Comprehensive Analysis of Management Accounting Systems and Reporting

VerifiedAdded on 2020/10/05

|19

|5458

|483

Report

AI Summary

This report provides a detailed analysis of management accounting systems and reporting methods, focusing on their application within Equilibrium Asset Management. It begins with an introduction to management accounting, differentiating it from financial accounting, and explores various types of management accounting systems, including cost accounting, job costing, inventory management, and price optimization. The report then delves into different management accounting reporting methods, such as budget reports, account receivable aging reports, performance reports, and financial reports, highlighting their significance in strategic planning and decision-making. Furthermore, it evaluates the benefits of different management accounting systems, emphasizing their role in cost control, price optimization, and inventory management. Finally, the report assesses the integration of management accounting systems and reporting within organizations for strategic planning. The report also includes the use of different planning tools for budgetary control.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INRODUCTION..............................................................................................................................1

LO1..................................................................................................................................................1

Management accounting and its different types of system....................................................1

Difference between management accounting and financial accounting................................3

2 Explain different method of management accounting reporting........................................3

Evaluation of benefits of various management accounting systems......................................4

Evaluation of Management Accounting System and Reporting............................................5

LO 2.................................................................................................................................................6

Calculation of income statement using marginal and absorption costs:.................................6

Application of a range of management accounting techniques..............................................9

LO3................................................................................................................................................11

Advantages and disadvantages of different types of planning tools used for budgetary control

..............................................................................................................................................11

Use of different accounting tools and their application for preparing and forecasting budgets.

..............................................................................................................................................13

LO 4...............................................................................................................................................13

How organisation adapting management accounting respond to financial problems..........13

How management accounting can deal with financial problems and attains sustainable

success..................................................................................................................................15

Planning tools to solve financial problems:..........................................................................15

REFRENCES.................................................................................................................................17

Books and journals...............................................................................................................17

INRODUCTION..............................................................................................................................1

LO1..................................................................................................................................................1

Management accounting and its different types of system....................................................1

Difference between management accounting and financial accounting................................3

2 Explain different method of management accounting reporting........................................3

Evaluation of benefits of various management accounting systems......................................4

Evaluation of Management Accounting System and Reporting............................................5

LO 2.................................................................................................................................................6

Calculation of income statement using marginal and absorption costs:.................................6

Application of a range of management accounting techniques..............................................9

LO3................................................................................................................................................11

Advantages and disadvantages of different types of planning tools used for budgetary control

..............................................................................................................................................11

Use of different accounting tools and their application for preparing and forecasting budgets.

..............................................................................................................................................13

LO 4...............................................................................................................................................13

How organisation adapting management accounting respond to financial problems..........13

How management accounting can deal with financial problems and attains sustainable

success..................................................................................................................................15

Planning tools to solve financial problems:..........................................................................15

REFRENCES.................................................................................................................................17

Books and journals...............................................................................................................17

INRODUCTION

Management accounting refers to the process of recording, estimating, analysing and

summarizing the data associated with operations of organisation. It is field of accounting that

studies every features related to company's operation (Erserim, 2012). The main purpose of

preparing such accounts is to ensure the smooth running of business. Techniques and tools such

as cost analysis, budgetary control helps in assessing the expenditure incurred and how the

expenses can be controlled. There are different types of management system we will discuss

them in detail in the following report. Equilibrium asset management is medium-sized financial

consulting firm that lends variety of services to it's clients. This company incorporates different

forms of systems in order to maintain information concerning enterprise to efficiently achieve

goals of the organisation. This method helps in systematically organising functions performed by

several department. Equilibrium asset management provides advices with respect to investment

and wealth management. The following report contains detailed description of management

accounting systems, analysis and advantages and disadvantages of planning tools. Let's examine

them step by step.

LO1

Management accounting and its different types of system.

Management accounting is the systematic process of recording the transaction which

occur daily in the business. The financial transactions which occur daily are recorded in the

books. The process of analysing, summarizing of the these transactions for the top level of

management is known as accounting. Financial statements such as balance sheet, cash flows are

also included in the accounting process and these transactions are recorded by the employees

working in the finance division of the company.

The process in which the business analyse its cost for the preparation of the financial

statements to see the actual position of the company is called the management accounting also

known as the managerial accounting or cost accounting. This helps the management to find out

the problems related to the financial accounting in analysing the financial reports and preparing

it. The main objective of the management accounting is cost optimization and reduce the cost to

help company to survive in the market and stand against its competitors. Management

accounting helps the organisation in decision-making process and planning for the future in order

1

Management accounting refers to the process of recording, estimating, analysing and

summarizing the data associated with operations of organisation. It is field of accounting that

studies every features related to company's operation (Erserim, 2012). The main purpose of

preparing such accounts is to ensure the smooth running of business. Techniques and tools such

as cost analysis, budgetary control helps in assessing the expenditure incurred and how the

expenses can be controlled. There are different types of management system we will discuss

them in detail in the following report. Equilibrium asset management is medium-sized financial

consulting firm that lends variety of services to it's clients. This company incorporates different

forms of systems in order to maintain information concerning enterprise to efficiently achieve

goals of the organisation. This method helps in systematically organising functions performed by

several department. Equilibrium asset management provides advices with respect to investment

and wealth management. The following report contains detailed description of management

accounting systems, analysis and advantages and disadvantages of planning tools. Let's examine

them step by step.

LO1

Management accounting and its different types of system.

