500*9800

)

784000 835130

Add:

Opening stock 0 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

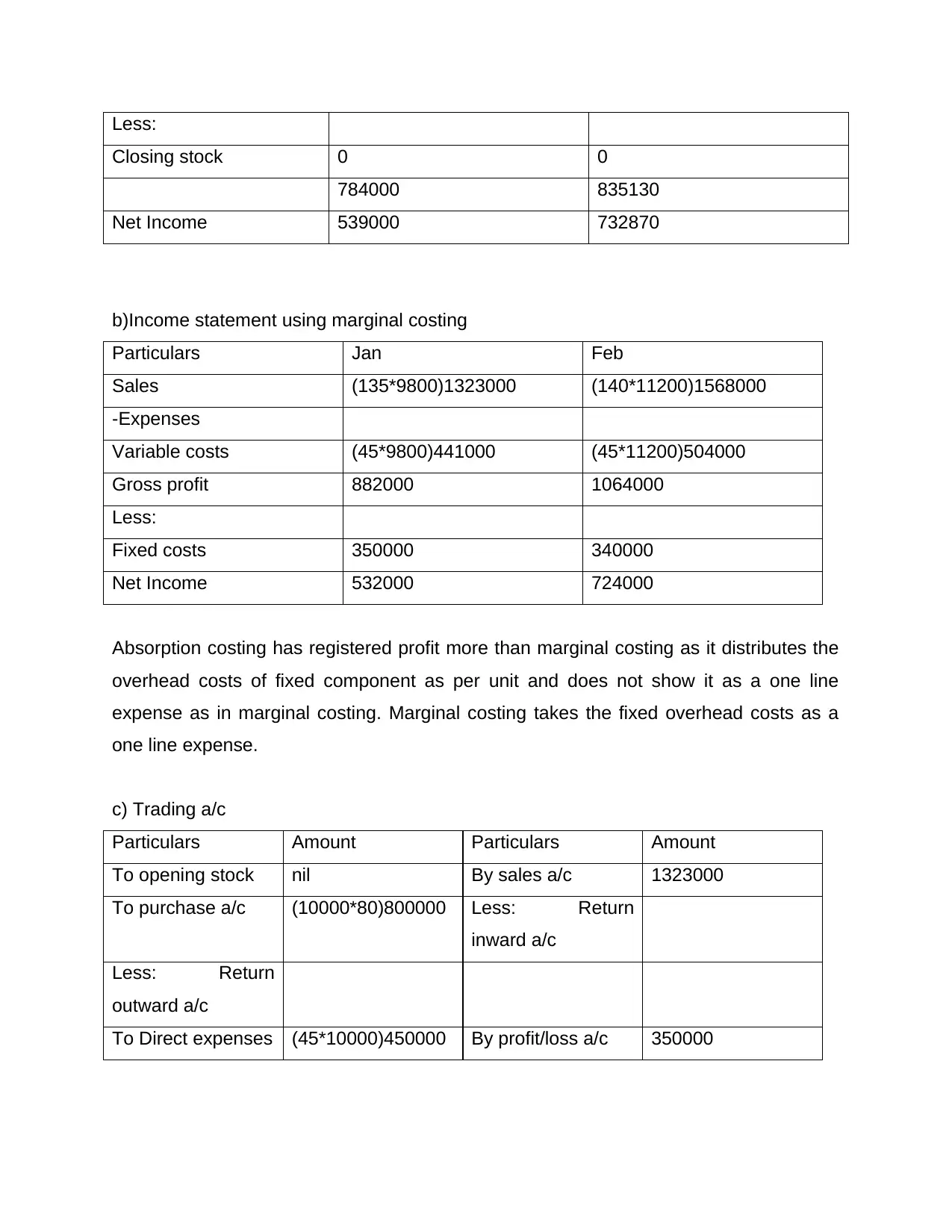

Less:

Closing stock 0 0

784000 835130

Net Income 539000 732870

b)Income statement using marginal costing

Particulars Jan Feb

Sales (135*9800)1323000 (140*11200)1568000

-Expenses

Variable costs (45*9800)441000 (45*11200)504000

Gross profit 882000 1064000

Less:

Fixed costs 350000 340000

Net Income 532000 724000

Absorption costing has registered profit more than marginal costing as it distributes the

overhead costs of fixed component as per unit and does not show it as a one line

expense as in marginal costing. Marginal costing takes the fixed overhead costs as a

one line expense.

c) Trading a/c

Particulars Amount Particulars Amount

To opening stock nil By sales a/c 1323000

To purchase a/c (10000*80)800000 Less: Return

inward a/c

Less: Return

outward a/c

To Direct expenses (45*10000)450000 By profit/loss a/c 350000

Closing stock 0 0

784000 835130

Net Income 539000 732870

b)Income statement using marginal costing

Particulars Jan Feb

Sales (135*9800)1323000 (140*11200)1568000

-Expenses

Variable costs (45*9800)441000 (45*11200)504000

Gross profit 882000 1064000

Less:

Fixed costs 350000 340000

Net Income 532000 724000

Absorption costing has registered profit more than marginal costing as it distributes the

overhead costs of fixed component as per unit and does not show it as a one line

expense as in marginal costing. Marginal costing takes the fixed overhead costs as a

one line expense.

c) Trading a/c

Particulars Amount Particulars Amount

To opening stock nil By sales a/c 1323000

To purchase a/c (10000*80)800000 Less: Return

inward a/c

Less: Return

outward a/c

To Direct expenses (45*10000)450000 By profit/loss a/c 350000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To profit and loss

a/c

350000

Trading account is statement prepared by business firm. The gross profit is reflected by

the business activities during the specific period. Speaking in other words, trading

account gives details of the total sales, purchases and direct expenses which have

occurred within given time period.

