Management Accounting Report: Systems, Methods, and Planning Tools

VerifiedAdded on 2023/01/16

|16

|4368

|81

Report

AI Summary

This comprehensive report delves into the realm of management accounting, providing a detailed analysis of its systems, methods, and planning tools. It begins by outlining the fundamental differences between management accounting and financial accounting, followed by an exploration of key concepts such as cost accounting systems, inventory management, and job costing. The report then examines various methods used in management accounting reporting, including budget reports and cost managerial reports, emphasizing the importance of relevant and accurate information for users. Additionally, the report evaluates the integration of management accounting systems and reports within the operational processes of Excite Entertainment Ltd. The report further explores planning tools and financial problem-solving techniques, offering a complete overview of management accounting principles and their practical applications.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SCENARIO 1...................................................................................................................................1

Section A – Understanding Management Accounting Systems..................................................1

a) Differences between Management & Financial accounting. ........................................1

b) Cost Accounting Systems..............................................................................................2

c) Inventory management systems ....................................................................................3

d) Job Costing Systems .....................................................................................................4

e) Benefits of Management Accounting Systems .............................................................4

Section B : Methods used in management accounting reporting.................................................6

a) Different management accounting reports....................................................................6

b) Information made available to the users should be relevant, accurate and reliable to the

user.....................................................................................................................................8

c) Evaluating management accounting systems and reports to be integrated in Excite

Entertainment Ltd operational process. ............................................................................8

SCENARIO 2...................................................................................................................................9

Comparison of profit or loss under different cost accounting techniques. .................................9

SCENARIO 3.................................................................................................................................11

Part A ........................................................................................................................................11

Comparing and contrasting planning tools used in management accounting. ................11

Part B ........................................................................................................................................12

Comparing the ways in which financial problems can be dealt and can be prevented. . 12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

SCENARIO 1...................................................................................................................................1

Section A – Understanding Management Accounting Systems..................................................1

a) Differences between Management & Financial accounting. ........................................1

b) Cost Accounting Systems..............................................................................................2

c) Inventory management systems ....................................................................................3

d) Job Costing Systems .....................................................................................................4

e) Benefits of Management Accounting Systems .............................................................4

Section B : Methods used in management accounting reporting.................................................6

a) Different management accounting reports....................................................................6

b) Information made available to the users should be relevant, accurate and reliable to the

user.....................................................................................................................................8

c) Evaluating management accounting systems and reports to be integrated in Excite

Entertainment Ltd operational process. ............................................................................8

SCENARIO 2...................................................................................................................................9

Comparison of profit or loss under different cost accounting techniques. .................................9

SCENARIO 3.................................................................................................................................11

Part A ........................................................................................................................................11

Comparing and contrasting planning tools used in management accounting. ................11

Part B ........................................................................................................................................12

Comparing the ways in which financial problems can be dealt and can be prevented. . 12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Accounting refers to the process of recording the financial of the business. Accounting

process deals with making summary, analysis and reporting the transactions to the regulators,

oversight agencies and the tax authorities. Financial statements prepared in the accounting are

the brief summary of the financial transactions carried by the organization represent the

operation of business and its position. There are different types of accounting that has been used

for different accounting purposes within organization. Financial accounting (FA) and

management accounting(MA) are the two accounting that are mostly in practice and is used by

most of the organizations. Present report will reveal about the management accounting. It will

include the difference between MA & FA, other accounting systems will also be explained. It

will provide knowledge about the different methods use in the management accounting and

reporting. It will also involve the understanding about the planning tools use in management

accounting for ensuring financial performance and stability. Different management accounting

with the use of numericals will also be explained in the present report. Project will be providing

detailed information and understanding about the management accounting.

SCENARIO 1

Section A – Understanding Management Accounting Systems

a) Differences between Management & Financial accounting.

Management accounting

The accounting is also called managerial accounting. It is an accounting used by the

managers for helping the management of organisation in formulating the policies and

procedures, forecasting, in planning & controlling routine business operations carried out by the

organisation(Cokins and Dybvig, 2018). Management accounting captures both qualitative and

quantitative information. Management accounting is not limited over providing the costs or

financial informations only. It is also used in extracting the material and relevant informations

from cost and financial accounting for setting goals, budgeting, decision making and like

activities.