Management accounting is the systematic process of recording the transaction which

occur daily in the business. The financial transactions which occur daily are recorded in the

books. The process of analysing, summarizing of the these transactions for the top level of

management is known as accounting. Financial statements such as balance sheet, cash flows are

also included in the accounting process and these transactions are recorded by the employees

working in the finance division of the company.

The process in which the business analyse its cost for the preparation of the financial

statements to see the actual position of the company is called the management accounting also

known as the managerial accounting or cost accounting. This helps the management to find out

the problems related to the financial accounting in analysing the financial reports and preparing

it. The main objective of the management accounting is cost optimization and reduce the cost to

help company to survive in the market and stand against its competitors. Management

accounting helps the organisation in decision-making process and planning for the future in order

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to make new strategic plans and properly implement those plans (Grabner and Moers, 2013).

There are four types of different management accounting systems as described below:

Cost Accounting System: Cost accounting system is a system in which the main

objective of an accountant is to capture and focus on the company's costs for the production. The

aim of the cost accounting system is to properly and effectively allocate the cost related to

production. It focuses mainly on the cost used for production purposes only it analyse the cost

related to production and find out the new methods to reduce the cost of production and achieve

the maximum profit. As Equilibrium Assets Management is providing the financial consultancy

to other small and medium size businesses the cost which is incurred is high and to be properly

managed.

Job Costing System: This type of management accounting system is used by the

organisation to optimize and allocate the cost to the particular job. This type of management

system is used to keep the track of the work done by an individual as well as team performance.

This types of system helps the top level managers to identify the individual cost of production for

a specific service or product. This organisation is into financial consultancy services which

provides different services to different clients, this job costing system helps it to keep the record

of the individual project.

Inventory Management System: This system involves in management of the inventory

of a company. Inventory is all the stock in the organisation including the finished stock and work

in progress stock. A management system is used to mange the inventories of the organisation

which helps the organisation to check that at what time they have to finish their inventory so that

their work does not stops. Inventory management system also includes the raw material and

keeps track of it so that the raw material can be reordered as early as possible so the production

process does not stops.

Price Optimization: Price optimization is the method which helps the organisation to

determine the price of it products and how they can effectively optimize their price. It is a tools

frequently used by the organisation to analyse the buying pattern of the consumers and determine

the price according to it. As Equilibrium asset management is into the financial consultancy

services they have to optimize the price related to their service what service is to be given or

what price is to be charged to the particular service provided (Mancini, Vaassen and Dameri,

2013).

2

There are four types of different management accounting systems as described below:

Cost Accounting System: Cost accounting system is a system in which the main

objective of an accountant is to capture and focus on the company's costs for the production. The

aim of the cost accounting system is to properly and effectively allocate the cost related to

production. It focuses mainly on the cost used for production purposes only it analyse the cost

related to production and find out the new methods to reduce the cost of production and achieve

the maximum profit. As Equilibrium Assets Management is providing the financial consultancy

to other small and medium size businesses the cost which is incurred is high and to be properly

managed.

Job Costing System: This type of management accounting system is used by the

organisation to optimize and allocate the cost to the particular job. This type of management

system is used to keep the track of the work done by an individual as well as team performance.

This types of system helps the top level managers to identify the individual cost of production for

a specific service or product. This organisation is into financial consultancy services which

provides different services to different clients, this job costing system helps it to keep the record

of the individual project.

Inventory Management System: This system involves in management of the inventory

of a company. Inventory is all the stock in the organisation including the finished stock and work

in progress stock. A management system is used to mange the inventories of the organisation

which helps the organisation to check that at what time they have to finish their inventory so that

their work does not stops. Inventory management system also includes the raw material and

keeps track of it so that the raw material can be reordered as early as possible so the production

process does not stops.

Price Optimization: Price optimization is the method which helps the organisation to

determine the price of it products and how they can effectively optimize their price. It is a tools

frequently used by the organisation to analyse the buying pattern of the consumers and determine

the price according to it. As Equilibrium asset management is into the financial consultancy

services they have to optimize the price related to their service what service is to be given or

what price is to be charged to the particular service provided (Mancini, Vaassen and Dameri,

2013).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Difference between management accounting and financial accounting

Management accounting Financial accounting

The executives Management is utilized for

inside management.

While it is utilized for interior and outer

purposes.

This Management framework is not mandatory

to maintain.

Financial accounting is should have been

finished with in a particular time span. It is

necessary.

It isn't compulsory to finish in bookkeeping

period

It ought to be finished by the accounting time

frame.

This does not pursue any bookkeeping

guidelines and regulation.

Financial accounting is finished by the

bookkeeping principles and guideline.

2 Explain different method of management accounting reporting.

Management accounting reporting is done to make sure that the management has the

clear picture of the financial health and financial position of the company. These reports also

helps the top level management to design new strategies, planing and decision making process.

These reports are used by the management to take the necessary and critical decisions, these

reports are prepared very carefully by the accountants so that it does not have any errors as the

managers only relay on these reports while taking important decision for the company. Some of

the different methods of management accounting system are as follows:

Budget Report: Budget report are the reports which are prepared to analyse the budget

for the company and also it helps in the analysis of the actual performance of the company in

contrast to its budget estimation. These reports are prepared internally for the self evaluation of

the company this report shows the comparison between the actual and the budgeted performance

of the company during the year. These budgets are made on the basis of estimation and future

predictions and are based on financial goals. These budgets helps the managers to make new

changes in the incentive plans for the employees.