Task 3

Budgetary Planning

Budgetary management is the process of allocating money for operations based on

projections of previous years' capital allocation in different parts of the company.

Budgeting based on previous financials which suit the scheme, but it can also go wrong

due to changes in the organization's structure and market factors (Nuta and Nuta,

2018).

Budgetary monitoring begins with the planning of future budgets, and after that, the

management accountant, after meeting their objectives as expected, prepares a report

to determine the major output deviations. The preparation of a budget allows for the

minimization of significant variations in output and the matching of real performance to

expected performance. Budgets assist in reaching goals with greater ease. Inside the

company, a potential monitoring system may be created to control differences and

eliminate unnecessary activities. Each employee in the company understands what is

expected of them and the benchmarks by which their success will be measured.

The following are some of the benefits of budgetary control:

a) Having a plan: It lays out the strategies for achieving the organization's goals. It aids

in determining what needs to be accomplished early on, as well as checking on costs

and calculating funding sources.

a/c

350000

Trading account is statement prepared by business firm. The gross profit is reflected by

the business activities during the specific period. Speaking in other words, trading

account gives details of the total sales, purchases and direct expenses which have

occurred within given time period.

Task 3

Budgetary Planning

Budgetary management is the process of allocating money for operations based on

projections of previous years' capital allocation in different parts of the company.

Budgeting based on previous financials which suit the scheme, but it can also go wrong

due to changes in the organization's structure and market factors (Nuta and Nuta,

2018).

Budgetary monitoring begins with the planning of future budgets, and after that, the

management accountant, after meeting their objectives as expected, prepares a report

to determine the major output deviations. The preparation of a budget allows for the

minimization of significant variations in output and the matching of real performance to

expected performance. Budgets assist in reaching goals with greater ease. Inside the

company, a potential monitoring system may be created to control differences and

eliminate unnecessary activities. Each employee in the company understands what is

expected of them and the benchmarks by which their success will be measured.

The following are some of the benefits of budgetary control:

a) Having a plan: It lays out the strategies for achieving the organization's goals. It aids

in determining what needs to be accomplished early on, as well as checking on costs

and calculating funding sources.

b) Coordination: It focuses on coordinating with other departments or divisions of a

company. The committee establishes departmental roles and obligations and

communicates with them.

c) Variance analysis: It can be used to determine which departments adhered to budget

limits and which departments violated them. This makes it easier to determine which

departments have done well and which departments need additional attention.

d)Measures results: By offering comparative methods, it aids in the measurement of the

performance of different departments. It identifies the factors that cause the budget

standards to deviate.

e)Cost management: Planning and budgeting help control expenses that could

otherwise go unnoticed if not done with a budget in mind. Both departments have been

given orders to keep expenditures within the budgeted limits.

f)Benefit maximisation: It seeks to increase the value of an organization's capital while

reducing costs. The output of all divisions is monitored, and appropriate measures are

taken to improve efficiency.

Budgetary Control's Drawbacks

The following are the drawbacks:

Project inaccuracies: Budgets are framed for potential events that necessitate

estimates. It's also possible that the forecasts would be incorrect due to changing

market conditions. The criteria for different divisions may be higher than those set (Nuta

and Nuta, 2018).

Expensive process: Creating a budget is costly since each division must be taken into

account, as well as different categories that must be assessed. It costs a lot of money to

do analysis and forecasting.

It might be necessary to revise the budget from time to time, depending on the

organization's changing circumstances. As a result, it necessitates daily attention.

company. The committee establishes departmental roles and obligations and

communicates with them.

c) Variance analysis: It can be used to determine which departments adhered to budget

limits and which departments violated them. This makes it easier to determine which

departments have done well and which departments need additional attention.

d)Measures results: By offering comparative methods, it aids in the measurement of the

performance of different departments. It identifies the factors that cause the budget

standards to deviate.

e)Cost management: Planning and budgeting help control expenses that could

otherwise go unnoticed if not done with a budget in mind. Both departments have been

given orders to keep expenditures within the budgeted limits.

f)Benefit maximisation: It seeks to increase the value of an organization's capital while

reducing costs. The output of all divisions is monitored, and appropriate measures are

taken to improve efficiency.

Budgetary Control's Drawbacks

The following are the drawbacks:

Project inaccuracies: Budgets are framed for potential events that necessitate

estimates. It's also possible that the forecasts would be incorrect due to changing

market conditions. The criteria for different divisions may be higher than those set (Nuta

and Nuta, 2018).

Expensive process: Creating a budget is costly since each division must be taken into

account, as well as different categories that must be assessed. It costs a lot of money to

do analysis and forecasting.

It might be necessary to revise the budget from time to time, depending on the

organization's changing circumstances. As a result, it necessitates daily attention.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.