Financial accounting

1

Accounting refers to the process of recording the financial of the business. Accounting

process deals with making summary, analysis and reporting the transactions to the regulators,

oversight agencies and the tax authorities. Financial statements prepared in the accounting are

the brief summary of the financial transactions carried by the organization represent the

operation of business and its position. There are different types of accounting that has been used

for different accounting purposes within organization. Financial accounting (FA) and

management accounting(MA) are the two accounting that are mostly in practice and is used by

most of the organizations. Present report will reveal about the management accounting. It will

include the difference between MA & FA, other accounting systems will also be explained. It

will provide knowledge about the different methods use in the management accounting and

reporting. It will also involve the understanding about the planning tools use in management

accounting for ensuring financial performance and stability. Different management accounting

with the use of numericals will also be explained in the present report. Project will be providing

detailed information and understanding about the management accounting.

SCENARIO 1

Section A – Understanding Management Accounting Systems

a) Differences between Management & Financial accounting.

Management accounting

The accounting is also called managerial accounting. It is an accounting used by the

managers for helping the management of organisation in formulating the policies and

procedures, forecasting, in planning & controlling routine business operations carried out by the

organisation(Cokins and Dybvig, 2018). Management accounting captures both qualitative and

quantitative information. Management accounting is not limited over providing the costs or

financial informations only. It is also used in extracting the material and relevant informations

from cost and financial accounting for setting goals, budgeting, decision making and like

activities.

Financial accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The accounting system deals with preparation of the financial statements for outside

parties like shareholders, creditors, suppliers, investors etc. It is purest accounting form having

proper record of every transaction and reporting the financial data for providing the material and

relevant information for users. It is based over various assumptions, conventions, principles like

materiality, going concern accrual, consistency etc.

Key differences between the accounting methods.

MA keeps record and reports about both financial & non financial informations of

enterprise. FA deals only with keeping track records of all financial information related

to an entity.

Financial accounting information is used by both internal management as well as

external parties, where the management accounting information is only relevant for

internal management of company.

Management accounting is for internal use of enterprise therefore very confidential,

where financial accounting is prepared for public use.

Management accounting prepared reports considering monetary as well as non monetary

information like number of staff, raw material consumption and sale etc. On the other

hand financial accounting deals only with monetary information in its reports.

Management accounting is focused over providing information for helping the

management in performance evaluation and decision making for future. Financial

accounting is focused over providing information to the users about functioning of

company.

Financial accounting is done over specific periods where management accounting as per

the requirement of management.

Financial reports are prepared after the transactions or events are occurred where the

management accounting is done at both times prior for preparing budgets and after the

production to analyse the performance and variations.

b) Cost Accounting Systems

Cost accounting deals with examining the cost structure followed in business. This is

done by collecting the information of costs which are incurred by activities and operations of

2

parties like shareholders, creditors, suppliers, investors etc. It is purest accounting form having

proper record of every transaction and reporting the financial data for providing the material and

relevant information for users. It is based over various assumptions, conventions, principles like

materiality, going concern accrual, consistency etc.

Key differences between the accounting methods.

MA keeps record and reports about both financial & non financial informations of

enterprise. FA deals only with keeping track records of all financial information related

to an entity.

Financial accounting information is used by both internal management as well as

external parties, where the management accounting information is only relevant for

internal management of company.

Management accounting is for internal use of enterprise therefore very confidential,

where financial accounting is prepared for public use.

Management accounting prepared reports considering monetary as well as non monetary

information like number of staff, raw material consumption and sale etc. On the other

hand financial accounting deals only with monetary information in its reports.

Management accounting is focused over providing information for helping the

management in performance evaluation and decision making for future. Financial

accounting is focused over providing information to the users about functioning of

company.

Financial accounting is done over specific periods where management accounting as per

the requirement of management.