Account Receivable Ageing Reports: Account Receivable Ageing Report helps the

organisation to keep track of the debtors. If the organisation relay too much on credit sales than

this report helps the organisation to keep check on the defaulters and helps them to manage

accordingly such that it does not affect the profit of the organisation and find the issues relate to

3

Management accounting Financial accounting

The executives Management is utilized for

inside management.

While it is utilized for interior and outer

purposes.

This Management framework is not mandatory

to maintain.

Financial accounting is should have been

finished with in a particular time span. It is

necessary.

It isn't compulsory to finish in bookkeeping

period

It ought to be finished by the accounting time

frame.

This does not pursue any bookkeeping

guidelines and regulation.

Financial accounting is finished by the

bookkeeping principles and guideline.

2 Explain different method of management accounting reporting.

Management accounting reporting is done to make sure that the management has the

clear picture of the financial health and financial position of the company. These reports also

helps the top level management to design new strategies, planing and decision making process.

These reports are used by the management to take the necessary and critical decisions, these

reports are prepared very carefully by the accountants so that it does not have any errors as the

managers only relay on these reports while taking important decision for the company. Some of

the different methods of management accounting system are as follows:

Budget Report: Budget report are the reports which are prepared to analyse the budget

for the company and also it helps in the analysis of the actual performance of the company in

contrast to its budget estimation. These reports are prepared internally for the self evaluation of

the company this report shows the comparison between the actual and the budgeted performance

of the company during the year. These budgets are made on the basis of estimation and future

predictions and are based on financial goals. These budgets helps the managers to make new

changes in the incentive plans for the employees.

Account Receivable Ageing Reports: Account Receivable Ageing Report helps the

organisation to keep track of the debtors. If the organisation relay too much on credit sales than

this report helps the organisation to keep check on the defaulters and helps them to manage

accordingly such that it does not affect the profit of the organisation and find the issues relate to

3

the debtors payment. This report is generally made to see that how much money is stuck in the

market in the form of debtors. This report also helps to reframe its credit policy if the number of

defaulters are more in any organisation.

Performance Report: Performance reports are made to check the performance of the

company in order to see that they are performing well or not than their competitors (Ramljak and

Rogošić, 2012). This report helps the management to re think their strategies in order to compete

with their competitors. These reports play an important role in helping the mangers to make the

strategic decisions for the future of the company as this report show the clear picture of the

health and performance of the company. Managers analyse these reports very carefully to find

out the flaws and overcome them in the near future by making the necessary changes in the

system.

Financial Report: Financial reports shows the actual financial position and financial

capabilities of the organisation. These are prepared by the finance department, financial reports

include all the financial statements such as balance sheet, profit and loss statements and cash

flow statement of the company in a report form which helps the management to decide that from

which sources it need to raise its capital and where to invest to grow and expand its business.

The information from these reports helps the management to see that how there profit and losses

have fluctuated over the period of time.

Cost Managerial Accounting Reports: This report computes the cost of the product and

the cost of procurement of the raw material, labour, overhead and all the direct and in direct cost

related to the manufacturing of product. This report helps the managers to identify the cost and

the profit which is charged against that product. This report consist of the cost which is incurred

by the production department to produce the goods and the profit which is to be charged on that

particular product.

Evaluation of benefits of various management accounting systems.

Management Accounting System Benefits

Cost Accounting System Cost accounting system helps the organisation

to fix its price more efficiently, as this system

provides the details of the cost.

This system helps the management to improve

4

market in the form of debtors. This report also helps to reframe its credit policy if the number of

defaulters are more in any organisation.

Performance Report: Performance reports are made to check the performance of the

company in order to see that they are performing well or not than their competitors (Ramljak and

Rogošić, 2012). This report helps the management to re think their strategies in order to compete

with their competitors. These reports play an important role in helping the mangers to make the

strategic decisions for the future of the company as this report show the clear picture of the

health and performance of the company. Managers analyse these reports very carefully to find

out the flaws and overcome them in the near future by making the necessary changes in the

system.

Financial Report: Financial reports shows the actual financial position and financial

capabilities of the organisation. These are prepared by the finance department, financial reports

include all the financial statements such as balance sheet, profit and loss statements and cash

flow statement of the company in a report form which helps the management to decide that from

which sources it need to raise its capital and where to invest to grow and expand its business.

The information from these reports helps the management to see that how there profit and losses

have fluctuated over the period of time.

Cost Managerial Accounting Reports: This report computes the cost of the product and

the cost of procurement of the raw material, labour, overhead and all the direct and in direct cost

related to the manufacturing of product. This report helps the managers to identify the cost and

the profit which is charged against that product. This report consist of the cost which is incurred

by the production department to produce the goods and the profit which is to be charged on that

particular product.

Evaluation of benefits of various management accounting systems.

Management Accounting System Benefits

Cost Accounting System Cost accounting system helps the organisation

to fix its price more efficiently, as this system

provides the details of the cost.

This system helps the management to improve

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and measure the cost effectively and efficiently

Price Optimization It helps the managers to set the price of the

product according to the demand. Equilibrium

asset management uses this system to identify

the price for their services (Richardson, 2012).

It can also be used to see the buying behaviour

of the consumers as in financial consultancy

service clients usually have same problems.

Inventory Management System In the financial service providers there is not

much inventory. In this only monetary

instruments and the accounts of the client are

the inventory

Job Costing System This helps in the control on the cost or products

or services provided to the clients. As in

Equilibrium Asset Management clients have

different work so the cost is allocated

differently on the work.

As different client has different jobs so the

profit for each job is calculated differently.

Evaluation of Management Accounting System and Reporting.

Management accounting system and Management Accounting Reporting is used in the

organisations interrelatedly to find out the flaws in the system and rectify it it also gives the

organisation to plan its resources in the better way to achieve the maximum profit. As in the

Equilibrium Asset Management the managers uses both the system together to make necessary

changes in the organisation (Schaltegger and Burritt, 2017). Different type of management

accounting system and management accounting reporting is used to see the financial position of

the company. Managers analyse these reports and while making and planing to implement new

system in an organisation. Both the systems are integrated within the organisational processes for

strategic planing to have the competitive advantage over their competitors.

5

Price Optimization It helps the managers to set the price of the

product according to the demand. Equilibrium

asset management uses this system to identify

the price for their services (Richardson, 2012).

It can also be used to see the buying behaviour

of the consumers as in financial consultancy

service clients usually have same problems.

Inventory Management System In the financial service providers there is not

much inventory. In this only monetary

instruments and the accounts of the client are

the inventory

Job Costing System This helps in the control on the cost or products

or services provided to the clients. As in

Equilibrium Asset Management clients have

different work so the cost is allocated

differently on the work.

As different client has different jobs so the

profit for each job is calculated differently.

Evaluation of Management Accounting System and Reporting.

Management accounting system and Management Accounting Reporting is used in the

organisations interrelatedly to find out the flaws in the system and rectify it it also gives the

organisation to plan its resources in the better way to achieve the maximum profit. As in the

Equilibrium Asset Management the managers uses both the system together to make necessary

changes in the organisation (Schaltegger and Burritt, 2017). Different type of management

accounting system and management accounting reporting is used to see the financial position of

the company. Managers analyse these reports and while making and planing to implement new

system in an organisation. Both the systems are integrated within the organisational processes for

strategic planing to have the competitive advantage over their competitors.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO 2

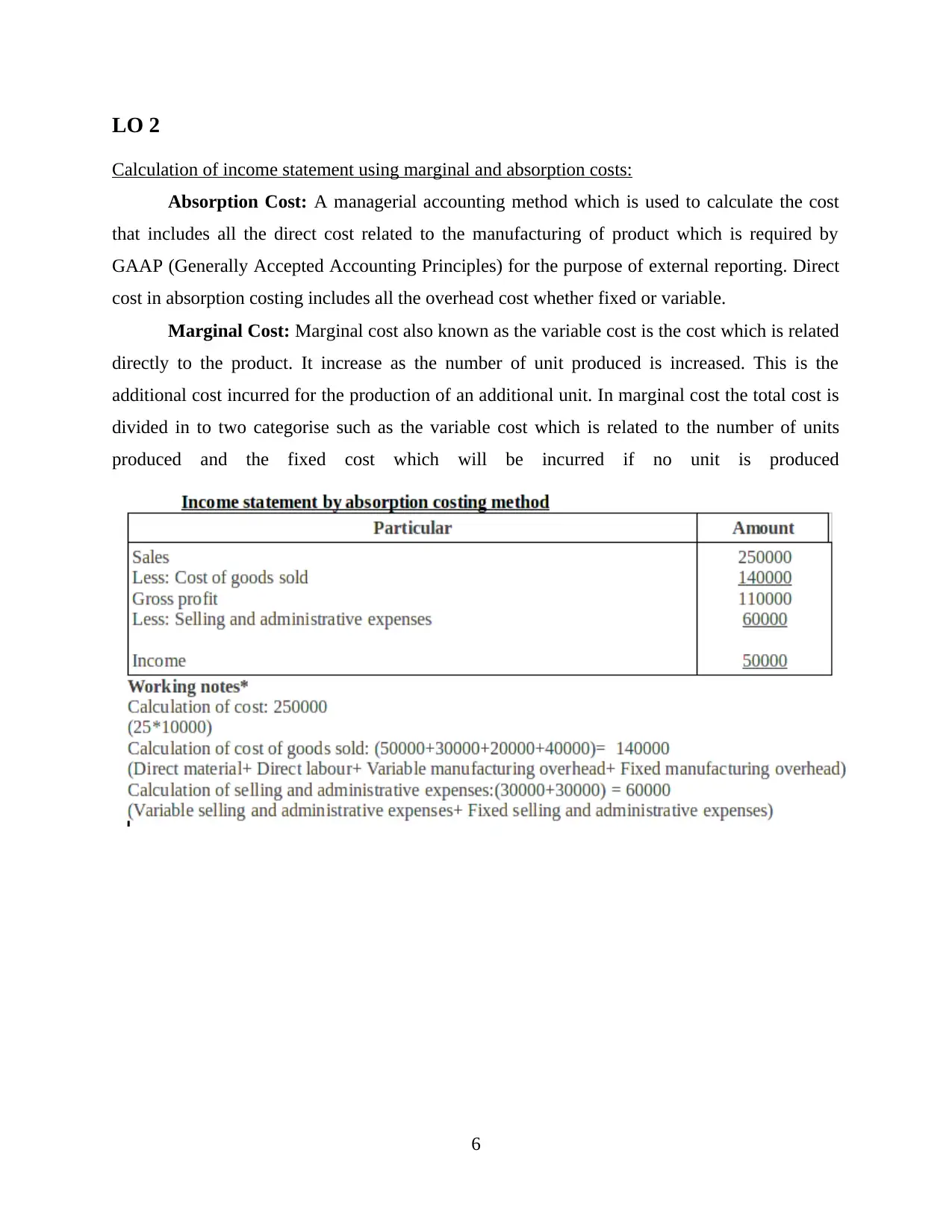

Calculation of income statement using marginal and absorption costs:

Absorption Cost: A managerial accounting method which is used to calculate the cost

that includes all the direct cost related to the manufacturing of product which is required by

GAAP (Generally Accepted Accounting Principles) for the purpose of external reporting. Direct

cost in absorption costing includes all the overhead cost whether fixed or variable.