Financial reports are prepared after the transactions or events are occurred where the

management accounting is done at both times prior for preparing budgets and after the

production to analyse the performance and variations.

b) Cost Accounting Systems

Cost accounting deals with examining the cost structure followed in business. This is

done by collecting the information of costs which are incurred by activities and operations of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company, to assign the selected over products & services. This also evaluates the efficiency of

cost operations it is focused mainly over identifying the areas where companies could earn or

lose money. This helps them in effective decision making for generation of future profits. Cost

accounting is important for the business enterprise in proper allocation of its cost and resources

in the activities of companies. It involves preparation of budgets for the different operations of

entity and comparing the actual output for measuring the variances so that the corrective

measures can be taken by company. It involves different costing techniques like standard

costing, direct costing, marginal costing and absorption costing.

Direct Costing

Direct costing means specialized kind of the cost analysis which uses the variable costs

for making the decisions(Cokins and Dybvig, 2018). The costing do not consider the fixed costs

as they are assumed as associated with period in which it is incurred. Direct costing is used

mainly for the short term decision making. It is an analysis of the incremental costs. It is used

mainly as an analysis tool. Direct costing do not involve allocating overheads that are not

productive or irrelevant for the enterprise in decision making.

Standard Costing

Standard costing can be known as practice for substituting expected costs for actual costs

in accounting records. Difference between the actual and budgeted are shown by recording the

variances. The approach can be referred as simplified alternative for cost cost layering system,

like LIFO & FIFO where historical cost information are maintained. Standard costing includes

creation of expected costs for the defined activities in an organisation. Standard costing is used

as it provides results within short period of time.

c) Inventory management systems

Inventory management is combination of processes, technology and the procedures

which are used to oversee maintenance and monitoring of the products, these products could be

assets, supplies , raw materials or finished products. Inventory management is used for tracking

the movements in products in the processes. The management systems is used for checking rawa

3

cost operations it is focused mainly over identifying the areas where companies could earn or

lose money. This helps them in effective decision making for generation of future profits. Cost

accounting is important for the business enterprise in proper allocation of its cost and resources

in the activities of companies. It involves preparation of budgets for the different operations of

entity and comparing the actual output for measuring the variances so that the corrective

measures can be taken by company. It involves different costing techniques like standard

costing, direct costing, marginal costing and absorption costing.

Direct Costing

Direct costing means specialized kind of the cost analysis which uses the variable costs

for making the decisions(Cokins and Dybvig, 2018). The costing do not consider the fixed costs

as they are assumed as associated with period in which it is incurred. Direct costing is used

mainly for the short term decision making. It is an analysis of the incremental costs. It is used

mainly as an analysis tool. Direct costing do not involve allocating overheads that are not

productive or irrelevant for the enterprise in decision making.

Standard Costing

Standard costing can be known as practice for substituting expected costs for actual costs

in accounting records. Difference between the actual and budgeted are shown by recording the

variances. The approach can be referred as simplified alternative for cost cost layering system,

like LIFO & FIFO where historical cost information are maintained. Standard costing includes

creation of expected costs for the defined activities in an organisation. Standard costing is used

as it provides results within short period of time.

c) Inventory management systems

Inventory management is combination of processes, technology and the procedures

which are used to oversee maintenance and monitoring of the products, these products could be

assets, supplies , raw materials or finished products. Inventory management is used for tracking

the movements in products in the processes. The management systems is used for checking rawa

3

materials & finished goods quantities, so that entities can produce the goods accordingly. It is

also defined as process of storing, ordering and of using the inventory of company. Companies

having complex manufacturing process and supply chains it is difficult to balance risks related to

inventory gluts & shortages. For achieving these balance, entities have come up with two of the

major inventory management methods that are materials requirement planning and just in time. It

is essential for the businesses to have an effective management of inventory. Firms should have

inventory management software that keeps record of every movement of goods within or outside

of organisation. This will help the management in making informed business decisions.

FIFO – The inventory management where the inventory purchased at first will be sold at first by

the manufacturing units.

LIFO – To put value over the inventory the method deals with selling at first the inventory which

is purchased at last.

AVCO – The method deals with computing cost by dividing the total costs with number of units.

d) Job Costing Systems

Job costing refers to the costing method which is applied by industries for measuring

production in completed jobs(Bromwich and Scapens, 2016). In job costing costs are compiled

for job or the work order. Production is made on the orders of customers and not for stock. Job

costing can be defined as method for recording cost of manufacturing job, instead of process.