Marginal Cost: Marginal cost also known as the variable cost is the cost which is related

directly to the product. It increase as the number of unit produced is increased. This is the

additional cost incurred for the production of an additional unit. In marginal cost the total cost is

divided in to two categorise such as the variable cost which is related to the number of units

produced and the fixed cost which will be incurred if no unit is produced

6

Calculation of income statement using marginal and absorption costs:

Absorption Cost: A managerial accounting method which is used to calculate the cost

that includes all the direct cost related to the manufacturing of product which is required by

GAAP (Generally Accepted Accounting Principles) for the purpose of external reporting. Direct

cost in absorption costing includes all the overhead cost whether fixed or variable.

Marginal Cost: Marginal cost also known as the variable cost is the cost which is related

directly to the product. It increase as the number of unit produced is increased. This is the

additional cost incurred for the production of an additional unit. In marginal cost the total cost is

divided in to two categorise such as the variable cost which is related to the number of units

produced and the fixed cost which will be incurred if no unit is produced

6

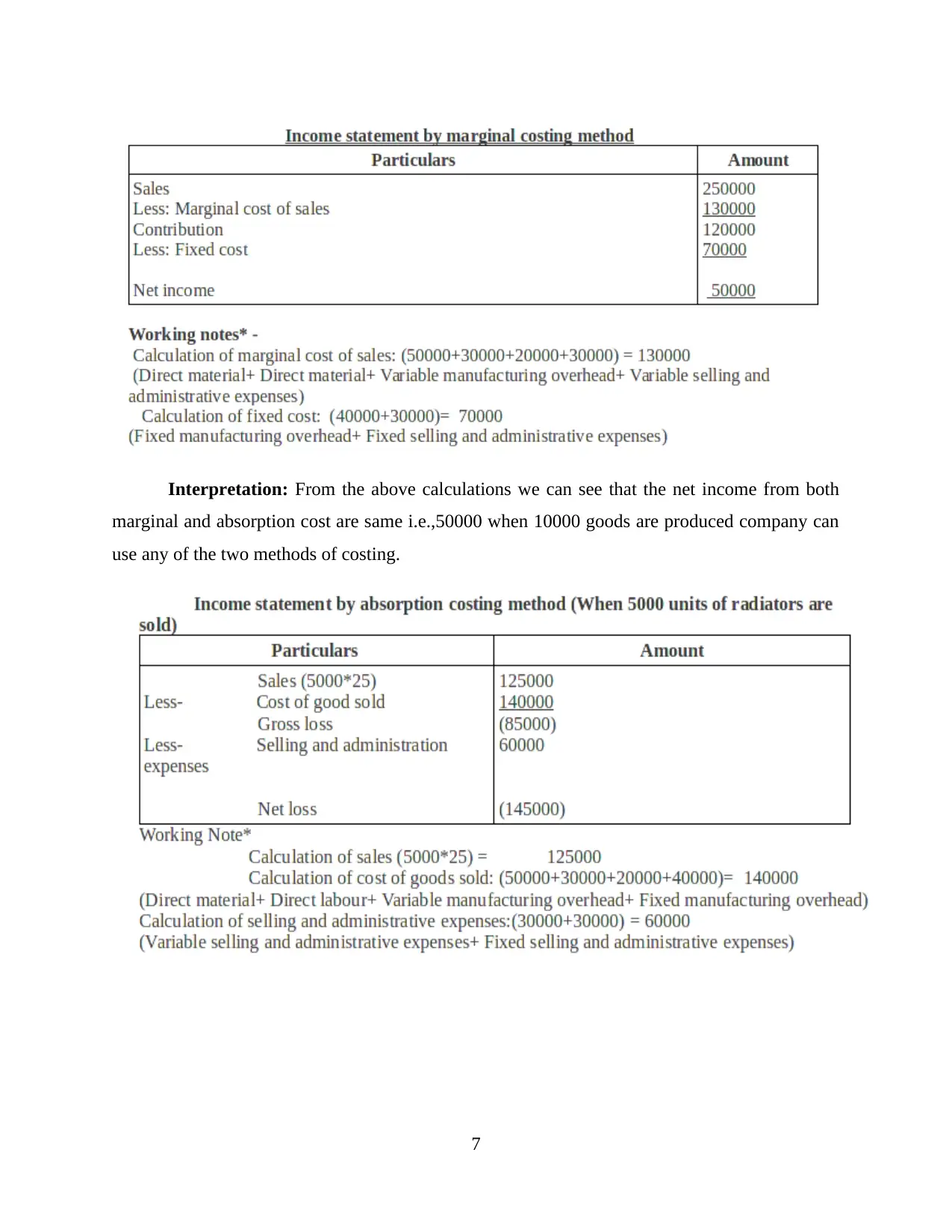

Interpretation: From the above calculations we can see that the net income from both

marginal and absorption cost are same i.e.,50000 when 10000 goods are produced company can

use any of the two methods of costing.

7

marginal and absorption cost are same i.e.,50000 when 10000 goods are produced company can

use any of the two methods of costing.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

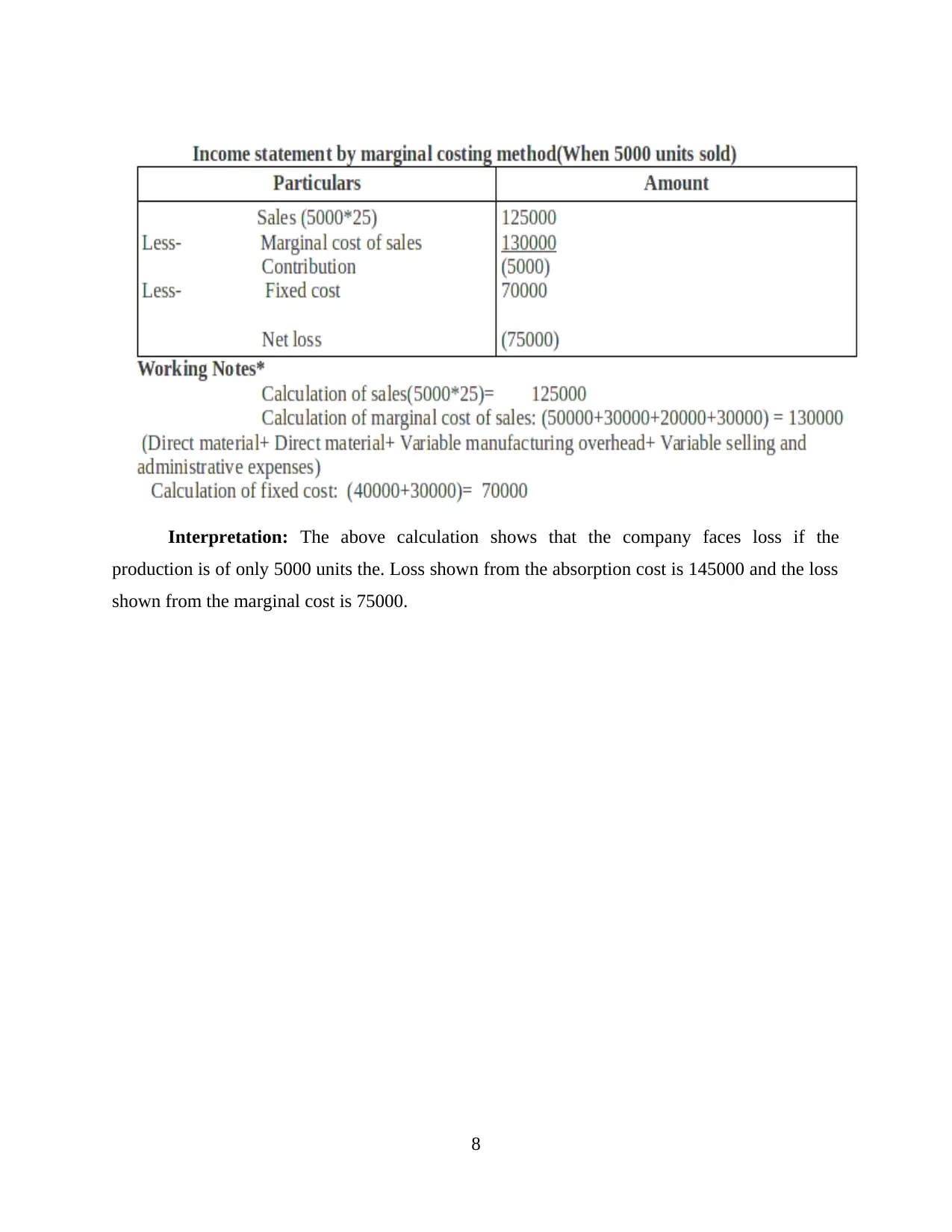

Interpretation: The above calculation shows that the company faces loss if the

production is of only 5000 units the. Loss shown from the absorption cost is 145000 and the loss

shown from the marginal cost is 75000.

8

production is of only 5000 units the. Loss shown from the absorption cost is 145000 and the loss

shown from the marginal cost is 75000.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