Using the job costing system managers can keep record of costs related to every job, and to

maintain the data relevant for operations of business. IT is an accounting methodology used for

tracking the cost of creating product. Certain projects like construction, requires performance of

different operations, the methodology is used by accountants for tracing the expenses of every

job. Job costing provides space for the inclusion of costs of direct materials, direct labour & the

overhead. Cost of jobs stays in work in progress till the duration of job. Job is completed, they

are transferred toi the accounts of finished goods.

4

also defined as process of storing, ordering and of using the inventory of company. Companies

having complex manufacturing process and supply chains it is difficult to balance risks related to

inventory gluts & shortages. For achieving these balance, entities have come up with two of the

major inventory management methods that are materials requirement planning and just in time. It

is essential for the businesses to have an effective management of inventory. Firms should have

inventory management software that keeps record of every movement of goods within or outside

of organisation. This will help the management in making informed business decisions.

FIFO – The inventory management where the inventory purchased at first will be sold at first by

the manufacturing units.

LIFO – To put value over the inventory the method deals with selling at first the inventory which

is purchased at last.

AVCO – The method deals with computing cost by dividing the total costs with number of units.

d) Job Costing Systems

Job costing refers to the costing method which is applied by industries for measuring

production in completed jobs(Bromwich and Scapens, 2016). In job costing costs are compiled

for job or the work order. Production is made on the orders of customers and not for stock. Job

costing can be defined as method for recording cost of manufacturing job, instead of process.

Using the job costing system managers can keep record of costs related to every job, and to

maintain the data relevant for operations of business. IT is an accounting methodology used for

tracking the cost of creating product. Certain projects like construction, requires performance of

different operations, the methodology is used by accountants for tracing the expenses of every

job. Job costing provides space for the inclusion of costs of direct materials, direct labour & the

overhead. Cost of jobs stays in work in progress till the duration of job. Job is completed, they

are transferred toi the accounts of finished goods.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

e) Benefits of Management Accounting Systems

Cost Accounting System

Advantages & Disadvantages of Costs accounting

Advantages

Improvised and new production methods are followed in the cost accounting systems

which helps in reducing the costs.

It helps the enterprise in identifying the reasons of increase or decrease in profits. It

helps in taking remedial actions for maintaining and improving the profitability of

company.

The cost information also helps the enterprise in making their buy or sell decision. It helps in controlling the costs of operation within the business.

Disadvantages

Decision are taken on past information for the future activities, as costs are appreciated

every year.

Costs are ascertained on the basis of full capacity utilization. Costs may vary with the

capacity.

Inventory Management System

Advantages and disadvantages of Inventory management system.

Advantages

Inventory management systems helps in keeping record of every movement of goods

within organisation.

This helps in making accurate inventory orders.

It helps company in maintaining centralized record for every asset & item in control of

organisation(Modugno and Di Carlo, 2019).

Efficiency in inventory management systems raises the operational performance leading

to more productiveness. Good inventory management system helps in saving time and money for company.

Disadvantages

The cost of inventory management is high and this increases the costs of company.

5

Cost Accounting System

Advantages & Disadvantages of Costs accounting

Advantages

Improvised and new production methods are followed in the cost accounting systems

which helps in reducing the costs.

It helps the enterprise in identifying the reasons of increase or decrease in profits. It

helps in taking remedial actions for maintaining and improving the profitability of

company.

The cost information also helps the enterprise in making their buy or sell decision. It helps in controlling the costs of operation within the business.

Disadvantages

Decision are taken on past information for the future activities, as costs are appreciated

every year.

Costs are ascertained on the basis of full capacity utilization. Costs may vary with the

capacity.

Inventory Management System

Advantages and disadvantages of Inventory management system.

Advantages

Inventory management systems helps in keeping record of every movement of goods

within organisation.

This helps in making accurate inventory orders.

It helps company in maintaining centralized record for every asset & item in control of

organisation(Modugno and Di Carlo, 2019).

Efficiency in inventory management systems raises the operational performance leading

to more productiveness. Good inventory management system helps in saving time and money for company.