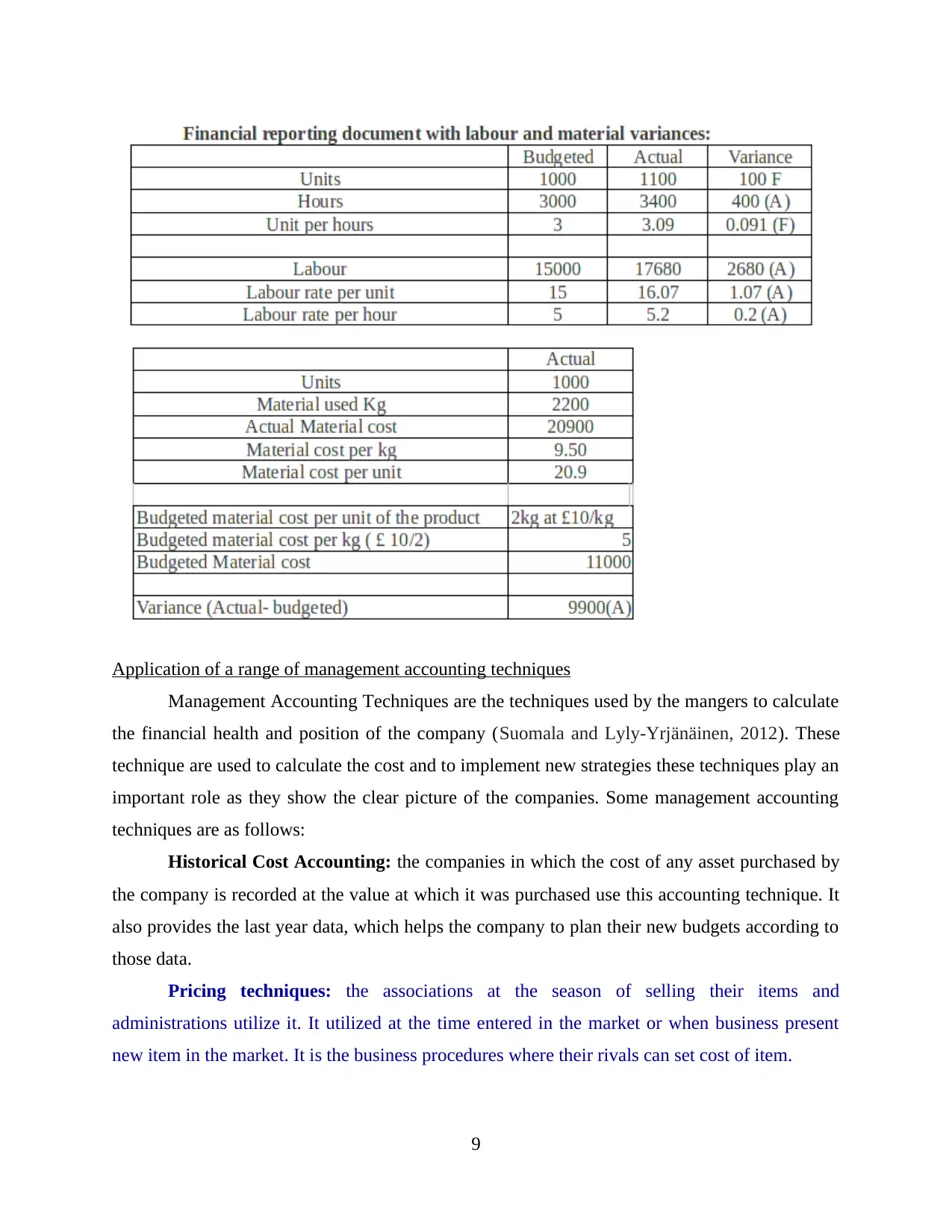

Application of a range of management accounting techniques

Management Accounting Techniques are the techniques used by the mangers to calculate

the financial health and position of the company (Suomala and Lyly-Yrjänäinen, 2012). These

technique are used to calculate the cost and to implement new strategies these techniques play an

important role as they show the clear picture of the companies. Some management accounting

techniques are as follows:

Historical Cost Accounting: the companies in which the cost of any asset purchased by

the company is recorded at the value at which it was purchased use this accounting technique. It

also provides the last year data, which helps the company to plan their new budgets according to

those data.

Pricing techniques: the associations at the season of selling their items and

administrations utilize it. It utilized at the time entered in the market or when business present

new item in the market. It is the business procedures where their rivals can set cost of item.

9

Management Accounting Techniques are the techniques used by the mangers to calculate

the financial health and position of the company (Suomala and Lyly-Yrjänäinen, 2012). These

technique are used to calculate the cost and to implement new strategies these techniques play an

important role as they show the clear picture of the companies. Some management accounting

techniques are as follows:

Historical Cost Accounting: the companies in which the cost of any asset purchased by

the company is recorded at the value at which it was purchased use this accounting technique. It

also provides the last year data, which helps the company to plan their new budgets according to

those data.

Pricing techniques: the associations at the season of selling their items and

administrations utilize it. It utilized at the time entered in the market or when business present

new item in the market. It is the business procedures where their rivals can set cost of item.