Disadvantages

The cost of inventory management is high and this increases the costs of company.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ineffective inventory management may lay gap between the production inventory

requirements.

Ineffective management may cause the company in increased carrying cost of company.

Job Costing System

Advantages and Disadvantages of Job Costing system.

Advantages

Costs could be ascertained over ant stage of job completion which helps in controlling

the costs by taking corrective measures.

Profits and expenses of every job could be identified separately(Marota and et.al., 2017).

On job completion the cost elements , selling, profits, prices could be compared by

company with future estimated to control the costs, so that profits could be maximized. Estimates could be made by the manager over the past records. Defectives and spoilage

arising from jobs could be identified easily, therefore costs could be controlled.

Disadvantages

Jobs have no standardisation in job costing, therefore closes supervision is required.

Costs cannot be controlled as steps of control could be taken after the expenses have been

incurred in job costing.

Ascertaining accurate costs informations are not obtained as large number of jobs are

executed in the job costing.

Section B : Methods used in management accounting reporting

a) Different management accounting reports

Report is the process of presenting the business functions to check the profitability of the

business. These reports helps the management in analysing the effectiveness level from several

activities.

There are various types of management accounting reports that could be prepared by Excite

Entertainment ltd.

Budget Reports

6

requirements.

Ineffective management may cause the company in increased carrying cost of company.

Job Costing System

Advantages and Disadvantages of Job Costing system.

Advantages

Costs could be ascertained over ant stage of job completion which helps in controlling

the costs by taking corrective measures.

Profits and expenses of every job could be identified separately(Marota and et.al., 2017).

On job completion the cost elements , selling, profits, prices could be compared by

company with future estimated to control the costs, so that profits could be maximized. Estimates could be made by the manager over the past records. Defectives and spoilage

arising from jobs could be identified easily, therefore costs could be controlled.

Disadvantages

Jobs have no standardisation in job costing, therefore closes supervision is required.

Costs cannot be controlled as steps of control could be taken after the expenses have been

incurred in job costing.

Ascertaining accurate costs informations are not obtained as large number of jobs are

executed in the job costing.

Section B : Methods used in management accounting reporting

a) Different management accounting reports

Report is the process of presenting the business functions to check the profitability of the

business. These reports helps the management in analysing the effectiveness level from several

activities.

There are various types of management accounting reports that could be prepared by Excite

Entertainment ltd.

Budget Reports

6

These management accounting reports are prepared in measuring the performance of

company and it may generated for departments, specific activities or for the business(McInnis,

2018). Every company prepared budget for understanding the business scheme. Budget refers to

an estimate about the costs and revenues. It is made on the basis of previous estimates, assessing

previous experiences. Objective of company is to control the cost and achieve its goals and

objectives. Budget reports guides the managers in proper allocation of the resources, cutting

costs and using the resources in the best possible manner. Budgets are prepared by every

business for controlling the costs and achieving the desired targets with available resources.

Cost Managerial Reports

Management accounting is used for computing costs of the articles which are

manufactured. It takes into account labour, overhead, material costs and all the other costs. The

reports of cost management offers summary of these informations. Report provides managers

capacity of realizing costs prices of the items against their selling prices. Margins of profits are

monitors and estimated by these reports as it provides more clear pictures of costs of

procurement or production of the articles. Labour costs per hour, inventory waste and the

overheads cost are part of the cost managerial accounting report. It provides the management

with exact understanding related to all the expenses being incurred, for better resource

optimisation.

Performance Reports

Companies prepare performance reports for reviewing performance of company as whole

for every employee and for whole enterprise. Performance reports for different departments are

also generated by some organisations(Cristea, 2017). These reports are used by the managers in

making important strategic decisions for the future performance of organisation. Individuals are

awarded for the commitments to organisation and under-performers are dealt according using

these reports. The reports provide for the performance in carrying out given activity or business.

The performance of the company is analysed using theses reports. The areas where the

improvement are required may be made using these reports.

7

company and it may generated for departments, specific activities or for the business(McInnis,

2018). Every company prepared budget for understanding the business scheme. Budget refers to

an estimate about the costs and revenues. It is made on the basis of previous estimates, assessing

previous experiences. Objective of company is to control the cost and achieve its goals and

objectives. Budget reports guides the managers in proper allocation of the resources, cutting

costs and using the resources in the best possible manner. Budgets are prepared by every

business for controlling the costs and achieving the desired targets with available resources.

Cost Managerial Reports

Management accounting is used for computing costs of the articles which are

manufactured. It takes into account labour, overhead, material costs and all the other costs. The

reports of cost management offers summary of these informations. Report provides managers

capacity of realizing costs prices of the items against their selling prices. Margins of profits are

monitors and estimated by these reports as it provides more clear pictures of costs of

procurement or production of the articles. Labour costs per hour, inventory waste and the

overheads cost are part of the cost managerial accounting report. It provides the management

with exact understanding related to all the expenses being incurred, for better resource

optimisation.

Performance Reports

Companies prepare performance reports for reviewing performance of company as whole

for every employee and for whole enterprise. Performance reports for different departments are

also generated by some organisations(Cristea, 2017). These reports are used by the managers in

making important strategic decisions for the future performance of organisation. Individuals are

awarded for the commitments to organisation and under-performers are dealt according using

these reports. The reports provide for the performance in carrying out given activity or business.

The performance of the company is analysed using theses reports. The areas where the

improvement are required may be made using these reports.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Information made available to the users should be relevant, accurate and reliable to the

user.

The management accounting information is used for making the business decisions. The

information provided should be accurate, relevant and reliable. Management makes estimates in

management accounting for various activities and budgeting processes. If the information

provided is not accurate, wrong estimates will be made which will be made by the management

for future activities. Allocation of resources over different process activities and departments will

not be accurate(Bottomley and Bosman, 2018). Inaccuracy of resource allocation will increase

the cost of production. The actual areas where the improvements are required to made will not be

identified. This is essential for the business enterprise that the management is provided with

information that is accurate and reliable. Controlling the cost would not be possible in absence of

reliable information. The strategic decisions for the process improvements and cost reduction are

essential. The overall performance of the company will be affected if the future budgets and

estimates are made on irrelevant or inaccurate information. Timely information should be

provided the managers so that review of the budgetary reports and other activities could be made

and corrective actions can be taken on time.

c) Evaluating management accounting systems and reports to be integrated in Excite

Entertainment Ltd operational process.

Management Accounting Systems

System Application in Excite Entertainment

Cost Accounting System The system will help the excite for developing manufacturing

processes and to identify the ways for increasing the profits and

controlling cost(Zahller, 2017).

Inventory Management

System

Inventory management system will help in making the goods

required for production available on time without any gap. This

will increase the production efficiency.

Job Costing System The different costs could be identified of jobs that will help in

8

user.

The management accounting information is used for making the business decisions. The

information provided should be accurate, relevant and reliable. Management makes estimates in

management accounting for various activities and budgeting processes. If the information

provided is not accurate, wrong estimates will be made which will be made by the management

for future activities. Allocation of resources over different process activities and departments will

not be accurate(Bottomley and Bosman, 2018). Inaccuracy of resource allocation will increase

the cost of production. The actual areas where the improvements are required to made will not be

identified. This is essential for the business enterprise that the management is provided with

information that is accurate and reliable. Controlling the cost would not be possible in absence of

reliable information. The strategic decisions for the process improvements and cost reduction are

essential. The overall performance of the company will be affected if the future budgets and

estimates are made on irrelevant or inaccurate information. Timely information should be

provided the managers so that review of the budgetary reports and other activities could be made

and corrective actions can be taken on time.

c) Evaluating management accounting systems and reports to be integrated in Excite

Entertainment Ltd operational process.

Management Accounting Systems

System Application in Excite Entertainment

Cost Accounting System The system will help the excite for developing manufacturing

processes and to identify the ways for increasing the profits and

controlling cost(Zahller, 2017).

Inventory Management

System

Inventory management system will help in making the goods

required for production available on time without any gap. This

will increase the production efficiency.

Job Costing System The different costs could be identified of jobs that will help in

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

measuring the total cost of products. Identifying the cost of jobs

will help in accurate cost calculations.