9

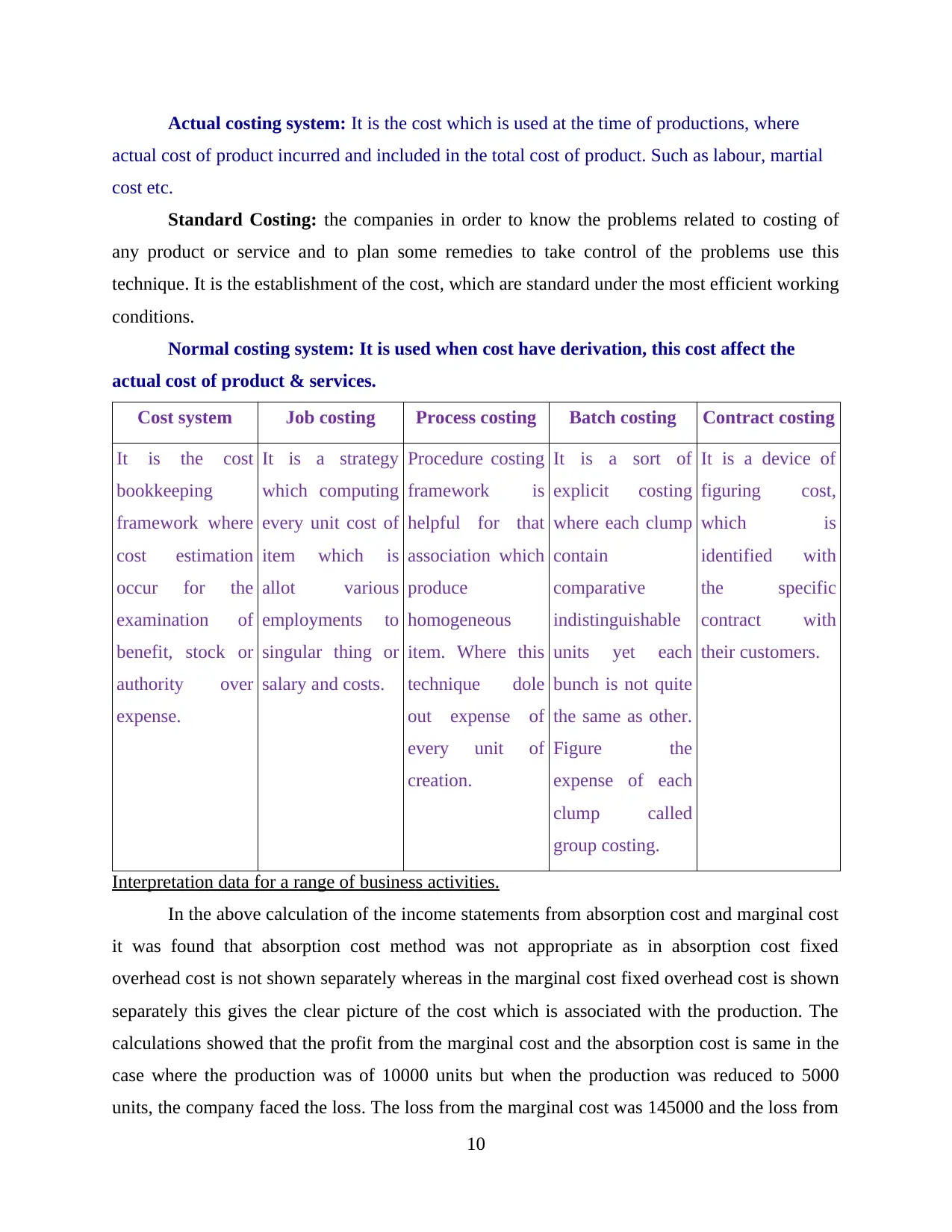

Actual costing system: It is the cost which is used at the time of productions, where

actual cost of product incurred and included in the total cost of product. Such as labour, martial

cost etc.

Standard Costing: the companies in order to know the problems related to costing of

any product or service and to plan some remedies to take control of the problems use this

technique. It is the establishment of the cost, which are standard under the most efficient working

conditions.

Normal costing system: It is used when cost have derivation, this cost affect the

actual cost of product & services.

Cost system Job costing Process costing Batch costing Contract costing

It is the cost

bookkeeping

framework where

cost estimation

occur for the

examination of

benefit, stock or

authority over

expense.

It is a strategy

which computing

every unit cost of

item which is

allot various

employments to

singular thing or

salary and costs.

Procedure costing

framework is

helpful for that

association which

produce

homogeneous

item. Where this

technique dole

out expense of

every unit of

creation.

It is a sort of

explicit costing

where each clump

contain

comparative

indistinguishable

units yet each

bunch is not quite

the same as other.

Figure the

expense of each

clump called

group costing.

It is a device of

figuring cost,

which is

identified with

the specific

contract with

their customers.

Interpretation data for a range of business activities.

In the above calculation of the income statements from absorption cost and marginal cost

it was found that absorption cost method was not appropriate as in absorption cost fixed

overhead cost is not shown separately whereas in the marginal cost fixed overhead cost is shown

separately this gives the clear picture of the cost which is associated with the production. The

calculations showed that the profit from the marginal cost and the absorption cost is same in the

case where the production was of 10000 units but when the production was reduced to 5000

units, the company faced the loss. The loss from the marginal cost was 145000 and the loss from

10

actual cost of product incurred and included in the total cost of product. Such as labour, martial

cost etc.

Standard Costing: the companies in order to know the problems related to costing of

any product or service and to plan some remedies to take control of the problems use this

technique. It is the establishment of the cost, which are standard under the most efficient working

conditions.

Normal costing system: It is used when cost have derivation, this cost affect the

actual cost of product & services.

Cost system Job costing Process costing Batch costing Contract costing

It is the cost

bookkeeping

framework where

cost estimation

occur for the

examination of

benefit, stock or

authority over

expense.

It is a strategy

which computing

every unit cost of

item which is

allot various

employments to

singular thing or

salary and costs.

Procedure costing

framework is

helpful for that

association which

produce

homogeneous

item. Where this

technique dole

out expense of

every unit of

creation.

It is a sort of

explicit costing

where each clump

contain

comparative

indistinguishable

units yet each

bunch is not quite

the same as other.

Figure the

expense of each

clump called

group costing.

It is a device of

figuring cost,

which is

identified with

the specific

contract with

their customers.

Interpretation data for a range of business activities.

In the above calculation of the income statements from absorption cost and marginal cost

it was found that absorption cost method was not appropriate as in absorption cost fixed

overhead cost is not shown separately whereas in the marginal cost fixed overhead cost is shown

separately this gives the clear picture of the cost which is associated with the production. The

calculations showed that the profit from the marginal cost and the absorption cost is same in the

case where the production was of 10000 units but when the production was reduced to 5000

units, the company faced the loss. The loss from the marginal cost was 145000 and the loss from

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.