Management Accounting Reports

System Application in Excite Entertainment

Budget Reports Excite entertainment will be preparing these reports to identify the

variances between the expected and actual results(Muller, 2019).

This helps in identifying the areas where corrective steps need to

be taken.

Management accounting

report

Management accounting reports will help the Excite ltd in

identifying the cost of products. All the factors will be considered

for coming at actual cost incurred for preparing the product.

Performance Report Performance will help the company to identify the process which

is more efficient and area that requires improvements. Company

will be able to promote and reward the employees.

SCENARIO 2

Comparison of profit or loss under different cost accounting techniques.

Marginal Costing

It is defined as costing technique where the variable costs are only charged to the cost of

product. The costing techniques do not takes into account fixed cost as it is treated as period

costs. It is used by managers in making decisions and only variable costs are considered.

Benefits

It facilitates comparison and cost control(Wild, 2017).

It is helpful in making the pricing decisions over the product life cycle. It helps in defraying profitability and break-even chart effectively.

Drawbacks

9

will help in accurate cost calculations.

Management Accounting Reports

System Application in Excite Entertainment

Budget Reports Excite entertainment will be preparing these reports to identify the

variances between the expected and actual results(Muller, 2019).

This helps in identifying the areas where corrective steps need to

be taken.

Management accounting

report

Management accounting reports will help the Excite ltd in

identifying the cost of products. All the factors will be considered

for coming at actual cost incurred for preparing the product.

Performance Report Performance will help the company to identify the process which

is more efficient and area that requires improvements. Company

will be able to promote and reward the employees.

SCENARIO 2

Comparison of profit or loss under different cost accounting techniques.

Marginal Costing

It is defined as costing technique where the variable costs are only charged to the cost of

product. The costing techniques do not takes into account fixed cost as it is treated as period

costs. It is used by managers in making decisions and only variable costs are considered.

Benefits

It facilitates comparison and cost control(Wild, 2017).

It is helpful in making the pricing decisions over the product life cycle. It helps in defraying profitability and break-even chart effectively.

Drawbacks

9

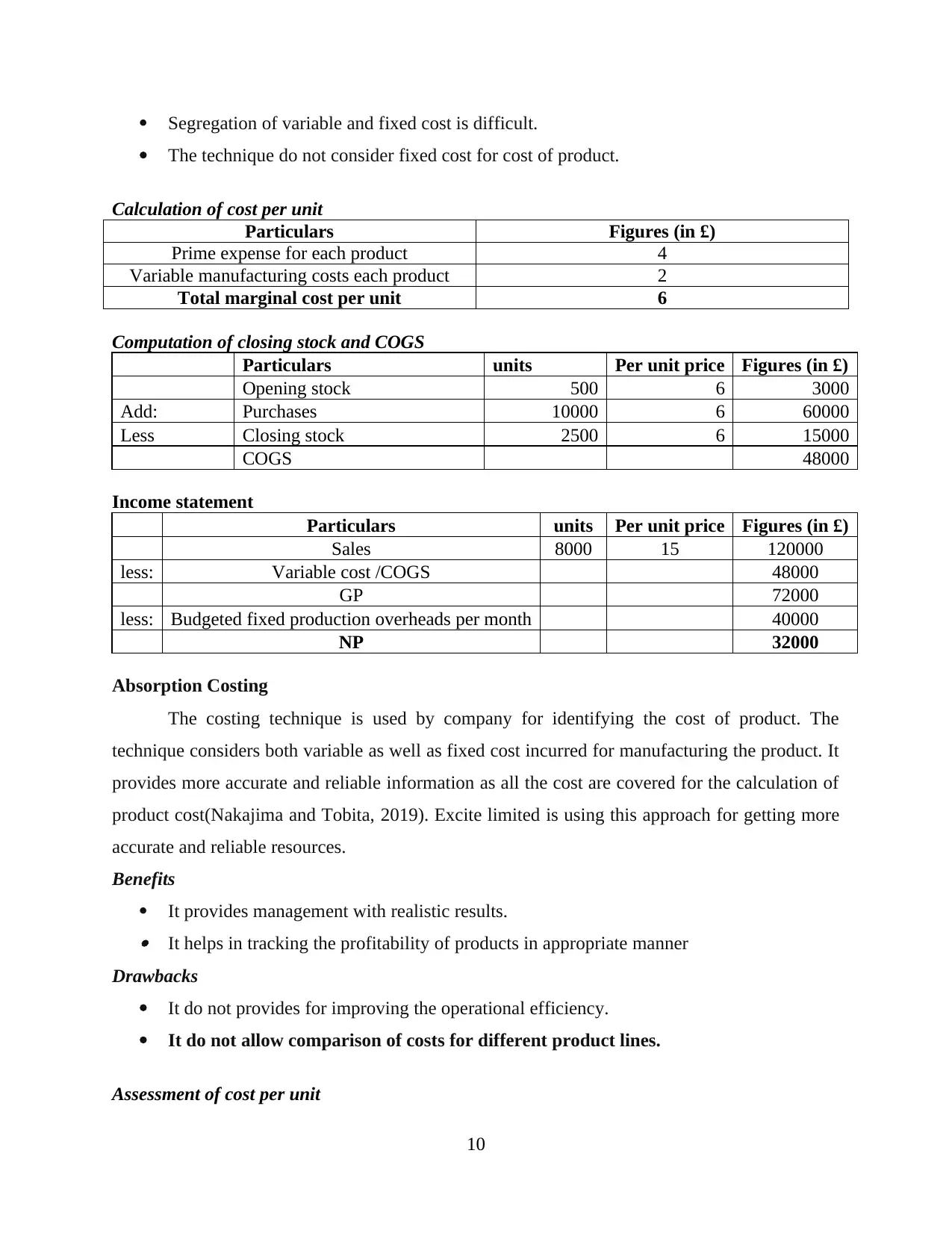

Segregation of variable and fixed cost is difficult.

The technique do not consider fixed cost for cost of product.

Calculation of cost per unit

Particulars Figures (in £)

Prime expense for each product 4

Variable manufacturing costs each product 2

Total marginal cost per unit 6

Computation of closing stock and COGS

Particulars units Per unit price Figures (in £)

Opening stock 500 6 3000

Add: Purchases 10000 6 60000

Less Closing stock 2500 6 15000

COGS 48000

Income statement

Particulars units Per unit price Figures (in £)

Sales 8000 15 120000

less: Variable cost /COGS 48000

GP 72000

less: Budgeted fixed production overheads per month 40000

NP 32000

Absorption Costing

The costing technique is used by company for identifying the cost of product. The

technique considers both variable as well as fixed cost incurred for manufacturing the product. It

provides more accurate and reliable information as all the cost are covered for the calculation of

product cost(Nakajima and Tobita, 2019). Excite limited is using this approach for getting more

accurate and reliable resources.

Benefits

It provides management with realistic results. It helps in tracking the profitability of products in appropriate manner

Drawbacks

It do not provides for improving the operational efficiency.

It do not allow comparison of costs for different product lines.

Assessment of cost per unit

10

The technique do not consider fixed cost for cost of product.

Calculation of cost per unit

Particulars Figures (in £)

Prime expense for each product 4

Variable manufacturing costs each product 2

Total marginal cost per unit 6

Computation of closing stock and COGS

Particulars units Per unit price Figures (in £)

Opening stock 500 6 3000

Add: Purchases 10000 6 60000

Less Closing stock 2500 6 15000

COGS 48000

Income statement

Particulars units Per unit price Figures (in £)

Sales 8000 15 120000

less: Variable cost /COGS 48000

GP 72000

less: Budgeted fixed production overheads per month 40000

NP 32000

Absorption Costing

The costing technique is used by company for identifying the cost of product. The

technique considers both variable as well as fixed cost incurred for manufacturing the product. It

provides more accurate and reliable information as all the cost are covered for the calculation of

product cost(Nakajima and Tobita, 2019). Excite limited is using this approach for getting more

accurate and reliable resources.

Benefits

It provides management with realistic results. It helps in tracking the profitability of products in appropriate manner

Drawbacks

It do not provides for improving the operational efficiency.

It do not allow comparison of costs for different product lines.

Assessment of cost per unit

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.